FlowSpike ES — BB • RSI • VWAP + AVWAP + News MuteThis indicator is purpose-built for E-mini S&P 500 (ES) futures traders, combining volatility bands, momentum filters, and session-anchored levels into a streamlined tool for intraday execution.

Key Features:

• ES-Tuned Presets

Automatically optimized settings for scalping (1–2m), daytrading (5m), and swing trading (15–60m) timeframes.

• Bollinger Band & RSI Signals

Entry signals trigger only at statistically significant extremes, with RSI filters to reduce false moves.

• VWAP & Anchored VWAPs

Session VWAP plus anchored VWAPs (RTH open, weekly, monthly, and custom) provide high-confidence reference levels used by professional order-flow traders.

• Volatility Filter (ATR in ticks)

Ensures signals are only shown when the ES is moving enough to offer tradable edges.

• News-Time Mute

Suppresses signals around scheduled economic releases (customizable windows in ET), helping traders avoid whipsaw conditions.

• Clean Alerts

Long/short alerts are generated only when all conditions align, with optional bar-close confirmation.

Why It’s Tailored for ES Futures:

• Designed around ES tick size (0.25) and volatility structure.

• Session settings respect RTH hours (09:30–16:00 ET), the period where most liquidity and institutional flows concentrate.

• ATR thresholds and RSI bands are pre-tuned for ES market behavior, reducing the need for manual optimization.

⸻

This is not a generic indicator—it’s a futures-focused tool created to align with the way ES trades day after day. Whether you scalp the open, manage intraday swings, or align to weekly/monthly anchored flows, FlowSpike ES gives you a clear, rules-based signal framework.

Daytrading

Futures Playbook: VWAP + OR + Cross-Asset TellsFutures Playbook: VWAP + OR + Cross-Asset Tells (with Trade Messages + Coach Panel)

This all-in-one futures trading toolkit combines Opening Range (OR) levels, VWAP, and cross-asset signals to help traders quickly read intraday structure, manage execution, and filter noise.

Core Features

• Opening Range (OR):

• Customizable OR window with High/Low and Midpoint.

• Automatic shading of the OR zone.

• VWAP & Bands:

• Built-in or session-anchored VWAP.

• Optional standard deviation bands for context.

• Cross-Asset Tells:

• Live reads on US 10Y yield, DXY, Crude, and Gold.

• Regime detection: rates risk, USD strength, energy softness, and real-rate easing.

• Confirmations:

• Volume vs. moving average filter.

• Cumulative delta with smoothing.

• ATR-based chop filter to avoid low-quality trends.

Trade Messages + Coach Panel

• Trade Messages (labels): Automatic on-chart prompts for OR completion, VWAP reclaim/loss, long/short setups, and EU close flows.

• Coach Panel (table): Real-time dashboard with regime context, directional bias, execution notes, risk reminders, and key levels (ORH, ORL, VWAP).

Alerts

• OR breakout (long/short with confirmations).

• VWAP reclaim or loss.

• 10Y yield crossing risk threshold.

Use Case

Designed for futures traders and scalpers who rely on VWAP + OR dynamics and need cross-asset confirmation before committing to trades. Great for structuring entries, managing risk, and filtering market noise throughout the session.

Custom Time Range HighlightThis indicator highlights specific time ranges on your TradingView chart with customizable background colors and labels, making it easier to identify key trading sessions and ICT (Inner Circle Trader) Killzones. It is designed for traders who want to mark important market hours, such as major sessions (Asia, New York, London) or high-volatility Killzones, with full control over activation, timing, colors, and transparency.

Features

Customizable Time Ranges: Define up to 9 different time ranges, including one custom range, three major market sessions (Asia, New York, London), and five ICT Killzones (Asia, NY Open, NY Close, London Open, London Close).

Individual Activation: Enable or disable each time range independently via checkboxes in the settings. By default, only the ICT Killzones are active.

Custom Colors and Transparency: Set unique background and label colors for each range, with adjustable transparency for both.

Labeled Time Ranges: Each active range is marked with a customizable label at the start of the period, displayed above the chart for easy identification.

Priority Handling: If multiple ranges overlap, the range with the higher number (e.g., Asia Killzone over Custom Range) determines the background color.

CET Time Zone: Time ranges are based on Central European Time (CET, Europe/Vienna). Adjust the hours and minutes to match your trading needs.

Settings

The indicator settings are organized into three groups for clarity:

Custom Range: A flexible range (default: 15:30–18:00 CET) for user-defined periods.

Session - Asia, NY, London: Major market sessions (Asia: 01:00–10:00, New York: 14:00–23:00, London: 09:00–18:00 CET).

ICT Killzones - Asia, NY, London: High-volatility periods (NY Open: 13:00–16:00, NY Close: 20:00–23:00, London Open: 08:00–11:00, London Close: 16:00–18:00, Asia: 02:00–05:00 CET).

For each range, you can:

Toggle activation (default: only ICT Killzones enabled).

Adjust start and end times (hours and minutes).

Customize the label text.

Choose background and label colors with transparency levels (0–100).

How to Use

Add the indicator to your chart.

Open the settings to enable/disable specific ranges, adjust their times, or customize colors and labels.

The chart will highlight active time ranges with the selected background colors and display labels at the start of each range.

Use it to focus on key trading periods, such as ICT Killzones for high-probability setups or major sessions for market analysis.

Notes

Ensure your time ranges align with your trading instrument’s session times.

Overlapping ranges prioritize higher-numbered ranges (e.g., Asia Killzone overrides London Session).

Ideal for day traders, scalpers, or ICT strategy followers who need clear visual cues for specific market hours.

Feedback

If you have suggestions for improvements or need help with customization, feel free to leave a comment or contact the author!

Stacey Burke Signal Day LTE“Previously published as ‘Day Zero Fakeout Detector MTF’”

Stacey Burke Signal Day LTE

Automatic detection of Day Zero, Inside Days, and Outside Days for Stacey Burke’s intraday playbook

🔎 Stacey Burke’s Signal Days

This indicator highlights the key daily patterns that often lead to high-probability intraday setups in Stacey Burke’s methodology:

1️⃣ Day Zero

The reset days within a 3-day cycle (e.g. breakout → continuation → exhaustion/reversal).

Can mark the beginning of a new directional phase.

Trades back inside the prior range after a Peak Formation High (PFH) or Peak Formation Low (PFL).

Bias: Look for measured parabolic session moves. When combined with trend following indicators, these signal days can be very powerful.

