SMA-Extendido-Indicador por NeilDescription:

Indicator that identifies entry and exit operations, using 3 moving averages and 5 strategies. New strategies are implemented such as the prediction of closing operations, independent of the events that justify entry operations.

How does it work:

1) Long strategy: if SMA5 crosses up to SMA200 and SMA200 is bullish , a buy operation begins, if SMA5 crosses down to SMA200 and SMA200 is bearish , a sale begins.

2) Short strategy with smooth filtering of operations: if SMA5 crosses up to SMA20 and SMA20 is bullish and (SMA5 are above SMA200) a buy operation is initiated. If SMA5 crosses down to SMA20 and SMA20 is bearish and (SMA5 are below SMA200) a sell trade is initiated

3) Short strategy with strong filtering of operations: if SMA5 crosses up to SMA20 and SMA20 is bullish and (SMA5 and SMA20 are above SMA200 and SMA200 is bullish ) a buy is initiated, in other words, buy operations occur only if SMA5 and SMA20 are above SMA200; if SMA5 crosses down to SMA20 and SMA20 is bearish and (SMA5 and SMA20 are below SMA200 and SMA200 is bearish ) a sell is initiated, that is, sell operations occur only if SMA5 and SMA20 are below SMA200

4) Short strategy without filtering operations: if SMA5 crosses up to SMA20 and SMA20 is bullish , a buy is initiated (the location of MA200 does not matter). If SMA5 crosses down to SMA20 and SMA20 is bearish , a sell is initiated (it does not matter where the MA200 is located)

5) Prediction of closing operations: the algorithm evaluates potential closing operations differently and considers the following rules: If there is an active buy trade and SMA5 crosses down to SMA20, we close the current buy (the location of the SMA200 does not matter). If there is an active sell trade and SMA5 crosses up to SMA20, we close the sale in progress (the location of the SMA200 does not matter)

How to use it:

Press the "Indicators" option, go to the "Public Librarian" segment, write the name "SMA-Extendido-Indicador por Neil", double-click on the record in question and you will have it added in your work panel, now, just It remains to be used to identify the inputs and outputs and you can do it visually or by defining the automatic notification alerts.

ATR

Rosebud Trend Backtest [DepthHouse]*Past Performance Does Not Guarantee Future Results*

*Strategy created for backtesting purposes only.

*Backtesting assesses the viability of a trading strategy or pricing model by discovering how it would have played out retrospectively using historical data.

* Please be sure to read all updates below as the information below could change with future updates.

Rosebud Trend Indicator uses complex range calculations to easily detect trend changes, critical support and resistance levels, and even aid in spotting reversals. The Critical Support & Resistance Zones are plotted via the red and green cloud. This cloud not only visually displays the expected trend direction but often acts as major support and resistance zones. The outer band measures the expected range in which the assets trade over longer periods of time.

The Rosebud Trend Backtest combines the calculations of the ATR Auto Oscillator & the Rosebud Trend Indicator to demonstrate backtest performance.

// Settings //

Users can switch the ‘ Trend Sensitivity ’ between ‘ Low ', ' Med ', and ‘ High ’ to increase or decrease the rate at which the cloud changes.

By altering the S/R Band Thickness users can furthermore increase or decrease the rate at which a trend changes by altering the thickness of the cloud. Default is .50 however this can be lowered if needed.

Bar colors are generated by a combination of Rosebuds primary function and our ATR AUTO Oscillator base functions. Users have 3 bar color options to select from: Simple, Complex, and Off.

Simple: Bars colors alternate between shades of red and green based on the trend direction and the ATR Auto strength. The stronger the shade, the stronger the trend.

Complex: This adds a few extra variables to the script which generates a more complex bar color display. Using this option, Rosebud will generate light red bars in a bull trend if downward movement is strong and vice versa in a bear trend. It also will generate a purple bar if the candle successfully closes above or below the Top & Bottom Range Bands; We call this a range break, and it could be an early sign of strong upward or downward movement.

Off: In case you like to keep things even simpler, this option hides all overlay bar colors.

ATR Options: Used for Light & Strong Entries/Exits // Bar Colors also based on these settings

ATR Smoothed Signal Option: Turns advance smoothing on or off. On will reduce signal noise, while Off could land you that perfect bottom signal with a lower success rate.

