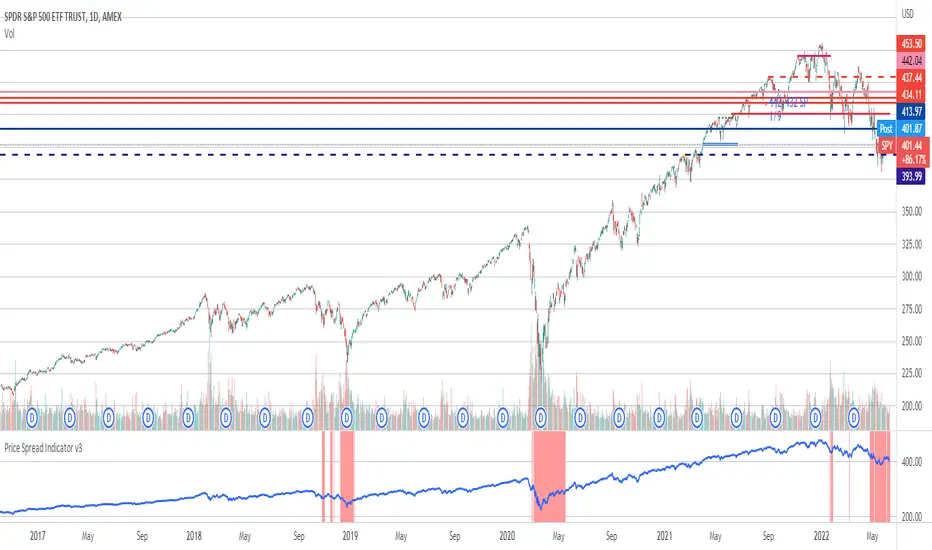

Price Spread Indicator v2Version 2 of this script. Looks at the spread of current price to two prior MA's. Defaults to 200 and 90 however 20 and 58 provide some nice results. A -1.3% spread ratio is used to trigger alerts ie -1.3% spread on 200 and 90. This has been derived from backtesting what optimised P&L.

Ideal for investors rather than traders. Out performs simple buy and hold by 5-6 times.

Gestion de portefeuille

Portfolio SummaryThe stocks in my portfolio has very poor performance since the FED hiked the rate.

since the covid-19, i came to the stock market and buy a stock that i ever heard the name which i don't even know its fundamental.

Some stock, i bought them at the hilltop (and sell at the bottom, hehe).

Everyone is a genius in a bull market ; and now i realized i am gonna loss money.

I have to do something, so i looked for an indicator that allow me to manage my portfolio.

unfortunately, i cannot find one that fit me.

so i make this indicator.

How you can get the benefit from this indicator

This indicator will summarize the gain/loss since you bought the stock.

it also include the dividend.

So that you can see how much you gain and loss, and make a decision as you wish.

How to use it

1. Input some neccessary data like ticker/stock (up to 20 tickers, yeah i know, it is too much), share, average price which you can input manually or depend on your entry date.

2. The indicator will calculate gain/loss, dividend, % of your portfolio.

3. You can select how to display based on "Index" or "Market Value".

4. You can toggle on/off both label and table.

Disclaimer

This indicator may display inaccurate and need a lot of improvement.

pls use carefully.

if you have any suggestion, pls dont hersitate to comment below.

Enjoy.

