Parametric VaRValue at Risk can also be computed parametrically using a method known as variance/co-variance VaR. This method allows you to simulate a range of possibilities based on historical return distribution properties rather than actual return values. It's actually more accurate even though it assumes a normal distribution especially when not much data is available

Risk!!!

Trend & atr day & calcHi!

Why for what and how in this script?

At the time of publication the script consists of three modules, it may increase in the future.

1. Bottom left corner : daytime ATR module

(idea and basis of the author's script - ???)

- The size of the daily ATR based on 14 bars;

- intraday ATR progress;

- colour indication of the progress status, for easier visual perception (green < 70%, yellow 70-90 and red over 90% of ATR)

By evaluating the progress of the daily ATR, it is possible to suggest and expedient to enter/exit/hold a trade.

2. Top right: trend module

The trend is calculated based on Bill Williams' alligator indicator

- trend status on specified timeframes for the current ticker;

- colour indication for visual perception (green - growing trend, yellow - alligator is sleeping, red - downtrend)

Do not forget that the alligator is based on moving averages with the resulting consequences.

Its purpose is to assess the state of the trend on other ticker TFs, without additional actions (switching to another screen or TF)

3. In the bottom left corner - risk and position calculator

(based on an idea of the risk calculator by @andrei.bunulu)

It helps to determine the advisability of entering the trade and also what size position to enter into the trade, within money management strategy chosen.

- The calculator works in two directions: long deal and short deal (short deal calculation is enabled by check-box in settings)

- two calculation methods:

a. based on the set stop loss % (default is 0.3%), in this mode the stop and takeout level is automatically calculated (default is 1 / 3).

b. by entering the desired price levels (entry, stop and take profit points)

To make this work correctly please do not forget to choose the type of calculation (% or price) in the settings, and the currency symbol (for visual representation in the results).

The calculator can take into account the set commissions and spreads.

When hovering over the module - tooltips are displayed.

Each module can be enabled / disabled in the settings.

The size and arrangement of the modules is made for joint use with the script - "Abnormal Bar".

/// а по-русски это так ///

Привет!

Зачем для чего и как в этом скрипте?

На момент публикации скрипт состоит из трех модулей, возможно в будущем увеличится.

1. В левом нижнем углу : модуль дневного ATR

(идея и основа скрипт автора - ???)

- размер дневной ATR на основании 14 баров;

- прогресс ATR внутри дня;

- цветовая индикация состояния прогресса, для более простого визуального восприятия (зеленый < 70%, желтый 70-90 и красный более 90% ATR)

Оценивая прогресс дневного ATR, можно предположить и целесообразности входа / выхода / удержания из сделки.

2. В правом верхнем углу: модуль тренда

Тренд рассчитывается на основе индикатора - аллигатор Билла Вильямса

- состояние тренда на указанных таймфреймах для текущего тикера;

- цветовая индикация для визуального восприятия (зеленый - растущий тренд, желтый - аллигатор спит, красный - нисходящий тренд)

Не забываем, что аллигатор построен на основе скользящих средних с вытекающими последствиями.

Назначение - оценить состояние тренда на других ТФ тикера, без дополнительных действий (переключения на другой экран или ТФ)

3. В нижнем левом углу - калькулятор рисков и позиции

(на основе идеи калькулятора аuthor: @andrei.bunulu)

Помогает определить целесообразность входа в сделку, а также каким размером позиции входить в сделку, в рамках выбранной стратегии мани менеджмента.

- калькулятор работает в два направления: длинная и короткая сделка (расчет по короткой включается в настройках чек-боксом)

- два варианта расчета:

а. на основании установленного % стоп лосса (по-умолчанию 0,3%), при этом режиме происходит автоматический расчет уровня стопа и тейка (по умолчанию 1 / 3).

b. путем ввода данных желаемых уровней цены (точки входа, стопа и тейк профита)

Для корректной работы не забываем в настройках выбирать тип расчета (% или цена), а также символ валюты (для визуального отображения в итогах).

