WaveMacBollI wanted to see the two indicators in the candle chart, not in a separate window. And within the Bollinger band, it seemed to put it fine.

Important Note on Line Styles

Due to TradingView's multi-timeframe environment restrictions (timeframe = '', timeframe_gaps = true), I couldn't implement dotted or dashed line styles programmatically. The indicator uses solid lines by default.

If you prefer dotted/dashed lines for better visual distinction:

Add the indicator to your chart

Click on the indicator settings (gear icon)

Go to "Style" tab

Manually change line styles for each plot

Unfortunately, PineScript doesn't support line.new() or similar drawing functions in multi-timeframe mode, limiting our styling options to basic plot styles.

If you know a good solution for implementing dotted/dashed lines in multi-timeframe indicators without using drawing objects, please share it in the comments! I'd love to improve this aspect of the indicator

Educational

Volume-Weighted RSI & Multi-Normalized MACD### Description for Publishing: Volume-Weighted RSI & Multi-Normalized MACD

**Overview**

The "Volume-Weighted RSI & Multi-Normalized MACD" indicator is a powerful and versatile tool designed for traders seeking enhanced momentum and trend analysis. Combining a volume-weighted Relative Strength Index (VW-RSI) with a customizable Moving Average Convergence Divergence (MACD) featuring multiple normalization methods, this indicator provides deep insights into market dynamics. It supports multi-timeframe (MTF) analysis and includes an optional stepped plotting mode for discrete signal visualization, making it ideal for both trend-following and mean-reversion strategies across various markets (stocks, forex, crypto, etc.).

**Key Features**

1. **Volume-Weighted RSI (VW-RSI)**:

- A modified RSI that incorporates trading volume for greater sensitivity to market activity.

- Normalized to a user-defined range (default: -50 to +50) for consistent analysis.

- Optional smoothing with multiple moving average types (SMA, EMA, WMA, VWMA, SMMA, or SMA with Bollinger Bands) to reduce noise and highlight trends.

- Overbought (+20) and oversold (-20) levels for quick reference.

2. **Multi-Normalized MACD**:

- Offers six normalization methods for MACD, allowing traders to tailor the output to their strategy:

- Normalized Volume Weighted MACD (unbounded).

- Min-Max Normalization (bounded).

- Volatility Normalization (unbounded, volatility-adjusted).

- Volatility Normalization with Min-Max (bounded).

- Hyperbolic Tangent Normalization (bounded).

- Arctangent Normalization (bounded).

- Min-Max with Smoothing (bounded).

- All bounded methods scale to the user-defined range (default: -50 to +50), ensuring comparability with VW-RSI.

- Dynamic color changes for MACD line (lime/red) and histogram (aqua/blue/red/maroon) based on momentum and signal line crosses.

3. **Stepped Plotting Mode**:

- Optional mode to plot RSI and MACD as discrete, stepped lines, reducing noise by only updating when values change significantly (configurable thresholds).

- Ideal for traders focusing on clear, actionable signal changes.

4. **Multi-Timeframe Support**:

- Configurable timeframe input (default: chart timeframe) for analyzing RSI and MACD on higher or lower timeframes, enhancing cross-timeframe strategies.

5. **Customizable Display**:

- Toggle options to show/hide MACD line, signal line, histogram, and cross dots.

- Bollinger Bands for RSI smoothing (optional) with adjustable standard deviation multiplier.

- Clear visual cues with horizontal lines for overbought/oversold levels, midline, and MACD bounds.

**Usage Instructions**

1. **Add to Chart**: Apply the indicator to any symbol (e.g., BTCUSD, SPY) on any timeframe (1H, 1D, etc.).

2. **Configure Settings**:

- **General**: Adjust `Lower Bound` (-50 default) and `Upper Bound` (+50 default) for the output range. Set `Timeframe` for MTF analysis. Enable `Stepped?` for discrete plotting.

- **RSI**: Choose `Price Source` (default: ohlc4), `RSI Length` (default: 9), and smoothing options (e.g., EMA, Bollinger Bands). Adjust `RSI Diff Threshold` for stepped mode.

- **MACD**: Select `Price Source`, `Fast Length` (9), `Slow Length` (21), `Signal Length` (9), and a normalization method (default: Volatility Min-Max). Adjust `MACD Diff Threshold` for stepped mode.

- **Display Options**: Toggle MACD components and histogram colors for clarity.

3. **Interpretation**:

- **VW-RSI**: Watch for crosses above +20 (overbought) or below -20 (oversold) for potential reversals. Use smoothed RSI or Bollinger Bands for trend confirmation.

- **MACD**: Look for MACD/Signal line crosses (dots indicate crossings) and histogram changes for momentum shifts. Bounded normalizations align with RSI for unified analysis.

- **Stepped Mode**: Focus on significant changes in RSI/MACD for clearer signals.

4. **Companion Overlay**: For visualization on the main price chart, use the companion script "VW-RSI & MACD Price Overlay" (available separately, requires this script to be published). It plots RSI and MACD as price-scaled echo lines, with toggles to show/hide and customizable scaling (high/low or ATR).

**Who Is This For?**

- **Trend Traders**: Use MACD normalizations and MTF to identify momentum shifts across timeframes.

- **Mean-Reversion Traders**: Leverage VW-RSI’s overbought/oversold signals for entry/exit points.

- **Technical Analysts**: Customize normalization and smoothing to match specific market conditions.

- **All Markets**: Works on stocks, forex, cryptocurrencies, and more, with any timeframe.

**Notes**

- Unbounded MACD normalizations (`enable_nvw`, `enable_vol`) may produce values outside -50/+50, suitable for volatility-focused strategies.

- For price chart overlay, publish this script and use its ID in the companion script’s `request.security` call.

- Adjust scaling inputs in the companion script for optimal visualization on volatile or stable assets.

**Author’s Note**

Developed by NEPOLIX, this indicator combines volume-weighted precision with flexible normalization for robust technical analysis. Feedback and suggestions are welcome to enhance future versions!

Custom Candle Coloring (3% Drop / Breakout / Follow-through)Naveen's custom bars. It helps with custom color of the bars to see significant candle movements and their interpretations

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

Universal Gann Square & Cube LevelsUniversal Gann Square & Cube Levels - Dynamic Support/Resistance

Description:

📊 UNIVERSAL GANN LEVELS INDICATOR

This powerful indicator automatically plots Gann Square and Cube levels around the current stock price, providing dynamic support and resistance levels based on W.D. Gann's mathematical theories.

🎯 KEY FEATURES:

✅ Auto-Adaptive: Works for ANY stock price (₹20 to ₹100,000+)

✅ Real-time Detection: Uses current close price automatically

✅ Dual Level System: Square levels (black) + Cube levels (red)

✅ Customizable Range: Adjust percentage range (5% to 50%)

✅ Clean Display: Toggle square/cube lines independently

✅ Universal Compatibility: Works on all timeframes and instruments

📈 HOW IT WORKS:

Square Levels (Black Lines): Based on perfect squares (n²) around current price

Cube Levels (Red Lines): Based on perfect cubes (n³) around current price

Smart Range: Automatically calculates relevant levels within your specified percentage range

Info Display: Shows current price and level counts

⚙️ SETTINGS:

Price Range %: Control how many levels appear (default: 15%)

Show Square Levels: Toggle black square lines on/off

Show Cube Levels: Toggle red cube lines on/off

🔥 PERFECT FOR:

Day traders seeking precise entry/exit points

Swing traders identifying key support/resistance zones

Gann theory practitioners and students

Multi-timeframe analysis across all instruments

💡 USAGE TIPS:

Use 10-20% range for active day trading

Use 30-50% range for swing trading analysis

Watch for price reactions at square/cube intersections

Combine with volume analysis for confirmation

🌟 WHY THIS INDICATOR?

Unlike fixed Gann calculators, this indicator dynamically adapts to ANY price level, making it truly universal for Indian stocks, crypto, forex, and commodities.

