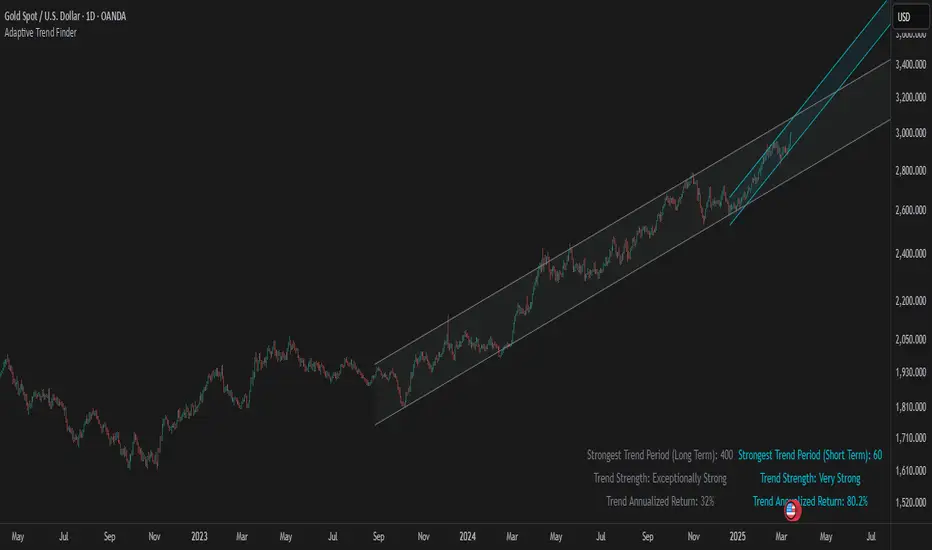

Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

Regression

Smoothed Gaussian Trend Filter [AlgoAlpha]Experience seamless trend detection and market analysis with the Smoothed Gaussian Trend Filter by AlgoAlpha! This cutting-edge indicator combines advanced Gaussian filtering with linear regression smoothing to identify and enhance market trends, making it an essential tool for traders seeking precise and actionable signals.

Key Features :

🔍 Gaussian Trend Filtering: Utilizes a customizable Gaussian filter with adjustable length and pole settings for tailored smoothing and trend identification.

📊 Linear Regression Smoothing: Reduces noise and further refines the Gaussian output with user-defined smoothing length and offset, ensuring clarity in trend representation.

✨ Dynamic Visual Highlights: Highlights trends and signals based on volume intensity, allowing for real-time insights into market behavior.

📉 Choppy Market Detection: Identifies ranging or choppy markets, helping traders avoid false signals.

🔔 Custom Alerts: Set alerts for bullish and bearish signals, trend reversals, or choppy market conditions to stay on top of trading opportunities.

🎨 Color-Coded Visuals: Fully customizable colors for bullish and bearish signals, ensuring clear and intuitive chart analysis.

How to Use :

Add the Indicator: Add it to your favorites and apply it to your TradingView chart.

Interpret the Chart: Observe the trend line for directional changes and use the accompanying buy/sell signals for entry and exit opportunities. Choppy market conditions are flagged for additional caution.

Set Alerts: Enable alerts for trend signals or choppy market detections to act promptly without constant chart monitoring.

How It Works :

The Smoothed Gaussian Trend Filter uses a combination of advanced smoothing techniques to identify trends and enhance market clarity. First, a Gaussian filter is applied to price data, using a user-defined length (Gaussian length) and poles (smoothness level) to calculate an alpha value that determines the degree of smoothing. This creates a refined trend line that minimizes noise while preserving key market movements. The output is then further processed using linear regression smoothing, allowing traders to adjust the length and offset to flatten minor oscillations and emphasize the dominant trend. To incorporate market activity, volume intensity is analyzed through a normalized Hull Moving Average (HMA), dynamically adjusting the trend line's color transparency based on trading activity. The indicator also identifies trend direction by comparing the smoothed trend line with a calculated SuperTrend-style level, generating clear trend regimes and highlighting ranging or choppy conditions where trends are less reliable and avoiding false signals. This seamless integration of Gaussian smoothing, regression analysis, and volume dynamics provides traders with a powerful and intuitive tool for market analysis.

LRI Momentum Cycles [AlgoAlpha]Discover the LRI Momentum Cycles indicator by AlgoAlpha, a cutting-edge tool designed to identify market momentum shifts using trend normalization and linear regression analysis. This advanced indicator helps traders detect bullish and bearish cycles with enhanced accuracy, making it ideal for swing traders and intraday enthusiasts alike.

Key Features :

🎨 Customizable Appearance : Set personalized colors for bullish and bearish trends to match your charting style.

🔧 Dynamic Trend Analysis : Tracks market momentum using a unique trend normalization algorithm.

📊 Linear Regression Insight : Calculates real-time trend direction using linear regression for better precision.

🔔 Alert Notifications : Receive alerts when the market switches from bearish to bullish or vice versa.

How to Use :

🛠 Add the Indicator : Favorite and apply the indicator to your TradingView chart. Adjust the lookback period, linear regression source, and regression length to fit your strategy.

📊 Market Analysis : Watch for color changes on the trend line. Green signals bullish momentum, while red indicates bearish cycles. Use these shifts to time entries and exits.

🔔 Set Alerts : Enable notifications for momentum shifts, ensuring you never miss critical market moves.

How It Works :

The LRI Momentum Cycles indicator calculates trend direction by applying linear regression on a user-defined price source over a specified period. It compares historical trend values, detecting bullish or bearish momentum through a dynamic scoring system. This score is normalized to ensure consistent readings, regardless of market conditions. The indicator visually represents trends using gradient-colored plots and fills to highlight changes in momentum. Alerts trigger when the momentum state changes, providing actionable trading signals.

Log Regression OscillatorThe Log Regression Oscillator transforms the logarithmic regression curves into an easy-to-interpret oscillator that displays potential cycle tops/bottoms.

🔶 USAGE

Calculating the logarithmic regression of long-term swings can help show future tops/bottoms. The relationship between previous swing points is calculated and projected further. The calculated levels are directly associated with swing points, which means every swing point will change the calculation. Importantly, all levels will be updated through all bars when a new swing is detected.

The "Log Regression Oscillator" transforms the calculated levels, where the top level is regarded as 100 and the bottom level as 0. The price values are displayed in between and calculated as a ratio between the top and bottom, resulting in a clear view of where the price is situated.

The main picture contains the Logarithmic Regression Alternative on the chart to compare with this published script.

Included are the levels 30 and 70. In the example of Bitcoin, previous cycles showed a similar pattern: the bullish parabolic was halfway when the oscillator passed the 30-level, and the top was very near when passing the 70-level.

🔹 Proactive

A "Proactive" option is included, which ensures immediate calculations of tentative unconfirmed swings.

Instead of waiting 300 bars for confirmation, the "Proactive" mode will display a gray-white dot (not confirmed swing) and add the unconfirmed Swing value to the calculation.

The above example shows that the "Calculated Values" of the potential future top and bottom are adjusted, including the provisional swing.

When the swing is confirmed, the calculations are again adjusted, showing a red dot (confirmed top swing) or a green dot (confirmed bottom swing).

🔹 Dashboard

When less than two swings are available (top/bottom), this will be shown in the dashboard.

The user can lower the "Threshold" value or switch to a lower timeframe.

🔹 Notes

Logarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time, meaning some symbols/tickers will fit better than others.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Users have to check the validity of swings; for example, if the direction of swings is downwards, then the dataset is not fitted for logarithmic regression.

In the example above, the "Threshold" is lowered. However, the calculated levels are unreliable due to the swings, which do not fit the model well.

Here, the combination of downward bottom swings and price accelerates slower at first and faster recently, resulting in a non-fit for the logarithmic regression model.

Note the price value (white line) is bound to a limit of 150 (upwards) and -150 (down)

In short, logarithmic regression is best used when there are enough tops/bottoms, and all tops are around 100, and all bottoms around 0.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 DETAILS

In mathematics, the dot product or scalar product is an algebraic operation that takes two equal-length sequences of numbers (arrays) and returns a single number, the sum of the products of the corresponding entries of the two sequences of numbers.

The usual way is to loop through both arrays and sum the products.

In this case, the two arrays are transformed into a matrix, wherein in one matrix, a single column is filled with the first array values, and in the second matrix, a single row is filled with the second array values.

After this, the function matrix.mult() returns a new matrix resulting from the product between the matrices m1 and m2.

