Divergence DetectorOverview:

- Identifies divergence on the specified indicator. Support for additional indicators in development.

- Divergence labels indicate strength of divergence, making it easy to spot stronger divergence.

- Fully customizable (including inputs for indicator type and length, pivot lengths, divergence type, lookback range, price source, and more), allowing you to see exactly what you want based on your chart type and timeframe.

Inputs:

See tooltips on Inputs page in settings.

Please report any issues/bugs, enhancement suggestions, or requests for additional indicator support.

Indice de force relative (RSI)

Relative Strength Index ColoredThis is a slight nuanced version of the RSI that adds color to the RSI MA based on the slope. This makes it easier to see a potential direction.

RSI with Slow and Fast MA Crossing Strategy (by Coinrule)This strategy utilises 3 different conditions that have to be met to buy and 1 condition to sell. This strategy works best on the ETH/USDT pair on the 4-hour timescale.

In order for the strategy to enter the trade, it must meet all of the conditions listed below:

ENTRY

RSI increases by 5

RSI is lower than 70

MA9 crosses above MA50

To exit a trade, the below condition must be met:

EXIT

MA50 crosses above MA9

This strategy works well on LINK/USDT on the 1-day timeframe, MIOTA/USDT on the 2-hour timeframe, BTC/USDT on the 4-hour timeframe, and BEST/USDT on the 1-day timeframe (and 4h).

Back-tested from 1 January 2020.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

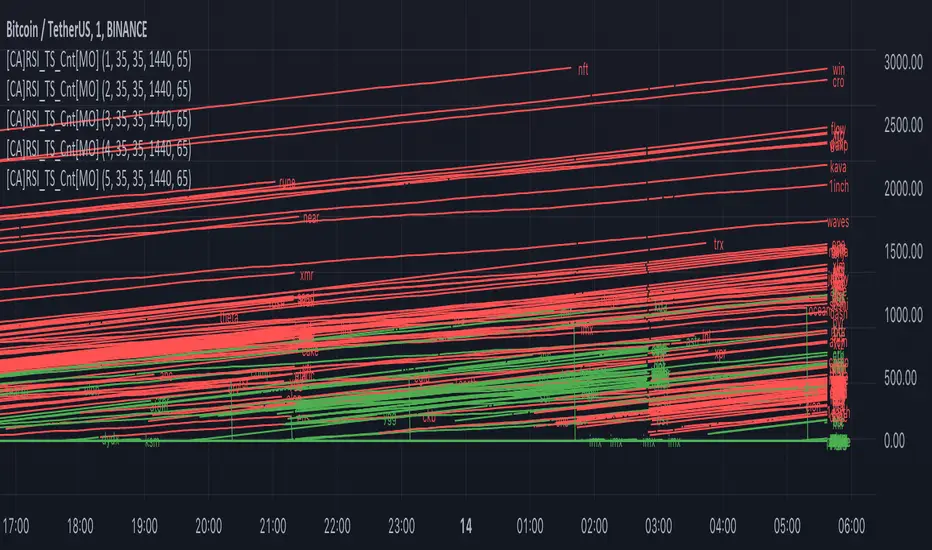

[ChasinAlts] RSI (Time-Spent) Count[MO]// Hello fellow traduers, hope all is well in your neck of the woods. Anywho, I'll attempt to be short and sweet.

// I've been doing a LOT of work recently with RSI to figure out what its all about and to learn the ins and outs.

// Some great ideas (I think at least) have come to fruition from the deep-dive into RSI, thus, I've got 2 of these ideas

// to share. One notable feature for the RSI is when there is a BULLISH trend, it is VERY likely to stay within the upper

// 2/3rds of the RSI extremes (0-100) and vise-versa for BEARISH trends and the lower 2/3rds of the RSI extremes.

// That is where this script's idea was derived. Now PLEASE, do tell, if you disagree with me (preferably via a cool,

// calm, and collected comment...but hey, that's up to you). Ok, now the script.