ATR Candlestick Length: Default factor for bar color and shape generation, the higher the number the fewer signals that will generate.

ATR Candlestick Smoothing: Default smoothing for the Candlestick Length

Signal Lookback: Adjust the factor at which Bull, Bear, Up, and Down. Lower this to 2 for more signals.

// ⇅ BackTest Settings ⇅ //

Short Trading: Option to see backtest results for both long and short positions. Default is Long Only.

Strategy Entry Options:

Trend Only: Positions are entered right as there is a cloud trend change.

Light Entry: This enters a trade as soon as there is a breakout or breakdown signal generated from the ATR settings.

Strong Entry: Multiple conditions must be met; Price action must be near the Trend Base and must receive either a bullish or bearish crossover in the oversold or overbought range of the ATR Settings.

Strategy Exit Options:

Trend Only: Exits all positions after there is a primary trend change.

Light Exit: Exits a user set percentage of open positions when the ATR generates a breakdown or breakout. Will continue to do this at each occurrence. Presets are built in to keep these from triggering too often in volatile conditions.

Strong Exit: Exits a user set percentage of open positions when the ATR generates a bullish or bearish crossover in the overbought or oversold ranges. Will continue to do this with each occurrence. Presets are built in to keep these from triggering too often in volatile conditions.

Profit Points: Exits a set percentage of the position up to 3 times at a user set percentage gap from the entry. Any remaining amount in the position exits upon a trend change.

Profit QTY Percent: Percent of the position to exit when an exit condition triggers. This does not apply to the “Trend Only” exit option.

Profit Percent Gap: Percent gap for Profit Point Exits. Recommend adjusting based on timeframe. See example below.

DCA_PREMIUMOur new indicator tracks trends to create buy and sell alerts, see below how it works.

HOW IT WORKS:

It uses RMA which is the same moving average used by RSI and HMA, they intersect give us an entry signal, be it a buy or sell, as the entry signal the script will color the bars according to the signal.

When a GREEN candle appears, it indicates a large purchase volume and when a PURPLE candle appears, it indicates a large sales volume.

The indicator will alert for entries only according to the trend of the traded asset

FOR EXAMPLE:

I am trading USDJPY in an uptrend, the indicator will only alert me for buy entries, if it applies to downtrend.

DASHBOARD:

Our dashboard indicates the volatility of the traded asset, the short-term trend and the trade signal.

HOW TO USE:

Choose the asset you want to trade and, in the settings, change the time period you want for your trading style, for example: Swing Trade, Day Trade or Position.

See regions with large trading volumes indicating price manipulation or just supports and resistances too strong to break.

Chonky Hourly Volatility StatsShows a table of the average volatility per hour of day.

Can inform about the more/less opportune times to trade a particular asset.

Gaps are not accounted for; ranges only consist of high - low.

Use on the hourly time frame only.

Timeweighted Colored VWAP with SlopeHey, traders!

This script calculates the VWAP's change rate against ATR in a number of k-lines. It controls the VWAP line's color based on the average change rate, and it changes its color in a time-weighted way.

1. Calculating vwapValue's rate of change

2. Controlling Line's color based on the average change rate against ATR

3. Calculating average change rate in the past k-lines

K线的数量:计算多少根K线的VWAP值的变化率的平均值,相当于用K线的数量来时间加权

变化率阈值:线条颜色变化的阈值,VWAP值的变化率比这个大或者小时改变颜色,否则延续原来的颜色

Good luck with your trading!

SD - Average True Range v5 - DoubleSD - Average True Range - Daily Weekly Monthly Yearly v5

It gives ATR intervals as 4 hours, daily, weekly, monthly and yearly. The expectation is to fill the ATR targets within the specified ranges. It can be used to determine target points on charts with a clear direction on the train.

Unlike the previous version, it is provided to use 2 different periods in the same indicator.

Note: Developed based on the source codes of the original SD ADR indicator.

