A13: Micro MAP Scalping StrategyA13: Micro MAP Scalping Strategy — Institutional Breakout Scalper (Pine Script v6 – Protected Source)

A completely original, professional scalping strategy developed from scratch over several months of research and live-market testing. The system is built around institutional breakout zones with a unique multi-stage validation process, strict confirmation requirements, and sophisticated risk management — all designed specifically for 1–15 minute timeframes.

Why this implementation is original and the source code is protected

The entire logic — from breakout detection to entry confirmation, multi-filter stop-loss engines, and dynamic position sizing — was built independently without relying on any existing public libraries, built-ins, or open-source code beyond standard Pine functions. The proprietary validation rules, ATR-scaled gap filtering, and layered confirmation system required extensive original development to achieve consistent performance in real-market conditions. Protecting the source code is necessary to preserve the unique edge that distinguishes this system from standard or publicly available implementations.

Core concepts and methodology (fully transparent — no code revealed)

1. Institutional Breakout Zone Detection

• Real-time identification of high-probability zones using a custom ATR-based minimum gap filter

• Zones are only considered valid when accompanied by clear price displacement and volume confirmation

• No reliance on standard Fair Value Gap or order block libraries — completely custom validation

2. Strict Dual Confirmation Entry Logic

• Entry requires one of two precise conditions:

— Confirmed pullback retest of the validated breakout zone, or

— Clean inside-bar formation fully contained within the zone

• Both conditions must align with the directional bias of the breakout

3. Five Independent Stop-Loss Engines

• ATR-based (default and recommended)

• Swing Low/High levels

• Pivot Point structure

• Trailing Stop with ATR offset

• Fixed percentage

• Every engine includes minimum and maximum stop-loss filters to prevent unrealistic risk during extreme volatility

4. Professional Risk & Position Sizing Engine

• Fixed percentage risk per trade (default 1%)

• Optional compounding mode for growing accounts

• Real-time calculation based on exact stop distance and current equity

• Full integration with leverage settings

5. Multi-Layer Filtering System

• Multi-timeframe EMA filter (default 60-period, fully customizable timeframe)

• Complete trading session control with UTC offset support

• Date range filtering for strategy deployment control

• Consecutive loss protection (optional multi-stop filter)

• Minimum/maximum stop-loss filters to eliminate low-probability setups

6. Real-Time Performance Dashboard

• Live display of win rate, net profit, maximum drawdown, total trades

• Consecutive win/loss streak tracking

• Current position size and average entry price

• All statistics visible directly on chart

Backtesting settings used in the published chart

• Symbol: BTC/USD

• Timeframe: 15-minute

• Initial capital: $10,000

• Risk per trade: 1%

• Commission: 0.04% (realistic for major brokers)

• Slippage: enabled

• Sample size: 200+ trades

These are the exact default Properties settings of the strategy.

The strategy is completely free to add and use on your charts.

#Scalping #Breakout #Intraday #Institutional #RiskManagement #ProfessionalStrategy

Indicateurs et stratégies

MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)

JYL Trend Pro V1.0 BETAJYL Trend Pro V1.0 is a rule‑based trend‑following strategy built on a proprietary smoothed price engine.

It focuses on clear trend states and position management rather than classic indicators, and can be used on both long and short side depending on the user’s settings.

Three Signal Modes

1. Stable Mode

Stable mode is the “classic” version of the system.

It reacts only when the trend state clearly flips, and then manages the position with simple rules:

First strong bullish state → open / add to long

First strong bearish state → open / add to short

When the trend weakens but does not fully reverse, the strategy can reduce position size (partial exit)

When the trend flips in the opposite direction, the strategy fully exits the existing position

This mode is designed for traders who prefer fewer signals and smoother equity curves.

2. Impulsive Mode

Impulsive mode keeps the same core logic, but allows the strategy to react earlier and manage exits more actively:

Opportunistic early entries around strong moves

Protective “early stop” logic for those aggressive entries

Segment‑based partial exits after extended bullish or bearish runs

Fast full exits when momentum fades quickly or the trend flips

This mode is aimed at users who accept more trade frequency in exchange for faster reactions.

3. IMP+ Mode (Impulsive Plus)

IMP+ is the advanced version of Impulsive mode. It keeps all core behavior and adds extra controls for power‑users:

Adjustable presets for how early the system can enter a move

Adjustable presets for how quickly early entries are cut if they fail

Smarter add‑ons after a bullish / bearish segment, so adds can occur either at the next strong signal or on a “pullback‑type” bar inside the ongoing trend

Flexible multi‑level partial‑exit packages after a strong run

Additional “emergency exit” logic that can flatten positions when price opens too close to the previous bar after a strong trend segment

All of these options are exposed as presets in the Inputs tab, so users can experiment without touching code.

Signals & Usage

The strategy prints clear labels on the chart:

LONG / SHORT – open or add to position

REDUCE SIZE – partial profit‑taking or risk reduction

SELL LONG / SHORT COVER – full exit of long / short positions

A trade‑direction filter lets you run the system as long‑only, short‑only, or long & short.

This script is provided for educational and research purposes only.

It is not financial advice and does not guarantee any future performance. Always test on a demo account, adjust risk to your own situation, and consult your broker or advisor before trading live.

Internally, this strategy is based on the private JYL Trend Pro rule set and risk‑management framework.

