Commodity Channel Index CCI + EMA strategy

================================================================================

COMMODITY CHANNEL INDEX CCI + EMA STRATEGY - STRATEGY GUIDE 📊

================================================================================

💡 COLLABORATION & SUPPORT

---------------------------

If you want to collaborate, have an idea for a strategy, or need help writing

or customizing code, send an email to burdytrader@gmail.com or send me a

message. Suggestions, ideas, and comments are always welcome! 🤝

I also develop automated trading codes for other trading platforms including:

- CTrader (C#)

- MetaTrader 4 (MQL4)

- MetaTrader 5 (MQL5)

If you need a strategy converted or developed for any of these platforms, feel

free to contact me!

================================================================================

⚠️ IMPORTANT: INSTRUMENT SELECTION 📈

-------------------------------------

This strategy performs BEST with currency pairs (forex). The CCI indicator

works particularly well in the forex market due to the nature of currency

movements and the effectiveness of the CCI in identifying overbought and

oversold conditions in trending markets.

Why Currency Pairs? 🎯

- CCI is highly effective in identifying reversals in forex markets

- Currency pairs show clear overbought/oversold patterns

- EMA filter (50/200) aligns well with major forex trends

- High liquidity ensures reliable signal execution

Performance Highlights:

In specific currency pairs, when properly configured, this strategy can achieve:

- Profit Factor: Over 2.0

- Win Rate: Up to 70%

- Particularly effective pairs: USDCAD, EURUSD, GBPJPY

While the strategy can work with other instruments (stocks, indices, commodities),

currency pairs provide the most consistent and reliable results. For optimal

performance, focus on major forex pairs with good liquidity and clear trending

characteristics.

================================================================================

WHAT DOES THIS STRATEGY DO? 🎯

---------------------------

This strategy combines the Commodity Channel Index (CCI) with Exponential

Moving Averages (EMA) to identify high-probability trading opportunities.

The strategy uses CCI crossovers with a smoothing moving average and filters

signals using EMA trend confirmation. The strategy automatically enters trades

when CCI crosses the smoothing MA in specific zones, indicating potential trend

reversals or continuations.

HOW IT WORKS? ⚙️

---------------

1. CCI CALCULATION 📈

The strategy calculates the Commodity Channel Index using:

- CCI = (Price - SMA(Price, length)) / (0.015 × Deviation(Price, length))

- Default length: 20 periods

- Source: HLC3 (typical price)

The CCI shows:

- Values above +100 = Overbought conditions

- Values below -100 = Oversold conditions

- Values around 0 = Neutral conditions

2. SMOOTHING MOVING AVERAGE 📊

A moving average is applied to the CCI to smooth out fluctuations:

- Types available: SMA, EMA, SMMA (RMA), WMA, VWMA

- Default: SMA with length 14

- Can be disabled (set to "None")

This smoothed line acts as a reference for crossover signals.

3. EMA TREND FILTER 🎯

Two EMAs are calculated on the CCI:

- EMA 50 (fast EMA)

- EMA 200 (slow EMA)

When the EMA filter is enabled:

- LONG signals only occur when EMA50 > EMA200 (uptrend confirmation)

- SHORT signals only occur when EMA50 < EMA200 (downtrend confirmation)

This filter can be enabled/disabled via the "Use EMA Filter" option.

4. ENTRY CONDITIONS 🎲

LONG ENTRY (Buy Signal):

- CCI crosses ABOVE the Smoothing MA (crossover)

- CCI is between Lower Level (-100) and Middle Level (0)

- EMA Filter: EMA50 > EMA200 (if filter enabled)

- No existing positions (or close opposite positions first)

SHORT ENTRY (Sell Signal):

- CCI crosses BELOW the Smoothing MA (crossunder)

- CCI is between Middle Level (0) and Upper Level (+100)

- EMA Filter: EMA50 < EMA200 (if filter enabled)

- No existing positions (or close opposite positions first)

5. POSITION MANAGEMENT 💰

The strategy uses a simple position management approach:

- Only ONE position at a time (no pyramiding)

- If a signal occurs in the opposite direction, closes existing position first

- Then opens new position in the new direction

- This prevents overexposure and simplifies risk management

6. TAKE PROFIT & STOP LOSS SETTINGS 🎯

The strategy uses percentage-based TP/SL:

- Take Profit: 1.0% (default, configurable)

- Stop Loss: 0.5% (default, configurable)

- Risk/Reward Ratio: 2:1 (TP is double the SL)

TP/SL are calculated once when the position opens and remain fixed.

