Cnagda Pure Price ActionCnagda Pure Price Action (CPPA) indicator is a pure price action-based system designed to provide traders with real-time, dynamic analysis of the market. It automatically identifies key candles, support and resistance zones, and potential buy/sell signals by combining price, volume, and multiple popular trend indicators.

How Price Action & Volume Analysis Works

Silver Zone – Logic, Reason, and Trade Planning

Logic & Visualization:

The Silver Zone is created when the closing price is the lowest in the chosen window and volume is the highest in that window.

Visually, a large silver-colored box/rectangle appears on the chart.

Thick horizontal lines (top and bottom) are drawn at the high and low of that candle/bar, extending to the right.

Reasoning:

This combination typically occurs at strong “accumulation” or support areas:

Sellers push the price down to the lowest point, but aggressive buyers step in with high volume, absorbing supply.

Indicates potential exhaustion of selling and likely shift in market control to buyers.

How to Plan Trades Using Silver Zone:

Watch if price returns to the Silver Zone in the future: It often acts as powerful support.

Bullish entries (buys) can be planned when price tests or slightly pierces this zone, especially if new buy signals occur (like yellow/green candle labels).

Place your stop-loss below the bottom line of the Silver Zone.

Target: Look for the nearest resistance or opposing zone, or use indicator’s bullish label as confirmation.

Extra Tip:

Multiple touches of the Silver Zone reinforce its importance, but if price closes deeply below it with high volume, that’s a caution signal—support may be breaking.

Black Zone – Logic, Reason, and Trade Planning (as CPPA):

Logic & Visualization:

The Black Zone is created when the closing price is the highest in the chosen window and volume is the lowest in that window.

Visually, a large black-colored box/rectangle appears on the chart, along with thick horizontal lines at the top (high) and bottom (low) of the candle, extending to the right.

Reasoning:

This combination signals a strong “distribution” or resistance area:

Buyers push the price up to a local high, but low volume means there is not much follow-through or conviction in the move.

Often marks exhaustion where uptrend may pause or reverse, as sellers can soon step in.

How to Plan Trades Using Black Zone:

If price revisits the Black Zone in the future, it often acts as major resistance.

Bearish entries (sells) are considered when price is near, testing, or slightly above the Black Zone—especially if new sell signals appear (like blue/red candle labels).

Place your stop-loss just above the top line of the Black Zone.

Target: Nearest support zone (such as a Silver Zone) or next indicator’s bearish label.

Extra Tip:

Multiple touches of the Black Zone make it stronger, but if price closes far above with rising volume, be cautious—resistance might be breaking.

Support Line – Logic, Reason, and Trade Planning (as Cppa):

Logic & Visualization:

The Support Line is a dynamically drawn dashed line (usually blue) that marks key price levels where the market has previously shown significant buying interest.

The line is generated whenever a candle forms a high price with high volume (orange logic).

The script checks for historical pivot lows, past support zones, and even higher timeframe (HTF) supports, and then extends a blue dashed line from that price level to the right, labeling it (sometimes as “Prev Support Orange, HTF”).

Reasoning:

This line helps you visually identify where demand has been strong enough to hold price from falling further—essentially a floor in the market used by professional traders.

If price approaches or re-tests this line, there’s a good chance buyers will defend it again.

How to Plan Trades Using Support Line:

Watch for price to approach the Support Line during down moves. If you see a bullish candlestick pattern, buy labels (yellow/green), or other indicators aligning, this can be a high-probability entry zone.

Great for planning stop-loss for long trades: place stops just below this line.

Target: Next resistance zone, Black Zone, or the top of the last swing.

Extra Tip:

Multiple confirmations (support line + Silver Zone + bullish label) provide powerful entry signals.

If price closes strongly below the Support Line with volume, be cautious—support may be breaking, and a trend reversal or deeper correction could follow.

Resistance Line – Logic, Reason, and Trade Planning (from CPPA):

Logic & Visualization:

The Resistance Line is a dynamically drawn dashed line (usually purple or red) that identifies price levels where the market has previously faced significant selling pressure.

This line is created when a candle reaches a high price combined with high volume (orange logic), or from a historical pivot high/resistance,

The script also tracks higher timeframe (HTF) resistance lines, labeled as “Prev Resistance Orange, HTF,” and extends these dashed lines to the right across the chart.

Reasoning:

Resistance Lines are visual markers of “supply zones,” where buyers previously failed, and sellers took control.

If the price returns to this line later, sellers may get active again to defend this level, halting the uptrend.

How to Plan Trades Using Resistance Line:

Watch for price to approach the Resistance Line during up moves. If you see bearish candlestick patterns, sell labels (blue/red), or bearish indicator confirmation, this becomes a strong shorting opportunity.

Perfect for placing stop-loss in short trades—put your stop just above the Resistance Line.

Target: Next support zone (Silver Zone) or bottom of the last swing.

If the price breaks above with high volume, avoid shorting—resistance may be failing.

Extra Tip:

Multiple resistances (Resistance Line + Black Zone + bearish label) make short signals stronger.

Choppy movement around this line often signals indecision; wait for a clear rejection before entering trades.

Bullish / Bearish Label – Logic, Reason, and Trade Planning:

Logic & Visualization:

The indicator constantly calculates a "Bull Score" and a "Bear Score" based on several factors:

Trend direction from price slope

Confirmation by popular indicators (RSI, ADX, SAR, CMF, OBV, CCI, Bollinger Bands, TWAP)

Adaptive scoring (higher score for each bullish/bearish condition met)

If Bull Score > Bear Score, the chart displays a green "BULLISH" label (usually below the bar).

If Bear Score > Bull Score, the chart displays a red "BEARISH" label (usually above the bar).

If neither dominates, a "NEUTRAL" label appears.

Reasoning:

The labels summarize complex price action and indicator analysis into a simple, actionable sentiment cue:

Bullish: Majority of conditions indicate buying strength; trend is up.

Bearish: Majority signals show selling pressure; trend is down.

How to Use in Trade Planning:

Use the Bullish label as confirmation to enter or hold long (buy) positions, especially if near support/Silver Zone.

Use the Bearish label to enter/hold short (sell) positions, especially if near resistance/Black Zone.

For best results, combine with candle color, volume analysis, or other labels (yellow/green for buys, blue/red for sells).

Avoid trading against these labels unless you have strong confluence from zones/support levels.

Yellow Label (Buy Signal) – Logic, Reason & Trade Planning:

Logic & Visualization:

The yellow label appears below a candle (label.style_label_up, yloc.belowbar) and marks a potential buy signal.

Script conditions:

The candle must be a “yellow candle” (which means it’s at the local lowest close, not a high, with normal volume).

Volume is decreasing for 2 consecutive candles (current volume < previous volume, previous volume < second previous).

When these conditions are met, a yellow label is plotted below the candle.

Reasoning:

This scenario often marks the end of selling pressure and start of possible accumulation—buyers may be stepping in as sellers exhaust.

Decreasing volume during a local price low means selling is slowing, possibly hinting at a reversal.

How to Trade Using Yellow Label:

Entry: Consider buying at/just above the yellow-labeled candle’s close.

Stop-loss: A bit below the candle’s low (or Silver Zone line, if present).

Target: Next resistance level, Black Zone, or chart’s bullish label.

Extra Tip:

If the yellow label is found at/near a Silver Zone or Support Line, and trend is “Bullish,” the setup gets even stronger.

Avoid trading if overall indicator shows “Bearish.”

Green Label (Buy with Increasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The green label is plotted below a candle (label.style_label_up, yloc.belowbar) and marks a strong buy signal.

Script conditions:

The candle must be a “yellow candle” (at the local lowest close, normal volume).

Volume is increasing for 2 consecutive candles (current volume > previous volume, previous volume > second previous).

When these conditions are met, a green label is plotted below the candle.

Reasoning:

This scenario signals that buyers are stepping in aggressively at a local price low—the end of a downtrend with strong, rising activity.

Increasing volume at a price low is a classic sign of accumulation, where institutions or large players may be buying.

How to Trade Using Green Label:

Entry: Consider buying at/just above the green-labeled candle’s close for a momentum-based reversal.

Stop-loss: Slightly below the candle’s low, or the Silver Zone/support line if present.

Target: Nearest resistance zone/Black Zone, indicator’s bullish label, or next swing high.

Extra Tip:

If the green label is near other supports (Silver Zone, Support Line), the setup is extra strong.

Use confirmation from Bullish labels or trend signals for best results.

Green label setups are suitable for quick, high momentum trades due to increasing volume

Blue Label (Sell Signal on Decreasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The blue label is plotted above a candle (label.style_label_down, yloc.abovebar) as a potential sell signal.

Script conditions:

The candle is a “blue candle” (local highest close, but not also lowest, and volume is neither highest nor lowest).

Volume is decreasing over 2 consecutive candles (current volume < previous, previous < two ago).

When these match, a blue label appears above the candle.

Reasoning:

This typically signals buyer exhaustion at a local high: price has gone up, but volume is dropping, suggesting big players may not be buying any more at these levels.

The trend is losing strength, and a reversal or pullback is likely.

How to Trade Using Blue Label:

Entry: Look to sell at/just below the candle with the blue label.

Stop-loss: Just above the candle’s high (or above the Black Zone/resistance if present).

Target: Nearest support, Silver Zone, or a swing low.