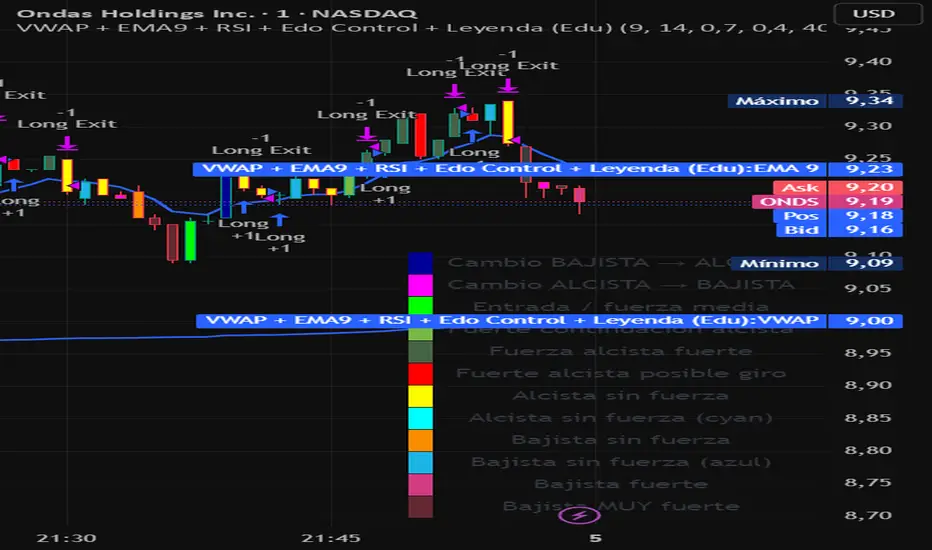

VWAP + EMA9 + RSI + Edo Control (Edu)VWAP + EMA9 + RSI + Edo Control (Edu)

A complete intraday scalping system that combines institutional levels, fast trend signaling and enhanced candle-color analysis for maximum clarity and confirmation.

This indicator includes:

1. VWAP (Volume Weighted Average Price)

The institutional reference line used to determine value zones, liquidity bias and directional pressure.

2. EMA9 (Fast Exponential Moving Average)

A micro-trend guide that reacts quickly to short-term movements and improves timing on pullback entries.

3. RSI (Relative Strength Index)

A clean momentum filter using the classic >50 (bullish) and <50 (bearish) bias.

Edo Control – Advanced Colored Candle System

This version integrates Edo Control, a custom candle-color engine that visualizes market strength shifts based on Williams %R, directional movement and ADX behavior.

Each candle color represents a different market condition, such as:

Trend acceleration

Trend weakening

Possible reversals

Momentum spikes

Bullish or bearish pressure

Transition zones

A built-in movable legend explains the meaning of each color directly on the chart, so traders can identify conditions instantly without guessing.

Why this indicator works

The combination of VWAP + EMA9 + RSI + colored candle strength creates a multi-layer confirmation system that cuts noise and highlights only meaningful setups.

Designed for 1m, 3m, 5m charts, but also effective on higher timeframes.

Suitable for: stocks, indices, futures, forex, crypto.

NYAM Trend PullbackThis is an trend-following strategy designed for trades taken during New York Morning. It aims to capture trend continuations by entering positions when price aligns with the dominant trend relative to a Exponential Moving Average (EMA).

If price is above the EMA then it is bullish and enters long, and if its below the EMA it is bearish and enters a short.

JYL Trend Pro V1.0 BETANASDAQ:TSLA

JYL Trend Pro V1.0 is a rule‑based trend‑following strategy built on a proprietary smoothed price engine.

It focuses on clear trend states and position management rather than classic indicators, and can be used on both long and short side depending on the user’s settings.

Three Signal Modes

1. Stable Mode

Stable mode is the “classic” version of the system.

It reacts only when the trend state clearly flips, and then manages the position with simple rules:

First strong bullish state → open / add to long

First strong bearish state → open / add to short

When the trend weakens but does not fully reverse, the strategy can reduce position size (partial exit)

When the trend flips in the opposite direction, the strategy fully exits the existing position

This mode is designed for traders who prefer fewer signals and smoother equity curves.

2. Impulsive Mode

Impulsive mode keeps the same core logic, but allows the strategy to react earlier and manage exits more actively:

Opportunistic early entries around strong moves

Protective “early stop” logic for those aggressive entries

Segment‑based partial exits after extended bullish or bearish runs

Fast full exits when momentum fades quickly or the trend flips

This mode is aimed at users who accept more trade frequency in exchange for faster reactions.

3. IMP+ Mode (Impulsive Plus)

IMP+ is the advanced version of Impulsive mode. It keeps all core behavior and adds extra controls for power‑users:

Adjustable presets for how early the system can enter a move

Adjustable presets for how quickly early entries are cut if they fail

Smarter add‑ons after a bullish / bearish segment, so adds can occur either at the next strong signal or on a “pullback‑type” bar inside the ongoing trend

Flexible multi‑level partial‑exit packages after a strong run

Additional “emergency exit” logic that can flatten positions when price opens too close to the previous bar after a strong trend segment

All of these options are exposed as presets in the Inputs tab, so users can experiment without touching code.