Калькулятор может учитывать установленный размер комиссий и спреда.

При наведении на модуль - отображаются подсказки.

Каждый модуль можно включить / выключить в настройках.

Размер и расположение модулей сделано для совместного использования со скриптом - "Abnormal Bar"

VIX - SKEW DivergenceThe CBOE VIX is a well-known index representing market expectations for volatility over the next 30 days.

The CBOE SKEW is an index reflecting the perceived tail risk over the next 30 days.

When the SKEW rises over a certain level (~140/150), that means investors are hedging their exposure with options, because they are worried about an incoming market crash or a "black swan". If that happens when the VIX is very low and apparently there is no uncertainty, this can warn of a sudden change in direction of the market. You will see for yourself that an increasing divergence often anticipates a sharp fall of leading stock indexes, usually within two to four months.

This is probably not very relevant for the short-term trader but mid/long-term traders and market analysts may find it useful to clearly visualize the extent of the distance between the VIX and the SKEW. For that reason, I wrote this highly customizable script with which you can plot the two indexes and fill the space within them with a color gradient to highlight the maximum and minimum divergence. Additionally, you can fill the beneath VIX area with four different colors. It is also possible to plot the divergence value itself, so if you want you can draw trendlines and support/resistance levels on it.

Please note that the divergence per se doesn't predict anything and it's meant to be used synergistically with other technical analysis tools.

More informations here:

www.cboe.com

www.cboe.com

Value At Risk Channel [AstrideUnicorn]The Value at Risk Channel (VaR Channel) is a trading indicator designed to help traders control the level of risk exposure in their positions. The user can select a time period and a probability value, and the indicator will plot the upper and lower limits that the price can reach during the selected time period with the given probability.

CONCEPTS

The indicator is based on the Value at Risk (VaR) calculation. VaR is an important metric in risk management that quantifies the degree of potential financial loss within a position, portfolio or company over a specific period of time. It is widely used by financial institutions like banks and investment companies to forecast the extent and likelihood of potential losses in their portfolios.

We use the so-called “historical method” to compute VaR. The algorithm looks at the history of past returns and creates a histogram that represents the statistical distribution of past returns. Assuming that the returns follow a normal distribution, one can assign a probability to each value of return. The probability of a specific return value is determined by the distribution percentile to which it belongs.

HOW TO USE

Let’s assume you want to plot the upper and lower limits that price will reach within 4 hours with 5% probability. To do this, go to the indicator Settings tab and set the Timeframe parameter to "4 hours'' and the Probability parameter to 5.0.

You can use the indicator to set your Stop-Loss at the price level where it will trigger with low probability. And what's more, you can measure and control the probability of triggering.

You can also see how likely it is that the price will reach your Take-Profit within a specific period of time. For example, you expect your target level to be reached within a week. To determine this probability, set the Timeframe parameter to "1 week" and adjust the Probability parameter so that the upper or lower limit of your VaR channel is close to your Take-Profit level. The resulting Probability parameter value will show the probability of reaching your target in the expected time.

The indicator can be a useful tool for measuring and managing risk, as well as for developing and fine-tuning trading strategies. If you find other uses for the indicator, feel free to share them in the comments!

SETTINGS

Timeframe - sets the time period, during which the price can reach the upper or lower bound of the VaR channel with the probability, set by the Probability parameter.

Probability - specifies the probability with which the price can reach the upper or lower bound of the VaR channel during the time period specified by the Timeframe parameter.

Window - specifies the length of history (number of historical bars) used for VaR calculation.