⚠️ DISCLAIMER:

This indicator is for educational and informational purposes only. It is not financial advice and should not be considered as a recommendation to buy or sell any security. Trading involves significant risk of loss and may not be suitable for all investors. Past performance does not guarantee future results. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. The developer assumes no responsibility for any trading losses incurred through the use of this indicator.

📋 COMPATIBILITY:

All TradingView plans

All timeframes (1m to 1M)

Stocks, Crypto, Forex, Commodities

Mobile and desktop platforms

Simple Turnover (Enhanced v2)📊 Simple Turnover (Enhanced)

🔹 Overview

The Simple Turnover Indicator calculates a stock’s turnover by combining both price and volume, and then compares it against quarterly highs. This helps traders quickly gauge whether market participation in a move is strong enough to confirm a breakout, or weak and likely to be false.

Unlike volume alone, turnover considers both traded volume and price level, giving a truer reflection of capital flow in/out of a stock.

________________________________________

🔹 Formulae Used

1. Average Price (SMA)

AvgPrice=SMA(Close,n)

2. Average Volume (SMA)

AvgVol=SMA(Volume,n)

3. Turnover (Raw)

Turnover raw=AvgPrice × AvgVol

4. Unit Adjustment

• If Millions → Turnover = Turnover raw × 10^−6

• If Crores → Turnover = Turnover raw × 10^−7

• If Raw → Turnover = Turnover raw

5. Quarterly High Turnover (qHigh)

Within each calendar quarter (Jan–Mar, Apr–Jun, Jul–Sep, Oct–Dec), we track the maximum turnover seen:

qHigh=max (Turnover within current quarter)

________________________________________

🔹 Visualization

• Bars → Color follows price candle:

o Green if Close ≥ Open

o Red if Close < Open

• Blue Line → Rolling Quarterly High Turnover (qHigh)

________________________________________

🔹 Strategy Use Case

The Simple Turnover Indicator is most effective for confirming true vs false breakouts.

• A true breakout should be supported by increasing turnover, showing real capital backing the move.

• A false breakout often occurs with weak or declining turnover, suggesting lack of conviction.

📌 Example Strategy (3H timeframe):

1. Identify a demand zone using your preferred supply-demand indicator.

2. From this demand zone, monitor turnover bars.

3. A potential long entry is validated when:

o The current turnover bar is at least 20% higher than the previous one or two bars.

o Example setting: SMA length = 5 (i.e., turnover = 5-bar average close × 5-bar average volume).

4. This confirms strong participation in the move, increasing probability of a sustained breakout.

________________________________________

🔹 Disclaimer

⚠️ This indicator/strategy does not guarantee 100% accurate results.

It is intended to improve the probability of identifying true breakouts.

The actual success of the strategy will depend on price action, market momentum, and prevailing market conditions.

Always use this as a supporting tool along with broader trading analysis and risk management.

RMA EMA Crossover | MisinkoMasterThe RMA EMA Crossover (REMAC) is a trend-following overlay indicator designed to detect shifts in market momentum using the interaction between a smoothed RMA (Relative Moving Average) and its EMA (Exponential Moving Average) counterpart.

This combination provides fast, adaptive signals while reducing noise, making it suitable for a wide range of markets and timeframes.

🔎 Methodology

RMA Calculation

The Relative Moving Average (RMA) is calculated over the user-defined length.

RMA is a type of smoothed moving average that reacts more gradually than a standard EMA, providing a stable baseline.

EMA of RMA

An Exponential Moving Average (EMA) is then applied to the RMA, creating a dual-layer moving average system.

This combination amplifies trend signals while reducing false crossovers.

Trend Detection (Crossover Logic)

Bullish Signal (Trend Up) → When RMA crosses above EMA.

Bearish Signal (Trend Down) → When EMA crosses above RMA.

This simple crossover system identifies the direction of momentum shifts efficiently.

📈 Visualization

RMA and EMA are plotted directly on the chart.

Colors adapt dynamically to the current trend:

Cyan / Green hues → RMA above EMA (bullish momentum).

Magenta / Red hues → EMA above RMA (bearish momentum).

Filled areas between the two lines highlight zones of trend alignment or divergence, making it easier to spot reversals at a glance.

⚡ Features

Adjustable length parameter for RMA and EMA.

Overlay format allows for direct integration with price charts.

Visual trend scoring via color and fill for rapid assessment.

Works well across all asset classes: crypto, forex, stocks, indices.

✅ Use Cases

Trend Following → Stay on the right side of the market by following momentum shifts.

Reversal Detection → Crossovers highlight early trend changes.

Filter for Trading Systems → Use as a confirmation overlay for other indicators or strategies.

Visual Market Insight → Filled zones provide immediate context for trend strength.

AVGO Advanced Day Trading Strategy📈 Overview

The AVGO Advanced Day Trading Strategy is a comprehensive, multi-timeframe trading system designed for active day traders seeking consistent performance with robust risk management. Originally optimized for AVGO (Broadcom), this strategy adapts well to other liquid stocks and can be customized for various trading styles.

🎯 Key Features

Multiple Entry Methods

EMA Crossover: Classic trend-following signals using fast (9) and medium (16) EMAs

MACD + RSI Confluence: Momentum-based entries combining MACD crossovers with RSI positioning

Price Momentum: Consecutive price action patterns with EMA and RSI confirmation

Hybrid System: Advanced multi-trigger approach combining all methodologies

Advanced Technical Arsenal

When enabled, the strategy analyzes 8+ additional indicators for confluence:

Volume Price Trend (VPT): Measures volume-weighted price momentum

On-Balance Volume (OBV): Tracks cumulative volume flow

Accumulation/Distribution Line: Identifies institutional money flow

Williams %R: Momentum oscillator for entry timing

Rate of Change Suite: Multi-timeframe momentum analysis (5, 14, 18 periods)

Commodity Channel Index (CCI): Cyclical turning points

Average Directional Index (ADX): Trend strength measurement

Parabolic SAR: Dynamic support/resistance levels

🛡️ Risk Management System

Position Sizing

Risk-based position sizing (default 1% per trade)

Maximum position limits (default 25% of equity)

Daily loss limits with automatic position closure

Multiple Profit Targets

Target 1: 1.5% gain (50% position exit)

Target 2: 2.5% gain (30% position exit)

Target 3: 3.6% gain (20% position exit)

Configurable exit percentages and target levels

Stop Loss Protection

ATR-based or percentage-based stop losses

Optional trailing stops

Dynamic stop adjustment based on market volatility

📊 Technical Specifications

Primary Indicators

EMAs: 9 (Fast), 16 (Medium), 50 (Long)

VWAP: Volume-weighted average price filter

RSI: 6-period momentum oscillator

MACD: 8/13/5 configuration for faster signals

Volume Confirmation

Volume filter requiring 1.6x average volume

19-period volume moving average baseline

Optional volume confirmation bypass

Market Structure Analysis

Bollinger Bands (20-period, 2.0 multiplier)

Squeeze detection for breakout opportunities

Fractal and pivot point analysis

⏰ Trading Hours & Filters

Time Management

Configurable trading hours (default: 9:30 AM - 3:30 PM EST)

Weekend and holiday filtering

Session-based trade management

Market Condition Filters

Trend alignment requirements

VWAP positioning filters

Volatility-based entry conditions

📱 Visual Features

Information Dashboard

Real-time display of:

Current entry method and signals

Bullish/bearish signal counts

RSI and MACD status

Trend direction and strength

Position status and P&L

Volume and time filter status

Chart Visualization

EMA plots with customizable colors

Entry signal markers

Target and stop level lines

Background color coding for trends

Optional Bollinger Bands and SAR display

🔔 Alert System

Entry Alerts

Customizable alerts for long and short entries

Method-specific alert messages

Signal confluence notifications

Advanced Alerts

Strong confluence threshold alerts

Custom alert messages with signal counts

Risk management alerts

⚙️ Customization Options

Strategy Parameters

Enable/disable long or short trades

Adjustable risk parameters

Multiple entry method selection

Advanced indicator on/off toggle

Visual Customization

Color schemes for all indicators

Dashboard position and size options

Show/hide various chart elements

Background color preferences

📋 Default Settings

Initial Capital: $100,000

Commission: 0.1%

Default Position Size: 10% of equity

Risk Per Trade: 1.0%

RSI Length: 6 periods

MACD: 8/13/5 configuration

Stop Loss: 1.1% or ATR-based

🎯 Best Use Cases

Day Trading: Designed for intraday opportunities

Swing Trading: Adaptable for longer-term positions

Momentum Trading: Excellent for trending markets

Risk-Conscious Trading: Built-in risk management protocols

⚠️ Important Notes

Paper Trading Recommended: Test thoroughly before live trading

Market Conditions: Performance varies with market volatility

Customization: Adjust parameters based on your risk tolerance

Educational Purpose: Use as a learning tool and customize for your needs

🏆 Performance Features

Detailed performance metrics

Trade-by-trade analysis capability

Customizable risk/reward ratios

Comprehensive backtesting support

This strategy is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and consider your financial situation before trading.

