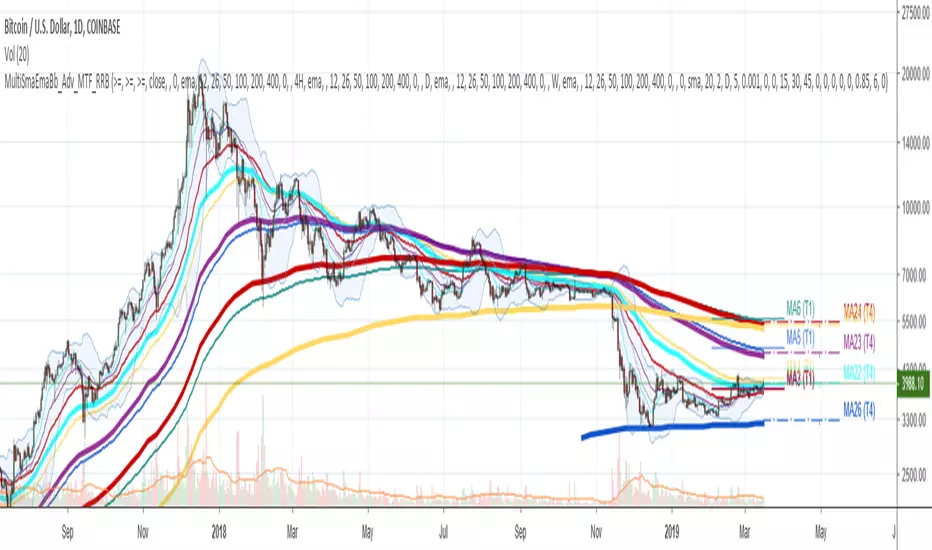

Multi SMA EMA WMA HMA BB (5x8 MAs Bollinger Bands) MAX MTF - RRBMulti SMA EMA WMA HMA 4x7 Moving Averages with Bollinger Bands MAX MTF by RagingRocketBull 2019

Version 1.0

All available MAX MTF versions are listed below (They are very similar and I don't want to publish them as separate indicators):

ver 1.0: 4x7 = 28 MTF MAs + 28 Levels + 3 BB = 59 < 64

ver 2.0: 5x6 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 3.0: 3x10 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 4.0: 5(4+1)x8 = 8 CurTF MAs + 32 MTF MAs + 20 Levels + 3 BB = 63 < 64

ver 5.0: 6(5+1)x6 = 6 CurTF MAs + 30 MTF MAs + 24 Levels + 3 BB = 63 < 64

ver 6.0: 4(3+1)x10 = 10 CurTF MAs + 30 MTF MAs + 20 Levels + 3 BB = 63 < 64

Fib numbers: 8, 13, 21, 34, 55, 89, 144, 233, 377

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group, a total of 4 TFs * 7 MAs = 28 MAs. You can assign any type/timeframe combo to a group, for example:

- EMAs 9,12,26,50,100,200,400 x H1, H4, D1, W1 (4 TFs x 7 MAs x 1 type)

- EMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 x M15, H1 (2 TFs x 14 MAs x 1 type)

- D1 EMAs and SMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 (1 TF x 14 MAs x 2 types)

- H1 WMAs 13,21,34,55,89,144,233; H4 HMAs 9,12,26,50,100,200,400; D1 EMAs 12,26,89,144,169,233,377; W1 SMAs 9,12,26,50,100,200,400 (4 TFs x 7 MAs x 4 types)

- +1 extra MA type/timeframe for BB

There are several versions: Simple, MTF, Pro MTF, Advanced MTF, MAX MTF and Ultimate MTF. This is the MAX MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF) +1 TF for BB, TF XY smoothing

- Pro MTF: 4 custom Timeframes for each group (4x3 MTF), 1 TF for BB, MA levels and show max bars back options

- Advanced MTF: +4 extra MAs/group (4x7 MTF), custom Ticker/Symbols, Timeframe <>= filter, Remove Duplicates Option

- MAX MTF: +2 subtypes/group, packed to the limit with max possible MAs/TFs: 4x7, 5x6, 3x10, 4(3+1)x10, 5(4+1)x8, 6(5+1)x6

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

MAX MTF version tests the limits of Pinescript trying to squeeze as many MAs/TFs as possible into a single indicator.

It's basically a maxed out Advanced version with subtypes allowing for mixed types within a group (i.e. both emas and smas in a single group/TF)

Pinescript has the following limits:

- max 40 security calls (6 calls are reserved for dupe checks and smoothing, 2 are used for BB, so only 32 calls are available)

- max 64 plot outputs (BB uses 3 outputs, so only 61 plot outputs are available)

- max 50000 (50kb) size of the compiled code

Based on those limits, you can only have the following MAs/TFs combos in a single script:

1. 4x7, 5x6, 3x10 - total number of MTF MAs must always be <= 32, and you can still have BB and Num Levels = total MAs, without any compromises

2. 5(4+1)x8, 6(5+1)x6, 4(3+1)x10 - you can use the Current Symbol/Timeframe as an extra (+1) fixed TF with the same number of MTF MAs

- you don't need to call security to display MAs on the Current Symbol/Timeframe, so the total number of MTF MAs remains the same and is still <= 32

- to fit that many MAs into the max 64 plot outputs limit you need to reduce the number of levels (not every MA Group will have corresponding levels)

Features:

- 4x7 = 28 MAs of any type

- 4x MTF groups with XY step line smoothing

- +1 extra TF/type for BB MAs

- 2 MA subtypes within each group/TF

- 4x7 = 28 MA levels with adjustable group offsets, indents and shift

- supports any existing type of MA: SMA, EMA, WMA, Hull Moving Average (HMA)

- custom tickers/symbols for each group

- show max bars back option

- show/hide both groups of MAs/levels/BB and individual MAs

- timeframe filter: show only MAs/Levels with TFs <>= Current TF

- hide MAs/Levels with duplicate TFs

- support for custom TFs that are not available in free accounts: 2D, 3D etc

- support for timeframes in H: H, 2H, 4H etc

Notes:

- Uses timeframe textbox instead of input resolution dropdown to allow for 240 120 and other custom TFs

- Uses symbol textbox instead of input symbol to avoid establishing multiple dummy security connections to the current ticker - otherwise empty symbols will prevent script from running

- Possible reasons for missing MAs on a chart:

- there may not be enough bars in history to start plotting it. For example, W1 EMA200 needs at least 200 bars on a weekly chart.

- for charts with low/fractional prices i.e. 0.00002 << 0.001 (default Y smoothing step) decrease Y smoothing as needed (set Y = 0.0000001) or disable it completely (set X,Y to 0,0)

- for charts with high price values i.e. 20000 >> 0.001 increase Y smoothing as needed (set Y = 10-20). Higher values exceeding MAs point density will cause it to disappear as there will be no points to plot. Different TFs may require diff adjustments

- TradingView Replay Mode UI and Pinescript security calls are limited to TFs >= D (D,2D,W,MN...) for free accounts

- attempting to plot any TF < D1 in Replay Mode will only result in straight lines, but all TFs will work properly in history and real-time modes. This is not a bug.

- Max Bars Back (num_bars) is limited to 5000 for free accounts (10000 for paid), will show error when exceeded. To plot on all available history set to 0 (default)

- Slow load/redraw times. This indicator becomes slower, its UI less responsive when:

- Pinescript Node.js graphics library is too slow and inefficient at plotting bars/objects in a browser window. Code optimization doesn't help much - the graphics engine is the main reason for general slowness.

- the chart has a long history (10000+ bars) in a browser's cache (you have scrolled back a couple of screens in a max zoom mode).

- Reload the page/Load a fresh chart and then apply the indicator or

- Switch to another Timeframe (old TF history will still remain in cache and that TF will be slow)

- in max possible zoom mode around 4500 bars can fit on 1 screen - this also slows down responsiveness. Reset Zoom level

- initial load and redraw times after a param change in UI also depend on TF. For example: D1/W1 - 2 sec, H1/H4 - 5-6 sec, M30 - 10 sec, M15/M5 - 4 sec, M1 - 5 sec. M30 usually has the longest history (up to 16000 bars) and W1 - the shortest (1000 bars).

- when indicator uses more MAs (plots) and timeframes it will redraw slower. Seems that up to 5 Timeframes is acceptable, but 6+ Timeframes can become very slow.

- show_last=last_bars plot limit doesn't affect load/redraw times, so it was removed from MA plot

- Max Bars Back (num_bars) default/custom set UI value doesn't seem to affect load/redraw times

- In max zoom mode all dynamic levels disappear (they behave like text)

- Dupe check includes symbol: symbol, tf, both subtypes - all must match for a duplicate group

- For the dupe check to work correctly a custom symbol must always include an exchange prefix. BB is not checked for dupes

Good Luck! Feel free to learn from/reuse the code to build your own indicators.

