Relative Strength ComparisonThis script plots the ratio between a ticker and the selected index. Currently, I have US equities indexes listed + BTC. It's a great way to check for relative strength, determine if absolute highs relative to the ratio are being made, etc.

Additionally, optional comparison of the RSI is included. I was just testing something out but figured I'd leave in here because why not. If you use this, enable the 1.0 line.

Script is a bit slow, will try to optimize eventually.

SPX (S&P 500 Index)

Improved Bollinger Swing Strategy Stock NasdaqThis is an improved bollinger band strategy adapted to Nasdaq Index/Stocks.

The new update include a multiple logic calculation BB adapted for long and short, together with a risk management using movement in %.

Rules for entry

For long we have a crossover between the close and the lower band from the bb

For long we have a crossover between the close and the upper band from the bb

Rules for exit

We exit when we either find a reverse condition, or if we hit the take profit/stop loss levels.

If you have any questions, let me know !

Stock trending strategy This is a long only strategy designed maily for stock markets and futures. In general it works best with 1h, however it can be optimized with other timeframes as well.

Components:

VWAP

MACD histogram

EMA 9

Rules for entry

Long :

For VWAP: close is above the vwap daily

EMA: close is above the moving average

MACD histogram is above 0

Short:

For VWAP: close is belowthe vwap daily

EMA: close is below the moving average

MACD histogram is below 0

Rules for exit

This strategy does not have any risk management inside. Instead it exits whenver it receives an opposite signal form the original one used for entry.

If you have any questions let me know !

Ichimoku with MACD/ CMF/ TSIThis is a very powerful trend strategy designed for markets such as stocks market , stock index and crypto.

For time frames I found out that 1h seems to do the trick.

Components:

Ichimoku full pack

MACD histogram

CMF oscillator

TSI oscillator

Rules for entry

Long :

For Ichimoku:Tenkan part of cloud is bigger than kijun, Chikou is above 0 , close of a candle is above the Senkou

MACD histogram is above 0

CMF oscillator is positive and bigger than 0.1

TSI oscillator is above 0

Short:

For Ichimoku:Tenkan part of cloud is smaller than kijun, Chikou is below 0 , close of a candle is belowthe Senkou

MACD histogram is below 0

CMF oscillator is negative and below -0.1

TSI oscillator is below 0

Rules for exit

This strategy does not have any risk management inside. Instead it exits whenver it receives an opposite signal form the original one used for entry.

If you have any questions let me know !

Vix Jump for Selling Puts or Buying CallsThis script aims to identify optimal times when to write Puts for premium, for example using the SPX Weeklies model or simply buying Calls. Not perfect but provides some additional confidence when playing Puts on SPX or the Wheel on SPY.

What it does:

We compare current VIX with a lookback VIX for X% delta. If there is a jump of say 20% over a defined period then that would indicate an opportunity to sell Puts, run a straddle or buy Calls. We use VVIX as a check to stop to many false positives ie VVIX falls of faster than VIX.

You can also use this loosely as a bottom finder.

SectorsThis script attempts to show the relative strength of the 11 sectors in the SPX, which can be accomplished in three ways:

1. Sectors - displays all sector indices as they appear normally

2. Sector Relativity - displays each sector divided by the sum of the other 10 sectors

3. Sector Alpha - displays the alpha of each sector as compared to the sum of the other 10 sectors

I have seen some other iterations of this script that compare each sector to the SPX as a whole, a couple problems with that:

1. SPX sector weightings are unequal and change quarterly, meaning you will get an inaccurate depiction of relative sector strength across time.

2. Even if using an equal-weight SPX, you would be comparing a sector to itself as all 11 sectors are included in the SPX, not just the complementary 10 you are looking to compare one sector to.

For more information on the sectors in the SPX or the calculation of Alpha, visit the links at the top of the script.

*Includes an option for repainting -- default value is true, meaning the script will repaint the current bar.

False = Not Repainting = Value for the current bar is not repainted, but all past values are offset by 1 bar.

True = Repainting = Value for the current bar is repainted, but all past values are correct and not offset by 1 bar.

In both cases, all of the historical values are correct, it is just a matter of whether you prefer the current bar to be realistically painted and the historical bars offset by 1, or the current bar to be repainted and the historical data to match their respective price bars.

As explained by TradingView,`f_security()` is for coders who want to offer their users a repainting/no-repainting version of the HTF data.

