Buy and Sell Signals (Altius Consulting)Generates Buy and Sell signals based on MACD and RSI.

- Plots MACD, Signal & Histogram (optional pane).

- Buy Label (toggle): Bullish MACD crossover + RSI < threshold (no convergence requirement).

- Sell Label: Bearish MACD crossover (MACD crosses below Signal) prints a SELL tag.

- Alert: Provided for convergence-based buy condition (add your own for simple crossover if desired).

Forecasting

Stock Valuation Models - Professional Investment Analysis Tool📊 Overview

Stock Valuation Models is a comprehensive financial analysis indicator that combines multiple valuation methodologies to calculate intrinsic stock value. This professional-grade tool implements 7 different valuation methods , risk assessment framework, and financial health metrics to provide data-driven investment decisions.

🎯 Key Features

📈 Multiple Valuation Methods

Graham's Valuation - Conservative asset-based approach by Benjamin Graham

Multiples Valuation - Market-based P/E and P/B ratios from sector peers

Discounted Cash Flow (DCF) - Future cash flow projections with present value calculation

Dividend Discount Model - Gordon Growth Model for dividend-paying stocks

FCFF Model - Enterprise-level Free Cash Flow to Firm analysis

EVA Model - Economic Value Added measurement above cost of capital

Advanced Multiples - Enterprise Value ratios (EV/EBITDA, EV/Sales)

🏥 Financial Health Metrics

Altman Z-Score - Bankruptcy prediction and financial distress assessment

Piotroski F-Score - 9-point fundamental strength evaluation

Beneish M-Score - Earnings manipulation detection system

Magic Formula - Joel Greenblatt's combined quality and value scoring

⚖️ Risk Assessment Framework

Multi-Factor Risk Scoring - Fundamental, market, quality, and data quality risks

Risk-Adjusted Margin of Safety - Dynamic safety thresholds based on risk level

Position Sizing Guidance - Risk-appropriate investment allocation recommendations

🔍 Data Quality System

Real-Time Quality Tracking - Visual warnings for insufficient data

Fallback Methodology - Alternative calculations when primary data unavailable

Confidence Scoring - Method agreement and data quality assessment

⚙️ Settings & Parameters

Main Settings

Margin of Safety (%) - Minimum discount required before buying (Default: 15%)

Table Font Size - Choose between "Small" and "Normal" text size

Valuation Methods

Graham's Valuation - Best for mature, stable companies with strong fundamentals

Multiples Valuation - Compares to industry peers using dynamic sector ratios

Discounted Cash Flow - Ideal for growth companies with predictable cash flows

Dividend Discount Model - For consistent dividend-paying stocks (disabled by default)

FCFF Model - Enterprise approach for leveraged companies and M&A analysis

EVA Model - Measures value creation above cost of capital

Advanced Multiples - Wall Street standard EV ratios for professional analysis

Additional Metrics

Magic Formula - Combined quality and value scoring system

Altman Z-Score - Bankruptcy risk assessment (Safe >2.99, Distress <1.81)

Piotroski F-Score - Fundamental quality score (Excellent ≥8, Poor <4)

Beneish M-Score - Manipulation detector (High Risk >-2.22, Low Risk ≤-2.22)

🔧 How It Works

Dynamic Calculations

Sector-Based Ratios - Automatically detects company sector and applies appropriate valuation multiples

Economic Integration - Uses real-time risk-free rates, VIX volatility, and GDP growth data

Quality Weighting - Adjusts method weights based on company type (growth/mature/distressed) and market conditions

Negative Value Handling - Shows actual calculated values but excludes negative results from weighted average

Risk-Adjusted Analysis

VIX Integration - Higher market volatility increases required margin of safety

Sector Risk Premiums - Energy and Financial sectors get higher risk multipliers

Quality Adjustments - High Piotroski F-Score companies get lower risk ratings

Data Quality Impact - Insufficient data increases risk score and safety requirements

Visual Display

Horizontal Table Layout - Organized by method groups (Valuation → Results → Risk → Health)

Color-Coded Results - Green/Yellow/Red indicators for risk levels and recommendations

Warning Symbols - ⚠️ for data quality issues, ❌ for excluded negative values

Dollar Amounts - Both percentage and dollar-based margin of safety calculations

📈 Interpretation Guide

💎 Intrinsic Value Results

Weighted Average - Combines all enabled methods based on intelligent weighting

Confidence Level - High/Medium/Low based on method agreement and data quality

Method Count - Number of successful valuation calculations

🎯 Margin of Safety

Percentage - Current discount/premium to calculated intrinsic value

Dollar Amount - Absolute dollar difference per share

Buy Price - Risk-adjusted target purchase price

⚖️ Risk Assessment

Low Risk (Green) - Normal position sizing (3-5%)

Medium Risk (Yellow) - Reduced position sizing (1-3%)

High Risk (Red) - Minimal position sizing (<1%)

📊 Recommendations

STRONG BUY - Low risk + adequate margin + high confidence

BUY - Meets risk-adjusted margin requirements

HOLD - Positive margin but higher risk

SELL - Insufficient margin for risk level

🎓 Educational Tooltips

Every parameter includes detailed explanations accessible by hovering over the setting. Learn about:

When to use each valuation method

How different metrics are calculated

Interpretation thresholds and ratings

Risk factors and quality indicators

💡 Best Practices

🚀 For Growth Stocks

Enable DCF and Advanced Multiples

Focus on Piotroski F-Score for quality assessment

Use higher margin of safety due to volatility

💰 For Value Stocks

Enable Graham's and Multiples Valuation

Check Altman Z-Score for financial stability

Consider Magic Formula rating

📈 For Dividend Stocks

Enable Dividend Discount Model

Focus on sustainable dividend coverage

Check for consistent dividend history

⚠️ For Distressed Situations

Prioritize Graham's asset-based approach

Monitor Altman Z-Score closely

Use higher risk-adjusted margins

⚠️ Important Notes & Data Limitations

📅 Data Timing Considerations

Fundamental Data Lag - Company financial data (earnings, cash flows, balance sheet items) may be 1-3 months behind current market conditions

Quarterly Reporting Delays - Most recent available data reflects the company's situation as of the last filed quarterly/annual report

Market vs. Fundamentals Gap - Stock prices react instantly to news, while fundamental data updates occur periodically

Accuracy Impact - Recent business changes, market events, or company developments may not be reflected in current calculations

🔧 Technical Limitations

Data Dependencies - Requires fundamental data availability from TradingView

Quality Warnings - Pay attention to ⚠️ symbols indicating insufficient data

Risk Context - Always consider risk score in investment decisions

Market Conditions - Tool automatically adjusts for market volatility (VIX)

Sector Specificity - Ratios automatically adjust based on company's sector

💡 Best Practice Recommendations

Supplement with Current Analysis - Always combine with recent news, earnings calls, and management guidance

Monitor Data Quality - Check when the underlying financial data was last updated

Consider Market Context - Factor in recent market events that may affect company performance

Use as Starting Point - Treat calculations as baseline analysis requiring additional research

🔗 Methodology

Based on established academic research and professional practices:

Benjamin Graham - Security Analysis principles

Joel Greenblatt - Magic Formula methodology

Edward Altman - Z-Score bankruptcy prediction

Joseph Piotroski - Fundamental analysis scoring

Messod Beneish - Earnings manipulation detection

Modern Portfolio Theory - Risk-adjusted decision making

This indicator is designed for educational and analytical purposes. Always conduct additional research and consider consulting with financial professionals before making investment decisions.