AVAILABLE PARAMETERS ⚙️

-----------------------

CCI SETTINGS:

1. CCI Length (Default: 20)

- Period for CCI calculation

- Lower values = More sensitive to recent price action

- Higher values = More smoothed, less sensitive

2. CCI Source (Default: HLC3)

- Price source for CCI calculation

- Options: close, open, high, low, hlc3, hlcc4, ohlc4

3. CCI Lower Level (Default: -100)

- Lower boundary for LONG entry zone

- Typically -100 for oversold conditions

4. CCI Middle Level (Default: 0)

- Neutral level separating LONG and SHORT zones

5. CCI Upper Level (Default: +100)

- Upper boundary for SHORT entry zone

- Typically +100 for overbought conditions

SMOOTHING MA:

6. Type (Default: SMA)

- Moving average type: None, SMA, EMA, SMMA (RMA), WMA, VWMA

- Set to "None" to disable smoothing

7. Length (Default: 14)

- Period for smoothing MA

- Range: 7-28, step 7

EMA FILTER:

8. EMA 1 Length (Default: 50)

- Fast EMA period applied to CCI

9. EMA 2 Length (Default: 200)

- Slow EMA period applied to CCI

10. Use EMA Filter (Default: true)

- Enable/disable EMA trend filter

- When enabled: LONG only if EMA50 > EMA200, SHORT only if EMA50 < EMA200

RISK MANAGEMENT:

11. Take Profit (%) (Default: 1.0%)

- Profit target as percentage of entry price

- For LONG: Entry × (1 + TP%)

- For SHORT: Entry × (1 - TP%)

12. Stop Loss (%) (Default: 0.5%)

- Stop loss as percentage of entry price

- For LONG: Entry × (1 - SL%)

- For SHORT: Entry × (1 + SL%)

VISUALIZATION 📊

---------------

The strategy displays in a separate panel below the price chart:

1. CCI LINE

- Blue line showing the CCI value

- Oscillates around zero

2. SMOOTHING MA LINE

- Yellow line showing the smoothed CCI

- Reference line for crossover signals

3. CCI LEVEL LINES

- Red dashed line: Upper Level (+100)

- Green dashed line: Lower Level (-100)

- Yellow dashed line: Middle Level (0)

4. ENTRY SIGNALS

- Green cross: LONG entry signal (when CCI crosses above MA)

- Red cross: SHORT entry signal (when CCI crosses below MA)

RECOMMENDED SETTINGS 🎯

-----------------------

To get started, you can use these settings:

CCI SETTINGS:

- CCI Length: 20 (default)

- CCI Source: HLC3 (default)

- CCI Lower Level: -100 (default)

- CCI Middle Level: 0 (default)

- CCI Upper Level: +100 (default)

SMOOTHING MA:

- Type: SMA (default) or EMA for faster response

- Length: 14 (default)

EMA FILTER:

- EMA 1 Length: 50 (default)

- EMA 2 Length: 200 (default)

- Use EMA Filter: true (recommended for better signal quality)

RISK MANAGEMENT:

- Take Profit (%): 1.0% (adjust based on your risk/reward preference)

- Stop Loss (%): 0.5% (adjust based on your risk tolerance)

For more aggressive trading:

- Reduce CCI Length to 14-16

- Reduce Smoothing MA Length to 7

- Disable EMA Filter

For more conservative trading:

- Increase CCI Length to 24-30

- Increase Smoothing MA Length to 21-28

- Keep EMA Filter enabled

RECOMMENDED CURRENCY PAIRS 💱

------------------------------

This strategy is optimized for currency pairs and performs exceptionally well

on the following pairs when properly configured:

TOP PERFORMING PAIRS:

- USDCAD: Can achieve Profit Factor > 2.0 and Win Rate up to 70%

- EURUSD: Excellent performance with consistent signals

- GBPJPY: Strong results with proper EMA filter configuration

These pairs have shown the best historical performance due to:

- Clear trending characteristics

- Good response to CCI overbought/oversold levels

- Strong alignment with EMA 50/200 trend filter

- High liquidity ensuring reliable execution

When trading these pairs, use the default settings or slightly adjusted

parameters based on the pair's volatility. Always backtest on historical

data before using real money to find the optimal configuration for each

specific pair.

PRACTICAL EXAMPLE 📝

--------------------

Scenario: LONG Entry on EUR/USD

1. Market conditions:

- Price: 1.1000

- CCI: -80 (in oversold zone)

- Smoothing MA: -90

- CCI crosses above Smoothing MA (crossover occurs)

- EMA50: -50, EMA200: -70 (EMA50 > EMA200, uptrend confirmed)

2. Strategy checks conditions:

✓ Smoothing MA enabled: Yes

✓ Crossover: Yes (CCI crosses above MA)

✓ CCI in range: Yes (-100 <= -80 <= 0)

✓ EMA Filter: Yes (EMA50 > EMA200)

✓ No existing position: Yes

3. Strategy opens position:

- Direction: LONG (Buy)

- Entry: 1.1000 (current close)

- Take Profit: 1.1110 (1.0% above entry)

- Stop Loss: 1.0945 (0.5% below entry)

- Risk/Reward: 2:1

4. Outcome scenarios:

- If price rises to 1.1110 → Take Profit hit (profit)

- If price falls to 1.0945 → Stop Loss hit (loss limited)

IMPORTANT NOTE ⚠️

-----------------

This strategy is a technical analysis tool based on CCI and EMA indicators.

Like all trading strategies, it does NOT guarantee profits. Trading involves

significant risks and you can lose money, including your entire investment.

Past performance does not guarantee future results.