VIX Implied Move Bands for ES/Emini futuresThis script uses the close of the VIX on a daily resolution to provide the 'implied move' for the E-mini SP500 futures. While it can be applied to any equity index, it's crucial to know that the VIX is calculated using SPX options, and may not reflect the implied volatility of other indices. The user can adjust the length of the moving average used to calculate the bands, the window of days used to calculate the implied move, and the multiplier that effects the width of the bands.

Nico's SPX Dynamic ChannelsTest of dynamic channels and some statistics made by hand.

This indicator was done specifically for the S&P500 index.

As you can see, below the 125 EMA there's a lot more volatility than in the upside. I've made some kind of a dynamic linear regression of the lows and the highs.

I've chosen the MA that best fits the SPX, and then calculated in Excel the percental mean and SDs of most important peaks and valleys that I've chosen in comparison to the 125 MA. This lead to the green, orange and red zones. BUT, I've calculated the peaks and valleys separately, as I assumed that a bear market and crashes have way more volatility than bull markets. That's why the difference between the upper and the lower channels.

The neutral blue zone is composed by an upper EMA of the highs and lower EMA of the lows. No MA in this script uses the close price as a source.

This MA makes sense because it represents a semester of trading, for this particular asset.

Backtest results

It's also interesting to try it here too, as it has a little bit more of data:

SPCFD:SPX

As it's not a trading system, I have no batting average nor ratios for this.

Still, the measures of the peaks and valleys are very accurate and repeat themselves over and over again. The results were:

3rd resistance: 12.88%

2nd resistance: 10.12%

1st resistance: 7.36%

1st support: -6.42%

2nd support: -14.8%

3rd support: -23.18%

All referred to the mean, which is the 125 EMA zone.

After the 1950's works like magic, but not before. You will see that it doesn't work in the great depression and it's crash.

How to use this indicator

Green = First grade support/resistance .

Orange = Second grade support/resistance . Caution.

Red = Third grade support/resistance . High chances of mean reversal.

Blue zone = This is the neutral zone, where the prices are not cheap nor expensive.

Often in a trending market, the price will have the blue zone as it's main support and when trending the price will stick to the green MA.

When the price touches the orange MA, the most probable is that it will return to the green MA.

If the price touches the red zone, there's a high chance that this is a big turning point and it will reverse to the mean (green or blue zone).

Imagine you've bought each time the price touched the red support, check that and you'll start liking this indicator. I think it is a great entry point for investors. The red resistance is good too, but of course it works for a short period of time.

I've backtested this indicator since the beginning of the dataset and it works like magic, but ONLY for the SPX index (spot price).

Leave a comment or some coins if you like it!!!

(I've posted it before like an analysis, not as a script, my bad)

Doms 0dte/hassan conversion v2 Hello Guys

This is a reupload!

The 0dte is for options trading and is used for the main 1 to 0 odte strategy!

It uses volume, sector and tik analysis in order to give an understanding of looking which way to play.

The next version will look at correlations between the es! Feel free to point out bugs and reach out as I want this to grow into something way stronger!

Higher vs Lower Pivots overlayA simple script that I made that draws lines between the high and low pivots. The color of the line define if the pivot is higher or lower than the previous pivot. The main thing to tune is the pivot look back vs look ahead, which are the same params used by the tradingview pivot indicator. There are several other params you can tweaks to get the look you want.

Equity Index Extended HoursHighlights the extended hours/Globex session for US Equity Index Futures.

Cyclic Smoothed RSI with Divergence IndicatorI created a single indicator that combines 1) Cyclic Smoothed RSI and 2) the Divergence indicator (bull, bear). It is very handy when used with the MACD and crossover points.

Please refer to for info on how to use the cRSI indicator.

Info on the chart.

1) Red dotted lines = cRSI crossed back from overbought and crossover in MACD

2) Red solid lines = Bear divergence and crossover in MACD

3) Green dotted lines = cRSI crossed back from oversold and crossover in MACD

4) Green solid lines = Bull divergence and crossover in MACD

5) Black transition = cRSI crossover but NO crossover in MACD

Fama-French 3 Factor ModelFama-French 3 Factor Model

Extension of the Capital Asset Pricing Model (CAPM)

CAPM

Ra = Rfr +

where,

Ra = Return of the Asset

Rfr = Risk-Free Rate

βa = Beta Coefficient of the Asset

Rm - Rfr = Market Risk Premium

Fama-French 3 Factor

r = rf + β1*(rm - rf) + β2(smh) +β3(hml)

r = Expected rate of return

rf = Risk-free rate

ß = Factor’s coefficient (sensitivity)