Extra Tip:

Blue label signals are stronger if they appear near Black Zones or Resistance Lines, or when the general market label is "Bearish."

As with buy setups, always check for confirmation from trend or volume before trading aggressively.

Blue Label (Sell Signal on Decreasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The blue label is plotted above a candle (label.style_label_down, yloc.abovebar) as a potential sell signal.

Script conditions:

The candle is a “blue candle” (local highest close, but not also lowest, and volume is neither highest nor lowest).

Volume is decreasing over 2 consecutive candles (current volume < previous, previous < two ago).

When these match, a blue label appears above the candle.

Reasoning:

This typically signals buyer exhaustion at a local high: price has gone up, but volume is dropping, suggesting big players may not be buying any more at these levels.

The trend is losing strength, and a reversal or pullback is likely.

How to Trade Using Blue Label:

Entry: Look to sell at/just below the candle with the blue label.

Stop-loss: Just above the candle’s high (or above the Black Zone/resistance if present).

Target: Nearest support, Silver Zone, or a swing low.

Extra Tip:

Blue label signals are stronger if they appear near Black Zones or Resistance Lines, or when the general market label is "Bearish."

As with buy setups, always check for confirmation from trend or volume before trading aggressively.

Here’s a summary of all key chart labels, zones, and trading logic of your Price Action script:

Silver Zone: Powerful support zone. Created at lowest close + highest volume. Best for buy entries near its lines.

Black Zone: Strong resistance zone. Created at highest close + lowest volume. Ideal for short trades near its levels.

Support Line: Blue dashed line at historical demand; buyers defend here. Look for bullish setups when price approaches.

Resistance Line: Purple/red dashed line at supply; sellers defend here. Great for bearish setups when price nears.

Bullish/Bearish Labels: Summarize trend direction using price action + multiple indicator confirmations. Plan buys, holds on bullish; sells, shorts on bearish.

Yellow Label: Buy signal on decreasing volume and local price low. Entry above candle, stop below, target next resistance.

Green Label: Strong buy on increasing volume at a price low. Entry for momentum trade, stop below, target next zone.

Blue Label: Sell signal on dropping volume and local price high. Entry below candle, stop above, target next support.

Best Practices:

Always combine zone/label signals for higher probability trades.

Use stop-loss near zones/lines for risk management.

Prefer trading in the trend direction (bullish/bearish label agrees with your entry).

if Any Question, Suggestion Feel free to ask

Disclaimer:

All information provided by this indicator is for educational and analysis purposes only, and should not be considered financial advice.

Recherche dans les scripts pour "accumulation"

RVol+ Enhanced Relative Volume Indicator📊 RVol+ Enhanced Relative Volume Indicator

Overview

RVol+ (Relative Volume Plus) is an advanced time-based relative volume indicator designed specifically for swing traders and breakout detection. Unlike simple volume comparisons, RVol+ analyzes volume at the same time of day across multiple sessions, providing statistically significant insights into institutional activity and breakout potential.

🎯 Key Features

Core Volume Analysis

Time-Based RVol Calculation - Compares current cumulative volume to the average volume at this exact time over the past N days

Statistical Z-Score - Measures volume in standard deviations from the mean for true anomaly detection

Volume Percentile - Shows where current volume ranks historically (0-100%)

Sustained Volume Filter - 3-bar moving average prevents false signals from single-bar spikes

Breakout Detection

🚀 Confirmed Breakouts - Identifies price breakouts validated by high volume (RVol > 1.5x)

⚠️ False Breakout Warnings - Alerts when price breaks key levels on low volume (high failure risk)

Multi-Timeframe Context - Weekly volume overlay prevents chasing daily noise

Advanced Metrics

OBV Divergence Detection - Spots bullish/bearish accumulation/distribution patterns

Volume Profile Integration - Identifies institutional positioning

Money Flow Analysis - Tracks smart money vs retail activity

Extreme Volume Alerts - 🔥 Labels mark unusual spikes beyond the display cap

Visual Intelligence

Smart Color Coding:

🟢 Bright Teal = High activity (RVol ≥ 1.5x)

🟡 Medium Teal = Caution zone (RVol ≥ 1.2x)

⚪ Light Teal = Normal activity

🟠 Orange = Breakout confirmed

🔴 Red = False breakout risk

Comprehensive Stats Table:

Current Volume (formatted as M/K/B)

RVol ratio

Z-Score with significance

Volume percentile

Historical average and standard deviation

Sustained volume confirmation

📈 How to Use

For Swing Trading (1D - 3W Holds)

Perfect Setup:

✓ RVol > 1.5x (bright teal)

✓ Z-Score > 2.0 (⚡ alert)

✓ Percentile > 90%

✓ Sustained = ✓

✓ 🚀 Breakout label appears

Avoid:

✗ Red "Low Vol" warning during breakouts

✗ RVol < 1.0 at key levels

✗ Sustained volume not confirmed

Signal Interpretation

⚡ Z>2 Labels - Statistically significant volume (95th+ percentile) - highest probability moves

↗️ OBV+ Labels - Bullish accumulation (OBV rising while price consolidates)

↘️ OBV- Labels - Bearish distribution (OBV falling while price rises)

🔵 Blue Background - Weekly volume elevated (confirms daily strength)

⚙️ Customization

Basic Settings

N Day Average - Number of historical days for comparison (default: 5)

RVol Thresholds - Customize highlight levels (default: 1.2x, 1.5x)

Visual Display Cap - Prevent extreme spikes from compressing view (default: 4.0x)

Advanced Metrics (Toggle On/Off)

Z-Score analysis

Weekly RVol context

OBV divergence detection

Volume percentile ranking

Breakout signal generation

Table Customization

Position - 9 placement options to avoid chart overlap

Size - Tiny to Huge

Colors - Full customization of positive/negative/neutral values

Transparency - Adjustable background

Debug Mode

Enable Pine Logs for calculation transparency

Adjustable log frequency

Real-time calculation breakdown

🔬 Technical Details

Algorithm:

Binary search for historical lookups (O(log n) performance)

Time-zone aware session detection

DST-safe timestamp calculations

Exponentially weighted standard deviation

Anti-repainting architecture

Performance:

Optimized for max_bars_back = 5000

Efficient array management

Built-in function optimization

Memory-conscious data structures

📊 What Makes RVol+ Different?

vs. Standard Volume:

Context-aware (time-of-day matters)

Statistical significance testing

False breakout filtering

vs. Basic RVol:

Z-Score normalization (2-3 sigma detection)

Multi-timeframe confirmation

OBV divergence integration

Sustained volume filtering

Smart visual scaling

vs. Professional Tools:

Free and open-source

Fully customizable

No black-box algorithms

Educational debug logs

💡 Best Practices

Wait for Confirmation - Don't enter on first bar; wait for sustained volume ✓

Combine with Price Action - RVol validates, price structure determines entry

Weekly Context Matters - Blue background = institutional interest

Z-Score is King - Focus on ⚡ alerts for highest probability

Avoid Low Volume Breakouts - Red ⚠️ labels = high failure risk

🎓 Trading Psychology

Volume precedes price. When RVol+ shows:

High RVol + Rising OBV = Accumulation before breakout

High RVol at Resistance = Test of conviction

Low RVol on Breakout = Retail-driven (fade candidate)

Z-Score > 3 = Potential "whale" positioning

📝 Credits

Based on the time-based RVol concept from /u/HurlTeaInTheSea, enhanced with:

Statistical analysis (z-scores, percentiles)

Multi-timeframe integration

OBV divergence detection

Professional-grade visualization

Swing trading optimization

🔧 Version History

v2.0 - Enhanced Edition

Added Z-Score analysis

Multi-timeframe volume context

OBV divergence detection

Breakout confirmation system

Smart color coding

Customizable stats table

Debug logging mode

Performance optimizations

📚 Learn More

For optimal use with swing trading:

Combine with support/resistance levels

Watch for volume clusters in consolidation

Use weekly timeframe for trend confirmation

Monitor OBV divergence for early warnings

⚠️ Disclaimer

This indicator is for educational purposes. Volume analysis is one component of trading decisions. Always use proper risk management, consider multiple timeframes, and validate signals with price structure. Past performance does not guarantee future results.

🚀 Getting Started

Add indicator to chart

Adjust "N Day Average" to your preference (5-10 days typical)

Position stats table to avoid overlap

Enable features you want to monitor

Watch for 🚀 breakout confirmations!

Happy Trading! 📈

EMA Percentile Rank [SS]Hello!

Excited to release my EMA percentile Rank indicator!

What this indicator does

Plots an EMA and colors it by short-term trend.

When price crosses the EMA (up or down) and remains on that side for three subsequent bars, the cross is “confirmed.”

At the moment of the most recent cross, it anchors a reference price to the crossover point to ensure static price targets.

It measures the historical distance between price and the EMA over a lookback window, separately for bars above and below the EMA.

It computes percentile distances (25%, 50%, 85%, 95%, 99%) and draws target bands above/below the anchor.

Essentially what this indicator does, is it converts the raw “distance from EMA” behavior into probabilistic bands and historical hit rates you can use for targets, stop placement, or mean-reversion/continuation decisions.

Indicator Inputs

EMA length: Default is 21 but you can use any EMA you prefer.

