T3 [RATE OF CHANGE] by SKiNNiEHDeveloped by Tim Tillson, the Tilson Moving Average (T3) is a trend indicator with the advantage of having less lag than other ones. That is, a faster moving average. The T3 moving average is an "indicator of an indicator" as it includes several EMAs of another EMA. Unlike other moving averages, the t3 adds the so-called volume factor, a value between 0 and 1.

The T3 RATE OF CHANGE by SKiNNiEH is a unique indicator that integrates the T3 moving average with a normalized Rate of Change (RoC) calculation. Unlike traditional T3 moving averages, this indicator provides additional smoothing modes (SINGLE, DOUBLE & TRIPLE) for the T3, whilst enhancing visual feedback of the plotted line by generating a dynamic line thickness, a dynamic line color & brightness and trade entry bars, offering traders a more dynamic view of market conditions without going "overboard" with settings.

How It Works

Visualization

The T3 line varies in thickness and color based on the RoC values, giving traders visual cues about market strength and direction.

Thicker and brighter lines indicate stronger trends, while thinner and duller lines suggest weaker trends.

Rate of Change Filte r

This filter refines trend detection by using the line thickness measurement.

Adjustable from 0 (disabled) to 4, where higher settings only consider stronger trends for signals.

The T3 line turns gray when the filter is triggered or when the RoC is extremely low, signaling a weak or neutral market.

T3 Calculation (mode)

SINGLE

The T3 calculation is applied once to the closing price.

This mode has the least smoothing effect and the least lag. It reacts more quickly to price changes but is less smooth.

DOUBLE

The T3 calculation is applied twice sequentially.

The first T3 calculation smooths the closing price.

The second T3 calculation smooths the result of the first T3 calculation.

This mode provides more smoothing and introduces more lag compared to SINGLE mode. It is smoother but reacts slower to price changes.

TRIPLE

The T3 calculation is applied three times sequentially.

The first T3 calculation smooths the closing price.

The second T3 calculation smooths the result of the first T3 calculation.

The third T3 calculation smooths the result of the second T3 calculation.

This mode provides the most smoothing and introduces the most lag by reacting the slowest to price changes.

Rate of Change (RoC) Calculation

The script calculates the Rate of Change (RoC) for the T3 values based on the selected mode (SINGLE, DOUBLE, TRIPLE). The RoC measures the percentage change between the most recent value and a value in the past. The measurement is then normalized in three different ranges.

Normalization 5: Determines T3 line thickness on a scale from 0 - 5

Normalization 10: Determines T3 color brightness on a scale from 0 - 10

Normalization 100: Determines Rate of Change percentage

Rate of Change Filter

The script uses the RoC filter to refine the trend detection logic. By using the line thickness measurement, a filter can be enabled by setting this input on 1 - 4. As an example, setting this to 4 means that only a line thickness of 5 would be considered for a trade signal. Setting this to 0 disables the filter. The T3 line will turn gray when the filter is triggered, the T3 line can also turn gray without the filter, when the Rate of Change is extremely low.

Trade Signals

A trade signal is printed as a vertical green or red bar when the following conditions are met:

Long:

Closing price is above the T3 line

Rate of Change percentage is above 0

Previous trade signal was a short signal **

Rate of Change is not filtered

Short:

Closing price is below the T3 line

Rate of Change percentage is below 0

Previous trade signal was a long signal **

Rate of Change is not filtered

** Or this is the very first recorded trade signal

It should be noted that the trade signals in this script are trade entry signals, not trade exit signals. Use at your own risk.

Instructions for Use

Setting Up the Indicator

Apply the indicator to your trading chart.

Choose the desired T3 mode (SINGLE, DOUBLE, TRIPLE) based on your need for smoothing and lag.

Set the desired length (lookback period).

Set the desired factor between 0 and 1 (increments of 0.1)

Choose an overall line thickness and brightness that suits your screen and taste preferences.

Apply the Rate of Change filter. Setting this to 0 will disable the filter

Tip: use the trade entry vertical bars as a visual calibration tool the adjust mode, length, factor and filter.

Interpreting Visual Cues

Observe the T3 line's thickness: thicker lines indicate stronger trends, while thinner lines suggest weaker trends.

Observe the T3 line's color and color brightness: green indicates a more bullish trend, while red indicates a more bearish trend. A brighter color suggest a stronger trend. A gray color means the RoC is very low / neutral, or the RoC filter is active.

Observe the T3 line's location relative to price: below price indicates a more bullish trend, above price indicates a more bearish trend. The T3 line distance from price can also be an indication of trend strength.

Observe vertical bars: a vertical bar is printed green when long conditions are met, a vertical bar is printed red when short conditions are met. See the rules that explain the trigger for this bar above.

Alerts

Go to the settings tab, set the condition to T3.RoC.S + LONG or SHORT.

Enter an alert name and message.

Configure your notification preferences in the notifications tab and create the alert

Notifications-tab: Choose your notification preferences

Create the alert.

Taux de change (ROC)

LBR-S310ROC @shrilssOriginally made by Linda Raschke, The S310ROC Indicator combines the Rate of Change (ROC) indicator with the 3-10 Oscillator (Modified MACD) and plots to capture rapid price movements and gauge market momentum.

- Rate of Change (ROC): This component of the indicator measures the percentage change in price over a specified short interval, which can be set by the user (default is 2 days). It is calculated by subtracting the closing price from 'X' days ago from the current close.

- 3-10 Oscillator (MACD; 3,10,16): This is a specialized version of the Moving Average Convergence Divergence (MACD) but uses simple moving averages instead of exponential. Using a fast moving average of 3 days and a slow moving average of 10 days with a smoothing period of 16.

- ROC Dots: A great feature based on the oscillator's readings. Dots are displayed directly on the oscillator or the price chart to provide visual momentum cues:

- Aqua Dots: Appear when all lines (ROC, MACD, Slowline) are sloping downwards, indicating bearish momentum and potentially signaling a sell opportunity.