Recherche dans les scripts pour "12月4号是什么星座"

Multi SMA EMA WMA HMA BB (4x5 MAs Bollinger Bands) Adv MTF - RRBMulti SMA EMA WMA HMA 4x5 Moving Averages with Bollinger Bands Advanced MTF by RagingRocketBull 2019

Version 1.0

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group, a total of 4 TFs * 5 MAs = 20 MAs. You can assign any type/timeframe combo to a group, for example:

- EMAs 12,26,50,100,200 x H1, H4, D1, W1 (4 TFs x 5 MAs x 1 type)

- EMAs 8,10,13,21,30,50,55,100,200,400 x M15, H1 (2 TFs x 10 MAs x 1 type)

- D1 EMAs and SMAs 8,10,12,26,30,50,55,100,200,400 (1 TF x 10 MAs x 2 types)

- H1 WMAs 7,77,89,167,231; H4 HMAs 12,26,50,100,200; D1 EMAs 89,144,169,233,377; W1 SMAs 12,26,50,100,200 (4 TFs x 5 MAs x 4 types)

- +1 extra MA type/timeframe for BB

There are several versions: Simple, MTF, Pro MTF, Advanced MTF and Ultimate MTF. This is the Advanced MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF) +1 TF for BB, TF XY smoothing

- Pro MTF: 4 custom Timeframes for each group (4x3 MTF), 1 TF for BB, MA levels and show max bars back options

- Advanced MTF: +2 extra MAs/group (4x5 MTF), custom Ticker/Symbols, Timeframe <>= filter, Remove Duplicates Option

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

Features:

- 4x5 = 20 MAs of any type

- 4x MTF groups with XY step line smoothing

- +1 extra TF/type for BB MAs

- 4x5 = 20 MA levels with adjustable group offsets, indents and shift

- supports any existing type of MA: SMA, EMA, WMA, Hull Moving Average (HMA)

- custom tickers/symbols for each group - you can compare MAs of the same symbol across exchanges

- show max bars back option

- show/hide both groups of MAs/levels/BB and individual MAs

- timeframe filter: show only MAs/Levels with TFs <>= Current TF

- hide MAs/Levels with duplicate TFs

- support for custom TFs that are not available in free accounts: 2D, 3D etc

- support for timeframes in H: H, 2H, 4H etc

Notes:

- Uses timeframe textbox instead of input resolution dropdown to allow for 240 120 and other custom TFs

- Uses symbol textbox instead of input symbol to avoid establishing multiple dummy security connections to the current ticker - otherwise empty symbols will prevent script from running

- Possible reasons for missing MAs on a chart:

- there may not be enough bars in history to start plotting it. For example, W1 EMA200 needs at least 200 bars on a weekly chart.

- price << default Y smoothing step 5. For charts with low/fractional prices (i.e. 0.00002 << 5) adjust X Y smoothing as needed (set Y = 0.0000001) or disable it completely (set X,Y to 0,0)

- TradingView Replay Mode UI and Pinescript security calls are limited to TFs >= D (D,2D,W,MN...) for free accounts

- attempting to plot any TF < D1 in Replay Mode will only result in straight lines, but all TFs will work properly in history and real-time modes. This is not a bug.

- Max Bars Back (num_bars) is limited to 5000 for free accounts (10000 for paid), will show error when exceeded. To plot on all available history set to 0 (default)

- Slow load/redraw times. This indicator becomes slower, its UI less responsive when:

- Pinescript Node.js graphics library is too slow and inefficient at plotting bars/objects in a browser window. Code optimization doesn't help much - the graphics engine is the main reason for general slowness.

- the chart has a long history (10000+ bars) in a browser's cache (you have scrolled back a couple of screens in a max zoom mode).

- Reload the page/Load a fresh chart and then apply the indicator or

- Switch to another Timeframe (old TF history will still remain in cache and that TF will be slow)

- in max possible zoom mode around 4500 bars can fit on 1 screen - this also slows down responsiveness. Reset Zoom level

- initial load and redraw times after a param change in UI also depend on TF. For example:

D1/W1 - 2 sec, H1/H4 - 5-6 sec, M30 - 10 sec, M15/M5 - 4 sec, M1 - 5 sec.

M30 usually has the longest history (up to 16000 bars) and W1 - the shortest (1000 bars).

- when indicator uses more MAs (plots) and timeframes it will redraw slower. Seems that up to 5 Timeframes is acceptable, but 6+ Timeframes can become very slow.

- show_last=last_bars plot limit doesn't affect load/redraw times, so it was removed from MA plot

- Max Bars Back (num_bars) default/custom set UI value doesn't seem to affect load/redraw times

- In max zoom mode all dynamic levels disappear (they behave like text)

1. based on 3EmaBB, uses plot*, barssince and security functions

2. you can't set certain constants from input due to Pinescript limitations - change the code as needed, recompile and use as a private version

3. Levels = trackprice implementation

4. Show Max Bars Back = show_last implementation

5. swma has a fixed length = 4, alma and linreg have additional offset and smoothing params

6. Smoothing is applied by default for visual aesthetics on MTF. To use exact ma mtf values (lines with stair stepping) - disable it

Good Luck! You can explore, modify/reuse the code to build your own indicators.

ShiftPower StochasticThis indicator is a combination of the following three slow stochastics commonly used.

ⓐ 5 - 3 - 3

ⓑ 10 - 6 - 6

ⓒ 20 - 12 - 12

( n - %k - %d )

I hope it helps. Thanks.

<한국어>

일반적으로 많이 사용하는 다음 3개의 슬로우 스토케스틱을 하나로 합친 지표입니다.

ⓐ 5 - 3 - 3

ⓑ 10 - 6 - 6

ⓒ 20 - 12 - 12

( n - %k - %d )

도움이 됐으면 좋겠습니다. 감사합니다.

MACD Crossover Backtest MACD – Moving Average Convergence Divergence. The MACD is calculated

by subtracting a 26-day moving average of a security's price from a

12-day moving average of its price. The result is an indicator that

oscillates above and below zero. When the MACD is above zero, it means

the 12-day moving average is higher than the 26-day moving average.

This is bullish as it shows that current expectations (i.e., the 12-day

moving average) are more bullish than previous expectations (i.e., the

26-day average). This implies a bullish, or upward, shift in the supply/demand

lines. When the MACD falls below zero, it means that the 12-day moving average

is less than the 26-day moving average, implying a bearish shift in the

supply/demand lines.

A 9-day moving average of the MACD (not of the security's price) is usually

plotted on top of the MACD indicator. This line is referred to as the "signal"

line. The signal line anticipates the convergence of the two moving averages

(i.e., the movement of the MACD toward the zero line).

Let's consider the rational behind this technique. The MACD is the difference

between two moving averages of price. When the shorter-term moving average rises

above the longer-term moving average (i.e., the MACD rises above zero), it means

that investor expectations are becoming more bullish (i.e., there has been an

upward shift in the supply/demand lines). By plotting a 9-day moving average of

the MACD, we can see the changing of expectations (i.e., the shifting of the

supply/demand lines) as they occur.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Forex session - Opening Range- Jayy fixed updatedOpening Range (OR) for Forex 24 hour regular session. This is not for regular market day sessions addressed in a separate script.

This script fixes four issues:

syntax error when code compiles

messed up opening range the day after a holiday Monday

flaky plotting of the opening range and targets that required page reloading

TradingView problems with starting forex session at 1700 hours EST/EDT when using certain securities eg FX_IDC currently (Jan 2017)

Additions in his code are more options for trading range

Time compensation option for some securities that incorrectly start sessions at 1200 hrs instead of 1700 hrs NY time

- this glitch is likely temporary but present when this script update was created

More opening range time period choices

Opening Range Targets:

Opening Range Targets as per Leaf_West

Targets are set at 127% , 162%, 200 %, 262 %, 362%, 423%, 685%, 1109% and 1794% and this can be traded intraday using methods described here charts-by-leaf.com I also have some Leaf West PDFs that describe how the targets are set and how they are traded. There are others that use opening range.

The Time Session Glitch and the Fix:

The script will correctly default to 1700 hrs to 1700hrs EDT/EST session for FXCM.

Strangely some securities appear to erroneously start their session at 1200 hrs ie. My guess is that they are somehow tied to GMT+0 instead of New York time (GMT+5). See this for yourself by selecting EURUSD using the FXCM exchange (FX:EURUSD) and then EURUSD from the IDC exchange (FX_IDC:EURUSD). The FX-IDC session opening range starts 5 hours

before it actually should at 1700 hrs EDT/EST. To correct for this I have implemented an automatic fix (default) and a user selected "5 hour time shift adjust. ment needed on some securities".

There is also a 4 hour time shift button which might be necessary when New York reverts from Eastern Standard Time

to Eastern Daylight Time (1 hour difference) in March (and then back again in November). In the default auto adjust mode you will need to select the 1 hour time shift. That is if this glitch still exists at that time.

I have looked at other scripts, other than my own and where the script is available, that need to use information about the opening bar and all have the same time shift issue

What are the choices for Opening Range?

The dialogue box offers the standard TradingView options.

Also where you see Pick Opening Range 1 to 12 hours , SET TO 0 To USE LINE ABOVE TO DETERMINE OR LENGTH

As the note says a number other than 0 will override the standard options from the line above

The dialogue box below in offers choices by hours 1 to 12. A number greater than 12 will still only give

720 minutes (12 hours) for the length of Opening Range.

What sessions within the FOREX time-frame are available?

The default is 1700 hours to 1700 hours EST/EDT

Check any one (only one) of the time periods to change the opening range period to suit.

New York opens at 8:00 am to 5:00 pm EST (EDT)

Tokyo opens at 7:00 pm to 4:00 am EST (EDT)

Sydney opens at 5:00 pm to 2:00 am EST (EDT)

London opens at 3:00 am to 12:00 noon EST (EDT)

There is a build your own session (click the button to select)

The two lines for inputting session times are almost identical except that the second line starts the be the same as each other.

The default for the build your own session is 2200 hours to 2200 hours. As of the time of publishing this plots EURUSD FX-IDC just right. The GMT+5 and GMT+4 do not apply to this selection.

See my comments above on this strange aberration.

The script originated from work done by Chris Moody. It has changed significantly but there are remnants of that script lurking within.

Script is free to all - that way you can see what is inside

Cheers Jayy

MACD Crossover MACD – Moving Average Convergence Divergence. The MACD is calculated

by subtracting a 26-day moving average of a security's price from a

12-day moving average of its price. The result is an indicator that

oscillates above and below zero. When the MACD is above zero, it means

the 12-day moving average is higher than the 26-day moving average.

This is bullish as it shows that current expectations (i.e., the 12-day

moving average) are more bullish than previous expectations (i.e., the

26-day average). This implies a bullish, or upward, shift in the supply/demand

lines. When the MACD falls below zero, it means that the 12-day moving average

is less than the 26-day moving average, implying a bearish shift in the

supply/demand lines.

