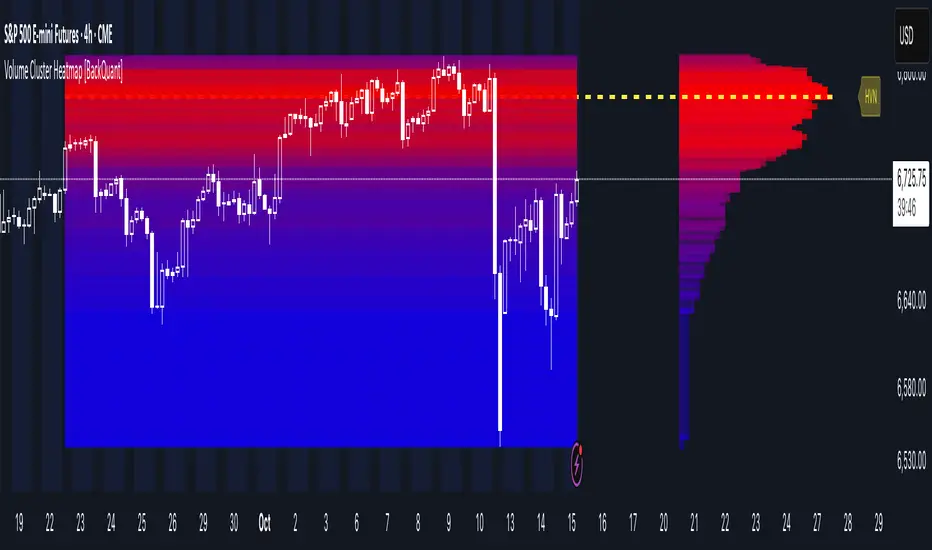

Volume Cluster Heatmap [BackQuant]Volume Cluster Heatmap

A visualization tool that maps traded volume across price levels over a chosen lookback period. It highlights where the market builds balance through heavy participation and where it moves efficiently through low-volume zones. By combining a heatmap, volume profile, and high/low volume node detection, this indicator reveals structural areas of support, resistance, and liquidity that drive price behavior.

What Are Volume Clusters?

A volume cluster is a horizontal aggregation of traded volume at specific price levels, showing where market participants concentrated their buying and selling.

High Volume Nodes (HVN) : Price levels with significant trading activity; often act as support or resistance.

Low Volume Nodes (LVN) : Price levels with little trading activity; price moves quickly through these areas, reflecting low liquidity.

Volume clusters help identify key structural zones, reveal potential reversals, and gauge market efficiency by highlighting where the market is balanced versus areas of thin liquidity.

By creating heatmaps, profiles, and highlighting high and low volume nodes (HVNs and LVNs), it allows traders to see where the market builds balance and where it moves efficiently through thin liquidity zones.

Example: Bitcoin breaking away from the high-volume zone near 118k and moving cleanly through the low-volume pocket around 113k–115k, illustrating how markets seek efficiency:

Core Features

Visual Analysis Components:

Heatmap Display : Displays volume intensity as colored boxes, lines, or a combination for a dynamic view of market participation.

Volume Profile Overlay : Shows cumulative volume per price level along the right-hand side of the chart.

HVN & LVN Labels : Marks high and low volume nodes with color-coded lines and labels.

Customizable Colors & Transparency : Adjust high and low volume colors and minimum transparency for clear differentiation.

Session Reset & Timeframe Control : Dynamically resets clusters at the start of new sessions or chosen timeframes (intraday, daily, weekly).

Alerts

HVN / LVN Alerts : Notify when price reaches a significant high or low volume node.

High Volume Zone Alerts : Trigger when price enters the top X% of cumulative volume, signaling key areas of market interest.

How It Works

Each bar’s volume is distributed proportionally across the horizontal price levels it touches. Over the lookback period, this builds a cumulative volume profile, identifying price levels with the most and least trading activity. The highest cumulative volume levels become HVNs, while the lowest are LVNs. A side volume profile shows aggregated volume per level, and a heatmap overlay visually reinforces market structure.

Applications for Traders

Identify strong support and resistance at HVNs.

Detect areas of low liquidity where price may move quickly (LVNs).

Determine market balance zones where price may consolidate.

Filter noise: because volume clusters aggregate activity into levels, minor fluctuations and irrelevant micro-moves are removed, simplifying analysis and improving strategy development.

Combine with other indicators such as VWAP, Supertrend, or CVD for higher-probability entries and exits.

Use volume clusters to anticipate price reactions to breaking points in thin liquidity zones.

Advanced Display Options

Heatmap Styles : Boxes, lines, or both. Boxes provide a traditional heatmap, lines are better for high granularity data.

Line Mode Example : Simplified line visualization for easier reading at high level counts:

Profile Width & Offset : Adjust spacing and placement of the volume profile for clarity alongside price.

Transparency Control : Lower transparency for more opaque visualization of high-volume zones.

Best Practices for Usage

Reduce the number of levels when using line mode to avoid clutter.

Use HVN and LVN markers in conjunction with volume profiles to plan entries and exits.

Apply session resets to monitor intraday vs. multi-day volume accumulation.

Combine with other technical indicators to confirm high-probability trading signals.

Watch price interactions with LVNs for potential rapid movements and with HVNs for possible support/resistance or reversals.

Technical Notes

Each bar contributes volume proportionally to the price levels it spans, creating a dynamic and accurate representation of traded interest.

Volume profiles are scaled and offset for visual clarity alongside live price.

Alerts are fully integrated for HVN/LVN interaction and high-volume zone entries.

Optimized to handle large lookback windows and numerous price levels efficiently without performance degradation.

This indicator is ideal for understanding market structure, detecting key liquidity areas, and filtering out noise to model price more accurately in high-frequency or algorithmic strategies.

Recherche dans les scripts pour "accumulation"

Volume Sampled Supertrend [BackQuant]Volume Sampled Supertrend

A Supertrend that runs on a volume sampled price series instead of fixed time. New synthetic bars are only created after sufficient traded activity, which filters out low participation noise and makes the trend much easier to read and model.

Original Script Link

This indicator is built on top of my volume sampling engine. See the base implementation here:

Why Volume Sampling

Traditional charts print a bar every N minutes regardless of how active the tape is. During quiet periods you accumulate many small, low information bars that add noise and whipsaws to downstream signals.

Volume sampling replaces the clock with participation. A new synthetic bar is created only when a pre-set amount of volume accumulates (or, in Dollar Bars mode, when pricevolume reaches a dollar threshold). The result is a non-uniform time series that stretches in busy regimes and compresses in quiet regimes. This naturally:

filters dead time by skipping low volume chop;

standardizes the information content per bar, improving comparability across regimes;

stabilizes volatility estimates used inside banded indicators;

gives trend and breakout logic cleaner state transitions with fewer micro flips.

What this tool does

It builds a synthetic OHLCV stream from volume based buckets and then applies a Supertrend to that synthetic price. You are effectively running Supertrend on a participation clock rather than a wall clock.

Core Features

Sampling Engine - Choose Volume buckets or Dollar Bars . Thresholds can be dynamic from a rolling mean or median, or fixed by the user.

Synthetic Candles - Plots the volume sampled OHLC candles so you can visually compare against regular time candles.

Supertrend on Synthetic Price - ATR bands and direction are computed on the sampled series, not on time bars.

Adaptive Coloring - Candle colors can reflect side, intensity by volume, or a neutral scheme.

Research Panels - Table shows total samples, current bucket fill, threshold, bars-per-sample, and synthetic return stats.

Alerts - Long and Short triggers on Supertrend direction flips for the synthetic series.

How it works

Sampling

Pick Sampling Method = Volume or Dollar Bars.

Set the dynamic threshold via Rolling Lookback and Filter (Mean or Median), or enable Use Fixed and type a constant.

The script accumulates volume (or pricevolume) each time bar. When the bucket reaches the threshold, it finalizes one or more synthetic candles and resets accumulation.

Each synthetic candle stores its own OHLCV and is appended to the synthetic series used for all downstream logic.

Supertrend on the sampled stream

Choose Supertrend Source (Open, High, Low, Close, HLC3, HL2, OHLC4, HLCC4) derived from the synthetic candle.