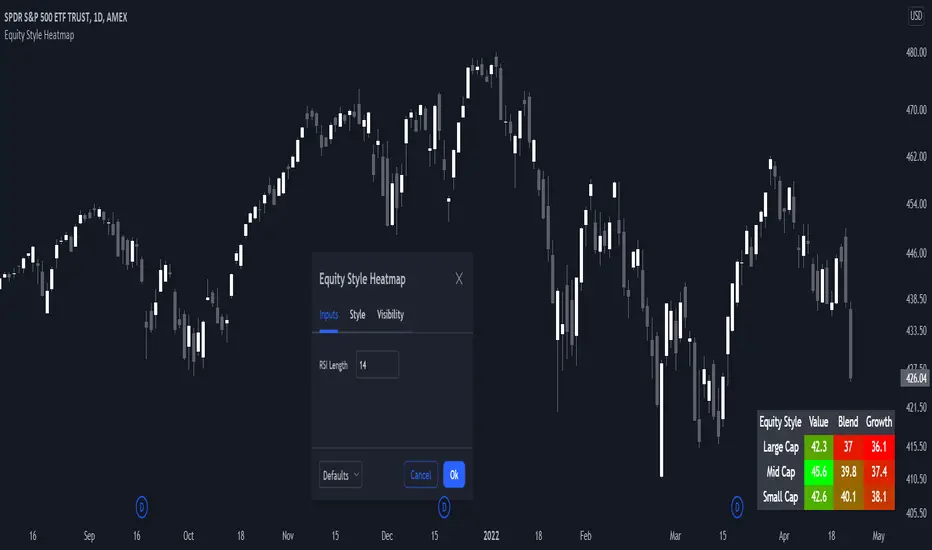

Morningstar Equity Style Box HeatmapStyle boxes are a classification scheme created by Morningstar. They visually provide a graphical representation of investing categories for equity investments. A style box is a valuable tool for investors to use when determining asset allocation.

There are 9 categories:

Large Value, Large Blend, Large Growth

Medium Value, Medium Blend, Medium Growth

Small Value, Small Blend, Small Growth

The strength of the 9 categories are found by using 9 Vanguard ETF's that follow the respective CRSP index of their category.

Niteya Multi Ticker Dollar-Based Pricing Ver 1.3The main purpose of the indicator is to make a future price estimation based on the highest dollar-based price of the stock in the past, especially for stocks that exceed their past prices in chart currency terms. There should be no expectation that this prediction will necessarily come true.

A table with six columns and 19 rows (excluding the header) is created on the graph, positioned bottom and left.

The first column contains the ticker code, the second column contains the highest historical price of the stock in currency, the third column contains the past high price of the stock in USD, the fourth column contains the closing price, the fifth column contains the value obtained by multiplying the past highest USD price of the stock by the daily dollar price, and the sixth column is includes the rate of increase.

Using the indicator interface, you can select the ticker value in the first row of the table from among 22 different values via a selection box, and for the 18 rows below, you can directly type the ticker name.

* The currency of the chart must be compatible with the dollar conversion currency. For example, if the conversion currency is "USDTRY", the currency of the chart should be "TRY".

All stocks in the indicator are randomly selected. Investment information, stock selections, comments and recommendations herein are not within the scope of investment consultancy. Investment consultancy service is provided within the framework of investment consultancy agreement to be signed between brokerage houses, portfolio management companies, non-deposit banks and the customer.

Türkçe açıklama

Göstergenin temel amacı, özellikle grafik para birimi (TRY) bazında geçmiş fiyatlarının üzerine çıkmış hisselerde, hissenin geçmişteki en yüksek dolar bazlı fiyatını esas alarak, geleceğe yönelik bir fiyat tahmininde bulunmaktır. Bu tahminin mutlaka gerçekleşeceği beklentisi olmamalıdır.

Grafik üzerinde, üste ve ortalanmış olarak, altı sütun ve başlık kısmı hariç 19 satırlık bir tablo oluşturulmaktadır.

İlk sütun hisse kodunu, ikinci sütun hissenin geçmiş en yüksek fiyatını TRY olarak, üçüncü sütun hissenin geçmiş en yüksek fiyatını USD olarak, dördüncü sütun kapanış fiyatını, beşinci sütun hissenin geçmiş en yüksek USD fiyatının günlük dolar kuru ile çarpılarak elde edilen değeri, altıncı sütun ise artış oranını içerir.

Gösterge arayüzünü kullanarak, tablonun ilk satırındaki ticker (hisse) değerini 22 farklı değer arasından (BIST 100 ve 21 şirket) bir seçim kutusu yoluyla, altta yer alan 18 satır için ise, doğrudan hisse adını yazabilirsiniz.

* Grafiğin para birimi dolar çevrim kuru ile uyumlu olmalıdır. Örneğin, çevrim kuru "USDTRY" ise, grafiğin para birimi "TRY" olmalıdır.