//

// What this does is gives you a Bullish and Bearish count for the bars. Bullish Cnt counts up by +1 per every PRINTED bar

// that is above OverSold and vise-versa for the Bearish Cnt and being below OverBought. That does VERY MUCH make it

// possible for both counts to have a high value if RSI is staying between OverBought and OverSold for extended periods

// of time. Though, the ONLY count that will be shown is the one with the highest value.

//

// There are tooltips describing each of the settings but I will quickly talk about 3 more things. First of all, I prefer

// to have as few settings in the settings menu as possible thus the "Boundaries to OB/OS" setting can be viewed as the

// OverSold input and the OverBought setting is configured from this by subtracting "Boundaries to OB/OS" from 100

// (ie. 100-Oversold = OverBought). There Lastly, there is the option to show ONLY the coin with the MAX Count from each

// 'set' of coins. When that count resets to 0 then the next highest count coin will take its place. To use this instead

// of how the script is currently constructed you only need to comment out (add '//' at the beginning of each line of) the current

// plot functions and uncomment the lines at the very bottom under the 'MAX' section. Doing so also reveals the possibility of

// setting an alert for when the coin with the max count changes between different coins. This is very helpful because since it

// only gives the top count of ALL the coins in the selected set, this count is most likely going to continue forward with its

// count for a while thus when the alert goes off I prefer to look at the potential trades in the opposite direction of which

// the max coin was just in (ie. if its count plot/label is red and it stops then look for a potential long trade on the coin

// who's count just reset. Only ONE more piece of the script I have yet to talk about. There is a filter in the code and you

// can select to use or not use within the settings. What this filter does is it counts all the printed bars within the last

// ___bars(user selectable). This is due to the fact that if there is no trade that occurs on a bar then TradingView does not

// print the bar. The coins that have fewer updates also tend to stay within a tighter range for it's RSI thus many times

// giving the illusion that the coin is a good trade bc its trending count is very high (tending to be higher than the others)

// thus hogging the precious chart space if using the script in its current form, or hogging up the MAX slot so that no other

// (and most likely BETTER-TO-TRADE) coins will be shown. It is a great volatility indicator (that of which I have published

// a script using the idea in the recent past). If selected in the settings menu and if the % of printed bars count goes below

// the user set minimum % then both Bullish and Bearish counts will be reset. This is indicated within the counts plots by looking

// at the plots whose counts reset and rather than the plots just stopping printing in mid-air, they will continue to plot while the

// counts reset and fall down to 0. These types of coins will keep you in a trade longer that you'd probably want gaining less than

// you'd probably expect.

//

// Peace Folks & Happy Trading,

//

// ChasinAlts

Stable Coin Dominance RSIThe Stable Coin Dominance RSI evaluates the relative dominance of stable coins within the crypto ecosystem as compared to the total market cap. As stable coin dominance rises, it suggests that market participants are exiting out of crypto assets and into dollar pegged stable coins. The opposite is true inversely; as stable coin dominance diminishes, it suggests that market participants are divesting out of stable coins and into crypto assets.

Stable coin dominance can be expressed as a percentage of the total market cap as follows: Stable Coins / Total Crypto. The Stable Coin Dominance RSI indicator uses this percentage and converts it into an oscillator using the formula for the relative strength index.

The calculation for the indicator is: RSI

The users can select from USDT and USDC, two most dominant stable tokens by market cap, and compare their relative dominance against Bitcoin and the alt market.

The Stable Coin Dominance RSI may be useful on larger timeframes when attempting to identify the market’s appetite for risk along with oversold and undersold readings which may indicate pivots or turn arounds along market extremes.

The limitation of the indicator lies in the fact that stable coins continue to make up a growing percentage of the total market cap over time and thus comparisons to earlier cycles will not be a perfect apples-to-apples evaluation. This being said, the smoothing function of the RSI’s look back helps to moderate these comparative differences.

Risk Management Strategy TemplateThis strategy is intended to be used as a base template for building new strategies.