Then, the matrix.eigenvalues() function transforms this matrix into an array, where the array.sum() function finally returns the sum of the array's elements, which is the dot product.

dot(x, y)=>

if x.size() > 1 and y.size() > 1

m1 = matrix.new()

m2 = matrix.new()

m1.add_col(m1.columns(), y)

m2.add_row(m2.rows (), x)

m1.mult (m2)

.eigenvalues()

.sum()

🔶 SETTINGS

Threshold: Period used for the swing detection, with higher values returning longer-term Swing Levels.

Proactive: Tentative Swings are included with this setting enabled.

Style: Color Settings

Dashboard: Toggle, "Location" and "Text Size"

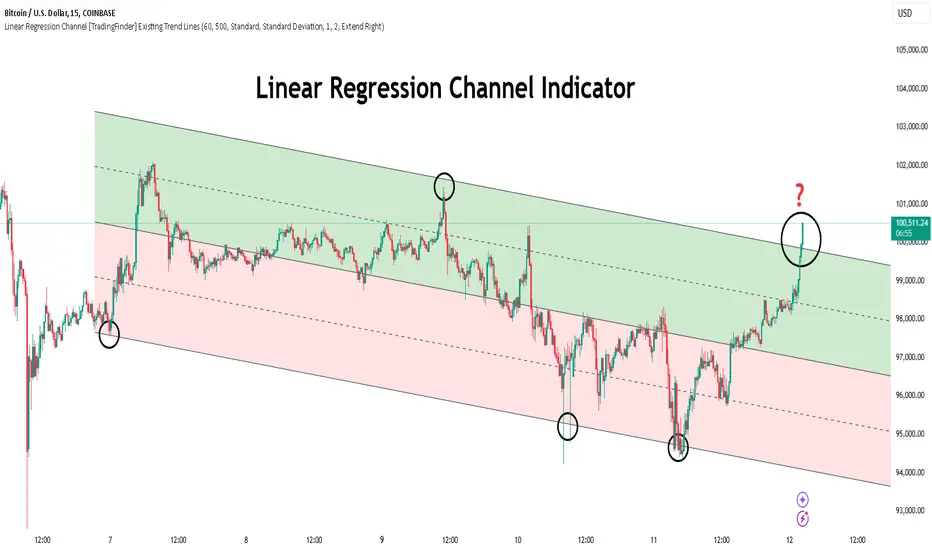

Linear Regression Channel [TradingFinder] Existing Trend Line🔵 Introduction

The Linear Regression Channel indicator is one of the technical analysis tool, widely used to identify support, resistance, and analyze upward and downward trends.

The Linear Regression Channel comprises five main components : the midline, representing the linear regression line, and the support and resistance lines, which are calculated based on the distance from the midline using either standard deviation or ATR.

This indicator leverages linear regression to forecast price changes based on historical data and encapsulates price movements within a price channel.

The upper and lower lines of the channel, which define resistance and support levels, assist traders in pinpointing entry and exit points, ultimately aiding better trading decisions.

When prices approach these channel lines, the likelihood of interaction with support or resistance levels increases, and breaking through these lines may signal a price reversal or continuation.

Due to its precision in identifying price trends, analyzing trend reversals, and determining key price levels, the Linear Regression Channel indicator is widely regarded as a reliable tool across financial markets such as Forex, stocks, and cryptocurrencies.

🔵 How to Use

🟣 Identifying Entry Signals

One of the primary uses of this indicator is recognizing buy signals. The lower channel line acts as a support level, and when the price nears this line, the likelihood of an upward reversal increases.

In an uptrend : When the price approaches the lower channel line and signs of upward reversal (e.g., reversal candlesticks or high trading volume) are observed, it is considered a buy signal.

In a downtrend : If the price breaks the lower channel line and subsequently re-enters the channel, it may signal a trend change, offering a buying opportunity.

🟣 Identifying Exit Signals

The Linear Regression Channel is also used to identify sell signals. The upper channel line generally acts as a resistance level, and when the price approaches this line, the likelihood of a price decrease increases.

In an uptrend : Approaching the upper channel line and observing weakness in the uptrend (e.g., declining volume or reversal patterns) indicates a sell signal.

In a downtrend : When the price reaches the upper channel line and reverses downward, this is considered a signal to exit trades.

🟣 Analyzing Channel Breakouts

The Linear Regression Channel allows traders to identify price breakouts as strong signals of potential trend changes.

Breaking the upper channel line : Indicates buyer strength and the likelihood of a continued uptrend, often accompanied by increased trading volume.

Breaking the lower channel line : Suggests seller dominance and the possibility of a continued downtrend, providing a strong sell signal.

🟣 Mean Reversion Analysis

A key concept in using the Linear Regression Channel is the tendency for prices to revert to the midline of the channel, which acts as a dynamic moving average, reflecting the price's equilibrium over time.

In uptrends : Significant deviations from the midline increase the likelihood of a price retracement toward the midline.

In downtrends : When prices deviate considerably from the midline, a return toward the midline can be used to identify potential reversal points.

🔵 Settings

🟣 Time Frame

The time frame setting enables users to view higher time frame data on a lower time frame chart. This feature is especially useful for traders employing multi-time frame analysis.

🟣 Regression Type

Standard : Utilizes classical linear regression to draw the midline and channel lines.

Advanced : Produces similar results to the standard method but may provide slightly different alignment on the chart.

🟣 Scaling Type

Standard Deviation : Suitable for markets with stable volatility.

ATR (Average True Range) : Ideal for markets with higher volatility.

🟣 Scaling Coefficients

Larger coefficients create broader channels for broader trend analysis.

Smaller coefficients produce tighter channels for precision analysis.

🟣 Channel Extension

None : No extension.

Left: Extends lines to the left to analyze historical trends.

Right : Extends lines to the right for future predictions.

Both : Extends lines in both directions.

🔵 Conclusion

The Linear Regression Channel indicator is a versatile and powerful tool in technical analysis, providing traders with support, resistance, and midline insights to better understand price behavior. Its advanced settings, including time frame selection, regression type, scaling options, and customizable coefficients, allow for tailored and precise analysis.

One of its standout advantages is its ability to support multi-time frame analysis, enabling traders to view higher time frame data within a lower time frame context. The option to use scaling methods like ATR or standard deviation further enhances its adaptability to markets with varying volatility.

Designed to identify entry and exit signals, analyze mean reversion, and assess channel breakouts, this indicator is suitable for a wide range of markets, including Forex, stocks, and cryptocurrencies. By incorporating this tool into your trading strategy, you can make more informed decisions and improve the accuracy of your market predictions.

Scatter PlotThe Price Volume Scatter Plot publication aims to provide intrabar detail as a Scatter Plot .

🔶 USAGE

A dot is drawn at every intrabar close price and its corresponding volume , as can seen in the following example:

Price is placed against the white y-axis, where volume is represented on the orange x-axis.

🔹 More detail

A Scatter Plot can be beneficial because it shows more detail compared with a Volume Profile (seen at the right of the Scatter Plot).

The Scatter Plot is accompanied by a "Line of Best Fit" (linear regression line) to help identify the underlying direction, which can be helpful in interpretation/evaluation.

It can be set as a screener by putting multiple layouts together.

🔹 Easier Interpretation

Instead of analysing the 1-minute chart together with volume, this can be visualised in the Scatter Plot, giving a straightforward and easy-to-interpret image of intrabar volume per price level.

One of the scatter plot's advantages is that volumes at the same price level are added to each other.

A dot on the scatter plot represents the cumulated amount of volume at that particular price level, regardless of whether the price closed one or more times at that price level.

Depending on the setting "Direction" , which sets the direction of the Volume-axis, users can hoover to see the corresponding price/volume.

🔹 Highest Intrabar Volume Values

Users can display up to 5 last maximum intrabar volume values, together with the intrabar timeframe (Res)

🔹 Practical Examples

When we divide the recent bar into three parts, the following can be noticed:

Price spends most of its time in the upper part, with relative medium-low volume, since the intrabar close prices are mostly situated in the upper left quadrant.

Price spends a shorter time in the middle part, with relative medium-low volume.

Price moved rarely below 61800 (the lowest part), but it was associated with high volume. None of the intrabar close prices reached the lowest area, and the price bounced back.

In the following example, the latest weekly candle shows a rejection of the 45.8 - 48.5K area, with the highest volume at the 45.8K level.

The next three successive candles show a declining maximum intrabar volume, after which the price broke through the 45.8K area.

