OPEN-SOURCE SCRIPT

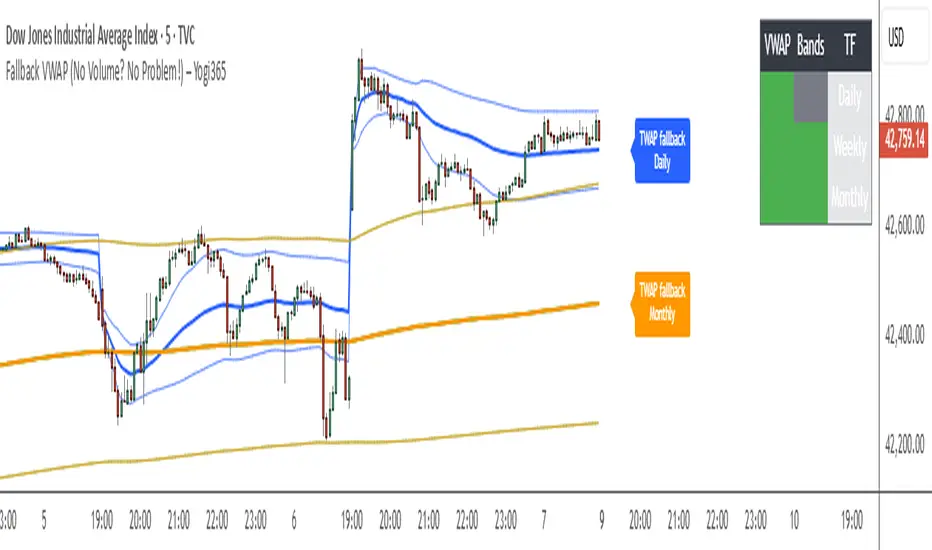

Fallback VWAP (No Volume? No Problem!) – Yogi365

Fallback VWAP (No Volume? No Problem!) – Yogi365

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

Script open-source

Dans l'esprit TradingView, le créateur de ce script l'a rendu open source afin que les traders puissent examiner et vérifier ses fonctionnalités. Bravo à l'auteur! Bien que vous puissiez l'utiliser gratuitement, n'oubliez pas que la republication du code est soumise à nos Règles.

Clause de non-responsabilité

Les informations et publications ne sont pas destinées à être, et ne constituent pas, des conseils ou recommandations financiers, d'investissement, de trading ou autres fournis ou approuvés par TradingView. Pour en savoir plus, consultez les Conditions d'utilisation.

Script open-source

Dans l'esprit TradingView, le créateur de ce script l'a rendu open source afin que les traders puissent examiner et vérifier ses fonctionnalités. Bravo à l'auteur! Bien que vous puissiez l'utiliser gratuitement, n'oubliez pas que la republication du code est soumise à nos Règles.

Clause de non-responsabilité

Les informations et publications ne sont pas destinées à être, et ne constituent pas, des conseils ou recommandations financiers, d'investissement, de trading ou autres fournis ou approuvés par TradingView. Pour en savoir plus, consultez les Conditions d'utilisation.