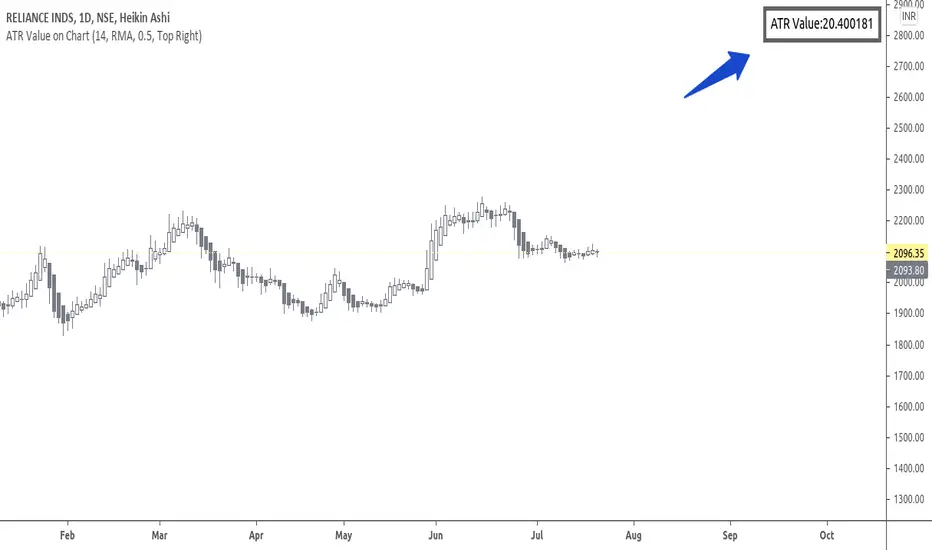

ATR Value on ChartHi Friends & TradingView community.

Greetings to you.

Many traders use ATR to set Stop loss.

The built in ATR indicator plots the ATR values as a line. However, many traders do not want the ATR to be plotted on their charts, but are only interested in the ATR value as such.

This script does that - it just prints the latest ATR with your set Multiplier value on the chart. I have used the built-in ATR indicator and made necessary additions to the code.

I hope this script proves useful to traders.

Queries / feedback welcome.

All the best.

Kifier's MFI/STOCH Hidden Divergence/Trend BeaterMFI/STOCH Hidden Divergence/Trend Beater

General Idea:

My premise around this strategy was to make a general strategy for crypto that would help out with finding entry positions for when you’re bullish on a crypto and want to hold on for a while, and at the same time avoiding massive drops. Essentially a way to mix long term/ swing trading; I somewhat achieved my goal however it still requires a lot of logic tuning of the trend averages.

I’m a huge proponent of volume indicators and coupled with average closing price, I think this gives a really good idea of what is happening with the market. It gives an idea on the market and retail investor sentiment. This generally gives you logical entry positions (Although I don’t know how amazing that will work with all cryptos, there’s a fine line between a good strategy and one that just rides bubble market conditions, some would argue that’s still a success and others not)

How it works:

There are many components to the strategy that try to do different things:

First of all there are two types of entries, a MFI hidden divergence with a STOCH check, essentially it will only fire when a divergence is detected while STOCH is above 50%, however this might be changed in the future as due to the volatile nature of cryptos, the STOCH is not too effective. The second entry is a simple MFI/STOCH trend, if STOCH is above 50% and the trend is detected to be in a trending long, once a MFI crossover over the 50% line is detected an entry is placed, this is designed to get out profit where the divergence would otherwise be less accurate during strongly trending conditions.

-MFI is a great indicator, as a volume weighted momentum indicator I find it the most accurate of all, the STOCH however is a great indicator to get a general picture of simple market conditions and can filter out the emotional noise of retail investors.

-VWMA and an SMA (The bottom oscillator) gives an idea of the trend tacking into account of the volume, this serves as a more short term filter of the trend for filters.

-OBV checks are done between the OBV and an EMA of the OBV, to get the idea of a volume weighted long trend, which is important for crypto as there are massive rallies to go up due to retail greed, it’s great to jump onto it at the beginning, and get off before the stack of cards fall apart.

-ATR is used to detect when the market is relatively just ranging or moving sideways, which is where the hidden divergence entries are done, during predictable and profitable market conditions.

- Stop loss is based on the closest support of the entry, this is a nice medium of room to breath but also an actual stop loss.

Future plans and improvements:

Currently there’s a lot I want to improve, mostly the divergence detection and the overall sharpe ratio could be much better, but the current value of 0.5 gives me hope that the strategy is onto something. I also want to change TP from a percentage stop to something more dynamic but that might be too optimistic. The current plan is to paper trade test this either by manual or by a python bot, to see how it performs with some user input as well.