🔹 Visual Options

There are many visual options available.

🔹 Change Direction

The Scatter Plot can be set in 4 different directions.

🔶 NOTES

🔹 Notes

The script uses the maximum available resources to draw the price/volume dots, which are 500 boxes and 500 labels. When the population size exceeds 1000, a warning is provided ( Not all data is shown ); otherwise, only the population size is displayed.

The Scatter Plot ideally needs a chart which contains at least 100 bars. When it contains less, a warning will be shown: bars < 100, not all data is shown

🔹 LTF Settings

When 'Auto' is enabled ( Settings , LTF ), the LTF will be the nearest possible x times smaller TF than the current TF. When 'Premium' is disabled, the minimum TF will always be 1 minute to ensure TradingView plans lower than Premium don't get an error.

Examples with current Daily TF (when Premium is enabled):

500 : 3 minute LTF

1500 (default): 1 minute LTF

5000: 30 seconds LTF (1 minute if Premium is disabled)

🔶 SETTINGS

Direction: Direction of Volume-axis; Left, Right, Up or Down

🔹 LTF

LTF: LTF setting

Auto + multiple: Adjusts the initial set LTF

Premium: Enable when your TradingView plan is Premium or higher

🔹 Character

Character: Style of Price/Volume dot

Fade: Increasing this number fades dots at lower price/volume

Color

🔹 Linear Regression

Toggle (enable/disable), color, linestyle

Center Cross: Toggle, color

🔹 Background Color

Fade: Increasing this number fades the background color near lower values

Volume: Background color that intensifies as the volume value on the volume-axis increases

Price: Background color that intensifies as the price value on the price-axis increases

🔹 Labels

Size: Size of price/volume labels

Volume: Color for volume labels/axis

Price: Color for price labels/axis

Display Population Size: Show the population size + warning if it exceeds 1000

🔹 Dashboard

Location: Location of dashboard

Size: Text size

Display LTF: Display the intrabar Lower Timeframe used

Highest IB volume: Display up to 5 previous highest Intrabar Volume values

Logarithmic Regression AlternativeLogarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time. Bitcoin is a good example.

𝑦 = 𝑎 + 𝑏 * ln(𝑥)

With this logarithmic regression (log reg) formula 𝑦 (price) is calculated with constants 𝑎 and 𝑏, where 𝑥 is the bar_index .

Instead of using the sum of log x/y values, together with the dot product of log x/y and the sum of the square of log x-values, to calculate a and b, I wanted to see if it was possible to calculate a and b differently.

In this script, the log reg is calculated with several different assumed a & b values, after which the log reg level is compared to each Swing. The log reg, where all swings on average are closest to the level, produces the final 𝑎 & 𝑏 values used to display the levels.

🔶 USAGE

The script shows the calculated logarithmic regression value from historical swings, provided there are enough swings, the price pattern fits the log reg model, and previous swings are close to the calculated Top/Bottom levels.

When the price approaches one of the calculated Top or Bottom levels, these levels could act as potential cycle Top or Bottom.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Swings are based on Weekly bars. A Top Swing, for example, with Swing setting 30, is the highest value in 60 weeks. Thirty bars at the left and right of the Swing will be lower than the Top Swing. This means that a confirmation is triggered 30 weeks after the Swing. The period will be automatically multiplied by 7 on the daily chart, where 30 becomes 210 bars.

Please note that the goal of this script is not to show swings rapidly; it is meant to show the potential next cycle's Top/Bottom levels.

🔹 Multiple Levels

The script includes the option to display 3 Top/Bottom levels, which uses different values for the swing calculations.

Top: 'high', 'maximum open/close' or 'close'

Bottom: 'low', 'minimum open/close' or 'close'

These levels can be adjusted up/down with a percentage.

Lastly, an "Average" is included for each set, which will only be visible when "AVG" is enabled, together with both Top and Bottom levels.

🔹 Notes

Users have to check the validity of swings; the above example only uses 1 Top Swing for its calculations, making the Top level unreliable.

Here, 1 of the Bottom Swings is pretty far from the bottom level, changing the swing settings can give a more reliable bottom level where all swings are close to that level.

Note the display was set at "Logarithmic", it can just as well be shown as "Regular"

In the example below, the price evolution does not fit the logarithmic regression model, where growth should accelerate rapidly at first and then slows over time.

Please note that this script can only be used on a daily timeframe or higher; using it at a lower timeframe will show a warning. Also, it doesn't work with bar-replay.

🔶 DETAILS

The code gathers data from historical swings. At the last bar, all swings are calculated with different a and b values. The a and b values which results in the smallest difference between all swings and Top/Bottom levels become the final a and b values.

The ranges of a and b are between -20.000 to +20.000, which means a and b will have the values -20.000, -19.999, -19.998, -19.997, -19.996, ... -> +20.000.

As you can imagine, the number of calculations is enormous. Therefore, the calculation is split into parts, first very roughly and then very fine.

The first calculations are done between -20 and +20 (-20, -19, -18, ...), resulting in, for example, 4.

The next set of calculations is performed only around the previous result, in this case between 3 (4-1) and 5 (4+1), resulting in, for example, 3.9. The next set goes even more in detail, for example, between 3.8 (3.9-0.1) and 4.0 (3.9 + 0.1), and so on.

1) -20 -> +20 , then loop with step 1 (result (example): 4 )

2) 4 - 1 -> 4 +1 , then loop with step 0.1 (result (example): 3.9 )

3) 3.9 - 0.1 -> 3.9 +0.1 , then loop with step 0.01 (result (example): 3.93 )

4) 3.93 - 0.01 -> 3.93 +0.01, then loop with step 0.001 (result (example): 3.928)

This ensures complicated calculations with less effort.

These calculations are done at the last bar, where the levels are displayed, which means you can see different results when a new swing is found.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 SETTINGS

Three sets

High/Low

• color setting

• Swing Length settings for 'High' & 'Low'

• % adjustment for 'High' & 'Low'

• AVG: shows average (when both 'High' and 'Low' are enabled)

Max/Min (maximum open/close, minimum open/close)

• color setting

• Swing Length settings for 'Max' & 'Min'

• % adjustment for 'Max' & 'Min'

• AVG: shows average (when both 'Max' and 'Min' are enabled)

Close H/Close L (close Top/Bottom level)

• color setting

• Swing Length settings for 'Close H' & 'Close L'

• % adjustment for 'Close H' & 'Close L'

• AVG: shows average (when both 'Close H' and 'Close L' are enabled)

Show Dashboard, including Top/Bottom levels of the desired source and calculated a and b values.

Show Swings + Dot size

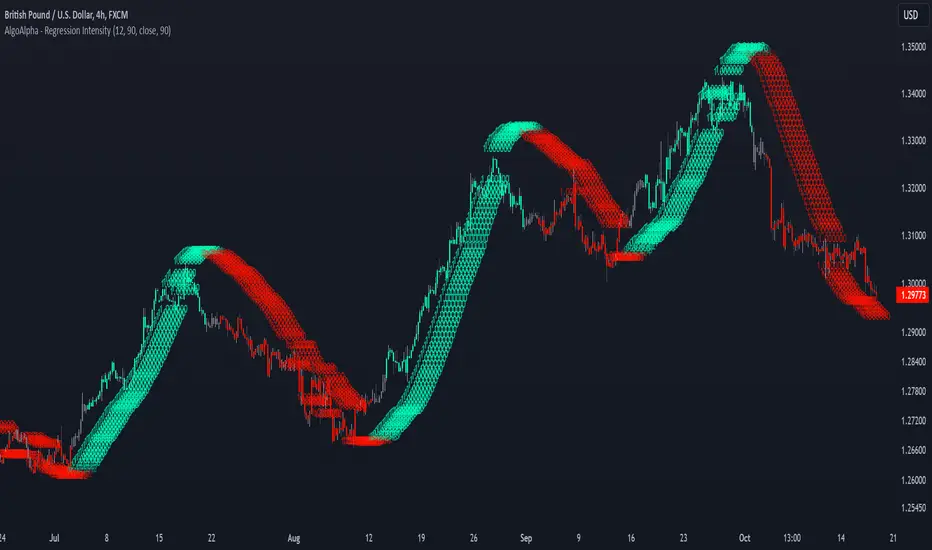

Linear Regression Intensity [AlgoAlpha]Introducing the Linear Regression Intensity indicator by AlgoAlpha, a sophisticated tool designed to measure and visualize the strength of market trends using linear regression analysis. This indicator not only identifies bullish and bearish trends with precision but also quantifies their intensity, providing traders with deeper insights into market dynamics. Whether you’re a novice trader seeking clearer trend signals or an experienced analyst looking for nuanced trend strength indicators, Linear Regression Intensity offers the clarity and detail you need to make informed trading decisions.