2️⃣ Inside Day

A day where the entire range is contained within the prior day’s range.

Signals consolidation and energy build-up.

Often leads to explosive breakouts in the next session.

Bias: Trade breakouts of the inside day’s high/low or breakout reversal in the session at key timings in the direction of higher timeframe bias. When combined with trend following indicators, these signal days can be very powerful.

3️⃣ Outside Day (Engulfing Day)

`

A day where the range is larger than the prior day’s range, engulfing both high and low.

Marks trapped traders and fakeouts on both sides.

Often precedes strong continuations or sharp reversals from outside of the ranges.

Bias: Align trades with the true continuation move. When combined with trend following indicators, these signal days can be very powerful.

📌 How They Work Together

Day Zero → Signals the new cycle after PFH/PFL.

Inside Day → Signals compression → expect breakout setups.

Outside Day → Signals exhaustion/fakeouts → expect reversals or continuations.

Together, they give traders a clear daily roadmap for where liquidity sits and when to expect the highest-probability setups.

✅ Example in Practice

Market rallies for 3 days → PFH forms → Day Zero short bias.

Next day prints an Inside Day → watch for breakout continuation short, and breakout reversals.

Later, an Outside Day traps both longs and shorts → the following session offers a clean intraday reversal or continuation trade in line with the underlying MTF trend/bias.

⚙️ Features of This Indicator

Automatic detection of Day Zero, Inside Days, and Outside Days

Multi-Timeframe (MTF) support for cycle alignment

Visual markers for PFH/PFL and consolidation zones

Measured move projections for breakout targets

👉 Stacey Burke Signal Day LTE gives traders just a few of the most important signal days — Day Zero, Inside Day, and Outside Day — to structure their intraday trades around fake outs, breakouts, and reversals within the daily cycles of the week. (This is work in progress: Next up, FRD/FGD's, 3-day cycle detecting, 3DLs, 3DSs).

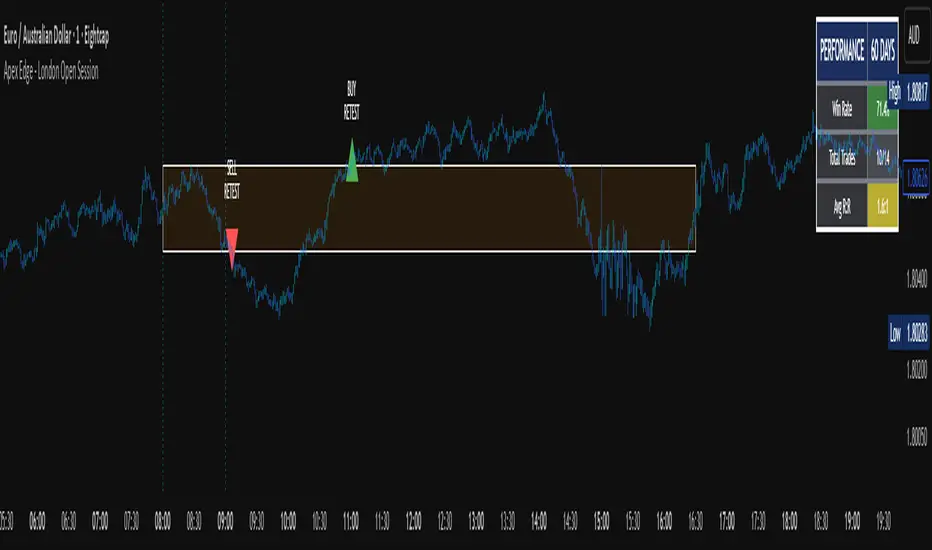

Apex Edge - London Open Session# Apex Edge - London Open Session Trading System

## Overview

The London Open Session indicator captures institutional price action during the first hour of the London forex session (8:00-9:00 AM GMT) and identifies high-probability breakout and retest opportunities. This system tracks the session's high/low range and generates precise entry signals when price breaks or retests these key institutional levels.

## Core Strategy

**Session Tracking**: Automatically identifies and marks the London Open session boundaries, creating a trading zone from the first hour's price range.

**Dual Entry Logic**:

- **Breakout Entries**: Triggers when price closes beyond the session high/low and continues in that direction

- **Retest Entries**: Activates when price returns to test the broken level as new support/resistance

**Performance Analytics**: Built-in win rate tracking displays real-time performance statistics over user-defined lookback periods, enabling data-driven optimization for each currency pair.

## Key Features

### Automated Zone Detection

- Precise London session timing with timezone offset controls

- Visual session boundaries with customizable colours

- Automatic high/low range calculation and display

### Smart Entry System

- Breakout confirmation requiring candle close beyond zone

- Retest detection with configurable pip distance tolerance

- Separate risk/reward ratios for breakout vs retest entries

- Visual entry arrows with clear trade direction labels

### Performance HUD

- Real-time win rate calculation over customizable periods (7-365 days)

- Total trades tracking with win/loss breakdown

- Average risk-reward ratio display

- Color-coded performance metrics (green >70%, yellow >50%, red <50%)

### PineConnector Integration

- Direct MT4/MT5 execution via PineConnector alerts

- Proper forex pip calculations for all currency pairs

- Customizable risk percentage per trade

- Symbol override capability for broker compatibility

- Automatic SL/TP level calculation in pips

## Critical Usage Requirements

### Pair-Specific Optimization

Each currency pair requires individual optimization due to varying volatility characteristics, institutional participation levels, and typical price ranges during London hours. The performance HUD is essential for identifying optimal settings before live trading.

**Recommended Testing Process**:

1. Apply indicator to desired currency pair and timeframe

2. Experiment with session timing - while 8:00-9:00 AM GMT is standard, some pairs may show improved performance with alternative hourly windows (e.g., 7:00-8:00 AM or 9:00-10:00 AM)

3. Adjust Stop Loss distances, Risk/Reward ratios, and Retest distances

4. Monitor win rate over 30+ day periods using the performance HUD

5. Only proceed with live alerts once consistent 60%+ win rates are achieved

6. Create separate optimized chart setups for each profitable pair/timeframe combination

### Timeframe Specifications

This indicator is specifically designed and tested for:

- **1-minute charts**: Optimal for capturing immediate institutional reactions

- **5-minute charts**: Balanced approach between noise reduction and opportunity frequency

Higher timeframes generally produce inferior results due to increased noise and reduced institutional edge during the London session window.