Always:

- Use appropriate risk management

- Never risk more than you can afford to lose

- Test the strategy on historical data (backtesting) before using real money

- Start with small position sizes or paper trading

- Understand that no strategy works 100% of the time

- Consider market conditions, news events, and other factors

- Keep a trading journal to learn and improve

The author and contributors are NOT responsible for any losses incurred from

using this strategy. Trading decisions are your own responsibility. Profits

are NOT guaranteed, and losses are possible.

LICENSE 📄

----------

This code is open source and available for modification. You are free to use,

modify, and distribute this strategy. If you republish or share a modified

version, please kindly mention the original author.

================================================================================

Index

Mean Reversion Trading V1Overview

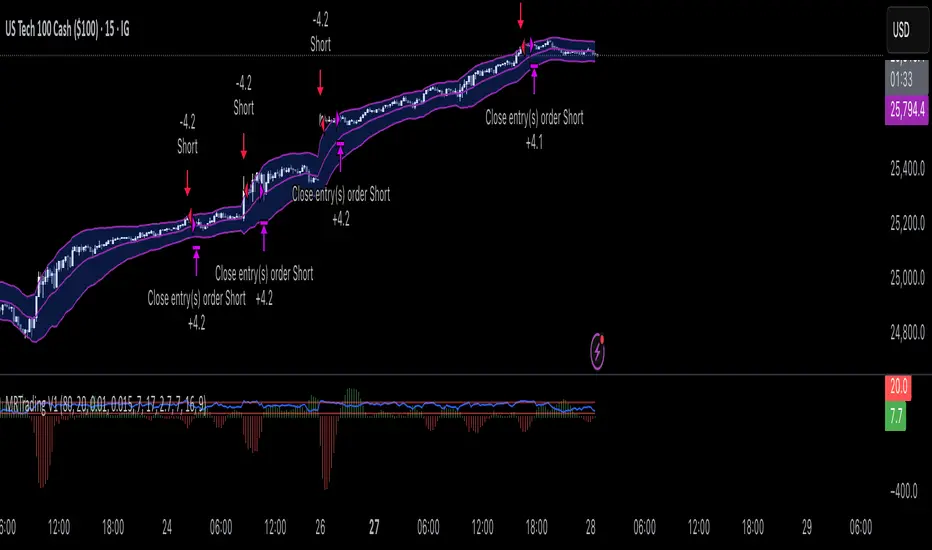

This is a simple mean reversion strategy that combines RSI, Keltner Channels, and MACD Histograms to predict reversals. Current parameters were optimized for NASDAQ 15M and performance varies depending on asset. The strategy can be optimized for specific asset and timeframe.

How it works

Long Entry (All must be true):

1. RSI < Lower Threshold

2. Close < Lower KC Band

3. MACD Histogram > 0 and rising

4. No open trades

Short Entry (All must be true):

1. RSI > Upper Threshold

2. Close > Upper KC Band

3. MACD Histogram < 0 and falling

4. No open trades

Long Exit:

1. Stop Loss: Average position size x ( 1 - SL percent)

2. Take Profit: Average position size x ( 1 + TP percent)

3. MACD Histogram crosses below zero

Short Exit:

1. Stop Loss: Average position size x ( 1 + SL percent)

2. Take Profit: Average position size x ( 1 - TP percent)

3. MACD Histogram crosses above zero

Settings and parameters are explained in the tooltips.

Important

Initial capital is set as 100,000 by default and 100 percent equity is used for trades

RSI Momentum ScalperOverview

The "RSI Momentum Scalper" is a Pine Script v5 strategy crafted for trading highly volatile markets, with a special focus on newly listed cryptocurrencies. This strategy harnesses the Relative Strength Index (RSI) alongside volume analysis and momentum thresholds to pinpoint short-term trading opportunities. It supports both long and short trades, managed with customizable take profit, stop loss, and trailing stop levels, which are visually plotted on the chart for easy tracking.

Why I Created This Strategy

I developed the "RSI Momentum Scalper" because I was seeking a reliable trading strategy tailored to newly listed, highly volatile cryptocurrencies. These assets often experience rapid price fluctuations, rendering traditional strategies less effective. I aimed to create a tool that could exploit momentum and volume spikes while managing risk through adaptable exit parameters. This strategy is designed to address that need, offering a flexible approach for traders in dynamic crypto markets.

How It Works

The strategy utilizes RSI to identify momentum shifts, combined with volume confirmation, to trigger long or short entries. Trades are controlled with take profit, stop loss, and trailing stop levels, which adjust dynamically as the price moves in your favor. The trailing stop helps lock in profits, while the plotted exit levels provide clear visual cues for trade management.

Customizable Settings

The script is highly customizable, allowing you to adjust it to various market conditions and trading styles. Here’s a brief overview of the key settings:

Trade Mode: Select "Both," "Long Only," or "Short Only" to determine the trade direction.

(Default: Both)

RSI Length: Sets the lookback period for the RSI calculation (2 to 30).

(Default: 8)

A shorter length increases RSI sensitivity, suitable for volatile assets.

RSI Overbought: Defines the upper RSI threshold (60 to 99) for short entries.

(Default: 90)

Higher values signal stronger overbought conditions.

RSI Oversold: Defines the lower RSI threshold (1 to 40) for long entries.

(Default: 10)

Lower values indicate stronger oversold conditions.