Key Features:

📊 Comprehensive Trend Analysis: Utilizes linear regression over customizable periods to assess and quantify trend strength.

🎨 Customizable Appearance: Choose your preferred colors for bullish and bearish trends to align with your trading style.

🔧 Flexible Parameters: Adjust the lookback period, range tolerance, and regression length to tailor the indicator to your specific strategy.

📉 Dynamic Bar Coloring: Instantly visualize trend states with color-coded bars—green for bullish, red for bearish, and gray for neutral.

🏷️ Intensity Labels: Displays dynamic labels that represent the intensity of the current trend, helping you gauge market momentum at a glance.

🔔 Alert Conditions: Set up alerts for strong bullish or bearish trends and trend neutrality to stay ahead of market movements without constant monitoring.

Quick Guide to Using Linear Regression Intensity:

🛠 Add the Indicator: Simply add Linear Regression Intensity to your TradingView chart from your favorites. Customize the settings such as lookback period, range tolerance, and regression length to fit your trading approach.

📈 Market Analysis: Observe the color-coded bars to quickly identify the current trend state. Use the intensity labels to understand the strength behind each trend, allowing for more strategic entry and exit points.

🔔 Set Up Alerts: Enable alerts for when strong bullish or bearish trends are detected or when the trend reaches a neutral zone. This ensures you never miss critical market movements, even when you’re away from the chart.

How It Works:

The Linear Regression Intensity indicator leverages linear regression to calculate the underlying trend of a selected price source over a specified length. By analyzing the consistency of the regression values within a defined lookback period, it determines the trend’s intensity based on a percentage tolerance. The indicator aggregates pairwise comparisons of regression values to assess whether the trend is predominantly upward or downward, assigning a state of bullish, bearish, or neutral accordingly. This state is then visually represented through dynamic bar colors and intensity labels, offering a clear and immediate understanding of market conditions. Additionally, the inclusion of Average True Range (ATR) ensures that the intensity visualization accounts for market volatility, providing a more robust and reliable trend assessment. With customizable settings and alert conditions, Linear Regression Intensity empowers traders to fine-tune their strategies and respond swiftly to evolving market trends.

Elevate your trading strategy with Linear Regression Intensity and gain unparalleled insights into market trends! 🌟📊

N-Degree Moment-Based Adaptive Detection🙏🏻 N-Degree Moment-Based Adaptive Detection (NDMBAD) method is a generalization of MBAD since the horizontal line fit passing through the data's mean can be simply treated as zero-degree polynomial regression. We can extend the MBAD logic to higher-degree polynomial regression.

I don't think I need to talk a lot about the thing there; the logic is really the same as in MBAD, just hit the link above and read if you want. The only difference is now we can gather cumulants not only from the horizontal mean fit (degree = 0) but also from higher-order polynomial regression fit, including linear regression (degree = 1).

Why?

Simply because residuals from the 0-degree model don't contain trend information, and while in some cases that's exactly what you need, in other cases, you want to model your trend explicitly. Imagine your underlying process trends in a steady manner, and you want to control the extreme deviations from the process's core. If you're going to use 0-degree, you'll be treating this beautiful steady trend as a residual itself, which "constantly deviates from the process mean." It doesn't make much sense.

How?

First, if you set the length to 0, you will end up with the function incrementally applied to all your data starting from bar_index 0. This can be called the expanding window mode. That's the functionality I include in all my scripts lately (where it makes sense). As I said in the MBAD description, choosing length is a matter of doing business & applied use of my work, but I think I'm open to talk about it.

I don't see much sense in using degree > 1 though (still in research on it). If you have dem curves, you can use Fourier transform -> spectral filtering / harmonic regression (regression with Fourier terms). The job of a degree > 0 is to model the direction in data, and degree 1 gets it done. In mean reversion strategies, it means that you don't wanna put 0-degree polynomial regression (i.e., the mean) on non-stationary trending data in moving window mode because, this way, your residuals will be contaminated with the trend component.

By the way, you can send thanks to @aaron294c , he said like mane MBAD is dope, and it's gonna really complement his work, so I decided to drop NDMBAD now, gonna be more useful since it covers more types of data.

I wanned to call it N-Order Moment Adaptive Detection because it abbreviates to NOMAD, which sounds cool and suits me well, because when I perform as a fire dancer, nomad style is one of my outfits. Burning Man stuff vibe, you know. But the problem is degree and order really mean two different things in the polynomial context, so gotta stay right & precise—that's the priority.

∞

Half Trend Regression [AlgoAlpha]Introducing the Half Trend Regression indicator by AlgoAlpha, a cutting-edge tool designed to provide traders with precise trend detection and reversal signals. This indicator uniquely combines linear regression analysis with ATR-based channel offsets to deliver a dynamic view of market trends. Ideal for traders looking to integrate statistical methods into their analysis to improve trade timing and decision-making.

Key Features

🎨 Customizable Appearance : Adjust colors for bullish (green) and bearish (red) trends to match your charting preferences.

🔧 Flexible Parameters : Configure amplitude, channel deviation, and linear regression length to tailor the indicator to different time frames and trading styles.

📈 Dynamic Trend Line : Utilizes linear regression of high, low, and close prices to calculate a trend line that adapts to market movements.

🚀 Trend Direction Signals : Provides clear visual signals for potential trend reversals with plotted arrows on the chart.

📊 Adaptive Channels : Incorporates ATR-based channel offsets to account for market volatility and highlight potential support and resistance zones.

🔔 Alerts : Set up alerts for bullish or bearish trend changes to stay informed of market shifts in real-time.

How to Use

🛠 Add the Indicator : Add the Half Trend Regression indicator to your chart from the TradingView library. Access the settings to customize parameters such as amplitude, channel deviation, and linear regression length to suit your trading strategy.

📊 Analyze the Trend : Observe the plotted trend line and the filled areas under it. A green fill indicates a bullish trend, while a red fill indicates a bearish trend.

🔔 Set Alerts : Use the built-in alert conditions to receive notifications when a trend reversal is detected, allowing you to react promptly to market changes.

How It Works

The Half Trend Regression indicator calculates linear regression lines for the high, low, and close prices over a specified period to determine the general direction of the market. It then computes moving averages and identifies the highest and lowest points within these regression lines to establish a dynamic trend line. The trend direction is determined by comparing the moving averages and previous price levels, updating as new data becomes available. To account for market volatility, the indicator calculates channels above and below the trend line, offset by a multiple of half the Average True Range (ATR). These channels help visualize potential support and resistance zones. The area under the trend line is filled with color corresponding to the current trend direction—green for bullish and red for bearish. When the trend direction changes, the indicator plots arrows on the chart to signal a potential reversal, and alerts can be set up to notify you. By integrating linear regression and ATR-based channels, the indicator provides a comprehensive view of market trends and potential reversal points, aiding traders in making informed decisions.

Enhance your trading strategy with the Half Trend Regression indicator by AlgoAlpha and gain a statistical edge in the markets! 🌟📊

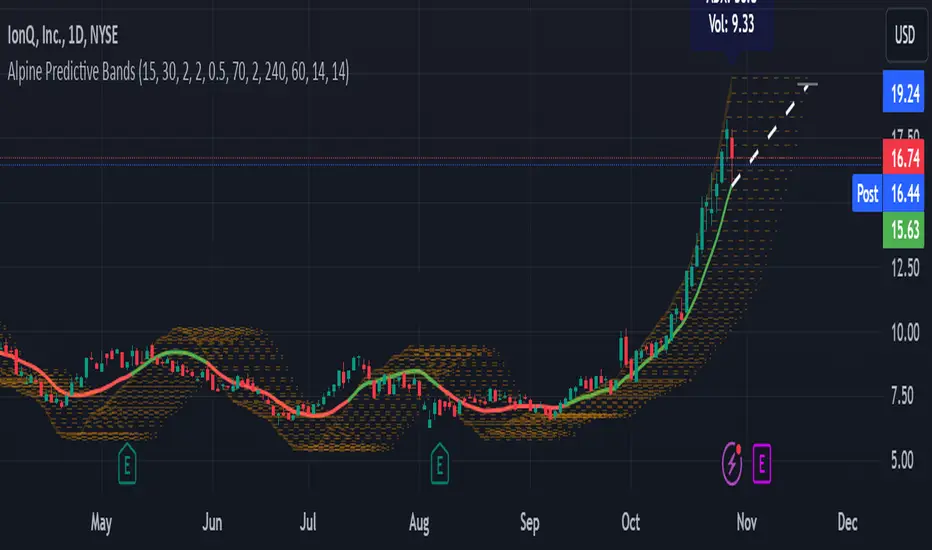

Alpine Predictive BandsAlpine Predictive Bands - ADX & Trend Projection is an advanced indicator crafted to estimate potential price zones and trend strength by integrating dynamic support/resistance bands, ADX-based confidence scoring, and linear regression-based price projections. Designed for adaptive trend analysis, this tool combines multi-timeframe ADX insights, volume metrics, and trend alignment for improved confidence in trend direction and reliability.