## Settings Configuration

### Session Timing

- **London Open/Close Hours**: Adjust for your chart's timezone

- **Rectangle End Time**: Set to 4:30 PM to stop signals before NY session close

- **Timezone Offset**: Ensure accurate London session capture

### Entry Parameters

- **Retest Distance**: 3-8 pips depending on pair volatility

- **Stop Loss Pips**: Separate settings for breakouts (10-15 pips) and retests (8-12 pips)

- **Risk/Reward Ratios**: Independent ratios for different entry types

### PineConnector Setup

- **License ID**: Your PineConnector license key

- **Symbol Override**: MT4/MT5 symbol names if different from TradingView

- **Risk Percentage**: Position size as percentage of account balance

- **Prefix/Comment**: Organize trades in terminal

## Manual Trading Limitations

Without PineConnector automation, traders face significant practical challenges:

**Settings Management**: Each currency pair requires different optimized parameters. Switching between charts means manually adjusting multiple settings each time, creating potential for errors and missed opportunities.

**Timing Sensitivity**: London Open signals can occur rapidly during high-volatility periods. Manual execution may result in slippage or missed entries.

**Multi-Pair Monitoring**: Tracking 4-11 currency pairs simultaneously while manually adjusting settings for each switch becomes impractical for most traders.

**Parameter Consistency**: Risk of using suboptimal settings when quickly switching between pairs, potentially compromising the careful optimization work.

## Recommended Workflow

1. **Historical Testing**: Use win rate HUD to identify profitable pairs and optimal parameters

2. **Demo Automation**: Test PineConnector alerts on demo accounts with optimized settings

3. **Live Implementation**: Deploy alerts only on proven profitable pair/timeframe combinations

4. **Ongoing Monitoring**: Regular review of performance metrics to maintain edge

## Risk Disclaimer

This indicator provides analysis tools and automation capabilities but does not guarantee profitable trading outcomes. Past performance does not predict future results. Users should thoroughly backtest and demo trade before risking live capital. The London session strategy works best during specific market conditions and may underperform during low volatility or unusual market environments.

## Support Requirements

Successful implementation requires:

- Basic understanding of London session market dynamics

- PineConnector subscription for automation features

- Patience for proper optimization process

- Realistic expectations about win rates and drawdown periods

This system is designed for serious traders willing to invest time in proper optimization and risk management rather than plug-and-play solutions.

Stoch TraderSimple example strategy that has greater than 60% win rate on 1m, 3m, and 5m views. Using something as simple as this with leverage can produce decent returns within 15-30min. It's also very easy to lose money doing this.

OHLC Lines – Yesterday & Today (Minimalist Option)This indicator draws horizontal lines representing the Open, High, Low, and Close (OHLC) levels of yesterday and today directly on your chart. It automatically updates each day, showing only the lines for the previous day and the current day, keeping your chart clean and focused.

Features:

Display Yesterday’s OHLC levels.

Display Today’s OHLC levels.

Optional Minimalist Mode with customizable color, width, and line style.

Lines automatically update each day and remove old lines.

Fully customizable colors, visibility, and line width for each OHLC level.

Use Case:

Perfect for traders who want to monitor key daily price levels, identify support/resistance zones, or incorporate OHLC levels into intraday strategies.

Apex Edge – Liquidity RaiderApex Edge – Liquidity Raider

The Predator That Hunts Where Retail Never Looks

The Liquidity Raider is not your average liquidity line plotter.

This is an institutional-grade hunting system that tracks the pools of liquidity Smart Money algos stalk — and tells you exactly when price is circling in for the strike.

Where most retail tools simply mark lines, this one acts like a predator:

Scans the chart dynamically to detect clustered highs & lows (pivot-based liquidity zones).

Filters noise with sensitivity & price rounding so you only get real liquidity levels — not every random swing.

Plots live BSL (Buy-Side Liquidity) & SSL (Sell-Side Liquidity) lines in clean dotted format.

Auto-deletes levels when swept, so your chart stays clean and focused.

Triggers directional arrows when price comes within your specified % distance to the target liquidity pool — before the market moves.

EMA confluence layer lets you align with institutional flow (customizable Fast & Slow EMAs).

Core Power

Cluster Logic – Finds high-probability liquidity zones using repeated pivot levels.

Sweep Awareness – Lines vanish the moment liquidity is taken, keeping focus on the next pool.

Proximity Strike Detection – Arrow signals only when price is within striking range.

Directional Clarity – Red arrows = targeting BSL, Green arrows = targeting SSL.

Scalable Across Timeframes – Adapts to your chart’s timeframe with dynamic lookback scaling.

Institutional Flow Filter – Optional EMA confirmation keeps you aligned with the real trend.

How to Use

Identify liquidity pools – Dotted green = buy-side, dotted red = sell-side.

Watch proximity arrows – These mean price is in range and hunting that pool.

Align with EMA bias – Enter only in the direction of institutional momentum.

Target the sweep – Your take profit is where the liquidity is resting.

Why Liquidity Raider Wins

This is not a lagging signal system.

It’s a real-time, clean, predictive tool designed to mimic the targeting logic of high-frequency algos.

By removing swept levels and focusing only on the next available pools, Liquidity Raider keeps you one step ahead of the crowd — and perfectly positioned for the kill shot.

Previous Day High/Low Levels [OWI]📘 How to Use the “Previous Day High/Low Levels ” Indicator

This TradingView indicator automatically tracks and displays the previous day's high and low during the Regular Trading Hours (RTH) session. It’s perfect for traders who want to visualize key support/resistance levels from the prior day in futures like CME_MINI:NQ1! and COMEX:GC1! .

🛠 Setup Instructions

1. Customize RTH Session Times

- In the Settings panel, adjust the following under the Levels group:

- RTH Start Hour and RTH Start Minute: Default is 9:30 AM (New York time).

- RTH End Hour and RTH End Minute: Default is 4:15 PM.

- These define the active trading session used to calculate the day’s high and low.

2. Toggle Labels

- Use the Show PDH/PDL Labels checkbox to display or hide the “PDH” and “PDL” labels on the chart.

- Labels appear after the session ends and follow price dynamically.

📊 What the Indicator Does

- During the RTH session:

- Tracks the highest and lowest price of the day.

- After the session ends:

- Draws horizontal lines at the previous day’s high (green) and low (red).

- Optionally displays labels ("PDH" and "PDL") at those levels.

- Lines extend into the current day to help identify potential support/resistance zones.

✅ Best Practices

- Use this indicator on intraday timeframes (e.g., 5m, 15m, 1h) for best results.