RSI Momentum Threshold: Sets the minimum RSI momentum change (1 to 15) to trigger entries.

(Default: 14)

Adjusts the sensitivity to price momentum.

Volume Multiplier: Multiplies the volume moving average to filter high-volume bars (1.0 to 3.0).

(Default: 1)

Higher values require stronger volume confirmation.

Volume MA Length: Sets the lookback period for the volume moving average (5 to 50).

(Default: 13)

Influences the volume trend sensitivity.

Take Profit %: Sets the profit target as a percentage of the entry price (0.1 to 10.0).

(Default: 4.15)

Determines when to close a winning trade.

Stop Loss %: Sets the loss limit as a percentage of the entry price (0.1 to 6.0).

(Default: 1.85)

Protects against significant losses.

Trailing Stop %: Sets the trailing stop distance as a percentage (0.1 to 4.0).

(Default: 2.55)

Locks in profits as the price moves favorably.

Visual Features

Exit Levels: Take profit (green), fixed stop loss (red), and trailing stop (orange) levels are plotted when in a position.

Performance Table: Displays win rate, total trades, and net profit in the top-right corner.

How to Use

Add the strategy to your chart in TradingView.

Adjust the input settings based on the cryptocurrency and timeframe you’re trading.

Monitor the plotted exit levels for trade management.

Use the performance table to assess the strategy’s performance over time.

Notes

Test the strategy on a demo account or with historical data before live trading.

The strategy is optimized for short-term scalping; adjust settings for longer timeframes if needed.

Simple APF Strategy Backtesting [The Quant Science]Simple backtesting strategy for the quantitative indicator Autocorrelation Price Forecasting. This is a Buy & Sell strategy that operates exclusively with long orders. It opens long positions and generates profit based on the future price forecast provided by the indicator. It's particularly suitable for trend-following trading strategies or directional markets with an established trend.

Main functions

1. Cycle Detection: Utilize autocorrelation to identify repetitive market behaviors and cycles.

2. Forecasting for Backtesting: Simulate trades and assess the profitability of various strategies based on future price predictions.

Logic

The strategy works as follow:

Entry Condition: Go long if the hypothetical gain exceeds the threshold gain (configurable by user interface).

Position Management: Sets a take-profit level based on the future price.

Position Sizing: Automatically calculates the order size as a percentage of the equity.

No Stop-Loss: this strategy doesn't includes any stop loss.

Example Use Case

A trader analyzes a dayli period using 7 historical bars for autocorrelation.

Sets a threshold gain of 20 points using a 5% of the equity for each trade.

Evaluates the effectiveness of a long-only strategy in this period to assess its profitability and risk-adjusted performance.

User Interface

Length: Set the length of the data used in the autocorrelation price forecasting model.

Thresold Gain: Minimum value to be considered for opening trades based on future price forecast.

Order Size: percentage size of the equity used for each single trade.

Strategy Limit

This strategy does not use a stop loss. If the price continues to drop and the future price forecast is incorrect, the trader may incur a loss or have their capital locked in the losing trade.

Disclaimer!

This is a simple template. Use the code as a starting point rather than a finished solution. The script does not include important parameters, so use it solely for educational purposes or as a boilerplate.

Intramarket Difference Index StrategyHi Traders !!

The IDI Strategy:

In layman’s terms this strategy compares two indicators across markets and exploits their differences.

note: it is best the two markets are correlated as then we know we are trading a short to long term deviation from both markets' general trend with the assumption both markets will trend again sometime in the future thereby exhausting our trading opportunity.

📍 Import Notes:

This Strategy calculates trade position size independently (i.e. risk per trade is controlled in the user inputs tab), this means that the ‘Order size’ input in the ‘Properties’ tab will have no effect on the strategy. Why ? because this allows us to define custom position size algorithms which we can use to improve our risk management and equity growth over time. Here we have the option to have fixed quantity or fixed percentage of equity ATR (Average True Range) based stops in addition to the turtle trading position size algorithm.

‘Pyramiding’ does not work for this strategy’, similar to the order size input togeling this input will have no effect on the strategy as the strategy explicitly defines the maximum order size to be 1.

This strategy is not perfect, and as of writing of this post I have not traded this algo.

Always take your time to backtests and debug the strategy.

🔷 The IDI Strategy:

By default this strategy pulls data from your current TV chart and then compares it to the base market, be default BINANCE:BTCUSD . The strategy pulls SMA and RSI data from either market (we call this the difference data), standardizes the data (solving the different unit problem across markets) such that it is comparable and then differentiates the data, calling the result of this transformation and difference the Intramarket Difference (ID). The formula for the the ID is

ID = market1_diff_data - market2_diff_data (1)

Where

market(i)_diff_data = diff_data / ATR(j)_market(i)^0.5,

where i = {1, 2} and j = the natural numbers excluding 0

Formula (1) interpretation is the following

When ID > 0: this means the current market outperforms the base market

When ID = 0: Markets are at long run equilibrium

When ID < 0: this means the current market underperforms the base market

To form the strategy we define one of two strategy type’s which are Trend and Mean Revesion respectively.