- White Dots: Appear when all lines are sloping upwards, suggesting bullish momentum and possibly a buy signal.

ROC [CHE] with Kernel SelectionIntroduction:

The script titled "ROC with Kernel Selection" utilizes Rate of Change (ROC) to analyze price momentum in financial markets. It incorporates a kernel selection mechanism to smooth ROC values, enhancing clarity in trend identification.

Middle Part:

The script begins by calculating ROC over a specified period using the formula:

roc = (close - close ) / close * 100

The period length determined by the user. The result is plotted alongside a zero line for reference.

The kernel selection aspect allows users to choose from various smoothing techniques:

Linear

Exponential

Epanechnikov

Triangular

Cosine

Each kernel applies a different weighting function to ROC values, influencing the sensitivity and smoothness of the plotted line. Users can customize parameters such as bandwidth and color preferences for up and down movements, facilitating visual interpretation.

The main logic of the script involves iterating through historical data to compute weighted averages of ROC values based on the selected kernel. It adjusts graphical elements dynamically, highlighting changes in momentum direction with color-coded lines and directional symbols (▲ or ▼).

Conclusion:

In conclusion, "ROC with Kernel Selection" offers a flexible toolset for traders and analysts to assess price momentum robustly. By integrating kernel-based smoothing techniques, it enhances the clarity of ROC signals, aiding in the identification of trends and potential reversals in financial markets.

DeltaDetector PINESCRIPTLABSDescription:

This technical indicator, DeltaDetector PINESCRIPTLABS, is designed to identify significant changes in the price of an asset relative to the previous close. Users can customize the percentage change they want to monitor.

Usage Instructions:

Adjust the desired percentage change using the "Price Change Value (%)" user input.

Observe the green diamonds to identify significant price increases above the specified percentage.

Observe the red diamonds to identify significant price decreases below the specified percentage.

"In the following image, we observe a 4-hour timeframe for EURUSD, where we set a candle change percentage of 0.45%. We can see how the price reacts afterwards to the size of these candles."

"In the pair BTCUSDT.P, we designated a single candle change percentage of 3%, and observed how the price reacted after that candle."

This allows you to easily identify significant price movements within the range specified by the percentage change you have set.

Español:

Descripción:

Este indicador técnico, DeltaDetector PINESCRIPTLABS, está diseñado para identificar cambios significativos en el precio de un activo en relación con el cierre anterior. Los usuarios pueden personalizar el porcentaje de cambio que desean monitorear.

Instrucciones de uso:

Ajuste el porcentaje de cambio deseado utilizando la entrada de usuario "Price Change Value (%)".

Observe los diamantes verdes para identificar aumentos significativos en el precio por encima del porcentaje especificado.

Observe los diamantes rojos para identificar disminuciones significativas en el precio por debajo del porcentaje especificado.

"En la siguiente imagen, observamos un marco de tiempo de 4 horas para EURUSD, donde establecimos un porcentaje de cambio de vela del 0,45%. Podemos ver cómo reacciona el precio después al tamaño de estas velas."

"En el par BTCUSDT.P, designamos un porcentaje de cambio de vela único del 3%, y observamos cómo reaccionó el precio después de esa vela."

Esto te permite identificar fácilmente movimientos significativos en el precio dentro del rango especificado por el porcentaje de cambio que has establecido.

IndexogramIndexogram is a platform designed to help traders analyze the Commitment of Traders (COT) report data. It specifically focuses on the Rate Of Change (ROC) of the COT data, visualized using a unique polyline plotting technique.

Commitments of Traders % Rate Of Change (%ROC):

The COT %ROC indicates the momentum of trader positions over a specified period. This measure is crucial for understanding shifts in market sentiment and potential future price movements.

Unique Polyline Plotting Technique:

Unlike traditional line or bar charts, the polyline plotting technique used in Indexogram offers a more nuanced and detailed view of the %ROC data.

Multiple Ticker Monitoring:

Indexogram allows the setup of up to five different tickers. Traders can assign different weightages to these tickers, enabling a customized and weighted view of their %ROC data. This feature is beneficial for tracking a diversified portfolio or comparing different assets.

Average ROI Plot:

An additional feature is the Average ROI plot, which provides the average return on investment (ROI) of the five selected tickers. This plot helps traders quickly assess the overall performance of their monitored assets.

Strategy for Traders

Diversified Monitoring:

By setting up five different tickers with varying weightages, traders can diversify their monitoring efforts across different assets or markets. This diversification helps in reducing risk and identifying opportunities in different sectors or asset classes.

Weightage Customization:

Assign weightages based on market conditions or personal trading strategy. For example, if a trader believes that commodities are likely to outperform equities in the near term, they can assign a higher weightage to commodities-related tickers.

Analyzing %ROC Trends:

Use the polyline plots to identify significant %ROC trends. A rising %ROC might indicate increasing momentum and a potential buying opportunity, while a falling %ROC could signal decreasing momentum and a potential selling opportunity.

Average ROI Analysis:

Use the Average ROI plot to gauge the overall performance of the selected assets. If the average ROI is positive and trending upwards, it indicates a generally favorable market condition for the monitored assets.

Tactical Adjustments:

Regularly review and adjust the selected tickers and their weightages based on changing market conditions, news, and personal insights. This flexibility allows traders to adapt their strategy in response to new information.

Important Notes:

Indexogram is a tool to identify potential tradings, not a guaranteed predictor of future price movements.

Trend, Momentum, Volume Delta Ratings Emoji RatingsThis indicator provides a visual summary of three key market conditions - Trend, Momentum, and Volume Delta - to help traders quickly assess the current state of the market. The goal is to offer a concise, at-a-glance view of these important technical factors.