- Combine with volume or price action analysis to confirm reactions at PDH/PDL levels.

- Adjust session times if trading non-US markets or custom hours.

TSD Quantum [Moeinudin Montazerfaraj] 🔸 "TSD" stands for **Trend 1-2-3 and Supply & Demand**, which is the foundation of the trading style this indicator is built upon.

🔹 TSD Quantum is a specialized indicator designed exclusively for day traders who trade EURUSD, XAUUSD (Gold), and DAX40 on the 1H, 15M, and 5M timeframes using a Supply & Demand-based strategy.

This indicator is **not suitable for other symbols** and has been tailored specifically for these three assets to ensure high precision and effectiveness.

---

### 🔍 Key Features:

✅ **Trading Checklist Panel**

A built-in checklist helps you track every rule in your trading plan. If even one condition is left unchecked, the system highlights it in red and marks the trade as "Not Allowed." This feature enhances trading discipline.

✅ **Spread & ATR Control Panel**

Supports both auto-calculated and fixed values for spread and ATR. This is especially helpful when placing stop-losses quickly and accurately.

✅ **Inside & Outside Candle Detection**

A dedicated panel highlights whether the last candle is inside or outside. Hovering your mouse over the chart elements automatically colorizes the candles:

🔵 Blue = Outside candle

🔴 Red = Inside candle

Also displays the high/low of the latest outside bar.

✅ **Weekly Trade Stats Panel**

Custom-built for the mentioned three assets. You can enter your trades using either fixed risk or floating risk models.

✅ **Performance Metrics**

Helps you build and adjust a floating risk model—so you don’t have to enter every trade with the same lot size. Improves risk management across multiple trades.

✅ **Base Candles Display**

Grey and white base candles are marked based on supply and demand zones.

✅ **EOT Candles**

Candles with a green dot underneath indicate valid EOT opportunities for potential move-outs.

✅ **RC (Rejection Candle) Detection**

RC candles are automatically detected to alert you of potential traps or weaknesses during Supply/Demand formations.

---

### ⚠️ Disclaimer

This indicator does **not** issue buy/sell signals and **cannot guarantee profit or prevent loss**. It is a **tool for discretionary trading**, not an automated expert advisor.

All decisions must be made by the trader based on their own strategy and risk tolerance.

This is the **latest tested version** of TSD Quantum. All features have been validated and function as intended. Future updates will be provided if needed.

---

🙏 Thank you for reviewing this script. We hope it becomes a valuable addition to your day trading toolkit!

Daily Weekly Monthly Highs & Lows [Dova Lazarus]Daily Weekly Monthly Highs & Lows

📊 Overview

This Pine Script indicator displays key support and resistance levels by plotting the highs and lows from Daily, Weekly, and Monthly timeframes on your current chart. It's designed as an educational tool to help traders understand multi-timeframe analysis and identify significant price levels.

🎯 Key Features

Multi-Timeframe Support & Resistance

- Daily Levels: Shows previous daily highs and lows

- Weekly Levels: Displays weekly highs and lows

- Monthly Levels: Plots monthly highs and lows

- Smart Display: Only shows relevant timeframes based on your current chart timeframe

Fully Customizable Appearance

- Individual Colors: Set unique colors for each timeframe

- Line Styles: Choose between Solid, Dashed, or Dotted lines

- Line Width: Adjust thickness from 1-4 pixels

- Lookback Periods: Control how many historical levels to display

User-Friendly Options

- Enable/Disable: Toggle any timeframe on/off

- Line Extension: Option to extend lines into the future

- Clean Interface: Organized settings groups for easy configuration

🔧 Settings

Timeframes Group

- Show Daily/Weekly/Monthly Levels: Enable or disable each timeframe

- Lookback Periods: Number of historical levels to display (1-10)

Line Settings Group

- Color: Choose custom colors for each timeframe

- Style: Select line appearance (Solid/Dashed/Dotted)

- Width: Set line thickness (1-4 pixels)

Display Options Group

- Extend Lines Forward: Project lines 20 bars into the future

📈 How to Use

1. Add to Chart: Apply the indicator to any timeframe chart

2. Configure Timeframes: Enable the timeframes you want to see

3. Customize Appearance: Set colors and line styles for easy identification

4. Identify Levels: Use the plotted levels as potential support/resistance zones

5. Plan Trades: Look for price reactions at these key levels

💡 Trading Applications

- Support & Resistance: Identify key price levels where reversals may occur

- Entry Points: Look for bounces or breaks at these levels

- Stop Loss Placement: Use levels to set logical stop losses

- Target Setting: Previous highs/lows can serve as profit targets

- Multi-Timeframe Analysis: Understand the bigger picture context

🎓 Educational Value

This indicator is perfect for:

- Learning Pine Script: Clean, well-commented code structure

- Understanding Multi-Timeframe Analysis: See how different timeframes interact

- Practicing Technical Analysis: Identify key support/resistance concepts

- Code Study: Full variable names and detailed comments for learning

⚙️ Technical Details

- Version: Pine Script v6

- Overlay: True (plots directly on price chart)

- Max Lines: 500 (handles multiple timeframes efficiently)

- Compatibility: Works on all timeframes (shows relevant levels only)

🔍 What Makes This Different

- Educational Focus: Designed for learning with clear code structure

- Simplified Interface: Easy-to-use settings without overwhelming options

- Visual Clarity: Clean line display with customizable appearance

- Practical Application: Real trading tool, not just a demonstration

📋 Requirements

- TradingView account (any plan)

- Basic understanding of support/resistance concepts

- Any chart timeframe (indicator adapts automatically)

🚀 Quick Start

1. Add indicator to your chart

2. Default settings work great out of the box

3. Customize colors if desired (Green=Daily, Orange=Weekly, Red=Monthly)

4. Watch for price reactions at the plotted levels

5. Use as part of your technical analysis toolkit

---

*This indicator is designed as an educational tool and should be used in conjunction with other forms of analysis. Past performance does not guarantee future results.*

Fair Value MSThis indicator introduces rigid rules to familiar concepts to better capture and visualize Market Structure and Areas of Support and Resistance in a way that is both rule-based and reactive to market movements.

Typical "Market Structure" or "Zig-Zag" methods determine swing points based on fixed thresholds (length or percentage). While this does provide rigid structure, the results may be lagging or confusing due to the timing, since it is fixed to static parameters.

I believe the concept of Fair Value Gaps can solve this problem.

As you will notice, there are no length settings in this indicator.