🔸 Trend Case:

Given the ‘‘Strategy Type’’ is equal to TREND we define a threshold for which if the ID crosses over we go long and if the ID crosses under the negative of the threshold we go short.

The motivating idea is that the ID is an indicator of the two symbols being out of sync, and given we know volatility clustering, momentum and mean reversion of anomalies to be a stylised fact of financial data we can construct a trading premise. Let's first talk more about this premise.

For some markets (cryptocurrency markets - synthetic symbols in TV) the stylised fact of momentum is true, this means that higher momentum is followed by higher momentum, and given we know momentum to be a vector quantity (with magnitude and direction) this momentum can be both positive and negative i.e. when the ID crosses above some threshold we make an assumption it will continue in that direction for some time before executing back to its long run equilibrium of 0 which is a reasonable assumption to make if the market are correlated. For example for the BTCUSD - ETHUSD pair, if the ID > +threshold (inputs for MA and RSI based ID thresholds are found under the ‘‘INTRAMARKET DIFFERENCE INDEX’’ group’), ETHUSD outperforms BTCUSD, we assume the momentum to continue so we go long ETHUSD.

In the standard case we would exit the market when the IDI returns to its long run equilibrium of 0 (for the positive case the ID may return to 0 because ETH’s difference data may have decreased or BTC’s difference data may have increased). However in this strategy we will not define this as our exit condition, why ?

This is because we want to ‘‘let our winners run’’, to achieve this we define a trailing Donchian Channel stop loss (along with a fixed ATR based stop as our volatility proxy). If we were too use the 0 exit the strategy may print a buy signal (ID > +threshold in the simple case, market regimes may be used), return to 0 and then print another buy signal, and this process can loop may times, this high trade frequency means we fail capture the entire market move lowering our profit, furthermore on lower time frames this high trade frequencies mean we pay more transaction costs (due to price slippage, commission and big-ask spread) which means less profit.

By capturing the sum of many momentum moves we are essentially following the trend hence the trend following strategy type.

Here we also print the IDI (with default strategy settings with the MA difference type), we can see that by letting our winners run we may catch many valid momentum moves, that results in a larger final pnl that if we would otherwise exit based on the equilibrium condition(Valid trades are denoted by solid green and red arrows respectively and all other valid trades which occur within the original signal are light green and red small arrows).

another example...

Note: if you would like to plot the IDI separately copy and paste the following code in a new Pine Script indicator template.

indicator("IDI")

// INTRAMARKET INDEX

var string g_idi = "intramarket diffirence index"

ui_index_1 = input.symbol("BINANCE:BTCUSD", title = "Base market", group = g_idi)

// ui_index_2 = input.symbol("BINANCE:ETHUSD", title = "Quote Market", group = g_idi)

type = input.string("MA", title = "Differrencing Series", options = , group = g_idi)

ui_ma_lkb = input.int(24, title = "lookback of ma and volatility scaling constant", group = g_idi)

ui_rsi_lkb = input.int(14, title = "Lookback of RSI", group = g_idi)

ui_atr_lkb = input.int(300, title = "ATR lookback - Normalising value", group = g_idi)

ui_ma_threshold = input.float(5, title = "Threshold of Upward/Downward Trend (MA)", group = g_idi)

ui_rsi_threshold = input.float(20, title = "Threshold of Upward/Downward Trend (RSI)", group = g_idi)

//>>+----------------------------------------------------------------+}

// CUSTOM FUNCTIONS |

//<<+----------------------------------------------------------------+{

// construct UDT (User defined type) containing the IDI (Intramarket Difference Index) source values

// UDT will hold many variables / functions grouped under the UDT

type functions

float Close // close price

float ma // ma of symbol

float rsi // rsi of the asset

float atr // atr of the asset

// the security data

getUDTdata(symbol, malookback, rsilookback, atrlookback) =>

indexHighTF = barstate.isrealtime ? 1 : 0

= request.security(symbol, timeframe = timeframe.period,

expression = [close , // Instentiate UDT variables

ta.sma(close, malookback) ,

ta.rsi(close, rsilookback) ,

ta.atr(atrlookback) ])

data = functions.new(close_, ma_, rsi_, atr_)

data

// Intramerket Difference Index

idi(type, symbol1, malookback, rsilookback, atrlookback, mathreshold, rsithreshold) =>

threshold = float(na)

index1 = getUDTdata(symbol1, malookback, rsilookback, atrlookback)

index2 = getUDTdata(syminfo.tickerid, malookback, rsilookback, atrlookback)

// declare difference variables for both base and quote symbols, conditional on which difference type is selected

var diffindex1 = 0.0, var diffindex2 = 0.0,

// declare Intramarket Difference Index based on series type, note

// if > 0, index 2 outpreforms index 1, buy index 2 (momentum based) until equalibrium

// if < 0, index 2 underpreforms index 1, sell index 1 (momentum based) until equalibrium