A 9-day moving average of the MACD (not of the security's price) is usually

plotted on top of the MACD indicator. This line is referred to as the "signal"

line. The signal line anticipates the convergence of the two moving averages

(i.e., the movement of the MACD toward the zero line).

Let's consider the rational behind this technique. The MACD is the difference

between two moving averages of price. When the shorter-term moving average rises

above the longer-term moving average (i.e., the MACD rises above zero), it means

that investor expectations are becoming more bullish (i.e., there has been an

upward shift in the supply/demand lines). By plotting a 9-day moving average of

the MACD, we can see the changing of expectations (i.e., the shifting of the

supply/demand lines) as they occur.

Dynamic Equity Allocation Model//@version=6

indicator('Dynamic Equity Allocation Model', shorttitle = 'DEAM', overlay = false, precision = 1, scale = scale.right, max_bars_back = 500)

// DYNAMIC EQUITY ALLOCATION MODEL

// Quantitative framework for dynamic portfolio allocation between stocks and cash.

// Analyzes five dimensions: market regime, risk metrics, valuation, sentiment,

// and macro conditions to generate allocation recommendations (0-100% equity).

//

// Uses real-time data from TradingView including fundamentals (P/E, ROE, ERP),

// volatility indicators (VIX), credit spreads, yield curves, and market structure.

// INPUT PARAMETERS

group1 = 'Model Configuration'

model_type = input.string('Adaptive', 'Allocation Model Type', options = , group = group1, tooltip = 'Conservative: Slower to increase equity, Aggressive: Faster allocation changes, Adaptive: Dynamic based on regime')

use_crisis_detection = input.bool(true, 'Enable Crisis Detection System', group = group1, tooltip = 'Automatic detection and response to crisis conditions')

use_regime_model = input.bool(true, 'Use Market Regime Detection', group = group1, tooltip = 'Identify Bull/Bear/Crisis regimes for dynamic allocation')

group2 = 'Portfolio Risk Management'

target_portfolio_volatility = input.float(12.0, 'Target Portfolio Volatility (%)', minval = 3, maxval = 20, step = 0.5, group = group2, tooltip = 'Target portfolio volatility (Cash reduces volatility: 50% Equity = ~10% vol, 100% Equity = ~20% vol)')

max_portfolio_drawdown = input.float(15.0, 'Maximum Portfolio Drawdown (%)', minval = 5, maxval = 35, step = 2.5, group = group2, tooltip = 'Maximum acceptable PORTFOLIO drawdown (not market drawdown - portfolio with cash has lower drawdown)')

enable_portfolio_risk_scaling = input.bool(true, 'Enable Portfolio Risk Scaling', group = group2, tooltip = 'Scale allocation based on actual portfolio risk characteristics (recommended)')

risk_lookback = input.int(252, 'Risk Calculation Period (Days)', minval = 60, maxval = 504, group = group2, tooltip = 'Period for calculating volatility and risk metrics')

group3 = 'Component Weights (Total = 100%)'

w_regime = input.float(35.0, 'Market Regime Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_risk = input.float(25.0, 'Risk Metrics Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_valuation = input.float(20.0, 'Valuation Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_sentiment = input.float(15.0, 'Sentiment Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_macro = input.float(5.0, 'Macro Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

group4 = 'Crisis Detection Thresholds'

crisis_vix_threshold = input.float(40, 'Crisis VIX Level', minval = 30, maxval = 80, group = group4, tooltip = 'VIX level indicating crisis conditions (COVID peaked at 82)')

crisis_drawdown_threshold = input.float(15, 'Crisis Drawdown Threshold (%)', minval = 10, maxval = 30, group = group4, tooltip = 'Market drawdown indicating crisis conditions')

crisis_credit_spread = input.float(500, 'Crisis Credit Spread (bps)', minval = 300, maxval = 1000, group = group4, tooltip = 'High yield spread indicating crisis conditions')

group5 = 'Display Settings'

show_components = input.bool(false, 'Show Component Breakdown', group = group5, tooltip = 'Display individual component analysis lines')

show_regime_background = input.bool(true, 'Show Dynamic Background', group = group5, tooltip = 'Color background based on allocation signals')

show_reference_lines = input.bool(false, 'Show Reference Lines', group = group5, tooltip = 'Display allocation percentage reference lines')

show_dashboard = input.bool(true, 'Show Analytics Dashboard', group = group5, tooltip = 'Display comprehensive analytics table')

show_confidence_bands = input.bool(false, 'Show Confidence Bands', group = group5, tooltip = 'Display uncertainty quantification bands')

smoothing_period = input.int(3, 'Smoothing Period', minval = 1, maxval = 10, group = group5, tooltip = 'Smoothing to reduce allocation noise')

background_intensity = input.int(95, 'Background Intensity (%)', minval = 90, maxval = 99, group = group5, tooltip = 'Higher values = more transparent background')

// Styling Options

color_scheme = input.string('EdgeTools', 'Color Theme', options = , group = 'Appearance', tooltip = 'Professional color themes')

use_dark_mode = input.bool(true, 'Optimize for Dark Theme', group = 'Appearance')

main_line_width = input.int(3, 'Main Line Width', minval = 1, maxval = 5, group = 'Appearance')

// DATA RETRIEVAL

// Market Data

sp500 = request.security('SPY', timeframe.period, close)

sp500_high = request.security('SPY', timeframe.period, high)

sp500_low = request.security('SPY', timeframe.period, low)

sp500_volume = request.security('SPY', timeframe.period, volume)

// Volatility Indicators

vix = request.security('VIX', timeframe.period, close)

vix9d = request.security('VIX9D', timeframe.period, close)

vxn = request.security('VXN', timeframe.period, close)

// Fixed Income and Credit

us2y = request.security('US02Y', timeframe.period, close)

us10y = request.security('US10Y', timeframe.period, close)

us3m = request.security('US03MY', timeframe.period, close)

hyg = request.security('HYG', timeframe.period, close)

lqd = request.security('LQD', timeframe.period, close)

tlt = request.security('TLT', timeframe.period, close)

// Safe Haven Assets

gold = request.security('GLD', timeframe.period, close)

usd = request.security('DXY', timeframe.period, close)

yen = request.security('JPYUSD', timeframe.period, close)

// Financial data with fallback values

get_financial_data(symbol, fin_id, period, fallback) =>

data = request.financial(symbol, fin_id, period, ignore_invalid_symbol = true)

na(data) ? fallback : data

// SPY fundamental metrics

spy_earnings_per_share = get_financial_data('AMEX:SPY', 'EARNINGS_PER_SHARE_BASIC', 'TTM', 20.0)

spy_operating_earnings_yield = get_financial_data('AMEX:SPY', 'OPERATING_EARNINGS_YIELD', 'FY', 4.5)

spy_dividend_yield = get_financial_data('AMEX:SPY', 'DIVIDENDS_YIELD', 'FY', 1.8)

spy_buyback_yield = get_financial_data('AMEX:SPY', 'BUYBACK_YIELD', 'FY', 2.0)

spy_net_margin = get_financial_data('AMEX:SPY', 'NET_MARGIN', 'TTM', 12.0)

spy_debt_to_equity = get_financial_data('AMEX:SPY', 'DEBT_TO_EQUITY', 'FY', 0.5)

spy_return_on_equity = get_financial_data('AMEX:SPY', 'RETURN_ON_EQUITY', 'FY', 15.0)

spy_free_cash_flow = get_financial_data('AMEX:SPY', 'FREE_CASH_FLOW', 'TTM', 100000000)

spy_ebitda = get_financial_data('AMEX:SPY', 'EBITDA', 'TTM', 200000000)

spy_pe_forward = get_financial_data('AMEX:SPY', 'PRICE_EARNINGS_FORWARD', 'FY', 18.0)

spy_total_debt = get_financial_data('AMEX:SPY', 'TOTAL_DEBT', 'FY', 500000000)

spy_total_equity = get_financial_data('AMEX:SPY', 'TOTAL_EQUITY', 'FY', 1000000000)

spy_enterprise_value = get_financial_data('AMEX:SPY', 'ENTERPRISE_VALUE', 'FY', 30000000000)

spy_revenue_growth = get_financial_data('AMEX:SPY', 'REVENUE_ONE_YEAR_GROWTH', 'TTM', 5.0)

// Market Breadth Indicators

nya = request.security('NYA', timeframe.period, close)

rut = request.security('IWM', timeframe.period, close)

// Sector Performance

xlk = request.security('XLK', timeframe.period, close)

xlu = request.security('XLU', timeframe.period, close)

xlf = request.security('XLF', timeframe.period, close)

// MARKET REGIME DETECTION

// Calculate Market Trend

sma_20 = ta.sma(sp500, 20)

sma_50 = ta.sma(sp500, 50)

sma_200 = ta.sma(sp500, 200)

ema_10 = ta.ema(sp500, 10)

// Market Structure Score

trend_strength = 0.0

trend_strength := trend_strength + (sp500 > sma_20 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_50 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_200 ? 2 : -2)

trend_strength := trend_strength + (sma_50 > sma_200 ? 2 : -2)