Lookback: Default window is 500, this is length that the percentiles are calculated. You can increase or decrease it according to your preference and performance.

Show Accumulation Table: This allows you to see the table that shows the hits/price accumulation of each of the percentile ranges. UCL means upper confidence and LCL means lower confidence (so upper and lower targets).

About Percentiles

A percentile is a way of expressing the position of a value within a dataset relative to all the other values.

It tells you what percentage of the data points fall at or below that value.

For example:

The 25th percentile means 25% of the values are less than or equal to it.

The 50th percentile (also called the median) means half the values are below it and half are above.

The 99th percentile means only 1% of the values are higher.

Percentiles are useful because they turn raw measurements into context — showing how “extreme” or “typical” a value is compared to historical behavior.

In the EMA Percentile Rank indicator, this concept is applied to the distance between price and the EMA. By calculating percentile distances, the script can mark levels that have historically been reached often (low percentiles) or rarely (high percentiles), helping traders gauge whether current price action is stretched or within normal bounds.

Use Cases

The EMA Percentile Rank indicator is best suited for traders who want to quantify how far price has historically moved away from its EMA and use that context to guide decision-making.

One strong use case is target setting after trend shifts: when a confirmed crossover occurs, the percentile bands (25%, 50%, 85%, 95%, 99%) provide statistically grounded levels for scaling out profits or placing stops, based on how often price has historically reached those distances. This makes it valuable for traders who prefer data-driven risk/reward planning instead of arbitrary point targets. Another use case is identifying stretched conditions — if price rapidly tags the 95% or 99% band after a cross, that’s an unusually large move relative to history, which could signal exhaustion and prompt mean-reversion trades or protective actions.

Conversely, if the accumulation table shows price frequently resides in upper bands after bullish crosses, traders may anticipate continuation and hold positions longer . The indicator is also effective as a trend filter when combined with its EMA color-coding : only taking trades in the trend’s direction and using the bands as dynamic profit zones.

Additionally, it can support multi-timeframe confluence (if you align your chart to the timeframes of interest), where higher-timeframe trend direction aligns with lower-timeframe percentile behavior for higher-probability setups. Swing traders can use it to frame pullbacks — entering near lower percentile bands during an uptrend — while intraday traders might use it to fade extremes or ride breakouts past the median band. Because the anchor price resets only on EMA crosses, the indicator preserves a consistent reference for ongoing trades, which is especially helpful for managing swing positions through noise .

Overall, its strength lies in transforming raw EMA distance data into actionable, probability-weighted levels that adapt to the instrument’s own volatility and tendencies .

Summary

This indicator transforms a simple EMA into a distribution-aware framework: it learns how far price tends to travel relative to the EMA on either side, and turns those excursions into percentile bands and historical hit rates anchored to the most recent cross. That makes it a flexible tool for targets, stops, and regime filtering, and a transparent way to reason about “how stretched is stretched?”—with context from your chosen market and timeframe.

I hope you all enjoy!

And as always, safe trades!

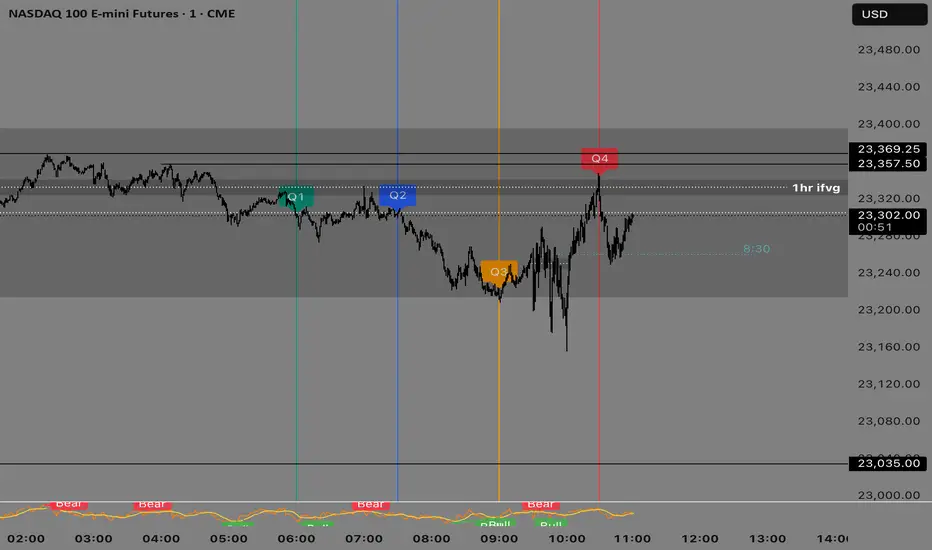

Quarterly Theory —Q1,Q2,Q3,Q4The Quarterly Theory Indicator is a trading tool designed to visualize the natural time-based cycles of the market, based on the principles of Quarterly Theory, popularized by the Inner Circle Trader (ICT). The indicator divides market sessions into four equal “quarters” to help traders identify potential accumulation, manipulation, and distribution phases (AMD model) and improve the timing of entries and exits.

Key Features:

Quarter Divisions (Q1–Q4):

Each market session (e.g., NY AM, London, Asia) is divided into four quarters.

Vertical lines mark the beginning of each quarter, making it easy to track session structure.

Optional labels show Q1, Q2, Q3, and Q4 directly on the chart.

True Open (Q2 Open):

The True Open is the opening price of Q2, considered a key reference point in Quarterly Theory.

A horizontal red line is drawn at the True Open price with a label showing the exact value.

This line helps traders filter bullish and bearish setups:

Buy below the True Open if the market is bullish.

Sell above the True Open if the market is bearish.

Session Awareness:

The indicator can automatically detect market sessions and reset lines and labels for each new session.

Ensures that only the current session’s True Open and quarter lines are displayed, reducing chart clutter.

Timeframe Flexibility:

Works on any chart timeframe (1-minute to daily).

Maintains accurate alignment of quarters and True Open regardless of the timeframe used.

Purpose of Quarterly Theory:

Quarterly Theory is based on the idea that market behavior is fractal and time-driven. By dividing sessions into four quarters, traders can anticipate potential market phases:

Q1: Initial price discovery and setup for the session.

Q2: Accumulation or manipulation phase, where the True Open is established.

Q3: Manipulation or Judas Swing phase designed to trap traders.

Q4: Distribution or trend continuation/reversal.

By visualizing these quarters and the True Open, traders can reduce ambiguity, identify high-probability setups, and improve their timing in line with the ICT AMD (Accumulation, Manipulation, Distribution) framework.

Linh's Anomaly Radar v2What this script does

It’s an event detector for price/volume anomalies that often precede or confirm moves.

It watches a bunch of patterns (Wyckoff tests, squeezes, failed breakouts, turnover bursts, etc.), applies robust z-scores, optional trend filters, cooldowns (to avoid spam), and then fires:

A shape/label on the bar,

A row in the mini panel (top-right),

A ready-made alertcondition you can hook into.

How to add & set up (TradingView)

Paste the script → Save → Add to chart on Daily first (works on any TF).

Open Settings → Inputs:

General

• Use Robust Z (MAD): more outlier-resistant; keep on.

• Z Lookback: 60 bars is ~3 months; bump to 120 for slower regimes.

• Cooldown: min bars to wait before the same signal can fire again (default 5).

• Use trend filter: if on, “bullish” signals only fire above SMA(tfLen), “bearish” below.

Thresholds: fine-tune sensitivity (defaults are sane).

To create alerts: Right-click chart → Add alert

Condition: Linh’s Anomaly Radar v2 → choose a specific signal or Composite (Σ).

Options: “Once per bar close” (recommended).

Customize message if you want ticker/timeframe in your phone push.

The mini panel (top-right)

Signal column: short code (see cheat sheet below).

Fired column: a dot “•” means that on the latest bar this signal fired.

Score (right column): total count of signals that fired this bar.

Σ≥N shows your composite threshold (how many must fire to trigger the “Composite” alert).

Shapes & codes (what’s what)

Code Name (category) What it’s looking for Why it matters

STL Stealth Volume z(volume)>5 & ** z(return)

EVR Effort vs Result squeeze z(vol)>3 & z(TR)<−0.5 Heavy effort, tiny spread → absorption

TGV Tight+Heavy (HL/ATR)<0.6 & z(vol)>3 Tight bar + heavy tape → pro activity

CLS Accumulation cluster ≥3 of last 5 bars: up, vol↑, close near high Classic accumulation footprint

GAP Open drive failure Big gap not filled (≥80%) & vol↑ One-sided open stalls → fade risk

BB↑ BB squeeze breakout Squeeze (z(BBWidth)<−1.3) → close > upperBB & vol↑ Regime shift with confirmation

ER↑ Effort→Result inversion Down day on vol then next bar > prior high Demand overwhelms supply

OBV OBV divergence OBV slope up & ** z(ret20)

WER Wide Effort, Opposite Result z(vol)>3, close+1 Selling into strength / distribution

NS No-Supply (Wyckoff) Down bar, HL<0.6·ATR, vol << avg Sellers absent into weakness

ND No-Demand (Wyckoff) Up bar, HL<0.6·ATR, vol << avg Buyers absent into strength

VAC Liquidity Vacuum z(vol)<−1.5 & ** z(ret)

UTD UTAD (failed breakout) Breaks swing-high, closes back below, vol↑ Stop-run, reversal risk

SPR Spring (failed breakdown) Breaks swing-low, closes back above, vol↑ Bear trap, reversal risk

PIV Pocket Pivot Up bar; vol > max down-vol in lookback Quiet base → sudden demand

NR7 Narrow Range 7 + Vol HL is 7-bar low & z(vol)>2 Coiled spring with participation

52W 52-wk breakout quality New 52-wk close high + squeeze + vol↑ High-quality breakouts

VvK Vol-of-Vol kink z(ATR20,200)>0.5 & z(ATR5,60)<0 Long-vol wakes up, short-vol compresses

TAC Turnover acceleration SMA3 vol / SMA20 vol > 1.8 & muted return Participation surging before move

RBd RSI Bullish div Price LL, RSI HL, vol z>1 Exhaustion of sellers

RS↑ RSI Bearish div Price HH, RSI LH, vol z>1 Exhaustion of buyers

Σ Composite Count of all fired signals ≥ threshold High-conviction bar

Placement:

Triangles up (below bar) → bullish-leaning events.