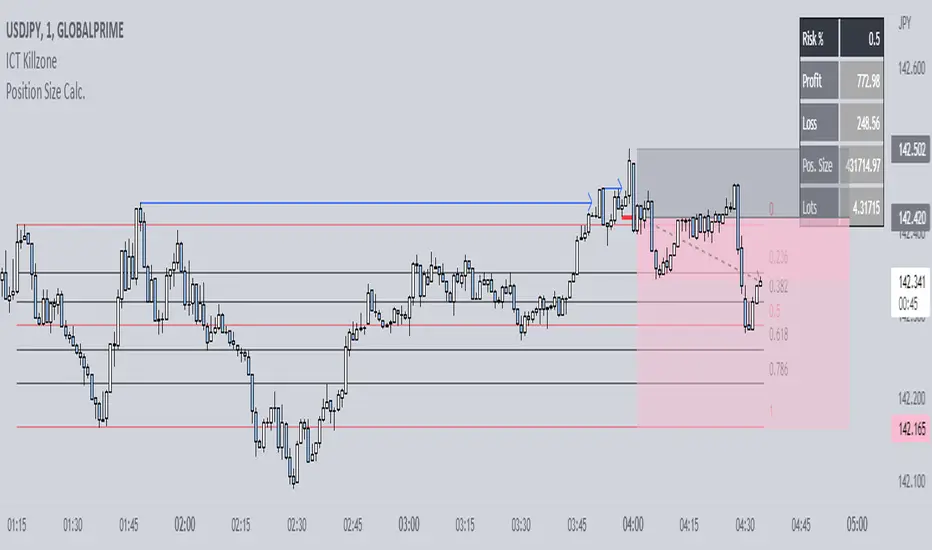

Position Size Calc. (Minimalist)This is a simplified position size calculator in the form of a table.

The reason I published this script is because all other position size calculator scripts try to provide way too much when it should be much simpler, position in strange areas of the chart and leave unwanted chart pollution.

This is a bare-bones functional table that takes your risk level, entry, stop and take profit as inputs, and calculates your loss, profit and required position size for your chosen risk level as a result.

Inspired by a table type position size calculator made by DojiEmoji design/color-wise. Functionally different however.

I hope you find this script useful and include it on your trading journey.

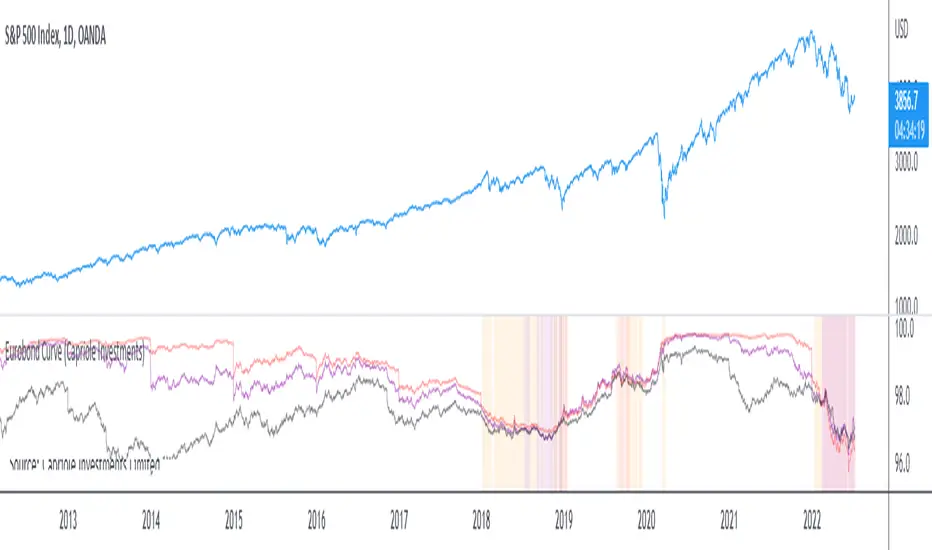

Eurobond CurveABOUT

Dynamically plots 3 no. forward EUROBOND curves. When the curves converge (or worse crossover) there is higher risk of financial uncertainty and potential market correction.

The Eurobond Curves work in a similar way to treasury "yield curve inversion"; except the EUROBOND curves can signal much earlier than Treasuries therefore providing a leading indicator.