Compute ATR over the synthetic series with ATR Period , then form upperBand = src + factorATR and lowerBand = src - factorATR .

Apply classic trailing band and direction rules to produce Supertrend and trend state.

Because bars only come when there is sufficient participation, band touches and flips tend to align with meaningful pushes, not idle prints.

Reading the display

Synthetic Volume Bars - The non-uniform candles that represent equal information buckets. Expect more candles during active sessions and fewer during lulls.

Volume Sampled Supertrend - The main line. Green when Trend is 1, red when Trend is -1.

Markers - Small dots appear when a new synthetic sample is created, useful for aligning activity cycles.

Time Bars Overlay (optional) - Plot regular time candles to compare how the synthetic stream compresses quiet chop.

Settings you will use most

Data Settings

Sampling Method - Volume or Dollar Bars.

Rolling Lookback and Filter - Controls the dynamic threshold. Median is robust to outliers, Mean is smoother.

Use Fixed and Fixed Threshold - Force a constant bucket size for consistent sampling across regimes.

Max Stored Samples - Ring buffer limit for performance.

Indicator Settings

SMA over last N samples - A moving average computed on the synthetic close series. Can be hidden for a cleaner layout.

Supertrend Source - Price field from the synthetic candle.

ATR Period and Factor - Standard Supertrend controls applied on the synthetic series.

Visuals and UI

Show Synthetic Bars - Turn synthetic candles on or off.

Candle Color Mode - Green/Red, Volume Intensity, Neutral, or Adaptive.

Mark new samples - Puts a dot when a bucket closes.

Show Time Bars - Overlay regular candles for comparison.

Paint candles according to Trend - Colors chart candles using current synthetic Supertrend direction.

Line Width , Colors , and Stats Table toggles.

Some workflow notes:

Trend Following

Set Sampling Method = Volume, Filter = Median, and a reasonable Rolling Lookback so busy regimes produce more samples.

Trade in the direction of the Volume Sampled Supertrend. Because flips require real participation, you tend to avoid micro whipsaws seen on time bars.

Use the synthetic SMA as a bias rail and trailing reference for partials or re-entries.

Breakout and Continuation

Watch for rapid clustering of new sample markers and a clean flip of the synthetic Supertrend.

The compression of quiet time and expansion in busy bursts often makes breakouts more legible than on uniform time charts.

Mean Reversion

In instruments that oscillate, faded moves against the synthetic Supertrend are easier to time when the bucket cadence slows and Supertrend flattens.

Combine with the synthetic SMA and return statistics in the table for sizing and expectation setting.

Stats table (top right)

Method and Total Samples - Sampling regime and current synthetic history length.

Current Vol or Dollar and Threshold - Live bucket fill versus the trigger.

Bars in Bucket and Avg Bars per Sample - How much time data each synthetic bar tends to compress.

Avg Return and Return StdDev - Simple research metrics over synthetic close-to-close changes.

Why this reduces noise

Time based bars treat a 5 minute print with 1 percent of average participation the same as one with 300 percent. Volume sampling equalizes bar information content. By advancing the bar only when sufficient activity occurs, you skip low quality intervals that add variance but little signal. For banded systems like Supertrend, this often means fewer false flips and cleaner runs.

Notes and tips

Use Dollar Bars on assets where nominal price varies widely over time or across symbols.

Median filter can resist single burst outliers when setting dynamic thresholds.

If you need a stable research baseline, set Use Fixed and keep the threshold constant across tests.

Enable Show Time Bars occasionally to sanity check what the synthetic stream is compressing or stretching.

Link again for reference

Original Volume Based Sampling engine:

Bottom line

When you let participation set the clock, your Supertrend reacts to meaningful flow instead of idle prints. The result is a cleaner state machine, fewer micro whipsaws, and a trend read that respects when the market is actually trading.

Crypto Exchange PremiumDescription: Crypto Exchange Premium

The Crypto Exchange Premium indicator is designed to quantify and visualize price disparities between different types of crypto markets — specifically between spot and perpetual futures markets, or between any two customizable sources of price data. By consolidating live data from multiple major exchanges, it creates a unified, cross-market measure of premium (or discount), helping traders identify institutional activity (i. e. by comparing exchanges with high institutional activity against others), arbitrage opportunities, and shifts in market sentiment before they become visible in price action alone.

Concept and Purpose

In cryptocurrency markets, price divergence between spot and perpetual pairs reflects the real-time interaction of demand and liquidity across market segments.

When perpetual prices trade above spot, it implies aggressive long positioning or bullish leverage (positive funding expectations).

Conversely, when spot trades above perps, it may reflect net selling pressure in futures or strong spot accumulation.

Unlike most tools that rely on funding rates or open interest alone, this indicator measures the actual traded price spread dynamically across exchanges. This allows traders to visualize the “premium curve” of the crypto market in a clear, data-driven format.

How It Works

The indicator aggregates real-time prices from a wide selection of exchanges, normalizes them into groups, and computes the difference (“premium”) between two chosen reference markets.

1. Exchange Aggregation:

Users can toggle individual exchanges for both spot and perpetual aggregation groups.

The script automatically calculates group averages by dividing the sum of all enabled exchange prices by the number of valid feeds.

Non-USD exchanges (e.g., KRW pairs on Upbit or Bithumb) are automatically converted into USD using live FX data (USDKRW) for accurate normalization.

2. Flexible Comparison Logic:

Each leg of the comparison (First vs. Second Source) can be chosen as one of:

Local chart symbol

Custom symbol

Aggregated Spot group

Aggregated Perpetual group

This allows users to compare, for example:

Binance Spot vs. Global Perp Average

Coinbase Spot vs. Binance Perp

BTCUSD vs. BTCUSDT.P (or any cross-exchange combination)

3. Premium Calculation:

The final value is computed as:

Premium = First Source Price − Second Source Price

and is plotted as a histogram (positive = green, negative = red). This visual instantly shows whether the first source trades at a premium or discount relative to the second.

How to Use

Select Data Sources:

Configure the “First Symbol” and “Second Symbol” in the settings. For most use cases:

First Symbol → Perps (Aggregated)

Second Symbol → Spot (Aggregated)

Adjust Exchange Selection:

Enable or disable individual exchanges to fine-tune your data set. For instance, disabling Korean exchanges filters out regional FX distortions.

Originality and Value

While many exchange difference or “premium indicators” track one or two exchanges, this script introduces multi-exchange aggregation, cross-market normalization, and user-configurable pairing, resulting in a more holistic and accurate reflection of market structure.

It bridges a gap between macro market breadth and microstructural price dynamics, empowering traders to:

Detect arbitrage inefficiencies between spot and perps.

Track regional price dislocations (USD vs. KRW).

Gauge the intensity of speculative leverage over time.

Anticipate funding rate shifts and liquidation clusters before they happen.

Volume Candle Rings [CHE]Volume Candle Rings – Spot Volume Extremes Fast 🔍

Marks exceptionally high volume right on the candle as concentric rings. Instantly see how extreme the spike is (levels 1–10), where it happens (anchor on HL2/Close/BodyMid), and how big it is relative to volatility (ATR-scaled). No magic, no blind signals—just clean context for better decisions.

Why it helps 🎯

Catch true extremes: Positive-side Z-Score maps spikes into 10 levels. By default, only 8/9/10 show—the ones that matter.

Context over clutter: Rings sit on the candle, scale with ATR (market regime), and widen in bars (time). Read absorption, breakout thrusts, or capitulation in context.

Signal the new, not the noise: Optional OFF→ON only drawing cuts chart noise and highlights fresh events.

How it works ⚙️

Z-Score: `z = (Vol – SMA(Vol, lookback)) / StDev(Vol, lookback)` → clipped at `zScoreCap`, normalized, and binned to 1..10 (0 = none). Only z > 0 counts.

Geometry: Vertical diameter = `Level × ATR(atrLength) × atrPerLevel`; horizontal radius = `Level × xBarsPerLevel` bars; curvatureFactor controls roundness.

Anchor: Choose HL2, Close, or BodyMid for the vertical center.

Performance: Keeps up to maxStoredCircles; FIFO cleanup to stay smooth.

Typical use cases 📈

Breakout confirmation: Clusters of 8–10 at range edges → rising initiative.