SuperTrend+Based upon popular SuperTrend (AKA: ATR Trailing Stop) indicator with the following differences and improvements:

Defaults to using Volume-Adjusted WMA ( VAWMA ) for ATR. (Can still be configured to behave exactly like classic SuperTrend.)

Can use SMA, EMA, WMA, VWMA, and VAWMA instead of just SMA.

Confirmation close bars for avoiding false breaks.

Details:

If the confirmation closing bars value is greater than zero (default of two bars), the trend will only reverse if the price closes outside the boundary for that number of bars (does not need to be consecutive) or if the opposite side of the bar exceeds the boundary.

The confirmation bar count will reset if the trend has resumed (opposite boundary is broken).

Confirmation examples:

In a down-trend, but the previous two bars close above the boundary.

In a down-trend, but the low of the previous bar exceeds the boundary.

In a down-trend, but the high of the previous bar exceeds the boundary when confirmation bars are set to zero.

Awesome ATRB1rd's Awesome ATR:

An objective method of determining an initial Take Profit and Stop Loss, based on true market volatility and not arbitrary price levels. This indicator gives the user a powerful range of input variation with myriad permutations of smoothing and look back lengths, to build an objective value from which to measure profit and stop levels. This indicator also has a build-in alert function to keep you up to date with latest price developments regarding the ATR levels.

This indicator also automatically calculates a recommended position size based on our position sizing methodology. Simply input your capital amount and desired risk level. This indicator will display your optimum position size in USD or in Coin.

Purpose:

To give clear objective stop losses and take profit levels based off price volatility rather than arbitrary price levels, percentage points, ticks, pips, etc.

hammerCandle & starCandleIn this scrip we have combine Pinbar Candlesticks calculated using Fibonacci, the bullish hammer candlestick and bearish star candlestick with EMAs and ATR.

I have used 12 Hour time frame which works well EUR/USD, this script works well on higher time frames such as Daily, 12 hours etc.

I have used 1.5 times the ATR as the stop loss and 1 times the ATR as the take profit as these risk to reward ratio gives us the best results for the 12 hour time frame for EUR/USD. Past result are not a prove of performance of the future.

I have added 1 for slippage and 1 for commission.

This script contains AutoView syntax and is fully automated if you connect TradingView to AutoView and a broker, prefebly Oanda.

This script uses two exponential moving averages for trend detection and Average True Range , ATR for stop loss and take profit targets. All of these setting are adjustable.

We only trade with the trend if the 50 period exponential moving averages is above the 200 period exponential moving averages, if a hammer candle is formed for entry.

Likewise with sell trade if a star candle is formed for entry and if the 50 period exponential moving averages is below the 200 period exponential moving averages.

This script does not trail your stop loss as I have noticed it does not give me good results. Stop loss is a fix stop loss based on Average True Range and so is the profit target.

This script has risk management, it risk a certain percent of the inputted capital amount in the setting. See settings for more details.

Note: Due to auto risk management this script only works on Forex.

Green line is 50 period exponential moving averages and red line is the the 200 period exponential moving average . Blue line is stop loss for long trade and black line stop loss for short trade.

Please trade at your own risk, all the setting in the script are adjustable for you to test before trading.

Many Thanks,

Honet Trader

EMA - MA 21/55/100/200 with Horizontal Lines and LabelsThis indicator will help you to get dynamic support lines of EMA 21,55,100,200 and MA 55,100,200. You can get the Price of EMA And MA in Labels also.

SOLID LINES - 4 HOUR

DOTTED LINES - 1 DAY

DASHED LINE - 1 HOUR

Hope It will help you.

Trade with your own risk. I am not liable for any loss and profit based on this indicator.

Thank you.

NSDT Trend CandlesThis script changes the color of the candles based on uptrend (green), downtrend (red), neutral/chop (yellow). It uses an ATR and Pivots to determine the direction, or lack of. Since all markets move differently and market volatility changes, you will need to adjust the settings to find a potential match for the day. It's pretty simple to use. Just enter in the direction of the trend and exit (or reverse) when the candle color changes.

Dynamic SMAThis script uses dynamic length to create a different sma type.