Gösterge içinde yer alan tüm hisseler rastgele seçilmiştir. Buradaki yatırım bilgileri, hisse seçimleri, yorum ve tavsiyeleri yatırım danışmanlığı kapsamında değildir. Yatırım danışmanlığı hizmeti, aracı kurumlar, portföy yönetim şirketleri, mevduat kabul etmeyen bankalar ile müşteri arasında imzalanacak yatırım danışmanlığı sözleşmesi çerçevesinde sunulmaktadır.

MilleMachineHello traders,

I hereby present to you the second stage of my journey to finding a reliable, profitable trading strategy.

The "Millemachine" is based on the "Millebot", my previous published strategy. This means the backbone of the strategy is still the same: a trend following system. Instead of using a fixed TP and SL, a trailing stoploss is now used. To limit the losses when the trend weakens, the trailing stoploss automatically gets smaller, as it is based on the ATR.

A new utility is you can now easily switch between indicators on which the decision making is based. This allows the user to discover which indicators work best for entry, long/short switching and stoploss configuration.

The strategy has been proven to be very profitable in trending markets, but can suffer losses during ranging market. To make the system more robust, the strategy cannot solely rely on a trending system. Other systems must be added.

I believe that a good trading bot must consist of more than 4 different strategies, based on different systems. This is what I am currently working on.

My goal for publishing this strategy is to help other traders build their own. In my journey I found it difficult to find a good strategy that employs a decent risk management, which is truly essential for having good, consistent results. Also, a realistic commission needs to be defined to have a realistic performance prediction. This weighs on the profitability and therefore is often set at 0 by authors of other strategies, which I find misleading.

If you have found this strategy informative or useful, please leave a comment.

Greetings Michael

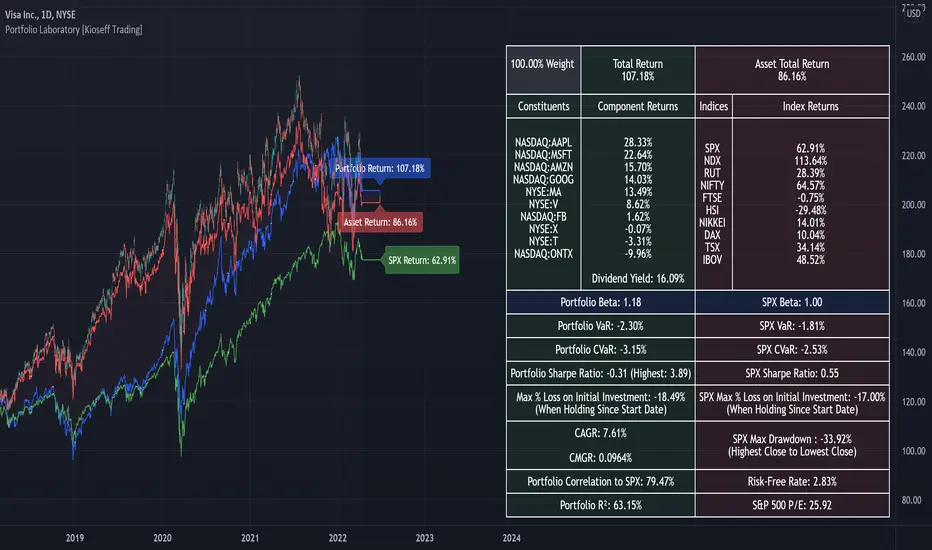

Portfolio Laboratory [Kioseff Trading]Hello!

This script looks to experiment with historical portfolio performance. However, a hypothetical cash balance is not used; weighted percentage increases and decreases are used.

You can select up to 10 assets to include in the portfolio. Long and short positions are possible.

Show in the image are the portfolio's weight, the total return of the portfolio and the total return of the asset on the chart over the selected timeframe.

Shown in the image above are the constituents of the portfolio, which can include any asset, the weighted percentage gain/loss of the constituents in addition to 10 major indices and their respective total percentage gain/loss over the timeframe.

Shown in the image above are the dividend yield % of the portfolio and relevant portfolio metrics - ex-post calculations are applied and are predicated on simple returns.

Shown in the image above is a portfolio of all short positions; portfolio calculations adjusted to the modifications.