Signals & Usage

The strategy prints clear labels on the chart:

LONG / SHORT – open or add to position

REDUCE SIZE – partial profit‑taking or risk reduction

SELL LONG / SHORT COVER – full exit of long / short positions

A trade‑direction filter lets you run the system as long‑only, short‑only, or long & short.

This script is provided for educational and research purposes only.

It is not financial advice and does not guarantee any future performance. Always test on a demo account, adjust risk to your own situation, and consult your broker or advisor before trading live.

Internally, this strategy is based on the private JYL Trend Pro rule set and risk‑management framework.

BTC Fear & Greed Incremental StrategyIMPORTANT: READ SETUP GUIDE BELOW OR IT WON'T WORK

# BTC Fear & Greed Incremental Strategy — TradeMaster AI (Pure BTC Stack)

## Strategy Overview

This advanced Bitcoin accumulation strategy is designed for long-term hodlers who want to systematically take profits during greed cycles and accumulate during fear periods, while preserving their core BTC position. Unlike traditional strategies that start with cash, this approach begins with a specified BTC allocation, making it perfect for existing Bitcoin holders who want to optimize their stack management.

## Key Features

### 🎯 **Pure BTC Stack Mode**

- Start with any amount of BTC (configurable)

- Strategy manages your existing stack, not new purchases

- Perfect for hodlers who want to optimize without timing markets

### 📊 **Fear & Greed Integration**

- Uses market sentiment data to drive buy/sell decisions

- Configurable thresholds for greed (selling) and fear (buying) triggers

- Automatic validation to ensure proper 0-100 scale data source

### 🐂 **Bull Year Optimization**

- Smart quarterly selling during bull market years (2017, 2021, 2025)

- Q1: 1% sells, Q2: 2% sells, Q3/Q4: 5% sells (configurable)

- **NO SELLING** during non-bull years - pure accumulation mode

- Preserves BTC during early bull phases, maximizes profits at peaks

### 🐻 **Bear Market Intelligence**

- Multi-regime detection: Bull, Early Bear, Deep Bear, Early Bull

- Different buying strategies based on market conditions

- Enhanced buying during deep bear markets with configurable multipliers

- Visual regime backgrounds for easy market condition identification

### 🛡️ **Risk Management**

- Minimum BTC allocation floor (prevents selling entire stack)

- Configurable position sizing for all trades

- Multiple safety checks and validation

### 📈 **Advanced Visualization**

- Clean 0-100 scale with 2 decimal precision

- Three main indicators: BTC Allocation %, Fear & Greed Index, BTC Holdings

- Real-time portfolio tracking with cash position display

- Enhanced info table showing all key metrics

## How to Use

### **Step 1: Setup**

1. Add the strategy to your BTC/USD chart (daily timeframe recommended)

2. **CRITICAL**: In settings, change the "Fear & Greed Source" from "close" to a proper 0-100 Fear & Greed indicator

---------------

I recommend Crypto Fear & Greed Index by TIA_Technology indicator

When selecting source with this indicator, look for "Crypto Fear and Greed Index:Index"

---------------

3. Set your "Starting BTC Quantity" to match your actual holdings

4. Configure your preferred "Start Date" (when you want the strategy to begin)

### **Step 2: Configure Bull Year Logic**

- Enable "Bull Year Logic" (default: enabled)

- Adjust quarterly sell percentages:

- Q1 (Jan-Mar): 1% (conservative early bull)

- Q2 (Apr-Jun): 2% (moderate mid bull)

- Q3/Q4 (Jul-Dec): 5% (aggressive peak targeting)

- Add future bull years to the list as needed

### **Step 3: Fine-tune Thresholds**

- **Greed Threshold**: 80 (sell when F&G > 80)

- **Fear Threshold**: 20 (buy when F&G < 20 in bull markets)

- **Deep Bear Fear Threshold**: 25 (enhanced buying in bear markets)

- Adjust based on your risk tolerance

### **Step 4: Risk Management**

- Set "Minimum BTC Allocation %" (default 20%) - prevents selling entire stack

- Configure sell/buy percentages based on your position size

- Enable bear market filters for enhanced timing

### **Step 5: Monitor Performance**

- **Orange Line**: Your BTC allocation percentage (target: fluctuate between 20-100%)

- **Blue Line**: Actual BTC holdings (should preserve core position)

- **Pink Line**: Fear & Greed Index (drives all decisions)

- **Table**: Real-time portfolio metrics including cash position

## Reading the Indicators

### **BTC Allocation Percentage (Orange Line)**

- **100%**: All portfolio in BTC, no cash available for buying

- **80%**: 80% BTC, 20% cash ready for fear buying

- **20%**: Minimum allocation, maximum cash position

### **Trading Signals**

- **Green Buy Signals**: Appear during fear periods with available cash

- **Red Sell Signals**: Appear during greed periods in bull years only

- **No Signals**: Either allocation limits reached or non-bull year

## Strategy Logic

### **Bull Years (2017, 2021, 2025)**

- Q1: Conservative 1% sells (preserve stack for later)

- Q2: Moderate 2% sells (gradual profit taking)

- Q3/Q4: Aggressive 5% sells (peak targeting)

- Fear buying active (accumulate on dips)

### **Non-Bull Years**

- **Zero selling** - pure accumulation mode

- Enhanced fear buying during bear markets

- Focus on rebuilding stack for next bull cycle

## Important Notes

- **This is not financial advice** - backtest thoroughly before use

- Designed for **long-term holders** (4+ year cycles)

- **Requires proper Fear & Greed data source** - validate in settings

- Best used on **daily timeframe** for major trend following

- **Cash calculations**: Use allocation % and BTC holdings to calculate available cash: `Cash = (Total Portfolio × (1 - Allocation%/100))`

## Risk Disclaimer

This strategy involves active trading and position management. Past performance does not guarantee future results. Always do your own research and never invest more than you can afford to lose. The strategy is designed for educational purposes and long-term Bitcoin accumulation thesis.