// for idi to be valid both series must be stationary and normalised so both series hae he same scale

intramarket_difference = 0.0

if type == "MA"

threshold := mathreshold

diffindex1 := (index1.Close - index1.ma) / math.pow(index1.atr*malookback, 0.5)

diffindex2 := (index2.Close - index2.ma) / math.pow(index2.atr*malookback, 0.5)

intramarket_difference := diffindex2 - diffindex1

else if type == "RSI"

threshold := rsilookback

diffindex1 := index1.rsi

diffindex2 := index2.rsi

intramarket_difference := diffindex2 - diffindex1

//>>+----------------------------------------------------------------+}

// STRATEGY FUNCTIONS CALLS |

//<<+----------------------------------------------------------------+{

// plot the intramarket difference

= idi(type,

ui_index_1,

ui_ma_lkb,

ui_rsi_lkb,

ui_atr_lkb,

ui_ma_threshold,

ui_rsi_threshold)

//>>+----------------------------------------------------------------+}

plot(intramarket_difference, color = color.orange)

hline(type == "MA" ? ui_ma_threshold : ui_rsi_threshold, color = color.green)

hline(type == "MA" ? -ui_ma_threshold : -ui_rsi_threshold, color = color.red)

hline(0)

Note it is possible that after printing a buy the strategy then prints many sell signals before returning to a buy, which again has the same implication (less profit. Potentially because we exit early only for price to continue upwards hence missing the larger "trend"). The image below showcases this cenario and again, by allowing our winner to run we may capture more profit (theoretically).

This should be clear...

🔸 Mean Reversion Case:

We stated prior that mean reversion of anomalies is an standerdies fact of financial data, how can we exploit this ?

We exploit this by normalizing the ID by applying the Ehlers fisher transformation. The transformed data is then assumed to be approximately normally distributed. To form the strategy we employ the same logic as for the z score, if the FT normalized ID > 2.5 (< -2.5) we buy (short). Our exit conditions remain unchanged (fixed ATR stop and trailing Donchian Trailing stop)

🔷 Position Sizing:

If ‘‘Fixed Risk From Initial Balance’’ is toggled true this means we risk a fixed percentage of our initial balance, if false we risk a fixed percentage of our equity (current balance).

Note we also employ a volatility adjusted position sizing formula, the turtle training method which is defined as follows.

Turtle position size = (1/ r * ATR * DV) * C

Where,

r = risk factor coefficient (default is 20)

ATR(j) = risk proxy, over j times steps

DV = Dollar Volatility, where DV = (1/Asset Price) * Capital at Risk

🔷 Risk Management:

Correct money management means we can limit risk and increase reward (theoretically). Here we employ

Max loss and gain per day

Max loss per trade

Max number of consecutive losing trades until trade skip

To read more see the tooltips (info circle).

🔷 Take Profit:

By defualt the script uses a Donchain Channel as a trailing stop and take profit, In addition to this the script defines a fixed ATR stop losses (by defualt, this covers cases where the DC range may be to wide making a fixed ATR stop usefull), ATR take profits however are defined but optional.

ATR SL and TP defined for all trades

🔷 Hurst Regime (Regime Filter):

The Hurst Exponent (H) aims to segment the market into three different states, Trending (H > 0.5), Random Geometric Brownian Motion (H = 0.5) and Mean Reverting / Contrarian (H < 0.5). In my interpretation this can be used as a trend filter that eliminates market noise.

We utilize the trending and mean reverting based states, as extra conditions required for valid trades for both strategy types respectively, in the process increasing our trade entry quality.

🔷 Example model Architecture:

Here is an example of one configuration of this strategy, combining all aspects discussed in this post.

Future Updates

- Automation integration (next update)

[Pt] Premarket Breakout StrategyThis is a 1 trade per day strategy for trading SPY or QQQ index. By default, this is designed for 1 min time frame. This was an experimental script that seems to be profitable at the time of publication.

How it works:

Pre-market high and low is defined per trading day between 9:00 to 9:30 EST.

Then we looking for the first breakout on either PM high or PM low.

- Breakout high = long trade

- Breakout low = short trade

If long trade, we wait until Stochastic RSI D signal line to hit a lower threshold (18 by default). Then we enter long when K crosses above D line.

If short trade, we wait until Stochastic RSI D signal line to hit an upper threshold (82 by default). Then we enter short when K crosses below D line.

Stop loss for long

- set to PM low if entry is above PM high + %ATR buffer

- or set to PM range + %ATR buffer

Stop loss for short

- set to PM high if entry is below PM low + %ATR buffer

- or set to PM range + %ATR buffer

Profit target is set to 2x the risk by default.

*Note: Different Stochastic RSI lengths should be used if trading 5 min time frame. See tooltip.

Happy trading~~!

Ichimoku with MACD/ CMF/ TSIThis is a very powerful trend strategy designed for markets such as stocks market , stock index and crypto.

For time frames I found out that 1h seems to do the trick.

Components:

Ichimoku full pack

MACD histogram

CMF oscillator

TSI oscillator

Rules for entry

Long :

For Ichimoku:Tenkan part of cloud is bigger than kijun, Chikou is above 0 , close of a candle is above the Senkou

MACD histogram is above 0

CMF oscillator is positive and bigger than 0.1

TSI oscillator is above 0

Short:

For Ichimoku:Tenkan part of cloud is smaller than kijun, Chikou is below 0 , close of a candle is belowthe Senkou

MACD histogram is below 0

CMF oscillator is negative and below -0.1

TSI oscillator is below 0

Rules for exit

This strategy does not have any risk management inside. Instead it exits whenver it receives an opposite signal form the original one used for entry.