The length of the "Dynamic SMA" - "dSMA" can be:

'RSI', 'Stoch', 'ATR', 'MFI' or '%R'

For example 'RSI' -> the length of the sSMA will be the RSI itself

The biggest challenge was:

'Pine cannot determine the referencing length of a series. Try using max_bars_back' error

The writer of 'referencing length of a series' issue gave following solution:

bar_index == 0 ? 4999 : len

or in case of values which don't go above 100:

bar_index == 0 ? 100 : len

This assigns the necessary buffer to the function.

I'm most grateful for the given solution!

These dSMA's can give Support/Resistance levels, also crossovers of different dSMA's can give extra information

Examples:

RSI

ATR (close / atr(len)

Stoch

MFI

%R

"show regular SMA" will show the "SMA" with the same length (with default lighter color)

ATR Stop Loss FinderThis Indicator uses Average True Range (ATR) to determine a safe place to put stop losses to avoid being stop hunted or stopped out of a trade due to a tight stop loss. Default multiplier setting is 1.5. For a more conservative stop loss use 2 and for a tighter stop loss use 1. ATR and stop loss prices are displayed in table at bottom of screen. Use high(red) for shorts and low(teal) for longs.

RSI Strategy w/ Trailing SL / TP Optimized for Crypto [Strategy]This strategy is designed to use the RSI and EMA filters. A 200 period EMA is used for short / long filters, and the 50 period EMA is used to determine the direction of the short term trend.

In addition, the script uses "rate of change" for the fast EMA (trend), volume , RSI (momentum), and price (volatility) and only takes trades when all are in optimal conditions.

I.E., the EMA is in an uptrend, the volume is increasing, price is in an uptrend, and the RSI is in an uptrend, so we will place a Long trade.

This strategy uses EMAs as a trailing stop loss and take profit. As this is a trend following strategy, the idea is to maximize profits when correct and minimize losses when

wrong.

It was designed specifically using crypto pairs, and was optimized for the 10 minute chart.

My goal was to get the best use out of the RSI indicator. I was originally an MACD fanboy, but have recently converted.

Want to help me improve this code or strategy? Have suggestions for improvement? Leave them in the comments below.

Thanks for using my script! I hope it works well for you and good luck in the markets.

If you have any questions, please leave them in the comments and I'll do my best to respond.

This script does not repaint as it only relies on close data to make a decision to enter a trade.

How to use this strategy:

___________________________

Enable Long Entries? - Used to enable or disable the strategy from executing long entries.

Enable Short Entries? - Used to enable or disable the strategy from executing short entries.

How Many Bars To Look Back for Hi/Lo: - This is used for the Stop Loss and Take Profit targets. An integer of bars is used to look back and calculate the values.

RSI Length (Rec: 8) - The length of the RSI

Source - The RSI Source

Use Slow EMA? - If checked, a 200 period EMA will be used to filter entries long or short (only take shorts when the price is below, long when above). In addition, the script will close any trades that cross the 200 period EMA. By default this is disabled.

EMA Slow - the period of the Slow EMA (200 by default)

EMA Slow Src - what to use to calculate the Slow EMA (high by default)

EMA Fast - The Fast EMA (50 period) is used to calculate the direction of the short term trend. This also factored into the Rates of Change.

EMA Fast Src - what to use to calculate the Fast EMA

ATR Length - If used, the ATR length is used to calculate the Stop Loss and Take Profit targets.

SL Multiplier - The distance away from the initial value to multiply the Stop Loss

TP Multiplier - The distance away from the initial value to multiply the Take Profit.

Use EMA as SL / TP? - If true (default) a 3 period EMA is used to calculate Stop Loss and Take Profit targets. Else, an ATR is used to calculate these values.

Stop Loss / Take Profit Offset - Default: 3 - this is used to shift the EMA / ATR Stop Loss and Take Profit lines to the right X bars. This is to ensure that they are hit properly and not exceeded.

Short Len Vol - Use to calculate the volume of the short length, used in rate of change calculations

Long Len - Use to calculate the volume of the long length, used in rate of change calculations

RSI Long Entry Val - Minimum RSI crossover value to enter a trade Long. If the RSI is below this value, trade entries are not valid.

RSI Long Cutoff Threshold - Long entry RSI value cutoff to no longer enter trades. If the RSI is above this value, trades entries are not valid.

RSI Short Entry Val - Minimum RSI crossover value to enter a trade Short. If the RSI is above this value, trade entries are not valid.