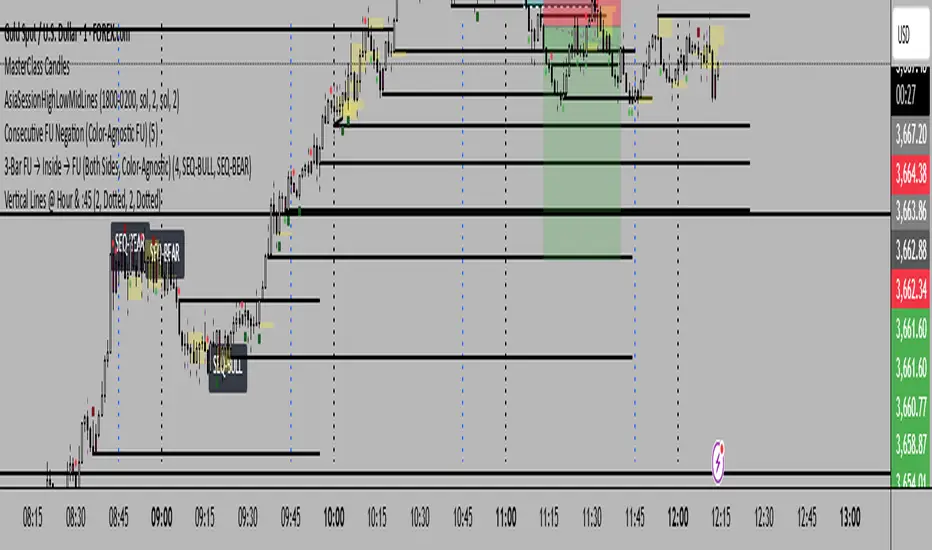

Vertical Lines @ Hour & :45vertical lines at hour and 45 past each hour

when manipulation is most likely to happen

Otekura Range Trade Algorithm [Tradebuddies]The Range Trade Algorithm calculates the levels for Monday.

On the chart you will see that the Monday levels will be marked as 1 0 -1.

The M High level calculates Monday's high close and plots it on the screen.

M Low calculates the low close of Monday and plots it on the screen.

The coloured lines on the screen are the points of the range levels formulated with fibonacci values.

The indicator has its own Value table. The prices of the levels are written.

Potential Range breakout targets tell prices at points matching the fibonacci values. These are Take profit or reversal points.

Buy and Sell indicators are determined by the range breakout.

Users can set an alarm on the indicator and receive direct notification with their targets when a new range occurs.

Fib values are multiplied by range values and create an average target according to the price situation. These values represent an area. Breakdown targets show that the target is targeted until the area.

MTF Levels [OmegaTools]📖 Introduction

The Ω Levels Indicator is a complete market structure and level-mapping framework designed to help traders identify key zones where price is likely to react.

It blends classic technical anchors (VWAP, pivots, means, standard deviations) with modern statistical pattern recognition to dynamically project areas of manipulation, extension, and equilibrium.

At its core, Ω Levels creates an evolving map of market balance vs. imbalance, showing traders where liquidity is most likely to build and where price could pivot or accelerate.

But what makes it truly unique is the Pivot Forecaster — an embedded predictive engine that applies machine-learning inspired logic to recognize conditions that historically precede market turning points.

🔎 Key Features

Customizable Levels Framework

Define up to three levels (manipulation, extensions, VWAP, pivots, stdev bands, or prior extremes).

Choose mean references such as Open, VWAP, Pivot Mean, or Previous Session Mean.

Style controls (solid, dotted, dashed) and fill modes (internal, external, ranges) allow you to adapt the chart to your visual workflow.

Dynamic Zone Highlighting

Automatic fills between internal/external levels, or between specific level pairs (1–2, 1–3, 2–3).

Makes it easy to visualize value areas, expansions, and compression zones at a glance.

Multi-Timeframe Anchoring

Works on any timeframe, but calculations can be anchored to a higher timeframe (e.g., show daily VWAP & pivots on a 15m chart).

This allows traders to align intraday execution with higher timeframe context.

Pivot Forecaster (Machine Learning / Pattern Recognition)

This is the advanced predictive component.

The algorithm collects historical conditions observed around pivot highs and lows (volume state, ATR state, % candle expansion, oscillator conditions).

It then builds statistical “profiles” of typical pivot behavior and compares them in real-time against current market conditions.

When conditions match the “signature” of a pivot, the indicator highlights a Forecast Pivot High or Forecast Pivot Low (displayed as small diamond markers).

This functions as a pattern-recognition system, effectively learning from past pivots to anticipate where the next turning point is more likely to occur.

⚡ How Traders Can Use It

Intraday Execution: Use VWAP, manipulation, and extension levels to frame trades around liquidity zones.

Swing Context: Overlay higher timeframe pivots and means to guide medium-term positioning.

Fade Setups: Forecasted pivots often coincide with exhaustion zones where fading momentum carries edge.

Breakout Validation: When price breaks a structural level but the forecaster does not confirm a pivot, continuation probability is higher.

Risk Management: Levels provide natural stop/target placements, while pivot forecasts serve as warning signals for potential reversals.

⚙️ Settings Overview

Timeframe: Choose the anchor timeframe for calculations (default: Daily).

Means: Two selectable mean references (Open, VWAP, Pivot Point, Previous Mean).

Levels: Three levels can be customized (Manipulation, Extension, 1–2 StDev, Pivot Point, VWAP, Previous Extremes).

Fill Modes: Highlight zones between internal/external levels or custom ranges.

Visual Customization: Colors, line styles, fill opacity, and toggle for old levels.

Pivot Forecaster: Fully automated — no settings required, it adapts to instrument and timeframe.