Absorption / fade: Extreme ring (9–10) without follow-through → potential stall or reversal.

Blow-off / climax: Single huge ring after a long run → higher odds of mean reversion.

News filtering: Show the real outliers, not every minor bump.

Inputs (mapped 1:1) 🧩

Z-Score & Levels

Lookback (SMA/StDev) – default 200

Z-Score Clipping – default 5.0

Behavior

Draw every bar – default ON; OFF = only on OFF→ON switches

Max circles to retain – default 120

Anchoring & Geometry

Anchor on candle – HL2 / Close / BodyMid

ATR Length – default 50

ATR per Level (Y) – default 0.25

Bars per Level (X) – default 0.15

Circle curvature – default 0.70

Level Selection (1–10)

Default: 8/9/10 ON, 1–7 OFF. Colors grade from teal/green → orange → red; fill opacity separate.

Quick presets ⏱️

Intraday (1–5m): Lookback 150–250, Cap 4.0–5.0, ATR/Level 0.20–0.30, Bars/Level 0.10–0.20, Draw every bar OFF.

Swing (1H–1D): Lookback 200–300, Cap 5.0, ATR/Level 0.25–0.35, Bars/Level 0.15–0.25, keep 8–10.

Aggressive scouting: Also enable Level 7 for early accumulation.

Pro tips 💡

Control object load: Reduce maxStoredCircles or switch Draw every bar OFF on busy charts.

Seek confluence: Combine rings with S/R, range edges, VWAP, session H/L. A ring is information, not an entry by itself.

Color discipline: Reserve red (9/10) for true extremes; keep lower levels subtle.

Limits & notes 🧭

This is visualization, not alerts or auto signals.

Many polylines can slow charts—tune Behavior settings.

Works across markets/timeframes; adapt parameters to the asset’s character.

Who it’s for 🙌

Traders who read volume in price context—breakouts, fades, reversals. See when the market is truly stepping on the gas.

Volume Candle Rings \ turns raw volume into precise, scale-aware markers. Spot extremes faster, avoid confusing “loud” with “important,” and make cleaner, context-driven decisions. 🚀

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

Primitive Delta DivergencePrimitive Delta Divergence

This indicator detects volume-price divergences by analyzing the relationship between price direction and volume bias over a rolling lookback period, revealing potential momentum shifts before they become apparent in price action alone.

Instead of relying solely on price movements, you can identify moments when volume sentiment contradicts price direction — a core concept borrowed from footprint chart analysis, adapted for traditional bar charts.

For example, when price moves higher but volume is predominantly bearish, or when price declines while volume shows bullish accumulation.

🔹 How it works

Lookback Period (n) → defines the rolling window for analyzing price and volume relationships

Creates a "meta-candle" from the lookback period, comparing its open vs. close for price bias

Volume classification → separates each bar's volume into bullish (green candles), bearish (red candles), or neutral (doji candles)

Volume bias calculation → generates a continuous score (-1 to +1) representing the directional volume pressure

Plots divergence signals when price direction and volume bias disagree

🔹 Use cases

Spot early momentum exhaustion when price and volume move in opposite directions

Identify potential reversal zones where volume suggests underlying weakness or strength

Enhance entry/exit timing by incorporating volume-based confirmation alongside price action

Apply footprint-style analysis to any timeframe without specialized charting tools

✨ Primitive Delta Divergence reveals the hidden story volume tells about price, uncovering divergences that traditional indicators might miss.

Up/Down Volume with Table (High Contrast)Up/Down Volume with Table (High Contrast) — Script Summary & User Guide

Purpose of the Script

This TradingView indicator, Up/Down Volume with Table (High Contrast), visually separates and quantifies up-volume and down-volume for each bar, providing both a color-coded histogram and a dynamic table summarizing the last five bars. The indicator helps traders quickly assess buying and selling pressure, recent volume shifts, and their relationship to price changes, all in a highly readable format.

Key Features

Up/Down Volume Columns:

Green columns represent volume on bars where price closed higher than the previous bar (up volume).

Red columns represent volume on bars where price closed lower than the previous bar (down volume).

Delta Line:

Plots the net difference between up and down volume for each bar.

Green when up-volume exceeds down-volume; red when down-volume dominates.

Interactive Table:

Displays the last five bars, showing up-volume, down-volume, delta, and close price.

Color-coding for quick interpretation.

Table position, decimal places, and timeframe are all user-configurable.

Custom Timeframe Support:

Calculate all values on the chart’s timeframe or a custom timeframe of your choice (e.g., daily, hourly).

High-Contrast Design:

Table and plot colors are chosen for maximum clarity and accessibility.

User Inputs & Configuration

Use custom timeframe:

Toggle between the chart’s timeframe and a user-specified timeframe.

Custom timeframe:

Set the timeframe for calculations if custom mode is enabled (e.g., "D" for daily, "60" for 60 minutes).

Decimal Places:

Choose how many decimal places to display in the table.

Table Location:

Select where the table appears on your chart (e.g., Bottom Right, Top Left, etc.).

How to Use

Add the Script to Your Chart:

Copy and paste the code into a new Pine Script indicator on TradingView.

Add the indicator to your chart.

Configure Inputs:

Open the indicator settings.

Adjust the timeframe, decimal places, and table location as desired.

Read the Table:

The table appears on your chart (location is user-selectable) and displays the following for the last five bars:

Bar: "Now" for the current bar, then "Bar -1", "Bar -2", etc. for previous bars.

Up Vol: Volume on bars where price closed higher than previous bar, shown in black text.

Down Vol: Volume on bars where price closed lower than previous bar, shown in black text.

Delta: Up Vol minus Down Vol, colored green for positive, red for negative, black for zero.

Close: Closing price for each bar, colored green if price increased from previous bar, red if decreased, black if unchanged.

Interpret the Histogram and Lines:

Green Columns:

Represent up-volume. Tall columns indicate strong buying volume.

Red Columns:

Represent down-volume. Tall columns indicate strong selling volume.

Delta Line:

Plotted as a line (not a column), colored green for positive values (more up-volume), red for negative (more down-volume).

Large positive or negative spikes may indicate strong buying or selling pressure, respectively.

How to Interpret the Table

Column Meaning Color Coding

Bar "Now" (current bar), "Bar -1" (previous bar), etc. Black text

Up Vol Volume for bars with higher closes than previous bar Black text

Down Vol Volume for bars with lower closes than previous bar Black text

Delta Up Vol - Down Vol. Green if positive, red if negative, black if zero Green/Red/Black

Close Closing price for the bar. Green if price increased, red if decreased, black if unchanged Green/Red/Black

Green Delta: Indicates net buying pressure for that bar.

Red Delta: Indicates net selling pressure for that bar.

Close Price Color:

Green: Price increased from previous bar.

Red: Price decreased.

Black: No change.

Practical Trading Insights

Consistently Green Delta (Histogram & Table):

Sustained buying pressure; may indicate bullish sentiment or accumulation.

Consistently Red Delta:

Sustained selling pressure; may indicate bearish sentiment or distribution.

Large Up/Down Volume Spikes:

Big green or red columns can signal strong market activity or potential reversals if they occur at trend extremes.

Delta Flipping Colors:

Rapid alternation between green and red deltas may indicate a choppy or indecisive market.

Close Price Color in Table:

Use as a quick confirmation of whether volume surges are pushing price in the expected direction.

Troubleshooting & Notes

No Volume Data Error:

If your symbol doesn’t provide volume data (e.g., some indices or synthetic assets), the script will display an error.

Custom Timeframe:

If using a custom timeframe, ensure your chart supports it and that there is enough data for meaningful calculations.

High-Contrast Table:

Designed for clarity and accessibility, but you can adjust colors in the code if needed for your personal preferences.

Summary Table Legend

Bar Up Vol Down Vol Delta Close

Now ... ... ... ...

Bar-1 ... ... ... ...

... ... ... ... ...

Colors reflect the meaning as described above.

In Summary

This indicator visually and numerically breaks down buying and selling volume, helping you spot shifts in market sentiment, volume surges, and price/volume divergences at a glance.

Use the table for precise recent data, the histogram for overall flow, and the color cues for instant market context.