> FVG Market Structure

Fair Value Gaps are a well known concept used to indicate directional intent, forming when price moves aggressively in one direction, leaving behind an imbalance between buyers and sellers. While the term FVG was popularized by ICT, the underlying concept predates them, known historically as imbalances, inefficiencies, or liquidity voids in institutional trading.

Note: For simplicity, in this indicator they'll be called FVGs.

By reading into this, we are able to clearly and rigidly define market structure simply by "looking" at the chart, using objective price events rather than subjective interpretation, or lengths.

By using FVGs to determine structure direction, the length, and speed of identification lies entirely on the market. If an FVG Down occurs immediately after a New Higher High forms, it is reasonable to assume there was a seller at that point, so the script would indicate a New Swing High.

The script is NOT stuck, waiting for a % retrace, or # bars to pass to identify it as such.

Sometimes the market is in a steady trend in a single direction and no FVGs form; therefore, no structure forms. -> Why would we try to impose structure on a clear trend?

Ultimately, the FVG Structure Method uses real reactions from the market to determine Market structure, and is not fixed to specific parameters.

As with other market structure indicators, "Market Structure Breaks" are still identifiable when price moves outside the most recent swing points.

These are helpful to indicate larger direction. In the following section you will see how these help us determine when we should start the search for an "Area of Interest (AOI)".

> Areas of Interest (AOIs)

"Area of Interest (AOI)" is a generalized term, and could refer to many types of zones you might recognize under different names. While the AOIs in this indicator are specialized in their own way, I have chosen to simply use the term "Area of Interest" because it’s more important to understand how they behave and why they exist than to focus on what they’re called.

The goal of an AOI is to point out reasonable areas where buyers or sellers may be staging, as is typical with support and resistance.

In order to reasonably identify these areas, we look for cause and effect relationships. When considering these relationships, it's easier to understand the placement of the points to define each zone.

(Buyer Examples)

Cause: Strong Buyers step in at Swing Low

Effect: Fair Value Gap Forms

Cause: Sustained Buying Pressure

Effect: Market Structure Breaks

In this example, The zone is drawn from the Swing Low, to the Bottom of the FVG closest to the swing point.

In theory, the participation at the swing point was strong and aggressive enough to create the FVG imbalance. Which then found acceptance and continued into a Market Structure Break. So with these AOIs, we are trying to locate the aggressive Buyers or Sellers which were positioned BEFORE the FVG.

These Zones are intended to act as areas to look for reactions from market participants, to judge where price may be going. When revisiting these zones, we look for a reaction or a break, to further provide us information to if the buyers or sellers are still there.

As seen in the screenshot above, The information we gain is not from the creation of these zones, but from the behavior we witness when these zones are revisited.

Technical Note: In this indicator, Market Structure Breaks are only considered when price closes outside the recent swing points. Wicks are not considered as confirmation, therefore are not used to detect structural breaks.

Inside each AOI you can optionally display a readout of the volume which accumulated during the time starting at the swing point and going until the closing bar of the FVG.

Note: We are counting volume until the closing bar of the FVG since the FVG is a 3 bar formation, and aggressive volume is required throughout to create the imbalance.

There are multiple FVGs that typically occur in a single direction, but we do not look to every single one to be indicative of structure, only the first FVG in the opposite direction of the previous direction (which is determined by previous FVGs)

You will probably notice, the AOIs do not form from the closest swing or FVG to the break, this is because we are targeting larger directional changes to draw these AOIs from.

Since they do not always happen perfectly every time, the AOI formation waits for an FVG to occur AND a Market structure break to happen. One without the other will result in no Zone displaying.

> Reflection Lines

While they may seem slightly redundant, Reflection Lines serve as reminders of previous support and resistance pivots. They are drawn at the same Pivots where and AOI is formed, and extend beyond the mitigation of the AOI.

These lines are often points of price to look for "Support Flips", a re-test pattern where price trades through previous support (or resistance) then returns to it and rejects, continuing into a larger move or trend.

Their namesake is based on the behavior of price, "reflecting" at these levels.

The Reflection lines are simple and change color based on price's location.

If price is above, we would typically look to a reflection line in with support in mind.

As a basic filter, these lines use an average price to determine their color, this way they will not change their color as frequently in choppy situations.

> Session Start/End Lines

For analysis purposes and trade review, it is helpful to analyze with context.

For that reason, I have implemented start and end session lines into the indicator, these are helpful when reviewing historical charts to not provide additional context.

By default, they are set to the NYSE Session, but can be changed to fit any needs.

These lines are not advanced, and simply draw a line as the chart passes the start and end of the sessions. It's very likely that you may need to adjust the session for your specific needs.

Note: The Timezone can be adjusted within the code if needed. By Default, the indicator uses "America/New_York" Timezone.

> Conclusion

If you’ve ever felt like your structure tools were confusing or lagging, drawing zones too late, or zones that simply don't make sense, this should feel like a breath of fresh air.

By removing arbitrary length settings and instead using FVGs to define structure and as a basis for AOIs, you're getting a more accurate look at what price is doing and where it's reacting from.

This indicator is rule-based, reactive, and aims to keep things logical without fluff or false confidence.

Enjoy!

day trading check indicatorDay Trading Check Indicator

By Trades per Minute · Creator: Trader Malik

Overview

The Day Trading Check Indicator is an on‐chart status panel that gives you a quick “go/no-go” snapshot of four key metrics—MACD, VWAP, Float, and Bearish Sell-Off—directly in TradingView’s top-right corner. It’s designed for fast decision-making during high-velocity intraday sessions, letting you instantly see whether each metric is “bullish” (green) or “bearish” (red), plus live float data.

What It Shows

Column Description

Metric The name of each metric: MACD, VWAP, Float, Bearish Sell-Off

Status/Value A color-coded status (“GREEN”/“RED” or “YES”/“NO”) or the float value formatted in K/M/B

Metrics & Calculations

MACD (1-Minute)

Calculation: Standard MACD using EMA (12) – EMA (26) with a 9-period signal line, all fetched from the 1-minute timeframe via request.security().

Status:

GREEN if MACD ≥ Signal

RED if MACD < Signal

VWAP (Session-Anchored)

Calculation: Built-in session VWAP (ta.vwap(close)) resets each new trading session.

Status:

GREEN if current price ≥ VWAP

RED if current price < VWAP

Float

Calculation: Retrieves syminfo.shares_outstanding_float (total float), then scales it into thousands (K), millions (M), or billions (B), e.g. “12.3 M.”