It incorporates the following features:

Risk management:

Configurable X% loss per stop loss

Configurable R:R ratio

Trade entry:

Calculated position size based on risk tolerance

Trade exit:

Stop Loss currently configurable ATR multiplier but can be replaced based on strategy

Take Profit calculated from Stop Loss using R:R ratio

Backtesting:

Configurable backtesting range by date

Trade drawings:

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: Price is above EMA line

C2: RSI is crossing out of oversold area

SHORT

C1: Price is below EMA line

C2: RSI is crossing out of overbought area

Trade exit:

Stop Loss: Stop Loss ATR multiplier is hit

Take Profit: R:R multiplier * Stop Loss is hit

The idea is to use RSI to catch pullbacks within the main trend.

Note that this strategy is intended to be a simple base strategy for building upon. It was not designed to be traded in its current form.

Relative Index StrengthThis script shows relative strength of custom stock compared to Index. It is helpful in detecting how strongly a stock is performing when compared to an Index.

When the index is falling but the custom stock is rising, indicator shows this in red with its relative strength compared to index, indicating the stock is moving strongly against market trend.

When the index and the custom stock are moving in same direction, indicator remains neutral, indicating the stock is aligned with the market trend.

Relative Strength Index 2 buy a sellThis is my tool, I wanted to publish it so that my friend can easily find my tool

RSI + MA, LinReg, ZZ (HH HL LH LL), Div, Ichi, MACD and TSI HistRelative Strength Index with Moving Average, Linear Regression, Zig Zag (Highs and Lows), Divergence, Ichimoku Cloud, Moving Average Convergence Divergence and True Strength Index Histogram

This script is based on zdmre's RSI script, I revamped a lot of things and added a few indicators from ParkF's RSI script.

Disable Labels in the Style tab and the histogram if you don't enlarge the indicator and it seems too small.

Look to buy in the oversold area and bounce of the support of the linear regression.

Look to sell in the overbought area and bounce of the resistance of the linear regression.

Look for retracement to the moving average or horizontal lines, and divergences for potential reversal.

RSI

The Relative Strength Index (RSI) is a well versed momentum based oscillator which is used to measure the speed (velocity) as well as the change (magnitude) of directional price movements.

Moving Average

Moving Average (MA) is a good way to gauge momentum as well as to confirm trends, and define areas of support and resistance.

Linear Regression

The Linear Regression indicator visualizes the general price trend of a specific part of the chart based on the Linear Regression calculation.

Zig Zag (Highs and Lows)

The Zig Zag indicator is used to identify price trends, and in doing so plots points on the chart to mark whenever prices reverse by a larger percentage point than a predetermined variable or marker.

Divergence

The divergence indicator warns traders and technical analysts of changes in a price trend, oftentimes that it is weakening or changing direction.

Ichimoku Cloud

The Ichimoku Cloud is a package of multiple technical indicators that signal support, resistance, market trend, and market momentum.

MACD and TSI Histogram

MACD can be used to identify aspects of a security's overall trend.

The True Strength Index indicator is a momentum oscillator designed to detect, confirm or visualize the strength of a trend.

SUPER RSI [Gabbo]this indicator serves to differentiate the classic source of RSI

with these inputs you can modify the inputs of the different Bar's, you can choose between:

Candles = classic Candles

Heikin Hashi

Kagi

Line break

Pointfigure

Renko

Selecting the input: "Use Different Source ???" you can use a source with multiple elements of your choice

2 = (Source 1 + Source 2) / 2

3 = (Source 1 + Source 2 + Source 3) / 3

4 = (Source 1 + Source 2 + Source 3 + Source 4) / 4

5 = (Source 1 + Source 2 + Source 3 + Source 4 + Source 5) / 5

Koncorde PlusKONCORDE IS ONLY INTENDED TO BE APPLIED TO ASSETS WHERE VOLUME DATA IS PROVIDED.