The indicator looks the the "near" (next year EUROBOND), "mid" (EUROBOND 2 years out) and "far" (EUROBOND 5 years out) to assess for crossovers.

When the "near" and "mid" curves crossover the "far" curve, concerning economic conditions are developing and it may be a good idea to reduce risk exposure to markets.

LIMITATIONS

The EUROBOND curve crossover events are rare, and this indicator uses data back to 2005 (using approximately 25 TradingView security functions). Given there are relatively few crossover events, the reliability of this indicator should be considered low. Nonetheless, there is decent alignment with treasury yield curve inversions in the 20 year period assessed. Given treasury yield curve inversions have predicted every recession for the last 70 years, we still think the EUROBOND Curves are a useful datapoint to monitor into the future and provide confluence to other risk management strategies.

Koalafied Risk ManagementTables and labels/lines showing trade levels and risk/reward. Use to manage trade risk compared to portfolio size.

Initial design optimised for tickers denominated against USD.

trailing_drawdown

Description:

Drawdown was a tool to measure historical risk, derived from measuring current wealth from its previous peak, casually from portfolio construction (weights allocation), will consider to having a minimum drawdown. In this indicator, the drawdown for individual assets is utilized to measure its value or percentage from its trailing peak (default to 1-yr period).

Drawdown:

drawdown = (price/peaks)-1

Feature:

Static: display drawdown as percentage

Dynamic: display drawdown as value

PhinkTrade Risk Manager EssentialsHello there, fellow traders!

So, happy to bring you a new, free tool: my Risk Manager Essentials .

(To use it, click on "Add to favorite indicators" below, and then look for it in your charts’ "Indicators & Strategies" dialog window, inside "Favorites" tab.)

The main objective of this indicator is to help and incentivize as many traders as possible to adopt essential risk management practices .

First and foremost, it helps you define how much you can buy or sell, at your chosen price levels, in order to keep your risk always under control (in other words: in order to limit the amount you can potentially lose with a trade if your stop loss order is hit).

This is fundamental if you want to have a lasting and successful trading career: protect your capital, always . Because without it, you know: it’s game over.

Indicator also helps you visualize where minimum ideal target / take profit level is , given your risk, using the popular 3:1 Return/Risk ratio (R/R) .

3:1 R/R ratio is popular because with it you only need to “be right” (have price reach your targets) about 33% of the time, in order to be profitable : in other words, the fewer successful trades will pay you more than the sum of your unsuccessful ones will take from you.

So, make sure your strategy has a success rate greater than 33% and apply 3:1 R/R to your trades . This indicator will help you that, and with developing the necessary discipline . For example, by knowing where the ideal target should be, given your choices, you can assess the likelihood of it being reached in current price context. If that would look like a hard to happen scenario, it would probably be a good idea to avoid taking that particular trade.

Now, let’s see how it works:

When you deploy the indicator to the chart for the first time, you’ll be asked to define:

Your 1st entry price (interactively: you can define and adjust levels directly on the chart, thanks to the new Interactive Mode introduced by TradingView (ty, TV team!))

Your stop loss price (likewise)

Your 1st target price (likewise)

Your starting capital (via initial Input dialog)

Your risk (likewise)

Your risk is how much of your starting capital you are willing to lose if your stop loss is hit (define it as a % of your starting capital).

There’s a good practice here too: to risk only 1 percent of your capital per trade . This way, you can reinforce the odds of making more money than you lose and keep your peace of mind in all trades – and avoid messing up with your plans – and statistics – along the way.

Successful trading is a statistics-based endeavor. So, you want to implement and maintain consistency. Again, this indicator helps with that.

After initial setup:

You can also define additional entries and targets (up to 3 each) . Just open indicator’s Settings window and adjust accordingly.

If you have more than one entry – or target, the amounts involved will be split evenly between them. You can also enable the display of the Average Entry and Average Target labels , to see the equivalent, should you have taken (or take) a single order for each.