(rm – rf) = Market risk premium

SMB (Small Minus Big) = Historic excess returns of small-cap companies over large-cap companies

HML (High Minus Low) = Historic excess returns of value stocks (high book-to-price ratio) over growth stocks (low book-to-price ratio)

Small is set to $EWSC

Invesco S&P SmallCap 600® Equal Weight ETF

Big is set to $EQLW

Invesco S&P 100 Equal Weight ETF

High is set to $IUSV

iShares Core S&P US Value ETF

Low is set to $IUSG

iShares Core S&P US Growth ETF

returns selections

'returns'

'logarithmic returns' (use for realized (historical) returns)

'geometric returns' (compounded returns)

risk-free rate selections:

$DTB3

$DGS2

$DGS5

$DGS10

$DGS30

tf = primary time-frame

rtf = reference time-frame

Realized Variables for Options ComparisonThese variables can be used in comparison with the implied volatility of options.

Variables:

Realized Volatility

mathematical notation lowercase 'sigma'

Realized Variance

mathematical notation lowercase 'sigma' squared

Realized Beta

mathematical notation lowercase 'beta'

Timeframes:

Yearly = 250 or 365

Quarterly = 50 or 90

Monthly = 20 or 30

Important Note:

Options Contract Expiry = barmerge.lookahead_on

"Merge strategy for the requested data position. Requested barset is merged with current barset in the order of sorting bars by their opening time. This merge strategy can lead to undesirable effect of getting data from "future" on calculation on history. This is unacceptable in backtesting strategies, but can be useful in indicators."

[ All other timeframes barmerge.lookahead is disabled.

SPX-VIX Intraday DivergenceAs a long-term buyer/short-seller, you will always find different ways to enter the market , moving average crossovers, breakouts , overbought/oversold conditions being some of the classy methods. However, they are decreasingly effective... 😢

Recently I have realized that analysis beyond the technical indicators will bring trading to the next level because I will be able to confirm my trading signals without relying too much on basic price actions and patterns which are easily manipulated by big banks and institutions. 👍

Today I will introduce you to my divergence indicator making use of SPX and VIX. Unlike MacD or RSI divegence , which would involve normative judgement , it will take account of the unusual move by SPX alongwith the VIX , to the exploit chances that options market, where most experienced investors participated in has a preceding insight into the equity market about the upcoming moves.

I have divided signals into two groups.

Bullish divergence - SPX Down , VIX also Down 👇

Bearish divergence - SPX Up , VIX also Up 👆

I hope this script will enable us to take advantage of the options market activities , to provide a REAL divergence signal, and be used coupled with our own chart patterns or other price signals, and more importantly to score more and more winning trades!!!

If you want more useful scripts from me, please like and share my posts. And don't forget to follow my account to grab the latest ideas and tools! 😘

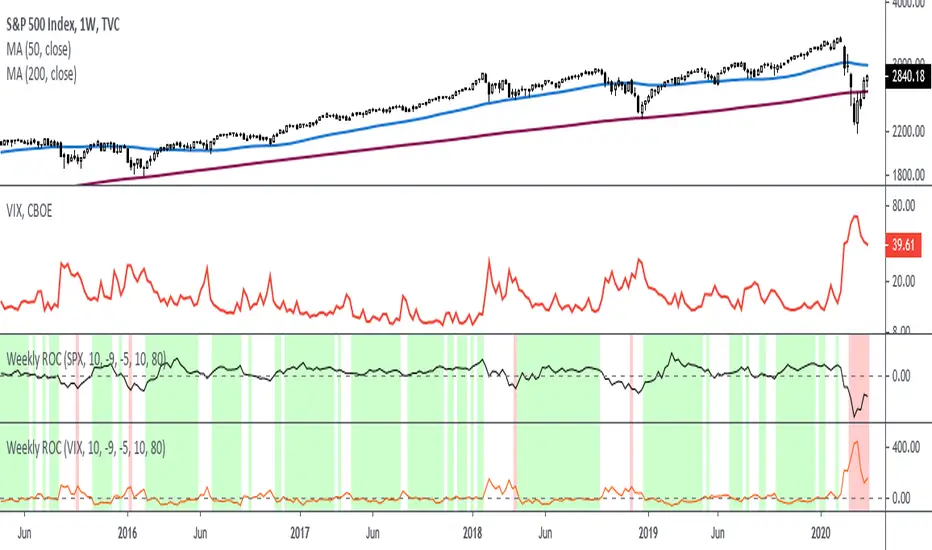

Rate Of Change - Weekly SignalsRate of Change - Weekly Signals

This indicator gives a potential "buy signal" using Rate of Change of SPX and VIX together,

using the following criteria:

SPX Weekly ROC(10) has been BELOW -9 and now rises ABOVE -5

*PLUS*

VIX Weekly ROC(10) has been ABOVE +80 and now falls BELOW +10

The background will turn RED when ROC(SPX) is below -9 and ROC(VIX) is above +80.