Trend (HMA): The indicator uses a Hull Moving Average (HMA) to assess the overall trend direction. If the current price is above the HMA, the trend is considered "Good" or bullish (represented by a 😀 emoji). If the price is below the HMA, the trend is "Bad" or bearish (🤮). If the price is equal to the HMA, the trend is considered "Neutral" (😐).

Momentum (ROC): The Rate of Change (ROC) is used to measure the momentum of the market. A positive ROC indicates "Good" or bullish momentum (😀), a negative ROC indicates "Bad" or bearish momentum (🤮), and a zero ROC is considered "Neutral" (😐).

Volume Delta: The indicator calculates the difference between the current trading volume and a simple moving average of the volume (Volume Delta). If the Volume Delta is above a user-defined threshold, it is considered "Good" or bullish (😀). If the Volume Delta is below the negative of the threshold, it is "Bad" or bearish (🤮). Values within the threshold are considered "Neutral" (😐).

The indicator displays these three ratings in a compact table format in the top-right corner of the chart. The table uses color-coding to quickly convey the overall market conditions - green for "Good", red for "Bad", and gray for "Neutral".

This indicator can be useful for traders who want a concise, at-a-glance view of the current market trend, momentum, and volume activity. By combining these three technical factors, traders can get a more well-rounded understanding of the market conditions and potentially identify opportunities or areas of concern more easily.

The user can customize the indicator by adjusting the lengths of the HMA, ROC, and Volume moving average, as well as the Volume Delta threshold. The colors used in the table can also be customized to suit the trader's preferences.

Rate of Change Suite [QuantraSystems]Rate of Change Suite

Introduction

The "Rate of Change Suite" (𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮) refines traditional RoC concepts by incorporating additional elements that provide more nuanced views of market trends, potential reversions, and momentum shifts.

Its main benefits are that it allows traders to detect momentum changes and frontrun trend shifts.

The suite is designed to be highly adaptable, catering to various trading styles, timeframes and market conditions. It is comprised of 3 metrics:

The RoC base line plots the rate of change, the Signal Histogram to confirm trends, and the Signal Confirmation Oscillator to inform reversal probabilities. For the early detection of trend shifts, the 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 is a comprehensive tool for the toolkit of modern traders.

A core component of the 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 is the ability to apply its processing techniques to any other indicator found on TradingView - essentially leveraging the signal power of existing analysis methods. This is achieved by modifying the ‘Source’ input.

Legend

𝓡𝓸𝓒 base line: The primary component of the suite, the RoC Line, offers a direct view of market momentum. An upward trending RoC line informs the potential for a long position, while a downward trend might signal the opportunity for a short position. Both include a secondary confirmation by the color change of the line itself. The Heikin Ashi transformed version of the RoC line provides greater resistance to rapid movements, or outliers.

Signal Histogram: This feature works in tandem with the base RoC Line, providing an additional third confirmation of trends. A rising histogram supports the presence of an upward trend. Conversely, a declining histogram aligns with downward trends.

Signal Confirmation Oscillator: This dotted-line is crucial for detecting peaks or troughs in market momentum: These can precede reversals or shifts in the prevailing trend. Traders can use this signal to anticipate and prepare for potential changes quicker than others.

Case Study

Primarily a tool to follow trends, the 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 implies much more – you can trade with a confirmed trend signal entry and a mean reversion signal for the exit:

Here we see two practical cases of the 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 on the 1h BTC chart.

In the first scenario, the trader waits for three confirmations from the indicator.

The 𝓡𝓸𝓒 baseline to lead the run and looks for confirmation two and three:

𝓡𝓸𝓒 base line color shifts

and the Signal Histogram follows past the null midline.

The trader has adjusted their risk beforehand and enters the long position.

The 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 shows traders when to take profit:

The Signal Confirmation Oscillator (SCO, dotted line) moves beyond the 𝓡𝓸𝓒 baseline and the Signal Histogram. The trader can take 50% of the profit already.

The trader waits patiently, and if the SCO reverses, the rest of the position is closed.

The same works inversely for the second trade, which successfully frontran the decline shortly after.

Recommended Settings

Day Trading (1H chart)

Length: 30

Smooth Length: 10

Display Variant: Classic

Choose Mode: Trend Following

Investing – Follow Trend (1D chart)

Default settings

Notes

Quantra Standard Value Contents:

The Heikin-Ashi (HA) candle visualization smoothes out the signal line to provide more informative insights into momentum and trends. This allows earlier entries and exits by observing the indicator values transformed by the HA.

Various visualization options are available to adjust the indicator to the user’s preference: Aside from HA, a classic line, or a hybrid of both.

A special feature of Quantra’s indicators is that they are probabilistically built - therefore they work well as confluence and can easily be stacked to increase signal accuracy.

To add to Quantra's indicators’ utility we have added the option to change the price bars’ colors based on different signals:

Choose Mode for Coloring

Trend Following (Indicator above mid line counts as uptrend, below is downtrend)

Extremes (Everything beyond the SD bands is highlighted to signal mean reversion)

Candles (Color of HA candles as barcolor)

Reversions (Only for HA) (Reversion Signals via the triangles if HA candles change trend while beyond the SD bands, high probability entries/exits)

Divergence Sensitivity: Quantra’s 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 is finely tuned to detect divergences, a key feature for identifying possible trend reversals.

Trend Following and Reversions: Primarily a tool for trend following, the 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 is also adept at spotting potential reversions and slowdowns in momentum.

Range Trading Compatibility: In its Heikin Ashi Candles mode, the suite becomes particularly effective for range trading strategies.

High Customizability: Traders can customize the suite with various visualization options, including classic line representation, HA transformation, and bar coloring. These can be based on Heikin Ashi Candles or Trend Following approaches, providing flexibility to adapt to different trading scenarios.

Methodology

The 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 is built on a foundation of functions that define and calculate the Rate of Change. They employ a variety of moving average types (SMA, EMA, DEMA, TEMA, WMA, etc.) which can be selected to optimize the RoC line.