// Volatility Regime

returns = math.log(sp500 / sp500 )

realized_vol_20d = ta.stdev(returns, 20) * math.sqrt(252) * 100

realized_vol_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

ewma_vol = ta.ema(math.pow(returns, 2), 20)

realized_vol = math.sqrt(ewma_vol * 252) * 100

vol_premium = vix - realized_vol

// Drawdown Calculation

running_max = ta.highest(sp500, risk_lookback)

current_drawdown = (running_max - sp500) / running_max * 100

// Regime Score

regime_score = 0.0

// Trend Component (40%)

if trend_strength >= 4

regime_score := regime_score + 40

regime_score

else if trend_strength >= 2

regime_score := regime_score + 30

regime_score

else if trend_strength >= 0

regime_score := regime_score + 20

regime_score

else if trend_strength >= -2

regime_score := regime_score + 10

regime_score

else

regime_score := regime_score + 0

regime_score

// Volatility Component (30%)

if vix < 15

regime_score := regime_score + 30

regime_score

else if vix < 20

regime_score := regime_score + 25

regime_score

else if vix < 25

regime_score := regime_score + 15

regime_score

else if vix < 35

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Drawdown Component (30%)

if current_drawdown < 3

regime_score := regime_score + 30

regime_score

else if current_drawdown < 7

regime_score := regime_score + 20

regime_score

else if current_drawdown < 12

regime_score := regime_score + 10

regime_score

else if current_drawdown < 20

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Classify Regime

market_regime = regime_score >= 80 ? 'Strong Bull' : regime_score >= 60 ? 'Bull Market' : regime_score >= 40 ? 'Neutral' : regime_score >= 20 ? 'Correction' : regime_score >= 10 ? 'Bear Market' : 'Crisis'

// RISK-BASED ALLOCATION

// Calculate Market Risk

parkinson_hl = math.log(sp500_high / sp500_low)

parkinson_vol = parkinson_hl / (2 * math.sqrt(math.log(2))) * math.sqrt(252) * 100

garman_klass_vol = math.sqrt((0.5 * math.pow(math.log(sp500_high / sp500_low), 2) - (2 * math.log(2) - 1) * math.pow(math.log(sp500 / sp500 ), 2)) * 252) * 100

market_volatility_20d = math.max(ta.stdev(returns, 20) * math.sqrt(252) * 100, parkinson_vol)

market_volatility_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

market_drawdown = current_drawdown

// Initialize risk allocation

risk_allocation = 50.0

if enable_portfolio_risk_scaling

// Volatility-based allocation

vol_based_allocation = target_portfolio_volatility / math.max(market_volatility_20d, 5.0) * 100

vol_based_allocation := math.max(0, math.min(100, vol_based_allocation))

// Drawdown-based allocation

dd_based_allocation = 100.0

if market_drawdown > 1.0

dd_based_allocation := max_portfolio_drawdown / market_drawdown * 100

dd_based_allocation := math.max(0, math.min(100, dd_based_allocation))

dd_based_allocation

// Combine (conservative)

risk_allocation := math.min(vol_based_allocation, dd_based_allocation)

// Dynamic adjustment

current_equity_estimate = 50.0

estimated_portfolio_vol = current_equity_estimate / 100 * market_volatility_20d

estimated_portfolio_dd = current_equity_estimate / 100 * market_drawdown

vol_utilization = estimated_portfolio_vol / target_portfolio_volatility

dd_utilization = estimated_portfolio_dd / max_portfolio_drawdown

risk_utilization = math.max(vol_utilization, dd_utilization)

risk_adjustment_factor = 1.0

if risk_utilization > 1.0

risk_adjustment_factor := math.exp(-0.5 * (risk_utilization - 1.0))

risk_adjustment_factor := math.max(0.5, risk_adjustment_factor)

risk_adjustment_factor

else if risk_utilization < 0.9

risk_adjustment_factor := 1.0 + 0.2 * math.log(1.0 / risk_utilization)

risk_adjustment_factor := math.min(1.3, risk_adjustment_factor)

risk_adjustment_factor

risk_allocation := risk_allocation * risk_adjustment_factor

risk_allocation

else

vol_scalar = target_portfolio_volatility / math.max(market_volatility_20d, 10)

vol_scalar := math.min(1.5, math.max(0.2, vol_scalar))

drawdown_penalty = 0.0

if current_drawdown > max_portfolio_drawdown

drawdown_penalty := (current_drawdown - max_portfolio_drawdown) / max_portfolio_drawdown

drawdown_penalty := math.min(1.0, drawdown_penalty)

drawdown_penalty

risk_allocation := 100 * vol_scalar * (1 - drawdown_penalty)

risk_allocation

risk_allocation := math.max(0, math.min(100, risk_allocation))

// VALUATION ANALYSIS

// Valuation Metrics

actual_pe_ratio = spy_earnings_per_share > 0 ? sp500 / spy_earnings_per_share : spy_pe_forward

actual_earnings_yield = nz(spy_operating_earnings_yield, 0) > 0 ? spy_operating_earnings_yield : 100 / actual_pe_ratio

total_shareholder_yield = spy_dividend_yield + spy_buyback_yield

// Equity Risk Premium (multi-method calculation)

method1_erp = actual_earnings_yield - us10y

method2_erp = actual_earnings_yield + spy_buyback_yield - us10y

payout_ratio = spy_dividend_yield > 0 and actual_earnings_yield > 0 ? spy_dividend_yield / actual_earnings_yield : 0.4

sustainable_growth = spy_return_on_equity * (1 - payout_ratio) / 100

method3_erp = spy_dividend_yield + sustainable_growth * 100 - us10y

implied_growth = spy_revenue_growth * 0.7

method4_erp = total_shareholder_yield + implied_growth - us10y

equity_risk_premium = method1_erp * 0.35 + method2_erp * 0.30 + method3_erp * 0.20 + method4_erp * 0.15

ev_ebitda_ratio = spy_enterprise_value > 0 and spy_ebitda > 0 ? spy_enterprise_value / spy_ebitda : 15.0

debt_equity_health = spy_debt_to_equity < 1.0 ? 1.2 : spy_debt_to_equity < 2.0 ? 1.0 : 0.8

// Valuation Score

base_valuation_score = 50.0

if equity_risk_premium > 4

base_valuation_score := 95

base_valuation_score

else if equity_risk_premium > 3

base_valuation_score := 85

base_valuation_score

else if equity_risk_premium > 2

base_valuation_score := 70

base_valuation_score

else if equity_risk_premium > 1

base_valuation_score := 55

base_valuation_score

else if equity_risk_premium > 0

base_valuation_score := 40

base_valuation_score

else if equity_risk_premium > -1

base_valuation_score := 25

base_valuation_score

else

base_valuation_score := 10

base_valuation_score

growth_adjustment = spy_revenue_growth > 10 ? 10 : spy_revenue_growth > 5 ? 5 : 0

margin_adjustment = spy_net_margin > 15 ? 5 : spy_net_margin < 8 ? -5 : 0

roe_adjustment = spy_return_on_equity > 20 ? 5 : spy_return_on_equity < 10 ? -5 : 0

valuation_score = base_valuation_score + growth_adjustment + margin_adjustment + roe_adjustment

valuation_score := math.max(0, math.min(100, valuation_score * debt_equity_health))

// SENTIMENT ANALYSIS

// VIX Term Structure

vix_term_structure = vix9d > 0 ? vix / vix9d : 1

backwardation = vix_term_structure > 1.05

steep_backwardation = vix_term_structure > 1.15

// Safe Haven Flows

gold_momentum = ta.roc(gold, 20)

dollar_momentum = ta.roc(usd, 20)

yen_momentum = ta.roc(yen, 20)

treasury_momentum = ta.roc(tlt, 20)

safe_haven_flow = gold_momentum * 0.3 + treasury_momentum * 0.3 + dollar_momentum * 0.25 + yen_momentum * 0.15

// Advanced Sentiment Analysis

vix_percentile = ta.percentrank(vix, 252)

vix_zscore = (vix - ta.sma(vix, 252)) / ta.stdev(vix, 252)

vix_momentum = ta.roc(vix, 5)

vvix_proxy = ta.stdev(vix_momentum, 20) * math.sqrt(252)

risk_reversal_proxy = (vix - realized_vol) / realized_vol

// Sentiment Score

base_sentiment = 50.0

vix_adjustment = 0.0

if vix_zscore < -1.5

vix_adjustment := 40

vix_adjustment

else if vix_zscore < -0.5

vix_adjustment := 20

vix_adjustment

else if vix_zscore < 0.5

vix_adjustment := 0

vix_adjustment

else if vix_zscore < 1.5

vix_adjustment := -20

vix_adjustment

else

vix_adjustment := -40

vix_adjustment

term_structure_adjustment = backwardation ? -15 : steep_backwardation ? -30 : 5

vvix_adjustment = vvix_proxy > 2.0 ? -10 : vvix_proxy < 1.0 ? 10 : 0

sentiment_score = base_sentiment + vix_adjustment + term_structure_adjustment + vvix_adjustment

sentiment_score := math.max(0, math.min(100, sentiment_score))

// MACRO ANALYSIS

// Yield Curve

yield_spread_2_10 = us10y - us2y

yield_spread_3m_10 = us10y - us3m

// Credit Conditions

hyg_return = ta.roc(hyg, 20)

lqd_return = ta.roc(lqd, 20)

tlt_return = ta.roc(tlt, 20)

hyg_duration = 4.0

lqd_duration = 8.0

tlt_duration = 17.0

hyg_log_returns = math.log(hyg / hyg )

lqd_log_returns = math.log(lqd / lqd )

hyg_volatility = ta.stdev(hyg_log_returns, 20) * math.sqrt(252)

lqd_volatility = ta.stdev(lqd_log_returns, 20) * math.sqrt(252)

hyg_yield_proxy = -math.log(hyg / hyg ) * 100

lqd_yield_proxy = -math.log(lqd / lqd ) * 100

tlt_yield = us10y

hyg_spread = (hyg_yield_proxy - tlt_yield) * 100

lqd_spread = (lqd_yield_proxy - tlt_yield) * 100

hyg_distance = (hyg - ta.lowest(hyg, 252)) / (ta.highest(hyg, 252) - ta.lowest(hyg, 252))

lqd_distance = (lqd - ta.lowest(lqd, 252)) / (ta.highest(lqd, 252) - ta.lowest(lqd, 252))

default_risk_proxy = 2.0 - (hyg_distance + lqd_distance)

credit_spread = hyg_spread * 0.5 + (hyg_volatility - lqd_volatility) * 1000 * 0.3 + default_risk_proxy * 200 * 0.2

