OPEN-SOURCE SCRIPT

Mis à jour Fractal Regression Bands [DW]

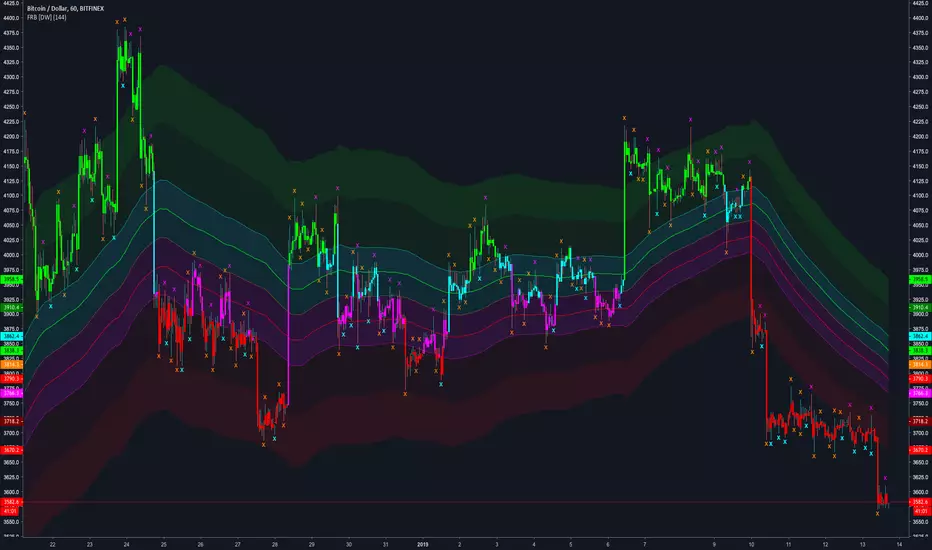

This study is an experimental regression curve built around fractal and ATR calculations.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

Notes de version

Updates:Due to inefficiencies and its arbitrary nature, the slope factor calculation has been removed from the script.

Due to the linear regression's significant amount of overshoot, especially at greater sampling lengths, the basis line is now calculated using exponential smoothing, which fits the price series much better with minimal overshoot.

Changed the size of the fractal signals.

Script open-source

Dans l'esprit TradingView, le créateur de ce script l'a rendu open source afin que les traders puissent examiner et vérifier ses fonctionnalités. Bravo à l'auteur! Bien que vous puissiez l'utiliser gratuitement, n'oubliez pas que la republication du code est soumise à nos Règles.

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

Clause de non-responsabilité

Les informations et publications ne sont pas destinées à être, et ne constituent pas, des conseils ou recommandations financiers, d'investissement, de trading ou autres fournis ou approuvés par TradingView. Pour en savoir plus, consultez les Conditions d'utilisation.

Script open-source

Dans l'esprit TradingView, le créateur de ce script l'a rendu open source afin que les traders puissent examiner et vérifier ses fonctionnalités. Bravo à l'auteur! Bien que vous puissiez l'utiliser gratuitement, n'oubliez pas que la republication du code est soumise à nos Règles.

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

Clause de non-responsabilité

Les informations et publications ne sont pas destinées à être, et ne constituent pas, des conseils ou recommandations financiers, d'investissement, de trading ou autres fournis ou approuvés par TradingView. Pour en savoir plus, consultez les Conditions d'utilisation.