The background will turn GREEN when ROC(SPX) is above -5 and ROC(VIX) is below +10.

So the potential "buy signal" is when you start to get GREEN BARS AFTER RED - usually with

some white/empty bars in between...but wait for the green. This indicates that the volatility

has settled down, and the market is starting to turn up.

This indicator gives excellent entry points, but be careful of the occasional false signals.

See Nov. 2001 and Nov. 2008, in both cases the market dropped another 25-30% before the final

bottom was formed. Always have an exit strategy, especially when buying in after a downtrend.

How I use this indicator, pretty much as shown in the preview. Weekly SPX as the main chart with

some medium/long moving averages to identify the trend, VIX added as a "Compare Symbol" in red,

and then the Weekly ROC signals below.

For the ROC graphs, you can show SPX+VIX together, SPX alone, or VIX alone. I prefer to display

them separately because they don't scale well together (VIX crowds out the SPX when it spikes).

Background color is still based on both SPX/VIX together, regardless of which graph is shown.

Note that there is no VIX data available on Trading View prior to 1990, so for those dates the

formula is using only ROC(SPX) and the assigned thresholds (-9 and -5, or whatever you choose).

Relative Strength(RSMK) + Perks - Markos KatsanosIf you are desperately looking for a novel RSI, this isn't that. This is another lesser known novel species of indicator. Hot off the press, in multiple stunning color schemes, I present my version of "Relative Strength (RSMK)" employing PSv4.0, originally formulated by Markos Katsanos for TASC - March 2020 Traders Tips. This indicator is used to compare performance of an asset to a market index of your choosing. I included the S&P 500 index along side the Dow Jones and the NASDAQ indices selectively by an input() in "Settings". You may comparatively analyze other global market indices by adapting the code, if you are skilled enough in Pine to do so.

With this contribution to the Tradingview community, also included is MY twin algorithmic formulation of "Comparative Relative Strength" as a supplementary companion indicator. They are eerily similar, so I decided to include it. You may easily disable my algorithm within the indicator "Settings". I do hope you may find both of them useful. Configurations are displayed above in multiple scenarios that should be suitable for most traders.

As always, I have included advanced Pine programming techniques that conform to proper "Pine Etiquette". For those of you who are newcomers to Pine Script, this script may also help you understand advanced programming techniques in Pine and how they may be utilized in a most effective manner. Utilizing the "Power of Pine", I included the maximum amount of features I could surmise in an ultra small yet powerful package, being less than a 60 line implementation at initial release.

Unfortunately, there are so many Pine mastery techniques included, I don't have time to write about all of them. I will have to let you discover them for yourself, excluding the following Pine "Tricks and Tips" described next. Of notable mention with this release, I have "overwritten" the Pine built-in function ema(). You may overwrite other built-in functions too. If you weren't aware of this Pine capability, you now know! Just heed caution when doing so to ensure your replacement algorithms are 100% sound. My ema() will also accept a floating point number for the period having ultimate adjustability. Yep, you heard all of that properly. Pine is becoming more impressive than `impressive` was originally thought of...

Features List Includes:

Dark Background - Easily disabled in indicator Settings->Style for "Light" charts or with Pine commenting

AND much, much more... You have the source!

The comments section below is solely just for commenting and other remarks, ideas, compliments, etc... regarding only this indicator, not others. When available time provides itself, I will consider your inquiries, thoughts, and concepts presented below in the comments section, should you have any questions or comments regarding this indicator. When my indicators achieve more prevalent use by TV members, I may implement more ideas when they present themselves as worthy additions. As always, "Like" it if you simply just like it with a proper thumbs up, and also return to my scripts list occasionally for additional postings. Have a profitable future everyone!

TradersAI_UTBotCREDITS to @HPotter for the orginal code.