---

*Developed by Sol_Crypto for the Bitcoin community. Happy stacking! 🚀*

PSAR with EMA FilterThis indicator combines the Parabolic SAR (PSAR) with an EMA trend filter to generate more accurate trend-following signals.

PSAR helps identify potential trend reversals and trailing stop levels, while the EMA ensures that trades are aligned with the overall market direction.

MACD with EMA FilterThis indicator combines the MACD (Moving Average Convergence Divergence) with an EMA-based trend filter to improve the quality of entry signals.

MACD identifies changes in momentum and potential trend reversals, while the EMA ensures that signals are taken only in the direction of the broader trend.

RSI with EMA FilterThis indicator combines the Relative Strength Index (RSI) with a trend-filtering Exponential Moving Average (EMA) to generate higher-quality momentum signals.

RSI identifies overbought and oversold market conditions, while the EMA confirms the overall trend direction, helping traders avoid false signals in choppy markets.

Supertrend + MAXTRA inputsThe Supertrend strategy is a trend-following trading method that uses the Supertrend indicator, which is calculated based on the ATR (Average True Range). When the price closes above the Supertrend line, it generates a buy signal, and when the price closes below the Supertrend line, it generates a sell signal. The indicator continuously trails the price, helping traders identify trend direction, ride trends, and manage stop-loss levels.

EMA + Sessions + RSI Strategy v1.0A professional trading strategy that combines multiple technical indicators for high-probability entries. This system uses EMA crossovers, RSI zone filtering, and trend confirmation to identify optimal trading opportunities while managing risk with advanced position management tools.

Key Features:

✅ Dual Entry Signals (EMA21 + EMA100 crossover conditions)

✅ Trend Filter EMA750 (trade only with the major trend)

✅ Complete Risk Management (SL 1%, TP 3% default)

✅ Trailing Stop & Breakeven (maximize profits, protect capital)

✅ Compact Statistics Table (real-time performance metrics)

✅ RSI & Session Filters (avoid low-probability setups)

✅ Optional Pyramiding (scale into winning positions)

Perfect for swing trading and trend-following on any timeframe. Fully customizable to match your trading style.

Supertrend Cloud ProSupertrend Cloud Pro is a next-generation trend + breakout system designed for traders who want clean structure, early breakout confirmation, and disciplined exits.

The strategy combines Fast + Slow Supertrend layers, a dynamic cloud compression model , and a breakout-based entry engine to deliver clarity in trending as well as contracting markets.

How It Works

1. Dual Supertrend Structure (Fast + Slow)

Fast ST reacts quickly to volatility

Slow ST establishes dominant trend bias

Combined color logic instantly reveals market direction

Green Cloud → Bullish Trend

Red Cloud → Bearish Trend

Yellow Cloud → Compression / Squeeze Zone

2. Cloud Compression Logic

The zone between Fast/Slow Supertrend creates a structure-based “cloud.”

When price enters this zone, markets are typically preparing for expansion.

Yellow shading highlights these high-probability breakout zones.

3. Breakout Entry Engine

Long Entry : Price closes above the cloud top

Short Entry: Price closes below the cloud bottom

This avoids premature entries and filters out false noise.

4. Smart Exit Logic

Positions exit automatically when Fast or Slow Supertrend flips direction, ensuring disciplined exit and minimizing emotional decisions.

BTC Trend-Following Strategy (Limited Version)This is a trend-following strategy designed specifically for Bitcoin (BTC).

It has demonstrated consistent performance and profitable opportunities over multiple years of historical data.

The strategy aims to capture major trends while managing risk effectively, making it suitable for traders looking for a systematic BTC trading approach.

EMA AAyushA basis trend filter of ema 200 and ema 50 and taking entry with crossover and ATR as SL and Target.

Pro Bollinger Bands Strategy [Breno]This strategy excels in highly volatile financial instruments, including cryptocurrencies, high-beta stocks, commodity futures, and certain exchange-traded funds (ETFs) that exhibit clear mean-reversion characteristics around their Bollinger Bands. The system's ability to utilize scaling (position averaging) and an ATR-based stop loss makes it particularly effective in markets with significant price swings, allowing the trader to capture profits from price extremes while managing increased volatility-related risk.

Core Strategy Logic

This Strategy implements a comprehensive trend-following and mean-reversion strategy primarily leveraging the Bollinger Bands (BB) indicator for entry and exit signals, complemented by an Average True Range (ATR)-based Stop Loss mechanism and an optional EMA filter. It is designed with robust features for capital management, including configurable leverage and a sophisticated position averaging (scaling) system.

Long Entry: A long position is initiated when the closing price crosses over the Lower Bollinger Band (ta.crossover(close,lowerBB)). This signals a potential mean-reversion opportunity following a price dip.