🧭 Best Practices

Align Levels With Market Profile: Treat the levels as dynamic S/R zones and watch how price interacts with them.

Use Forecaster as Confirmation: The diamonds are not standalone signals; they are context filters that help you decide whether a move has higher reversal odds.

Higher Timeframe Anchoring: On intraday charts, set the timeframe to Daily or Weekly to trade with institutional levels.

Combine With ATR: Pair with the Ω ATR Indicator to size positions according to volatility while Ω Levels provides the structural roadmap.

📌 Summary

The Ω Levels Indicator is more than a level plotter — it’s a market map + predictive engine.

By combining traditional levels with an intelligent pivot forecaster, it gives traders both the static structure of where price should react, and the dynamic signal of where it is likely to react next.

This dual-layer approach — structural + predictive — makes it an invaluable tool for discretionary intraday traders, swing traders, and anyone who wants to anticipate price behavior instead of just reacting to it.

Implied Volatility RangeThe Implied Volatility Range is a forward-looking tool that transforms option market data into probability ranges for future prices. Based on the lognormal distribution of asset prices assumed in modern option pricing models, it converts the implied volatility curve into a volatility cone with dynamic labels that show the market’s expectations for the price distribution at a specific point in time. At the selected future date, it displays projected price levels and their percentage change from today’s close across 1, 2, and 3 standard deviation (σ) ranges:

1σ range = ~68.2% probability the price will remain within this range.

2σ range = ~95.4% probability the price will remain within this range.

3σ range = ~99.7% probability the price will remain within this range.

What makes this indicator especially useful is its ability to incorporate implied volatility skew. When only ATM IV (%) is entered, the indicator displays the standard Black–Scholes lognormal distribution. By adding High IV (%) and Low IV (%) values tied to strikes above and below the current price, the indicator interpolates between these inputs to approximate the implied volatility skew. This adjustment produces a market-implied probability distribution that indicates whether the option market is leaning bullish or bearish, based on the data entered in the menu:

ATM IV (%) = Implied volatility at the current spot price (at-the-money).

High IV (%) = Implied volatility at a strike above the current spot price.

High Strike = Strike price corresponding to the High IV input (OTM call).

Low IV (%) = Implied volatility at a strike below the current spot price.

Low Strike = Strike price corresponding to the Low IV input (OTM put).

Expiration (Day, Month, Year) = Option expiration date for the projection.

Once these inputs are entered, the indicator calculates implied probability ranges and, if both High IV and Low IV values are provided, adjusts for skew to approximate the option market’s distribution. If no implied volatility data is supplied, the indicator defaults to a lognormal distribution based on historical volatility, using past realized volatility over the same forward horizon. This keeps the tool functional even without implied volatility inputs, though in that case the output represents only an approximation of ATM IV, not the actual market view.

In summary, the Implied Volatility Range is a powerful tool that translates implied volatility inputs into a clear and practical estimate of the market’s expectations for future prices. It allows traders to visualize the probability of price ranges while also highlighting directional bias, a dimension often difficult to interpret from traditional implied volatility charts. It should be emphasized, however, that this tool reflects only the market’s expectations at a specific point in time, which may change as new information and trading activity reshape implied volatility.

Piano Frequency LevelsPiano Frequency Levels

This indicator applies the mathematical principles of musical harmony to market analysis, creating support and resistance levels based on authentic piano frequency ratios. Drawing from centuries-old musical theory, it maps the precise mathematical relationships between piano keys to price levels.

How It Works: The indicator uses the exact frequency ratios from equal temperament tuning - the same mathematical system that makes pianos sound harmonious. Each level represents an actual piano key frequency, scaled proportionally to your chosen anchor price.

Key Features:

• Piano-Based Ratios: Uses authentic 12-tone equal temperament frequency relationships (1.05946 ratio between semitones)

• Directional Intelligence: Automatically creates ascending levels from lows (resistance) or descending levels from highs (support)

• Musical Note Labels: Optional display of actual piano key names (C4, D#5, F6, etc.) alongside price levels

• Black Key Subdivisions: Toggle authentic sharp/flat keys between natural notes for additional precision

• Octave Color Coding: Each musical octave displays in a different color for easy visual identification

• Anchor Reference: Bright green line clearly marks your C-note reference point

Musical Foundation: Every level corresponds to an actual piano key. The anchor point represents "C" (the musical root), with levels progressing through the natural musical sequence: C, D, E, F, G, A, B, then repeating in higher octaves. This creates proportional spacing that mirrors the harmonic relationships musicians have used for centuries.

Usage:

1. Set your anchor to a significant market high or low

2. Choose your desired number of levels (typically 12-24 for 1-2 octaves)

3. Enable "Add Black Keys" for additional intermediate levels

4. Enable "Show Note Names" to see which piano key each level represents

The Theory: Musical harmony is based on precise mathematical ratios that create pleasing relationships between frequencies. These same mathematical principles may manifest in market movements, as price action often exhibits proportional relationships similar to musical intervals.

Unique Advantages:

• Based on established mathematical principles rather than arbitrary ratios

• Provides both major levels (white keys) and intermediate levels (black keys)

• Automatically adapts direction based on anchor type (high vs low)

• Maintains authentic musical relationships across all timeframes and price ranges

Important Note: This indicator presents a theoretical framework for market analysis. Like all technical analysis tools, it should be used in conjunction with other forms of analysis and proper risk management. The musical ratios provide a unique perspective on potential support and resistance levels, but past performance does not guarantee future results.

Transform your charts into a musical instrument and discover the hidden harmonies in market movements.

Expected Value Monte CarloI created this indicator after noticing that there was no Expected Value indicator here on TradingView.

The EVMC provides statistical Expected Value to what might happen in the future regarding the asset you are analyzing.

It uses 2 quantitative methods:

Historical Backtest to ground your analysis in long-term, factual data.

Monte Carlo Simulation to project a cone of probable future outcomes based on recent market behavior.

This gives you a data-driven edge to quantify risk, and make more informed trading decisions.

The indicator includes:

Dual analysis: Combines historical probability with forward-looking simulation.

Quantified projections: Provides the Expected Value ($ and %), Win Rate, and Sharpe Ratio for both methods.

Asset-aware: Automatically adjusts its calculations for Stocks (252 trading days) and Crypto (365 days) for mathematical accuracy.

The projection cone shows the mean expected path and the +/- 1 standard deviation range of outcomes.

No repainting

Calculation:

1. Historical Expected Value:

This is a systematic backtest over thousands of bars. It calculates the return Rᵢ for N past trades (buy-and-hold). The Historical EV is the simple average of these returns, giving a baseline performance measure.