You can also define (via Settings, then interactively) a particular date and time for the trade . This way, labels will be presented near that moment, instead of constantly show near the latest bar.

Finally, you can personalize some other display settings: levels precision (number of decimal places), labels positions , and labels colors .

In conclusion:

You are very welcome to check it out – and adopt it on your daily use!

Please let me know your feedbacks as well. If you find any issues, or have any suggestions, I’ll be glad to hear. You can contact me here, via TradingView, or Telegram.

Finally, check the updates section below , as new stuff may show from time to time.

Thank you very much for your attention, and enjoy!

PhinkTrade

Sell Half On DoubleNotes:

- In settings leave 0 for actual price, or set a new price and the SHOD levels will change too.

ADR in 0.5 / 1 / 3 / 5top of the morning!

This indicator is a tiny bit different then the previous one i published.

As per my little study into the ATR, i have decided to remove it out of my indicator and instead put in a half an ADR in dollar vallue.

For me, i can use this value to check at what level i would like my stop. The next evolvement of this indicator might be a total new one since i'd be one for a lower timeframe with the 0.5 and 0.3 adr down from current high otd.

Hope you enjoy it,

Peace

Bitcoin Risk Long Term indicatorOBJECTIVE:

The purpose of this indicator is to synthesize via an average several indicators from a wide choice with in order to simplify the reading of the bitcoin price and that on a long term vision.

Useful for those who want to see things simply, typically to make a smart DCA based on risk.

I originally used this script as a sandbox to understand and test the usefulness of several indicators, and to develop my PineScript skills, but finally the Risk Indicator output seems relevant so I decided to share it.

USAGE:

The selected indicators are the ones that I think give the best market bottoms, but the idea here is that anyone can try and use any set of indicators based on those preferences (post in comments if you find a relevant config)

Most of the indicator inputs are configurable. And some are not taken into account in the calculation of the Risk indicator because I consider them not relevant, this script is also a test more than a final version.

NOTES :

If you have any idea of adding an indicator, modification, criticism, bug found: share them, it is appreciated!

In the future I will create another more versatile Risk indicator that will not be focused on bitcoin in weekly. (this indicator is still usable on other assets and timeframe)

THANKS:

to Benjamin Cowen for inspiring me with his Bitcoin Risk metric

to Lazybear for his Wavetrend Indicator and all the scripts he shares

to Mabonyi for his Bitcoin Logarithmic Growth Curves & Zones script

to VuManChu for his VMC Cypher B Divergence

to the Trading view team for developing TV and PineScript

And to all the community for all the published codes that allowed me to progress and create this script

---- FR ----

OBJECTIF :

L'objectif de cet indicateur est de synthétiser via une moyenne plusieurs indicateurs parmi un large choix avec afin de simplifier la lecture du cours de bitcoin et cela sur une vision longue terme.

Utile pour ceux qui veulent voir les choses simplement, typiquement faire un DCA intelligent en fonction du risque.

À la base j'ai utilisé ce script comme un bac à sable pour comprendre puis tester l'utilité de plusieurs indicateurs, et développer mes compétences PineScript, mais finalement l'output Risk Indicateur me semble pertinent donc autant le partager.

UTILISATION :

Les indicateurs sélectionnés sont ceux qui permettent selon moi d'avoir les meilleurs point bas de marché, mais l'idée ici est que chacun puisse essayer et utiliser n'importe quel ensemble d'indicateur en fonction de ces préférences (poster en commentaire si vous trouvez une configuration pertinente)

La plupart des inputs indicateurs sont paramétrables. Et certains ne sont pas pris en compte dans le calcul du Risk indicateur car je les estime non pertinent, ce script est aussi un essai plus qu'une version finale.

NOTES :

Si vous avez la moindre idée d'ajout d'indicateur, modification, critique, bug trouvé : partagez-les, c'est apprécié !

à l'avenir je créerais un autre Risk indicator plus polyvalent qui ne sera pas focalisé sur bitcoin en weekly. (cet indicateur est tout de même utilisable sur d'autre actif et timeframe)

REMERCIEMENT :

à Benjamin Cowen pour m'avoir inspiré avec son Bitcoin Risk metric

à Lazybear pour son Wavetrend Indicator et globalement tout les scripts qu'il partage

à Mabonyi pour son script Bitcoin Logarithmic Growth Curves & Zones

à VuManChu pour son VMC Cypher B Divergence

à l'équipe Trading view pour avoir développé TV et PineScript

Et à toute la communauté pour tous les codes publiés qui m'ont permis de progresser et de créer ce script

Position Sizing CalculatorThis is an intuitive risk management tool with a minimalist design.

This calculator will determine your position size per trade, profit, loss, risk/reward ratio and leverage if any.

It will calculate your leverage if you are trading financial instruments e.g. Mini Futures , Turbo Warrants etc. that have a financing level.

Tip: Use this as a complement to the Long/Short Position tool.

Provide the following inputs to get a calculation:

- Position type

- Account balance

- Risk per trade percentage

- Financing level (if any for leveraged instruments), else let it be 0

- Entry price

- Target price

- Stopp loss price

You can also choose the color of the output text, its background and position in the chart window.

Enjoy!

Risk AssistAs the profit level increases, the amount of profit taking required to avoid risk asymptotically reaches zero.

This indicator displays the % of the established position required to exit in order to ensure the trade is not a loss if the stop is hit.

Values in green (at or below 100%) indicate a winning position.

Values in red (above 100%) indicate a losing position.

Alert Examples:

If you are intent on "selling half" to avoid risk, you can set an alert on the value of this indicator for 50.

If you are intent on "selling a 3rd" to avoid risk, you can set an alert on the value of this indicator for 33.3.

Market Risk IndicatorThere are many tools for swing traders. Position traders have not as much, perhaps because they live in the fringe zone between fundamental analysis and trend following.

In order to bridge this gap between fundamental analysis and technical analysis on large timeframes, we decided to work on building a market indicator that assesses its risk and quantifies it on a single dimension number.

The challenge is to consider as input different assets, that individually are themselves often market driving forces, and collectively, more often than not, are sufficient to determine the market status quo.

We came up with DXY , US10Y , HYG and WTI. The latter, the bigger the better; the former, vice versa.

Each asset is evaluated against its recent max/min range, percentually. The positive ones add up and vice versa.

This is still ongoing work. the math and code are simple. the heart of the matter is selecting the proper assets and processing them even better.

Thank you.

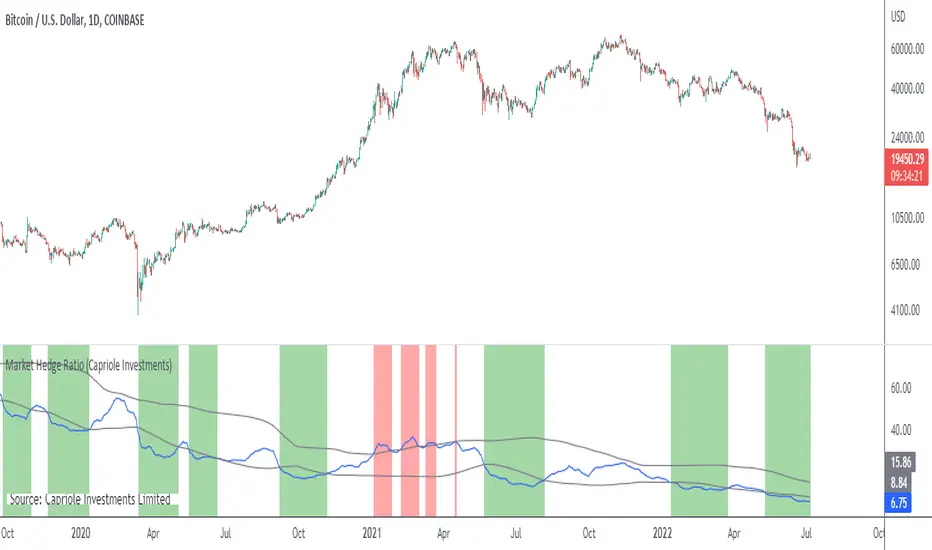

Market Hedge RatioRatio of crypto (total, Bitcoin, or Ethereum market cap) to major stable coins.

A low ratio suggests a lot of people are sitting in cash (sidelined if crypto rallies).

A high ratio suggests possible demand saturation.

Modified Mannarino Market Risk IndicatorThis indicator is meant to give an overall indication of risk and a very basic implementation of the modified mannarino market risk indicator. I take no credit for the original formula, and just decided to hack this together so that it could be useful to the community

Value-at-Risk Value-at-Risk is a risk measurement tool widely used by banks and institutions.

This script uses historical simulation method for the calculation of VaR. The default settings are 250-days period. 1 percentile (or 99 percentile confidence level.)

This means the daily loss for the past 250 days should not exceed the risk measure 99% of the time.

traders can calculate the desired level of risk by converting the timeframe OR by multiplying the square root (expected holding period) to find out the VaR value for 5 days, 25 days, 250 days etc.

Do take note that the default assumes a long position, if you are taking a short position, the percentile value has to be adjusted accordingly (to find the worst 1 percent loss for shorts will require changing the input to 99)

SignalsThis script allows you to calculate position size, and future profit, loses.

- You can add 3 target values and 1 stop loss

- Optionally you can display table, position it as you like, and see risk ratio

Plans:

- add profit loss to the labels

BTC Risk Metric - Estimates the risk of BTC price versus the USD

- To be used on the daily timeframe

- Works best on a BTC pair that has a lot of bars, e.g. The Bitcoin All Time History Index

- 0 is the lowest risk, 1 is the highest risk

- Historically, buying when the risk was low and selling when the risk was high would have yielded good ROI

- The risk bands are 0.1 in width and are highlighted on the plot

Typical Strategy:

- weighted DCA into the market when risk <0.5, do nothing between 0.5-0.6 and weighted DCA out of the market when risk >0.6

- x = buy amount per DCA interval

- y = 1/10th total BTC held by the user

- if 0 ≤ Risk < 0.1 then buy 5x

- if 0.1 ≤ Risk < 0.2 then buy 4x

- if 0.2 ≤ Risk < 0.3 then buy 3x

- if 0.3 ≤ Risk < 0.4 then buy 2x

- if 0.4 ≤ Risk < 0.5 then buy x

- if 0.5 ≤ Risk < 0.6 then do nothing

- if 0.6 ≤ Risk < 0.7 then sell y

- if 0.7 ≤ Risk < 0.8 then sell 2y

- if 0.8 ≤ Risk < 0.9 then sell 3y

- if 0.9 ≤ Risk ≤ 1.0 then sell 4y

Position size FX and CryptoThis indicator I am using to calculate the position size to order for Forex and Crypto Future

Risk adjusted returns data (volatility optimised)RAR - risk adjusted returns. This methodology could be helpful in portfolio creation and position size risk management. We can set our own preference of risk tolerance via the X variable which is the exponent of volatility in our calculations. This gives an unlimited set of example portfolios on a given time-frame that can be sorted from return oriented to volatility reduction oriented as X increases. RARs are to be compared against eachother.

BTCUSD Risk Oscillator- To be used with the BTCUSD All Time History Index (on the daily)

- Estimates the current risk of BTCUSD

- The risk model oscillates between 0 and 1 (0 is the lowest risk, 1 is the highest)

- Historically, buying when the risk is low and selling when the risk is high yields good ROI

- User inputs generally do not need to be changed, they are used to create integers for the normalization process