CREDITS to @Yo_adriiiiaan for recently publishing the UT Bot study based on the original code -

I just added some simple code to turn it into a strategy. Now, anyone can simply add the strategy to their chart to see the backtesting results!

While @Yo_adriiiiaan mentions it works best on a 4-hour timeframe or above, I am happy to share that this seems to be working on a 15-minute chart on e-mini S&P 500 Index (using the KeyValue setting at 10)! You can play around with the different settings, and may be you might discover even better settings.

Hope this helps. Btw, if any of you play with different settings and discover great settings for a specific instrument, please share them with the community here - it will be rewarded back multiple times!

(JS)S&P 500 Volatility Oscillator For Options 2.0I am going to start taking requests to open source my indicators and they will also be updated to Version 4 of Pinescript.

I added some features to the original code such the ability to smooth the oscillator and select the look back periods for the historical volatility.

Link to original:

Original post:

"The idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX ). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX ) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility . (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M ) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX , SPY , even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Feb 17, 2019

Release Notes: Cosmetic update for a much cleaner look:

-Replaced the "HIGH IV" with a simlple "H"

-Now the white line is constantly showing you the relationship between VIX and VIX3M - when VIX is greater than VIX3M the background still goes red

-However, now when VIX drops below Historical Volatility, the background is bright green

-When both above are true - it's dark green

-The Average True Range on the bottom is now a series of crosses"

A.I.Driven TradersAI Model Trades for 20190612The entry and exit levels here are NOT derived from any specific indicator but are coming from our A.I. driven proprietary models.

This is an attempt at exploring the trading community here at TradingView and sharing our daily trading plans published at our site with the community here in the form a Pine Script - just starting and learning this platform. Please help point out any obvious errors or gotchas committed in the scripts. Thanks and have a great trading day!

**** The Trading Plan Published for today ****

>>>> Medium-Frequency Models: <<<<< For today, Wednesday 06/12, our medium-frequency models indicate using the 2895 as a pivot point - opening a long on a break above 2895, and opening a short on a break below 2895 (wait for a close on at least a five minute chart to determine the break), both sides with a 9-point trailing stop.

Note: For the trades to trigger, the breaks should occur during the regular session hours starting at 9:30am ET. By design, these models do NOT open any new positions after 3:45pm. Only one open position at any given time.

>>>>> Aggressive Intraday Models: <<<<< For today, Wednesday 06/12, our aggressive intraday models indicate going long on a break above 2892 or 2875 with an 6-point trailing stop, and going short on a break below 2887 or 2878 with an 8-point trailing stop.

Note: For the trades to trigger, the breaks should occur during regular session hours starting at 9:30am ET. Due to the intraday nature of these aggressive models, they indicate closing any open trades at 3:55pm and remaining flat into the session close. No opening of new positions after 3:45pm. Only one open position at any given time.

Kal’s MTF ADX Rangoli RollerKaly MTF ADX Rangoli Roller is a method/study for finding trending stocks, indexes and cryptocurrencies using two different data periods (10, 5) of ADX Overlap over different time-frames (10m, 1H, 4H, 1D, 1W, 1M). In the study, I used 5-Period ADX for all mentioned time-frames. You may use 10-Period ADX for lower time-frames especially 10m and 1H.

Sample Image of the pinescript code(at the end of this post) in Tradingview looks as follows:

Note: Kal's MTF ADX Rangoli Roller is the lower Plot. The upper plot is KAL’s ADX Overlap Technical Study with MACD Filter( )

Description:

----------------

In the study plot, the lowest row is 10m, row above is 1H, row above is 4H, then 1D, then 1W and highest row is 1M

Lime(Bright Green) dot implies Trending Uptrend for that time-frame (first phase)

Green dot implies Trending Uptrend for that time-frame (second phase near exhaustion)

Red dot implies Trending Downward for that time-frame (first phase)

Maroon dot implies Trending Downward for that time-frame (second phase near exhaustion)

Lime cross implies Strong Trending Uptrend for that time-frame (first phase)

Green cross implies Strong Trending Uptrend for that time-frame (second phase near exhaustion)

Red cross implies Trending Strong Downward for that time-frame (first phase)

Maroon cross implies Trending Strong Downward for that time-frame (second phase near exhaustion)

Yellow is ‘Squeeze On’ setting. During the squeeze period, the ADX signals are almost always ineffective. One may wait and watch over during this time. Once the Squeeze is released (i.e. no longer yellow), the trend corresponds to the color of the dots and crosses.