credit_spread := math.max(50, credit_spread)

credit_market_health = hyg_return > lqd_return ? 1 : -1

flight_to_quality = tlt_return > (hyg_return + lqd_return) / 2

// Macro Score

macro_score = 50.0

yield_curve_score = 0

if yield_spread_2_10 > 1.5 and yield_spread_3m_10 > 2

yield_curve_score := 40

yield_curve_score

else if yield_spread_2_10 > 0.5 and yield_spread_3m_10 > 1

yield_curve_score := 30

yield_curve_score

else if yield_spread_2_10 > 0 and yield_spread_3m_10 > 0

yield_curve_score := 20

yield_curve_score

else if yield_spread_2_10 < 0 or yield_spread_3m_10 < 0

yield_curve_score := 10

yield_curve_score

else

yield_curve_score := 5

yield_curve_score

credit_conditions_score = 0

if credit_spread < 200 and not flight_to_quality

credit_conditions_score := 30

credit_conditions_score

else if credit_spread < 400 and credit_market_health > 0

credit_conditions_score := 20

credit_conditions_score

else if credit_spread < 600

credit_conditions_score := 15

credit_conditions_score

else if credit_spread < 1000

credit_conditions_score := 10

credit_conditions_score

else

credit_conditions_score := 0

credit_conditions_score

financial_stability_score = 0

if spy_debt_to_equity < 0.5 and spy_return_on_equity > 15

financial_stability_score := 20

financial_stability_score

else if spy_debt_to_equity < 1.0 and spy_return_on_equity > 10

financial_stability_score := 15

financial_stability_score

else if spy_debt_to_equity < 1.5

financial_stability_score := 10

financial_stability_score

else

financial_stability_score := 5

financial_stability_score

macro_score := yield_curve_score + credit_conditions_score + financial_stability_score

macro_score := math.max(0, math.min(100, macro_score))

// CRISIS DETECTION

crisis_indicators = 0

if vix > crisis_vix_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if vix > 60

crisis_indicators := crisis_indicators + 2

crisis_indicators

if current_drawdown > crisis_drawdown_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if current_drawdown > 25

crisis_indicators := crisis_indicators + 1

crisis_indicators

if credit_spread > crisis_credit_spread

crisis_indicators := crisis_indicators + 1

crisis_indicators

sp500_roc_5 = ta.roc(sp500, 5)

tlt_roc_5 = ta.roc(tlt, 5)

if sp500_roc_5 < -10 and tlt_roc_5 < -5

crisis_indicators := crisis_indicators + 2

crisis_indicators

volume_spike = sp500_volume > ta.sma(sp500_volume, 20) * 2

sp500_roc_1 = ta.roc(sp500, 1)

if volume_spike and sp500_roc_1 < -3

crisis_indicators := crisis_indicators + 1

crisis_indicators

is_crisis = crisis_indicators >= 3

is_severe_crisis = crisis_indicators >= 5

// FINAL ALLOCATION CALCULATION

// Convert regime to base allocation

regime_allocation = market_regime == 'Strong Bull' ? 100 : market_regime == 'Bull Market' ? 80 : market_regime == 'Neutral' ? 60 : market_regime == 'Correction' ? 40 : market_regime == 'Bear Market' ? 20 : 0

// Normalize weights

total_weight = w_regime + w_risk + w_valuation + w_sentiment + w_macro

w_regime_norm = w_regime / total_weight

w_risk_norm = w_risk / total_weight

w_valuation_norm = w_valuation / total_weight

w_sentiment_norm = w_sentiment / total_weight

w_macro_norm = w_macro / total_weight

// Calculate Weighted Allocation

weighted_allocation = regime_allocation * w_regime_norm + risk_allocation * w_risk_norm + valuation_score * w_valuation_norm + sentiment_score * w_sentiment_norm + macro_score * w_macro_norm

// Apply Crisis Override

if use_crisis_detection

if is_severe_crisis

weighted_allocation := math.min(weighted_allocation, 10)

weighted_allocation

else if is_crisis

weighted_allocation := math.min(weighted_allocation, 25)

weighted_allocation

// Model Type Adjustment

model_adjustment = 0.0

if model_type == 'Conservative'

model_adjustment := -10

model_adjustment

else if model_type == 'Aggressive'

model_adjustment := 10

model_adjustment

else if model_type == 'Adaptive'

recent_return = (sp500 - sp500 ) / sp500 * 100

if recent_return > 5

model_adjustment := 5

model_adjustment

else if recent_return < -5

model_adjustment := -5

model_adjustment

// Apply adjustment and bounds

final_allocation = weighted_allocation + model_adjustment

final_allocation := math.max(0, math.min(100, final_allocation))

// Smooth allocation

smoothed_allocation = ta.sma(final_allocation, smoothing_period)

// Calculate portfolio risk metrics (only for internal alerts)

actual_portfolio_volatility = smoothed_allocation / 100 * market_volatility_20d

actual_portfolio_drawdown = smoothed_allocation / 100 * current_drawdown

// VISUALIZATION

// Color definitions

var color primary_color = #2196F3

var color bullish_color = #4CAF50

var color bearish_color = #FF5252

var color neutral_color = #808080

var color text_color = color.white

var color bg_color = #000000

var color table_bg_color = #1E1E1E

var color header_bg_color = #2D2D2D

switch color_scheme // Apply color scheme

'Gold' =>

primary_color := use_dark_mode ? #FFD700 : #DAA520

bullish_color := use_dark_mode ? #FFA500 : #FF8C00

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #C0C0C0 : #808080

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A00 : #FFFEF0

header_bg_color := use_dark_mode ? #2D2600 : #F5F5DC

header_bg_color

'EdgeTools' =>

primary_color := use_dark_mode ? #4682B4 : #1E90FF

bullish_color := use_dark_mode ? #4CAF50 : #388E3C

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #708090 : #696969

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0F1419 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A3A : #E6F3FF

header_bg_color

'Behavioral' =>

primary_color := #808080

bullish_color := #00FF00

bearish_color := #8B0000

neutral_color := #FFBF00

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A1A : #F8F8F8

header_bg_color := use_dark_mode ? #2D2D2D : #E8E8E8

header_bg_color

'Quant' =>

primary_color := #808080

bullish_color := #FFA500

bearish_color := #8B0000

neutral_color := #4682B4

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0D0D0D : #FAFAFA

header_bg_color := use_dark_mode ? #1A1A1A : #F0F0F0

header_bg_color

'Ocean' =>

primary_color := use_dark_mode ? #20B2AA : #008B8B

bullish_color := use_dark_mode ? #00CED1 : #4682B4

bearish_color := use_dark_mode ? #FF4500 : #B22222

neutral_color := use_dark_mode ? #87CEEB : #2F4F4F

text_color := use_dark_mode ? #F0F8FF : #191970

bg_color := use_dark_mode ? #001F3F : #F0F8FF

table_bg_color := use_dark_mode ? #001A2E : #E6F7FF

header_bg_color := use_dark_mode ? #002A47 : #CCF2FF

header_bg_color

'Fire' =>

primary_color := use_dark_mode ? #FF6347 : #DC143C

bullish_color := use_dark_mode ? #FFD700 : #FF8C00

bearish_color := use_dark_mode ? #8B0000 : #800000

neutral_color := use_dark_mode ? #FFA500 : #CD853F

text_color := use_dark_mode ? #FFFAF0 : #2F1B14

bg_color := use_dark_mode ? #2F1B14 : #FFFAF0

table_bg_color := use_dark_mode ? #261611 : #FFF8F0

header_bg_color := use_dark_mode ? #3D241A : #FFE4CC

header_bg_color

'Matrix' =>

primary_color := use_dark_mode ? #00FF41 : #006400

bullish_color := use_dark_mode ? #39FF14 : #228B22

bearish_color := use_dark_mode ? #FF073A : #8B0000

neutral_color := use_dark_mode ? #00FFFF : #008B8B

text_color := use_dark_mode ? #C0FF8C : #003300

bg_color := use_dark_mode ? #0D1B0D : #F0FFF0

table_bg_color := use_dark_mode ? #0A1A0A : #E8FFF0

header_bg_color := use_dark_mode ? #112B11 : #CCFFCC

header_bg_color

'Arctic' =>

primary_color := use_dark_mode ? #87CEFA : #4169E1

bullish_color := use_dark_mode ? #00BFFF : #0000CD

bearish_color := use_dark_mode ? #FF1493 : #8B008B

neutral_color := use_dark_mode ? #B0E0E6 : #483D8B

text_color := use_dark_mode ? #F8F8FF : #191970

bg_color := use_dark_mode ? #191970 : #F8F8FF

table_bg_color := use_dark_mode ? #141B47 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A5C : #E0F0FF

header_bg_color

// Transparency settings

bg_transparency = use_dark_mode ? 85 : 92

zone_transparency = use_dark_mode ? 90 : 95

band_transparency = use_dark_mode ? 70 : 85

table_transparency = use_dark_mode ? 80 : 15

// Allocation color

alloc_color = smoothed_allocation >= 80 ? bullish_color : smoothed_allocation >= 60 ? color.new(bullish_color, 30) : smoothed_allocation >= 40 ? primary_color : smoothed_allocation >= 20 ? color.new(bearish_color, 30) : bearish_color

// Dynamic background

var color dynamic_bg_color = na

if show_regime_background

if smoothed_allocation >= 70

dynamic_bg_color := color.new(bullish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation <= 30

dynamic_bg_color := color.new(bearish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation > 60 or smoothed_allocation < 40

dynamic_bg_color := color.new(primary_color, math.min(99, background_intensity + 2))

dynamic_bg_color

bgcolor(dynamic_bg_color, title = 'Allocation Signal Background')

// Plot main allocation line

plot(smoothed_allocation, 'Equity Allocation %', color = alloc_color, linewidth = math.max(1, main_line_width))