SIP Evaluator and Screener [Trendoscope®]The SIP Evaluator and Screener is a Pine Script indicator designed for TradingView to calculate and visualize Systematic Investment Plan (SIP) returns across multiple investment instruments. It is tailored for use in TradingView's screener, enabling users to evaluate SIP performance for various assets efficiently.

🎲 How SIP Works

A Systematic Investment Plan (SIP) is an investment strategy where a fixed amount is invested at regular intervals (e.g., monthly or weekly) into a financial instrument, such as stocks, mutual funds, or ETFs. The goal is to build wealth over time by leveraging the power of compounding and mitigating the impact of market volatility through disciplined, consistent investing. Here’s a breakdown of how SIPs function:

Regular Investments : In an SIP, an investor commits to investing a fixed sum at predefined intervals, regardless of market conditions. This consistency helps inculcate a habit of saving and investing.

Cost Averaging : By investing a fixed amount regularly, investors purchase more units when prices are low and fewer units when prices are high. This approach, known as dollar-cost averaging, reduces the average cost per unit over time and mitigates the risk of investing a large amount at a peak price.

Compounding Benefits : Returns generated from the invested amount (e.g., capital gains or dividends) are reinvested, leading to exponential growth over the long term. The longer the investment horizon, the greater the potential for compounding to amplify returns.

Dividend Reinvestment : In some SIPs, dividends received from the underlying asset can be reinvested to purchase additional units, further enhancing returns. Taxes on dividends, if applicable, may reduce the reinvested amount.

Flexibility and Accessibility : SIPs allow investors to start with small amounts, making them accessible to a wide range of individuals. They also offer flexibility in terms of investment frequency and the ability to adjust or pause contributions.

In the context of the SIP Evaluator and Screener , the script simulates an SIP by calculating the number of units purchased with each fixed investment, factoring in commissions, dividends, taxes and the chosen price reference (e.g., open, close, or average prices). It tracks the cumulative investment, equity value, and dividends over time, providing a clear picture of how an SIP would perform for a given instrument. This helps users understand the impact of regular investing and make informed decisions when comparing different assets in TradingView’s screener. It offers insights into key metrics such as total invested amount, dividends received, equity value, and the number of installments, making it a valuable resource for investors and traders interested in understanding long-term investment outcomes.

🎲 Key Features

Customizable Investment Parameters: Users can define the recurring investment amount, price reference (e.g., open, close, HL2, HLC3, OHLC4), and whether fractional quantities are allowed.

Commission Handling: Supports both fixed and percentage-based commission types, adjusting calculations accordingly.

Dividend Reinvestment: Optionally reinvests dividends after a user-specified period, with the ability to apply tax on dividends.

Time-Bound Analysis: Allows users to set a start year for the analysis, enabling historical performance evaluation.

Flexible Dividend Periods: Dividends can be evaluated based on bars, days, weeks, or months.

Visual Outputs: Plots key metrics like total invested amount, dividends, equity value, and remainder, with customizable display options for clarity in the data window and chart.

🎲 Using the script as an indicator on Tradingview Supercharts

In order to use the indicator on charts, do the following.

Load the instrument of your choice - Preferably a stable stocks, ETFs.

Chose monthly timeframe as lower timeframes are insignificant in this type of investment strategy

Load the indicator SIP Evaluator and Screener and set the input parameters as per your preference.

Indicator plots, investment value, dividends and equity on the chart.

🎲 Visualizations

Installments : Displays the number of SIP installments (gray line, visible in the data window).

Invested Amount : Shows the cumulative amount invested, excluding reinvested dividends (blue area plot).

Dividends : Tracks total dividends received (green area plot).

Equity : Represents the current market value of the investment based on the closing price (purple area plot).

Remainder : Indicates any uninvested cash after each installment (gray line, visible in the data window).

🎲 Deep dive into the settings

The SIP Evaluator and Screener offers a range of customizable settings to tailor the Systematic Investment Plan (SIP) simulation to your preferences. Below is an explanation of each setting, its purpose, and how it impacts the analysis:

🎯 Duration

Start Year (Default: 2020) : Specifies the year from which the SIP calculations begin. When Start Year is enabled via the timebound option, the script only considers data from the specified year onward. This is useful for analyzing historical SIP performance over a defined period. If disabled, the script uses all available data.

Timebound (Default: False) : A toggle to enable or disable the Start Year restriction. When set to False, the SIP calculation starts from the earliest available data for the instrument.

🎯 Investment

Recurring Investment (Default: 1000.0) : The fixed amount invested in each SIP installment (e.g., $1000 per period). This represents the regular contribution to the SIP and directly influences the total invested amount and quantity purchased.

Allow Fractional Qty (Default: True) : When enabled, the script allows the purchase of fractional units (e.g., 2.35 shares). If disabled, only whole units are purchased (e.g., 2 shares), with any remaining funds carried forward as Remainder. This setting impacts the precision of investment allocation.

Price Reference (Default: OPEN): Determines the price used for purchasing units in each SIP installment. Options include:

OPEN : Uses the opening price of the bar.

CLOSE : Uses the closing price of the bar.

HL2 : Uses the average of the high and low prices.

HLC3 : Uses the average of the high, low, and close prices.

OHLC4 : Uses the average of the open, high, low, and close prices. This setting affects the cost basis of each purchase and, consequently, the total quantity and equity value.

🎯 Commission

Commission (Default: 3) : The commission charged per SIP installment, expressed as either a fixed amount (e.g., $3) or a percentage (e.g., 3% of the investment). This reduces the amount available for purchasing units.

Commission Type (Default: Fixed) : Specifies how the commission is calculated:

Fixed ($) : A flat fee is deducted per installment (e.g., $3).

Percentage (%) : A percentage of the investment amount is deducted as commission (e.g., 3% of $1000 = $30). This setting affects the net amount invested and the overall cost of the SIP.

🎯 Dividends

Apply Tax On Dividends (Default: False) : When enabled, a tax is applied to dividends before they are reinvested or recorded. The tax rate is set via the Dividend Tax setting.

Dividend Tax (Default: 47) : The percentage of tax deducted from dividends if Apply Tax On Dividends is enabled (e.g., 47% tax reduces a $100 dividend to $53). This reduces the amount available for reinvestment or accumulation.

Reinvest Dividends After (Default: True, 2) : When enabled, dividends received are reinvested to purchase additional units after a specified period (e.g., 2 units of time, defined by Dividends Availability). If disabled, dividends are tracked but not reinvested. Reinvestment increases the total quantity and equity over time.

Dividends Availability (Default: Bars) : Defines the time unit for evaluating when dividends are available for reinvestment. Options include:

Bars : Based on the number of chart bars.

Weeks : Based on weeks.

Months : Based on months (approximated as 30.5 days). This setting determines the timing of dividend reinvestment relative to the Reinvest Dividends After period.

🎯 How Settings Interact

These settings work together to simulate a realistic SIP. For example, a $1000 recurring investment with a 3% commission and fractional quantities enabled will calculate the number of units purchased at the chosen price reference after deducting the commission. If dividends are reinvested after 2 months with a 47% tax, the script fetches dividend data, applies the tax, and adds the net dividend to the investment amount for that period. The Start Year and Timebound settings ensure the analysis aligns with the desired timeframe, while the Dividends Availability setting fine-tunes dividend reinvestment timing.

By adjusting these settings, users can model different SIP scenarios, compare performance across instruments in TradingView’s screener, and gain insights into how commissions, dividends, and price references impact long-term returns.

🎲 Using the script with Pine Screener

The main purpose of developing this script is to use it with Tradingview Pine Screener so that multiple ETFs/Funds can be compared.

In order to use this as a screener, the following things needs to be done.

Add SIP Evaluator and Screener to your favourites (Required for it to be added in pine screener)

Create a watch list containing required instruments to compare

Open pine screener from Tradingview main menu Products -> Screeners -> Pine or simply load the URL - www.tradingview.com

Select the watchlist created from Watchlist dropdown.

Chose the SIP Evaluator and Screener from the "Choose Indicator" dropdown

Set timeframe to 1 month and update settings as required.

Press scan to display collected data on the screener.