A bespoke function to calculate Heikin-Ashi values is engineered to offer a more consistent view of the trend.

The Signal Histogram is derived by mathematically processing the base RoC signal. The Signal Confirmation Oscillator is based on a modified formula, adjusted to align with the RoC dynamics.

With a range of customization options for its visual presentation, including color schemes and display styles, the 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 is designed to cater to both trend following indications as well as finding signals for mean reversion trades. This multifaceted approach enables the 𝓡𝓸𝓒 𝓢𝓾𝓲𝓽𝓮 to allow the trader to combine signals of both types to de-risk his positions.

Rate of Change RSIIndicator Name: Rate of Change RSI

Description:

The Rate of Change (ROC) of the Relative Strength Index (RSI) is a technical indicator designed to provide insights into the momentum of an asset's price movement. It combines the Relative Strength Index (RSI), a popular momentum oscillator, with the Rate of Change (ROC) concept to assess the speed at which RSI values are changing.

How It Works:

Relative Strength Index (RSI): The RSI measures the magnitude of recent price changes to evaluate overbought or oversold conditions in an asset. It oscillates between 0 and 100, with readings above 70 typically indicating overbought conditions and readings below 30 indicating oversold conditions.

Rate of Change (ROC): The ROC calculates the percentage change in a given indicator over a specified period. In this indicator, we apply the ROC to the RSI values to determine how quickly the RSI is changing over time.

Key Features:

Acceleration and Deceleration: The ROC of RSI helps traders identify whether the momentum of the RSI is accelerating or decelerating. Positive values suggest increasing momentum, while negative values indicate decreasing momentum.

Dynamic Color Change: The color of the ROC RSI line changes dynamically based on the RSI level. When the RSI is between 0 and 40, the line color is blue, indicating potential oversold conditions. When the RSI is between 40 and 60, the line color is yellow, suggesting neutral conditions. When the RSI is above 60, the line color changes to green, indicating potential overbought conditions.

How to Use:

Acceleration: When the ROC RSI is positive and increasing while the RSI is above 60 (green), it may signal strong upward momentum.

Deceleration: Conversely, if the ROC RSI is negative and decreasing while the RSI is below 40 (blue), it may indicate weakening downward momentum.

Originality and Usefulness:

This indicator combines the RSI, a well-known momentum oscillator, with the ROC concept to provide a unique perspective on momentum dynamics. By dynamically adjusting the color of the ROC RSI line based on RSI levels, traders can quickly assess potential overbought or oversold conditions in the market.

Chart:

The chart displayed alongside this script provides a clean and easy-to-understand visualization of the ROC RSI indicator. The ROC RSI line color changes dynamically based on RSI levels, allowing traders to visually identify potential market conditions at a glance.

TASC 2024.03 Rate of Directional Change█ OVERVIEW

This script implements the Rate of Directional Change (RODC) indicator introduced by Richard Poster in the "Taming The Effects Of Whipsaw" article featured in the March 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Richard Poster discusses an approach to potentially reduce false trend-following strategy entry signals due to whipsaws in forex data. The RODC indicator is central to this approach. The idea behind RODC is that one can characterize market whipsaw as alternating up and down ZigZag segments. By counting the number of up and down segments within a lookback window, the RODC indicator aims to identify if the window contains a significant whipsaw pattern:

RODC = 100 * Segments / Window Size (bars)

Larger RODC values suggest elevated whipsaw in the calculation window, while smaller values signify trending price activity.

█ CALCULATIONS

• For each price bar, the script iterates through the lookback window to identify up and down segments.

• If the price change between subsequent bars within the window is in the direction opposite to the current segment and exceeds the specified threshold , the calculation interprets the condition as a reversal point and the start of a new segment.

• The script uses the number of segments within the window to calculate RODC according to the above formula.

• Finally, the script applies a simple moving average to smoothen the RODC data.

Users can change the length of the lookback window , the threshold value, and the smoothing length in the "Inputs" tab of the script's settings.

Rate of Change MachineRate of Change Machine

Author: RWCS_LTD

Disclaimer: This script is provided for informational purposes only and should not be considered financial advice. Trading involves substantial risk, and past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions.

Introduction:

The Rate of Change Machine is a script designed to assist traders in analyzing multiple cryptocurrency trading pairs simultaneously. This comprehensive indicator offers a holistic view of the rate of change and related metrics, aiding traders in making informed decisions.

Asset Selection:

The script enables users to select up to nine different cryptocurrency trading pairs for in-depth analysis.

Volume Calculation:

Volume plays a crucial role in the analysis, with customizable parameters for volume weighting and length.

Relative Strength Calculation:

Relative Strength is determined through two Exponential Moving Averages (EMA) with user-defined lengths.

Timeframe Weightings:

Different timeframes (1D, AVG 3D, AVG 5D, AVG 7D, AVG 14D, AVG 30D) are assigned weightings to calculate a comprehensive trend score.

Weighted Average and Individual Rate of Change (RoC) Calculation:

The getWeightedAvgAndIndividualROC function calculates the RoC for each selected trading pair based on the given timeframes and weights.

Table Setup:

A table is created to display the results for each trading pair, including relative strength, volume trend, RoC for different timeframes, and a weighted trend score.

Table Formatting:

The table is formatted with different colors indicating positive or negative values for easier interpretation.

Table Position and Size:

Users can customize the position and size of the table on the chart.

Data Retrieval:

The script retrieves the calculated values for each trading pair using the request.security function.

Output:

The final output is a table on the chart, showing relevant information for the selected trading pairs, aiding traders in making informed decisions based on the rate of change and other factors. This indicator provides a comprehensive view of the rate of change and related metrics for multiple trading pairs, assisting traders in identifying potential trends and making informed trading decisions.