Black is CRSI Overbought condition for that time-frame. It’s best to wait and research for possibility of trend reversal because

1. Profit-booking/trimming happens after CRSI Overbought condition.

2. Large Short-sellers may take huge positions during this time pushing the stock prices up.

White is CRSI Oversold condition for that time-frame. It’s best to wait and research for possibility of trend reversal because

1. Profit-booking/trimming happens after CRSI Oversold conditions.

2. Large buyers may take huge positions during this time pushing the stock prices down.

I am a disabled man. Therefore, I am not able to write in detail here today. More Details will follow as time permits. Please let me know if I am missing anything…

Legal Disclaimer: I published here so I get replies from fellow viewers to educate myself and for my daily expenses. Hence, if anyone uses this script for making their decisions, I am not responsible for any failures incurred.

Safe Trading!

Kal Gandikota

PS: If you found this script interesting and edifying please follow and upvote.

PS2: Please kindly donate for my daily expenses (atleast as you would on streets) at the following addresses:

BTC Wallet: 1NeDC1GvpFa49DFLuT1v28ohFjqtoWXNQ5

ETH Wallet: 0x35e557F39A998e7d35dD27c6720C3553e1c65053

NEO Wallet: AUdiNJDW7boeUyYYNhX86p2T8eWwuELSGr

PS3: For more information on ADX and CRSI, please 'Google' or search here yourself.

PS4: This study is intended for research in creating automated Python Trading Systems using Pandas( steemit.com ).

Screenshots of the pinescript code looks as follows:

10minute Screenshot of Kal's MTF ADX Rangoli Roller (Above)

1 Hour Screenshot of Kal's MTF ADX Rangoli Roller (Above)

4 Hour Screenshot of Kal's MTF ADX Rangoli Roller (Above)

1 Day Screenshot of Kal's MTF ADX Rangoli Roller (Above)

1 Week Screenshot of Kal's MTF ADX Rangoli Roller (Above)

1 Month Screenshot of Kal's MTF ADX Rangoli Roller (Above)

@WACC Volatility Weighted PUT/CALL Positions [SPX]This indicator is based on Volatility and Market Sentiment. When volatility is high, and market sentiment is positive, the indicator is in a low or 'buy state'. When volatility is low and market sentiment is poor, the indicator is high.

The indicator uses the VIX as it's volatility input.

The indicator uses the spread between the Call Volume on SPX/SPY and the Put Volume.

This is pulled from CVSPX and PVSPX.

When volatility and put/call reaches a critical level, such as the levels present in a crisis or a sell off, the line will be green. See Sept 2015, 2008, and Feb 2018.

This level can be edited in the source code.

As the indicator is based on Put/Call, the indicator works best on larger time frames as the put/call ratio becomes a more discernible measure of sentiment over time.

IV/HV ratio 1.0 [dime]This script compares the implied volatility to the historic volatility as a ratio.

The plot indicates how high the current implied volatility for the next 30 days is relative to the actual volatility realized over the set period. This is most useful for options traders as it may show when the premiums paid on options are over valued relative to the historic risk.

The default is set to one year (252 bars) however any number of bars can be set for the lookback period for HV.

The default is set to VIX for the IV on SPX or SPY but other CBOE implied volatility indexes may be used. For /CL you have OVX/HV and for /GC you have GVX/HV.

Note that the CBOE data for these indexes may be delayed and updated EOD

and may not be suitable for intraday information. (Future versions of this script may be developed to provide a realtime intraday study. )

There is a list of many volatility indexes from CBOE listed at:

www.cboe.com

(Some may not yet be available on Tradingview)

RVX Russell 2000

VXN NASDAQ

VXO S&P 100

VXD DJIA

GVX Gold

OVX OIL

VIX3M 3-Month

VIX6M S&P 500 6-Month

VIX1Y 1-Year

VXEFA Cboe EFA ETF

VXEEM Cboe Emerging Markets ETF

VXFXI Cboe China ETF

VXEWZ Cboe Brazil ETF

VXSLV Cboe Silver ETF

VXGDX Cboe Gold Miners ETF

VXXLE Cboe Energy Sector ETF

EUVIX FX Euro

JYVIX FX Yen

BPVIX FX British Pound

EVZ Cboe EuroCurrency ETF Volatility Index

Amazon VXAZN

Apple VXAPL

Goldman Sachs VXGS

Google VXGOG

IBM VXIBM