Also shown is a change in the index the portfolio is calculated against. I have been asked a few times to include NIFTY 50 in my scripts - I made sure this was achieved, lol!

Show in the image is a performance line of performance of percentage increases/decreases for the index calculated against, the asset on the chart, and the portfolio.

All lines start simultaneously on the selected start date at the close price of the session for the asset on your chart.

However, the right-hand scale, whether displaying price or percent, cannot be used to assess the performance of each line - they are useful for visualization only and can extend below zero on a low-priced asset. Calculations will not execute correctly when selecting a start date prior to any asset in the portfolio's first trading session; calculations do not begin on the first bar of the asset on your chart.

I decided to code the script this way so statistics remain fixed when moving from asset to asset!

To compensate for this limitation, I included a label plot and background color change at the first session in which all assets in the portfolio had at least one bar of price data. You can adjust the calculation start date to the date portrayed on the label to test al possible price data!

The statistics table, and the performance lines, can be hidden in the user input section.

I plan on putting a bit more work into this script. I have some ideas on what to include; however, any input is greatly appreciated! If there's something you would like me to include please let me know.

@scheplick mentioned me in a script he recently coded:

My inspiration came from his script! I thank him for that!

Daily MovesShow percent daily moves with a 5 period look back. This helps visualize recent performance.

positionsize calculatorHow to use:

Use the cursor to select the time, entry, stop loss, and target position. Enter the trading fee to calculate the reward/risk ratio and the actual reward/risk ratio (including the commission) according to the price you selected.

Known error:

Settings of this script can't be saved as default might due to the interactive price selection function. If anyone knows how to fix it, please let me know.

feature:

The visual Risk/Reward box, have three price labels on the right hand of the box.

Calculate the actual reward/risk ratio based on the trading fee.

The visual Risk/Reward box will extend automatically.

Make Your Own Index!Intro

For my first script, I have released Make Your Own Index version 1. It has a long way to go so please stay tuned. Scroll down to read all the updates and notes as they come in.

Why it matters

Making your index is important to quickly see an index of symbols that you want to chart. Having the ability to assign weightings gives you the opportunity to make the index equal weighted or custom weighted. As we all know, indexes like the S&P 500 are NOT equal weighted, but more heavily weighted toward the winners. Now, you can make your own of a basket of symbols and make them custom weighted or equal weighted. Have some fun exploring this.

Features

You select the symbols of your choice and then chart them as one line with a specific weighting. This can be done in the settings menu once the indicator is selected. Use the symbol search field to add a symbol. From what I have tested, it works for any symbol whether it's stocks, crypto, FX and more. The default is set to stocks.

The Weight field in the settings menu is where you can assign a specific weight to the symbol of your choice. This way you can make an equal weighted index or a custom weighted index. By default each symbol is set to 10 or 10%. There are 10 symbols in the menu, so at 10%, they are equally weighted! In the script I have made it so each weighting is in percentage terms. So type in the percentage and you're good to go.

The chart is currently displayed in a separate window and not as an overlay. This may change in the future. The line can also be changed slightly and the color of it. Stay tuned for more on this.

Send in feedback

I am a Pine rookie in all regards and I am surely looking for support, feedback, and/or ideas. I want to add a lot more to this. If you look at the settings you will see have some input fields that are in their first iteration and currently needing to be improved. Rather than waiting to make them perfect, I just want to get this out there and update as I go. Also, as mentioned, I will definitely need a little support at adding more features that I have in mind.

Credit where credit is due

I used a lot of Open Source indicators as inspiration to quickly get going so thank you to the following people and accounts who share open source scripts that you can use to learn, test, and get started instantly:

@TradingView

@LucF

@PineCoders

@KioseffTrading

@norok

@RedKTrader

@NeoButane

And many others. That's the beauty of open source!

Closing note

Publishing it open source so people can fact check my code and thinking. One thing I know for sure is that this can probably be created in a more efficient way. Nonetheless, please a take look and let me know what you think - I am excited to make some updates over the coming weeks.

Thanks for reading!

Binance CHOP Dashboard by KziHere is a Dashboard to find the opportunuty of bigs moves with 20 pairs.

The Dashboard is too big for the phone view. I thinks we can use it only on computer view.

How it's work ?

I look for the CHOP on Weekly and Daily time frame

The CHOP give the "tension" of the pair.

So i look for the biggest "tension" to take the "big mooves"

I look for the align tension between weekly and daily

The CHOP can be 0 to 100 , the result is:

(Weeky CHOP x Daily CHOP) = 0 to 10 000

To make the result easy to read, i divide so that the "note" is between 0 and 10.

If you have more than 3 /10 = RED => HOT Opporunity for big mooves

If you have less than 1/10 = BLUE => COLD opporunity

Thanks for your comment,

Kzi

The code is well.

But i think there is an opportunity to do it better with some for loop.

Is some of you do it, please let's me know.

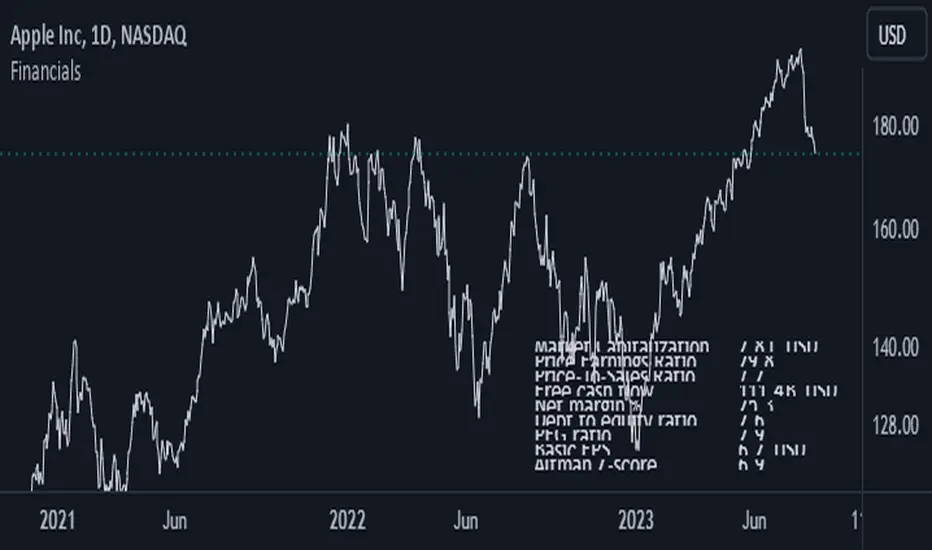

Key Financials A simple table with up to 9 key financials on your chart.

Simple, easy and configurable.

Trading the Equity Curve Position Sizing Example"Trading the equity curve" as a risk management method is the process of acting on trade signals depending on whether a system’s performance is indicating the strategy is in a profitable or losing phase.

The point of managing equity curve is to minimize risk in trading when the equity curve is in a downtrend. This strategy has two modes to determine the equity curve downtrend: By creating two simple moving averages of a portfolio's equity curve - a short-term and a longer-term one - and acting on their crossings. If the fast SMA is below the slow SMA, equity downtrend is detected (smafastequity < smaslowequity).

The second method is by using the crossings of equity itself with the longer-period SMA (equity < smasloweequity).

When Trading with the Equity Curve" is active, the position size will be reduced by a specified percentage if the equity is "under water" according to a selected rule. If you're a risk seeker, select "Increase size by %" - for some robust systems, it could help overcome their small drawdowns quicker.

Risk On Risk OffA helpful indicator for those who follow a systematic long-term investment approach.

What it shows:

It shows the 60 Day Cumulative Return of $BND Vanguard Total Bond Market ETF against the 60 Day Cumulative Return of $BIL SPDR Bloomberg Barclays 1-3 Month T-Bill ETF.

Why:

This Indicator will provide you a sense of where the economic environment is at, if the indicator shows that the 60 Day Cumulative return of $BND is ABOVE $BIL, it means that it's a good idea to go Risk ON in the stock market; On the other hand, if the inverse is true, it means that is a good idea to go Risk OFF in the stock market.

Example Uses:

Warren Buffet often advice Investors to just buy a S&P500 index tracking ETF like $SPY consistently and you will likely to be making money in the long-term.

With this indicator you will be able to make the Buffet Strategy even simpler: when the indicator shows Risk ON, buy the $SPY; when the indicator shows Risk OFF, consider hedges like $IEF iShares 7-10 Year Treasury Bond ETF. AMEX:SPY

Bond Yeild CurveBond Yeild Curve

A bond yeild curve is a line that plot the interest rate of bonds of each maturity dates.

The slope of the curve give the future of economy cycle.

if the slope could be normal (positive), flat or even inverted.

This indicator aquired data of bond yeild provided by TradingView.

How to use it.

Select the country of the bond / another country to compare.

Select the maturity of bond (this indicator set 2Y, 5Y, 10Y and 20Y as default).

You can toggle to 3 different data set; Yeild, Spread (10Y-2Y) and Yeild Curve.

In case that you select the "Yeild Curve", you can customize the desired past period to compare.

How we can get the benefit.

- If the current spread is greater than 1.0, it suppose that the economy of that country probably is ok.

- if the current spread is between 0 - 1.0, it suppose to be flatted and probably turn to invert and the economy cound be in a recession soon.

- if the current spread is below 0, it suppose to be inverted and economy is in recession.

when knowing the state of economy, it would help us to manage our investment.

When you select "Yeild"

When you select "Spread"

When you select "Yeild Curve"

I'm new for this.

if any idea, correction and suggestion, i do appreciate it.

LCDT Trade Entry ToolLCDT Trade Entry Tool

Enter the Offset for the X Axis for the Entry Tool.

Enter the Offset for the Y Axis for the Entry Tool.

Enter the Price for your Stop Loss in $.

Enter your desired Risk Amount in $.

Enter the max amount of of Capital per Trade in $.

There are toggle buttons in the setup to reveal/remove more data in the label that pops up, as well as a toggle to make the text larger.

Accumulation/Distribution Bands & Signals (BTC, 1D, BITSTAMP) This is an accumulation/distribution indicator for BTC/USD (D) based on variations of 1400D and 120D moving averages and logarithmic regression. Yellow plot signals Long Term Accumulation, which is based on 1400D (200W) ALMA, orange plot signals Mid Term Accumulation and is based on 120D ALMA, and finally the red plot signals Long Term Distribution that's based on log regression. It should be noted that for red plot to work BTC 1D BITSTAMP graph must be used, because the function of the logarithmic regression was modified according to the x axis of the BITSTAMP data.

Signal bands have different coefficients; long term accumulation (yellow) and and the log regression (red) plots have the highest coefficients and mid term accumulation (orange) has the lowest coefficients. Coefficients are 6x, 3x and 1.5x for the red (sell) and yellow (buy) plots and 1x, 2x and 3x for the orange (buy) plot. Selling coefficient for the yellow and the orange plots are respectively 2x and 1x. Buy and sell signals are summed up accordingly and plotted at the top of the highest band.

Acknowledgement: Credits for the logarithmic regression function are due @memotyka9009 and Benjamin Cowen

Overnight Gap AnalysisThere is a wide range of opinion on holding positions overnight due to gap risk. So, out of curiosity, I coded this analysis as a strategy to see what the result of only holding a position overnight on an asset would be. The results really surprised me. The script backtests 10+ years, and here are the findings:

Holding a position for 1 hour bar overnight on QQQ since January 2010 results in a 545% return. QQQ's entire return holding through the same period is 643%

The max equity drawdown on holding that position overnight is lower then the buy/hold drawdown on the underlying asset.

It doesn't matter if the last bar of the day is green or red, the results are similar.

It doesn't matter if it is a bull or bear market. Filtering the script to only trade when the price is above the 200-day moving average actually reduces its return from 545% to 301%, though it does also reduce drawdown.

I see similar patterns when applying the script to other index ETFs. Applying it to leveraged index ETFs can end up beating buy/hold of the underlying index.

Since this script holds through the 1st bar of the day, this could also speak to a day-opening price pattern

The default inputs are for the script to be applied to 1 hour charts only that have 7 bars on the chart per day. You can apply it to other chart types, but must follow the instructions below for it to work properly.