This indicator is made up of 6 indicators: 4 trend (RSI, MFI, BB, Stochastic) and 2 volume. The 2's for volume are the PVI (positive volume index) and the NVI (negative volume index). These two indicators are the interesting ones as they are programmed to proportionally attribute the volume traded between the strong hands (sharks) and the weak hands (minnows).

As for what time period to use, the bigger the better, since after all what we are doing is data analysis and therefore the more data, the better.

When strong hands (blue histogram) are below zero, they are said to be selling while when they are above zero, they are said to be buying. The same goes for weak hands (green histogram).

Meaning of each zone:

Blue histogram: strong hand (sharks). If it is positive it indicates accumulation and if it is negative distribution.

Green histogram: weak hand (minnows). If it is positive it indicates buy and if it is negative it indicates sale.

Brown histogram: Indicates the trend and depends on previous values of weak hands and trend indicators (RSI, MFI, BB, Stochastic).

Red line: It is an average that smoothes the trend indicated by the brown histogram (default is the EMA).

Crossing Pattern

The pattern gives us a bullish entry signal when the trend (brown histogram) crosses above the average (red line) and is positioned bearish when the trend crosses below the average.

Zero Pattern

When the price trend (brown histogram) tends to zero, it means that there will be a change in its trend. This pattern is for trading in a bullish position.

Spring Pattern

When a cross between the average (red line) and the trend (brown histogram) has already occurred, and in addition the weak hands are above the price trend, that "spring on the mountain" is formed that gives us to understand that the upward trend will be more than evident.

Mirror Pattern

This pattern occurs when there is panic in the market and weak hands are selling (below zero). If at that moment the strong hands are buyers, the price tends to level off to begin the rise later.

This pattern is compatible with the Crossover Pattern, having more guarantees of success. If just after finishing the mirror pattern, the Crossover Pattern plus the Spring Pattern appears, then we have a good chance of winning.

Bear Hug Pattern

This pattern is for bearish positions only. It is the opposite figure to the mirror pattern. That is, we have strong hands clearly selling and weak hands clearly buying and above the price trend (brown histogram). It is the figure where you can see that the strong hands are distributing the assets to the weak hands.

Harpoon Pattern

If when the mirror pattern occurs, the red line crosses the blue histogram, a very strong bullish entry signal is produced.

Add an exit signal which occurs when we are in a spring pattern but the big hands start selling, mostly coinciding with the start of the bear hug pattern.

General rules for operating the Mirror Pattern:

a) Wait for the green histogram to start recovery, rise to positive values; if possible, until it crosses from bottom to top the brown line (brown histogram) and/or red average .

b) The blue histogram should be consistently positive. If it turns and goes towards negative values it can indicate a failed pattern at that same point.

c) Locate the low of the lower candle within the pattern and place the Stop Loss just below it for reference.

d) If we are not sure (we almost never will be) that there will be a turn or if it could finally be a bearish continuation we can use the SL to go short .

Additional:

A panel with performance statistics of the analyzed asset was added.

Added an indicator that shows the cumulative delta volume in the form of triangles at the top of the chart.

Added of user @DonovanWall

PS: Unofficial version, I was guided by the description of the BLAI5 author's website www.blai5.net

DISCLAIMER: For educational and entertainment purposes only. Nothing in this content should be interpreted as financial advice or a recommendation to buy or sell any sort of security or investment including all types of cryptos. DYOR, TYOB.

Candle Fill % MeterFor use with Hollow Candles

Fills Candles based on either the value of the RSI or coppock scaled to fit properly between the open and close. Makes for a compact visual with lot's of information given. Toggle bells and whistles in settings such as arrows to indicate the direction of the value being measured, dividing levels, fill from candle open all the time instead of the bottom up and more.

Tutporial Pedia (Signal buy & Sell)Untuk mempermudah kita dalam bermain dan memahami Signal Trade View Rate 98 %

RSI+ by Wilson (alt)Extension of the excellent RSI+ script by Wilsonlibero. I tweaked the parameters to better fit crypto markets, and I added a few more visuals, such as midline, overbought/oversold threshold lines and areas, background coloration depending on RSI trend above or below midline, and a few other tweaks especially colors (fixed the transp parameter deprecation for example). The color theme is by default more optimized for dark mode charts, but all colors can be configured, and all drawings can be enabled/disabled/tweaked in the parameters.