If you have any questions let me know !

Combo Backtest 123 Reversal & Positive Volume Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The theory behind the indexes is as follows: On days of increasing volume,

you can expect prices to increase, and on days of decreasing volume, you can

expect prices to decrease. This goes with the idea of the market being in-gear

and out-of-gear. Both PVI and NVI work in similar fashions: Both are a running

cumulative of values, which means you either keep adding or subtracting price

rate of change each day to the previous day`s sum. In the case of PVI, if today`s

volume is less than yesterday`s, don`t add anything; if today`s volume is greater,

then add today`s price rate of change. For NVI, add today`s price rate of change

only if today`s volume is less than yesterday`s.

WARNING:

- For purpose educate only

- This script to change bars colors.

MACD oscillator with EMA strategy 4H This is a simple, yet efficient strategy, which is made from a combination of an oscillator and a moving average.

Its setup for 4h candles with the current settings, however it can be adapted to other different timeframes.

It works nicely ,beating the buy and hold for both BTC and ETH over the last 3 years.

As well with some optimizations and modifications it can be adapted to futures market, indexes(NASDAQ,NIFTY etc), forex(GBPUSD), stocks and so on.

Components:

MACD

EMA

Time condition

Long/short option

For long/exit short we enter when we are above the ema, histogram is positive and current candle is higher than previous.

For short /exit long , when close below ema, histo negative and current candles smaller than previous

If you have any questions please let me know !

Combo Backtest 123 Reversal & MASS Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Mass Index was designed to identify trend reversals by measuring

the narrowing and widening of the range between the high and low prices.

As this range widens, the Mass Index increases; as the range narrows

the Mass Index decreases.

The Mass Index was developed by Donald Dorsey.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Market Facilitation Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Market Facilitation Index is an indicator that relates price range to

volume and measures the efficency of price movement. Use the indicator to

determine if the market is trending. If the Market Facilitation Index increased,

then the market is facilitating trade and is more efficient, implying that the

market is trending. If the Market Facilitation Index decreased, then the market

is becoming less efficient, which may indicate a trading range is developing that

may be a trend reversal.

WARNING:

- For purpose educate only

- This script to change bars colors.

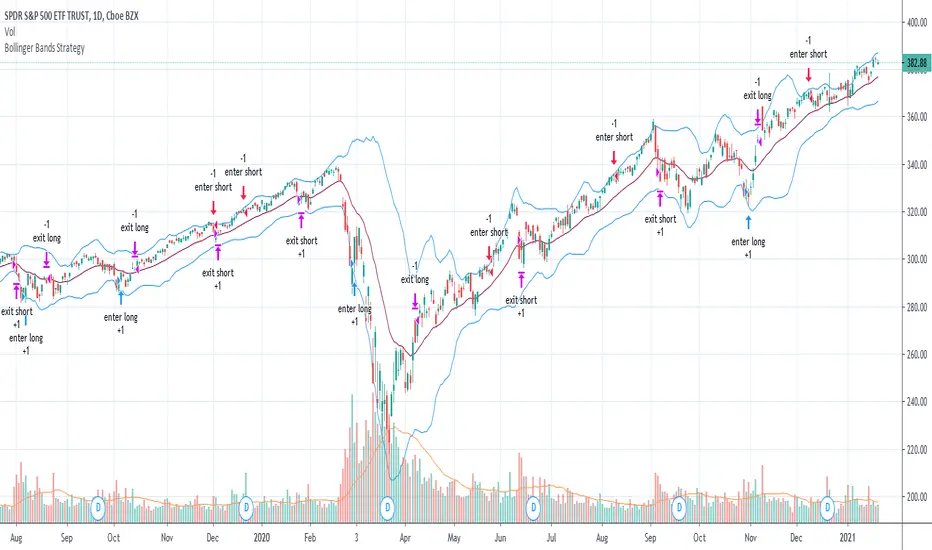

Bollinger Bands Strategy with Intraday Intensity IndexFor Educational Purposes. Results can differ on different markets and can fail at any time. Profit is not guaranteed.

This only works in a few markets and in certain situations. Changing the settings can give better or worse results for other markets.

This is a mean reversion strategy based on Bollinger Bands and the Intraday Intensity Index (a volume indicator). John Bollinger mentions that the Intraday Intensity Index can be used with Bollinger Bands and is one of the top indicators he recommends in his book. It seems he prefers it over the other volume indicators that he compares to for some reason. III looks a lot like Chaikin Money Flow but without the denominator in that calculation. On the default settings of the BBs, the III helps give off better entry signals. John Bollinger however is vague on how to use the BBs and it's hard to say if one should enter when it is below/above the bands or when the price crosses them. I find that with many indicators and strategies it's best to wait for a confirmation of some sort, in this case by waiting for some crossover of a band. Like most mean reversion strategies, the exit is very loose if using BBs alone. Usually the plan to exit is when the price finally reverts back to the mean or in this case the middle band. This can potentially lead to huge drawdowns and/or losses. Mean reversion strategies can have high win/loss ratios but can still end up unprofitable because of the huge losses that can occur. These drawdowns/losses that mean reversion strategies suffer from can potentially eat away at a large chunk of all that was previously made or perhaps up to all of it in the worst cases, can occur weeks or perhaps up to months after being profitable trading such a strategy, and will take a while and several trades to make it all back or keep a profitable track record. It is important to have a stop loss, trailing stop, or some sort of stop plan with these types of strategies. For this one, in addition to exiting the trade when price reverts to the middle band, I included a time-based stop plan that exits with a gain or with a loss to avoid potentially large losses, and to exit after only a few periods after taking the trade if in profit instead of waiting for the price to revert back to the mean.