Key Calculations and Components:

Linear Regression for Price Projection:

Purpose: Provides a trend-based projection line to illustrate potential price direction.

Calculation: The Linear Regression Centerline (LRC) is calculated over a user-defined lookbackPeriod. The slope, representing the rate of price movement, is extended forward using predictionLength. This projected path only appears when the confidence score is 70% or higher, revealing a white dotted line to highlight high-confidence trends.

Adaptive Prediction Bands:

Purpose: ATR-based bands offer dynamic support/resistance zones by adjusting to volatility.

Calculation: Bands are calculated using the Average True Range (ATR) over the lookbackPeriod, multiplied by a volatilityMultiplier to adjust the width. These shaded bands expand during higher volatility, guiding traders in identifying flexible support/resistance zones.

Confidence Score (ADX, Volume, and Trend Alignment):

Purpose: Reflects the reliability of trend projections by combining ADX, volume status, and EMA alignment across multiple timeframes.

ADX Component: ADX values from the current timeframe and two higher timeframes assess trend strength on a broader scale. Strong ADX readings across timeframes boost the confidence score.

Volume Component: Volume strength is marked as “High” or “Low” based on a moving average, signaling trend participation.

Trend Alignment: EMA alignment across timeframes indicates “Bullish” or “Bearish” trends, confirming overall trend direction.

Calculation: ADX, volume, and trend alignment integrate to produce a confidence score from 0% to 100%. When the score exceeds 70%, the white projection line is activated, underscoring high-confidence trend continuations.

User Guide

Projection Line: The white dotted line, which appears only when the confidence score is 70% or higher, highlights a high-confidence trend.

Prediction Bands: Adaptive bands provide potential support/resistance zones, expanding with market volatility to help traders visualize price ranges.

Confidence Score: A high score indicates a stronger, more reliable trend and can support trend-following strategies.

Settings

Prediction Length: Determines the forward length of the projection.

Lookback Period: Sets the data range for calculating regression and ATR.

Volatility Multiplier: Adjusts the width of bands to match volatility levels.

Disclaimer: This indicator is for educational purposes and does not guarantee future price outcomes. Additional analysis is recommended, as trading carries inherent risks.

Volume-Supported Linear Regression Trend TableThe "Volume-Supported Linear Regression Trend Table" (VSLRT Table) script helps traders identify buy and sell opportunities by analyzing price trends and volume dynamics across multiple timeframes. It uses linear regression to calculate the trend direction and volume strength, visually representing this data with color-coded signals on the chart and in a table. Green signals indicate buying opportunities, while red signals suggest selling, with volume acting as confirmation of trend strength. Traders can use these signals for both short and long positions, with additional risk management and multi-timeframe validation to enhance the strategy.

------------------------------------------------------------------------------

To use the "Volume-Supported Linear Regression Trend Table" (VSLRT Table) script in a trading strategy, you would incorporate it into your decision-making process to identify potential buy and sell opportunities based on the trend and volume dynamics. Here’s how you could apply it for trading:

1. Understanding the Key Elements:

Trend Direction (Slope of Price): The script uses linear regression to assess the trend direction of the price. If the price slope is positive, the asset is likely in an uptrend; if it's negative, the asset is in a downtrend.

Volume-Backed Signals: The buy or sell signal is not only based on the price trend but also on volume. Volume is crucial in validating the strength of a trend; large volume often indicates strong interest in a direction.

2. Interpreting the Table and Signals:

The table displayed at the bottom-right of your TradingView chart gives you a clear overview of the trends across different timeframes:

Trend Colors:

Green hues (e.g., ccol11, ccol12, etc.): Indicate a buying trend supported by volume.

Red hues (e.g., ccol21, ccol22, etc.): Indicate a selling trend supported by volume.

Gray: Indicates weak or unclear trends where no decisive direction is present.

Buy/Sell Signals:

The script plots triangles on the chart:

Upward triangle below the bar signals a potential buy.

Downward triangle above the bar signals a potential sell.

3. Building a Trading Strategy:

Here’s how you can incorporate the script’s information into a trading strategy:

Buy Signal (Long Entry):

Look for green triangles (indicating a buy signal) below a bar.

Confirm that the trend color in the table for the relevant timeframe is green, which shows that the buy signal is supported by strong volume.

Ensure that the price is in an uptrend (positive slope) and that volume is increasing on upward moves, as this indicates buying interest.

Execute a long position when these conditions align.

Sell Signal (Short Entry):

Look for red triangles (indicating a sell signal) above a bar.

Confirm that the trend color in the table for the relevant timeframe is red, which shows that the sell signal is supported by strong volume.

Ensure that the price is in a downtrend (negative slope) and that volume is increasing on downward moves, indicating selling pressure.

Execute a short position when these conditions align.

Exiting the Trade:

Exit a long position when a sell signal (red triangle) appears, or when the trend color in the table shifts to red.

Exit a short position when a buy signal (green triangle) appears, or when the trend color in the table shifts to green.

4. Multi-Timeframe Confirmation:

The script provides trends across multiple timeframes (tf1, tf2, tf3), which can help in validating your trade:

Short-Term Trading: Use shorter timeframes (e.g., 3, 5 minutes) for intraday trades. If both short and medium timeframes align in trend direction (e.g., both showing green), it strengthens the signal.

Longer-Term Trading: If you are trading on a higher timeframe (e.g., daily or weekly), confirm that the lower timeframes align with your intended trade direction.

5. Adding Risk Management:

Stop-Loss: Place stop-losses below recent lows (for long trades) or above recent highs (for short trades) to minimize risk.

Take Profit: Consider taking profit at key support/resistance levels or based on a fixed risk-to-reward ratio (e.g., 2:1).

Example Strategy Flow:

For Long (Buy) Trade:

Signal: A green triangle appears below a candle (Buy signal).

Trend Confirmation: Check that the color in the table for your selected timeframe is green, confirming the trend is supported by volume.

Execute Long: Enter a long trade if the price is trending upward (positive price slope).

Exit Long: Exit when a red triangle appears above a candle (Sell signal) or if the trend color shifts to red in the table.

For Short (Sell) Trade:

Signal: A red triangle appears above a candle (Sell signal).

Trend Confirmation: Check that the color in the table for your selected timeframe is red, confirming the trend is supported by volume.

Execute Short: Enter a short trade if the price is trending downward (negative price slope).

Exit Short: Exit when a green triangle appears below a candle (Buy signal) or if the trend color shifts to green in the table.

6. Fine-Tuning:

Backtesting: Before trading live, use TradingView’s backtesting features to test the strategy on historical data and optimize the settings (e.g., length of linear regression, timeframe).

Combine with Other Indicators: Use this strategy alongside other technical indicators (e.g., RSI, MACD) for better confirmation.

In summary, the script helps identify trends with volume support, giving more confidence in buy/sell decisions. Combining these signals with risk management and multi-timeframe analysis can create a solid trading strategy.