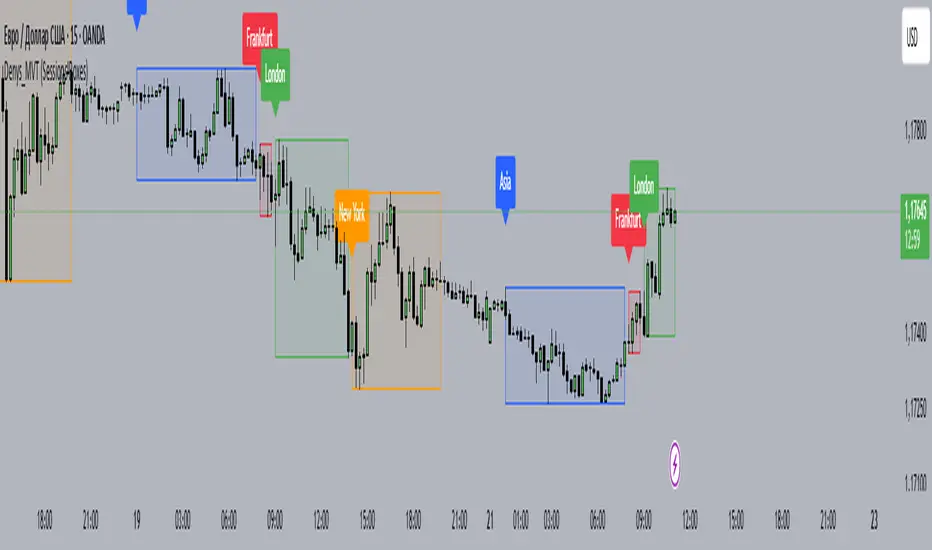

Denys_MVT (Sessions Boxes)Denys_MVT (Sessions Boxes)

This indicator highlights the main trading sessions — Asia, Frankfurt, London, and New York — directly on the chart.

It helps traders visually separate market activity during different times of the day and quickly understand which session is currently active.

🔹 How it works

You can choose between Box Mode (draws a box around the session’s high and low) or Fill Mode (background color for the session).

Each session has its own customizable time range and color.

Labels can be placed automatically at the beginning of each session.

The script uses the time() function with your selected UTC offset to precisely map session times.

🔹 Features

Displays Asia, Frankfurt, London, and New York sessions.

Option to toggle between boxes and background shading.

Adjustable transparency and session colors.

Session labels for easier visual reference.

Works on any symbol and timeframe.

🔹 How to use

Add the indicator to your chart.

Set your local UTC offset in the settings (default: UTC+2).

Enable/disable sessions, change colors, or switch between Box/Fill mode.

Use the session highlights to better understand when volatility typically increases and how different sessions interact.

Transaction Value Alert (4Cr+)Transactions with a value of INR 4 crore or above on a one-minute candle indicate FII or DII activity and confirms momentum and is an excellent indicator for the intraday trading

MSFusion- MultiScoreFusionThis Pine Script strategy, MSFusion - MultiScoreFusion, combines Ichimoku components and Hull Moving Average (HMA) signals to generate a composite score for each bar.

It evaluates several conditions—such as price crossing above HMA55, Tenkan and Kijun lines, and price position relative to the Ichimoku cloud—and assigns scores to each.

The script displays a label with the total score and a tooltip listing the contributing conditions when a strong bullish signal is detected. This approach helps traders quickly assess market momentum and trend strength using multiple technical criteria.

Small Business Economic Conditions - Statistical Analysis ModelThe Small Business Economic Conditions Statistical Analysis Model (SBO-SAM) represents an econometric approach to measuring and analyzing the economic health of small business enterprises through multi-dimensional factor analysis and statistical methodologies. This indicator synthesizes eight fundamental economic components into a composite index that provides real-time assessment of small business operating conditions with statistical rigor. The model employs Z-score standardization, variance-weighted aggregation, higher-order moment analysis, and regime-switching detection to deliver comprehensive insights into small business economic conditions with statistical confidence intervals and multi-language accessibility.

1. Introduction and Theoretical Foundation

The development of quantitative models for assessing small business economic conditions has gained significant importance in contemporary financial analysis, particularly given the critical role small enterprises play in economic development and employment generation. Small businesses, typically defined as enterprises with fewer than 500 employees according to the U.S. Small Business Administration, constitute approximately 99.9% of all businesses in the United States and employ nearly half of the private workforce (U.S. Small Business Administration, 2024).

The theoretical framework underlying the SBO-SAM model draws extensively from established academic research in small business economics and quantitative finance. The foundational understanding of key drivers affecting small business performance builds upon the seminal work of Dunkelberg and Wade (2023) in their analysis of small business economic trends through the National Federation of Independent Business (NFIB) Small Business Economic Trends survey. Their research established the critical importance of optimism, hiring plans, capital expenditure intentions, and credit availability as primary determinants of small business performance.

The model incorporates insights from Federal Reserve Board research, particularly the Senior Loan Officer Opinion Survey (Federal Reserve Board, 2024), which demonstrates the critical importance of credit market conditions in small business operations. This research consistently shows that small businesses face disproportionate challenges during periods of credit tightening, as they typically lack access to capital markets and rely heavily on bank financing.

The statistical methodology employed in this model follows the econometric principles established by Hamilton (1989) in his work on regime-switching models and time series analysis. Hamilton's framework provides the theoretical foundation for identifying different economic regimes and understanding how economic relationships may vary across different market conditions. The variance-weighted aggregation technique draws from modern portfolio theory as developed by Markowitz (1952) and later refined by Sharpe (1964), applying these concepts to economic indicator construction rather than traditional asset allocation.

Additional theoretical support comes from the work of Engle and Granger (1987) on cointegration analysis, which provides the statistical framework for combining multiple time series while maintaining long-term equilibrium relationships. The model also incorporates insights from behavioral economics research by Kahneman and Tversky (1979) on prospect theory, recognizing that small business decision-making may exhibit systematic biases that affect economic outcomes.

2. Model Architecture and Component Structure

The SBO-SAM model employs eight orthogonalized economic factors that collectively capture the multifaceted nature of small business operating conditions. Each component is normalized using Z-score standardization with a rolling 252-day window, representing approximately one business year of trading data. This approach ensures statistical consistency across different market regimes and economic cycles, following the methodology established by Tsay (2010) in his treatment of financial time series analysis.

2.1 Small Cap Relative Performance Component

The first component measures the performance of the Russell 2000 index relative to the S&P 500, capturing the market-based assessment of small business equity valuations. This component reflects investor sentiment toward smaller enterprises and provides a forward-looking perspective on small business prospects. The theoretical justification for this component stems from the efficient market hypothesis as formulated by Fama (1970), which suggests that stock prices incorporate all available information about future prospects.

The calculation employs a 20-day rate of change with exponential smoothing to reduce noise while preserving signal integrity. The mathematical formulation is:

Small_Cap_Performance = (Russell_2000_t / S&P_500_t) / (Russell_2000_{t-20} / S&P_500_{t-20}) - 1

This relative performance measure eliminates market-wide effects and isolates the specific performance differential between small and large capitalization stocks, providing a pure measure of small business market sentiment.

2.2 Credit Market Conditions Component

Credit Market Conditions constitute the second component, incorporating commercial lending volumes and credit spread dynamics. This factor recognizes that small businesses are particularly sensitive to credit availability and borrowing costs, as established in numerous Federal Reserve studies (Bernanke and Gertler, 1995). Small businesses typically face higher borrowing costs and more stringent lending standards compared to larger enterprises, making credit conditions a critical determinant of their operating environment.

The model calculates credit spreads using high-yield bond ETFs relative to Treasury securities, providing a market-based measure of credit risk premiums that directly affect small business borrowing costs. The component also incorporates commercial and industrial loan growth data from the Federal Reserve's H.8 statistical release, which provides direct evidence of lending activity to businesses.

The mathematical specification combines these elements as:

Credit_Conditions = α₁ × (HYG_t / TLT_t) + α₂ × C&I_Loan_Growth_t

where HYG represents high-yield corporate bond ETF prices, TLT represents long-term Treasury ETF prices, and C&I_Loan_Growth represents the rate of change in commercial and industrial loans outstanding.

2.3 Labor Market Dynamics Component

The Labor Market Dynamics component captures employment cost pressures and labor availability metrics through the relationship between job openings and unemployment claims. This factor acknowledges that labor market tightness significantly impacts small business operations, as these enterprises typically have less flexibility in wage negotiations and face greater challenges in attracting and retaining talent during periods of low unemployment.

The theoretical foundation for this component draws from search and matching theory as developed by Mortensen and Pissarides (1994), which explains how labor market frictions affect employment dynamics. Small businesses often face higher search costs and longer hiring processes, making them particularly sensitive to labor market conditions.

The component is calculated as:

Labor_Tightness = Job_Openings_t / (Unemployment_Claims_t × 52)

This ratio provides a measure of labor market tightness, with higher values indicating greater difficulty in finding workers and potential wage pressures.

2.4 Consumer Demand Strength Component

Consumer Demand Strength represents the fourth component, combining consumer sentiment data with retail sales growth rates. Small businesses are disproportionately affected by consumer spending patterns, making this component crucial for assessing their operating environment. The theoretical justification comes from the permanent income hypothesis developed by Friedman (1957), which explains how consumer spending responds to both current conditions and future expectations.

The model weights consumer confidence and actual spending data to provide both forward-looking sentiment and contemporaneous demand indicators. The specification is:

Demand_Strength = β₁ × Consumer_Sentiment_t + β₂ × Retail_Sales_Growth_t

where β₁ and β₂ are determined through principal component analysis to maximize the explanatory power of the combined measure.

2.5 Input Cost Pressures Component

Input Cost Pressures form the fifth component, utilizing producer price index data to capture inflationary pressures on small business operations. This component is inversely weighted, recognizing that rising input costs negatively impact small business profitability and operating conditions. Small businesses typically have limited pricing power and face challenges in passing through cost increases to customers, making them particularly vulnerable to input cost inflation.

The theoretical foundation draws from cost-push inflation theory as described by Gordon (1988), which explains how supply-side price pressures affect business operations. The model employs a 90-day rate of change to capture medium-term cost trends while filtering out short-term volatility:

Cost_Pressure = -1 × (PPI_t / PPI_{t-90} - 1)

The negative weighting reflects the inverse relationship between input costs and business conditions.

2.6 Monetary Policy Impact Component

Monetary Policy Impact represents the sixth component, incorporating federal funds rates and yield curve dynamics. Small businesses are particularly sensitive to interest rate changes due to their higher reliance on variable-rate financing and limited access to capital markets. The theoretical foundation comes from monetary transmission mechanism theory as developed by Bernanke and Blinder (1992), which explains how monetary policy affects different segments of the economy.

The model calculates the absolute deviation of federal funds rates from a neutral 2% level, recognizing that both extremely low and high rates can create operational challenges for small enterprises. The yield curve component captures the shape of the term structure, which affects both borrowing costs and economic expectations:

Monetary_Impact = γ₁ × |Fed_Funds_Rate_t - 2.0| + γ₂ × (10Y_Yield_t - 2Y_Yield_t)

2.7 Currency Valuation Effects Component

Currency Valuation Effects constitute the seventh component, measuring the impact of US Dollar strength on small business competitiveness. A stronger dollar can benefit businesses with significant import components while disadvantaging exporters. The model employs Dollar Index volatility as a proxy for currency-related uncertainty that affects small business planning and operations.

The theoretical foundation draws from international trade theory and the work of Krugman (1987) on exchange rate effects on different business segments. Small businesses often lack hedging capabilities, making them more vulnerable to currency fluctuations:

Currency_Impact = -1 × DXY_Volatility_t

2.8 Regional Banking Health Component

The eighth and final component, Regional Banking Health, assesses the relative performance of regional banks compared to large financial institutions. Regional banks traditionally serve as primary lenders to small businesses, making their health a critical factor in small business credit availability and overall operating conditions.

This component draws from the literature on relationship banking as developed by Boot (2000), which demonstrates the importance of bank-borrower relationships, particularly for small enterprises. The calculation compares regional bank performance to large financial institutions:

Banking_Health = (Regional_Banks_Index_t / Large_Banks_Index_t) - 1

3. Statistical Methodology and Advanced Analytics

The model employs statistical techniques to ensure robustness and reliability. Z-score normalization is applied to each component using rolling 252-day windows, providing standardized measures that remain consistent across different time periods and market conditions. This approach follows the methodology established by Engle and Granger (1987) in their cointegration analysis framework.

3.1 Variance-Weighted Aggregation

The composite index calculation utilizes variance-weighted aggregation, where component weights are determined by the inverse of their historical variance. This approach, derived from modern portfolio theory, ensures that more stable components receive higher weights while reducing the impact of highly volatile factors. The mathematical formulation follows the principle that optimal weights are inversely proportional to variance, maximizing the signal-to-noise ratio of the composite indicator.

The weight for component i is calculated as:

w_i = (1/σᵢ²) / Σⱼ(1/σⱼ²)

where σᵢ² represents the variance of component i over the lookback period.

3.2 Higher-Order Moment Analysis

Higher-order moment analysis extends beyond traditional mean and variance calculations to include skewness and kurtosis measurements. Skewness provides insight into the asymmetry of the sentiment distribution, while kurtosis measures the tail behavior and potential for extreme events. These metrics offer valuable information about the underlying distribution characteristics and potential regime changes.

Skewness is calculated as:

Skewness = E / σ³

Kurtosis is calculated as:

Kurtosis = E / σ⁴ - 3

where μ represents the mean and σ represents the standard deviation of the distribution.

3.3 Regime-Switching Detection

The model incorporates regime-switching detection capabilities based on the Hamilton (1989) framework. This allows for identification of different economic regimes characterized by distinct statistical properties. The regime classification employs percentile-based thresholds:

- Regime 3 (Very High): Percentile rank > 80

- Regime 2 (High): Percentile rank 60-80

- Regime 1 (Moderate High): Percentile rank 50-60

- Regime 0 (Neutral): Percentile rank 40-50

- Regime -1 (Moderate Low): Percentile rank 30-40

- Regime -2 (Low): Percentile rank 20-30

- Regime -3 (Very Low): Percentile rank < 20

3.4 Information Theory Applications

The model incorporates information theory concepts, specifically Shannon entropy measurement, to assess the information content of the sentiment distribution. Shannon entropy, as developed by Shannon (1948), provides a measure of the uncertainty or information content in a probability distribution:

H(X) = -Σᵢ p(xᵢ) log₂ p(xᵢ)

Higher entropy values indicate greater unpredictability and information content in the sentiment series.

3.5 Long-Term Memory Analysis

The Hurst exponent calculation provides insight into the long-term memory characteristics of the sentiment series. Originally developed by Hurst (1951) for analyzing Nile River flow patterns, this measure has found extensive application in financial time series analysis. The Hurst exponent H is calculated using the rescaled range statistic:

H = log(R/S) / log(T)

where R/S represents the rescaled range and T represents the time period. Values of H > 0.5 indicate long-term positive autocorrelation (persistence), while H < 0.5 indicates mean-reverting behavior.

3.6 Structural Break Detection

The model employs Chow test approximation for structural break detection, based on the methodology developed by Chow (1960). This technique identifies potential structural changes in the underlying relationships by comparing the stability of regression parameters across different time periods:

Chow_Statistic = (RSS_restricted - RSS_unrestricted) / RSS_unrestricted × (n-2k)/k

where RSS represents residual sum of squares, n represents sample size, and k represents the number of parameters.

4. Implementation Parameters and Configuration

4.1 Language Selection Parameters

The model provides comprehensive multi-language support across five languages: English, German (Deutsch), Spanish (Español), French (Français), and Japanese (日本語). This feature enhances accessibility for international users and ensures cultural appropriateness in terminology usage. The language selection affects all internal displays, statistical classifications, and alert messages while maintaining consistency in underlying calculations.

4.2 Model Configuration Parameters

Calculation Method: Users can select from four aggregation methodologies:

- Equal-Weighted: All components receive identical weights

- Variance-Weighted: Components weighted inversely to their historical variance

- Principal Component: Weights determined through principal component analysis

- Dynamic: Adaptive weighting based on recent performance

Sector Specification: The model allows for sector-specific calibration:

- General: Broad-based small business assessment

- Retail: Emphasis on consumer demand and seasonal factors

- Manufacturing: Enhanced weighting of input costs and currency effects

- Services: Focus on labor market dynamics and consumer demand

- Construction: Emphasis on credit conditions and monetary policy

Lookback Period: Statistical analysis window ranging from 126 to 504 trading days, with 252 days (one business year) as the optimal default based on academic research.

Smoothing Period: Exponential moving average period from 1 to 21 days, with 5 days providing optimal noise reduction while preserving signal integrity.

4.3 Statistical Threshold Parameters

Upper Statistical Boundary: Configurable threshold between 60-80 (default 70) representing the upper significance level for regime classification.

Lower Statistical Boundary: Configurable threshold between 20-40 (default 30) representing the lower significance level for regime classification.

Statistical Significance Level (α): Alpha level for statistical tests, configurable between 0.01-0.10 with 0.05 as the standard academic default.

4.4 Display and Visualization Parameters

Color Theme Selection: Eight professional color schemes optimized for different user preferences and accessibility requirements:

- Gold: Traditional financial industry colors

- EdgeTools: Professional blue-gray scheme

- Behavioral: Psychology-based color mapping

- Quant: Value-based quantitative color scheme

- Ocean: Blue-green maritime theme

- Fire: Warm red-orange theme

- Matrix: Green-black technology theme

- Arctic: Cool blue-white theme

Dark Mode Optimization: Automatic color adjustment for dark chart backgrounds, ensuring optimal readability across different viewing conditions.

Line Width Configuration: Main index line thickness adjustable from 1-5 pixels for optimal visibility.

Background Intensity: Transparency control for statistical regime backgrounds, adjustable from 90-99% for subtle visual enhancement without distraction.

4.5 Alert System Configuration

Alert Frequency Options: Three frequency settings to match different trading styles:

- Once Per Bar: Single alert per bar formation

- Once Per Bar Close: Alert only on confirmed bar close

- All: Continuous alerts for real-time monitoring

Statistical Extreme Alerts: Notifications when the index reaches 99% confidence levels (Z-score > 2.576 or < -2.576).

Regime Transition Alerts: Notifications when statistical boundaries are crossed, indicating potential regime changes.

5. Practical Application and Interpretation Guidelines

5.1 Index Interpretation Framework

The SBO-SAM index operates on a 0-100 scale with statistical normalization ensuring consistent interpretation across different time periods and market conditions. Values above 70 indicate statistically elevated small business conditions, suggesting favorable operating environment with potential for expansion and growth. Values below 30 indicate statistically reduced conditions, suggesting challenging operating environment with potential constraints on business activity.

The median reference line at 50 represents the long-term equilibrium level, with deviations providing insight into cyclical conditions relative to historical norms. The statistical confidence bands at 95% levels (approximately ±2 standard deviations) help identify when conditions reach statistically significant extremes.

5.2 Regime Classification System

The model employs a seven-level regime classification system based on percentile rankings:

Very High Regime (P80+): Exceptional small business conditions, typically associated with strong economic growth, easy credit availability, and favorable regulatory environment. Historical analysis suggests these periods often precede economic peaks and may warrant caution regarding sustainability.

High Regime (P60-80): Above-average conditions supporting business expansion and investment. These periods typically feature moderate growth, stable credit conditions, and positive consumer sentiment.

Moderate High Regime (P50-60): Slightly above-normal conditions with mixed signals. Careful monitoring of individual components helps identify emerging trends.

Neutral Regime (P40-50): Balanced conditions near long-term equilibrium. These periods often represent transition phases between different economic cycles.

Moderate Low Regime (P30-40): Slightly below-normal conditions with emerging headwinds. Early warning signals may appear in credit conditions or consumer demand.

Low Regime (P20-30): Below-average conditions suggesting challenging operating environment. Businesses may face constraints on growth and expansion.

Very Low Regime (P0-20): Severely constrained conditions, typically associated with economic recessions or financial crises. These periods often present opportunities for contrarian positioning.

5.3 Component Analysis and Diagnostics

Individual component analysis provides valuable diagnostic information about the underlying drivers of overall conditions. Divergences between components can signal emerging trends or structural changes in the economy.

Credit-Labor Divergence: When credit conditions improve while labor markets tighten, this may indicate early-stage economic acceleration with potential wage pressures.

Demand-Cost Divergence: Strong consumer demand coupled with rising input costs suggests inflationary pressures that may constrain small business margins.

Market-Fundamental Divergence: Disconnection between small-cap equity performance and fundamental conditions may indicate market inefficiencies or changing investor sentiment.

5.4 Temporal Analysis and Trend Identification

The model provides multiple temporal perspectives through momentum analysis, rate of change calculations, and trend decomposition. The 20-day momentum indicator helps identify short-term directional changes, while the Hodrick-Prescott filter approximation separates cyclical components from long-term trends.

Acceleration analysis through second-order momentum calculations provides early warning signals for potential trend reversals. Positive acceleration during declining conditions may indicate approaching inflection points, while negative acceleration during improving conditions may suggest momentum loss.

5.5 Statistical Confidence and Uncertainty Quantification

The model provides comprehensive uncertainty quantification through confidence intervals, volatility measures, and regime stability analysis. The 95% confidence bands help users understand the statistical significance of current readings and identify when conditions reach historically extreme levels.

Volatility analysis provides insight into the stability of current conditions, with higher volatility indicating greater uncertainty and potential for rapid changes. The regime stability measure, calculated as the inverse of volatility, helps assess the sustainability of current conditions.

6. Risk Management and Limitations

6.1 Model Limitations and Assumptions

The SBO-SAM model operates under several important assumptions that users must understand for proper interpretation. The model assumes that historical relationships between economic variables remain stable over time, though the regime-switching framework helps accommodate some structural changes. The 252-day lookback period provides reasonable statistical power while maintaining sensitivity to changing conditions, but may not capture longer-term structural shifts.

The model's reliance on publicly available economic data introduces inherent lags in some components, particularly those based on government statistics. Users should consider these timing differences when interpreting real-time conditions. Additionally, the model's focus on quantitative factors may not fully capture qualitative factors such as regulatory changes, geopolitical events, or technological disruptions that could significantly impact small business conditions.

The model's timeframe restrictions ensure statistical validity by preventing application to intraday periods where the underlying economic relationships may be distorted by market microstructure effects, trading noise, and temporal misalignment with the fundamental data sources. Users must utilize daily or longer timeframes to ensure the model's statistical foundations remain valid and interpretable.

6.2 Data Quality and Reliability Considerations

The model's accuracy depends heavily on the quality and availability of underlying economic data. Market-based components such as equity indices and bond prices provide real-time information but may be subject to short-term volatility unrelated to fundamental conditions. Economic statistics provide more stable fundamental information but may be subject to revisions and reporting delays.

Users should be aware that extreme market conditions may temporarily distort some components, particularly those based on financial market data. The model's statistical normalization helps mitigate these effects, but users should exercise additional caution during periods of market stress or unusual volatility.

6.3 Interpretation Caveats and Best Practices

The SBO-SAM model provides statistical analysis and should not be interpreted as investment advice or predictive forecasting. The model's output represents an assessment of current conditions based on historical relationships and may not accurately predict future outcomes. Users should combine the model's insights with other analytical tools and fundamental analysis for comprehensive decision-making.

The model's regime classifications are based on historical percentile rankings and may not fully capture the unique characteristics of current economic conditions. Users should consider the broader economic context and potential structural changes when interpreting regime classifications.

7. Academic References and Bibliography

Bernanke, B. S., & Blinder, A. S. (1992). The Federal Funds Rate and the Channels of Monetary Transmission. American Economic Review, 82(4), 901-921.

Bernanke, B. S., & Gertler, M. (1995). Inside the Black Box: The Credit Channel of Monetary Policy Transmission. Journal of Economic Perspectives, 9(4), 27-48.

Boot, A. W. A. (2000). Relationship Banking: What Do We Know? Journal of Financial Intermediation, 9(1), 7-25.

Chow, G. C. (1960). Tests of Equality Between Sets of Coefficients in Two Linear Regressions. Econometrica, 28(3), 591-605.

Dunkelberg, W. C., & Wade, H. (2023). NFIB Small Business Economic Trends. National Federation of Independent Business Research Foundation, Washington, D.C.

Engle, R. F., & Granger, C. W. J. (1987). Co-integration and Error Correction: Representation, Estimation, and Testing. Econometrica, 55(2), 251-276.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383-417.

Federal Reserve Board. (2024). Senior Loan Officer Opinion Survey on Bank Lending Practices. Board of Governors of the Federal Reserve System, Washington, D.C.

Friedman, M. (1957). A Theory of the Consumption Function. Princeton University Press, Princeton, NJ.

Gordon, R. J. (1988). The Role of Wages in the Inflation Process. American Economic Review, 78(2), 276-283.

Hamilton, J. D. (1989). A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle. Econometrica, 57(2), 357-384.

Hurst, H. E. (1951). Long-term Storage Capacity of Reservoirs. Transactions of the American Society of Civil Engineers, 116(1), 770-799.

Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263-291.

Krugman, P. (1987). Pricing to Market When the Exchange Rate Changes. In S. W. Arndt & J. D. Richardson (Eds.), Real-Financial Linkages among Open Economies (pp. 49-70). MIT Press, Cambridge, MA.

Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77-91.

Mortensen, D. T., & Pissarides, C. A. (1994). Job Creation and Job Destruction in the Theory of Unemployment. Review of Economic Studies, 61(3), 397-415.

Shannon, C. E. (1948). A Mathematical Theory of Communication. Bell System Technical Journal, 27(3), 379-423.

Sharpe, W. F. (1964). Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. Journal of Finance, 19(3), 425-442.

Tsay, R. S. (2010). Analysis of Financial Time Series (3rd ed.). John Wiley & Sons, Hoboken, NJ.

U.S. Small Business Administration. (2024). Small Business Profile. Office of Advocacy, Washington, D.C.

8. Technical Implementation Notes

The SBO-SAM model is implemented in Pine Script version 6 for the TradingView platform, ensuring compatibility with modern charting and analysis tools. The implementation follows best practices for financial indicator development, including proper error handling, data validation, and performance optimization.

The model includes comprehensive timeframe validation to ensure statistical accuracy and reliability. The indicator operates exclusively on daily (1D) timeframes or higher, including weekly (1W), monthly (1M), and longer periods. This restriction ensures that the statistical analysis maintains appropriate temporal resolution for the underlying economic data sources, which are primarily reported on daily or longer intervals.

When users attempt to apply the model to intraday timeframes (such as 1-minute, 5-minute, 15-minute, 30-minute, 1-hour, 2-hour, 4-hour, 6-hour, 8-hour, or 12-hour charts), the system displays a comprehensive error message in the user's selected language and prevents execution. This safeguard protects users from potentially misleading results that could occur when applying daily-based economic analysis to shorter timeframes where the underlying data relationships may not hold.

The model's statistical calculations are performed using vectorized operations where possible to ensure computational efficiency. The multi-language support system employs Unicode character encoding to ensure proper display of international characters across different platforms and devices.

The alert system utilizes TradingView's native alert functionality, providing users with flexible notification options including email, SMS, and webhook integrations. The alert messages include comprehensive statistical information to support informed decision-making.

The model's visualization system employs professional color schemes designed for optimal readability across different chart backgrounds and display devices. The system includes dynamic color transitions based on momentum and volatility, professional glow effects for enhanced line visibility, and transparency controls that allow users to customize the visual intensity to match their preferences and analytical requirements. The clean confidence band implementation provides clear statistical boundaries without visual distractions, maintaining focus on the analytical content.

Momentum Moving Averages | MisinkoMasterThe Momentum Moving Averages (MMA) indicator blends multiple moving averages into a single momentum-scoring framework, helping traders identify whether market conditions are favoring upside momentum or downside momentum.

By comparing faster, more adaptive moving averages (DEMA, TEMA, ALMA, HMA) against a baseline EMA, the MMA produces a cumulative score that reflects the prevailing strength and direction of the trend.

🔎 Methodology

Moving Averages Used

EMA (Exponential Moving Average) → Baseline reference.

DEMA (Double Exponential Moving Average) → Reacts faster than EMA.

TEMA (Triple Exponential Moving Average) → Even faster, reduces lag further.

ALMA (Arnaud Legoux Moving Average) → Smooth but adaptive, with adjustable σ and offset.

HMA (Hull Moving Average) → Very responsive, reduces lag, ideal for momentum shifts.

Scoring System

Each comparison is made against the EMA baseline:

If another MA is above EMA → +1 point.

If another MA is below EMA → -1 point.

The total score reflects overall momentum:

Positive score → Bullish bias.

Negative score → Bearish bias.

Trend Logic

Bullish Signal → When the score crosses above 0.1.

Bearish Signal → When the score crosses below -0.1.

Neutral or sideways trends are identified when the score remains between thresholds.

📈 Visualization

All five moving averages are plotted on the chart.

Colors adapt to the current score:

Cyan (Bullish bias) → Positive momentum.

Magenta (Bearish bias) → Negative momentum.

Overlapping fills between MAs highlight zones of convergence/divergence, making momentum shifts visually clear.

⚡ Features

Adjustable length parameter for all MAs.

Adjustable ALMA parameters (sigma and offset).

Cumulative momentum score system to filter false signals.

Works across all markets (crypto, forex, stocks, indices).

Overlay design for direct chart integration.

✅ Use Cases

Trend Confirmation → Ensure alignment with market momentum.

Momentum Shifts → Spot when faster MAs consistently outperform the baseline EMA.

Entry & Exit Filter → Avoid trades when the score is neutral or indecisive.

Divergence Visualizer → Filled zones make it easier to see when MAs begin separating or converging.

Low History Required → Unlike most For Loops, this script does not require that much history, making it less lagging and more responsive

⚠️ Limitations

Works best in trending conditions; performance decreases in sideways/choppy ranges.

Sensitivity of signals depends on chosen length and ALMA settings.

Should not be used as a standalone buy/sell system—combine with volume, structure, or higher timeframe analysis.

Scenario Screener — Consolidation → Bullish SetupThe script combines multiple indicators to filter out false signals and only highlight strong conditions:

Consolidation Check

Uses ATR % of price → filters out stocks in tight ranges.

Uses Choppiness Index → confirms sideways/non-trending behavior.

Momentum Shift (Bullish Bias)

MACD Histogram > 0 → bullish momentum starting.

RSI between 55–70 → strength without being overbought.

Stochastic %K & %D > 70 → confirms strong momentum.

Volume & Accumulation

Chaikin Money Flow (CMF > 0) → buying pressure.

Chaikin Oscillator > 0 (debug only) → accumulation phase.

Trend Direction

+DI > -DI (from DMI) → buyers stronger than sellers.

ADX between 18–40 → healthy trend strength (not too weak, not overheated).

Breakout Filter (Optional)

If enabled, requires price to cross above 20 SMA before signal confirmation.

📈 Outputs

✅ Green label (“MATCH”) below the bar when all bullish conditions align.

✅ Background highlight (light green) when signal appears.

✅ Info Table (top-right) summarizing key values:

Signal = True/False

MACD, CMF, Chaikin values

DynamoSent DynamoSent Pro+ — Professional Listing (Preview)

— Adaptive Macro Sentiment (v6)

— Export, Adaptive Lookback, Confidence, Boxes, Heatmap + Dynamic OB/OS

Preview / Experimental build. I’m actively refining this tool—your feedback is gold.

If you spot edge cases, want new presets, or have market-specific ideas, please comment or DM me on TradingView.

⸻

What it is

DynamoSent Pro+ is an adaptive, non-repainting macro sentiment engine that compresses VIX, DXY and a price-based activity proxy (e.g., SPX/sector ETF/your symbol) into a 0–100 sentiment line. It scales context by volatility (ATR%) and can self-calibrate with rolling quantile OB/OS. On top of that, it adds confidence scoring, a plain-English Context Coach, MTF agreement, exportable sentiment for other indicators, and a clean Light/Dark UI.

Why it’s different

• Adaptive lookback tracks regime changes: when volatility rises, we lengthen context; when it falls, we shorten—less whipsaw, more relevance.

• Dynamic OB/OS (quantiles) self-calibrates to each instrument’s distribution—no arbitrary 30/70 lines.

• MTF agreement + Confidence gate reduce false positives by highlighting alignment across timeframes.

• Exportable output: hidden plot “DynamoSent Export” can be selected as input.source in your other Pine scripts.

• Non-repainting rigor: all request.security() calls use lookahead_off + gaps_on; signals wait for bar close.

Key visuals

• Sentiment line (0–100), OB/OS zones (static or dynamic), optional TF1/TF2 overlays.

• Regime boxes (Overbought / Oversold / Neutral) that update live without repaint.

• Info Panel with confidence heat, regime, trend arrow, MTF readout, and Coach sentence.

• Session heat (Asia/EU/US) to match intraday behavior.

• Light/Dark theme switch in Inputs (auto-contrasted labels & headers).

⸻

How to use (examples & recipes)

1) EURUSD (swing / intraday blend)

• Preset: EURUSD 1H Swing

• Chart: 1H; TF1=1H, TF2=4H (default).

• Proxies: Defaults work (VIX=D, DXY=60, Proxy=D).

• Dynamic OB/OS: ON at 20/80; Confidence ≥ 55–60.

• Playbook:

• When sentiment crosses above 50 + margin with Δ ≥ signalK and MTF agreement ≥ 0.5, treat as trend breakout.

• In Oversold with rising Coach & TF agreement, take fade longs back toward mid-range.

• Alerts: Enable Breakout Long/Short and Fade; keep cooldown 8–12 bars.

2) SPY (daytrading)

• Preset: SPY 15m Daytrade; Chart: 15m.

• VIX (D) matters more; preset weights already favor it.

• Start with static 30/70; later try dynamic 25/75 for adaptive thresholds.

• Use Coach: in US session, when it says “Overbought + MTF agree → sell rallies / chase breakouts”, lean momentum-continuation after pullbacks.

3) BTCUSD (crypto, 24/7)

• Preset: BTCUSD 1H; Chart: 1H.

• DXY and BTC.D inform macro tone; keep Carry-forward ON to bridge sparse ticks.

• Prefer Dynamic OB/OS (15/85) for wider swings.

• Fade signals on weekend chop; Breakout when Confidence > 60 and MTF ≥ 1.0.

4) XAUUSD (gold, macro blend)

• Preset: XAUUSD 4H; Chart: 4H.

• Weights tilt to DXY and US10Y (handled by preset).

• Coach + MTF helps separate trend legs from news pops.

⸻

Best practices

• Theme: Switch Light/Dark in Inputs; the panel adapts contrast automatically.

• Export: In another script → Source → DynamoSent Pro+ → DynamoSent Export. Build your own filters/strategies atop the same sentiment.

• Dynamic vs Static OB/OS:

• Static 30/70: fast, universal baseline.

• Dynamic (quantiles): instrument-aware; use 20/80 (default) or 15/85 for choppy markets.

• Confidence gate: Start at 50–60% to filter noise; raise when you want only A-grade setups.

• Adaptive Lookback: Keep ON. For ultra-liquid indices, you can switch it OFF and set a fixed lookback.

⸻

Non-repainting & safety notes

• All request.security() calls use lookahead=barmerge.lookahead_off and gaps=barmerge.gaps_on.

• No forward references; signals & regime flips are confirmed on bar close.

• History-dependent funcs (ta.change, ta.percentile_linear_interpolation, etc.) are computed each bar (not conditionally).

• Adaptive lookback is clamped ≥ 1 to avoid lowest/highest errors.

• Missing-data warning triggers only when all proxies are NA for a streak; carry-forward can bridge small gaps without repaint.

⸻

Known limits & tips

• If a proxy symbol isn’t available on your plan/exchange, you’ll see the NA warning: choose a different symbol via Symbol Search, or keep Carry-forward ON (it defaults to neutral where needed).

• Intraday VIX is sparse—using Daily is intentional.

• Dynamic OB/OS needs enough history (see dynLenFloor). On short histories it gracefully falls back to static levels.

Thanks for trying the preview. Your comments drive the roadmap—presets, new proxies, extra alerts, and integrations.

Trend Compass (Manual)## Trend Compass (Manual) - A Discretionary Trader's Dashboard

### Summary

Trend Compass is a simple yet powerful dashboard designed for discretionary traders who want a constant, visual reminder of their market analysis directly on their chart. Instead of relying on automated indicators, this tool gives you **full manual control** to define the market state across different timeframes or conditions.

It helps you stay aligned with your higher-level analysis (e.g., HTF bias, current market structure) and avoid making impulsive decisions that go against your plan.

### Key Features

- **Fully Manual Control:** You decide the trend. No lagging indicators, no confusing signals. Just your own analysis, displayed clearly.

- **Multiple Market States:** Define each row as an `Uptrend`, `Downtrend`, `Pullback`, or `Neutral` market.

- **Customizable Rows:** Display up to 8 rows. You can label each one however you like (e.g., "D1", "H4", "Market Structure", "Liquidity Bias").

- **Flexible Panel:** Change all colors, text sizes, and place the panel in any of the 9 positions on your chart.

- **Clean & Minimalist:** Designed to provide essential information at a glance without cluttering your chart.

### How to Use

1. **Add to Chart:** Add the indicator to your chart.

2. **Open Settings:** Go into the indicator settings.

3. **Configure Rows:**

- In the "Rows (Manual Control)" section, set the "Number of rows" you want to display.

- For each row, give it a custom **Label** (e.g., "m15").

- Select its current state from the dropdown menu (`Uptrend`, `Downtrend`, etc.).

- To remove a row, simply set its state to `Hidden`.

4. **Customize Style:**

- In the "Panel & Visual Style" section, adjust colors, text sizes, and the panel's position to match your chart's theme.

This tool is perfect for price action traders, ICT/SMC traders, or anyone who values a clean chart and a disciplined approach to their analysis.

Ichimoku + MTF Dashboard (Confidence + Row Shading)Name: Ichimoku + Multi-Timeframe (MTF) Dashboard

Purpose

This indicator is designed to give a complete trend, momentum, and alignment picture of a stock across multiple timeframes (hourly, daily, weekly) using the Ichimoku Kinko Hyo system. It combines:

Classic Ichimoku signals: Tenkan/Kijun crossovers, cloud position (Kumo), Chikou span, and cloud twists.

MTF Dashboard: Aggregates hourly, daily, and weekly Ichimoku conditions into a clean visual table.

Dynamic coloring: Each signal is represented with green/red fills, and rows are shaded for full alignment. Aggregate column highlights mixed signals in yellow.

Entry Signals (Long/Short)The indicator visualizes precise entry signals for long and short setups directly on the price chart. Long is marked with a green triangle-up, short with a red triangle-down. To contextualize trend structure, the Fast EMA (5) is plotted in black and the Slow EMA (20) in blue (line width 1). Signals print only at bar close for reproducible execution. Applicable across all timeframes—ideal for top-down analysis from the 195-minute chart through daily to weekly.

Trend Magic EMA RMI Trend Sniper📌 Indicator Name:

Trend Magic + EMA + MA Smoothing + RMI Trend Sniper

📝 Description:

This is a multi-functional trend and momentum indicator that combines four powerful tools into a single overlay:

Trend Magic – Plots a dynamic support/resistance line based on CCI and ATR.

Helps identify trend direction (green = bullish, red = bearish).

Acts as a trailing stop or dynamic level for trade entries/exits.

Exponential Moving Average (EMA) – Smooths price data to highlight the underlying trend.

Customizable length, source, and offset.

Serves as a trend filter or moving support/resistance.

MA Smoothing + Bollinger Bands (Optional) – Adds a secondary smoothing filter based on your choice of SMA, EMA, WMA, VWMA, or SMMA.

Optional Bollinger Bands visualize volatility expansion/contraction.

Great for spotting consolidations and breakout opportunities.

RMI Trend Sniper – A momentum-based system combining RSI and MFI.

Highlights bullish (green) or bearish (red) conditions.

Plots a Range-Weighted Moving Average (RWMA) channel to gauge price positioning.

Provides visual BUY/SELL labels and optional bar coloring for fast decision-making.

📊 Uses & Trading Applications:

✅ Trend Identification: Spot the dominant market direction quickly with Trend Magic & EMA.

✅ Momentum Confirmation: RMI Sniper helps confirm whether the market has strong bullish or bearish pressure.

✅ Dynamic Support/Resistance: Trend Magic & EMA act as adaptive levels for stop-loss or trailing positions.

✅ Volatility Analysis: Optional Bollinger Bands show squeezes and potential breakout setups.

✅ Entry/Exit Signals: BUY/SELL alerts and color-coded candles make spotting trade opportunities simple.

💡 Best Use Cases:

Swing Trading: Follow Trend Magic + EMA alignment for higher probability trades.

Scalping/Intraday: Use RMI signals with bar coloring for quick momentum entries.

Trend Following Strategies: Ride trends until Trend Magic flips direction.

Breakout Trading: Watch for price closing outside the Bollinger Bands with RMI confirmation.

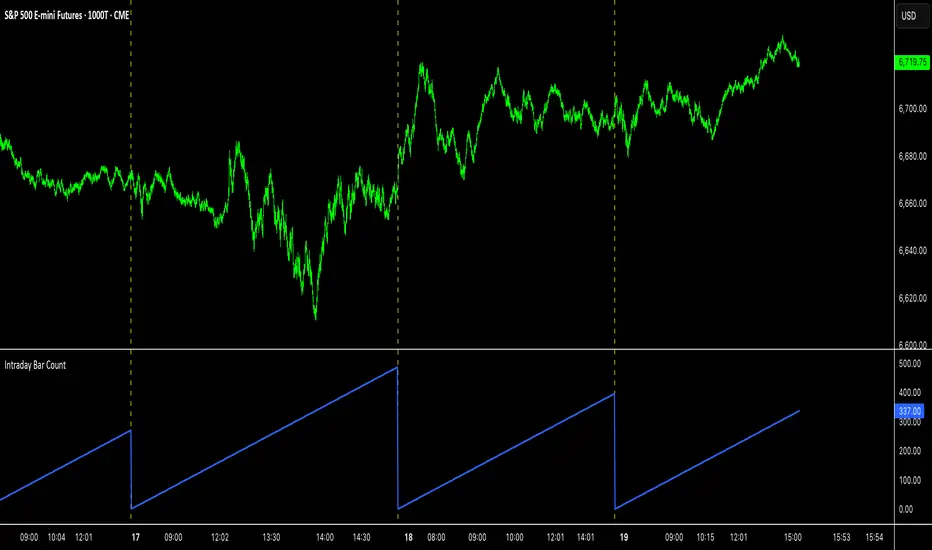

Intraday Bar CounterThis indicator plots a counter on the chart that tracks the number of bars since the beginning of the current day.

The counter resets to zero on the first bar of each new calendar day (midnight). This functionality is provided only on intraday and tick charts.

The indicator is designed to operate on a wide range of symbols without requiring manual adjustments for specific trading sessions.

Z-Score For Loop | MisinkoMasterThe Z-Score For Loop (ZSFL) is a unique trend-following oscillator designed to detect potential reversals and momentum shifts earlier than traditional tools, providing traders with fast, adaptive, and reliable signals.

Unlike common smoothing techniques (moving averages, medians, or modes), the ZSFL introduces a for-loop comparison method that balances speed and noise reduction, resulting in a powerful reversal-detection system.

🔎 Methodology

The indicator is built in two main stages:

Z-Score Calculation

Formula:

Z=(Source−Mean)/Standard Deviation

Z=

Standard Deviation

(Source−Mean)

The user can select the averaging method for the mean: SMA, EMA, WMA, HMA, DEMA, or TEMA.

Recommended: EMA, SMA, or WMA for balanced accuracy.

The choice of biased (sample) or unbiased (population) standard deviation is also available.

➝ On its own, the raw Z-score is fast but noisy, requiring additional filtering.

For Loop Logic (Noise Reduction)

Instead of using traditional smoothing (which adds lag), the indicator applies a for loop comparison.

The current Z-score is compared against previous values over a user-defined range (start → end).

Each comparison adds or subtracts “points”:

+1 point if the current Z-score is higher than a past Z-score.

-1 point if it is lower.

The final value is the cumulative score, reflecting whether the Z-score is generally stronger or weaker than its historical context.

➝ This approach keeps speed intact while removing much of the false noise that raw Z-scores generate.

📈 Trend Logic

Bullish Signal (Cyan) → Triggered when the score crosses above the upper threshold (default +45).

Bearish Signal (Magenta) → Triggered when the score crosses below the lower threshold (default -25).

Neutral → When the score remains between the thresholds.

Thresholds are adjustable, making the tool flexible for different assets and timeframes.

🎨 Visualization

The ZSFL score is plotted as a main oscillator line.

Upper and lower thresholds are plotted as static reference levels.

The price chart can also be color-coded with trend signals (cyan for bullish, magenta for bearish) to provide immediate visual confirmation.

⚡ Features

Adjustable Z-score length (len).

Multiple average types for the mean (SMA, EMA, WMA, HMA, DEMA, TEMA).

Toggle between biased vs. unbiased SD calculations.

Adjustable For Loop range (start, end).

Adjustable upper and lower thresholds for signal generation.

Works as both an oscillator and a price overlay tool.

✅ Use Cases

Reversal Detection → Spot early shifts before price confirms them.

Trend Confirmation → Use thresholds to filter false reversals.

System Filter → Combine with trend indicators to refine entries.

Multi-Timeframe Setup → Works well across different timeframes for swing, day, or intraday trading.

⚠️ Limitations

As with all oscillators, the ZSFL will generate false signals in sideways/choppy markets.

Optimal parameters (length, loop size, thresholds) may differ across assets.