The Lazy Trader - Index (ETF) Trend Following Robot50/150 moving average, index (ETF) trend following robot. Coded for people who cannot psychologically handle dollar-cost-averaging through bear markets and extreme drawdowns (although DCA can produce better results eventually), this robot helps you to avoid bear markets. Be a fair-weathered friend of Mr Market, and only take up his offer when the sun is shining! Designed for the lazy trader who really doesn't care...

Recommended Chart Settings:

Asset Class: ETF

Time Frame: Daily

Necessary ETF Macro Conditions:

a) Country must have healthy demographics, good ratio of young > old

b) Country population must be increasing

c) Country must be experiencing price-inflation

Default Robot Settings:

Slow Moving Average: 50 (integer) //adjust to suit your underlying index

Fast Moving Average: 150 (integer) //adjust to suit your underlying index

Bullish Slope Angle: 5 (degrees) //up angle of moving averages

Bearish Slope Angle: -5 (degrees) //down angle of moving averages

Average True Range: 14 (integer) //input for slope-angle formula

Risk: 100 (%) //100% risk means using all equity per trade

ETF Test Results (Default Settings):

SPY (1993 to 2020, 27 years), 332% profit, 20 trades, 6.4 profit factor, 7% drawdown

EWG (1996 to 2020, 24 years), 310% profit, 18 trades, 3.7 profit factor, 10% drawdown

EWH (1996 to 2020, 24 years), 4% loss, 26 trades, 0.9 profit factor, 36% drawdown

QQQ (1999 to 2020, 21 years), 232% profit, 17 trades, 3.6 profit factor, 2% drawdown

EEM (2003 to 2020, 17 years), 73% profit, 17 trades, 1.1 profit factor, 3% drawdown

GXC (2007 to 2020, 13 years), 18% profit, 14 trades, 1.3 profit factor, 26% drawdown

BKF (2009 to 2020, 11 years), 11% profit, 13 trades, 1.2 profit factor, 33% drawdown

A longer time in the markets is better, with the exception of EWH. 6 out of 7 tested ETFs were profitable, feel free to test on your favourite ETF (default settings) and comment below.

Risk Warning:

Not tested on commodities nor other financial products like currencies (code will not work), feel free to leave comments below.

Moving Average Slope Angle Formula:

Reproduced and modified from source:

Mean Reversion w/ Bollinger BandsThis is a more advanced version of my original mean reversion script.

It employs the famous Bollinger Bands.

This robot will buy when price falls below the lower Bollinger Band, and sell when price moves above the upper Bollinger Band.

I've only tested it on the S&P 500, though you could try it out on other assets to see the backtest performance.

During the recent COVID-19 bear market drop, it produced several buy signals on the S&P which I followed, and made some nice gains so far.

I still think this would make a better investing strategy (buy undervalued / sell over-valued), rather than a trading strategy.

I use this robot for my long term portfolio.

Combo Strategy 123 Reversal & CCI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Commodity Channel Index (CCI) is best used with markets that display cyclical or

seasonal characteristics, and is formulated to detect the beginning and ending of these

cycles by incorporating a moving average together with a divisor that reflects both possible

and actual trading ranges. The final index measures the deviation from normal, which indicates

major changes in market trend.

To put it simply, the Commodity Channel Index (CCI) value shows how the instrument is trading

relative to its mean (average) price. When the CCI value is high, it means that the prices are

high compared to the average price; when the CCI value is down, it means that the prices are low

compared to the average price. The CCI value usually does not fall outside the -300 to 300 range

and, in fact, is usually in the -100 to 100 range.

WARNING:

- For purpose educate only

- This script to change bars colors.

Commodity Selection Index Backtest The Commodity Selection Index ("CSI") is a momentum indicator. It was

developed by Welles Wilder and is presented in his book New Concepts in

Technical Trading Systems. The name of the index reflects its primary purpose.

That is, to help select commodities suitable for short-term trading.

A high CSI rating indicates that the commodity has strong trending and volatility

characteristics. The trending characteristics are brought out by the Directional

Movement factor in the calculation--the volatility characteristic by the Average

True Range factor.

Wilder's approach is to trade commodities with high CSI values (relative to other

commodities). Because these commodities are highly volatile, they have the potential

to make the "most money in the shortest period of time." High CSI values imply

trending characteristics which make it easier to trade the security.

The Commodity Selection Index is designed for short-term traders who can handle

the risks associated with highly volatile markets.

WARNING:

- For purpose educate only

- This script to change bars colors.