Short Entry: A short position is initiated when the closing price crosses under the Upper Bollinger Band (ta.crossunder(close,upperBB)). (Note: Short entries are disabled by default in the script inputs).

Exit Conditions (Profit Target): Long positions aim to exit upon interaction with the Upper Bollinger Band. Users can select from three exit methods:

"Close When Touch": Exits when close≥upperBB.

"Close Above then Below": Exits when the previous close was above the upper band, and the current close is below it (a reversal signal).

"High Above": Exits when high>upperBB. The strategy features an optional profitOnly setting, which restricts all exits to only occur if the trade is currently in profit (i.e., close is above the strategy.position_avg_price for longs).

Key Features and Customization

Bollinger Bands & Filters -

Customizable BB Parameters: The Length and Deviation of the Bollinger Bands are fully adjustable, allowing users to fine-tune the sensitivity of the entry and exit signals.

Optional EMA Filter: An optional EMA Filter can be enabled to align entries with the prevailing trend, where a Long entry is only permitted if close≥EMA(EmaFilterRange).

Risk and Capital Management -

Equity Allocation: Position size is dynamically calculated based on a Percentage of Equity (capitalPerc) combined with the set Leverage multiplier.

Dynamic Stop Loss (ATR-Based):

An optional Stop Loss (SL) is calculated using a multiple (slAtrInput) of the Average True Range (ATR).

The SL is set relative to the entry price upon trade activation, providing a volatility-adjusted risk management layer.

Position Averaging (Scaling): The script supports the addition of multiple units (pyramiding) to an existing position based on three user-selected criteria:

"No": No averaging.

"Percent": Adds to the position if the price has dropped by a set percentage (addPct) from the average price.

"ATR": Adds to the position if the current price is significantly below a calculated ATR-based support level from the average price.

XRP Non-Stop Strategy (TP 25% / SL 15%)XRP Non-Stop Strategy (TP 25% / SL 15%) is a continuous long-side trading system designed specifically for XRP. The strategy uses an EMA-based trend filter (EMA20/EMA50) to confirm bullish conditions before entering a long position. Each trade applies a fixed +25% Take Profit target and a −15% Stop Loss, calculated dynamically from the entry price.

When a trade closes—whether by TP or SL—the strategy automatically re-enters on the next qualifying signal, enabling uninterrupted position cycling.

Features include:

• EMA-based trend confirmation

• Dynamic TP/SL visualization on the chart

• Clear BUY and EXIT markers

• Dedicated alert conditions for automation

XRP Non-Stop Strategy (TP 25% / SL 15%)This strategy performs continuous automated trading exclusively on XRP. It opens long positions during favorable trend conditions, using a fixed Take Profit target of 25% above the entry price and a fixed Stop Loss of 15% below the entry. Once a trade is closed (either TP or SL), the strategy automatically re-enters on the next valid signal, enabling uninterrupted trading.

The script includes:

Dynamic Take Profit & Stop Loss lines

Optional EMA trend filter

Visual BUY and EXIT markers

TradingView alerts for automation or notifications

This strategy is built for traders who want a simple, price-action-driven system without fixed price levels, relying only on percentage-based movement from each entry.

BTC Mon 8am Buy / Wed 2pm Sell (NY Time, Daily + Intraday)This strategy implements a fixed weekly time-based trading schedule for Bitcoin, using New York market hours as the reference clock. It is designed to test whether a consistent pattern exists between early-week accumulation and mid-week distribution in BTC price behavior.

Entry Rule — Monday 8:00 AM (NY Time)

The strategy enters a long position every Monday at exactly 08:00 AM Eastern Time, one hour after the U.S. equities market pre-open activity begins influencing global liquidity.

This timing attempts to capture early-week directional moves in Bitcoin, which sometimes occur as traditional markets come online.

Exit Rule — Wednesday 2:00 PM (NY Time)

The strategy closes the position every Wednesday at 2:00 PM Eastern Time, a point in the week where:

U.S. equity markets are still open

BTC often experiences mid-week volatility rotations

Liquidity is generally high

This exit removes exposure before later-week uncertainty and gives a consistent, measurable time window for each trade.

Timeframe Compatibility

Works on intraday charts (recommended 1h or lower) using precise time-based triggers.

Also runs on daily charts, where entries and exits occur on the Monday and Wednesday bars respectively (daily charts cannot show intraday timestamps).

All timestamps are synced to America/New_York regardless of the exchange’s native timezone.

Trading Frequency

Exactly one trade per week, preventing overtrading and allowing comparison of weekly performance across years of historical BTC price data.

Purpose of the Strategy

This is not a value-based or trend-following system, but a behavioral/time-cycle analysis tool.

It helps evaluate whether a repeating short-term edge exists based solely on:

Weekday timing

Liquidity cycles

Institutional market influence

BTC’s habitual early-week momentum patterns

It is ideal for:

Backtesting weekly BTC behavior

Studying time-based edges

Comparing alternative weekday/time combinations

Visualizing weekly P&L structure

Risk Notes

This strategy does not attempt to predict price direction and should not be assumed profitable without robust backtesting.

Time-based edges can appear, disappear, or invert depending on macro conditions.

There is no stop loss or risk management included by default, so the strategy reflects raw timing-based performance.