🎲 Use Case

This indicator is ideal for educational purposes, allowing users to experiment with SIP strategies across different instruments. It can be applied in TradingView’s screener to compare SIP performance for stocks, ETFs, or other assets, helping users understand how factors like commissions, dividends, and price references impact returns over time.

Market Matrix ViewThis technical indicator is designed to provide traders with a quick and integrated view of market dynamics by combining several popular indicators into a single tool. It's not a magic bullet, but a practical aid for analyzing buying/selling pressure, trends, volume, and divergences, saving you time in the decision-making process. Built for flexibility, the indicator adapts to various trading styles (scalping, swing, or long-term) and offers customizable settings to suit your needs.

🟡 Multi-Timeframe Trends

➤ This section displays the trend direction (bullish, bearish, or neutral) across 15-minute, 1-hour, 4-hour, and Daily timeframes, providing multi-timeframe market context. Timeframes lower than the one currently selected will show "N/A."

➤It utilizes fast and slow Exponential Moving Averages (EMAs) for each timeframe:

15m: Fast EMA 42, Slow EMA 170

1h: Fast EMA 40, Slow EMA 100

4h: Fast EMA 36, Slow EMA 107

Daily: Fast EMA 20, Slow EMA 60

🟡 Smart Flow & RVOL

➤ This section displays "Buying Pressure" or "Selling Pressure" signals based on indicator confluence, alongside volume activity ("High Activity," "Normal Activity," or "Low Activity").

➤ Smart Flow combines Chaikin Money Flow (CMF) and Money Flow Index (MFI) to detect buying/selling pressure. CMF measures money flow based on price position within the high-low range, while MFI analyzes money flow considering typical price and volume. A signal is generated only when both indicators simultaneously increase/decrease beyond an adjustable threshold ("Buy/Sell Sensitivity") and volume exceeds a Simple Moving Average (SMA) scaled by the "Volume Multiplier."

➤ RVOL (Relative Volume) calculates relative volume separately for bullish and bearish candles, comparing recent volume (fast SMA) with a reference volume (slow SMA). Thresholds are adjusted based on the selected mode.

🟡 ADX & RSI

This section displays trend strength ("Strong," "Moderate," or "Weak"), its direction ("Bullish" or "Bearish"), and the RSI momentum status ("Overbought," "Oversold," "Buy/Sell Momentum," or "Neutral").

➤ ADX (Average Directional Index) measures trend strength (above 40 = "Strong," 20–40 = "Moderate," below 20 = "Weak"). Direction is determined by comparing +DI (upward movement) with -DI (downward movement). Additionally, an arrow indicates whether the trend's strength is decreasing or increasing.

➤RSI (Relative Strength Index) evaluates price momentum. Extreme levels (above 80/85 = "Overbought," below 15/20 = "Oversold") and intermediate zones (47–53 = "Neutral," above 53 = "Buy Momentum," below 47 = "Sell Momentum") are adjusted based on the selected mode.

🟡 When these signals are active for a potential trade setup, the table's background lights up green or red, respectively.

🟡 Volume Spikes

➤This feature highlights bars with significantly higher volume than the recent average, coloring them yellow on the chart to draw attention to intense market activity.

➤It uses the Z-Score method to detect volume anomalies. Current volume is compared to a 10-bar Simple Moving Average (SMA) and the standard deviation of volume over the same period. If the Z-Score exceeds a certain threshold, the bar is marked as a volume spike.

🟡 Divergences (Volume Divergence Detection)

➤ This feature marks divergences between price and technical indicators on the chart, using diamond-shaped labels (green for bullish divergences, red for bearish divergences) to signal potential trend reversals.

➤ It compares price deviations from a Simple Moving Average (SMA) with deviations of three indicators: Chaikin Money Flow (CMF), Money Flow Index (MFI), and On-Balance Volume (OBV). A bullish divergence occurs when price falls below its average, but CMF, MFI, and OBV rise above their averages, indicating hidden accumulation. A bearish divergence occurs when price rises above its average, but CMF, MFI, and OBV fall, suggesting distribution. The length of the moving averages is adjustable (default 13/10/5 bars for Scalping/Balanced/Swing), and detection thresholds are scaled by "Divergence Sensitivity" (default 1.0).

🟡 Adaptive Stop-Loss (ATR)

➤Draws dynamic stop-loss lines (red, dashed) on the chart for buy or sell signals, helping traders manage risk.Uses the Average True Range (ATR) to calculate stop-loss levels, set at low/high ± ATR × multiplier

🟡 Alerts for trend direction changes in the Info Panel:

➤ Triggers notifications when the trend shifts to Bullish (when +DI crosses above -DI) or Bearish (when +DI crosses below -DI), helping you stay informed about key market shifts.

How to use: Set alerts in Trading View for “Trend Changed to Bullish” or “Trend Changed to Bearish” with “Once Per Bar Close” for reliable signals.

🟡 Settings (Inputs)

➤ The indicator offers customizable settings to fit your trading style, but it's already optimized for Scalping (1m–15m), Balanced (16m–3h59m), and Swing (4h–Daily) modes, which automatically adjust based on the selected timeframe. The visible inputs allow you to adjust the following parameters:

Show Info Panel: Enables/disables the information panel (default: enabled).

Show Volume Spikes: Turns on/off coloring for volume spike bars (default: enabled).

Spike Sensitivity: Controls the Z-Score threshold for detecting volume spikes (default: 2.0; lower values increase signal frequency).

Show Divergence: Enables/disables the display of divergence labels (default: enabled).

Divergence Sensitivity: Adjusts the thresholds for divergence detection (default: 1.0; higher values reduce sensitivity).

Divergence Lookback Length: Sets the length of the moving averages used for divergences (default: 5, automatically adjusted to 13/10/5 for Scalping/Balanced/Swing).

RVOL Reference Period: Defines the reference period for relative volume (default: 20, automatically adjusted to 7/15/20).

RSI Length: Sets the RSI length (default: 14, automatically adjusted to 5/10/14).

Buy Sensitivity: Controls the increase threshold for Buying Pressure signals (default: 0.007; higher values reduce frequency).

Sell Sensitivity: Controls the decrease threshold for Selling Pressure signals (default: 0.007; higher values reduce frequency).

Volume Multiplier (B/S Pressure): Adjusts the volume threshold for Smart Flow signals (default: 0.6; higher values require greater volume).

🟡 This indicator is created to simplify market analysis, but I am not a professional in Pine Script or technical indicators. This indicator is not a standalone solution. For optimal results, it must be integrated into a well-defined trading strategy that includes risk management and other confirmations.

Cumulative Volume Delta📊 Indicator Name:

Cumulative Volume Delta (CVD) + Candle Divergence (Color DIfference)

📌 Purpose:

This indicator visualizes volume delta over a user-defined time anchor and highlights divergence between volume-based momentum and price movement. It's especially useful for identifying potential reversals, fakeouts, or hidden buying/selling pressure.

🔍 How It Works:

1. Volume Delta Calculation (CVD Candles):

The script uses ta.requestVolumeDelta() to approximate volume delta data over a chosen anchor period (e.g., 1D).

Volume delta = Buy Volume – Sell Volume

Each candle on the CVD chart represents changes in cumulative volume delta, with OHLC-style values:

openVolume: cumulative delta at the start of the bar

lastVolume: cumulative delta at the end of the bar

maxVolume, minVolume: intra-bar high and low

2. Visual Representation (CVD Candles):

Green/Teal candle: Delta is increasing (buying pressure dominates)

Red candle: Delta is decreasing (selling pressure dominates)

3. Divergence Detection:

The script compares the direction of the price candle with the direction of the CVD candle:

Price Up + CVD Down → Possible hidden selling (bearish divergence)

Price Down + CVD Up → Possible hidden buying (bullish divergence)

4. Color Highlighting:

Orange candle on the CVD chart signals divergence between price and volume delta.

This color override helps you quickly spot potential discrepancies between price movement and underlying volume pressure.

5. Alerting:

An alertcondition is added so you can receive a notification whenever a divergence occurs.

⚙️ User Inputs:

Anchor period (e.g., 1D): Timeframe over which the CVD is anchored.

Use custom timeframe: Allows you to override and define the internal lower timeframe used for volume estimation (e.g., 1-min).

📈 How to Use It:

✅ Bullish Divergence (Price down, CVD up)

This may indicate:

Buyers absorbing selling pressure.