Z-score changeAs a wise man once said that:

1. beginners think in $ change

2. intermediates think in % change

3. pros think in Z change

Here is the "Z-score change" indicator that calculates up/down moves normalized by standard deviation (volatility) displayed as bar chart with 1,2 and 3 stdev levels.

ROC & EMAIn summary, this allows you to plot the ROC, its EMA, and dynamically display the value of this EMA on the chart.

You can configure different lengths and colors.

Unpretentious code, just for the pleasure of sharing.

Thank you for sharing your comments with me, which will be welcome.

Nasan Rate of Change (ROC)**NOTE: FOR COMPARISON TRADITIONAL ROC IS PLOTTED WITH THE SAME ROC LENGTH OF 9. IT IS NOT PART OF THE INDICATOR"

The Nasan ROC indicator is smoothed version of the of the traditional ROC indicator. The Nasna ROC uses a triple pass moving average differencing strategy. A cumulative sum of the deviations obtained from the moving average differencing provides a smooth "noise free" trend and this cumulative sum of deviations is used for calculating ROC.

Let's break down the components and understand the indicator we discussed earlier:

Sequential Triple Pass Filter:

Three filters with lengths specified by length1, length2, and length3 are applied to the closing prices (close).

The filters involve calculating the cumulative sum of the differences between the closing prices and their respective moving averages.

The idea is to detrend the data and accumulate the deviations from the average over time, emphasizing longer-term trends.

Calculation of Rate of Change (ROC) of Cumulative Sum:

The Rate of Change (ROC) of the cumulative sum (rocCumulativeSum) is calculated using the ta.roc function with a specified length (rocLength).

ROC measures the percentage change in the cumulative sum over a specified period.

The ROC histogram provides insights into the momentum of the detrended series. Positive values suggest increasing momentum, while negative values suggest decreasing momentum.

Pay attention to the color of the histogram bars.

The histogram bars are colored green if the current ROC value is greater than or equal to the previous ROC value, and red otherwise.

This coloring is based on the concept that a positive ROC suggests upward momentum, while a negative ROC suggests downward momentum.

Volatility - Volume Impact:

The Average True Range (ATR) is calculated with a period of 14.

Volume strength is calculated as a factor (VCF) that considers the ratio of the simple moving average (SMA) of the current volume to the SMA of the volume over a longer period (144).

This volume factor (VCF) is then multiplied by ATR, creating a synergy with volatility and volume.

Visualization with Background Color Gradient:

A background color gradient is applied to the chart based on the calculated volume strength (f1).

The gradient color ranges from black (indicating low ATR and volume strength) to purple (indicating high ATR and volume strength). A low value indicates a ranging market with no significant price movements and it is safter to avoid signals generated from ROC histogram in these region.

Synergy of ROC and Volume Strength:

Observe how the ROC signals align with the background color gradient. For example, confirm whether positive ROC aligns with periods of high ATR and volume strength.

This synergy can provide confirmation or divergence signals, adding another layer of analysis.

Detrended Price Rate of ChangeThe Detrended Price Rate of Change is an oscillator developed to help traders identify potential conditions of overbought and oversold markets.

The formula of the oscillator includes both the Detrended price formula, useful to spot divergences, and the Rate of change simplified formula, which helps in identifying overextended markets and gives useful information on price momentum.

ROC slope indicatorI would like to present to you an indicator that I think is missing.

It is based on the ROC indicator (RATE OF CHANGE).

The ROC indicator is a measure of the rate of change in the exchange rate, as its name implies.

From which the angle of the slope of the change can be calculated. This angle is displayed on an oscillator.

The value of the oscillator can thus take max 90 and min -90 degrees as a result of the angle function calculation. Thus, the slope of the exchange rate can be continuously monitored on the indicator.

The length parameter is used to control how many candles should be included in the calculation, as is usually the case for all indicators, and a simple moving average is used to smooth the oscillator.

I added two more lines to allow monitoring of extreme high angle values.

This is a very simple indicator. I hope this approach will help you in your analysis of exchange rates and I welcome any ideas based on this oscillator.

Rate of Change StrategyRate of Change Strategy :

INTRODUCTION :

This strategy is based on the Rate of Change indicator. It compares the current price with that of a user-defined period of time ago. This makes it easy to spot trends and even speculative bubbles. The strategy is long term and very risky, which is why we've added a Stop Loss. There's also a money management method that allows you to reinvest part of your profits or reduce the size of your orders in the event of substantial losses.

RATE OF CHANGE (ROC) :

As explained above, the ROC is used to situate the current price compared to that of a certain period of time ago. The formula for calculating ROC in relation to the previous year is as follows :

ROC (365) = (close/close (365) - 1) * 100

With this formula we can find out how many percent the change in the current price is compared with 365 days ago, and thus assess the trend.

PARAMETERS :

ROC Length : Length of the ROC to be calculated. The current price is compared with that of the selected length ago.

ROC Bubble Signal : ROC value indicating that we are in a bubble. This value varies enormously depending on the financial product. For example, in the equity market, a bubble exists when ROC = 40, whereas in cryptocurrencies, a bubble exists when ROC = 150.

Stop Loss (in %) : Stop Loss value in percentage. This is the maximum trade value percentage that can be lost in a single trade.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by an amount chosen by the user.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:BTCUSD in 1D timeframe with the following parameters :

ROC Length = 365

ROC Bubble Signal = 180

Stop Loss (in %) = 6

LONG CONDITION :

We are in a LONG position if ROC (365) > 0 for at least two days. This allows us to limit noise and irrelevant signals to ensure that the ROC remains positive.

SHORT CONDITION :

We are in a SHORT position if ROC (365) < 0 for at least two days. We also open a SHORT position when the speculative bubble is about to burst. If ROC (365) > 180, we're in a bubble. If the bubble has been in existence for at least a week and the ROC falls back below this threshold, we can expect the asset to return to reasonable prices, and thus a downward trend. So we're opening a SHORT position to take advantage of this upcoming decline.