RSI Short Cutoff Threshold - Short entry RSI value cutoff to no longer enter trades. If the RSI is below this value, trades entries are not valid.

ROC Fast EMA - Calculates the rate of change between the Fast Ema now and 'X' bars ago. For a long entry, a positive value is needed, and for a short entry, a negative value is needed.

ROC Price - Calculates the rate of change between the most recent price close and 'X' bars ago. For a long entry, a positive value is needed, and for a short entry, a negative value is needed.

ROC RSI - Calculates the rate of change between the RSI now and 'X' bars ago. For a long entry, a positive value is needed, and for a short entry, a negative value is needed.

Use Close for SL - Default = Off - If checked, when a candle hits the stop loss, the trade will close on the next candle. If unchecked, the trade will remain open until the candle closes at or beyond the stop loss lines.

Custom Message Boxes - Primarily used for bots, but can be used to also insert your own messages for your trading alerts.

PMax on Rsi w/T3 *Strategy*Profit Maximizer Indicator on RSI with Tillson T3 Moving Average:

PMax uses ATR calculation inside, for this reason users couldn't manage to use PMax on RSI because RSI indicator doesn't have High and Low values in bars, but ATR needs that values. So I personally calculate RSI in a different way to have High and Low values of RSI wrt price bars.

IMPORTANT:

Because of the sudden movements and divergences on RSI , this indicator must firstly optimized for the charts before using. Optimization can be held by users for the meaningful parameters for each chart.

3 parameters are critical when optimizing:

First: Multiplier

Second: Tillson T3 Length

Third: T3 Volume Factor

Says, Kıvanç Özbilgiç. Here's the strategy version for you to backtest & optimize properly.

Enjoy.

Stronger Classical Support/Resistance + Round LevelsI wrote some Support/Resistance scripts before this. In this new script, I implemented the logic of the code from the scratch, so it's very different from my previous S/R indicators and I think it's more advanced, accurate and efficient.

As the result it could do the followings for now:

- Draw more strong classical resistance/support levels by checking previous direction changes of the chart as far as Pine technically allows

- Colorize the levels based on the counted points of retracement/pullback (The darker the color is, the stronger the level is.)

- Show the number of reactions to each level

- Change the color of each level based on its main role as support, resistance or both

- Draw close round levels to current price for Forex pairs

I suggest all users of my previous S/R indicators to try this one.

Feel free to send me any issue or opinion!

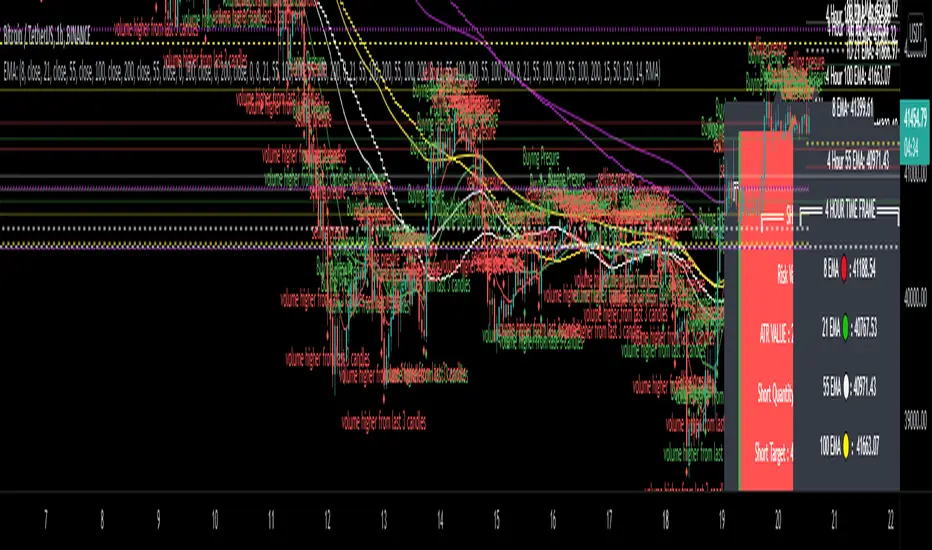

MM ATR Risk CalculatorBased on the NNFX Lot size position calculations MoneyMovesInvestments would like to provide to you the Free MM Atr Risk calculator