A potential reversal to the upside.

Hidden accumulation.

🚫 Bearish Divergence (Price up, CVD down)

This may indicate:

Sellers stepping in despite upward price.

A potential reversal to the downside.

Hidden distribution.

🧠 Trading Insights:

CVD is often used by order flow traders or those analyzing market depth and volume imbalances.

This version lets you visually align price action with underlying volume, improving decision-making.

The divergence signal can be combined with other technical tools like support/resistance, candlestick patterns, or trendlines for confirmation.

Smooth BTCSPL [GiudiceQuantico] – Dual Smoothed MAsSmooth BTCSPL – Dual Smoothed MAs

What it measures

• % of Bitcoin addresses in profit vs loss (on-chain tickers).

• Spread = profit % − loss % → quick aggregate-sentiment gauge.

• Optional alpha-decay normalisation ⇒ keeps the curve on a 0-1 scale across cycles.

User inputs

• Use Alpha-Decay Adjusted Input (true/false).

• Fast MA – type (SMA / EMA / WMA / VWMA) & length (default 100).

• Slow MA – type & length (default 200).

• Colours – Bullish (#00ffbb) / Bearish (magenta).

Computation flow

1. Fetch daily on-chain series.

2. Build raw spread.

3. If alpha-decay enabled:

alpha = (rawSpread − 140-week rolling min) / (1 − rolling min).

4. Smooth chosen base with Fast & Slow MAs.

5. Bullish when Fast > Slow, bearish otherwise.

6. Bars tinted with the same bull/bear colour.

How to read

• Fast crosses above Slow → rising “addresses-in-profit” momentum → bullish bias.

• Fast crosses below Slow → stress / capitulation risk.

• Price-indicator divergences can flag exhaustion or hidden accumulation.

Tips

• Keep in a separate pane (overlay = false); bar-colouring still shows on price chart.

• Shorter lengths for swing trades, longer for macro outlook.

• Combine with funding rates, NUPL or simple price-MA crossovers for confirmation.

Climax Detector (Buy & Sell)This indicator identifies potential Buying Climax (BC) and Selling Climax (SC) events based on volume spikes relative to historical averages.

• Buying Climax (BC):

• Detected when a green candle forms with volume significantly higher than the average (default: 2×).

• Often signals the end of an uptrend or distribution phase.

• Selling Climax (SC):

• Detected when a red candle forms with very high volume (default: 2× average).

• Often occurs at the end of a downtrend, suggesting panic selling and potential accumulation.

How it works:

• Calculates a moving average of volume over a user-defined period (default: 20 candles)

• Flags a climax when current volume exceeds the defined multiplier (default: 2.0×)

• Marks:

• BC with an orange triangle above the bar

• SC with a fuchsia triangle below the bar

Customizable Settings:

• Volume spike sensitivity

• Lookback period for average volume

Use Cases:

• Spot possible trend exhaustion

• Confirm Wyckoff phases

• Combine with support/resistance for reversal entries

Disclaimer: This tool is designed to assist in identifying high-probability exhaustion zones but should be used alongside other confirmations or strategies.

Fibonacci Volume Profiles [AlgoAlpha]Unlock a deeper understanding of price action with the Fibonacci Volume Profiles indicator by AlgoAlpha! This powerful tool blends Fibonacci retracement levels with customizable volume profiles, helping traders identify high-probability areas of support, resistance, and accumulation. Designed for both continuous dynamic levels and custom time periods, this indicator is a must-have for traders seeking confluence in market structure analysis.

🔑 Key Features

📈 Dual Mode Selection : Choose between Continuous Fibonacci levels, which adapt dynamically to pivots, or a Custom Period mode, where you set your own start and end points.

📊 Integrated Volume Profile : Visualize volume distributions at key Fibonacci retracement levels, revealing areas of strong buying/selling interest.

🎨 Customizable Colors & Transparency : Adjust Fibonacci level colors, fill zones, and profile transparency for a visually clear experience.

🔍 Profile Resolution & Scaling : Control the number of price levels and width of the volume profile for detailed market insights.

🛠 Extendable Levels : Optionally extend Fibonacci levels to the right of the chart for better visualization of future price interaction.

📌 How to Use

Add the Indicator: Click on the star icon to add it to your favorites and apply it to your TradingView chart.

Analyze The Market: Observe how price interacts with Fibonacci levels alongside the volume profile to confirm support/resistance zones. Switch between custom range or continuous mode to align the tool with your trading style.

⚙️ How It Works

The indicator calculates pivot highs/lows dynamically (or uses user-defined time periods) to plot Fibonacci retracement levels. It then builds a volume profile by analyzing historical volume data, grouping it into price bins to highlight volume-heavy zones. The Point of Control (PoC) is identified as the level with the highest traded volume, acting as a key price magnet. The color-coded Fibonacci levels help traders spot retracement zones, while the volume profile confirms strength or weakness in those areas.

Liquidity Heatmap & Volume-Weighted RSILiquidity Heatmap Indicator with Volume-Weighted RSI

Description:

The Liquidity Heatmap Indicator with Volume-Weighted RSI (VW-RSI) is a powerful tool designed for traders to visualize market liquidity zones while integrating a volume-adjusted momentum oscillator. This indicator provides a dynamic heatmap of liquidity levels across various price points and enhances traditional RSI by incorporating volume weight, making it more responsive to market activity.

Key Features:

Liquidity Heatmap Visualization: Identifies high-liquidity price zones, allowing traders to spot potential areas of support, resistance, and accumulation.

Volume-Weighted RSI (VW-RSI): Enhances the RSI by factoring in trading volume, reducing false signals and improving trend confirmation.

Customizable Sensitivity: Users can adjust parameters to fine-tune heatmap intensity and RSI smoothing.

Dynamic Market Insights: Helps identify potential price reversals and trend strength by combining liquidity depth with momentum analysis.

How to Use:

1. Identify Liquidity Zones: The heatmap colors indicate areas of high and low liquidity, helping traders pinpoint key price action areas.

2. Use VW-RSI for Confirmation: When VW-RSI diverges from price near a liquidity cluster, it signals a potential reversal or continuation.

3. Adjust Parameters: Fine-tune the RSI period, volume weighting, and heatmap sensitivity to align with different trading strategies.

This indicator is ideal for traders who rely on order flow analysis, volume-based momentum strategies, and liquidity-driven trading techniques.

Volume Distribution Before/After Top

Description

This script visualizes the distribution of volume before and after a price peak within a specified time interval. The green area represents the volume accumulated before the peak, and the red area represents the volume accumulated after the peak. The script also calculates and displays the volume-weighted average price (VWAP) on each side of the peak with a dotted line and a label.

The key features include:

Volume Visualization: Transparent green and red bars indicate volume fractions before and after the peak.

VWAP Markers: Centered labels with VWAP values are plotted above the corresponding levels.

Interactive Inputs: Define the start and end points of the analysis interval using customizable anchor times.

This tool is ideal for traders who want to analyze how volume dynamics are distributed around key price levels. It can help identify potential zones of support and resistance and improve the understanding of market behavior in response to volume accumulation.

Instructions

Select the start and end anchor times using the input fields.

Observe the volume distribution and VWAP levels on the chart.

Use the visual data to make more informed trading decisions.

Crypto SeasonDefinition

This indicator is an informative indicator aiming to predict when the Altcoin season will start and when Bitcoin will enter the month season.

The average of the graph shows the dominance of altcoins other than BTC, ETH and USDT. If this value is over 30, the BTC says that the bull season is over. This value indicates that 20 to 30 BTC is in the bull season or accumulation. If this value is less than 20, it means that the subcoin season has begun.

Disclaimer

This indicator is for informational purposes only and should be used for educational purposes only. You may lose money if you rely on this to trade without additional information. Use at your own risk.

Version

v1.0

Liquidity Swings [UAlgo]The "Liquidity Swings " indicator is designed to help traders identify liquidity swings within the market. This tool is particularly useful for visualizing areas where liquidity is accumulating and where it is being swept, providing valuable insights for making informed trading decisions. By tracking the pivots in price and associating them with volume, the indicator highlights zones of potential support and resistance, helping traders understand market dynamics more clearly.