I'm just giving back to the community since I could modify this script only because it was open-source. If you like this script, please don't give me any credit, but please show some love to the original author Wilsonlibero:

TDI w/ Variety RSI, Averages, & Source Types [Loxx]This hybrid indicator is developed to assist traders in their ability to decipher and monitor market conditions related to trend direction, market strength, and market volatility. Even though comprehensive, the Traders Dynamic Index (TDI) is easy to read and use. This version of TDI has 7 different types of RSI, 38 different types of Moving Averages, 33 source types, and 5 types of signals as well as alerts and coloring. Default RSI type is set to Jurik's RSX. This indicator can be used on any timeframe.

Green/Red line = RSI Price line

White line = Trade Signal line

Dark Green/Red lines = Volatility Band

Yellow line = Market Base Line

Gray dashed lines = Horizontal boundary lines, oversold/overbought

5 Signal Types w/ Alerts

Signal Crosses = Green/Red line crosses over or under White line

Floating Boundary Crosses = Green/Red line crosses over or under upper Dark Green/ lower Red lines

Horizontal Boundary Crosses = Green/Red line crosses over or under Gray dashed upper/lower lines

Floating Middle Crosses = Green/Red line crosses over or under Yellow line

Horizontal Middle Crosses = Green/Red line crosses over or under Gray dashed middle line

Manual Signal Types (no alerts included, this requires manual analysis)

Volatility Band Signals (Dark Green/Red lines) = When the Dark Green/Red lines are expanding, the market is strong and trending. When Dark Green/Red lines are constricting, the market is weak and in a range. When the Dark Green/Red lines are extremely tight in a narrow range, expect an economic announcement or other market condition to spike the market

Beyond these simple signal rules, there are various other signals or methods that can be used to derive long/short/exit signals from TDI included slope of the Green/Red line and bounces off the Yellow line.

Included

Loxx's Expanded Source Types

Loxx's Variety RSI

Loxx's Moving Averages

Signals

Alerts

Bar coloring

RSI mid partition color changeWhen RSI is above 50 our default bias is on buy side and when below 50 our bias is on sell side.

Therefore created 2 zones for easy identification.

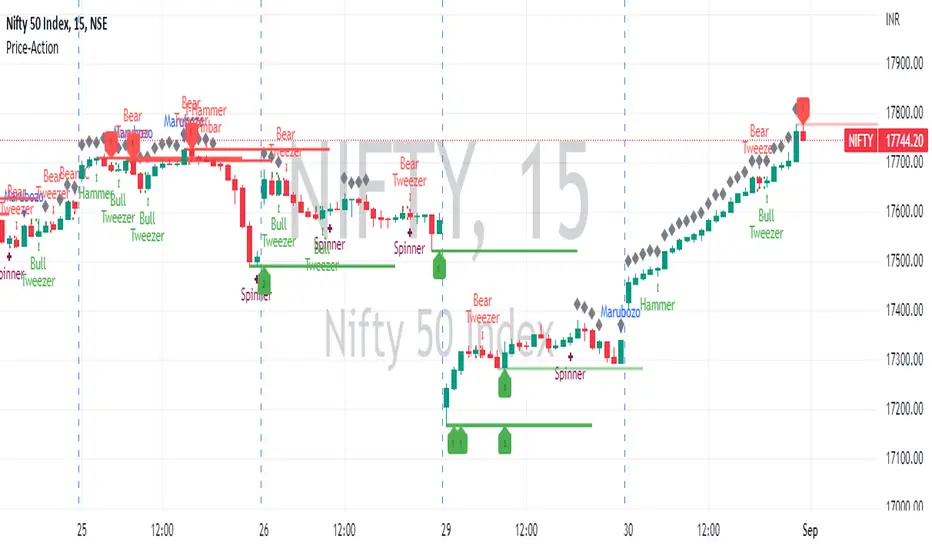

Price Action in action

What?

