Auto Keltner ChannelsThis version of Keltner Channels take measures the average volatility. By taking the 75th percentile of the average absolute value of the difference between the Source and the Mean divided by the True Range and using that as our multiplier for our Keltner Channels we can have a statistically safe trading zone. You notice that its dynamic, this is because it take into account the real volatility levels of a window and uses that to determine an appropriate multiplier. As always I hope you enjoy this release.

Gorx1

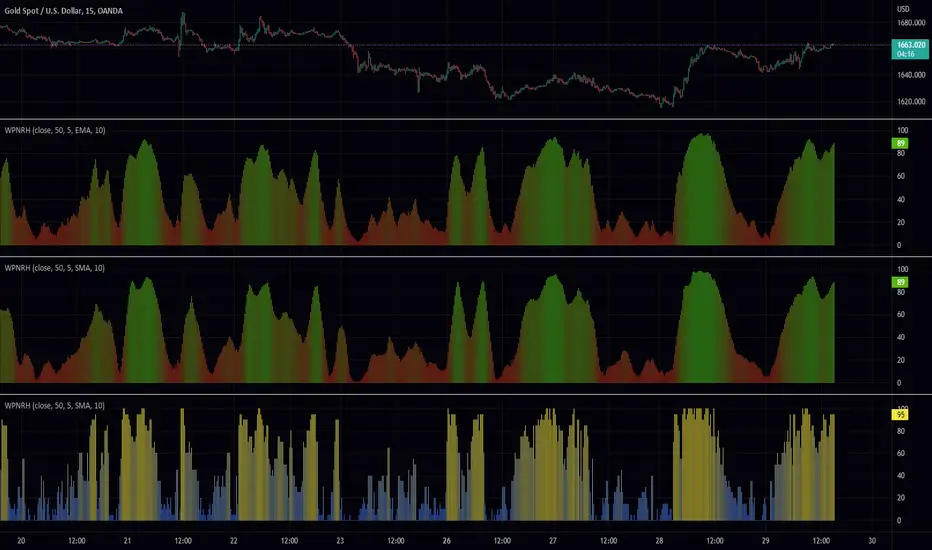

Weighted percentile nearest rank histogram (WPNRH)Original script

I tried to visualize what percentile the price is at as a column chart. It isnt as good as it could possibly be Im sure, but I could only fit in steps of 10 due to processing limits. Due to the flawed way I am attempting this there are some times gaps in the data. To fix this I added a gap fill feature that just takes the last known value and transfers it over to current.

I hope you enjoy!

Weighted percentile nearest rank oscillatorOriginal script

This is my attempt at making a price oscillator out of gorx1's weighted percentile nearest rank script. I centered everything to the 50th percentile and everything oscillates around that. The upper and lower bounds are 100th and 0th. Normalization normalizes the data to the top and bottom lines. The 'center line' represents the momentum of the 50th percentile in either direction. Good luck and happy hunting.

Relative slopeRelative slope metric

Description:

I was in need to create a simple, naive and elegant metric that was able to tell how strong is the trend in a given rolling window. While abstaining from using more complicated and arguably more precise approaches, I’ve decided to use Linearly Weighted Linear Regression slope for this goal. Outright values are useful, but the problem was that I wasn’t able to use it in comparative analysis, i.e between different assets & different resolutions & different window sizes, because obviously the outputs are scale-variant.

Here is the asset-agnostic, resolution-agnostic and window size agnostic version of the metric.

I made it asset agnostic & resolution agnostic by including spread information to the formula. In our case it's weighted stdev over differenced data (otherwise we contaminate the spread with the trend info). And I made it window size agnostic by adding a non-linear relation of length to the output, so finally it will be aprox in (-1, 1) interval, by taking square root of length, nothing fancy. All these / 2 and * 2 in unexpected places all around the formula help us to return the data to it’s natural scale while keeping the transformations in place.

Peace TV

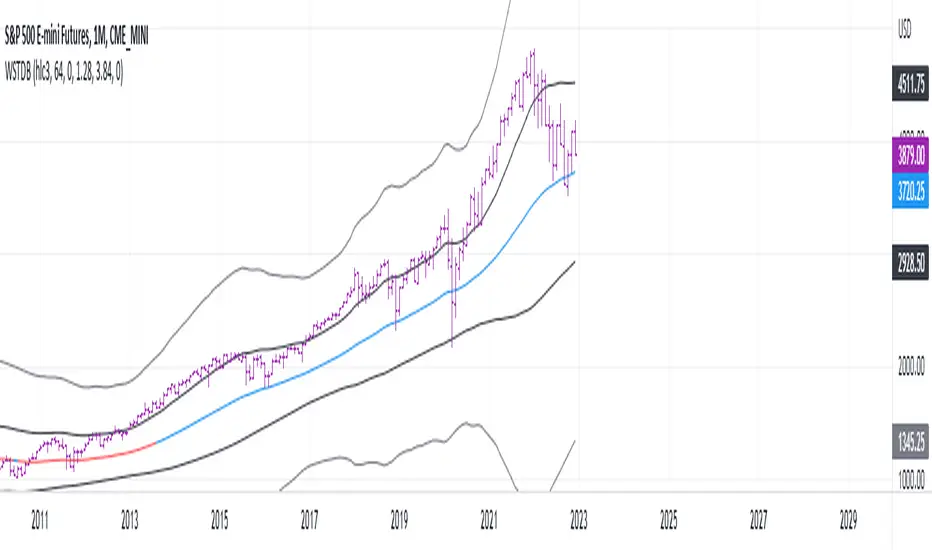

Weighted Standard Deviation BandsLinearly weighted standard deviations over linearly weighted mean.

The rationale of the study can be deduced from my latest publications where I go deeper into explaining the benefits of linear weighting, but in short, I can remind that by using linear weighting we are able to increase the information gain by communicating the sequential nature of time series to the calculations via linear weighting.

Note, that multiplier parameters can take both negative and positive values resulting in ability to have, for example, 1st and 6th weighted standard deviations higher than the weighted mean.

Despite the modification of the classic standard deviation formula, I assume that mathematical qualities of standard deviation will hold due to the fact we can alternately weight the window itself, and then apply the classic standard deviation over the weighted window. In both cases, the results will be the same.

Aight that was too formal, but your short strangles should be happy

Here is it, for you