🔶 Key Features

Liquidity Swing Sensitivity: Adjustable sensitivity settings to fine-tune the detection of liquidity swings according to market conditions and trader preferences.

Two modes of liquidity calculation:

Cumulative Liquidity: Aggregates unswept liquidity over multiple swings until it is swept, providing a broader view of liquidity accumulation.

Individual Liquidity: Displays the accumulated liquidity for each swing independently, offering a more granular perspective.

Visual Customization: Options to customize the colors and sizes of liquidity lines, areas, and informational text for better visual clarity.

Dynamic Updates: The indicator dynamically updates liquidity zones and labels, adjusting to new market data to keep traders informed in real-time.

🔶 Disclaimer

The "Liquidity Swings " indicator is provided for educational and informational purposes only.

It should not be considered as financial advice or a recommendation to buy or sell any financial instrument.

The use of this indicator involves inherent risks, and users should employ their own judgment and conduct their own research before making any trading decisions. Past performance is not indicative of future results.

🔷 Related Scripts

Liquidity Sweeps

Williams %R Liquidity Sweeps

Bitcoin Wave RainbowThis Bitcoin Wave Rainbow model is a powerful tool designed to help traders of all levels understand and navigate the Bitcoin market. It works only with BTC in any timeframe, but better looks in dayly or weekly timeframes. It provides valuable insights into historical price behavior and offers forecasts for the next decade, making it an essential asset for both short-term and long-term strategies.

How the Model Works

The model is built on a logarithmic trend, also known as a power law, represented by the green line on the chart. This line illustrates the expected price trajectory of Bitcoin over time. The model also incorporates a range of price fluctuations around this trend, represented by colored bands.

The width of these bands narrows over time, indicating that the model becomes increasingly accurate as it progresses. This is due to the exponential decrease in the range of price fluctuations, making the model a reliable tool for predicting future price movements.

Understanding the Zones

Blue Zone: This zone signifies that the price is below its trend, making it a recommended area for buying Bitcoin. It represents a level where the price is unlikely to fall further, providing a potential opportunity for accumulation.

Green Zone: This zone represents a fair price range, where the price is relatively close to its trend. In this zone, the price may continue to go up or down, depending on the halving season. ransiting up around any halving and transiting down around 2 years after each halving.

Yellow Zone: This zone indicates that the price is somewhat overheated, often due to the hype following a halving event. While there may still be room for the price to rise, traders should exercise caution in this zone, as a price correction could occur.

Red Zone: This zone represents a strong overbought condition, where the price is significantly above its trend. Traders should be extremely cautious in this zone and consider reducing their positions, as the price is likely to revert back towards the trend or even lower.

Using the Model in Your Trading Strategy

This indicator can be used in conjunction with the Bitcoin Wave Model, which complements it by showing harmonic price fluctuations associated with halving events. Together, these indicators provide a comprehensive view of the Bitcoin market, allowing traders to make informed decisions based on both historical data and future projections.

Benefits for Traders

This Bitcoin price model offers numerous benefits for traders, including:

Clear Visualization: The model provides a clear and concise visual representation of Bitcoin's price behavior, making it easy to understand and interpret.

Accurate Forecasting: The model's accuracy increases over time, providing reliable forecasts for future price movements.

Risk Management: The model helps traders identify overbought and oversold conditions, allowing them to manage their risk more effectively.

Strategic Decision-Making: By understanding the different zones and their implications, traders can make more informed decisions about when to buy, sell, or hold Bitcoin.

By incorporating this Bitcoin price model into your trading strategy, you can gain a deeper understanding of the market dynamics and improve your chances of success.

VWAP DivergenceThe "VWAP Divergence" indicator leverages the VWAP Rolling indicator available in TradingView's library to analyze price and volume dynamics. This custom indicator calculates a rolling VWAP (Volume Weighted Average Price) and compares it with a Simple Moving Average (SMA) over a specified historical period.

Advantages:

1. Accurate VWAP Calculation: The VWAP Rolling indicator computes a VWAP that dynamically adjusts based on recent price and volume data. VWAP is a vital metric used by traders to understand the average price at which a security has traded, factoring in volume.

2. SMA Comparison: By contrasting the rolling VWAP from the VWAP Rolling indicator with an SMA of the same length, the indicator highlights potential divergences. This comparison can reveal shifts in market sentiment.

3. Divergence Identification: The primary purpose of this indicator is to detect divergences between the rolling VWAP from VWAP Rolling and the SMA. Divergence occurs when the rolling VWAP significantly differs from the SMA, indicating potential changes in market dynamics.

Interpretation:

1. Positive Oscillator Values: A positive oscillator (difference between rolling VWAP and SMA) suggests that the rolling VWAP, derived from the VWAP Rolling indicator, is above the SMA. This could indicate strong buying interest or accumulation.

2. Negative Oscillator Values: Conversely, a negative oscillator value indicates that the rolling VWAP is below the SMA. This might signal selling pressure or distribution.

3. Divergence Signals: Significant divergences between the rolling VWAP (from VWAP Rolling) and SMA can indicate shifts in market sentiment. For instance, a rising rolling VWAP diverging upwards from the SMA might suggest increasing bullish sentiment.

4. Confirmation with Price Movements: Traders often use these divergences alongside price action to confirm potential trend reversals or continuations.

Implementation:

1. Length Parameter: Adjust the Length input to modify the lookback period for computing both the rolling VWAP from VWAP Rolling and the SMA. A longer period provides a broader view of market sentiment, while a shorter period is more sensitive to recent price movements.

2. Visualization: The indicator plots the VWAP SMA Oscillator, which visually represents the difference (oscillator) between the rolling VWAP (from VWAP Rolling) and SMA over time.

3. Zero Line: The zero line (gray line) serves as a reference point. Oscillator values crossing above or below this line can be interpreted as bullish or bearish signals, respectively.

4. Contextual Analysis: Interpret signals from this indicator in conjunction with broader market conditions and other technical indicators to make informed trading decisions.

This indicator, utilizing the VWAP Rolling component, is valuable for traders seeking insights into the relationship between volume-weighted price levels and traditional moving averages, aiding in the identification of potential trading opportunities based on market dynamics.

Volume-Blended Candlesticks [QuantVue]Introducing the Volume-Blended Candlestick Indicator, a powerful tool that seamlessly integrates volume information with candlesticks, providing you with a comprehensive view of market dynamics in a single glance.

The Volume-Blended Candlestick Indicator employs a unique approach of projecting volume totals by calculating the total volume traded per second and comparing it to the time left in the session as well as the historical average length selected by the user.

The indicator then dynamically adjusts the opacity of the candlestick colors based on the intensity of the projected volume. As volume intensifies, the candlestick colors become more pronounced, while low volume will cause colors to fade allowing you to visually perceive the level of buying or selling.

One of the standout features of the Volume-Blended Candlestick Indicator is its ability to identify pocket pivots. A pocket pivot is an up day with volume greater than any of the down days volume in the past 10 days. By highlighting these pocket pivots on your chart, the indicator helps you identify potential stealth accumulation.

In addition to blending volume with candlesticks and spotting pocket pivots, this versatile indicator provides you with an insightful table displaying key volume metrics. The table includes the average volume, average dollar volume, and the up-down volume ratio, allowing you to get a clear picture of buying and selling pressure.

Settings Include:

🔹Sensitivty Level: Normal, More, Less

🔹Volume MA Length

🔹Toggle Color based on previous close

🔹Show or hide volume info

🔹Chose candlestick colors

🔹Show or hide pocket pivots

🔹Show or hide volume info table

Don't hesitate to reach out with any questions or concerns.

We hope you enjoy!

Cheers.

RelativeValue█ OVERVIEW

This library is a Pine Script™ programmer's tool offering the ability to compute relative values, which represent comparisons of current data points, such as volume, price, or custom indicators, with their analogous historical data points from corresponding time offsets. This approach can provide insightful perspectives into the intricate dynamics of relative market behavior over time.

█ CONCEPTS

Relative values

In this library, a relative value is a metric that compares a current data point in a time interval to an average of data points with corresponding time offsets across historical periods. Its purpose is to assess the significance of a value by considering the historical context within past time intervals.