Price Action in Action is an indicator to help Price Action learners and practitioners to get everything related for Price Action in one place.

Price Action is:

Price + Volume = Action

In this indicator, we have the following features available:

Support/Resistance

Using the RSI with different periods in a multiple of 7 (7, 14, 21, 28), we first determine the overbought (above 70, customizable) and oversold (below 30, customizable) regions. Then we pick up the highest point and lowest point in the RSI values in the overbought and oversold regions, respectively. These are the point, historically supply/demand emerged for surety to push down/up the RSI indicator and the corresponding price. So, these are the most accurate way, we believe, to draw support/resistance (or demand/supply) in the chart. By default, the Support is green color and Resistance is red color. To give a visual representation, we differentiate the different shades of green and red. For example, for Level-1 (i.e. 7 by default) we use the darkest shade (0 transparency) and Level-4 (i.e. 28 by default) we use lighter shade (60 transparency). Note please: you can customize the color of support and resistance lines (say if you want resistance as green and support as red). The respective shades (transparency) will be automatically adjusted accordingly. But those shade (transparency) levels are not customizable, they are fixed (please bear with it for version-1 at least).

Strength of Support/Resistance

In the chart above/below the Resistance / Support lines you can see the tiny labels with some numbers like 1, 2.

We found out how many times a particular support/resistance is appearing across multiple RSI periods. E.g. if price P1 appears 2 times among 4 different RSI periods, the number will be 2 for that calculation, and so on.

There can be multiple presence of these numbers in a support/resistance line (i.e. multiple tiny labels). Something like: 1, 1, 2 (into different candles). This means the same support/resistance is tested so many times in different occasion (means there is a RSI max/min coincides in this level over multiple occasions) at different candles.

This will help you to intuitionally gauge the “strength” of a support/resistance line.

The more the marrier, unworthy to mention.

Candle Stick Patterns

Well: we don’t need to tell anything about the Candlestick. All of you know it better than us. And it’s a time proven, zero-lag mechanism to judge the Price-Action is unfolding in the market. We do not know if there is anything better possible than this time tested patterns to judge the prevailing sentiments of market.

Price-Action does not complete without finding out the Candlestick Patterns correctly.

And in this indicator your will get all of these: Single Candle such as Doji (default off), Marubozu, Spinner, hammers, inverted-hammer etc. ; 2 candles like Tweezer, Inside Candle, Engulfing; 3 candles like morning star/evening star.

In the multi candle patterns (2/3 candles), we are grouping the candles with a dotted rectangle such that it is clear which 2/3 candles are part of the pattern. E.g. Morning Star: 3 candles are grouped in a dotted rectangle and the Morning Star label will come to the latest candle (3rd most – as the pattern is detected reliably only on the completion of the 3rd final candle).

Of course, any program can not eliminate your trained eyes and brain to capture the patterns. But we have provided sufficient knobs to adjust various parameters to tweak the candle-pattern detection. Such as Strict Inside Candle(Harami) Boolean knob where the whole current candle including wicks will be inside the body part of the previous big candle. For non-strict mode, the current candle just inside the previous candle, possibly by wicks.

To make it better usable, for every such knobs (which are not obvious) we have added user-friendly tooltip (just mouse hover the question mark (?) besides the control/switch). There are plenty of it.

Volume

Here we have a rudimentary (yet effective) way to judge the volumes.

We find out the Volume Weighted Moving Average (VMWA) of the 20-period (default, but customizable) and the latest volume. If the latest volume is more than the 20 period vwma, we just add a grey diamond on the top of the candle to denote it’s attracting volumes. Of course, we provide a Weight coefficient (default is set to 1). So if the current bar’s volume on bar’s completion is more than the 20 period volume vmwa times the weigh-cofficient, we mark it with a tiny grey diamond.