// Reference lines (static colors for hline)

hline_bullish_color = color_scheme == 'Gold' ? use_dark_mode ? #FFA500 : #FF8C00 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4CAF50 : #388E3C : color_scheme == 'Behavioral' ? #00FF00 : color_scheme == 'Quant' ? #FFA500 : color_scheme == 'Ocean' ? use_dark_mode ? #00CED1 : #4682B4 : color_scheme == 'Fire' ? use_dark_mode ? #FFD700 : #FF8C00 : color_scheme == 'Matrix' ? use_dark_mode ? #39FF14 : #228B22 : color_scheme == 'Arctic' ? use_dark_mode ? #00BFFF : #0000CD : #4CAF50

hline_bearish_color = color_scheme == 'Gold' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'EdgeTools' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'Behavioral' ? #8B0000 : color_scheme == 'Quant' ? #8B0000 : color_scheme == 'Ocean' ? use_dark_mode ? #FF4500 : #B22222 : color_scheme == 'Fire' ? use_dark_mode ? #8B0000 : #800000 : color_scheme == 'Matrix' ? use_dark_mode ? #FF073A : #8B0000 : color_scheme == 'Arctic' ? use_dark_mode ? #FF1493 : #8B008B : #FF5252

hline_primary_color = color_scheme == 'Gold' ? use_dark_mode ? #FFD700 : #DAA520 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4682B4 : #1E90FF : color_scheme == 'Behavioral' ? #808080 : color_scheme == 'Quant' ? #808080 : color_scheme == 'Ocean' ? use_dark_mode ? #20B2AA : #008B8B : color_scheme == 'Fire' ? use_dark_mode ? #FF6347 : #DC143C : color_scheme == 'Matrix' ? use_dark_mode ? #00FF41 : #006400 : color_scheme == 'Arctic' ? use_dark_mode ? #87CEFA : #4169E1 : #2196F3

hline(show_reference_lines ? 100 : na, '100% Equity', color = color.new(hline_bullish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 80 : na, '80% Equity', color = color.new(hline_bullish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 60 : na, '60% Equity', color = color.new(hline_bullish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(50, '50% Balanced', color = color.new(hline_primary_color, 50), linestyle = hline.style_solid, linewidth = 2)

hline(show_reference_lines ? 40 : na, '40% Equity', color = color.new(hline_bearish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 20 : na, '20% Equity', color = color.new(hline_bearish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 0 : na, '0% Equity', color = color.new(hline_bearish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

// Component plots

plot(show_components ? regime_allocation : na, 'Regime', color = color.new(#4ECDC4, 70), linewidth = 1)

plot(show_components ? risk_allocation : na, 'Risk', color = color.new(#FF6B6B, 70), linewidth = 1)

plot(show_components ? valuation_score : na, 'Valuation', color = color.new(#45B7D1, 70), linewidth = 1)

plot(show_components ? sentiment_score : na, 'Sentiment', color = color.new(#FFD93D, 70), linewidth = 1)

plot(show_components ? macro_score : na, 'Macro', color = color.new(#6BCF7F, 70), linewidth = 1)

// Confidence bands

upper_band = plot(show_confidence_bands ? math.min(100, smoothed_allocation + ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Upper Band')

lower_band = plot(show_confidence_bands ? math.max(0, smoothed_allocation - ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Lower Band')

fill(upper_band, lower_band, color = show_confidence_bands ? color.new(neutral_color, zone_transparency) : na, title = 'Uncertainty')

// DASHBOARD

if show_dashboard and barstate.islast

var table dashboard = table.new(position.top_right, 2, 20, border_width = 1, bgcolor = color.new(table_bg_color, table_transparency))

table.clear(dashboard, 0, 0, 1, 19)

// Header

header_color = color.new(header_bg_color, 20)

dashboard_text_color = text_color

table.cell(dashboard, 0, 0, 'DEAM', text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

table.cell(dashboard, 1, 0, model_type, text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

// Core metrics

table.cell(dashboard, 0, 1, 'Equity Allocation', text_color = dashboard_text_color, text_size = size.small)

table.cell(dashboard, 1, 1, str.tostring(smoothed_allocation, '##.#') + '%', text_color = alloc_color, text_size = size.small)

table.cell(dashboard, 0, 2, 'Cash Allocation', text_color = dashboard_text_color, text_size = size.small)

cash_color = 100 - smoothed_allocation > 70 ? bearish_color : primary_color

table.cell(dashboard, 1, 2, str.tostring(100 - smoothed_allocation, '##.#') + '%', text_color = cash_color, text_size = size.small)

// Signal

signal_text = 'NEUTRAL'

signal_color = primary_color

if smoothed_allocation >= 70

signal_text := 'BULLISH'

signal_color := bullish_color

signal_color

else if smoothed_allocation <= 30

signal_text := 'BEARISH'

signal_color := bearish_color

signal_color

table.cell(dashboard, 0, 3, 'Signal', text_color = dashboard_text_color, text_size = size.small)

table.cell(dashboard, 1, 3, signal_text, text_color = signal_color, text_size = size.small)

// Market Regime

table.cell(dashboard, 0, 4, 'Regime', text_color = dashboard_text_color, text_size = size.small)

regime_color_display = market_regime == 'Strong Bull' or market_regime == 'Bull Market' ? bullish_color : market_regime == 'Neutral' ? primary_color : market_regime == 'Crisis' ? bearish_color : bearish_color

table.cell(dashboard, 1, 4, market_regime, text_color = regime_color_display, text_size = size.small)

// VIX

table.cell(dashboard, 0, 5, 'VIX Level', text_color = dashboard_text_color, text_size = size.small)

vix_color_display = vix < 20 ? bullish_color : vix < 30 ? primary_color : bearish_color

table.cell(dashboard, 1, 5, str.tostring(vix, '##.##'), text_color = vix_color_display, text_size = size.small)

// Market Drawdown

table.cell(dashboard, 0, 6, 'Market DD', text_color = dashboard_text_color, text_size = size.small)

market_dd_color = current_drawdown < 5 ? bullish_color : current_drawdown < 10 ? primary_color : bearish_color

table.cell(dashboard, 1, 6, '-' + str.tostring(current_drawdown, '##.#') + '%', text_color = market_dd_color, text_size = size.small)

// Crisis Detection

table.cell(dashboard, 0, 7, 'Crisis Detection', text_color = dashboard_text_color, text_size = size.small)

crisis_text = is_severe_crisis ? 'SEVERE' : is_crisis ? 'CRISIS' : 'Normal'

crisis_display_color = is_severe_crisis or is_crisis ? bearish_color : bullish_color

table.cell(dashboard, 1, 7, crisis_text, text_color = crisis_display_color, text_size = size.small)

// Real Data Section

financial_bg = color.new(primary_color, 85)

table.cell(dashboard, 0, 8, 'REAL DATA', text_color = dashboard_text_color, bgcolor = financial_bg, text_size = size.small)

table.cell(dashboard, 1, 8, 'Live Metrics', text_color = dashboard_text_color, bgcolor = financial_bg, text_size = size.small)

// P/E Ratio

table.cell(dashboard, 0, 9, 'P/E Ratio', text_color = dashboard_text_color, text_size = size.small)

pe_color = actual_pe_ratio < 18 ? bullish_color : actual_pe_ratio < 25 ? primary_color : bearish_color

table.cell(dashboard, 1, 9, str.tostring(actual_pe_ratio, '##.#'), text_color = pe_color, text_size = size.small)

// ERP

table.cell(dashboard, 0, 10, 'ERP', text_color = dashboard_text_color, text_size = size.small)

erp_color = equity_risk_premium > 2 ? bullish_color : equity_risk_premium > 0 ? primary_color : bearish_color

table.cell(dashboard, 1, 10, str.tostring(equity_risk_premium, '##.##') + '%', text_color = erp_color, text_size = size.small)

// ROE

table.cell(dashboard, 0, 11, 'ROE', text_color = dashboard_text_color, text_size = size.small)

roe_color = spy_return_on_equity > 20 ? bullish_color : spy_return_on_equity > 10 ? primary_color : bearish_color

table.cell(dashboard, 1, 11, str.tostring(spy_return_on_equity, '##.#') + '%', text_color = roe_color, text_size = size.small)

// D/E Ratio

table.cell(dashboard, 0, 12, 'D/E Ratio', text_color = dashboard_text_color, text_size = size.small)

de_color = spy_debt_to_equity < 0.5 ? bullish_color : spy_debt_to_equity < 1.0 ? primary_color : bearish_color

table.cell(dashboard, 1, 12, str.tostring(spy_debt_to_equity, '##.##'), text_color = de_color, text_size = size.small)

// Shareholder Yield

table.cell(dashboard, 0, 13, 'Dividend+Buyback', text_color = dashboard_text_color, text_size = size.small)

yield_color = total_shareholder_yield > 4 ? bullish_color : total_shareholder_yield > 2 ? primary_color : bearish_color

table.cell(dashboard, 1, 13, str.tostring(total_shareholder_yield, '##.#') + '%', text_color = yield_color, text_size = size.small)

// Component Scores

component_bg = color.new(neutral_color, 80)

table.cell(dashboard, 0, 14, 'Components', text_color = dashboard_text_color, bgcolor = component_bg, text_size = size.small)

table.cell(dashboard, 1, 14, 'Scores', text_color = dashboard_text_color, bgcolor = component_bg, text_size = size.small)

table.cell(dashboard, 0, 15, 'Regime', text_color = dashboard_text_color, text_size = size.small)

regime_score_color = regime_allocation > 60 ? bullish_color : regime_allocation < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 15, str.tostring(regime_allocation, '##'), text_color = regime_score_color, text_size = size.small)

table.cell(dashboard, 0, 16, 'Risk', text_color = dashboard_text_color, text_size = size.small)

risk_score_color = risk_allocation > 60 ? bullish_color : risk_allocation < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 16, str.tostring(risk_allocation, '##'), text_color = risk_score_color, text_size = size.small)

table.cell(dashboard, 0, 17, 'Valuation', text_color = dashboard_text_color, text_size = size.small)

val_score_color = valuation_score > 60 ? bullish_color : valuation_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 17, str.tostring(valuation_score, '##'), text_color = val_score_color, text_size = size.small)

table.cell(dashboard, 0, 18, 'Sentiment', text_color = dashboard_text_color, text_size = size.small)

sent_score_color = sentiment_score > 60 ? bullish_color : sentiment_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 18, str.tostring(sentiment_score, '##'), text_color = sent_score_color, text_size = size.small)

table.cell(dashboard, 0, 19, 'Macro', text_color = dashboard_text_color, text_size = size.small)

macro_score_color = macro_score > 60 ? bullish_color : macro_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 19, str.tostring(macro_score, '##'), text_color = macro_score_color, text_size = size.small)

// ALERTS

// Major allocation changes

alertcondition(smoothed_allocation >= 80 and smoothed_allocation < 80, 'High Equity Allocation', 'Equity allocation reached 80% - Bull market conditions')

alertcondition(smoothed_allocation <= 20 and smoothed_allocation > 20, 'Low Equity Allocation', 'Equity allocation dropped to 20% - Defensive positioning')

// Crisis alerts

alertcondition(is_crisis and not is_crisis , 'CRISIS DETECTED', 'Crisis conditions detected - Reducing equity allocation')

alertcondition(is_severe_crisis and not is_severe_crisis , 'SEVERE CRISIS', 'Severe crisis detected - Maximum defensive positioning')

// Regime changes

regime_changed = market_regime != market_regime

alertcondition(regime_changed, 'Regime Change', 'Market regime has changed')

// Risk management alerts

risk_breach = enable_portfolio_risk_scaling and (actual_portfolio_volatility > target_portfolio_volatility * 1.2 or actual_portfolio_drawdown > max_portfolio_drawdown * 1.2)

alertcondition(risk_breach, 'Risk Breach', 'Portfolio risk exceeds target parameters')

// USAGE

// The indicator displays a recommended equity allocation percentage (0-100%).

// Example: 75% allocation = 75% stocks, 25% cash/bonds.

//

// The model combines market regime analysis (trend, volatility, drawdowns),

// risk management (portfolio-level targeting), valuation metrics (P/E, ERP),

// sentiment indicators (VIX term structure), and macro factors (yield curve,

// credit spreads) into a single allocation signal.

//

// Crisis detection automatically reduces exposure when multiple warning signals

// converge. Alerts available for major allocation shifts and regime changes.

//

// Designed for SPY/S&P 500 portfolio allocation. Adjust component weights and

// risk parameters in settings to match your risk tolerance.

View in Pine

Kripto Fema ind/ This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © Femayakup

//@version=5

indicator(title = "Kripto Fema ind", shorttitle="Kripto Fema ind", overlay=true, format=format.price, precision=2,max_lines_count = 500, max_labels_count = 500, max_bars_back=500)

showEma200 = input(true, title="EMA 200")

showPmax = input(true, title="Pmax")

showLinreg = input(true, title="Linreg")

showMavilim = input(true, title="Mavilim")

showNadaray = input(true, title="Nadaraya Watson")

ma(source, length, type) =>

switch type

"SMA" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

"SMMA (RMA)" => ta.rma(source, length)

"WMA" => ta.wma(source, length)

"VWMA" => ta.vwma(source, length)

//Ema200

timeFrame = input.timeframe(defval = '240',title= 'EMA200 TimeFrame',group = 'EMA200 Settings')

len200 = input.int(200, minval=1, title="Length",group = 'EMA200 Settings')

src200 = input(close, title="Source",group = 'EMA200 Settings')

offset200 = input.int(title="Offset", defval=0, minval=-500, maxval=500,group = 'EMA200 Settings')

out200 = ta.ema(src200, len200)

higherTimeFrame = request.security(syminfo.tickerid,timeFrame,out200 ,barmerge.gaps_on,barmerge.lookahead_on)

ema200Plot = showEma200 ? higherTimeFrame : na

plot(ema200Plot, title="EMA200", offset=offset200)

//Linreq

group1 = "Linreg Settings"

lengthInput = input.int(100, title="Length", minval = 1, maxval = 5000,group = group1)

sourceInput = input.source(close, title="Source")

useUpperDevInput = input.bool(true, title="Upper Deviation", inline = "Upper Deviation", group = group1)

upperMultInput = input.float(2.0, title="", inline = "Upper Deviation", group = group1)

useLowerDevInput = input.bool(true, title="Lower Deviation", inline = "Lower Deviation", group = group1)

lowerMultInput = input.float(2.0, title="", inline = "Lower Deviation", group = group1)

group2 = "Linreg Display Settings"

showPearsonInput = input.bool(true, "Show Pearson's R", group = group2)

extendLeftInput = input.bool(false, "Extend Lines Left", group = group2)

extendRightInput = input.bool(true, "Extend Lines Right", group = group2)

extendStyle = switch

extendLeftInput and extendRightInput => extend.both

extendLeftInput => extend.left

extendRightInput => extend.right

=> extend.none

group3 = "Linreg Color Settings"

colorUpper = input.color(color.new(color.blue, 85), "Linreg Renk", inline = group3, group = group3)

colorLower = input.color(color.new(color.red, 85), "", inline = group3, group = group3)

calcSlope(source, length) =>

max_bars_back(source, 5000)

if not barstate.islast or length <= 1

else

sumX = 0.0

sumY = 0.0

sumXSqr = 0.0

sumXY = 0.0

for i = 0 to length - 1 by 1

val = source

per = i + 1.0

sumX += per

sumY += val

sumXSqr += per * per

sumXY += val * per

slope = (length * sumXY - sumX * sumY) / (length * sumXSqr - sumX * sumX)

average = sumY / length

intercept = average - slope * sumX / length + slope

= calcSlope(sourceInput, lengthInput)

startPrice = i + s * (lengthInput - 1)

endPrice = i

var line baseLine = na

if na(baseLine) and not na(startPrice) and showLinreg

baseLine := line.new(bar_index - lengthInput + 1, startPrice, bar_index, endPrice, width=1, extend=extendStyle, color=color.new(colorLower, 0))

else

line.set_xy1(baseLine, bar_index - lengthInput + 1, startPrice)

line.set_xy2(baseLine, bar_index, endPrice)

na

calcDev(source, length, slope, average, intercept) =>

upDev = 0.0

dnDev = 0.0

stdDevAcc = 0.0

dsxx = 0.0

dsyy = 0.0

dsxy = 0.0

periods = length - 1

daY = intercept + slope * periods / 2

val = intercept

for j = 0 to periods by 1

price = high - val

if price > upDev

upDev := price

price := val - low

if price > dnDev

dnDev := price

price := source

dxt = price - average

dyt = val - daY

price -= val

stdDevAcc += price * price

dsxx += dxt * dxt

dsyy += dyt * dyt

dsxy += dxt * dyt

val += slope

stdDev = math.sqrt(stdDevAcc / (periods == 0 ? 1 : periods))

pearsonR = dsxx == 0 or dsyy == 0 ? 0 : dsxy / math.sqrt(dsxx * dsyy)

= calcDev(sourceInput, lengthInput, s, a, i)

upperStartPrice = startPrice + (useUpperDevInput ? upperMultInput * stdDev : upDev)

upperEndPrice = endPrice + (useUpperDevInput ? upperMultInput * stdDev : upDev)

var line upper = na

lowerStartPrice = startPrice + (useLowerDevInput ? -lowerMultInput * stdDev : -dnDev)

lowerEndPrice = endPrice + (useLowerDevInput ? -lowerMultInput * stdDev : -dnDev)

var line lower = na

if na(upper) and not na(upperStartPrice) and showLinreg

upper := line.new(bar_index - lengthInput + 1, upperStartPrice, bar_index, upperEndPrice, width=1, extend=extendStyle, color=color.new(colorUpper, 0))

else

line.set_xy1(upper, bar_index - lengthInput + 1, upperStartPrice)

line.set_xy2(upper, bar_index, upperEndPrice)

na

if na(lower) and not na(lowerStartPrice) and showLinreg

lower := line.new(bar_index - lengthInput + 1, lowerStartPrice, bar_index, lowerEndPrice, width=1, extend=extendStyle, color=color.new(colorUpper, 0))

else

line.set_xy1(lower, bar_index - lengthInput + 1, lowerStartPrice)

line.set_xy2(lower, bar_index, lowerEndPrice)

na

showLinregPlotUpper = showLinreg ? upper : na

showLinregPlotLower = showLinreg ? lower : na

showLinregPlotBaseLine = showLinreg ? baseLine : na

linefill.new(showLinregPlotUpper, showLinregPlotBaseLine, color = colorUpper)

linefill.new(showLinregPlotBaseLine, showLinregPlotLower, color = colorLower)

// Pearson's R

var label r = na

label.delete(r )

if showPearsonInput and not na(pearsonR) and showLinreg

r := label.new(bar_index - lengthInput + 1, lowerStartPrice, str.tostring(pearsonR, "#.################"), color = color.new(color.white, 100), textcolor=color.new(colorUpper, 0), size=size.normal, style=label.style_label_up)

//Mavilim

group4 = "Mavilim Settings"

mavilimold = input(false, title="Show Previous Version of MavilimW?",group=group4)

fmal=input(3,"First Moving Average length",group = group4)

smal=input(5,"Second Moving Average length",group = group4)

tmal=fmal+smal

Fmal=smal+tmal

Ftmal=tmal+Fmal

Smal=Fmal+Ftmal

M1= ta.wma(close, fmal)

M2= ta.wma(M1, smal)

M3= ta.wma(M2, tmal)

M4= ta.wma(M3, Fmal)

M5= ta.wma(M4, Ftmal)

MAVW= ta.wma(M5, Smal)

col1= MAVW>MAVW

col3= MAVWpmaxsrc ? pmaxsrc-pmaxsrc : 0

vdd1=pmaxsrc

ma = 0.0

if mav == "SMA"

ma := ta.sma(pmaxsrc, length)

ma

if mav == "EMA"

ma := ta.ema(pmaxsrc, length)

ma

if mav == "WMA"

ma := ta.wma(pmaxsrc, length)

ma

if mav == "TMA"

ma := ta.sma(ta.sma(pmaxsrc, math.ceil(length / 2)), math.floor(length / 2) + 1)

ma

if mav == "VAR"

ma := VAR

ma

if mav == "WWMA"

ma := WWMA

ma

if mav == "ZLEMA"

ma := ZLEMA

ma

if mav == "TSF"

ma := TSF

ma

ma

MAvg=getMA(pmaxsrc, length)

longStop = Normalize ? MAvg - Multiplier*atr/close : MAvg - Multiplier*atr

longStopPrev = nz(longStop , longStop)

longStop := MAvg > longStopPrev ? math.max(longStop, longStopPrev) : longStop

shortStop = Normalize ? MAvg + Multiplier*atr/close : MAvg + Multiplier*atr

shortStopPrev = nz(shortStop , shortStop)

shortStop := MAvg < shortStopPrev ? math.min(shortStop, shortStopPrev) : shortStop

dir = 1

dir := nz(dir , dir)

dir := dir == -1 and MAvg > shortStopPrev ? 1 : dir == 1 and MAvg < longStopPrev ? -1 : dir

PMax = dir==1 ? longStop: shortStop

plot(showsupport ? MAvg : na, color=#fbff04, linewidth=2, title="EMA9")

pALL=plot(PMax, color=color.new(color.red, transp = 0), linewidth=2, title="PMax")

alertcondition(ta.cross(MAvg, PMax), title="Cross Alert", message="PMax - Moving Avg Crossing!")

alertcondition(ta.crossover(MAvg, PMax), title="Crossover Alarm", message="Moving Avg BUY SIGNAL!")

alertcondition(ta.crossunder(MAvg, PMax), title="Crossunder Alarm", message="Moving Avg SELL SIGNAL!")

alertcondition(ta.cross(pmaxsrc, PMax), title="Price Cross Alert", message="PMax - Price Crossing!")

alertcondition(ta.crossover(pmaxsrc, PMax), title="Price Crossover Alarm", message="PRICE OVER PMax - BUY SIGNAL!")

alertcondition(ta.crossunder(pmaxsrc, PMax), title="Price Crossunder Alarm", message="PRICE UNDER PMax - SELL SIGNAL!")

buySignalk = ta.crossover(MAvg, PMax)

plotshape(buySignalk and showsignalsk ? PMax*0.995 : na, title="Buy", text="Buy", location=location.absolute, style=shape.labelup, size=size.tiny, color=color.new(color.green, transp = 0), textcolor=color.white)

sellSignallk = ta.crossunder(MAvg, PMax)

plotshape(sellSignallk and showsignalsk ? PMax*1.005 : na, title="Sell", text="Sell", location=location.absolute, style=shape.labeldown, size=size.tiny, color=color.new(color.red, transp = 0), textcolor=color.white)

// buySignalc = ta.crossover(pmaxsrc, PMax)

// plotshape(buySignalc and showsignalsc ? PMax*0.995 : na, title="Buy", text="Buy", location=location.absolute, style=shape.labelup, size=size.tiny, color=#0F18BF, textcolor=color.white)

// sellSignallc = ta.crossunder(pmaxsrc, PMax)

// plotshape(sellSignallc and showsignalsc ? PMax*1.005 : na, title="Sell", text="Sell", location=location.absolute, style=shape.labeldown, size=size.tiny, color=#0F18BF, textcolor=color.white)

// mPlot = plot(ohlc4, title="", style=plot.style_circles, linewidth=0,display=display.none)

longFillColor = highlighting ? (MAvg>PMax ? color.new(color.green, transp = 90) : na) : na

shortFillColor = highlighting ? (MAvg math.exp(-(math.pow(x, 2)/(h * h * 2)))

//-----------------------------------------------------------------------------}

//Append lines

//-----------------------------------------------------------------------------{

n = bar_index

var ln = array.new_line(0)

if barstate.isfirst and repaint

for i = 0 to 499

array.push(ln,line.new(na,na,na,na))

//-----------------------------------------------------------------------------}

//End point method

//-----------------------------------------------------------------------------{

var coefs = array.new_float(0)

var den = 0.

if barstate.isfirst and not repaint

for i = 0 to 499

w = gauss(i, h)

coefs.push(w)

den := coefs.sum()

out = 0.

if not repaint

for i = 0 to 499

out += src * coefs.get(i)

out /= den

mae = ta.sma(math.abs(src - out), 499) * mult

upperN = out + mae

lowerN = out - mae

//-----------------------------------------------------------------------------}

//Compute and display NWE

//-----------------------------------------------------------------------------{

float y2 = na

float y1 = na

nwe = array.new(0)

if barstate.islast and repaint

sae = 0.

//Compute and set NWE point

for i = 0 to math.min(499,n - 1)

sum = 0.

sumw = 0.

//Compute weighted mean

for j = 0 to math.min(499,n - 1)

w = gauss(i - j, h)

sum += src * w

sumw += w

y2 := sum / sumw

sae += math.abs(src - y2)

nwe.push(y2)

sae := sae / math.min(499,n - 1) * mult

for i = 0 to math.min(499,n - 1)

if i%2 and showNadaray

line.new(n-i+1, y1 + sae, n-i, nwe.get(i) + sae, color = upCss)

line.new(n-i+1, y1 - sae, n-i, nwe.get(i) - sae, color = dnCss)

if src > nwe.get(i) + sae and src < nwe.get(i) + sae and showNadaray

label.new(n-i, src , '▼', color = color(na), style = label.style_label_down, textcolor = dnCss, textalign = text.align_center)

if src < nwe.get(i) - sae and src > nwe.get(i) - sae and showNadaray

label.new(n-i, src , '▲', color = color(na), style = label.style_label_up, textcolor = upCss, textalign = text.align_center)

y1 := nwe.get(i)

//-----------------------------------------------------------------------------}

//Dashboard

//-----------------------------------------------------------------------------{

var tb = table.new(position.top_right, 1, 1

, bgcolor = #1e222d

, border_color = #373a46

, border_width = 1

, frame_color = #373a46

, frame_width = 1)

if repaint

tb.cell(0, 0, 'Repainting Mode Enabled', text_color = color.white, text_size = size.small)

//-----------------------------------------------------------------------------}

//Plot

//-----------------------------------------------------------------------------}

// plot(repaint ? na : out + mae, 'Upper', upCss)

// plot(repaint ? na : out - mae, 'Lower', dnCss)

//Crossing Arrows

// plotshape(ta.crossunder(close, out - mae) ? low : na, "Crossunder", shape.labelup, location.absolute, color(na), 0 , text = '▲', textcolor = upCss, size = size.tiny)

// plotshape(ta.crossover(close, out + mae) ? high : na, "Crossover", shape.labeldown, location.absolute, color(na), 0 , text = '▼', textcolor = dnCss, size = size.tiny)

//-----------------------------------------------------------------------------}

//////////////////////////////////////////////////////////////////////////////////

enableD = input (true, "DIVERGANCE ON/OFF" , group="INDICATORS ON/OFF")

//DIVERGANCE

prd1 = input.int (defval=5 , title='PIVOT PERIOD' , minval=1, maxval=50 , group="DIVERGANCE")

source = input.string(defval='HIGH/LOW' , title='SOURCE FOR PIVOT POINTS' , options= , group="DIVERGANCE")

searchdiv = input.string(defval='REGULAR/HIDDEN', title='DIVERGANCE TYPE' , options= , group="DIVERGANCE")

showindis = input.string(defval='FULL' , title='SHOW INDICATORS NAME' , options= , group="DIVERGANCE")

showlimit = input.int(1 , title='MINIMUM NUMBER OF DIVERGANCES', minval=1, maxval=11 , group="DIVERGANCE")

maxpp = input.int (defval=20 , title='MAXIMUM PIVOT POINTS TO CHECK', minval=1, maxval=20 , group="DIVERGANCE")

maxbars = input.int (defval=200 , title='MAXIMUM BARS TO CHECK' , minval=30, maxval=200 , group="DIVERGANCE")

showlast = input (defval=false , title='SHOW ONLY LAST DIVERGANCE' , group="DIVERGANCE")

dontconfirm = input (defval=false , title="DON'T WAIT FOR CONFORMATION" , group="DIVERGANCE")

showlines = input (defval=false , title='SHOW DIVERGANCE LINES' , group="DIVERGANCE")

showpivot = input (defval=false , title='SHOW PIVOT POINTS' , group="DIVERGANCE")

calcmacd = input (defval=true , title='MACD' , group="DIVERGANCE")

calcmacda = input (defval=true , title='MACD HISTOGRAM' , group="DIVERGANCE")

calcrsi = input (defval=true , title='RSI' , group="DIVERGANCE")

calcstoc = input (defval=true , title='STOCHASTIC' , group="DIVERGANCE")

calccci = input (defval=true , title='CCI' , group="DIVERGANCE")

calcmom = input (defval=true , title='MOMENTUM' , group="DIVERGANCE")

calcobv = input (defval=true , title='OBV' , group="DIVERGANCE")

calcvwmacd = input (true , title='VWMACD' , group="DIVERGANCE")

calccmf = input (true , title='CHAIKIN MONEY FLOW' , group="DIVERGANCE")

calcmfi = input (true , title='MONEY FLOW INDEX' , group="DIVERGANCE")

calcext = input (false , title='CHECK EXTERNAL INDICATOR' , group="DIVERGANCE")