Directions are simple

Tells you the Atr value

Stop loss in pips

You can enter your account size

Based on your account size, enter the percent you want to risk

then the calculator will tell you your stop loss in pips based on current market and your lot size based on the account size and percent you want to risk

Check us out for your other trading needs

Link below or PM us for access to our other indicators

Happy Trading

Simple charting tool box (5 tools)This is a simple charting tool box that allows you to do 5 things:

1. Highlight custom time range with transparent background.

2. Plot High, Low of the custom time range and extension.

3. Plot previous day High, Low

4. Highlight market sessions (Sydney, Tokyo, London, New York), session times are customizable.

5. Plot ATR Projections

The drawings use exchange time of your data feed. For Oanda feed, it is NY time (UTC-4).

Hope the tool helps. Enjoy!

ADR% / ATR / LoD dist. TableDisplays the following values in a table in the upper right corner of the chart:

ADR%: Average daily range (in percent).

ATR: Average true range (hidden by default).

LoD dist.: Distance of current price to low of the day as a percentage of ATR.

All values are calculated based on daily bars, no matter what time frame you are currently viewing. Doesn't work for time frames >1D, which is why the table is not shown on weekly/monthly charts.

Credit to MikeC / TheScrutiniser and GlinckEastwoot for ADR% formula

StocasticRSI EMAs ATR StrategyA scalping based strategy thats works well with EUR/USD 30 minute time frame.

This strategy uses stochasticRSI for trade entry. Uses two exponential moving averages for trend detection. The strategy uses Average True Range for stop loss and for two profit targets.

We only trade with the trend if the 50 period exponential moving averages is above the 200 period exponential moving averages. StocasticRSI must cross below 30 level by default for a long entry if the rend is up. Likewise with a short entry the stochasticRSI must crossover above 70 level and if the trend is down.

This script does not trail your stop loss as I have noticed it does not give me good results. Stop loss is a fix stoploss based on Average True Range and so are the profit targets.

This script has risk management, it risk a certain percent of the inputed capital amount in the setting. See settings for more details.

Green line is 50 period exponential moving averages and red line is the the 200 period exponential moving average. Blue line is stoploss for short trade and black line stop loss for buy trade.

Since this is a scalping strategy be caution with the commission and slippage. I have inputed 1 for commission and 1 for sllipage.

Many Thanks,

Honest Trader

Supertrend BandsSupertrend Bands

What is the Supertrend indicator?

"The Supertrend indicator is a trend following overlay on your trading chart, much like a moving average, that shows you the current trend direction.

The indicator works well in a trending market but can give false signals when a market is trading in a range.

It uses the ATR (average true range) as part of its calculation which takes into account the volatility of the market. The ATR is adjusted using the multiplier setting which determines how sensitive the indicator is."

"For the basic Supertrend settings, you can adjust period and factor:

- The period setting is the lookback for the ATR calculation

- Factor is the what the ATR is multiplied by to offset the bands from price"

How to use this indicator

This indicator is inspired by a strategy I found. It includes four Supertrend indicators, each with different settings that displays trend strength and support/resistance zones. The default settings are optimal for cryptocurrency but do work quite well for traditional also. I highly recommend you try experimenting with different settings, increasing them to suit the instrument.

The bands are set from low to high, Band 1 being the fastest and Band 4 being the slowest. Band 4 is the one that sets the overall trend so when price is above Band 4, the trend is bullish and vice versa. Trend is strongest when price is above/below Band 1 and gets weaker as it filters through each band. Band 4 provides the strongest support/resistance and if that breaks the trend flips.

In the menu, you will see an option called "Remove Anti Trend?". It is enabled by default and it removes any bearish/resistance bands when the trend is up and any bullish/support bands when the trend is down. When turned off, it will show all Supertrend Bands as they are by default.

Bar Colors

Bar colors are optional and they reflect the current trend strength based on the Supertrend bands.

Alternate ways of using this indicator

You could leave everything as default or you can display individual bands. For instance, because I use many overlay indicators, most of the time I turn off all the bands and only show bar colors:

You can also turn off Bands 1 and 2 and only show the two slowest lengths:

This removes the noise of the two faster Supertrends.

Or just show the two fastest bands:

Any suggestions to improve this indicator are most welcome :)