For instance, suppose we wanted to calculate relative volume on an hourly chart over five daily periods, and the last chart bar is two hours into the current trading day. In this case, we would compare the current volume to the average of volume in the second hour of trading across five days. We obtain the relative volume value by dividing the current volume by this average.

This form of analysis rests on the hypothesis that substantial discrepancies or aberrations in present market activity relative to historical time intervals might help indicate upcoming changes in market trends.

Cumulative and non-cumulative values

In the context of this library, a cumulative value refers to the cumulative sum of a series since the last occurrence of a specific condition (referred to as `anchor` in the function definitions). Given that relative values depend on time, we use time-based conditions such as the onset of a new hour, day, etc. On the other hand, a non-cumulative value is simply the series value at a specific time without accumulation.

Calculating relative values

Four main functions coordinate together to compute the relative values: `maintainArray()`, `calcAverageByTime()`, `calcCumulativeSeries()`, and `averageAtTime()`. These functions are underpinned by a `collectedData` user-defined type (UDT), which stores data collected since the last reset of the timeframe along with their corresponding timestamps. The relative values are calculated using the following procedure:

1. The `averageAtTime()` function invokes the process leveraging all four of the methods and acts as the main driver of the calculations. For each bar, this function adds the current bar's source and corresponding time value to a `collectedData` object.

2. Within the `averageAtTime()` function, the `maintainArray()` function is called at the start of each anchor period. It adds a new `collectedData` object to the array and ensures the array size does not exceed the predefined `maxSize` by removing the oldest element when necessary. This method plays an essential role in limiting memory usage and ensuring only relevant data over the desired number of periods is in the calculation window.

3. Next, the `calcAverageByTime()` function calculates the average value of elements within the `data` field for each `collectedData` object that corresponds to the same time offset from each anchor condition. This method accounts for cases where the current index of a `collectedData` object exceeds the last index of any past objects by using the last available values instead.

4. For cumulative calculations, the `averageAtTime()` function utilizes the `isCumulative` boolean parameter. If true, the `calcCumulativeSeries()` function will track the running total of the source data from the last bar where the anchor condition was met, providing a cumulative sum of the source values from one anchor point to the next.

To summarize, the `averageAtTime()` function continually stores values with their corresponding times in a `collectedData` object for each bar in the anchor period. When the anchor resets, this object is added to a larger array. The array's size is limited by the specified number of periods to be averaged. To correlate data across these periods, time indexing is employed, enabling the function to compare corresponding points across multiple periods.

█ USING THIS LIBRARY

The library simplifies the complex process of calculating relative values through its intuitive functions. Follow the steps below to use this library in your scripts.

Step 1: Import the library and declare inputs

Import the library and declare variables based on the user's input. These can include the timeframe for each period, the number of time intervals to include in the average, and whether the calculation uses cumulative values. For example:

//@version=5

import TradingView/RelativeValue/1 as TVrv

indicator("Relative Range Demo")

string resetTimeInput = input.timeframe("D")

int lengthInput = input.int(5, "No. of periods")

Step 2: Define the anchor condition

With these inputs declared, create a condition to define the start of a new period (anchor). For this, we use the change in the time value from the input timeframe:

bool anchor = timeframe.change(resetTimeInput)

Step 3: Calculate the average

At this point, one can calculate the average of a value's history at the time offset from the anchor over a number of periods using the `averageAtTime()` function. In this example, we use True Range (TR) as the `source` and set `isCumulative` to false:

float pastRange = TVrv.averageAtTime(ta.tr, lengthInput, anchor, false)

Step 4: Display the data

You can visualize the results by plotting the returned series. These lines display the non-cumulative TR alongside the average value over `lengthInput` periods for relative comparison:

plot(pastRange, "Past True Range Avg", color.new(chart.bg_color, 70), 1, plot.style_columns)

plot(ta.tr, "True Range", close >= open ? color.new(color.teal, 50) : color.new(color.red, 50), 1, plot.style_columns)

This example will display two overlapping series of columns. The green and red columns depict the current TR on each bar, and the light gray columns show the average over a defined number of periods, e.g., the default inputs on an hourly chart will show the average value at the hour over the past five days. This comparative analysis aids in determining whether the range of a bar aligns with its typical historical values or if it's an outlier.

█ NOTES

• The foundational concept of this library was derived from our initial Relative Volume at Time script. This library's logic significantly boosts its performance. Keep an eye out for a forthcoming updated version of the indicator. The demonstration code included in the library emulates a streamlined version of the indicator utilizing the library functions.

• Key efficiencies in the data management are realized through array.binary_search_leftmost() , which offers a performance improvement in comparison to its loop-dependent counterpart.

• This library's architecture utilizes user-defined types (UDTs) to create custom objects which are the equivalent of variables containing multiple parts, each able to hold independent values of different types . The recently added feature was announced in this blog post.

• To enhance readability, the code substitutes array functions with equivalent methods .

Look first. Then leap.

█ FUNCTIONS

This library contains the following functions:

calcCumulativeSeries(source, anchor)

Calculates the cumulative sum of `source` since the last bar where `anchor` was `true`.

Parameters:

source (series float) : Source used for the calculation.

anchor (series bool) : The condition that triggers the reset of the calculation. The calculation is reset when `anchor` evaluates to `true`, and continues using the values accumulated since the previous reset when `anchor` is `false`.

Returns: (float) The cumulative sum of `source`.

averageAtTime(source, length, anchor, isCumulative)

Calculates the average of all `source` values that share the same time difference from the `anchor` as the current bar for the most recent `length` bars.

Parameters:

source (series float) : Source used for the calculation.

length (simple int) : The number of reset periods to consider for the average calculation of historical data.

anchor (series bool) : The condition that triggers the reset of the average calculation. The calculation is reset when `anchor` evaluates to `true`, and continues using the values accumulated since the previous reset when `anchor` is `false`.

isCumulative (simple bool) : If `true`, `source` values are accumulated until the next time `anchor` is `true`. Optional. The default is `true`.

Returns: (float) The average of the source series at the specified time difference.

The Rush

█ OVERVIEW

This script shows when buyers are in a rush to buy and when sellers are in a rush to sell

═════════════════════════════════════════════════════════════════════════

█ CONCEPTS

Prophet Mohamed Peace be upon Him once said something similar to this "It is not advisable to trade if you do not know the

Volume".

In his book "The Day Trader's Bible - Or My Secret In Day trading Of Stocks", Richard D. Kickoff wrote in page 55

"This shows that there was only 100 shares for sale at 180 1/8, none at all at 180f^, and only 500 at 3/8. The jump from 1 to 8 to 3/8

Emphasizes both the absence of pressure and persistency on the part of the buyers. They are not content to wait patiently until they can

Secure the stock at 180^/4; they "reach" for it."

This script was inspired by these two great men.

Prophet Mohamed Peace be upon Him showed the importance of the volume and Richard D. Kickoff explained what Prophet

Mohamed Peace be upon Him meant.

So I created this script that gauge the movement of the stock and the sentiments of the traders.

═════════════════════════════════════════════════════════════════════════

• FEATURES: The script calculates The Percentage Difference of the price and The Percentage Difference of the volume between

two success bullish candles (or two success bearish candles) and then it creates a ratio between these two Percentage

Differences and in the end the ratio is compared to the previous one to see if there is an increase or a decrease.

═════════════════════════════════════════════════════════════════════════

• HOW TO USE: if you see 2 or more successive red bars that mean bears are in hurry to sell and you can expect a bearish trend soon

if the Market Maker allows it or later if the Market Maker wants to do some distribution.

if you see 2 or more successive green bars that mean bulls are in hurry to buy and you can expect a bullish trend soon if the Market

Maker allows it or later if the Market Maker wants to do some accumulation.

═════════════════════════════════════════════════════════════════════════

• LIMITATIONS:

1- Use only Heikin Ashi chart

2- Good only if volume data is correct , meaning good for a centralized Market. (You can use it for forex or

crypto but at your own risk because those markets are not centralized)

═════════════════════════════════════════════════════════════════════════

• THANKS: I pay homage to Prophet Mohamed Peace be upon Him and Richard D. Kickoff who inspired the creation of this

Script.

═════════════════════════════════════════════════════════════════════════

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)