Display: Always shown as the absolute float value, white on semi-transparent black.

Bearish Sell-Off

Calculation: Checks the last five 1-minute bars for any “high-volume down” candle (volume above its 20-bar SMA and close < open).

Status:

YES if at least one such bar occurred in the past 5 minutes

NO otherwise

Key Features

Dynamic Table: Automatically shows only the metrics you enable via the Display Options group.

Size Selector: Choose Small, Medium, or Large text for easy visibility.

Clean Styling: Distinct header row with custom background, consistent row shading, centered status text, and a subtle gray border.

Lightweight Overlay: No cluttering plots—just a concise status panel in the corner.

Published by Trader Malik / Trades per Minute

Version: Pine Script v5

Super MTF Clouds (4x3 Pairs)Overview:

This script is based on Ripster's MTF clouds, which transcends the standard moving average cloud indicator by offering a powerful and deeply customizable Multi-Timeframe (MTF) analysis. Instead of being limited to the moving averages of your current charts from the current timeframe, this tool allows you to project and visualize the trend and key support/resistance zones from up to 4 different timeframes simultaneously. User can input up to 6 different EMA values which will form 3 pairs of EMA clouds, for each of the timeframes.

The primary purpose is to provide traders with immediate confluence. By observing how price interacts with moving average clouds from higher timeframes (e.g., Hourly, Daily, Weekly), you can make more informed decisions on your active trading timeframe (e.g., 10 Minute). It's designed as a complete MTF Cloud toolkit, allowing you to display all necessary MTFs in a single script to build a comprehensive view of the market structure without having to flick to different timeframe to look for cloud positions.

Key features:

Four Independent Multi-Timeframe Slots: Each slot can be assigned any timeframe available on TradingView (e.g., D, W, M, 4H).

Three MA Pairs Per Timeframe: For each timeframe, configure up to three separate MA clouds (e.g., a 9/12 EMA pair, a 20/50 EMA pair, and a 100/200 SMA pair).

Complete Customisation: For every single moving average (24 in total), you can independently control:

MA Type: Choose between EMA or SMA.

Length: Any period you require.

Line Color: Full colour selection.

Line Thickness: Adjust the visual weight of each line.

Cloud Control: For every pair (12 in total), you can set the fill colour and transparency.

How To Use This Script:

This tool is best used for confirmation and context. Here are some practical strategies that one can adopt:

Trend Confluence: Before taking a trade based on a signal on your current timeframe, glance at the higher timeframe clouds. If you see a buy signal on the 15-minute chart and the price is currently trading above a thick, bullish Daily cloud, the probability of that trade succeeding is significantly higher. Conversely, shorting into strong HTF support is a low-probability trade.

Dynamic Support & Resistance: The edges of the higher timeframe clouds often act as powerful, dynamic levels of support and resistance. A pullback to the 4-Hour 50 EMA on your 15-minute chart can be a prime area to look for entries in the direction of the larger trend.

Gauging Market Regimes: Use the toggles in the settings to quickly switch between different views. You can have a "risk-on" view with short-term clouds and a "macro" view with weekly and monthly clouds. This helps you adapt your trading style to the current market conditions.

Key Settings:

1. Global Setting

Source For All MAs: This determines the price data point used for every single moving average calculation.

Default: hl2 (an average of the High and Low of each bar). This gives a smooth midpoint price.

Options: You can change this to Close (the most common method), Open, High, Low, or ohlc4 (an average of the open, high, low, and close), among others.

Recommendation: For most standard trend analysis, the default hl2 is the common choice.

2. The Timeframe Group Structure

The rest of the settings are organized into four identical, collapsible groups: "Timeframe 1 Settings" through "Timeframe 4 Settings". Each group acts as a self-contained control panel for one multi-timeframe view.

Within each timeframe group, you have two master controls:

Enable Timeframe: This is the main power switch for the entire group. Uncheck this box to instantly hide all three clouds and lines associated with this timeframe. This is perfect for quickly decluttering your chart or focusing on a different set of analyses.

Timeframe: This dropdown menu is the heart of the MTF feature. Here, you select the higher timeframe you want to analyse (e.g., 1D for Daily, 1W for Weekly, 4H for 4-Hour). All calculations for the three pairs within this group will be based on the timeframe you select here.

3. Pair-Specific Controls

Inside each timeframe group, there are three sections for "Pair 1", "Pair 2", and "Pair 3". These control each individual moving average cloud.

Enable Pair: Just like the master switch for the timeframe, this checkbox turns a single cloud and its two MA lines on or off.

For each pair, the settings are further broken down:

Moving Average Lines (A and B): These two rows control the two moving averages that form the cloud. 'A' is typically used for the shorter-period MA and 'B' for the longer-period one.

Type (A/B): A dropdown menu to select either EMA (Exponential Moving Average) or SMA (Simple Moving Average). EMAs react more quickly to recent price changes, while SMAs are smoother and react more slowly.

Length (A/B): The lookback period for the moving average (e.g., 21, 50, 200).

Color (A/B): Sets the specific colour of the MA line itself on your chart.

Cloud Fill Settings

Fill Color: This controls the colour of the shaded area (the "cloud") between the two moving average lines. For a consistent look, you can set this to the same colour as your shorter MA line.

Transparency: Controls how see-through the cloud is, on a scale of 0 to 100. 0 is a solid, opaque colour, while 100 is completely invisible. The default of 85 provides a light, "cloud-like" appearance that doesn't obscure the price action.

----------------------------------------------------------------------

If anything is not clear please let me know!

Auto-Fibonacci Levels [ChartWhizzperer]Auto-Fibonacci Levels

Discover one of the most elegant and flexible Fibonacci indicators for TradingView – fully automatic, tastefully understated, and built entirely in Pine Script V6.

Key Features:

- Automatically detects the most recent swing high and swing low.

- Plots Fibonacci retracement levels and extensions (including 161.8%, 261.8%) perfectly aligned

to the prevailing trend.

- Distinctive, dashed lines with crystal-clear price labels right at the price scale

for maximum clarity.

- Line length and label offset are fully customisable for your charting preference.

- Absolutely no repainting: Only confirmed swings are used for reliable signals.

- Parameter: "Swing Detection Length"

The “Swing Detection Length” parameter determines how many bars must appear to the left and right of a potential high or low for it to be recognised as a significant swing point.

- Higher values make the script less sensitive (only major turning points are detected).

- Lower values make it more responsive to minor fluctuations (more fibs, more signals).

For best results, adjust this setting according to your preferred timeframe and trading style.