Long Only EMA Strategy (9/20 with 200 EMA Filter)Details:

This strategy is built around a very simple idea: follow the primary trend and enter only when momentum supports it.

It uses three EMAs on a standard candlestick chart:

1. 9‑period EMA – short‑term momentum

2. 20‑period EMA – medium‑term structure

3. 200‑period EMA – long‑term trend filter

The strategy is ** long‑only ** and is mainly designed for swing trading and positional trading.

It avoids counter‑trend trades by taking entries only when price is trading ** above the 200 EMA **, which is commonly used as a long‑term trend reference.

The rules are deliberately kept simple so that they are easy to understand, modify, and test on different markets and timeframes.

---

Key Features

1. **Trend‑Filtered Entries**

- Fresh long positions are considered only when:

- The 9 EMA crosses above the 20 EMA

- The closing price is **above** the 200 EMA

- This attempts to combine short‑term momentum with a higher‑timeframe trend filter.

2. **Clean Exit Logic**

- The long position is exited when the closing price crosses **below** the 20 EMA.

- This creates an objective, rule‑based way to trail the trade as long as the medium‑term structure remains intact.

3. **Long‑Only, No Short Selling**

- The script intentionally ignores short setups.

- This makes it suitable for markets or accounts where short selling is restricted, or for traders who prefer to participate only on the long side of the market.

4. **Simple Visuals**

- All three EMAs are plotted directly on the chart:

- 9 EMA (fast)

- 20 EMA (medium)

- 200 EMA (trend)

- Trade entries and exits are handled by TradingView’s strategy engine, so users can see results in the Strategy Tester as well as directly on the chart.

5. **Backtest‑Friendly Structure**

- Uses TradingView’s built‑in `strategy()` framework.

- Can be applied to different symbols, timeframes, and markets (equities, indices, crypto, etc.).

- Works on standard candlestick charts, which are supported by TradingView’s backtesting engine.

6. **Configurable in Code**

- The EMA periods are defined in the code and can be easily adjusted.

- Users can tailor the parameters to fit their own style (for example, faster EMAs for intraday trading, slower EMAs for positional trades).

---

How to Use

1. **Add the Strategy to Your Chart**

1. Open any symbol and select a **standard candlestick chart**.

2. Apply the strategy from your “My Scripts” section.

3. Make sure it is enabled so that the trades and results appear.

2. **Select Timeframe**

- The logic can be tested on various timeframes:

- Higher timeframes (1H, 4H, 1D) for swing and positional setups.

- Lower timeframes (5m, 15m) for more active trading, if desired.

- Users should experiment and see where the strategy behaves more consistently for their chosen market.

3. **Read the Signals**

- **Entry:**

- A long trade is opened when the 9 EMA crosses above the 20 EMA while the closing price is above the 200 EMA.

- **Exit:**

- The open long position is closed when the closing price crosses below the 20 EMA.

- All orders are generated automatically once the strategy is attached to the chart.

4. **Use the Strategy Tester**

- Go to the **Strategy Tester** tab in TradingView.

- Check:

- Net profit / drawdown

- Win rate and average trade

- List of trades and the equity curve

- Change the date range and timeframe to see how stable the results are over different periods.

5. **Adjust Parameters if Needed**

- Advanced users can open the code and experiment with:

- EMA lengths (for example 8/21 with 200, or 10/30 with 200)

- Risk sizing and capital settings within the `strategy()` call

- Any changes should be thoroughly re‑tested before considering real‑world application.

---

Practical Applications

1. **Swing Trading on Daily Charts**

- Can be applied to stocks, indices, or ETFs on the daily timeframe.

- The 200 EMA acts as a trend filter to stay aligned with the broad direction, while the 9/20 crossover helps catch medium‑term swings inside that trend.

2. **Positional Trades on Higher Timeframes**

- On 4H or 1D charts, this approach can help in holding trades for several days to weeks.

- The exit rule based on the 20 EMA crossing helps avoid emotional decisions and provides a rules‑based way to trail the trend.

3. **Trend‑Following Filter**

- Even if used purely as a filter, the 200 EMA condition can help traders:

- Avoid taking long trades when the market is in a clear downtrend.

- Focus only on instruments that are trading above their long‑term average.

4. **Educational Use**

- The script is intentionally kept straightforward so that newer users can:

- Learn how a moving average crossover strategy works.

- See how to combine a short‑term signal with a long‑term filter.

- Understand how TradingView’s strategy engine handles entries and exits.

5. **Basis for Further Development**

- This can serve as a starting point for more advanced systems.

- Traders can extend it by adding:

- Additional filters (RSI, volume, volatility filters, time‑of‑day filters, etc.)

- Risk management rules (fixed stop loss, take profit, trailing stops).

- The current version is kept minimal on purpose, so modifications are easy to implement and test.

---

Important Notes & Disclaimer

1. This strategy is provided **for testing, research, and educational purposes only**.

2. It is ** not ** a recommendation to buy or sell any financial instrument.

3. Past performance on historical data does not guarantee similar results in live markets.

4. Markets are risky and trading can lead to financial loss; users should always do their own research, manage risk appropriately, and consult a qualified financial professional if needed.

5. Before using any strategy with real capital, it is strongly advised to:

- Forward test it on a demo / paper trading account.

- Check how it behaves during different market phases (trending, sideways, high‑volatility conditions).

You are free to modify the parameters and logic to better align it with your own trading style and risk tolerance.

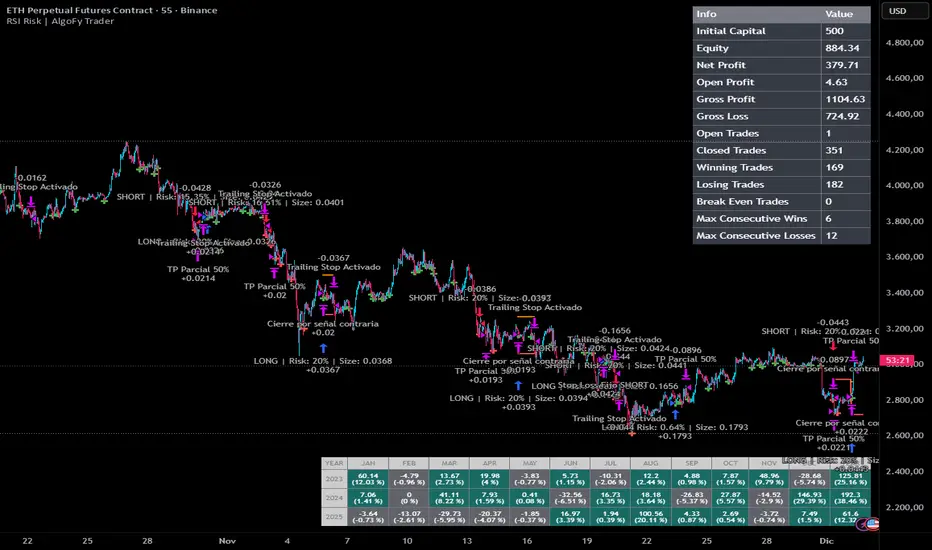

RSI Risk | AlgoFy TraderRSI Risk | AlgoFy Trader

Overview

The RSI Risk | AlgoFy Trader is a trading system that combines RSI-based entry signals with automated capital management. This strategy identifies potential momentum shifts while controlling risk through calculated position sizing.

Key Features

Dynamic Risk Management:

Fixed Risk Per Trade: Users set maximum risk percentage per trade.

Automatic Position Sizing: Calculates position size based on stop-loss distance.

Capital Protection: Limits each trade's risk to user-defined percentage.

RSI Entry System:

Momentum Detection: Uses RSI crossovers above/below defined thresholds.

Clear Signals: Provides long/short entries on momentum transitions.

Multiple Exit Layers:

Dynamic Stop Loss: Stop based on recent price structure.

Fixed Safety Stop: Optional percentage-based stop loss.

Partial Take Profit: Optional early profit-taking.

Trailing Stop: Optional dynamic profit protection.

Performance Tracking:

Trade Statistics: Tracks win/loss streaks and performance metrics.

Monthly Dashboard: Shows monthly/yearly P&L with equity views.

Trade Details: Displays risk percentage and position size.

How It Works

Signal Detection: Monitors RSI for crossover events.

Risk Calculation: Determines stop-loss based on recent volatility.

Position Sizing: Calculates exact position to match risk percentage.

Example:

Account: $10,000 | Risk: 2% ($200 max)

Stop loss at 4% distance

Position size: $5,000

Result: 4% loss on $5,000 = $200 (2% of account)

Recommended Settings

Risk: 1-2% per trade

Enable fixed stop at 3-4%

Consider trailing stop activation

This script provides disciplined RSI trading with automated risk control, adjusting exposure while maintaining strict risk limits.

Strategy: HMA 50 + Supertrend SniperHMA 50 + Supertrend Confluence Strategy (Trend Following with Noise Filtering)

Description:

Introduction and Concept This strategy is designed to solve a common problem in trend-following trading: Lag vs. False Signals. Standard Moving Averages often lag too much, while price action indicators can generate false signals during choppy markets. This script combines the speed of the Hull Moving Average (HMA) with the volatility-based filtering of the Supertrend indicator to create a robust "Confluence System."

The primary goal of this script is not just to overlay two indicators, but to enforce a strict rule where a trade is only taken when Momentum (HMA) and Volatility Direction (Supertrend) are in perfect agreement.

Why this combination? (The Logic Behind the Mashup)

Hull Moving Average (HMA 50): We use the HMA because it significantly reduces lag compared to SMA or EMA by using weighted calculations. It acts as our primary Trend Direction detector. However, HMA can be too sensitive and "whipsaw" during sideways markets.

Supertrend (ATR-based): We use the Supertrend (Factor 3.0, Period 10) as our Volatility Filter. It uses Average True Range (ATR) to determine the significant trend boundary.

How it Works (Methodology) The strategy uses a boolean logic system to filter out low-quality trades:

Bullish Confluence: The HMA must be rising (Slope > 0) AND the Close Price must be above the Supertrend line (Uptrend).

Bearish Confluence: The HMA must be falling (Slope < 0) AND the Close Price must be below the Supertrend line (Downtrend).

The "Choppy Zone" (Noise Filter): This is a unique feature of this script. If the HMA indicates one direction (e.g., Rising) but the Supertrend indicates the opposite (e.g., Downtrend), the market is considered "Choppy" or indecisive. In this state, the script paints the candles or HMA line Gray and exits all positions (optional setting) to preserve capital.

Visual Guide & Signals To make the script easy to interpret for traders who do not read Pine Script, I have implemented specific visual cues:

Green Cross (+): Indicates a LONG entry signal. Both HMA and Supertrend align bullishly.

Red Cross (X): Indicates a SHORT entry signal. Both HMA and Supertrend align bearishly.

Thick Line (HMA): The main line changes color based on the trend.

Green: Bullish Confluence.

Red: Bearish Confluence.

Gray: Divergence/Choppy (No Trade Zone).

Thin Step Line: This is the Supertrend line, serving as your dynamic Trailing Stop Loss.

Strategy Settings

HMA Length: Default is 50 (Mid-term trend).

ATR Factor/Period: Default is 3.0/10 (Standard for trend catching).

Exit on Choppy: A toggle switch allowing users to decide whether to hold through noise or exit immediately when indicators disagree.

Risk Warning This strategy performs best in trending markets (Forex, Crypto, Indices). Like all trend-following systems, it may experience drawdown during prolonged accumulation/distribution phases. Please backtest with your specific asset before using it with real capital.

Triple Screen Scalper [Pro] + Dynamic Risk Engine + Smart DCA🚀 Strategy Concept

This algorithm utilizes a Triple Screen methodology to filter market noise and align trades with the path of least resistance. Instead of relying on a single timeframe, it analyzes market structure across three distinct "horizons" to ensure high-probability execution:

The Tide (Long-Term): Analyzes the dominant directional flow and market bias on higher timeframes.

The Wave (Medium-Term): Measures the strength of the current momentum and pauses trading during weak or "choppy" market phases.

The Ripple (Short-Term): Pinpoints precise entry zones by detecting over-extended price action and mean-reversion opportunities within the larger trend.

The system is fortified with a Smart DCA (Dollar Cost Averaging) Engine that adapts to volatility. It does not blindly add to positions; it calculates "Risk Room" and "Trend Stability" before every additional entry, ensuring capital is deployed efficiently rather than recklessly.

⚙️ Configuration Guide (Variable Explanations)

💰 Position & Leverage

Trade Direction: Choose between Long, Short, or Auto. In "Auto," the system trades both directions based on the dominant trend.

Target Entry Leverage (x): The desired leverage for your initial entry.

Base Order Size (% of Equity): How much of your account balance is allocated to the very first trade of a sequence.

DCA Size Multiplier: Controls how much larger each subsequent order is compared to the previous one. A value of 1.0 means flat sizing; values above 1.0 increase the size of recovery orders.

KILL SWITCH: Max Effective Lev: A safety ceiling. If your total position's effective leverage exceeds this value, the strategy will force-close the position to prevent liquidation.

🚀 Profit Settings (Dynamic Exits)

Use Dynamic Profit?: If enabled, the take-profit target acts like a breathing lung—expanding during high volatility (to catch bigger moves) and contracting during quiet periods.

Gain Volatility Length: The lookback period used to measure recent market volatility.

Gain Multiplier: Scales the profit target. Higher numbers require a larger price move to hit profit; lower numbers take profit sooner.

Minimum Profit Floor %: A hard limit ensuring the target never drops below this percentage, even in extremely low-volatility markets.

📉 Trend & Momentum Filters

Trend Strength Threshold: Defines the minimum "velocity" required to trade. This filters out flat, ranging markets where trends are not established.

Momentum Sensitivity (K/D/Smooth): These variables tune the sensitivity of the entry trigger.

Lower numbers = Faster entries (more trades, potentially more noise).

Higher numbers = Slower, more confirmed entries.

Overbought / Oversold Levels: The specific zones (0-100) where price is considered statistically over-extended, triggering a reversal signal.

🛡️ Risk & DCA Settings

Enable Hard Stop Loss: A traditional safety stop based on a fixed percentage.

Max DCA Orders: The maximum number of times the strategy is allowed to "average down" on a position.

Require Trend for DCA?: If TRUE, the strategy will only add to a losing position if the broader market trend is still valid. If the trend breaks, it stops buying.

DCA Volatility Length/Multiplier: Controls the spacing between buy orders.

High Multiplier = Orders are spread far apart (safer for crashes).

Low Multiplier = Orders are closer together (faster recovery in normal dips).

Risk Scaling: A unique feature that pushes DCA orders further away as your leverage increases, protecting you from adding too much risk too quickly.

Base DCA %: The minimum distance required between orders, regardless of volatility.

⏱️ Timers & Cooldowns

Fast / Slow Cooldown: The minimum time (in seconds) the strategy must wait between realizing a profit and opening a new trade. This prevents "revenge trading" or entering twice on the same candle.

Position Cooldown: A specific timer applied after a large position is closed to let the market settle.

🎯 Daily S/R Targets

Enable Daily S/R: If enabled, the strategy will attempt to "snipe" exits at calculated daily support and resistance pivots.

Proximity Threshold: How close the price must get to a daily level to trigger an early exit.

⚠️ Risk Disclaimer

This script is an automated tool for analysis and execution assistance. It employs averaging techniques (DCA) which involve calculated risk. While the "Kill Switch" and "Risk Scaling" features are designed to mitigate exposure, users should thoroughly backtest and understand the "Multiplier" settings before deploying real capital. Past market structure is not a guarantee of future performance.