EXIT RULES FOR WINNING TRADE :

The strategy is self-regulating. We don't exit a LONG trade until a SHORT signal has arrived, and vice versa. So, to exit a winning position, you have to wait for the entry signal of the opposite position.

RISK MANAGEMENT :

This strategy is very risky, and we can easily end up on the wrong side of the trade. That's why we're going to manage our risk with a Stop Loss, limiting our losses as a percentage of the trade's value. By default, this percentage is set at 6%. Each trade will therefore take a maximum loss of 6%.

If the SL has been triggered, it probably means we were on the wrong side. This is why we change the direction of the trade when a SL is triggered. For example, if we were SHORT and lost 6% of the trade value, the strategy will close this losing trade and open a long position without taking into account the ROC value. This allows us to be in position all the time and not miss the best opportunities.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

NOTE :

Please note that the strategy is backtested from 2017-01-01. As the timeframe is 1D, this strategy is a medium/long-term strategy. That's why only 34 trades were closed. Be careful, as the test sample is small and performance may not necessarily reflect what may happen in the future.

Enjoy the strategy and don't forget to take the trade :)

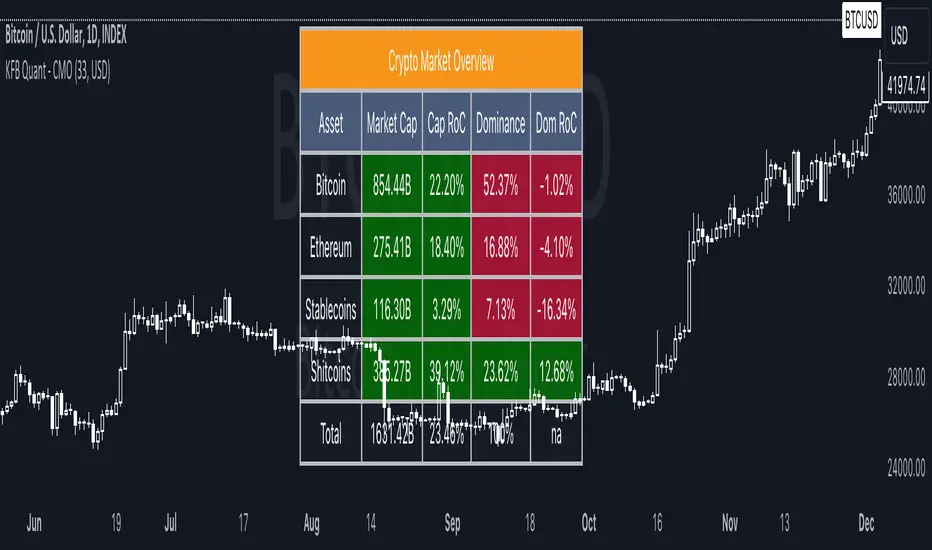

Crypto Market OverviewCrypto Market Overview

The Crypto Market Overview (CMO) indicator is your one-stop tool for keeping tabs on the cryptocurrency market. It provides a comprehensive snapshot of key data and trends, helping you make informed decisions in the fast-paced world of crypto trading. Here's what this indicator offers:

1. Lookback Period Control:

You can customize the lookback period for percentage change calculations, tailoring it to your specific analysis needs.

2. Currency Selection:

Choose your preferred currency to view market data in your desired denomination.

3. Major Market Cap Data:

Real-time information on Bitcoin (BTC) and Ethereum (ETH) market caps.

Total market capitalization data for the entire crypto market.

4. Stablecoin Market Cap Data:

Keep track of stablecoin market caps, including USDT, USDC, DAI, TUSD, and BUSD.

Get a clear picture of the stablecoin segment of the market.

5. Shitcoin Market Cap Data:

An interesting category that represents the market cap of all cryptocurrencies not classified as major or stable.

6. Dominance Data:

Dominance percentages for BTC, ETH, stablecoins and shitcoins.

Total market dominance, allowing you to gauge the influence of major cryptocurrencies.

7. Rate of Change (RoC) Metrics:

Monitor the RoC for market caps and dominance percentages.

Positive or negative trends are clearly highlighted with color-coded indicators.

8. Intuitive Table Layout:

A user-friendly table layout displays all the data.

Key assets such as Bitcoin and Ethereum are listed along with their market caps and dominance.

9. Color Coding:

Upward and downward trends are easily identifiable with color-coded cells.

A white background with bold text ensures readability.

The Crypto Market Overview indicator is an invaluable tool for cryptocurrency traders and enthusiasts, offering a quick and convenient way to stay updated on market dynamics. It's perfect for making data-driven decisions in the ever-changing world of digital assets.

Advanced Market Opening Gap DetectorThe Advanced Market Opening Gap Detector (AMOGD) is a Pine Script indicator designed to help you identify market gaps at the opening of a new trading day. Gaps are areas on a chart where the price of a security moves sharply up or down with little or no trading in between. They are significant as they may indicate a change in market sentiment. This indicator highlights the size and direction of the opening gap, allowing you to potentially adjust your strategies accordingly.

By setting a minimum gap size, you can filter out smaller, less significant gaps, focusing only on larger gaps which may have more substantial implications. You can define the minimum gap size in points or pips, providing flexibility based on your trading preferences and the asset being traded.

How-to Use:

Apply the AMOGD indicator to your TradingView chart.

Configure the minimum gap size and unit (points or pips) based on your preference using the settings panel.

At the opening of each new trading day, the indicator will check for a gap between the previous close and the opening price.

If a valid gap is detected (i.e., the gap size meets or exceeds the minimum gap size specified), the indicator will:

Draw lines to indicate the opening price and previous close.

Display a label indicating the size of the gap.

Highlight the gap on the chart for better visibility.