Points to be noted:

In all places we mark the indication only on the completion of the bar (technically speaking we have checks, as far as possible, with barstate.isconfirmed). However, if you wish, you can turn it off for Candlestick (as some experts may want to check candlestick on the real time, even before the closing of bars).

In case if you see the chart looks cluttered (because of many information, specially in smaller timeframes like 5 min), there are controls given in the settings to toggle each and every features.

By default, we turn off Doji candles (all 3 types of Doji’s – normal, Gravestone & Dragonfly) as they are mainly indecision. However, you can toggle it to turn it on.

It does not give you any Buy/Sell call. The interpretation it does not have.

Why?

What’s unique in it?

As we already mentioned our intention is to include Price (in forms of Support / Resistance), Volume and Action (sentiments in terms of Candlestick patterns) into a single place. And so far, to the best of our knowledge, we could not come across a single indicator provides all of these.

There were works available to determine the RSI based support / resistance zones. Those are great piece works at that time (lets say 3 years back when PineScript was in earlier versions). To the best of our knowledge those does not cover up finding out the lowest / highest point of RSI and the corresponding price to get the simplistic and distinct support/resistance lines.

We have the intuitive support/resistance strength included which we could not found out in current set of available indicators.

To the best of our knowledge, there seems no indicator can detect 3-candle patterns which are extremely popular to detect trend reversals (such as Morning Star or Evening Star). Moreover for the multi-candle patterns we are grouping the candles part of the pattens (2-candles or 3-candles) using a dotted rectangle such that it’s visually clearly (and a well educative material for Price-Action learners also).

Mentions:

There are many works which inspire us along the way. Honestly: we sometimes forgot which all indicators we experimented with. We are sincerely apologetic in case we forgot to mention. A few note-worthy:

There is an indicator from user “repo32” named as “Candlestick Patterns Identified (updated 3/11/15)”. (We could not be able to contact “repo32”). We are inspired from his work that it’s feasible to detect Candlestick patterns.

There is an awesome work done by “RSI Based Automatic Demand and Supply” by user “shtcoinr”. The idea of consulting multiple RSI levels to find out the demand/supply zone we inspired from him. (We did contact “shtcoinr” and got his kind permission to use the concept.)

We are greatly thankful to these abovementioned wizards for their pioneering a-prior work in this front.

And of course, this TradingView platform to provide this abstraction, facilitates and felicitates collaborative contributions.

Ultimately, what’s for you?

That’s the main question. What’s for you?

Price-action comprises of following 3 tasks (at least):

Draw support/resistance lines in the chart.

Once price reaches at the support/resistance line, you fervently look out the candles’ formation to mentally map to the candle patterns. Your aim is divine: You want to judge if the price-action will continue or take a rejection/reversal.

Then you double-confirm with the volume (in a non-overlaid chart below).

Finally take a trade.

For a price-action newbie or seasoned, expert practitioner, you must be doing all the above tasks regularly and manually, in a mechanical, mundane way. There come the humanly subjectivity & the inevitable emotions . This indicator, being a piece of program/code in PineScript latest version v5 , eliminates (or at least, reduces to a great extend) that subjectivity & emotions out of the way of decision making . Thus resulting better yield.

Of course, you can argue that you draw slanted trend lines also. We recommend an already existing indicator by user LuxAlgo named as “Trendlines with Breaks ”, if you wish so.

Disclaimer:

This piece of software does not come up with any warrantee or any rights of not changing it over the future course of time.

We are not responsible for any trading/investment decision you are taking out of the outcome of this indicator.

Happy trading.

RSI SMA Crossover StrategyOverview

RSI SMA Crossover Strategy works the same way as traditional MA crossover strategies, but using RSI instead of price. When RSI crosses over the SMA, a long position is opened (buy). When RSI crosses under the SMA, the long position is closed (sell).

This strategy can be very effective when the right inputs are used (see below). Be sure to use the backtesting tool to determine the optimal parameters for a given asset/timeframe.