What the script is doing :

This script is buying the close of the last bar of the day and closing the trade at the close of the next bar. So, all trades are being held for 1 bar. By default, the script is setup for use on a 1hr chart that has 7 bars per day. If you try to apply it to a different timeframe, you will need to adjust the count of the last bar of the day with the script input. I.e. There are 7 bars per day on an hour chart on US Stocks/ETFs, so the input is set to 7 by default.

Other ways this script can be used :

This script can also test the result of holding a position over any 1 bar in the day using that same input. For instance, on an hour chart you can input 6 on the script input, and it will model buying the close of the 6th bar of the day while selling on the close of the next bar. I used this out of curiosity to model what only holding the last bar of the day would result in. On average, you lose money on the last bar every day.

The irony here is that the root cause of this last bar of the day losing may be people selling their positions at the end of day so that they aren't exposed to overnight gap risk.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Position & Lot Size CalculatorBuilt with love "Position & Lot Size Calculator"

This indiator will help you to calculate your position size for managing the risk

Features :

1. Click-able Price Entry & SL (Easier Interface)

How to use it :

1. After add the indicator, set the Entry & SL Price with click price line in the chart

2. Set the risk and another parameter

Regards,

Hanabil

Risk AssistAs the profit level increases, the amount of profit taking required to avoid risk asymptotically reaches zero.

This indicator displays the % of the established position required to exit in order to ensure the trade is not a loss if the stop is hit.

Values in green (at or below 100%) indicate a winning position.

Values in red (above 100%) indicate a losing position.

Alert Examples:

If you are intent on "selling half" to avoid risk, you can set an alert on the value of this indicator for 50.

If you are intent on "selling a 3rd" to avoid risk, you can set an alert on the value of this indicator for 33.3.

Money Management_V2 [javadmhs]Hi every one

you can use this indicator in your trades for money and risk management.

Very easy to use. Just enter the requested information of your trade and see the amount of money you need to enter into a transaction. Also you can see your pnl%.

Risk = The amount of money that if you lose, does not matter to you. This will be a percentage of your total capital.

Balance = your total capital.

Leverage = If you trade in future, you can use this. set it 1 in spot.

Commision = The amount of exchange fee.

Usable Cap = The amount of money you should enter into a transaction, depending on your risk.

PNL% = Amount of profit and loss.

You Can use this for Short and Long.

Let me know if you see a problem.

Leverage CalculatorThis script is intended to be used as a risk management calculator.

It will calculate the best leverage to use based on the maximum percentage of loss you are willing to incur on your trading portfolio.

Also calculates the order value and order qty based on your inputs.

Please note this calculator does not take into account any trading fees imposed by the exchange you are using.

*** Only risking 1% to 5% of your portfolio is considered good risk management ***

*** Not financial advice ***

------ Settings Inputs -----------------------------------------------------------------------------------------------------

"Portfolio Size" -- enter your portfolio balance

"% Willing to lose on this trade" -- enter the percent of your portfolio you are willing to lose if the stop loss is hit

"Entry Price" -- enter the price at which you will enter the trade

"Stop Loss Price" -- enter the price at which your stop loss will be set

----------------------------------------------------------------------------------------------------------------------------

------ Outputs -------------------------------------------------------------------------------------------------------------

"Portfolio" -- displays the portfolio balance entered in settings

"max loss on trade" -- displays the % loss entered in settings and the corresponding amount of your portfolio

"Entry Price" -- displays the entry price entered in settings

"Stop Loss Price" -- displays the stop loss price entered in settings

"Stop Loss %" -- displays the calculated percentage loss from the entry price

"Leverage calc" -- displays the calculated leverage based on your max loss and stop loss settings

"Order Value" -- displays the value of the order based on the calculated leverage

"Order Qty" -- displays the calculated order qty based on the calculated leverage

SHAD helperDisplays lines and labels for prices following the SHAD strategy.

SHAD strategy consists in selling half the position every time price doubles, thus this indicator displays values for x2, x4, x8 and x16 of current closing price.

You can also see "/2" (-50%) and "/4 " (-75%) values.

You can edit display colors and labels text size in the indicator's settings