Historical EV % = (Σ Rᵢ) / N

2. Monte Carlo Projection:

This projection uses the Geometric Brownian Motion (GBM) model to simulate thousands of future price paths based on the market's recent behavior.

It first measures the drift (μ), or recent trend, and volatility (σ), or recent risk, from the Projection Lookback period. It then projects a final return for each simulation using the core GBM formula:

Projected Return = exp( (μ - σ²/2)T + σ√T * Z ) - 1

(Where T is the time horizon and Z is a random variable for the simulation.)

The purple line on the chart is the average of all simulated outcomes (the Monte Carlo EV). The cone represents one standard deviation of those outcomes.

The dashed lines represent one standard deviation (+/- 1σ) from the average, forming a cone of probable outcomes. Roughly 68% of the simulated paths ended within this cone.

This projection answers the question: "If the recent trend and volatility continue, where is the price most likely to go?"

Here's how to read the indicator

Expected Value ($/%): Is my average trade profitable?

Win Rate: How often can I expect to be right?

Sharpe Ratio: Am I being adequately compensated for the risk I'm taking?

User Guide

Max trade duration (bars): This is your analysis timeframe. Are you interested in the probable outcome over the next month (21 bars), quarter (63 bars), or year (252 bars)?

Position size ($): Set this to your typical trade size to see the Expected Value in real dollar terms.

Projection lookback (bars): This is the most important input for the Monte Carlo model. A short lookback (e.g., 50) makes the projection highly sensitive to recent momentum. Use this to identify potential recency bias. A long lookback (e.g., 252) provides a more stable, long-term projection of trend and volatility.

Historical Lookback (bars): For the historical backtest, more data is always better. Use the maximum that your TradingView plan allows for the most statistically significant results.

Use TP/SL for Historical EV: Check this box to see how the historical performance would have changed if you had used a simple Take Profit and Stop Loss, rather than just holding for the full duration.

I hope you find this indicator useful and please let me know if you have any suggestions. 😊

Stop Loss Advisor📊 Stop Loss Advisor - Advanced Risk Management Tool

A sophisticated Pine Script v5 indicator designed to suggest optimal stop loss distances based on market volatility, combining ATR and Standard Deviation analysis for precise risk management.

🎯 What Makes This Different from Bollinger Bands?

While Bollinger Bands focus on mean reversion and overbought/oversold conditions using a moving average center line, this indicator is specifically designed for risk management . It creates dynamic bands around the current price to suggest where NOT to place your stop loss, preventing you from being stopped out by normal market noise.

⚡ Key Features

Dynamic ATR Calculation - Fully customizable ATR periods with adaptive volatility filtering

Standard Deviation Integration - Optional StdDev component for enhanced statistical accuracy

Multiple Combination Modes - Average, Maximum, ATR Weighted, or StdDev Weighted

Flexible Price Sources - Choose from Close, HL2, HLC3, or OHLC4

Automatic Pip Calculation - Works across all instruments with automatic pip value detection

Smart Alerts System - Get notified when suggested stop loss exceeds your base risk tolerance

Real-time Information Table - Displays current values and risk status

Visual Labels - Shows exact pip distances directly on chart

Band Smoothing - Prevents erratic movements with customizable averaging

📈 How It Works

ATR Analysis : Calculates Average True Range to measure current market volatility

Statistical Enhancement : Optionally combines with Standard Deviation for more robust calculations

Dynamic Bands : Creates upper and lower bands that expand/contract with volatility

Pip Conversion : Automatically converts distances to pips for easy interpretation

Risk Assessment : Compares suggested distances with your base stop loss tolerance

🔧 Customization Options

ATR Settings:

Customizable ATR period (default: 14)

Adjustable multiplier with 0.1 step precision

Optional volatility filtering for enhanced sensitivity

Standard Deviation (Optional):

Independent period and multiplier settings

Multiple price source options

Four combination modes with ATR

Visual Customization:

Fully customizable colors for all elements

Multiple line styles (solid, dashed, dotted)

Optional band filling with transparency control

Show/hide ATR line overlay

Configurable band smoothing

💡 Perfect For

Forex Traders - Especially effective on major pairs and XAUUSD

Risk Managers - Calculate optimal stop distances before entering trades

Scalpers - Avoid being stopped out by normal market fluctuations

Swing Traders - Adapt stop losses to current volatility conditions

📊 Indicator Values

The information table displays:

Current ATR Value (in pips)

Suggested Long Stop Loss (distance in pips)

Suggested Short Stop Loss (distance in pips)

Risk Status - "SAFE" or "HIGH RISK" based on your base tolerance

Standard Deviation Value (when enabled)

Combination Method (when using both ATR and StdDev)

⚠️ Important Notes

This indicator suggests minimum stop loss distances, not entry/exit signals

Always combine with your trading strategy and risk management rules

Do not use as a standalone trading system

Backtesting recommended before live implementation

Default settings work well for most scenarios, but optimization is encouraged

🎨 Default Configuration

ATR Period: 14

ATR Multiplier: 2.0

Price Source: Close

Base Stop Loss: 20 pips

Band Smoothing: 3 periods

Standard Deviation: Optional (20 period, 2.0 multiplier)

🚀 Getting Started

Add the indicator to your chart

Set your base stop loss tolerance in the settings

Choose your preferred price source and ATR parameters

Enable Standard Deviation for enhanced accuracy (optional)

Monitor the information table for real-time risk assessment

Use the suggested distances as minimum stop loss levels

Pro Tip: In low volatility markets, the bands will contract suggesting tighter stops. In high volatility periods, they expand warning you to use wider stops to avoid being stopped out by normal price action.

📝 Version History & Updates

This indicator is actively maintained and updated based on user feedback. Future enhancements may include multi-timeframe analysis, trend-based asymmetric bands, and additional statistical measures.

Transform your risk management approach with data-driven stop loss suggestions that adapt to real market conditions!

The Maker StrategyDESCRIPTION

The Maker Strategy is a trend-following system built around exponential moving averages (EMAs). By analyzing the alignment of multiple EMAs, the strategy identifies strong bullish or bearish momentum and generates precise entry signals. This method is designed to capture sustained trends while filtering out sideways or noisy market conditions.