Inputs/Parameters

RSI Length: length for RSI calculation (default = 50)

SMA Length: length for SMA calculation (default = 25)

Strategy Properties

Initial Capital = $1000

No default properties are defined for Slippage, Commission, etc, so be sure to set these values to get accurate backtesting results. This script is being published open-source for a reason - save yourself a copy and adjust the settings as you like!

Backtesting Results

Testing on Bitcoin (all time index) 1D chart, with all default parameters.

$1,000 initial investment on 10/07/2010 turns into almost $2.5 billion as of 08/30/2022 (compared to $334 million if the initial investment was held over the same period)

Remember, results can vary greatly based on the variables mentioned above, so always be sure to backtest.

RSI ModifiedThe RSI is an excellent indicator for determining when equities are overbought/oversold. Though I believe there is a shortcoming in using the 70/30 levels since they are static and do not adjust for when an equity is trending. It stands to reason that in a downtrend, the overbought might be less than 70 and the oversold less than 30—Vice versa for a bull trend. Using the built-in function of pivots, I have attempted to create overbought/oversold lines that adjust with the trend. Leaving the 70/30 lines on the indicator also helps visualize the equity trend. All pivot settings are adjustable in the input menu. The pivot limits serve as a filter for recording pivot points. For example, with an upper pivot limit of 60, only pivots greater than 60 will be recorded into the array used to determine overbought. The crosses represent which values are used to determine overbought/oversold and do not provide timely indications.

Visual RSI {bebaps}Visual RSI

This script provides a visual way to view RSI data. Sometimes it may be useful to view RSI data on the price chart instead of in a separate pane. This script enables the following configurable options:

Plot shapes on the chart during key RSI events such as: crossing above or below the overbought or oversold level

Color bars based upon the current value of the RSI, such as: RSI currently oversold, or RSI currently between overbought and 50

All options are configurable. This is not meant to serve as a replacement for having the RSI on your chart, but it will make it easier to highlight key data points in real time.

smoothed_rsi

Description:

A well-known and vastly used momentum indicator, a Relative Strength Index (RSI) by J. Welles Wilder Jr., aims to evaluate the current price to its oversold/overbought area while giving an overview of bearish/bullish momentum. In this indicator, simply adding the super-smoother function (John F. Ehlers) was applied to the RSI line to create a more smoothed line and reduce its noise.

RSI:

RSI = 100 - 100/(1+RS)

RS = AvgUp/AvgDown

super_smoother(rsi)

Notes:

RSI > 70 indicates overbought

RSI < 30 indicates oversold

direction of the RSI line

Juirk-Filtered QQE Histogram [Loxx]Juirk-Filtered QQE Histogram is a QQE indicator with 7 different RSI types, Jurik-Filtering with the option of double filtering. 2 types of signals, and Loxx's Expanded Source types. These additions are useful to filter out noise.

What is Qualitative Quantitative Estimation (QQE)?

The Qualitative Quantitative Estimation (QQE) indicator works like a smoother version of the popular Relative Strength Index ( RSI ) indicator. QQE expands on RSI by adding two volatility based trailing stop lines. These trailing stop lines are composed of a fast and a slow moving Average True Range (ATR).

There are many indicators for many purposes. Some of them are complex and some are comparatively easy to handle. The QQE indicator is a really useful analytical tool and one of the most accurate indicators. It offers numerous strategies for using the buy and sell signals. Essentially, it can help detect trend reversal and enter the trade at the most optimal positions.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

Included:

Loxx's Expanded Source Types

Alerts

Signals

Bar coloring

Included Libraries

Loxx's Variety RSI

Loxx's Jurik Tools

Loxx's Expanded Source Types

Related indicators:

Natural Market Mirror (NMM) and NMAs w/ Dynamic Zones

RSI/RSX QQE Histogram w/ Discontinued Signal Line

Jurik CFB Adaptive QQE

Adaptive Qualitative Quantitative Estimation (QQE)