Triangles down (above bar) → bearish-leaning events.

Circles → neutral context (VAC, VvK, Composite).

Key inputs (quick reference)

General

Use Robust Z (MAD): keep on for noisy tickers.

Z Lookback (lenZ): 60 default; 120 if you want fewer alerts.

Trend filter: when on, bullish signals require close > SMA(tfLen), bearish require <.

Cooldown: prevents repeated firing of the same signal within N bars.

Phase-1 thresholds (core)

Stealth: vol z > 5, |ret z| < 1.

EVR: vol z > 3, TR z < −0.5.

Tight+Heavy: (HL/ATR) < 0.6, vol z > 3.

Cluster: window=5, min=3 strong bars.

GapFail: gap/ATR ≥1.5, fill <80%, vol z > 2.

BB Squeeze: z(BBWidth)<−1.3 then breakout with vol z > 2.

Eff→Res Up: prev bar heavy down → current bar > prior high.

OBV Div: OBV uptrend + |z(ret20)|<0.3.

Phase-2 thresholds (extras)

WER: vol z > 3, close1.

No-Supply/No-Demand: tight bar & very light volume vs SMA20.

Vacuum: vol z < −1.5, |ret z|>1.5.

UTAD/Spring: swing lookback N (default 20), vol z > 2.

Pocket Pivot: lookback for prior down-vol max (default 10).

NR7: 7-bar narrowest range + vol z > 2.

52W Quality: new 52-wk high + squeeze + vol z > 2.

VoV Kink: z(ATR20,200)>0.5 AND z(ATR5,60)<0.

Turnover Accel: SMA3/SMA20 > 1.8 and |ret z|<1.

RSI Divergences: compare to n bars back (default 14).

How to use it (playbooks)

A) Daily scan workflow

Run on Daily for your VN watchlist.

Turn Composite (Σ) alert on with Σ≥2 or ≥3 to reduce noise.

When a bar fires Σ (or a fav combo like STL + BB↑), drop to 60-min to time entries.

B) Breakout quality check

Look for 52W together with BB↑, TAC, and OBV.

If WER/ND appear near highs → downgrade the breakout.

C) Spring/UTAD reversals

If SPR fires near major support and RBd confirms → long bias with stop below spring low.

If UTD + WER/RS↑ near resistance → short/fade with stop above UTAD high.

D) Accumulation basing

During bases, you want CLS, OBV, TGV, STL, NR7.

A pocket pivot (PIV) can be your early add; manage risk below base lows.

Tuning tips

Too many signals? Raise stealthVolZ to 5.5–6, evrVolZ to 3.5, use Σ≥3.

Fast movers? Lower bbwZthr to −1.0 (less strict squeeze), keep trend filter on.

Illiquid tickers? Keep MAD z-scores on, increase lookbacks (e.g., lenZ=120).

Limitations & good habits

First lenZ bars on a new symbol are less reliable (incomplete z-window).

Some ideas (VWAP magnet, close auction spikes, ETF/foreign flows, options skew) need intraday/external feeds — not included here.

Pine can’t “screen” across the whole market; set alerts or cycle your watchlist.

Quick troubleshooting

Compilation errors: make sure you’re on Pine v6; don’t nest functions in if blocks; each var int must be declared on its own line.

No shapes firing: check trend filter (maybe price is below SMA and you’re waiting for bullish signals), and verify thresholds aren’t too strict.

VN30 Effort-vs-Result Multi-Scanner — LinhVN30 Effort-vs-Result Multi-Scanner (Pine v5)

Cross-section scanner for Vietnam’s VN30 stocks that surfaces Effort vs Result footprints and related accumulation/distribution and volatility tells. It renders a ranked table (Top-N) with per-ticker signals and key metrics.

What it does

Scans up to 30 tickers (editable input.symbol slots) using one security() call per symbol → stays under Pine’s 40-call limit and runs reliably on any chart.

Scores each ticker by counting active signals, then ranks and lists the top names.

Optional metrics columns: zVol(60), zTR(60), ATR(20), HL/ATR(20).

Signals (toggleable)

Price/Volume – Effort vs Result

EVR Squeeze (stealth): z(Vol,60) > 4 & z(TR,60) < −0.5

5σ Vol, ≤1σ Ret: z(Vol,60) > 5 & |z(Return,60)| < 1

Wide Effort, Opposite Result: z(Vol,60) > 3 & close < open & z(CLV×Vol,60) > 1

Spread Compression, Heavy Tape: (H−L)/ATR(20) < 0.6 & z(Vol,60) > 3

No-Supply / No-Demand: close < close & range < 0.6×ATR(20) & vol < 0.5×SMA(20)

Momentum & Volatility

Vol-of-Vol Kink: z(ATR20,200) rising & z(ATR5,60) falling

BB Squeeze → Expansion: BBWidth(20) in low regime (z<−1.3) then close > upper band & z(Vol,60) > 2

RSI Non-Confirmation: Price LL/HH with RSI HL/LH & z(Vol,60) > 1

Accumulation/Distribution

OBV Divergence w/ Flat Price: OBV slope > 0 & |z(ret20,260)| < 0.3

Accumulation Days Cluster: ≥3/5 bars: up close, higher vol, close near high

Effort-Result Inversion (Down): big vol on down day then next day close > prior high

How to use

Set the timeframe (works best on 1D for EOD scans).

Edit the 30 symbol slots to your VN30 constituents.

Choose Top N, toggle Show metrics/Only matches and enable/disable scenarios.

Read the table: Rank, Ticker, (metrics), Score, and comma-separated Signals fired.

Method notes

Z-scores use a population-std estimate; CLV×Vol is used for effort/location.

Rolling counts avoid ta.sum; OBV is computed manually; all logic is Pine v5-safe.

Intraday-only ideas (true VWAP magnets, auction volume, flows, futures/options) are not included—Pine can’t cross-scan those datasets.

Disclaimer: Educational tool, not financial advice. Always confirm signals on the chart and with your process.

BK AK-SILENCER🚨 Introducing BK AK-SILENCER — Volume Footprint Warfare, Right on the Price Bars 🚨

This isn’t a traditional indicator.

This is a tactical weapon — engineered to expose institutional behavior directly in the bar data, using volume logic, CVD divergence, and spike detection to pinpoint who’s really in control of the tape.

No panels. No clutter.

Just silent execution — built directly into price itself.

🔥 Why "SILENCER"?

Because real power moves in silence.

Institutions don’t chase — they build positions quietly, in size, beneath the surface.

BK AK-SILENCER gives you a real-time edge by visually revealing their footprints through color-coded bar behavior, divergence signals, and volume spike alerts — all directly on your chart.

🔹 “AK” honors my mentor A.K., whose training forged my trading discipline.

🔹 “SILENCER” represents the institutional mindset — high impact, low visibility. This tool lets you trade like them: without noise, without hesitation, with deadly clarity.

🧠 What Is BK AK-SILENCER?

A bar-level institutional detection tool, purpose-built to:

✅ Color-code bars based on volume aggression and close-location inside range

✅ Detect real-time bullish and bearish divergences between price and volume delta

✅ Tag volume spikes with a $ symbol to expose potential traps or silent position builds

✅ Overlay VWAP for real-time mean-reversion biasing

No extra windows.

No indicators talking over each other.

Just pure volume-logic weaponry embedded into price.

⚙️ What This Weapon Deploys

🔸 Bar Coloring Logic (Volume Footprint)

🟢 Power Buy = Strong close near highs on elevated volume

🟩 Accumulation = Weak close but still heavy volume

🔴 Power Sell = Strong close near lows on heavy selling

🟥 Distribution / Weakness = Low close without commitment

❗ Extreme Volume Spikes marked with $ — using standard deviation to highlight institutional bursts

🔸 CVD Divergence Detection

→ Tracks cumulative volume delta and compares it to price pivot behavior

Bullish Divergence = Price makes lower lows, CVD makes higher lows → hidden accumulation

Bearish Divergence = Price makes higher highs, CVD makes lower highs → hidden distribution

All plotted directly on bars with triangle markers.