USER INPUTS :

• EMA 1 Length (Default: 30)

• EMA 2 Length (Default: 35)

• EMA 3 Length (Default: 40)

• EMA 4 Length (Default: 45)

• EMA 5 Length (Default: 50)

• EMA 6 Length (Default: 60)

LONG CONDITION :

A long signal is triggered when all EMAs are perfectly aligned in ascending order:

EMA1 > EMA2 > EMA3 > EMA4 > EMA5 > EMA6

SHORT CONDITION :

A short signal is triggered when all EMAs are perfectly aligned in descending order:

EMA1 < EMA2 < EMA3 < EMA4 < EMA5 < EMA6

WHY IT IS UNIQUE:

Unlike traditional EMA crossover systems that rely on just 2 or 3 moving averages, The Maker Strategy uses 6 EMAs in sequence. This ensures that trades are only taken when there is clear and strong market momentum. The approach minimizes false signals in ranging markets and focuses on capturing trends with higher probability setups.

HOW USER CAN BENEFIT FROM IT :

• Clear entry alerts for both long and short positions.

• Visual confirmation through candle coloring and EMA band fills.

• Works on multiple timeframes and instruments (stocks, forex, crypto, indices).

• Helps traders stay on the right side of the trend while avoiding whipsaws.

• A simple yet effective tool for those who want a disciplined, rules-based strategy.

Adaptive Log Trend ChannelOne-line Summary / 一句话简介

EN: Adaptive log-scale trend channel using Pearson-optimized regression and deviation bands.

中文:基于皮尔逊优化回归的自适应对数趋势通道,带标准差波动带。

Full Description / 完整介绍

What it does / 功能

EN: This indicator fits a log-linear regression to price and builds a trend channel with ±k·σ deviation bands. It automatically selects the period with the highest Pearson correlation (R), ensuring the channel best matches the dominant market trend.

中文:该指标通过价格的对数线性回归拟合趋势,并在中线上下绘制 ±k·σ 偏差通道。它会自动选择皮尔逊相关系数 (R) 最高的周期,从而保证通道与主要趋势最贴合。

Why it’s useful / 适用价值

EN:

Naturally fits assets with multiplicative growth (crypto, tech stocks).

Adapts dynamically to different market regimes.

Provides CAGR estimates on Daily/Weekly charts for trend strength evaluation.

中文:

自然适用于呈现乘法增长的资产(如加密货币与科技股)。

可动态适应不同的市场阶段。

在日线/周线图上提供 趋势年化收益率 (CAGR),帮助评估趋势强度。

How it works / 工作原理

EN:

Computes log(price) → regression slope & intercept.

Draws a midline (log regression projection).

Upper & lower bands = ±k·σ in log space.

Info panel shows: Auto-Selected Period, Trend Strength (or Pearson’s R), and CAGR.

中文:

对价格取对数 → 计算回归斜率与截距。

绘制 中线(对数回归投影)。

上下轨 = 对数空间中的 ±k·σ。

信息面板显示:自动选择周期、趋势强度(或皮尔逊 R 值)、以及 CAGR 年化收益率。

Key Settings / 主要参数

EN:

Long-Term Mode: Uses extended periods (300–1200).

Deviation Multiplier (k): Controls channel width (default 2.0).

Styles: Colors, line type, and extension.

Panel Options: Toggle auto-period, Pearson’s R, and CAGR.

中文:

长期模式:采用更长周期 (300–1200)。

偏差倍数 (k):控制通道宽度(默认 2.0)。

样式:可设置颜色、线型、延长方式。

信息面板:可开关自动周期、皮尔逊 R、CAGR。

Notes / 注意事项

EN:

CAGR is only available on Daily/Weekly timeframes.

Regression-based tools may repaint as new bars form; treat it as context, not signals.

中文:

CAGR 仅在日线与周线周期可用。

回归类指标在新K线形成时可能重绘,仅用于趋势参考而非交易信号。

Shashwat Khurana's Pivot + Mean Reversion + RSI (Signals Only)Show BUY labels below bars when a bullish reversal is detected.

Show SELL labels above bars when a bearish reversal is detected.

Uses pivot levels, mean reversion, big candle, RSI, and volume filters.

Measured Move Volume XIndicator Description

The "Measured Move Volume X" indicator, developed for TradingView using Pine Script version 6, projects potential price targets based on the measured move concept, where the magnitude of a prior price leg (Leg A) is used to forecast a subsequent move. It overlays translucent boxes on the chart to visualize bullish (green) or bearish (red) price projections, extending them to the right for a user-specified number of bars. The indicator integrates volume analysis (relative to a simple moving average), RSI for momentum, and VWAP for price-volume weighting, combining these into a confidence score to filter entry signals, displayed as triangles on breakouts. Horizontal key level lines (large, medium, small) are drawn at significant price points derived from the measured moves, with customizable thresholds, colors, and styles. Exhaustion hints, shown as orange labels near box extremes, indicate potential reversal points. Anomalous candles, marked with diamond shapes, are identified based on volume spikes and body-to-range ratios. Optional higher timeframe candle coloring enhances context. The indicator is fully customizable through input groups for lookback periods, transparency, and signal weights, making it adaptable to various assets and timeframes.

Adjustment Tips for Optimization

To optimize the "Measured Move Volume X" indicator for specific assets or timeframes, adjust the following input parameters:

Leg A Lookback (default: 14 bars): Increase to 20-30 for volatile markets (e.g., cryptocurrencies) to capture larger price swings; decrease to 5-10 for intraday charts (e.g., stocks) for faster signals.

Extend Box to the Right (default: 30 bars): Extend to 50+ for daily or weekly charts to project further targets; shorten to 10-20 for lower timeframes to reduce clutter.

Volume SMA Length (default: 20) and Relative Volume Threshold (default: 1.5): Lower the threshold to 1.2-1.3 for low-volume assets (e.g., commodities) to detect subtler spikes; raise to 2.0+ for high-volume equities to filter noise. Match SMA length to RSI length for consistency.

RSI Parameters (default: length 14, overbought 70, oversold 30): Set overbought to 80 and oversold to 20 in trending markets to reduce premature exit signals; shorten length to 7-10 for scalping.

Key Level Thresholds (default: large 10%, medium 5%, small 5%): Increase thresholds (e.g., large to 15%) for volatile assets to focus on significant moves; disable medium or small lines to declutter charts.

Confidence Score Weights (default: volume 0.5, VWAP 0.3, RSI 0.2): Increase volume weight (e.g., 0.7) for volume-driven markets like futures; emphasize RSI (e.g., 0.4) for momentum-focused strategies.

Anomaly Detection (default: volume multiplier 1.5, small body ratio 0.2, large body ratio 0.75): Adjust the volume multiplier higher for stricter anomaly detection in noisy markets; fine-tune body-to-range ratios based on asset-specific candle patterns.

Use TradingView’s replay feature to test adjustments on historical data, ensuring settings suit the chosen market and timeframe.

Tips for Using the Indicator

Interpreting Signals: Green upward triangles indicate bullish breakout entries when price exceeds the prior high with a confidence score ≥40; red downward triangles signal bearish breakouts. Use these to identify potential entry points aligned with the projected box targets.

Box Projections: Bullish boxes project upward targets (top of box) equal to the prior leg’s height added to the breakout price; bearish boxes project downward. Monitor price action near box edges for target completion or reversal.

Exhaustion Hints: Orange labels near box tops (bullish) or bottoms (bearish) suggest potential exhaustion when price deviates within the set percentage (default: 5%) and RSI or volume conditions are met. Use these as cues to watch for reversals.

Key Level Lines: Large, medium, and small lines mark significant price levels from box tops/bottoms. Use these as potential support/resistance zones, especially when drawn with high volume (colored differently).

Anomaly Candles: Orange diamonds highlight candles with unusual volume/body characteristics, indicating potential reversals or pauses. Combine with box levels for context.

Higher Timeframe Coloring: Enable to color bars based on higher timeframe candle closures (e.g., 1, 2, 5, or 15 minutes) for added trend context.

Customization: Toggle "Only Show Bullish Moves" to focus on bullish setups. Adjust transparency and line styles for visual clarity. Test settings to balance signal frequency and chart readability.

Inputs: Organized into groups (e.g., "Measured Move Settings") using input.int, input.float, input.color, and input.bool for user customization, with tooltips for clarity.

Calculations: Computes relative volume (ta.sma(volume, volLookback)), VWAP (ta.vwap(hlc3)), RSI (ta.rsi(close, rsiLength)), and prior leg extremes (ta.highest/lowest) using prior bar data ( ) to prevent repainting.

Boxes and Lines: Creates boxes (box.new) for bullish/bearish projections and lines (line.new) for key levels. The f_addLine function manages line arrays (array.new_line), capping at maxLinesCount to avoid clutter.

Confidence Score: Combines volume, VWAP distance, and RSI into a weighted score (confScore), filtering entries (≥40). Rounded for display.

Exhaustion Hints: Functions like f_plotBullExitHint assess price deviation, RSI, and volume decrease, using label.new for dynamic orange labels.

Entry Signals and Plots: plotshape displays triangles for breakouts; plot and hline show VWAP and RSI levels; request.security handles higher timeframe coloring.

Anomaly Detection: Identifies candles with small-body high-volume or large-body average-volume patterns via ratios, plotted as diamonds.

DZ/SZ - HFM by MamaRight-Empty Wick Zones (MTF) draws Supply/Demand zones from the remaining wick of adjacent opposite-color candles (Classic & Non-classic rules). Zones extend right only through empty space and stop at the first touching candle. Multi-TF scan (H1/H4/1D/1W/1M) with TF-colored boxes and labels showing Demand/Supply + H/L.

Demand (red → green, adjacent):

Classic: if the red candle’s lower wick is longer than the green’s → zone = (the “excess” red wick).

Non-classic: if the red’s lower wick is shorter or equal → zone = (use the longer green wick).

Supply (green → red, adjacent):

Classic: if the green candle’s upper wick is longer than the red’s → zone = (the “excess” green wick).

Non-classic: if the green’s upper wick is shorter or equal → zone = (use the longer red wick).

After a zone is created, the box extends right and terminates at the very first bar whose price range (body or wick) overlaps the zone → ensures the plotted area is genuinely right-empty.

What you see

Zone boxes with distinct colors per timeframe (e.g., H1/H4/1D/1W/1M).

Optional labels on each box: H4 Demand / H1 Supply, plus H/L prices of the zone.

Labels can sit at the left edge or follow the right edge of the box.

Inputs

Toggles: Demand Classic / Demand Non-classic / Supply Classic / Supply Non-classic.

Timeframes to scan: H1, H4, 1D, 1W, 1M.

Min zone thickness (price): minimum height of a zone (in price units).

Initial right extension (bars): initial box length; the script auto-cuts at the first touch.

Show labels / place labels at the right edge.

How to use (suggestion)

Use higher TF (e.g., 1D) for bias and lower TFs (H1/H4) for execution zones.

Keep only the rule set (Classic/Non-classic) that matches your playbook.

Treat zones as areas of interest—wait for your own confirmations (e.g., swing rejection, wick re-entry, structure shift, volume cues) and manage risk accordingly.

Notes

Because zones are sourced from higher TFs via request.security, the drawing can update intrabar; a zone is final once the source TF bar closes.

Min zone thickness uses price units (e.g., on XAUUSD, 1.00 ≈ $1).

This tool is an analytical aid, not financial advice or an entry/exit signal.

อินดิเคเตอร์ DZ/SZ - HFM by Mama ใช้หา Demand/Supply zone จาก “ไส้ที่เหลือ” ของ คู่แท่งสีตรงข้ามที่ติดกัน แล้ววาดเป็นกล่อง ยืดไปทางขวาเฉพาะช่วงที่ว่าง และ หยุดตรงแท่งแรกที่เข้ามาแตะโซน รองรับหลาย Timeframe (H1/H4/1D/1W/1M) พร้อมสีแยก TF และป้ายกำกับ Demand/Supply + H/L ของโซน

รายละเอียดการทำงาน (ไทย)

แนวคิดหลัก

Demand: เลือกคู่ แดง→เขียว ที่ “ติดกัน”

Classic: ถ้า ไส้ล่าง ของแท่งแดงยาวกว่าแท่งเขียว → โซน =

Non-classic: ถ้า ไส้ล่าง ของแท่งแดงสั้นกว่าหรือเท่าเขียว → โซน =

Supply: เลือกคู่ เขียว→แดง ที่ “ติดกัน”

Classic: ถ้า ไส้บน ของแท่งเขียวยาวกว่าแท่งแดง → โซน =

Non-classic: ถ้า ไส้บน ของแท่งเขียวสั้นกว่าหรือเท่าแดง → โซน =

เมื่อสร้างโซนแล้ว กล่องจะ ยืดทางขวา ไปเรื่อย ๆ และ หยุดทันทีเมื่อมีแท่งแรกที่ช่วงราคา (ไส้หรือตัวแท่ง) ทับซ้อนกับโซน ⇒ ได้ “พื้นที่ขวาว่าง” ตามโจทย์

สิ่งที่แสดงบนกราฟ

กล่องโซนสีตาม Timeframe (เช่น H1=ฟ้า, H4=เขียว, 1D=ส้ม, 1W=ม่วง, 1M=เทา)

Label ที่มุมกล่อง: H4 Demand / H1 Supply + ราคาของ High/Low ของโซน

(เลือกวาง ซ้าย หรือ ขอบขวา ของกล่องได้ในตั้งค่า)

ตัวเลือกสำคัญใน Settings

เปิด/ปิด: Demand Classic / Demand Non-classic / Supply Classic / Supply Non-classic

เลือก TF ที่จะสแกน: H1, H4, 1D, 1W, 1M

Min zone thickness (price): กำหนด “ความหนา” ขั้นต่ำของโซน (หน่วยเป็นราคา เช่น XAUUSD = ดอลลาร์)

Initial right extension (bars): ความยาวยืดเริ่มต้น (อินดี้จะตัดให้สั้นลงเองเมื่อมีแท่งมาแตะ)

แสดง Label บนโซน และ วาง Label ที่ขอบขวากล่อง

วิธีใช้แนะนำ

เลือก TF ที่ต้องการ (เช่น ให้ H1/H4 เป็นโซนเทรดละเอียด และ 1D ใช้กรองทิศ)

เปิดเฉพาะโหมด (Classic/Non-classic) ที่ตรงกับแนวคิดการเทรดของคุณ

ใช้โซนเป็นบริเวณ “สนใจ” แล้วรอพฤติกรรมราคา/สัญญาณยืนยันเสริม (เช่น สวิงกลับ, rejection wick, โวลลุ่ม, หรือโครงสร้างจบคลื่น)

หมายเหตุสำคัญ

อินดี้ใช้ข้อมูลข้าม TF; สัญญาณจาก TF สูง อาจเปลี่ยนระหว่างแท่งยังไม่ปิด (ลักษณะ intrabar update) โซนจะ “นิ่ง” เมื่อแท่งของ TF ต้นทาง ปิดแล้ว

หน่วยของ Min zone thickness เป็น หน่วยราคา ไม่ใช่ pips (XAUUSD: 1.00 = $1)

อินดี้ไม่ได้ให้สัญญาณเข้า–ออกอัตโนมัติ ควรใช้ร่วมกับแผนเทรดและการจัดการความเสี่ยง

Short Sellingell signal when RSI < 40, MACD crosses zero or signal line downward in negative zone, close below 50 EMA, candle bearish.

Strong sell signal confirmed on 5-minute higher timeframe with same conditions.

Square off half/full signals as defined.

Target lines drawn bold based on previous swing lows and extended as described.

Blue candle color when RSI below 30.

One sell and one full square off per cycle, blocking repeated sells until full square off.

Value Investing IndicatorThis is based on PeterNagy Indicator. I just update it from v.4 to v.6 and modify. Open for tweak

ICT Largest Midnight–00:30 FVG (NY, 1 per day) — FIXEDmarks out the first and largest fvg on the 1 min chart from midnight open until 12:30 am est

ATR Future Movement Range Projection

The "ATR Future Movement Range Projection" is a custom TradingView Pine Script indicator designed to forecast potential price ranges for a stock (or any asset) over short-term (1-month) and medium-term (3-month) horizons. It leverages the Average True Range (ATR) as a measure of volatility to estimate how far the price might move, while incorporating recent momentum bias based on the proportion of bullish (green) vs. bearish (red) candles. This creates asymmetric projections: in bullish periods, the upside range is larger than the downside, and vice versa.

The indicator is overlaid on the chart, plotting horizontal lines for the projected high and low prices for both timeframes. Additionally, it displays a small table in the top-right corner summarizing the projected prices and the percentage change required from the current close to reach them. This makes it useful for traders assessing potential targets, risk-reward ratios, or option strategies, as it combines volatility forecasting with directional sentiment.

Key features:

- **Volatility Basis**: Uses weekly ATR to derive a stable daily volatility estimate, avoiding noise from shorter timeframes.

- **Momentum Adjustment**: Analyzes recent candle colors to tilt projections toward the prevailing trend (e.g., more upside if more green candles).

- **Time Horizons**: Fixed at 1 month (21 trading days) and 3 months (63 trading days), assuming ~21 trading days per month (excluding weekends/holidays).

- **User Adjustable**: The ATR length/lookback (default 50) can be tweaked via inputs.

- **Visuals**: Green/lime lines for highs, red/orange for lows; a semi-transparent table for quick reference.

- **Limitations**: This is a probabilistic projection based on historical volatility and momentum—it doesn't predict direction with certainty and assumes volatility persists. It ignores external factors like news, earnings, or market regimes. Best used on daily charts for stocks/ETFs.

The indicator doesn't generate buy/sell signals but helps visualize "expected" ranges, similar to how implied volatility informs option pricing.

### How It Works Step-by-Step

The script executes on each bar update (typically daily timeframe) and follows this logic:

1. **Input Configuration**:

- ATR Length (Lookback): Default 50 bars. This controls both the ATR calculation period and the candle count window. You can adjust it in the indicator settings.

2. **Calculate Weekly ATR**:

- Fetches the ATR from the weekly timeframe using `request.security` with a length of 50 weeks.

- ATR measures average price range (high-low, adjusted for gaps), representing volatility.

3. **Derive Daily ATR**:

- Divides the weekly ATR by 5 (approximating 5 trading days per week) to get an equivalent daily volatility estimate.

- Example: If weekly ATR is $5, daily ATR ≈ $1.

4. **Define Projection Periods**:

- 1 Month: 21 trading days.

- 3 Months: 63 trading days (21 × 3).

- These are hardcoded but based on standard trading calendar assumptions.

5. **Compute Base Projections**:

- Base projection = Daily ATR × Days in period.

- This gives the total expected movement (range) without direction: e.g., for 3 months, $1 daily ATR × 63 = $63 total range.

6. **Analyze Candle Momentum (Win Rate)**:

- Counts green candles (close > open) and red candles (close < open) over the last 50 bars (ignores dojis where close == open).

- Total colored candles = green + red.

- Win rate = green / total colored (as a fraction, e.g., 0.7 for 70%). Defaults to 0.5 if no colored candles.

- This acts as a simple momentum proxy: higher win rate implies bullish bias.

7. **Adjust Projections Asymmetrically**:

- Upside projection = Base projection × Win rate.

- Downside projection = Base projection × (1 - Win rate).

- This skews the range: e.g., 70% win rate means 70% of the total range allocated to upside, 30% to downside.

8. **Calculate Projected Prices**:

- High = Current close + Upside projection.

- Low = Current close - Downside projection.

- Done separately for 1M and 3M.

9. **Plot Lines**:

- 3M High: Solid green line.

- 3M Low: Solid red line.