Pro Tip:

Fibonacci levels refresh automatically whenever a new swing is confirmed.

Ideal for price action enthusiasts and Fibonacci purists alike.

Licence:

// Licence: CC BY-NC-SA 4.0 – Non-commercial use only, attribution required.

// © ChartWhizzperer

Cumulative Intraday Volume with Long/Short LabelsThis indicator calculates a running total of volume for each trading day, then shows on the price chart when that total crosses levels you choose. Every day at 6:00 PM Eastern Time, the total goes back to zero so it always reflects only the current day’s activity. From that moment on, each time a new candle appears the indicator looks at whether the candle closed higher than it opened or lower. If it closed higher, the candle’s volume is added to the running total; if it closed lower, the same volume amount is subtracted. As a result, the total becomes positive when buyers have dominated so far today and negative when sellers have dominated.

Because futures markets close at 6 PM ET, the running total resets exactly then, mirroring the way most intraday traders think in terms of a single session. Throughout the day, you will see this running total move up or down according to whether more volume is happening on green or red candles. Once the total goes above a number you specify (for example, one hundred thousand contracts), the indicator will place a small “Long” label at that candle on the main price chart to let you know buying pressure has reached that level. Similarly, once the total goes below a negative number you choose (for example, minus one hundred thousand), a “Short” label will appear at that candle to signal that selling pressure has reached your chosen threshold. You can set these threshold numbers to whatever makes sense for your trading style or the market you follow.

Because raw volume alone never turns negative, this design uses candle direction as a sign. Green candles (where the close is higher than the open) add volume, and red candles (where the close is lower than the open) subtract volume. Summing those signed volume values tells you in a single number whether buying or selling has been stronger so far today. That number resets every evening, so it does not carry over any buying or selling from previous sessions.

Once you have this indicator on your chart, you simply watch the “summed volume” line as it moves throughout the day. If it climbs past your long threshold, you know buyers are firmly in control and a long entry might make sense. If it falls past your short threshold, you know sellers are firmly in control and a short entry might make sense. In quieter markets or times of low volume, you might use a smaller threshold so that even modest buying or selling pressure will trigger a label. During very active periods, a larger threshold will prevent too many signals when volume spikes frequently.

This approach is straightforward but can be surprisingly powerful. It does not rely on complex formulas or hidden statistical measures. Instead, it simply adds and subtracts daily volume based on candle color, then alerts you when that total reaches levels you care about. Over several years of historical testing, this formula has shown an ability to highlight moments when intraday sentiment shifts decisively from buyers to sellers or vice versa. Because the indicator resets every day at 6 PM, it always reflects only today’s sentiment and remains easy to interpret without carrying over past data. You can use it on any intraday timeframe, but it works especially well on five-minute or fifteen-minute charts for futures contracts.

If you want a clear gauge of whether buyers or sellers are dominating in real time, and you prefer a rule-based method rather than a complex model, this indicator gives you exactly that. It shows net buying or selling pressure at a glance, resets each session like most intraday traders do, and marks the moments when that pressure crosses the levels you decide are important. By combining a daily reset with signed volume, you get a single number that tells you precisely what the crowd is doing at any given moment, without any of the guesswork or hidden calculations that more complicated indicators often carry.

Momentum Fusion v1Momentum Fusion v1

Overview

Momentum Fusion v1 (MFusion) is a multi-oscillator indicator that combines several components to analyze market momentum and trend strength. It incorporates modified versions of classic indicators such as PVI (Positive Volume Index), NVI (Negative Volume Index), MFI (Money Flow Index), RSI, Stochastic, and Bollinger Bands Oscillator. The indicator displays a histogram that changes color based on momentum strength and includes "FUSION🔥" signal labels when extreme values are reached.

Indicator Settings

Parameters:

EMA Length – Smoothing period for the moving average (default: 255).

Smoothing Period – Internal calculation smoothing parameter (default: 15).

BB Multiplier – Standard deviation multiplier for Bollinger Bands (default: 2.0).

Show verde / marron / media lines – Toggles the display of auxiliary lines.

Show FUSION🔥 label – Enables/disables signal labels.

Indicator Components

1. PVI (Positive Volume Index)

Formula:

pvi := volume > volume ? nz(pvi ) + (close - close ) / close * sval : nz(pvi )

Description:

PVI increases when volume rises compared to the previous bar and accounts for price percentage change. The stronger the price movement with increasing volume, the higher the PVI value.

2. NVI (Negative Volume Index)

Formula:

nvi := volume < volume ? nz(nvi ) + (close - close ) / close * sval : nz(nvi )

Description:

NVI tracks price movements during declining volume. If the price rises on low volume, it may indicate a "stealth" trend.

3. Money Flow Index (MFI)

Formula:

100 - 100 / (1 + up / dn)

Description:

An oscillator measuring money flow strength. Values above 80 suggest overbought conditions, while values below 20 indicate oversold conditions.

4. Stochastic Oscillator

Formula:

k = 100 * (close - lowest(low, length)) / (highest(high, length) - lowest(low, length))

Description:

A classic stochastic oscillator showing price position relative to the selected period's range.

5. Bollinger Bands Oscillator

Formula:

(tprice - BB midline) / (upper BB - lower BB) * 100

Description:

Indicates the price position relative to Bollinger Bands in percentage terms.

Key Lines & Histogram

1. Verde (Green Line)

Calculation:

verde = marron + oscp (normalized PVI)

Interpretation:

Higher values indicate stronger bullish momentum. A FUSION🔥 signal appears when the value reaches 750+.

2. Marron (Brown Line)

Calculation:

marron = (RSI + MFI + Bollinger Osc + Stochastic / 3) / 2

Interpretation:

A composite oscillator combining multiple indicators. Higher values suggest overbought conditions.

3. Media (Red Line)

Calculation:

media = EMA of marron with smoothing period

Interpretation:

Acts as a signal line for trend confirmation.

4. Histogram

Calculation:

histo = verde - marron

Colors:

Bright green (>100) – Strong bullish momentum.

Light green (>0) – Moderate bullish momentum.

Orange (<0) – Bearish momentum.

Red (<-100) – Strong bearish momentum.

Signals & Alerts

1. FUSION🔥 (Strong Momentum)

Condition:

verde >= 750

Visualization:

A "FUSION🔥" label appears below the chart.

Alert:

Can be set to trigger notifications when the condition is met.

2. Background Aura

Condition:

verde > 850

Visualization:

The chart background turns teal, indicating extreme momentum.

Usage Recommendations

FUSION🔥 Signal – Can be used as a long entry point when confirmed by other indicators.

Histogram:

1. Green bars – Potential long entry.

2. Red/orange bars – Potential short entry.

3. Media & Marron Crossover – Can serve as an additional trend filter.

4. Suitable for a 5-15 minute time frame

Conclusion

Momentum Fusion v1 is a powerful tool for momentum analysis, combining multiple indicators into a unified system. It is suitable for:

Trend traders (catching strong movements).

Scalpers (identifying short-term impulses).

Swing traders (filtering entry points).

The indicator features customizable settings and visual signals, making it adaptable to various trading styles.

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Open-Based Percentage Levelsv2

This is an updated version of my original script.

Changes:

I took off the displacement levels since there served no purpose on this script.

I also fixed it to where the percentage level lines are visible continually throughout the entire trading day. Old version had these lines disappearing.

I also updated the name to better reflect its purpose.

Now only works on 30 min and below as the higher time frames are meaningless. The older version allow higher time frames and the code is open source to adjust as desired

Open-Based Adjustable LevelsThis indicator gives signals for levels where the buy or sell volume is above adjustable levels (ex, volume at 100,000). And these levels will only signal after the price has gone above/below a certain 'adjustable' percentage of the stocks opening price.

Example: Signal sell when the price action is 0.7% above market opening price and when sell volume is above 120,000

or

Signal buy when buy volume is above 80,000 and the price is 0.5% below market opening price.

Great for day trading and detecting potential swings in the market. Above image is on a 3min chart.

Doesn't work as well on daily time frames or above.

Should be combined with other indicators like buy/sell channels, for the best confirmations

Multi VWAPsMulti VWAPs Inspired by Biran Shannon and his book:

"MAXIMUM TRADING GAINS WITH ANCHORED VWAP . The Perfect Combination of Price, Time & Volume."

(ISBN 9798986868004)

A comprehensive VWAP (Volume Weighted Average Price) indicator that combines multiple timeframes and sessions in one view. Perfect for day trading and swing trading across different markets.

Features:

• Multiple VWAP Timeframes:

- Daily VWAP

- Weekly VWAP

- Monthly VWAP

- Quarterly VWAP

- Yearly VWAP

• Session-specific VWAPs:

- London Session (3:00 AM - 11:30 AM NY time)

- New York Session (9:30 AM - 4:00 PM NY time)

• Additional Indicators:

- Midnight Price Line (Previous day's closing price)

- 5-Day Moving Average

- 50-Day Moving Average

• Customization Options:

- Toggle individual VWAPs and indicators

- Customize colors for each component

- Adjustable label positioning

- MA smoothing settings

- Option to show/hide previous day's midnight price

• Smart Features:

- Auto-adjusting calculations based on timeframe

- Clear session boundaries

- Optimized for all chart timeframes

- Clean label system

Perfect for:

• Day traders tracking multiple timeframe momentum

• Swing traders using longer-term VWAPs

• Session traders focusing on London/NY hours

• Multi-timeframe analysis

• Price action trading with VWAP support/resistance

This indicator combines essential trading tools in one clean interface, helping you make informed decisions without cluttering your chart.

Intraday Fibs RetracementFibonacci (Fibs) levels are often used by traders as a way to find support and resistance, based on the Fibonacci sequence. These levels are widely used in technical analysis to identify potential reversal points in the price of an asset.

Fibs retracement draws lines at these Fibs level between a significant high and low point on a price chart.

What it shows:

This indicator will automatically draw Fibs Retracement Levels on your chart without any manual work.

It is designed to be used for day trading, especially in scenarios where a ticker gaps up/down large compared to the prior day close. (i.e. scenario where the difference of day's open and prior day close is large)

The drawing will happen on each trading day the moment trading hours open, and will NOT draw during pre-market and post-market.

User can see the line of each Fibs level, labelled with the Fib percentage and price value for the corresponding levels.

User will specify a start and end point of Fibs and based on the choice the indicator will automatically compute the other user defined Fibs levels and display on the chart.

How to use it:

The Fib levels drawn can be a potential support and resistance zone. Therefore in scenario where you already have a position and are approaching one of these levels it could be a point to close out some or all the position as you are approaching a resistance. On the other hand when price do approach these levels you could enter a position for a reversal trade. These are few ways to use the indicator but there are other ways that can be used, which can be found out by researching "Fibonacci (Fibs) Retracement".

In the example on the chart you can see a price bounce from the 0.7886 Fibs level on this particular day, where the price gapped up and was coming down after market hours opened.

Key settings:

1. Fibs Retracement Start and end Point: User selects where the Fibs levels should be drawn.

Available Options are:

Start Points:

Market Open

Market Open High (Dependent on the time frame you are on)

Pre-market High

Day's High

End Points:

Previous Day Close

Previous Day Low

Previous Day High

Pre-market Low (Current Day)

Day's Low

2. Custom Fib Levels: User can manually enter the Fib levels they want to see. (Max 9)

Default values are: 0,0.236,0.382,0.5,0.618,0.786,1,1.618,2.618.

3. Display settings: User can specify the line colour, thickness and style.

4. Label Setting: User can choose to turn on/off the labels for the each Fibs Level. Label will show the fib percentage and the corresponding price. User can also choose the location of the labels, defined by an offset from the current candle.

----------------------------------------------------------------------

If anything is not clear please let me know!

Candlestick Pattern Indicator – Doji, Harami, More [algo_aakash]This Candlestick Pattern Indicator is designed to help traders identify key price action patterns like Bullish Engulfing, Bearish Engulfing, Doji, Hammer, Morning Star, Evening Star, and many more directly on your TradingView chart. With customizable options to display both bullish and bearish patterns , this indicator provides real-time visual markers and labels, helping you make informed trading decisions.

Key features of the indicator include:

Detects popular candlestick patterns such as Bullish Engulfing, Bearish Engulfing, Hammer, Morning Star, Tweezer Tops, and more.

Customizable settings for displaying pattern shapes, labels, and opacity, tailored to your trading preferences.

Option to plot signals only after a candle closes, ensuring accuracy.

Alerts for immediate notification of detected patterns.

Visual markers on the chart, including arrows and labels, for quick recognition of potential trade setups.

This indicator is ideal for traders who rely on candlestick patterns for technical analysis and want an automated tool to highlight these setups for easier decision-making.

Whether you're a beginner or an experienced trader, this tool will help you spot important patterns in real-time without cluttering your chart.