🔸 VWAP Overlay (Optional)

→ Anchored VWAP gives immediate context for intraday bias — above VWAP = demand, below = supply

🎯 How to Use BK AK-SILENCER

🔹 Silent Reversal Detection

Bullish divergence + Power Buy bar + VWAP reclaim = sniper entry

Bearish divergence + Power Sell bar + VWAP rejection = trap confirmation

🔹 Volume-Based Entry Triggers

Look for Power Buy + $ spike after a pullback → watch for quiet reversal

Accumulation colors clustering? Institutions are likely loading silently

🔹 Institutional Trap Warnings

$ spike + red distribution bar at highs = time to exit or flip

Weakness bar below VWAP? Don’t chase the long.

🛡️ Why It Matters

✅ Clean — it integrates into price action, no separate panels

✅ Silent — tracks institutions who build without alerts or indicators

✅ Tactical — no fluff, no lag, just real-time behavior recognition

This tool is ideal for:

🔸 Scalpers reading bar-by-bar

🔸 Intraday swing traders using VWAP and structure

🔸 Professionals who need volume behavior decoded in real-time

🔸 Anyone who wants signal without clutter

🙏 Final Thoughts

This tool isn’t just about trading — it’s about tactical awareness.

🔹 Dedicated to my mentor A.K., whose wisdom runs deep in every logic tree.

🔹 Above all, I give thanks to Gd, the source of clarity, courage, and conviction.

Without Him, even the sharpest system is blind.

With Him, we execute with structure, purpose, and divine alignment.

⚡ No noise. No clutter. No delay. Just raw, silent execution.

🔥 BK AK-SILENCER — Bar-Level Volume Footprint Precision 🔥

Gd bless every step you take in this market.

Trade with clarity, move with intention. 🙏

BTC Transaction Indicator Name: "Bitcoin On-Chain Volume & Dynamic Parabolic Curve Signals"

Purpose:

This indicator is designed for Bitcoin traders and long-term holders. It combines the analysis of Bitcoin's on-chain transaction volume with price action to generate "Whale" and "Bear" signals. Additionally, it features a unique dynamic parabolic curve that acts as a visual support line, adapting its visibility based on price interaction with a key Exponential Moving Average (EMA).

Key Components:

On-Chain Volume Analysis:

Utilizes Estimated Transaction Volume (ETRAV) data from the Bitcoin blockchain.

Calculates fast and slow Simple Moving Averages (SMAs) of this volume.

Identifies volume trends (up/down) and significant volume increases/decreases.

Employs fixed thresholds (2,500,000 for low volume and 25,000,000 for high volume) to define key activity levels, similar to how historical on-chain analysis defined accumulation and distribution zones.

Price Action Analysis:

Calculates fast and slow SMAs of the price.

Detects price trends (up/down), recoveries, and declines based on these price SMAs.

"Whale" and "Bear" Signals:

Whale Signals (Buy-side): Generated when there's an upward volume trend, significant volume increase, and a downward price trend followed by price recovery. These indicate potential accumulation phases.

Bear Signals (Sell-side): Generated when there's a downward volume trend, significant volume decrease, and an upward price trend followed by price decline. These indicate potential distribution phases.

Visuals: Both types of signals are plotted as small, colored circles directly on the price chart, with corresponding text labels ("Whale," "Buy," "Bear," "Sell," "Price Recovering," "Price Declining").

Dynamic Parabolic Curve:

Concept: A green parabolic (exponential) curve that serves as a dynamic visual support line.

Activation: The curve starts drawing automatically only when the price crosses over the EMA 500 (Exponential Moving Average of 500 periods). The curve's starting point is set at a user-defined percentage below the EMA 500 value at that exact crossover point.

Visibility: The curve remains visible and continues its trajectory only as long as the price stays above the EMA 500.

Deactivation: The curve disappears instantly if the price falls below or equals the EMA 500. It will only reappear if the price crosses above the EMA 500 again.

Customization: The curve's steepness (Tasa Crecimiento Curva) and its initial distance from the EMA 500 (Inicio Curva % por debajo de EMA500) are adjustable.

Dynamic Label: A "Parabólico" text label is plotted near the center of the active curve segment, with an adjustable vertical offset to ensure it stays visually appealing below the curve.

What is PLOTTED on the chart:

The small, colored circle signals for Whale/Buy and Bear/Sell activity.

The green dynamic parabolic curve.

What is NOT PLOTTED:

EMA 200, EMA 500 lines (though they are calculated internally for logic).

Raw volume data or volume Moving Averages (these are only used for signal calculation, not plotted).

Ideal for:

Bitcoin traders and investors focused on long-term trends and cycle analysis, who want visual cues for accumulation/distribution phases based on on-chain activity, complemented by a unique, dynamically appearing parabolic support curve.

Important Notes:

Relies on the availability of external on-chain data (QUANDL:BCHAIN) within TradingView.

Functions best on a daily timeframe for optimal on-chain data relevance.

Cycle Composite 3.6 WeightedThe Cycle Composite is a multi-factor market cycle model designed to classify long-term market behavior into distinct phases using normalized and weighted data inputs.

It combines ten key on-chain, dominance, volatility, sentiment, and trend-following metrics into a single composite output. The goal is to provide a clearer understanding of where the market may stand in the broader cycle (e.g., accumulation, early bull, late bull, or euphoria).

This version (3.4) introduces flexible weighting, trend strength markers, and additional context-aware signals such as risk-on confirmations and altseason flags.

Phases Identified:

The model categorizes the market into one of five zones:

Euphoria (> 85)

Late Bull (70 – 85)

Mid Bull (50 – 70)

Early Bull (30 – 50)

Fear (< 30)

Each phase is determined by a smoothed EMA of the weighted composite score.

Data Sources and Metrics Used (10 total):

BTC Dominance (CRYPTOCAP:BTC.D)

Stablecoin Dominance (USDT + USDC average) (inverted for risk-on)

ETH Dominance (CRYPTOCAP:ETH.D)

BBWP (normalized Bollinger Band Width % over 1-year window)

WVF (Williams VIX Fix for volatility spike detection)

NUPL (Net Unrealized Profit/Loss, external source)

CMF (Chaikin Money Flow, smoothed volume accumulation)

CEX Open Interest (custom input from DAO / external source)

Whale Inflows (custom input from whale exchange transfer data)

Google Trends Average (BTC, Crypto, Altcoin terms)

All inputs are normalized over a 200-bar window and combined via weighted averaging, where each weight is user-configurable.

Additional Features:

Phase Labels: Labels are printed only when a new phase is entered.

Bull Continuation Marker: Triangle up when composite makes higher highs and NUPL increases.

Weakening Marker: Triangle down when composite rolls over in Late Bull and NUPL falls.

Risk-On Signal: Green circle appears when CMF and Google Trends are both rising.

Altseason Flag: Orange diamond appears when dominance of "others.d" exceeds BTC.D and ETH.D and composite is above 50.

Background Shading: Each phase is shaded with a semi-transparent background color.

Timeframe-Aware Display: All markers and signals are shown only on weekly timeframe for clarity.

Intended Use:

This script is intended for educational and macro-trend analysis purposes.

It can be used to:

Identify macro cycle position (accumulation, bull phases, euphoria, etc.)

Spot long-term trend continuation or weakening signals

Add context to price action with external on-chain and sentiment data

Time rotation events such as altseason risk

Disclaimer:

This script does not constitute financial advice.

It is intended for informational and research purposes only.

Users should conduct their own due diligence and analysis before making investment decisions.

BTC Growth | AlchimistOfCrypto🌈 BTC Regression Bands & Halvings – Unveiling Bitcoin's Logarithmic Growth Fields 🌈

"The Bitcoin Regression Bands, engineered through advanced logarithmic mathematics, visualizes the probabilistic distribution of Bitcoin's price evolution within a multi-cycle growth paradigm. This indicator employs principles from hyperbolic regression where decay coefficients create mathematical boundaries that define Bitcoin's long-term value progression. Our implementation features algorithmically enhanced rainbow visualization derived from extensive cycle analysis, creating a dynamic representation of Bitcoin's logarithmic growth with adaptive color gradients that highlight critical halving-based phase transitions in the asset's monetary evolution."

📊 Professional Trading Application

The Bitcoin Regression Bands transcends traditional price prediction models with a sophisticated multi-band illumination system that reveals the underlying structure of Bitcoin's monetary evolution. Scientifically calibrated across multiple halving cycles and featuring seamless rainbow visualization, it enables investors to perceive Bitcoin's position within its macro growth trajectory with unprecedented clarity.

- Visual Theming 🎨

Scientifically designed rainbow gradient optimized for cycle pattern recognition:

- Violet-Blue: Lower value accumulation zones with highest mathematical growth potential

- Green: Fair value equilibrium zone representing the regression mean

- Yellow-Orange: Moderate overvaluation regions indicating potential resistance

- Red: Statistical extreme zones indicating mathematical cycle peaks

- Halving Visualization 🔍

- Precise cycle boundaries demarcating Bitcoin's fundamental supply shock events

- Adaptive band spacing based on mathematical cycle progression

- Multiple sub-cycle markers revealing the probabilistic nature of Bitcoin's trajectory

🚀 How to Use

1. Identify Macro Position ⏰: Locate Bitcoin's current price relative to the regression bands

2. Understand Cycle Context 🎚️: Note position within the current halving cycle for time-based analysis

3. Assess Mathematical Value 🌈: Determine potential over/undervaluation based on band location

4. Adjust Investment Strategy 🔎: Modulate position sizing based on mathematical value assessment

5. Identify Cycle Phases ✅: Monitor band transitions to detect accumulation and distribution zones

6. Invest with Precision 🛡️: Utilize lower bands for strategic accumulation, upper bands for strategic reduction

7. Manage Risk Dynamically 🔐: Scale investment allocations based on mathematical cycle positioning

Money Flow Pulse💸 In markets where volatility is cheap and structure is noisy, what matters most isn’t just the move — it’s the effort behind it. Money Flow Pulse (MFP) offers a compact, color-coded readout of real-time conviction by scoring volume-weighted price action on a five-tier scale. It doesn’t try to predict reversals or validate trends. Instead, it reveals the quality of the move in progress: is it fading , driving , exhausting , or hollow ?