- 1M High: Dashed lime line.

- 1M Low: Dashed orange line.

- Lines extend horizontally from the current bar onward.

10. **Display Table**:

- A 3-column table (Projection, Price, % Change) in the top-right.

- Rows for 1M High/Low and 3M High/Low, color-coded.

- % Change = ((Projected price - Close) / Close) × 100.

- Updates dynamically with new data.

The entire process repeats on each new bar, so projections evolve as volatility and momentum change.

### Examples

Here are two hypothetical examples using the indicator on a daily chart. Assume it's applied to a stock like AAPL, but with made-up data for illustration. (In TradingView, you'd add the script to see real outputs.)

#### Example 1: Bullish Scenario (High Win Rate)

- Current Close: $150.

- Weekly ATR (50 periods): $10 → Daily ATR: $10 / 5 = $2.

- Last 50 Candles: 35 green, 15 red → Total colored: 50 → Win Rate: 35/50 = 0.7 (70%).

- Base Projections:

- 1M: $2 × 21 = $42.

- 3M: $2 × 63 = $126.

- Adjusted Projections:

- 1M Upside: $42 × 0.7 = $29.4 → High: $150 + $29.4 = $179.4 (+19.6%).

- 1M Downside: $42 × 0.3 = $12.6 → Low: $150 - $12.6 = $137.4 (-8.4%).

- 3M Upside: $126 × 0.7 = $88.2 → High: $150 + $88.2 = $238.2 (+58.8%).

- 3M Downside: $126 × 0.3 = $37.8 → Low: $150 - $37.8 = $112.2 (-25.2%).

- On the Chart: Green/lime lines skewed higher; table shows bullish % changes (e.g., +58.8% for 3M high).

- Interpretation: Suggests stronger potential upside due to recent bullish momentum; useful for call options or long positions.

#### Example 2: Bearish Scenario (Low Win Rate)

- Current Close: $50.

- Weekly ATR (50 periods): $3 → Daily ATR: $3 / 5 = $0.6.

- Last 50 Candles: 20 green, 30 red → Total colored: 50 → Win Rate: 20/50 = 0.4 (40%).

- Base Projections:

- 1M: $0.6 × 21 = $12.6.

- 3M: $0.6 × 63 = $37.8.

- Adjusted Projections:

- 1M Upside: $12.6 × 0.4 = $5.04 → High: $50 + $5.04 = $55.04 (+10.1%).

- 1M Downside: $12.6 × 0.6 = $7.56 → Low: $50 - $7.56 = $42.44 (-15.1%).

- 3M Upside: $37.8 × 0.4 = $15.12 → High: $50 + $15.12 = $65.12 (+30.2%).

- 3M Downside: $37.8 × 0.6 = $22.68 → Low: $50 - $22.68 = $27.32 (-45.4%).

- On the Chart: Red/orange lines skewed lower; table highlights larger downside % (e.g., -45.4% for 3M low).

- Interpretation: Indicates bearish risk; might prompt protective puts or short strategies.

#### Example 3: Neutral Scenario (Balanced Win Rate)

- Current Close: $100.

- Weekly ATR: $5 → Daily ATR: $1.

- Last 50 Candles: 25 green, 25 red → Win Rate: 0.5 (50%).

- Projections become symmetric:

- 1M: Base $21 → Upside/Downside $10.5 each → High $110.5 (+10.5%), Low $89.5 (-10.5%).

- 3M: Base $63 → Upside/Downside $31.5 each → High $131.5 (+31.5%), Low $68.5 (-31.5%).

- Interpretation: Pure volatility-based range, no directional bias—ideal for straddle options or range trading.

In real use, test on historical data: e.g., if past projections captured actual moves ~68% of the time (1 standard deviation for ATR), it validates the volatility assumption. Adjust the lookback for different assets (shorter for volatile cryptos, longer for stable blue-chips).

nATR*ATR Multiplication Indicator - Optimal Selection Tool forThis indicator is specifically designed as an analysis tool for investors using grid bot strategies. It displays both nATR (Normalized Average True Range) and ATR (Average True Range) values on a single chart screen, calculating the multiplication of these two critical volatility measurements.

Primary Purpose of the Indicator:

To facilitate the selection of the most optimal stock and time period for grid bot trading. The nATR*ATR multiplication provides a hybrid measurement that combines both percentage-based return potential (nATR) and absolute volatility magnitude (ATR).

Importance for Grid Bot Strategy:

High nATR: Greater percentage-based return potential

High ATR: Wider price range = Fewer grid levels = More budget allocation per grid

Formula: Price Range/ATR = Theoretical Grid Count

Usage Advantages:

Test different time periods to find the highest multiplication value

Make optimal stock and time frame selections for grid bot setup

Monitor both nATR and ATR values on a single screen

High multiplication values indicate ideal conditions for grid bots

Technical Features:

Adjustable calculation period (1-500 candles)

Visual alert system (high/low multiplication values)

Real-time value tracking table

SMA-based smoothed calculations

This serves as a reliable guide for grid bot investors in optimal timing and stock selection.

Chanpreet RSI(3) Extreme Rays (4H, Adjustable Style)Chanpreet RSI(3) Extreme Rays (4H)

This indicator applies a short-length RSI (3) on the 4-hour timeframe and highlights momentum extremes directly on the chart.

🔎 What it does

Detects when RSI(3) moves into overbought (>80) or oversold (<20) territory.

Groups consecutive candles inside these zones into one “event” instead of marking each bar individually.

For each event:

• In overbought → records the highest high of the stretch and marks it with a horizontal ray.

• In oversold → records the lowest low of the stretch and marks it with a horizontal ray.

Keeps only the most recent N rays (default 5, adjustable).

⚙️ Inputs

Max Rays to Keep → how many unique events are kept visible.

Ray Thickness → adjust line thickness.

Overbought Ray Color → default red.

Oversold Ray Color → default green.

📈 How to use

Apply on any chart; RSI(3) values are always calculated from 4H data (via request.security).

Use rays as reference levels that highlight recent momentum extremes or exhaustion zones.

This is not a buy/sell signal by itself — combine with your own analysis, confirmation tools, and risk management.

Best Recommended time frame is 5 mins, 10 mins & 15 mins for intraday trading.

🧩 Unique features

Groups multiple bars into a single clean ray, reducing clutter.

Uses 4H RSI(3) regardless of the chart’s active timeframe.

Fully customizable appearance (colors, thickness, max events).

⚠️ Disclaimer

This script is provided for educational and informational purposes only.

It does not constitute financial advice or guarantee performance.

Always test thoroughly and use proper risk management before trading live.