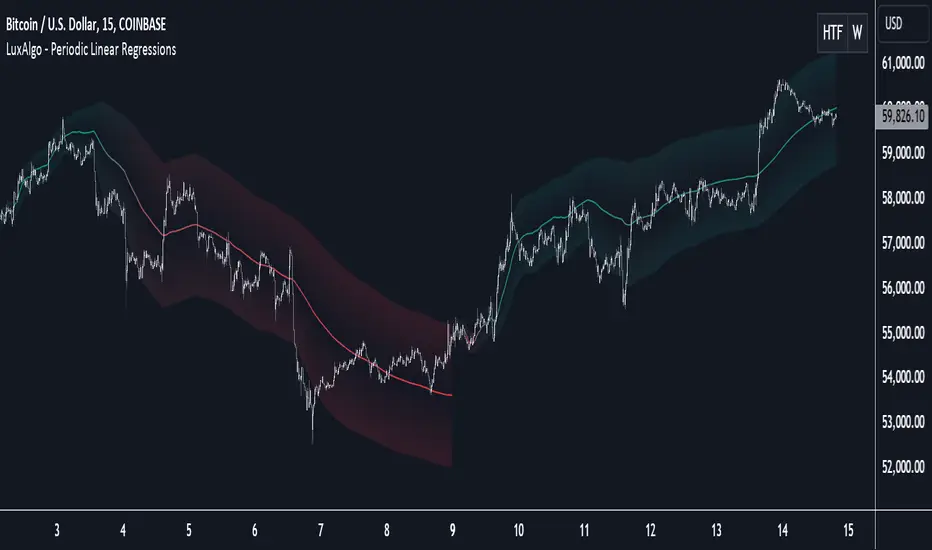

Periodic Linear Regressions [LuxAlgo]The Periodic Linear Regressions (PLR) indicator calculates linear regressions periodically (similar to the VWAP indicator) based on a user-set period (anchor).

This allows for estimating underlying trends in the price, as well as providing potential supports/resistances.

🔶 USAGE

The Periodic Linear Regressions indicator calculates a linear regression over a user-selected interval determined from the selected "Anchor Period".

The PLR can be visualized as a regular linear regression (Static), with a fit readjusting for new data points until the end of the selected period, or as a moving average (Rolling), with new values obtained from the last point of a linear regression fitted over the calculation interval. While the static method line is prone to repainting, it has value since it can further emphasize the linearity of an underlying trend, as well as suggest future trend directions by extrapolating the fit.

Extremities are included in the indicator, these are obtained from the root mean squared error (RMSE) between the price and calculated linear regression. The Multiple setting allows the users to control how far each extremity is from the other.

Periodic Linear Regressions can be helpful in finding support/resistance areas or even opportunities when ranging in a channel.

The anchor - where a new period starts - can be shown (in this case in the top right corner).

The shown bands can be visualized by enabling Show Extremities in settings ( Rolling or Static method).

The script includes a background gradient color option for the bands, which only applies when using the Rolling method.

The indicator colors can be suggestive of the detected trend and are determined as follows:

Method Rolling: a gradient color between red and green indicates the trend; more green if the output is rising, suggesting an uptrend, and more red if it is decreasing, suggesting a downtrend.

Method Static: green if the slope of the line is positive, suggesting an uptrend, red if negative, suggesting a downtrend.

🔶 DETAILS

🔹 Anchor Type

When the Anchor Type is set to Periodic , the indicator will be reset when the "Anchor Period" changes, after which calculations will start again.

An anchored rolling line set at First Bar won't reset at a new session; it will continue calculating the linear regression from the first bar to the last; in other words, every bar is included in the calculation. This can be useful to detect potential long-term tops/bottoms.

Note that a linear regression needs at least two values for its calculation, which explains why you won't see a static line at the first bar of the session. The rolling linear regression will only show from the 3rd bar of the session since it also needs a previous value.

🔹 Rolling/Static

When Anchor Type is set at Periodic , a linear regression is calculated between the first bar of the chosen session and the current bar, aiming to find the line that best fits the dataset.

The example above shows the lines drawn during the session. The offered script, though, shows the last calculated point connected to the previous point when the Rolling method is chosen, while the Static method shows the latest line.

Note that linear regression needs at least two values, which explains why you won't see a static line at the first bar of the session. The rolling line will only show from the 3rd bar of the session since it also needs a previous value.

🔶 SETTINGS

Method: Indicator method used, with options: "Static" (straight line) / "Rolling" (rolling linear regression).

Anchor Type: "Periodic / First Bar" (the latter works only when "Method" is set to "Rolling").

Anchor Period: Only applicable when "Anchor Type" is set at "Periodic".

Source: open, high, low, close, ...

Multiple: Alters the width of the bands when "Show Extremities" is enabled.

Show Extremities: Display one upper and one lower extremity.

🔹 Color Settings

Mono Color: color when "Bicolor" is disabled

Bicolor: Toggle on/off + Colors

Gradient: Background color when "Show extremities" is enabled + level of gradient

🔹 Dashboard

Show Dashboard

Location of dashboard

Text size

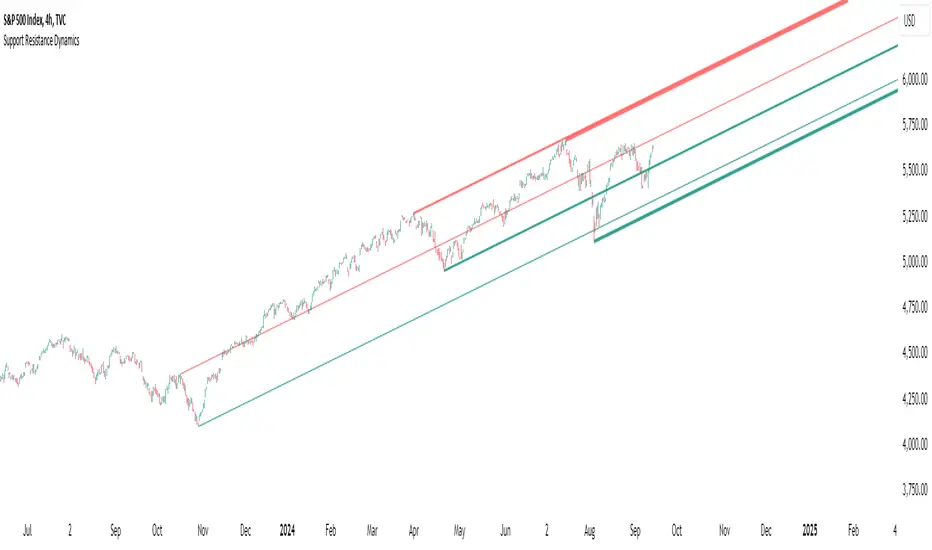

Support Resistance DynamicsThe Support Resistance Dynamics indicator is an advanced technical analysis tool designed to identify and visualize key support and resistance levels in real-time. This innovative indicator stands out from traditional support and resistance tools by employing a dynamic approach that adapts to market conditions.

Key Features:

Dynamic Level Calculation: Unlike static support and resistance indicators, this tool continuously updates levels based on recent price action, providing traders with the most relevant and up-to-date information.

Logarithmic Scale Option: The indicator offers a unique logarithmic scale feature, essential for analyzing long-term trends or assets with significant price changes. This allows for more accurate level plotting across various timeframes and price ranges.

Customizable Display: Users can adjust the number of support and resistance lines displayed, allowing for a clean and uncluttered chart view while focusing on the most significant levels.

Adaptive Slope Calculation: The indicator uses an innovative approach to calculate the slope of support and resistance lines, offering options from dynamic adaptation to fixed long-term periods. This ensures the lines remain relevant in both trending and ranging markets.

Enhanced Visualization: With customizable line colors, styles, and transparency, traders can easily distinguish between support and resistance levels, improving chart readability and analysis.

Flexible Period Settings: From dynamic calculations based on recent pivots to fixed long-term periods, the indicator adapts to various trading styles and timeframes.

The Support Resistance Dynamics indicator is particularly useful for:

Identifying potential reversal points in trends

Setting more accurate entry and exit points for trades

Placing stop-loss orders with greater precision

Recognizing breakout levels for potential new trends

By combining dynamic calculation methods with customizable visual elements, this indicator provides traders with a powerful tool for market analysis. Whether you're a day trader looking for short-term opportunities or a long-term investor analyzing macro trends, the Support Resistance Dynamics indicator offers valuable insights to enhance your trading strategy.

This indicator is provided for informational and educational purposes only. It should not be considered as financial advice or a recommendation to buy or sell any financial instrument. Past performance is not indicative of future results. Trading involves significant risk of loss. Users should conduct their own research and due diligence before making any investment decisions. The creator of this indicator is not responsible for any losses incurred from its use. Always test thoroughly on demo accounts before applying to live trading.

Multi Adaptive Moving Average (MAMA)The Multi Adaptive Moving Average (MAMA) indicator is an advanced tool for technical analysis, designed to provide traders with a detailed understanding of market trends and potential future price movements. This indicator utilizes multiple Simple Moving Averages (SMAs) and forecasting techniques to enhance decision-making processes.

Simple Moving Averages (SMAs):

Short MA (20-period): This moving average is highly responsive to price changes, making it ideal for capturing short-term trends. It helps traders identify quick market shifts and potential entry or exit points.

Mid MA (50-period): This average strikes a balance between short- and long-term trends, offering insights into the market's intermediate direction. It aids in confirming the sustainability of short-term trends.

Long MA (100-period): By smoothing out price data over a longer period, this moving average is useful for identifying long-term trends and filtering out short-term volatility.

Very Long MA (200-period): Often considered a critical indicator for determining the overall market trend, this average helps confirm the direction and strength of long-term movements.

Forecasting:

Flat Forecast: This approach assumes that prices will remain constant in the near future, which is particularly useful in markets trading sideways without a clear trend direction.

Linear Regression Forecast: This method uses historical data to project future price movements, offering a dynamic forecast based on existing trends. It helps traders anticipate potential price changes and plan their strategies accordingly.

Advantages:

Comprehensive Trend Analysis: By incorporating four different SMAs, the indicator provides a layered view of market trends across various timeframes. This enables traders to identify potential trend reversals and continuations with greater accuracy.

Predictive Insights: The forecasting feature offers traders a forward-looking perspective, enabling them to anticipate market movements and adjust their trading strategies proactively. This can be especially advantageous in volatile markets.

Customization: The MAMA indicator is highly customizable, allowing traders to adjust parameters such as the source of price data and the inclusion of the current unclosed candle. This flexibility ensures that the indicator can be tailored to fit different trading styles and market conditions.

Visual Clarity: The use of distinct colors for each SMA and their forecasts enhances visual interpretation, making it easier for traders to quickly assess market conditions and make informed decisions. The inclusion of a legend further aids in distinguishing between the different moving averages and their respective forecasts.

How to Use:

Trend Confirmation: Use the alignment of the SMAs to confirm market trends. For example, when the Short MA crosses above the Mid and Long MAs, it may indicate a bullish trend, while the opposite could suggest a bearish trend.

Entry and Exit Points: Look for crossovers between the SMAs as potential signals for entering or exiting trades. The forecasts can help in timing these decisions by providing an expectation of future price movements.

Risk Management: Utilize the Very Long MA to set stop-loss and take-profit levels, as it reflects the long-term trend and can help in avoiding trades against the prevailing market direction.

The MAMA indicator is intended to support technical analysis and should not be used as the sole basis for making trading decisions. Financial markets are inherently uncertain, and past performance does not guarantee future results. Traders should use this tool in conjunction with other analytical methods and consider their risk tolerance and investment objectives. It is advisable to conduct thorough research and consult with a financial advisor before making significant trading decisions. Always be aware of the risks involved in trading and invest only what you can afford to lose.

Viking Fun PredictОсобая благодарность за оригинальную идею Александру Горчакову

Индикатор предсказывает вырастет или упадет цена на следующей свече

Индикатор отображает красные или зеленые кружки над каждой из свечей

Зеленый кружок прогноз роста

Красный кружок прогноз падения

Индикатор выдает прогноз для шестой свечи на основе пяти свечей

Индикатор берет цены максимумов и минимумов пяти свечей и усредняет их, получая 5 значений. На основе полученных 5 значений строится линейная регрессия

Если линия линейной регрессии возрастает, то индикатор прогнозирует рост (зеленый кружок)

Если линия линейной регрессии возрастает, то индикатор прогнозирует падение (красный кружок)

Компания Викинг предоставляет профессиональный сервис, позволяющий реализовать арбитражные стратегии и маркет-мейкинг, осуществляет обучение трейдеров-арбитражеров.

---------------------------

Special thanks for the original idea to Alexander Gorchakov

The indicator predicts whether the price will rise or fall on the next candle

The indicator displays red or green circles above each of the candles

Green circle growth forecast

Red circle forecast of the fall

The indicator gives a forecast for the sixth candle based on five candles

The indicator takes the prices of the highs and lows of five candles and averages them, getting 5 values. Based on the obtained 5 values, a linear regression is constructed

If the linear regression line increases, the indicator predicts growth (green circle)

If the linear regression line increases, the indicator predicts a fall (red circle)

Viking provides a professional service that allows you to implement arbitrage strategies and market making, and provides training for arbitrage traders.

Machine Learning Signal FilterIntroducing the "Machine Learning Signal Filter," an innovative trading indicator designed to leverage the power of machine learning to enhance trading strategies. This tool combines advanced data processing capabilities with user-friendly customization options, offering traders a sophisticated yet accessible means to optimize their market analysis and decision-making processes. Importantly, this indicator does not repaint, ensuring that signals remain consistent and reliable after they are generated.

Machine Learning Integration

The "Machine Learning Signal Filter" employs machine learning algorithms to analyze historical price data and identify patterns that may not be immediately apparent through traditional technical analysis. By utilizing techniques such as regression analysis and neural networks, the indicator continuously learns from new data, refining its predictive capabilities over time. This dynamic adaptability allows the indicator to adjust to changing market conditions, potentially improving the accuracy of trading signals.

Key Features and Benefits

Dynamic Signal Generation: The indicator uses machine learning to generate buy and sell signals based on complex data patterns. This approach enables it to adapt to evolving market trends, offering traders timely and relevant insights. Crucially, the indicator does not repaint, providing reliable signals that traders can trust.

Customizable Parameters: Users can fine-tune the indicator to suit their specific trading styles by adjusting settings such as the temporal synchronization and neural pulse rate. This flexibility ensures that the indicator can be tailored to different market environments.

Visual Clarity and Usability: The indicator provides clear visual cues on the chart, including color-coded signals and optional display of signal curves. Users can also customize the table's position and text size, enhancing readability and ease of use.

Comprehensive Performance Metrics: The indicator includes a detailed metrics table that displays key performance indicators such as return rates, trade counts, and win/loss ratios. This feature helps traders assess the effectiveness of their strategies and make data-driven decisions.

How It Works

The core of the "Machine Learning Signal Filter" is its ability to process and learn from large datasets. By applying machine learning models, the indicator identifies potential trading opportunities based on historical data patterns. It uses regression techniques to predict future price movements and neural networks to enhance pattern recognition. As new data is introduced, the indicator refines its algorithms, improving its accuracy and reliability over time.

Use Cases

Trend Following: Ideal for traders seeking to capitalize on market trends, the indicator helps identify the direction and strength of price movements.

Scalping: With its ability to provide quick signals, the indicator is suitable for scalpers aiming for rapid profits in volatile markets.

Risk Management: By offering insights into trade performance, the indicator aids in managing risk and optimizing trade setups.

In summary, the "Machine Learning Signal Filter" is a powerful tool that combines the analytical strength of machine learning with the practical needs of traders. Its ability to adapt and provide actionable insights makes it an invaluable asset for navigating the complexities of financial markets.

The "Machine Learning Signal Filter" is a tool designed to assist traders by providing insights based on historical data and machine learning techniques. It does not guarantee profitable trades and should be used as part of a comprehensive trading strategy. Users are encouraged to conduct their own research and consider their financial situation before making trading decisions. Trading involves significant risk, and it is possible to lose more than the initial investment. Always trade responsibly and be aware of the risks involved.

FVG Price & Volume Graph [LuxAlgo]The FVG Price & Volume Graph tool plot recently detected fair value gaps relative to the volume traded within their area during their formation. This allows us to effectively visualize significant fair value gaps caused by high liquidity.

The indicator also returns levels from the fair value gaps areas average with the highest associated volume.

Do note that the indicator can consider the chart's visible range when being computed, which will recalculate the indicator when the chart's visible range changes.

🔶 USAGE

Fair Value Gaps (FVG) are core price action concepts occurring when the disparity between supply and demand is significant. Price has a tendency to come back to those areas and mitigating them, that is filling them.

The provided tools allow for effective visualization of both FVG's area's height as well as the volume originating from their creation, which is defined by the total traded volume located within the FVG during its creation. FVG's with more associated volume are displayed to the rightmost of the chart.

Users can determine the amount of most recent FVG's to display from the "Display Amount" setting. Disabling the "Consider Mitigation" setting will return mitigated FVGs in the plot, which can be useful to know where most FVGs were located.

We can use the area average of the FVGs with the most associated volume as potential support/resistance levels. Users can extend more FVG's averages by increasing the "Highest Volume Averages" setting.

🔹 Visualizing Volume/Price Relationships of FVG's

A linear regression is fit between FVG's areas average and their associated volume, with this linear regression helping us see where FVG's with specific volume might be located in the future based on existing FVG's.

Note that FVG's do not tend to exhibit linear relationships with their associated volume, the provided linear regression can give a general sense of tendency, but nothing necessarily accurate.

🔶 DETAILS

🔹 Intrabar Data TF

Given a formation of three candles causing an FVG, the volume traded within that FVG area is obtained by looking at the lower timeframe intrabar candles located within the intermediary candle of the formation. The volume of the intrabar candles located within the FVG areas is added up to obtain the associated volume of the FVG.

Using a lower "Intrabar Data TF" allows obtaining more precise volume results, at the cost of computation time and data availability (if there is a high difference between the "Intrabar Data TF" and the chart TF then less FVG can have their associated volume calculated due to Tradingview limitations).

🔹 Display

Users have access to multiple graphical settings affecting how the indicator is displayed.

The "Graph Resolution" setting determines the length of the X axis, with higher values returning more precise results on the location of FVGs over the X axis. Users can also control the number of labels displayed on the X-axis using the numerical input to the right of "Show X-Axis Labels".

Additionally, users can color FVG areas using a gradient relative to the size of the area, or the volume associated with the FVG.

🔶 SETTINGS

Display Amount: Amount of most recent FVGs to display.

Highest Volume Averages: Amount of FVG averages levels with the highest volume to display and extend.

Consider Mitigation: Only display unmitigated FVGs.

Filter FVGs Outside Visible Range: Only display FVGs areas that are located within the user chart visible range.

Intrabar Data TF: Timeframe used to obtain intrabar data. Should be lower than the user chart timeframe.

Composite Z-Score with Linear Regression Bands [UAlgo]The Composite Z-Score with Linear Regression Bands is a technical indicator designed to provide traders with a comprehensive analysis of price momentum, volatility, and volume. By combining multiple moving averages with slope analysis, volume/volatility compression-expansion metrics, and Z-Score calculations, this indicator aims to highlight potential breakout and breakdown points with high accuracy. The inclusion of linear regression bands further enhances the analysis by providing dynamic support and resistance levels, which adapt to market conditions. This makes the indicator particularly useful in identifying overbought/oversold conditions, volume squeezes, and the overall direction of the trend.

🔶 Key Features

Multi-Length Slope Calculation: The indicator uses multiple Hull Moving Averages (HMA) across various lengths to calculate slope angles, which are then converted into Z-Scores. This helps in capturing both short-term and long-term price momentum.

Volume/Volatility Composite Analysis: By calculating a composite value derived from both volume and volatility, the indicator identifies periods of compression (squeezes) and expansion, which are crucial for detecting potential breakout opportunities.

Linear Regression Bands: The inclusion of dynamic linear regression bands provides traders with adaptive support and resistance levels. These bands are enhanced by the composite value, which adjusts the band width based on market conditions, offering a clearer view of possible price reversals.

Overbought/Oversold Detection: The indicator highlights overbought and oversold conditions by comparing Z-Scores against the upper and lower bounds of the regression bands, which can signal potential reversal points.

Customizable Inputs: Users can customize key parameters such as the lengths of the moving averages, the regression band period, and the number of deviations used for the bands, allowing for flexibility in adapting the indicator to different market environments.

🔶 Interpreting the Indicator

Z-Score Plots: The individual Z-Score plots represent the normalized slope of the Hull Moving Averages over different periods. Positive values indicate upward momentum, while negative values suggest downward momentum. The combined Z-Sum provides a broader view of the overall market momentum.

Composite Value: The composite value is a ratio of volume to volatility, which highlights periods of market compression and expansion. When the composite value rises, it suggests increasing market activity, often preceding a breakout.

Why are we calculating values for multiple lengths?

The Composite Z-Score with Linear Regression Bands indicator employs a multi-timeframe analysis by calculating Z-scores for various moving average lengths. This approach provides a more comprehensive view of market dynamics and helps to identify trends and potential reversals across different timeframes. By considering multiple lengths, we can:

Capture a broader range of market behaviors: Different moving average lengths capture different aspects of price movement. Shorter lengths are more sensitive to recent price changes, while longer lengths provide a smoother representation of the underlying trend.

Reduce the impact of noise: By combining Z-scores from multiple lengths, we can help to filter out some of the noise that can be present in shorter-term data and obtain a more robust signal.

Enhance the reliability of signals: When Z-scores from multiple lengths align, it can increase the confidence in the identified trend or potential reversal. This can help to reduce the likelihood of false signals.

In essence, calculating values for multiple lengths allows the indicator to provide a more nuanced and reliable assessment of market conditions, making it a valuable tool for traders and analysts.

Linear Regression Bands: The central line represents the linear regression of the Z-Sum, while the upper and lower bands represent the dynamic resistance and support levels, respectively. The deviation from the regression line indicates the strength of the current trend. When price moves beyond these bands, it may signal an overbought (above upper band) or oversold (below lower band) condition.

Volume/Volatility Squeeze: When the price moves between the regression bands and the volume/volatility-adjusted bands, the market is in a squeeze. Breakouts from this squeeze can lead to significant price moves, which are indicated by the filling of areas between the Z-Score plots and the bands.

Color Interpretation: The indicator uses color changes to make it easier to interpret the data. Teal colors generally indicate upward momentum or strong conditions, while red suggests downward momentum or weakening conditions. The intensity of the color reflects the strength of the signal.

Overbought/Oversold Signals: The indicator marks potential overbought and oversold conditions when Z-Scores cross above or below the upper and lower regression bands, respectively. These signals are crucial for identifying potential reversal points in the market.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Regression Indicator [BigBeluga]Regression Indicator

Indicator Overview:

The Regression Indicator is designed to help traders identify trends and potential reversals in price movements. By calculating a regression line and a normalized regression indicator, it provides clear visual signals for market direction, aiding in making informed trading decisions. The indicator dynamically updates with the latest market data, ensuring timely and relevant signals.

Key Features:

⦾ Calculations

Regression Indicator: Calculates the linear regression coefficients (slope and intercept) and derives the normalized distance close from the regression line.

// @function regression_indicator is a Normalized Ratio of Regression Lines with close

regression_indicator(src, length) =>

sum_x = 0.0

sum_y = 0.0

sum_xy = 0.0

sum_x_sq = 0.0

distance = 0.0

// Calculate Sum

for i = 0 to length - 1 by 1

sum_x += i + 1

sum_y += src

sum_xy += (i + 1) * src

sum_x_sq += math.pow(i + 1, 2)

// Calculate linear regression coefficients

slope = (length * sum_xy - sum_x * sum_y)

/ (length * sum_x_sq - math.pow(sum_x, 2))

intercept = (sum_y - slope * sum_x) / length

// Calculate Regression Indicator

y1 = intercept + slope

distance := (close - y1)

distance_n = ta.sma((distance - ta.sma(distance, length1))

/ ta.stdev(distance, length1), 10)

⦿ Reversion Signals:

Marks potential trend reversal points.

⦿ Trend Identification:

Highlights when the regression indicator crosses above or below the zero line, signaling potential trend changes.

⦿ Color-Coded Candles:

Changes candle colors based on the regression indicator's value.

⦿ Arrow Markers:

Indicate trend directions on the chart.

⦿ User Inputs

Regression Length: Defines the period for calculating the regression line.

Normalization Length: Period used to normalize the regression indicator.

Signal Line: Length for averaging the regression indicator to generate signals.

Main Color: Color used for plotting the regression line and signals.

The Regression Indicator is a powerful tool for analyzing market trends and identifying potential reversal points. With customizable inputs and clear visual aids, it enhances the trader's ability to make data-driven decisions. The dynamic nature of the indicator ensures it remains relevant with up-to-date market information, making it a valuable addition to any trading strategy."

Multi-Regression StrategyIntroducing the "Multi-Regression Strategy" (MRS) , an advanced technical analysis tool designed to provide flexible and robust market analysis across various financial instruments.

This strategy offers users the ability to select from multiple regression techniques and risk management measures, allowing for customized analysis tailored to specific market conditions and trading styles.

Core Components:

Regression Techniques:

Users can choose one of three regression methods:

1 - Linear Regression: Provides a straightforward trend line, suitable for steady markets.

2 - Ridge Regression: Offers a more stable trend estimation in volatile markets by introducing a regularization parameter (lambda).

3 - LOESS (Locally Estimated Scatterplot Smoothing): Adapts to non-linear trends, useful for complex market behaviors.