🎨 MFP draws from the traditional Money Flow Index (MFI), a volume-enhanced momentum oscillator, but transforms it into a modular “pressure readout” that fits seamlessly into any structural overlay. Rather than oscillating between extremes with little interpretive guidance, MFP discretizes the flow into clean, color-coded regimes ranging from strong inflow (+2) to strong outflow (–2). The result is a responsive diagnostic layer that complements, rather than competes with, tools like ATR and/or On-Balance Volume.

5️⃣ MFP uses a normalized MFI value smoothed over 13 periods and classified into a 5-tier readout of Volume-Driven Conviction :

🍆 Exhaustion Inflow — usually a top or blowoff; not strength, but overdrive (+2)

🥝 Active Inflow — supportive of trend continuation (+1)

🍋 Neutral — chop, coil, or fakeouts (0)

🍑 Selling Intent — weakening structure, possible fade setups (-1)

🍆 Exhaustion Outflow — often signals forced selling or accumulation traps (-2)

🎭 These tiers are not arbitrary. Each one is tuned to reflect real capital behavior across timeframes. For instance, while +1 may support continuation, +2 often precedes exhaustion — especially on the lower timeframes. Similarly, a –1 reading during a pullback suggests sell-side pressure is building, but a shift to –2 may mean capitulation is already underway. The difference between the two can define whether a move is tradable continuation or strategic exhaustion .

🌊 The MFI ROC (Rate of Change) feature can be toggled to become a volatility-aware pulse monitor beneath the derived MFI tier. Instead of scoring direction or structure, ROC reveals how fast conviction is changing — not just where it’s headed, but how hard it's accelerating or decaying. It measures the raw Δ between the current and previous MFI values, exposing bursts of energy, fading pressure, or transitional churn .

🎢 Visually, ROC appears as a low-opacity area fill, anchored to a shared lemon-yellow zero line. When the green swell rises, buying pressure is accelerating; when the red drops, flow is actively deteriorating. A subtle bump may signal early interest — while a steep wave hints at an emotional overreaction. The ROC value itself provides numeric insight alongside the raw MFI score. A reading of +3.50 implies strong upside momentum in the flow — often supporting trend ignition. A score of –6.00 suggests rapid deceleration or full exhaustion — often preceding reversals or failed breakouts.

・ MFI shows you where the flow is

・ ROC tells you how it’s behaving

😎 This blend reveals not just structure or intent — but also urgency . And in flow-based trading, urgency often precedes outcome.

🧩 Divergence isn’t delay — it’s disagreement . One of the most revealing features of MFP is how it exposes momentum dissonance — situations where price and flow part ways. These divergences often front-run pivots , traps , or velocity stalls . Unlike RSI-style divergence, which whispers of exhaustion, MFI divergence signals a breakdown in conviction. The structure may extend — but the effort isn’t there.

・ Price ▲ MFI ▼ → Effortless Markup : Often signals distribution or a grind into liquidity. Without rising MFI, the rally lacks true flow participation — a warning of fragility.

・ Price ▼ MFI ▲ → Absorption or Early Accumulation : Price breaks down, but money keeps flowing in — a hidden bid. Watch for MFI tier shifts or ROC bursts to confirm a reversal.

🏄♂️ These moments don’t require signal overlays or setup hunting. MFP narrates the imbalance. When price breaks structure but flow does not — or vice versa — you’re not seeing trend, you’re seeing disagreement, and that's where edge begins.

💤 MFP is especially effective on intraday charts where volume dislocations matter most. On the 1H or 15m chart, it helps distinguish between breakouts with conviction versus those lacking flow. On higher timeframes, its resolution softens — it becomes more of a drift indicator than a trigger device. That’s by design: MFP prioritizes pulse, not position. It’s not the fire, it’s the heat.

📎 Use MFP in confluence with structural overlays to validate price behavior. A ribbon expansion with rising MFP is real. A compression breakout without +1 flow is "fishy". Watch how MFP behaves near key zones like anchored VWAP, MAs or accumulation pivots. When MFP rises into a +2 and fails to sustain, the reversal isn’t just technical — it’s flow-based.

🪟 MFP doesn’t speak loudly, but it never whispers without reason. It’s the pulse check before action — the breath of the move before the breakout. While it stays visually minimal on the chart, the true power is in the often overlooked Data Window, where traders can read and interpret the score in real time. Once internalized, these values give structure-aware traders a framework for conviction, continuation, or caution.

🛜 MFP doesn’t chase momentum — it confirms conviction. And in markets defined by noise, that signal isn’t just helpful — it’s foundational.

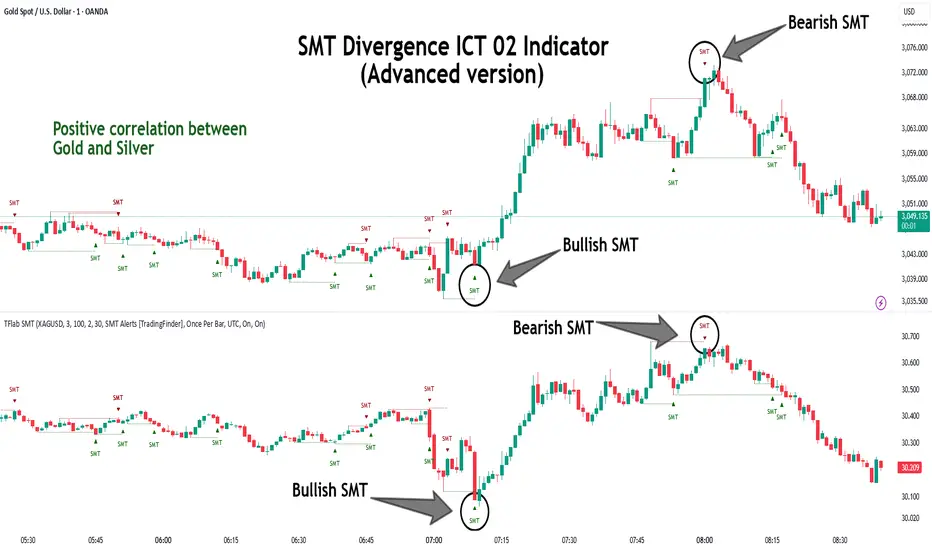

SMT Divergence ICT 02 [TradingFinder] Smart Money Technique SMC🔵 Introduction

SMT Divergence (Smart Money Technique Divergence) is a price action-based trading concept that detects discrepancies in market behavior between two assets that are generally expected to move in the same direction. Rooted in ICT (Inner Circle Trader) methodology, this approach helps traders recognize subtle signs of market manipulation or imbalance, often ahead of traditional indicators.

The core idea behind SMT divergence is simple: when two correlated instruments—such as currency pairs, indices, or assets from the same sector—start forming different swing points (highs or lows), this can reveal a lack of confirmation in the trend. Such divergence is often a precursor to a price reversal or pause in momentum.

This technique works effectively across various markets including Forex, stocks, and cryptocurrencies. It’s particularly valuable when used alongside concepts like liquidity sweeps, market structure breaks (MSBs), or order block identification.

In advanced use cases, Sequential SMT helps uncover patterns of alternating divergences across sessions, often signaling engineered liquidity traps before price reacts.

When combined with the Quarterly Theory—which segments market behavior into Accumulation, Manipulation, Distribution, and Continuation/Reversal phases—traders gain insight not only into where divergence happens, but when it's most likely to be significant within the market cycle.

Bullish SMT :

Bullish SMT Divergence occurs when one asset prints a higher low while the correlated asset forms a lower low. This asymmetry often suggests that the downside move is losing strength, hinting at a potential bullish shift.

Bearish SMT :

Bearish SMT Divergence is formed when one asset creates a higher high, while the second asset fails to confirm by printing a lower high. This typically signals weakening bullish pressure and the possibility of a reversal to the downside.

🔵 How to Use

The SMT Divergence indicator is designed to detect imbalances between two positively correlated assets—such as major currency pairs, indices, or commodities. These divergences often indicate early signs of market inefficiency or smart money manipulation and can help traders anticipate trend shifts with higher precision.

Unlike traditional divergence indicators or earlier versions of this script, this upgraded version does not rely solely on consecutive pivot comparisons. Instead, it dynamically scans all available pivots within the chart to identify divergences at any structural level—major or minor—across the price action. This broader detection method increases the reliability and frequency of meaningful SMT signals.

Moreover, when integrated with Sequential SMT logic, the indicator is capable of identifying multiple divergence sequences across sessions. These sequences often signal engineered liquidity traps and can be mapped within the Quarterly Theory framework, allowing traders to pinpoint not just the presence of divergence but also the phase of the market cycle it appears in (Accumulation, Manipulation, Distribution, or Continuation).