Importance:

Market gaps can be pivotal points indicating a possible new trend or a continuation of the current trend. Being able to identify and analyze these gaps is crucial for making informed trading decisions. The AMOGD indicator automates the process of identifying and visualizing opening market gaps, saving traders time and allowing for quick assessment of market conditions at the start of each trading day. By setting a minimum gap size, traders can also filter out less significant price movements, allowing them to focus on potentially trend-changing gaps. This tool can be a valuable addition to a trader's toolkit, aiding in the analysis and interpretation of market behavior at the open, which is often a very volatile and crucial period in the trading day.

DISCLAIMER! RISK WARNING!

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. TRADERS SHOULD NOT BASE THEIR DECISION ON INVESTING IN ANY TRADING PROGRAM SOLELY ON THE PAST PERFORMANCE PRESENTED, ADDITIONALLY, IN MAKING AN INVESTMENT DECISION, TRADERS MUST ALSO RELY ON THEIR OWN EXAMINATION OF THE PERSON OR ENTITY MAKING THE TRADING DECISIONS.

How To Input CSV List Of Symbol Data Used For ScreenerExample of how to input multiple symbols at once using a CSV list of ticker IDs. The input list is extracted into individual ticker IDs which are then each used within an example screener function that calculates their rate of change. The results for each of the rate of changes are then plotted.

For code brevity this example only demonstrates using up to 4 symbols, but the logic is annotated to show how it can easily be expanded for use with up to 40 ticker IDs.

The CSV list used for input may contain spaces or no spaces after each comma separator, but whichever format (space or no space) is used must be used consistently throughout the list. If the list contains any invalid symbols the script will display a red exclamation mark that when clicked will display those invalid symbols.

If more than 4 ticker IDs are input then only the first 4 are used. If less than 4 ticker IDs are used then the unused screener calls will return `float(na)`. In the published chart the input list is using only 3 ticker IDs so there are only 3 plots shown instead of 4.

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

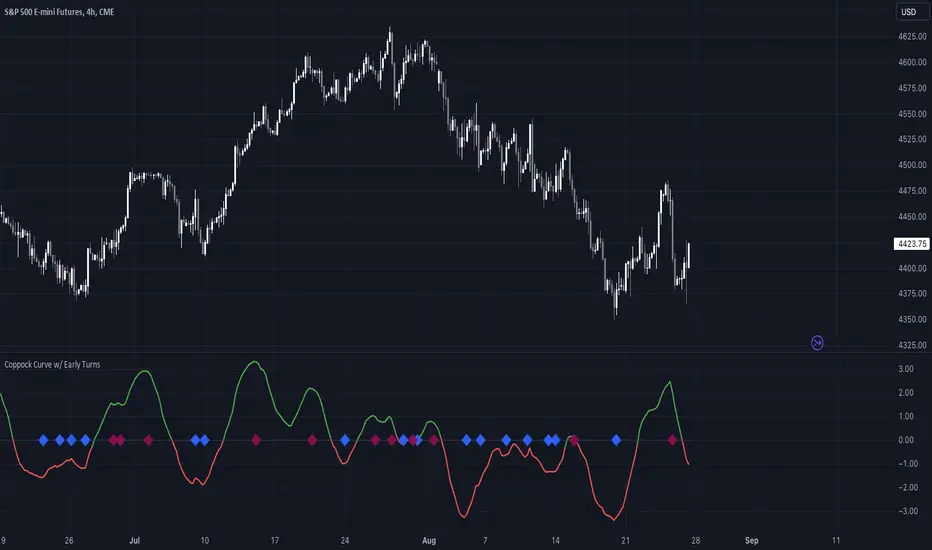

Coppock Curve w/ Early Turns [QuantVue]The Coppock Curve is a momentum oscillator developed by Edwin Coppock in 1962. The curve is calculated using a combination of the rate of change (ROC) for two distinct periods, which are then subjected to a weighted moving average (WMA).

History of the Coppock Curve:

The Coppock Curve was originally designed for use on a monthly time frame to identify buying opportunities in stock market indices, primarily after significant declines or bear markets.

Historically, the monthly time frame has been the most popular for the Coppock Curve, especially for long-term trend analysis and spotting the beginnings of potential bull markets after bearish periods.

The signal wasn't initially designed for finding sell signals, however it can be used to look for tops as well.

When the indicator is above zero it indicates a hold. When the indicator drops below zero it indicates a sell, and when the indicator moves above zero it signals a buy.

While this indicator was originally designed to be used on monthly charts of the indices, many traders now use this on individual equities and etfs on all different time frames.

About this Indicator:

The Coppock Curve is plotted with colors changing based on its position relative to the zero line. When above zero, it's green, and when below, it's red. (default settings)

An absolute zero line is also plotted in black to serve as a reference.

In addition to the classic Coppock Curve, this indicator looks to identify "early turns" or potential reversals of the Coppock Curve rather than waiting for the indicator to cross above or below the zero line.

Give this indicator a BOOST and COMMENT your thoughts!

We hope you enjoy.

Cheers!

Bar Color Long / Short Indicator With Advised SL Rev 1This is the Revised Version of Bar Color Long / Short Indicator With Advised SL with some extra features

Overview

This script is a trading indicator named "Bar Color Long / Short Indicator With Advised SL" designed for the TradingView platform. The indicator's primary purpose is to provide entry signals for long and short positions, based on various technical analysis methods. Additionally, the indicator suggests stop-loss levels for both long and short positions.

User Inputs

The indicator has several user inputs, such as:

Length

Smoothing

Multiplier

Show bar colors (ON/OFF)

When the bar colors are turned off, the alert signals for long and short positions will be displayed instead.

Custom Risk Calculation

The script calculates a custom risk level based on a modified version of the RSI (Relative Strength Index) formula. The custom risk level is divided into three categories: low, medium, and high.

Sentiment Score Calculation

The indicator calculates a sentiment score based on a combination of methods resembling EMA (Exponential Moving Average), MACD (Moving Average Convergence Divergence), and ROC (Rate of Change). The sentiment score is used to determine if the sentiment is positive or negative.

Bollinger Bands Percent and Combined Signal

The Bollinger Bands Percent is calculated, and the custom risk, sentiment score, and Bollinger Bands Percent are combined to generate a new signal. This signal is used in conjunction with EMA10 to determine the bar colors and provide entry signals.

Bar Colors

Based on the combined signal and EMA10, the script determines the bar colors as follows:

Orange: Positive sentiment

Blue: Negative sentiment

Gray: Neutral

Entry Signals and Alerts

When the bar colors are turned off, the indicator displays large green arrow signals for long (buy) positions and red arrow signals for short (sell) positions based on the sentiment and EMA10 conditions. The script also includes alert conditions for long and short signals, which can be used to set up notifications when these signals are triggered in the TradingView platform.

Advised Stop-Loss Levels

The indicator plots stop-loss lines for both long and short positions at the last candle, accompanied by labels showing the advised stop-loss levels in numeric values

Rev 1

added / changed :

SMA50 slope check

EMA20 higher or lower than EMA10

color ON/OFF changed

Signal once Buy and Sell

Kalman Filtered ROC & Stochastic with MA SmoothingThe "Smooth ROC & Stochastic with Kalman Filter" indicator is a trend following tool designed to identify trends in the price movement. It combines the Rate of Change (ROC) and Stochastic indicators into a single oscillator, the combination of ROC and Stochastic indicators aims to offer complementary information: ROC measures the speed of price change, while Stochastic identifies overbought and oversold conditions, allowing for a more robust assessment of market trends and potential reversals. The indicator plots green "B" labels to indicate buy signals and blue "S" labels to represent sell signals. Additionally, it displays a white line that reflects the overall trend for buy signals and a blue line for sell signals. The aim of the indicator is to incorporate Kalman and Moving Average (MA) smoothing techniques to reduce noise and enhance the clarity of the signals.

Rationale for using Kalman Filter:

The Kalman Filter is chosen as a smoothing tool in the indicator because it effectively reduces noise and fluctuations. The Kalman Filter is a mathematical algorithm used for estimating and predicting the state of a system based on noisy and incomplete measurements. It combines information from previous states and current measurements to generate an optimal estimate of the true state, while simultaneously minimizing the effects of noise and uncertainty. In the context of the indicator, the Kalman Filter is applied to smooth the input data, which is the source for the Rate of Change (ROC) calculation. By considering the previous smoothed state and the difference between the current measurement and the predicted value, the Kalman Filter dynamically adjusts its estimation to reduce the impact of outliers.

Calculation:

The indicator utilizes a combination of the ROC and the Stochastic indicator. The ROC is smoothed using a Kalman Filter (credit to © Loxx: ), which helps eliminate unwanted fluctuations and improve the signal quality. The Stochastic indicator is calculated with customizable parameters for %K length, %K smoothing, and %D smoothing. The smoothed ROC and Stochastic values are then averaged using the formula ((roc + d) / 2) to create the blended oscillator. MA smoothing is applied to the combined oscillator aiming to further reduce fluctuations and enhance trend visibility. Traders are free to choose their own preferred MA type from 'EMA', 'DEMA', 'TEMA', 'WMA', 'VWMA', 'SMA', 'SMMA', 'HMA', 'LSMA', and 'PEMA' (credit to: © traderharikrishna for this code: ).

Application:

The indicator's buy signals (represented by green "B" labels) indicate potential entry points for buying assets, suggesting a bullish trend. The white line visually represents the trend, helping traders identify and follow the upward momentum. Conversely, the sell signals (blue "S" labels) highlight possible exit points or opportunities for short selling, indicating a bearish trend. The blue line illustrates the bearish movement, aiding in the identification of downward momentum.

The "Smoothed ROC & Stochastic" indicator offers traders a comprehensive view of market trends by combining two powerful oscillators. By incorporating the ROC and Stochastic indicators into a single oscillator, it provides a more holistic perspective on the market's momentum. The use of a Kalman Filter for smoothing helps reduce noise and enhance the accuracy of the signals. Additionally, the indicator allows customization of the smoothing technique through various moving average types. Traders can also utilize the overbought and oversold zones for additional analysis, providing insights into potential market reversals or extreme price conditions. Please note that future performance of any trading strategy is fundamentally unknowable, and past results do not guarantee future performance.

[TTI] NDR 63-Day QQQ-QQEW ROC% SpreadWelcome to the NDR 63-Day QQQ-QQEW ROC% Spread script! This script is a powerful tool that calculates and visualizes the 63-day Rate of Change (ROC%) spread between the QQQ and QQEW tickers. This script is based on the research conducted by Ned Davis Research (NDR), a renowned name in the field of investment strategy.

⚙️ Key Features:

👉Rate of Change Calculation: The script calculates the 63-day Rate of Change (ROC%) for both QQQ and QQEW tickers. The ROC% is a momentum oscillator that measures the percentage price change over a given time period.

👉Spread Calculation: The script calculates the spread between the ROC% of QQQ and QQEW. This spread can be used to identify potential trading opportunities.

👉Visual Representation: The script plots the spread on the chart, providing a visual representation of the ROC% spread. This can help traders to easily identify trends and patterns.

👉Warning Lines: The script includes warning lines at +600 and -600 levels. These lines can be used as potential thresholds for trading decisions.

Usage:

To use this script, simply add it to your TradingView chart. The script will automatically calculate the ROC% for QQQ and QQEW and plot the spread on the chart. You can use this information to inform your trading decisions.

🚨 Disclaimer:

This script is provided for educational purposes only and is not intended as investment advice. Trading involves risk and is not suitable for all investors. Please consult with a financial advisor before making any investment decisions.

🎖️ Credits:

This script is based on the research conducted by Ned Davis Research (NDR). All credit for the underlying methodology and concept goes to NDR.