🟣 Bullish SMT Divergence

This signal occurs when the primary asset forms a higher low, while the correlated asset forms a lower low. This pattern implies weakening bearish momentum and a potential shift to the upside.

If the correlated asset breaks its previous low but the primary asset does not, this divergence suggests absorption of selling pressure and possible accumulation by smart money—making it a strong bullish signal, especially when aligned with a favorable market phase (e.g., the end of a manipulation phase in Q2).

🟣 Bearish SMT Divergence

This signal occurs when the primary asset creates a higher high, while the correlated asset forms a lower high. This mismatch indicates fading bullish momentum and a potential reversal to the downside.

If the correlated asset fails to confirm a breakout made by the main asset, the divergence may point to distribution or exhaustion. When seen within Q3 or Q4 phases of the Quarterly Theory, this pattern often precedes sharp declines or fake-outs engineered by smart money

🔵 Settings

⚙️ Logical Settings

Symbol : Choose the secondary asset to compare with the main chart asset (e.g., XAUUSD, US100, GBPUSD).

Pivot Period : Sets the sensitivity of the pivot detection algorithm. A smaller value increases responsiveness to price swings.

Activate Max Pivot Back : When enabled, limits the maximum number of past pivots to be considered for divergence detection.

Max Pivot Back Length : Defines how many past pivots can be used (if the above toggle is active).

Pivot Sync Threshold : The maximum allowed difference (in bars) between pivots of the two assets for them to be compared.

Validity Pivot Length : Defines the time window (in bars) during which a divergence remains valid before it's considered outdated.

🎨 Display Settings

Show Bullish SMT Line : Draws a line connecting the bullish divergence points.

Show Bullish SMT Label : Displays a label on the chart when a bullish divergence is detected.

Bullish Color : Sets the color for bullish SMT markers (label, shape, and line).

Show Bearish SMT Line : Draws a line for bearish divergence.

Show Bearish SMT Label : Displays a label when a bearish SMT divergence is found.

Bearish Color : Sets the color for bearish SMT visual elements.

🔔 Alert Settings

Alert Name : Custom name for the alert messages (used in TradingView’s alert system).

Message Frequency :

All : Every signal triggers an alert.

Once Per Bar : Alerts once per bar regardless of how many signals occur.

Per Bar Close : Only triggers when the bar closes and the signal still exists.

Time Zone Display : Choose the time zone in which alert timestamps are displayed (e.g., UTC).

Bullish SMT Divergence Alert : Enable/disable alerts specifically for bullish signals.

Bearish SMT Divergence Alert : Enable/disable alerts specifically for bearish signals

🔵Conclusion

The SMT Plus indicator offers a refined and powerful approach to detecting smart money behavior through divergence analysis between correlated assets. By removing the limitations of consecutive pivot comparisons and allowing for broader structural detection, it captures more accurate and timely signals that often precede major market moves.

When paired with frameworks like Sequential SMT and the Quarterly Theory, the indicator not only highlights where divergence occurs, but also when in the market cycle it's most likely to matter. Its flexible settings, customizable visuals, and integrated alert system make it suitable for intraday scalpers, swing traders, and even long-term macro analysts.

Whether you're using it as a standalone decision-making tool or combining it with other ICT concepts, SMT Plus gives you an edge in recognizing manipulation, timing reversals, and staying in sync with the real market narrative—not just the chart.

Composite Reversal IndicatorOverview

The "Composite Reversal Indicator" aggregates five technical signals to produce a composite score that ranges from -5 (strongly bearish) to +5 (strongly bullish). These signals come from:

Relative Strength Index (RSI)

Moving Average Convergence Divergence (MACD)

Accumulation/Distribution (A/D)

Volume relative to its moving average

Price proximity to support and resistance levels

Each signal contributes a value of +1 (bullish), -1 (bearish), or 0 (neutral) to the total score. The raw score is plotted as a histogram, and a smoothed version is plotted as a colored line to highlight trends.

Step-by-Step Explanation

1. Customizable Inputs

The indicator starts with user-defined inputs that allow traders to tweak its settings. These inputs include:

RSI: Length (e.g., 14), oversold level (e.g., 30), and overbought level (e.g., 70).

MACD: Fast length (e.g., 12), slow length (e.g., 26), and signal length (e.g., 9).

Volume: Moving average length (e.g., 20) and multipliers for high (e.g., 1.5) and low (e.g., 0.5) volume thresholds.

Price Levels: Period for support and resistance (e.g., 50) and proximity percentage (e.g., 2%).

Score Smoothing: Length for smoothing the score (e.g., 5).

These inputs make the indicator adaptable to different trading styles, assets, or timeframes.

2. Indicator Calculations

The script calculates five key indicators using the input parameters:

RSI: Measures momentum and identifies overbought or oversold conditions.

Formula: rsi = ta.rsi(close, rsi_length)

Example: With a length of 14, it analyzes the past 14 bars of closing prices.

MACD: Tracks trend and momentum using two exponential moving averages (EMAs).

Formula: = ta.macd(close, macd_fast, macd_slow, macd_signal)

Components: MACD line (fast EMA - slow EMA), signal line (EMA of MACD line).

Accumulation/Distribution (A/D): A volume-based indicator showing buying or selling pressure.

Formula: ad = ta.accdist

Reflects cumulative flow based on price and volume.

Volume Moving Average: A simple moving average (SMA) of trading volume.

Formula: vol_ma = ta.sma(volume, vol_ma_length)

Example: A 20-bar SMA smooths volume data.

Support and Resistance Levels: Key price levels based on historical lows and highs.

Formulas:

support = ta.lowest(low, price_level_period)

resistance = ta.highest(high, price_level_period)

Example: Over 50 bars, it finds the lowest low and highest high.

These calculations provide the raw data for generating signals.

3. Signal Generation

Each indicator produces a signal based on specific conditions:

RSI Signal:

+1: RSI < oversold level (e.g., < 30) → potential bullish reversal.

-1: RSI > overbought level (e.g., > 70) → potential bearish reversal.

0: Otherwise.

Logic: Extreme RSI values suggest price may reverse.

MACD Signal:

+1: MACD line > signal line → bullish momentum.

-1: MACD line < signal line → bearish momentum.

0: Equal.

Logic: Crossovers indicate trend shifts.

A/D Signal:

+1: Current A/D > previous A/D → accumulation (bullish).

-1: Current A/D < previous A/D → distribution (bearish).

0: Unchanged.

Logic: Rising A/D shows buying pressure.

Volume Signal:

+1: Volume > high threshold (e.g., 1.5 × volume MA) → strong activity (bullish).

-1: Volume < low threshold (e.g., 0.5 × volume MA) → weak activity (bearish).

0: Otherwise.

Logic: Volume spikes often confirm reversals.

Price Signal:

+1: Close near support (within proximity %, e.g., 2%) → potential bounce.

-1: Close near resistance (within proximity %) → potential rejection.

0: Otherwise.

Logic: Price near key levels signals reversal zones.

4. Composite Score

The raw composite score is the sum of the five signals:

Formula: score = rsi_signal + macd_signal + ad_signal + vol_signal + price_signal

Range: -5 (all signals bearish) to +5 (all signals bullish).

Purpose: Combines multiple perspectives into one number.

5. Smoothed Score

A smoothed version of the score reduces noise:

Formula: score_ma = ta.sma(score, score_ma_length)

Example: With a length of 5, it averages the score over 5 bars.

Purpose: Highlights the trend rather than short-term fluctuations.

6. Visualization

The indicator plots two elements:

Raw Score: A gray histogram showing the composite score per bar.

Style: plot.style_histogram

Color: Gray.

Smoothed Score: A line that changes color:

Green: Score > 0 (bullish).

Red: Score < 0 (bearish).

Gray: Score = 0 (neutral).

Style: plot.style_line, thicker line (e.g., linewidth=2).

These visuals make it easy to spot potential reversals.

How It Works Together

The indicator combines signals from:

RSI: Momentum extremes.

MACD: Trend shifts.

A/D: Buying/selling pressure.

Volume: Confirmation of moves.

Price Levels: Key reversal zones.

By summing these into a composite score, it filters out noise and provides a unified signal. A high positive score (e.g., +3 to +5) suggests a bullish reversal, while a low negative score (e.g., -3 to -5) suggests a bearish reversal. The smoothed score helps traders focus on the trend.

Practical Use

Bullish Reversal: Smoothed score is green and rising → look for buying opportunities.

Bearish Reversal: Smoothed score is red and falling → consider selling or shorting.

Neutral: Score near 0 → wait for clearer signals.

Traders can adjust inputs to suit their strategy, making it versatile for stocks, forex, or crypto.

Quarterly Theory ICT 02 [TradingFinder] True Open Session 90 Min🔵 Introduction

The Quarterly Theory ICT indicator is an advanced analytical system built on ICT (Inner Circle Trader) concepts and fractal time. It divides time into four quarters (Q1, Q2, Q3, Q4), and is designed based on the consistent repetition of these phases across all trading timeframes (annual, monthly, weekly, daily, and even shorter trading sessions).

Each cycle consists of four distinct phases: the first phase (Q1) is the Accumulation phase, characterized by price consolidation; the second phase (Q2), known as Manipulation or Judas Swing, is marked by initial false movements indicating a potential shift; the third phase (Q3) is Distribution, where price volatility peaks; and the fourth phase (Q4) is Continuation/Reversal, determining whether the previous trend continues or reverses.

🔵 How to Use

The central concept of this strategy is the "True Open," which refers to the actual starting point of each time cycle. The True Open is typically defined at the beginning of the second phase (Q2) of each cycle. Prices trading above or below the True Open serve as a benchmark for predicting the market's potential direction and guiding trading decisions.

The practical application of the Quarterly Theory strategy relies on accurately identifying True Open points across various timeframes.

True Open points are defined as follows :

Yearly Cycle :

Q1: January, February, March

Q2: April, May, June (True Open: April Monthly Open)

Q3: July, August, September

Q4: October, November, December

Monthly Cycle :

Q1: First Monday of the month

Q2: Second Monday of the month (True Open: Daily Candle Open price on the second Monday)

Q3: Third Monday of the month

Q4: Fourth Monday of the month

Weekly Cycle :

Q1: Monday

Q2: Tuesday (True Open: Daily Candle Open Price on Tuesday)

Q3: Wednesday

Q4: Thursday

Daily Cycle :

Q1: 18:00 - 00:00 (Asian session)

Q2: 00:00 - 06:00 (True Open: Start of London Session)

Q3: 06:00 - 12:00 (NY AM)

Q4: 12:00 - 18:00 (NY PM)

90 Min Asian Session :

Q1: 18:00 - 19:30

Q2: 19:30 - 21:00 (True Open at 19:30)

Q3: 21:00 - 22:30

Q4: 22:30 - 00:00

90 Min London Session :

Q1: 00:00 - 01:30

Q2: 01:30 - 03:00 (True Open at 01:30)

Q3: 03:00 - 04:30

Q4: 04:30 - 06:00

90 Min New York AM Session :

Q1: 06:00 - 07:30

Q2: 07:30 - 09:00 (True Open at 07:30)

Q3: 09:00 - 10:30

Q4: 10:30 - 12:00

90 Min New York PM Session :

Q1: 12:00 - 13:30

Q2: 13:30 - 15:00 (True Open at 13:30)

Q3: 15:00 - 16:30

Q4: 16:30 - 18:00

Micro Cycle (22.5-Minute Quarters) : Each 90-minute quarter is further divided into four 22.5-minute sub-segments (Micro Sessions).

True Opens in these sessions are defined as follows :

Asian Micro Session :

True Session Open : 19:30 - 19:52:30

London Micro Session :

T rue Session Open : 01:30 - 01:52:30

New York AM Micro Session :

True Session Open : 07:30 - 07:52:30

New York PM Micro Session :

True Session Open : 13:30 - 13:52:30

By accurately identifying these True Open points across various timeframes, traders can effectively forecast the market direction, analyze price movements in detail, and optimize their trading positions. Prices trading above or below these key levels serve as critical benchmarks for determining market direction and making informed trading decisions.

🔵 Setting

Show True Range : Enable or disable the display of the True Range on the chart, including the option to customize the color.

Extend True Range Line : Choose how to extend the True Range line on the chart, with the following options:

None: No line extension

Right: Extend the line to the right

Left: Extend the line to the left

Both: Extend the line in both directions (left and right)

Show Table : Determines whether the table—which summarizes the phases (Q1 to Q4)—is displayed.

Show More Info : Adds additional details to the table, such as the name of the phase (Accumulation, Manipulation, Distribution, or Continuation/Reversal) or further specifics about each cycle.

🔵 Conclusion

The Quarterly Theory ICT, by dividing time into four distinct quarters (Q1, Q2, Q3, and Q4) and emphasizing the concept of the True Open, provides a structured and repeatable framework for analyzing price action across multiple time frames.

The consistent repetition of phases—Accumulation, Manipulation (Judas Swing), Distribution, and Continuation/Reversal—allows traders to effectively identify recurring price patterns and critical market turning points. Utilizing the True Open as a benchmark, traders can more accurately determine potential directional bias, optimize trade entries and exits, and manage risk effectively.

By incorporating principles of ICT (Inner Circle Trader) and fractal time, this strategy enhances market forecasting accuracy across annual, monthly, weekly, daily, and shorter trading sessions. This systematic approach helps traders gain deeper insight into market structure and confidently execute informed trading decisions.

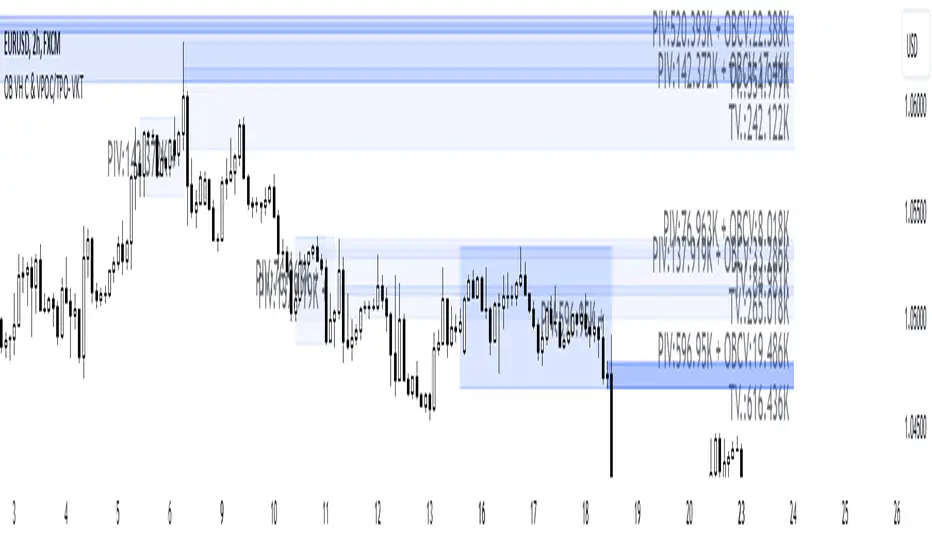

Order Blocks with Volume Heatmap & Clusters - VK TradingOrder Blocks with Volume Heatmap & Clusters - VK Trading

This script is designed to identify and highlight Order Blocks, a key concept in institutional trading, and combines it with powerful tools like volume heatmaps and accumulation clusters for enhanced market analysis. Suitable for traders of all experience levels, this script provides a clear and customizable visualization to help identify significant market zones effectively.

What Does This Script Do?

Order Block Identification: Highlights bullish and bearish order blocks directly on the chart, making it easier to spot key supply and demand zones.

Volume Heatmap: A dynamic heatmap adjusts colors based on relative volume, allowing you to quickly identify areas of heightened activity.

Institutional Accumulation Clusters: Zones of potential institutional accumulation are calculated using a combination of ATR (Average True Range), standardized volume, and RSI (Relative Strength Index).

Automatic Clearing: Invalidated order blocks are automatically removed, ensuring your charts remain clean and focused.

Key Features

Customizable Sensitivity: Adjust the script’s sensitivity to tailor order block detection to different market conditions and strategies.

Advanced Volume Display Options: Toggle volume visibility on or off. Customize the position, size, and color of volume labels for better integration with your chart's design.

Dynamic Heatmap Intensity: Fine-tune the heatmap’s intensity and color to highlight areas of interest based on trading volume.

Dual Order Block Detection: Uses two independent detection settings to analyze the market from multiple perspectives.

Visual Alerts: Automatically draws key level lines based on detected order blocks for better clarity.

User Benefits:

Clear Market Analysis: Helps pinpoint institutional activity and key levels with minimal effort.

Increased Efficiency: Automates plotting and analysis, allowing you to focus on decision-making.

Versatile Compatibility: Complements strategies like Smart Money Concepts, Wyckoff, and Price Action approaches.

Disclaimer

This script is intended as an analytical and educational tool. It does not guarantee specific outcomes or eliminate trading risks. Use this tool at your own discretion and always practice proper risk management.

Short Term Imbalance ContinuationShort Term Imbalance Continuation

This indicator identifies short-term trading opportunities based on imbalance situations followed by consolidation.

Functionality:

The indicator looks for a specific candle formation:

1. An imbalance candle where the low is above the high of the following candle (bearish) or the high is below the low of the following candle (bullish)

2. Followed by 1-2 inside candles (close within the range of the previous candle) in the same direction

Theory:

The formation is based on two important market mechanisms:

1. Imbalance and Momentum:

- The imbalance shows a strong move with one-sided orderflow dominance

- Inside candles in the same direction confirm that the opposing side cannot take control

2. Consolidation Behavior:

- Inside candles are a classic consolidation pattern

- They show that the market is "digesting" the previous strong movement

- Consolidation within the range indicates controlled accumulation/distribution

- Particularly relevant when large market participants are building or expanding positions

- Consolidation at higher/lower levels confirms the dominance of the trend direction

Settings:

- Choice between one or two inside candles for different consolidation phases

- Option whether both inside candles must have the same direction

- Customizable colors for bullish and bearish signals

Application:

The indicator is particularly suitable for:

- Trend confirmation after strong movements

- Entry into pullbacks during trends

- Identification of continuation setups after consolidations

- Detection of accumulation/distribution phases of large market participants

Notes: