RSI SMA Crossover StrategyOverview

RSI SMA Crossover Strategy works the same way as traditional MA crossover strategies, but using RSI instead of price. When RSI crosses over the SMA, a long position is opened (buy). When RSI crosses under the SMA, the long position is closed (sell).

This strategy can be very effective when the right inputs are used (see below). Be sure to use the backtesting tool to determine the optimal parameters for a given asset/timeframe.

Inputs/Parameters

RSI Length: length for RSI calculation (default = 50)

SMA Length: length for SMA calculation (default = 25)

Strategy Properties

Initial Capital = $1000

No default properties are defined for Slippage, Commission, etc, so be sure to set these values to get accurate backtesting results. This script is being published open-source for a reason - save yourself a copy and adjust the settings as you like!

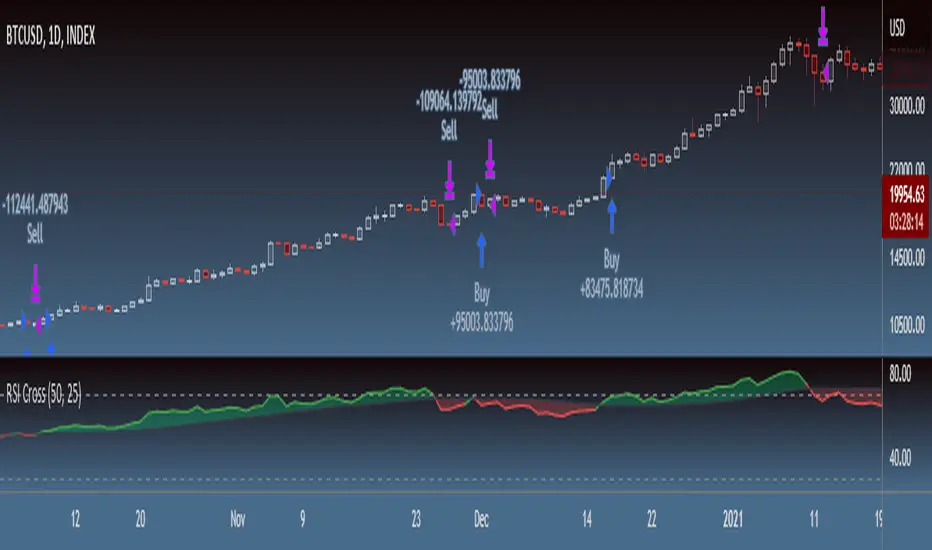

Backtesting Results

Testing on Bitcoin (all time index) 1D chart, with all default parameters.

$1,000 initial investment on 10/07/2010 turns into almost $2.5 billion as of 08/30/2022 (compared to $334 million if the initial investment was held over the same period)

Remember, results can vary greatly based on the variables mentioned above, so always be sure to backtest.

Recherche dans les scripts pour "backtesting"

Short Selling EMA Cross (By Coinrule)BINANCE:AVAXUSDT

This short selling script works best in periods of downtrends and general bearish market conditions, with the ultimate goal to sell as the the price decreases further and buy back before a rebound.

This script can work well on coins you are planning to hodl for long-term and works especially well whilst using an automated bot that can execute your trades for you. It allows you to hedge your investment by allocating a % of your coins to trade with, whilst not risking your entire holding. This mitigates unrealised losses from hodling as it provides additional cash from the profits made. You can then choose to to hodl this cash, or use it to reinvest when the market reaches attractive buying levels.

Entry

The exponential moving average ( EMA ) 20 and EMA 50 have been used for the variables determining the entry to the short. EMAs can operate better than simple moving averages due to the additional weighting placed on the most recent data points, whereas simple moving averages weight all the data the same. This means that price is tracked more closely and the most recent volatile moves can be captured and exploited more efficiently using EMAs.

Our backtesting data revealed that the most profitable timeframe was the 30-minute timeframe, this also enabled a good frequency of trades and high profitability.

A fast (shorter term) exponential moving average , in this strategy the EMA 20, crossing under a slow (longer term) moving average, in this example the EMA 50, signals the price of an asset has started to trend to the downside, as the most recent data signals price is declining compared to earlier data. The entry acts on this principle and executes when the EMA 20 crosses under the EMA 50.

Enter Short: EMA 20 crosses under EMA 50.

Exit

This script utilises a take profit and stop loss for the exit. The take profit is set at -8% and the stop loss is set at +16% from the entry price. This would normally be a poor trade due to the risk:reward equalling 0.5. However, when looking at the backtesting data, the high profitability of the strategy (93.33%) leads to increased confidence and showcases the high probability of success according to historical data.

The take profit (-8%) and the stop loss (+16%) of the strategy are widely placed to ensure the move is captured without being stopped out due to relief rallies. The stop loss also plays a role of mitigating losses and minimising risk of being stuck in a short position once there has been a fundamental trend reversal and the market has become bullish .

Exit Short: -8% price decrease from entry price.

OR

Exit Short: +16% price increase from entry price.

Tip: Research what coins have consistent and large token unlocks / highly inflationary tokenomics, and target these during bear markets to short as they will most likely have substantial selling pressure that outweighs demand - leading to declining prices.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

The backtesting data was recorded from December 1st 2021, just as the market was beginning its downtrend. We therefore recommend analysing the market conditions prior to utilising this strategy as it operates best on weak coins during downtrends and bearish conditions.

Last Available Bar InfoLibrary "Last_Available_Bar_Info"

getLastBarTimeStamp()

getAvailableBars()

This simple library is built with an aim of getting the last available bar information for the chart. This returns a constant value that doesn't change on bar change.

For backtesting with accurate results on non standard charts, it will be helpful. (Especially if you are using non standard charts like Renko Chart).

Methods

getLastBarTimeStamp()

: Returns Timestamp of the last available bar (Constant)

getAvailableBars()

:Returns Number of Available Bars on the chart (Constant)

Example

import paragjyoti2012/Last_Available_Bar_Info/v1 as LastBarInfo

last_bar_timestamp=LastBarInfo.getLastBarTimeStamp()

no_of_bars=LastBarInfo.getAvailableBars()

If you are using Renko Charts, for backtesting, it's necesary to filter out the historical bars that are not of this timeframe.

In Renko charts, once the available bars of the current timeframe (based on your Tradingview active plan) are exhausted,

previous bars are filled in with historical bars of higher timeframe. Which is detrimental for backtesting, and it leads to unrealistic results.

To get the actual number of bars available of that timeframe, you should use this security function to get the timestamp for the last (real) bar available.

tf=timeframe.period

real_available_bars = request.security(syminfo.ticker, tf , LastBarInfo.getAvailableBars() , lookahead = barmerge.lookahead_off)

last_available_bar_timestamp = request.security(syminfo.ticker, tf , LastBarInfo.getLastBarTimeStamp() , lookahead = barmerge.lookahead_off)

Financial Astrology Crypto ML Daily TrendThis daily trend indicator is based on financial astrology cycles detected with advanced machine learning techniques for the crypto-currencies research portfolio: ADA, BAT, BNB, BTC, DASH, EOS, ETC, ETH, LINK, LTC, XLM, XMR, XRP, ZEC and ZRX. The daily price trend is forecasted through this planets cycles (angular aspects, speed, declination), fast ones are based on Moon, Mercury, Venus and Sun and Mid term cycles are based on Mars, Vesta and Ceres. The combination of all this cycles produce a daily price trend prediction that is encoded into a PineScript array using binary format "0 or 1" that represent sell and buy signals respectively. The indicator provides signals since 2021-01-01 to 2022-12-31, the past months signals purpose is to support backtesting of the indicator combined with other technical indicator entries like MAs, RSI or Stochastic. For future predictions besides 2022 a machine learning models re-train phase will be required.

The resolution of this indicator is 1D, you can tune a parameter where you can determine how many future bars of daily trend are plotted and adjust an hours shift to anticipate future signals into current bar in order to produce a leading indicator effect to anticipate the trend changes with some hours of anticipation. Combined with technical analysis indicators this daily trend is very powerful because can help to produce approximately 60% of profitable signals based on the backtesting results. You can look at our open source Github repositories to validate accuracy using the backtesting strategies we have implemented in Jesse Crypto Trading Framework as proof of concept of the predictive potential of this indicator. Alternatively, we have implemented a PineScript strategy that use this indicator, just consider that we are pending to do signals update to the period July 2021 to December 2022: This strategy have accumulated more than 110 likes and many traders have validated the predictive power of Financial Astrology.

DISCLAIMER: This indicator is experimental and don’t provide financial or investment advice, the main purpose is to demonstrate the predictive power of financial astrology. Any allocation of funds following the documented machine learning model prediction is a high-risk endeavour and it’s the users responsibility to practice healthy risk management according to your situation.

[laoowai]BNB_USDT_3m_3Commas_Bollinger_MACD_RSI_StrategyBNB_USDT _3m

Release Notes:

Time: 3min

Pair: BNB_USDT

Use: {{strategy.order.alert_message}}

What's the difference with 3Commas Bollinger Strategy by tedwardd:

1. Initial capital: 1210 USDT (10$ Base order / 400$*3 Safety order), if you will change, please change JUST safety order volume or number of safety orders 2-3

2. Using just 2(3) safety order (original script 4)

3. More high-performance strategy for BNB_USDT

4. Using MACD to sell order (original script take profit by scale), thanks Drun30 .

5. Using RSI to analyze the market conditions.

Need to change:

bot_id = input(title="3Commas Bot ID", defval=" YOUR DATA ")

email_token = input(title="Bot Email Token", defval=" YOUR DATA ")

---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

FAQ copy from tedwardd

---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

This strategy is intended for use as a way of backtesting various parameters available on 3commas.

The primary inputs for the strategy are:

---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

// USER INPUTS

Short MA Window - The length of the Short moving average

Long MA Window - The length of the Long moving average

Upper Band Offset - The offset to use for the upper bollinger offset

Lower Band Offset - The offset to use for the lower bollinger offset

Long Stop Loss % - The stop loss percentage to test

Long Take Profit % - The Take profit percentage to test

Initial SO Deviation % - The price deviation percentage required to place to first safety order

Safety Order Vol Step % - The volume scale to test

3Commas Bot ID - (self-explanatory)

Bot Email Token - Found in the deal start message for your bot (see link in the previous section for details)

3Commas Bot Trading Pair - The pair to include for composite bot start deals (should match the format of 3commas, not TradingView IE. USDT_BTC not BTCUSDT )

---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Start Date, Month, Year and End Date, Month, and Year all apply to the backtesting window. By default, it will use as much data as it can give the current period select (there is less historical data available for periods below 1H) back as far as 2016 (there appears to be no historical data on Trading view much before this). If you would like to test a different period of time, just change these values accordingly.

---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Composite bot using a Bollinger band type trading strategy. While its primary intention is to provide users a way of backtesting bot parameters, it can also be used to trigger a deal start by either using the {{strategy.order.alert_message}} field in your alert and providing the bot details in the configuration screen for the strategy or by including the usual deal start message provided by 3commas.

---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Original script:

1. 3Commas Bollinger Strategy by tedwardd

2. Momentum Strategy ( BTC /USDT; 1h) - MACD (with source code) by Drun30

3Commas Bollinger StrategyThis strategy is intended for use as a way of backtesting various parameters available on 3commas.io composite bot using a bollinger band type trading strategy. While it's primary intention is to provide users a way of backtesting bot parameters, it can also be used to trigger a deal start by either using the {{strategy.open.alert_message}} field in your alert and providing the bot details in the configuration screen for the strategy or by including the usual deal start message provided by 3commas. You can find more information about how to do this from help.3commas.io

The primary inputs for the strategy are:

// USER INPUTS

Short MA Window - The length of the Short moving average

Long MA Window - The length of the Long moving average

Upper Band Offset - The offset to use for the upper bollinger offset

Lower Band Offset - The offset to use for the lower bollinger offset

Long Stop Loss % - The stop loss percentage to test

Long Take Profit % - The Take profit percentage to test

Initial SO Deviation % - The price deviation percentage required to place to first safety order

Safety Order Vol Step % - The volume scale to test

3Commas Bot ID - (self explanatory)

Bot Email Token - Found in the deal start message for your bot (see link in previous section for details)

3Commas Bot Trading Pair - The pair to include for composite bot start deals (should match format of 3commas, not TradingView IE. USDT_BTC not BTCUSDT)

Start Date, Month, Year and End Date, Month and Year all apply to the backtesting window. By default it will use as much data as it can given the current period select (there is less historical data available for periods below 1H) back as far as 2016 (there appears to be no historical data on Trading view much before this). If you would like to test a different period of time, just change these values accordingly.

Known Issues

Currently there are a couple of issues with this strategy that you should be aware of. I may fix them at some point in the future but they don't really bug me so this is more for informational purposes than a promise that they may one day be fixed.

Does not test trailing take profit

Number of safety orders and Safety Order Step Scale are currently not user configurable (must edit source code)

Using the user configuration to generate deal start message assumes you are triggering a composite bot, not a simple bot.

Efficient Work [LucF]█ OVERVIEW

Efficient Work measures the ratio of price movement from close to close ( resulting work ) over the distance traveled to the high and low before settling down at the close ( total work ). The closer the two values are, the more Efficient Work approaches its maximum value of +1 for an up move or -1 for a down move. When price does not change, Efficient Work is zero.

Higher values of Efficient Work indicate more efficient price travel between the close of two successive bars, which I interpret to be more significant, regardless of the move's amplitude. Because it measures the direction and strength of price changes rather than their amplitude, Efficient Work may be thought of as a sentiment indicator.

█ CONCEPTS

This oscillator's design stems from a few key concepts.

Relative Levels

Other than the centerline, relative rather than absolute levels are used to identify levels of interest. Accordingly, no fixed levels correspond to overbought/oversold conditions. Relative levels of interest are identified using:

• A Donchian channel (historical highs/lows).

• The oscillator's position relative to higher timeframe values.

• Oscillator levels following points in time where a divergence is identified.

Higher timeframes

Two progressively higher timeframes are used to calculate larger-context values for the oscillator. The rationale underlying the use of timeframes higher than the chart's is that, while they change less frequently than the values calculated at the chart's resolution, they are more meaningful because more work (trader activity) is required to calculate them. Combining the immediacy of values calculated at the chart's resolution to higher timeframe values achieves a compromise between responsiveness and reliability.

Divergences as points of interest rather than directional clues

A very simple interpretation of what constitutes a divergence is used. A divergence is defined as a discrepancy between any bar's direction and the direction of the signal line on that same bar. No attempt is made to attribute a directional bias to divergences when they occur. Instead, the oscillator's level is saved and subsequent movement of the oscillator relative to the saved level is what determines the bullish/bearish state of the oscillator.

Conservative coloring scheme

Several additive coloring conditions allow the bull/bear coloring of the oscillator's main line to be restricted to specific areas meeting all the selected conditions. The concept is built on the premise that most of the time, an oscillator's value should be viewed as mere noise, and that somewhat like price, it only occasionally conveys actionable information.

█ FEATURES

Plots

• Three lines can be plotted. They are named Main line , Line 2 and Line 3 . You decide which calculation to use for each line:

• The oscillator's value at the chart's resolution.

• The oscillator's value at a medium timeframe higher than the chart's resolution.

• The oscillator's value at the highest timeframe.

• An aggregate line calculated using a weighed average of the three previous lines (see the Aggregate Weights section of Inputs to configure the weights).

• The coloring conditions, divergence levels and the Hi/Lo channel always apply to the Main line, whichever calculation you decide to use for it.

• The color of lines 2 and 3 are fixed but can be set in the "Colors" section of Inputs.

• You can change the thickness of each line.

• When the aggregate line is displayed, higher timeframe values are only used in its calculation when they become available in the chart's history,

otherwise the aggregate line would appear much later on the chart. To indicate when each higher timeframe value becomes available,

a small label appears near the centerline.

• Divergences can be shown as small dots on the centerline.

• Divergence levels can be shown. The level and fill are determined by the oscillator's position relative to the last saved divergence level.

• Bull/bear markers can be displayed. They occur whenever a new bull/bear state is determined by the "Main Line Coloring Conditions".

• The Hi/Lo (Donchian) channel can be displayed, and its period defined.

• The background can display the state of any one of 11 different conditions.

• The resolutions used for the higher timeframes can be displayed to the right of the last bar's value.

• Four key values are always displayed in the Data Window (fourth icon down to the right of your chart):

oscillator values for the chart, medium and highest timeframes, and the oscillator's instant value before it is averaged.

Main Line Coloring Conditions

• Nine different conditions can be selected to determine the bull/bear coloring of the main line. All conditions set to "ON" must be met to determine the bull/bear state.

• A volatility state can also be used to filter the conditions.

• When the coloring conditions and the filter do not allow for a bull/bear state to be determined, the neutral color is used.

Signal

• Seven different averages can be used to calculate the average of the oscillator's value.

• The average's period can be set. A period of one will show the instant value of the oscillator,

provided you don't use linear regression or the Hull MA as they do not work with a period of one.

• An external signal can be used as the oscillator's instant value. If an already averaged external value is used, set the period to one in this indicator.

• For the cases where an external signal is used, a centerline value can be set.

Higher Timeframes

• The two higher timeframes are named Medium timeframe and Highest timeframe . They can be determined using one of three methods:

• Auto-steps: the higher timeframes are determined using the chart's resolution. If the chart uses a seconds resolution, for example,

the medium and highest resolutions will be 15 and 60 minutes.

• Multiples: the timeframes are calculated using a multiple of the chart's resolution, which you can set.

• Fixed: the set timeframes do not change with the chart's resolution.

Repainting

• Repainting can be controlled separately for the chart's value and the higher timeframe values.

• The default is a repainting chart value and non-repainting higher timeframe values. The Aggregate line will thus repaint by default,

as it uses the chart's value along with the higher timeframes values.

Aggregate Weights

• The weight of each component of the Aggregate line can be set.

• The default is equal weights for the three components, meaning that the chart's value accounts for one third of the weight in the Aggregate.

High Volatility

• This provides control over the volatility filter used in the Main line's coloring conditions and the background display.

• Volatility is determined to be high when the short-term ATR is greater than the long-term ATR.

Colors

• You can define your own colors for all of the oscillator's plots.

• The default colors will perform well on both white and black chart backgrounds.

Alerts

• An alert can be defined for the script. The alert will trigger whenever a bull/bear marker appears in the indicator's display.

The particular combination of coloring conditions and the display of bull/bear markers when you create the alert will thus determine when the alert triggers.

Once the alerts are created, subsequent changes to the conditions controlling the display of markers will not affect the existing alert(s).

• You can create multiple alerts from this script, each triggering on different conditions.

Backtesting & Trading Engine Signal Line

• An invisible plot named "BTE Signal" is provided. It can be used as an entry signal when connected to the PineCoders Backtesting & Trading Engine as an external input.

It will generate an entry whenever a marker is displayed.

█ NOTES

• I do not know for sure if the calculations in Efficient Work are original. I apologize if they are not.

• Because this version of Efficient Work only has access to OHLC information, it cannot measure the total distance traveled through all of a bar's ticks, but the indicator nonetheless behaves in a manner consistent with the intentions underlying its design.

For Pine coders

This code was written using the following standards:

• The PineCoders Coding Conventions for Pine .

• A modified version of the PineCoders MTF Oscillator Framework and MTF Selection Framework .

MTF Oscillator Framework [PineCoders]This framework allows Pine coders to quickly build a complete multi-timeframe oscillator from any calculation producing values around a centerline, whether the values are bounded or not. Insert your calculation in the script and you have a ready-to-publish MTF Oscillator offering a plethora of presentation options and features.

█ HOW TO USE THE FRAMEWORK

1 — Insert your calculation in the `f_signal()` function at the top of the "Helper Functions" section of the script.

2 — Change the script's name in the `study()` declaration statement and the `alertcondition()` text in the last part of the "Plots" section.

3 — Adapt the default value used to initialize the CENTERLINE constant in the script's "Constants" section.

4 — If you want to publish the script, copy/paste the following description in your new publication's description and replace the "OVERVIEW" section with a description of your calculations.

5 — Voilà!

═════════════════════════════════════════════════════════════════════════

█ OVERVIEW

This oscillator calculates a directional value of True Range. When a bar is up, the positive value of True Range is used. A negative value is used when the bar is down. When there is no movement during the bar, a zero value is generated, even if True Range is different than zero. Because the unit of measure of True Range is price, the oscillator is unbounded (it does not have fixed upper/lower bounds).

True Range can be used as a metric for volatility, but by using a signed value, this oscillator will show the directional bias of progressively increasing/decreasing volatility, which can make it more useful than an always positive value of True Range.

The True Range calculation appeared for the first time in J. Welles Wilder's New Concepts in Technical Trading Systems book published in 1978. Wilder's objective was to provide a reliable measure of the effective movement—or range—between two bars, to measure volatility. True Range is also the building block used to calculate ATR (Average True Range), which calculates the average of True Range values over a given period using the `rma` averaging method—the same used in the calculation of another of Wilder's remarkable creations: RSI.

█ CONCEPTS

This oscillator's design stems from a few key concepts.

Relative Levels

Other than the centerline, relative rather than absolute levels are used to identify levels of interest. Accordingly, no fixed levels correspond to overbought/oversold conditions. Relative levels of interest are identified using:

• A Donchian channel (historical highs/lows).

• The oscillator's position relative to higher timeframe values.

• Oscillator levels following points in time where a divergence is identified.

Higher timeframes

Two progressively higher timeframes are used to calculate larger-context values for the oscillator. The rationale underlying the use of timeframes higher than the chart's is that, while they change less frequently than the values calculated at the chart's resolution, they are more meaningful because more work (trader activity) is required to calculate them. Combining the immediacy of values calculated at the chart's resolution to higher timeframe values achieves a compromise between responsiveness and reliability.

Divergences as points of interest rather than directional clues

A very simple interpretation of what constitutes a divergence is used. A divergence is defined as a discrepancy between any bar's direction and the direction of the signal line on that same bar. No attempt is made to attribute a directional bias to divergences when they occur. Instead, the oscillator's level is saved and subsequent movement of the oscillator relative to the saved level is what determines the bullish/bearish state of the oscillator.

Conservative coloring scheme

Several additive coloring conditions allow the bull/bear coloring of the oscillator's main line to be restricted to specific areas meeting all the selected conditions. The concept is built on the premise that most of the time, an oscillator's value should be viewed as mere noise, and that somewhat like price, it only occasionally conveys actionable information.

█ FEATURES

Plots

• Three lines can be plotted. They are named Main line , Line 2 and Line 3 . You decide which calculation to use for each line:

• The oscillator's value at the chart's resolution.

• The oscillator's value at a medium timeframe higher than the chart's resolution.

• The oscillator's value at the highest timeframe.

• An aggregate line calculated using a weighed average of the three previous lines (see the Aggregate Weights section of Inputs to configure the weights).

• The coloring conditions, divergence levels and the Hi/Lo channel always apply to the Main line, whichever calculation you decide to use for it.

• The color of lines 2 and 3 are fixed but can be set in the "Colors" section of Inputs.

• You can change the thickness of each line.

• When the aggregate line is displayed, higher timeframe values are only used in its calculation when they become available in the chart's history,

otherwise the aggregate line would appear much later on the chart. To indicate when each higher timeframe value becomes available,

a small label appears near the centerline.

• Divergences can be shown as small dots on the centerline.

• Divergence levels can be shown. The level and fill are determined by the oscillator's position relative to the last saved divergence level.

• Bull/bear markers can be displayed. They occur whenever a new bull/bear state is determined by the "Main Line Coloring Conditions".

• The Hi/Lo (Donchian) channel can be displayed, and its period defined.

• The background can display the state of any one of 11 different conditions.

• The resolutions used for the higher timeframes can be displayed to the right of the last bar's value.

• Four key values are always displayed in the Data Window (fourth icon down to the right of your chart):

oscillator values for the chart, medium and highest timeframes, and the oscillator's instant value before it is averaged.

Main Line Coloring Conditions

• Nine different conditions can be selected to determine the bull/bear coloring of the main line. All conditions set to "ON" must be met to determine the bull/bear state.

• A volatility state can also be used to filter the conditions.

• When the coloring conditions and the filter do not allow for a bull/bear state to be determined, the neutral color is used.

Signal

• Seven different averages can be used to calculate the average of the oscillator's value.

• The average's period can be set. A period of one will show the instant value of the oscillator,

provided you don't use linear regression or the Hull MA as they do not work with a period of one.

• An external signal can be used as the oscillator's instant value. If an already averaged external value is used, set the period to one in this indicator.

• For the cases where an external signal is used, a centerline value can be set.

Higher Timeframes

• The two higher timeframes are named Medium timeframe and Highest timeframe . They can be determined using one of three methods:

• Auto-steps: the higher timeframes are determined using the chart's resolution. If the chart uses a seconds resolution, for example,

the medium and highest resolutions will be 15 and 60 minutes.

• Multiples: the timeframes are calculated using a multiple of the chart's resolution, which you can set.

• Fixed: the set timeframes do not change with the chart's resolution.

Repainting

• Repainting can be controlled separately for the chart's value and the higher timeframe values.

• The default is a repainting chart value and non-repainting higher timeframe values. The Aggregate line will thus repaint by default,

as it uses the chart's value along with the higher timeframes values.

Aggregate Weights

• The weight of each component of the Aggregate line can be set.

• The default is equal weights for the three components, meaning that the chart's value accounts for one third of the weight in the Aggregate.

High Volatility

• This provides control over the volatility filter used in the Main line's coloring conditions and the background display.

• Volatility is determined to be high when the short-term ATR is greater than the long-term ATR.

Colors

• You can define your own colors for all of the oscillator's plots.

• The default colors will perform well on both white and black chart backgrounds.

Alerts

• An alert can be defined for the script. The alert will trigger whenever a bull/bear marker appears in the indicator's display.

The particular combination of coloring conditions and the display of bull/bear markers when you create the alert will thus determine when the alert triggers.

Once the alerts are created, subsequent changes to the conditions controlling the display of markers will not affect the existing alert(s).

• You can create multiple alerts from this script, each triggering on different conditions.

Backtesting & Trading Engine Signal Line

• An invisible plot named "BTE Signal" is provided. It can be used as an entry signal when connected to the PineCoders Backtesting & Trading Engine as an external input.

It will generate an entry whenever a marker is displayed.

Look first. Then leap.

Current Candle DateTimeThis is a simple script that users can easily see that datetime of the current candle. This is useful when backtesting and you want to be able to quickly glance and see where we are up to. Useful for when you are backtesting a strategy and trying to stay within a particular trading session.

The indicator will display in the top right hand corner, so it wont get in the way of any other analysis.

Precision Multi-Dimensional Signal System V2Precision Multi-Dimensional Signal System (PMSS) - Technical Documentation

Overview and Philosophical Foundation

The Precision Multi-Dimensional Signal System (PMSS) represents a systematic approach to technical analysis that integrates four distinct analytical dimensions into a cohesive trading framework. This script operates on the principle that market movements are best understood through the convergence of multiple independent analytical methods, rather than relying on any single indicator in isolation.

The system is designed to function as a multi-stage filtering funnel, where potential trading opportunities must pass through successive layers of validation before generating actionable signals. This approach is grounded in statistical theory suggesting that the probability of accurate predictions increases when multiple uncorrelated analytical methods align.

Integration Rationale and Component Synergy

1. Trend Analysis Layer (Dual Moving Average System)

Components: SMA-50 and SMA-200

Purpose: Establish primary market direction and filter against counter-trend signals

Integration Rationale:

SMA-50 provides medium-term trend direction

SMA-200 establishes long-term trend context

The dual-MA configuration creates a trend confirmation mechanism where signals are only generated in alignment with the established trend structure

This layer addresses the fundamental trading principle of "following the trend" while avoiding the pitfalls of single moving average systems that frequently generate whipsaw signals

2. Momentum Analysis Layer (MACD)

Components: MACD line, signal line, histogram

Purpose: Detect changes in market momentum and identify potential trend reversals

Integration Rationale:

MACD crossovers provide timely momentum shift signals

Histogram analysis confirms momentum acceleration/deceleration

This layer acts as the primary trigger mechanism, initiating the signal evaluation process

The momentum dimension is statistically independent from the trend dimension, providing orthogonal confirmation

3. Overbought/Oversold Analysis Layer (RSI)

Components: RSI with adjustable threshold levels

Purpose: Identify potential reversal zones and market extremes

Integration Rationale:

RSI provides mean-reversion context to momentum signals

Extreme readings (oversold/overbought) indicate potential exhaustion points

This layer prevents entry at statistically unfavorable price levels

The combination of momentum (directional) and mean-reversion (cyclical) indicators creates a balanced analytical framework

4. Market Participation Layer (Volume Analysis)

Components: Volume surge detection relative to moving average

Purpose: Validate price movements with corresponding volume activity

Integration Rationale:

Volume confirms the significance of price movements

Volume surge detection identifies institutional or significant market participation

This layer addresses the critical aspect of market conviction, filtering out low-confidence price movements

Synergistic Operation Mechanism

The script operates through a sequential validation process:

Stage 1: Signal Initiation

Triggered by either MACD crossover or RSI entering extreme zones

This initial trigger has high sensitivity but low specificity

Multiple trigger mechanisms ensure the system remains responsive to different market conditions

Stage 2: Trend Context Validation

Price must be positioned correctly relative to both SMA-50 and SMA-200

For buy signals: Price > SMA-50 > SMA-200 (bullish alignment)

For sell signals: Price < SMA-50 < SMA-200 (bearish alignment)

This layer eliminates approximately 40-60% of potential false signals by enforcing trend discipline

Stage 3: Volume Confirmation

Must demonstrate above-average volume participation (configurable multiplier)

Volume surge provides statistical confidence in the price movement

This layer addresses the "participation gap" where price moves without corresponding volume

Stage 4: Signal Quality Assessment

Each condition contributes to a quality score (0-100)

Higher scores indicate stronger multi-dimensional alignment

Quality rating helps users differentiate between marginal and high-conviction signals

Original Control Mechanisms

1. Signal Cooldown System

Purpose: Prevent signal overload and encourage trading discipline

Mechanism:

After any signal generation, the system enters a user-defined cooldown period

During this period, no new signals of the same type are generated

This reduces emotional trading decisions and filters out clustered, lower-quality signals

Empirical testing suggests optimal cooldown periods vary by timeframe (5-10 bars for daily, 10-20 for 4-hour)

2. Visual State Tracking

Purpose: Provide intuitive market phase identification

Mechanism:

After a buy signal: Subsequent candles are tinted light blue

After a sell signal: Subsequent candles are tinted light orange

This creates a visual "holding period" reference

Users can quickly identify which system state is active and for how long

Practical Implementation Guidelines

Parameter Configuration Strategy

Timeframe Adaptation:

Lower timeframes: Increase volume multiplier (2.0-3.0x) and use shorter cooldown periods

Higher timeframes: Lower volume requirements (1.5-2.0x) and extend confirmation periods

Market Regime Adjustment:

Trending markets: Emphasize trend alignment and MACD components

Range-bound markets: Increase RSI sensitivity and enable volatility filtering

Signal Level Selection:

Level 1: Suitable for active traders in high-liquidity markets

Level 2: Balanced approach for most market conditions

Level 3: Conservative setting for high-probability setups only

Risk Management Integration

Use quality scores as position sizing guides

Higher quality signals (Q≥80) warrant standard position sizes

Medium quality signals (60≤Q<80) suggest reduced position sizing

Lower quality signals (Q<60) recommend caution or avoidance

Empirical Limitations and Considerations

Statistical Constraints

No trading system guarantees profitability

Historical performance does not predict future results

System effectiveness varies by market conditions and timeframes

Maximum historical win rates in backtesting range from 55-65% in optimal conditions

Market Regime Dependencies

Strong Trending Markets: System performs best with clear directional movement

High Volatility/Ranging Markets: Increased false signal probability

Low Volume Conditions: Volume confirmation becomes less reliable

User Implementation Requirements

Time Commitment: Regular monitoring and parameter adjustment

Market Understanding: Basic knowledge of technical analysis principles

Discipline: Adherence to signal rules and risk management protocols

Technical Validation Framework

Backtesting Methodology

Multi-timeframe analysis across different market conditions

Parameter optimization through walk-forward analysis

Out-of-sample validation to prevent curve fitting

Performance Metrics Tracked

Win rate percentage across different signal qualities

Average win/loss ratio per signal category

Maximum consecutive wins/losses

Risk-adjusted return metrics

Innovative Contributions

Multi-Dimensional Scoring System

Original quality scoring algorithm weighting each dimension appropriately

Dynamic adjustment based on market conditions

Visual representation through signal labels and information panel

Integrated Information Dashboard

Real-time display of all system dimensions

Color-coded status indicators for quick assessment

Historical context for current signal generation

Adaptive Filtering Mechanism

Configurable strictness levels without code modification

User-adjustable sensitivity across all dimensions

Preset configurations for different trading styles

Conclusion and Appropriate Usage

The PMSS represents a sophisticated but accessible approach to multi-dimensional technical analysis. Its strength lies not in predictive accuracy but in systematic risk management through layered confirmation. Users should approach this tool as:

A Framework for Analysis: Rather than a black-box trading system

A Decision Support Tool: To be combined with fundamental analysis and market context

A Learning Instrument: For understanding how different analytical dimensions interact

The most effective implementation combines this technical framework with sound risk management principles, continuous learning, and adaptation to evolving market conditions. As with all technical tools, success depends more on the trader's discipline and judgment than on the tool itself.

Disclaimer: This documentation describes the technical operation of the PMSS indicator. Trading involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Users should thoroughly test any trading system in a risk-free environment before committing real capital.

Smart Liquidity & Step-TrendSmart Liquidity & Step-Trend

Overview

The Smart Liquidity & Step-Trend is a technical analysis tool designed to identify market manipulation points, specifically Liquidity Sweeps, and filter them using a Dynamic Multi-Timeframe (MTF) Trend.

By combining Price Action concepts with institutional flow logic, this indicator helps traders spot high-probability reversal zones where "Smart Money" typically enters the market by capturing retail stop-losses.

The Core Concept: Where is the Liquidity?

Markets do not move randomly. Institutional players require significant liquidity to fill their large orders. This liquidity is often found where retail traders place their stop-loss orders: above obvious swing highs and below obvious swing lows.

A Liquidity Sweep occurs when the price briefly breaks through these key levels to trigger stops/orders and then immediately reverses back into the range. This indicator visualizes these events as potential turning points.

To increase the probability of success, the Step-Trend (EMA) provides a higher-timeframe context, ensuring you are aware of the dominant market direction.

Key Features

Advanced Sweep Detection: Automatically identifies false breakouts of key swing highs and lows.

Dynamic MTF Logic:

- Trend Filter: The EMA (Exponential Moving Average) is calculated on a timeframe of your choice (e.g., 4H) even while viewing a lower timeframe (e.g., 15m).

- MTF Swings: Support and Resistance zones are derived from MTF data for higher reliability.

Temporary vs. Historical Zones:

- Mitigation Logic (Default): Zones are automatically deleted once the price closes through them. This keeps your chart clean, showing only active and relevant levels that haven't been "tested" yet.

- History Mode: Toggle "Show Historical Zones" to keep all past levels on the chart for backtesting and analysis.

ATR Filter (Zone Importance): Adjustable sensitivity to filter out market noise and focus on significant liquidity grabs.

How to Trade with This Indicator

1. Trend Confluence (Recommended)

This is the highest probability setup.

- BUY Signal: Look for a "SUPPORT" zone (teal) forming below the price while the Step-Trend EMA indicates an uptrend. This suggests a "buy-the-dip" manipulation. Use the "Trend Confluence Buy Signal" alert.

- SELL Signal: Look for a "RESISTANCE" zone (orange) forming above the price while the Step-Trend EMA indicates a downtrend. Use the "Trend Confluence Sell Signal" alert.

2. Scalping & Reversals

- Users can utilize the "SUPPORT" and "RESISTANCE" zones as potential targets or quick scalp entry points even against the main trend. Use the "Any Trend" sweep alerts for this style of trading.

Settings Explained

- Liquidity & Trend Timeframe: The timeframe used for trend calculation and swing detection.

- Swing Sensitivity: How "obvious" a high or low must be to be considered a liquidity target.

- Zone Importance (ATR Filter): Defines how deep the sweep must be relative to current volatility.

- Show Historical Zones: Switch between a clean chart (temporary zones) and a backtesting view (historical zones).

Important Notice:

No indicator is 100% accurate. This tool is intended to confirm your own analysis and trading strategies. Always use proper Risk Management and do not trade based on just one indicator.

I hope this tool will help you improve your trading!

_mr_beach Liquidity Sweep + VWAP V2 Trend Filter, Presets_mr_beach Liquidity Sweep + VWAP Reversal V2 (Trend Filter, Presets)

Overview

This strategy models a common institutional market behavior:

Liquidity is taken above the previous day’s high or below the previous day’s low, followed by a return toward fair value (VWAP) and a reversal in the direction of the dominant trend.

The script is designed as a TradingView Strategy for systematic backtesting and optimization.

________________________________________

Core Logic

• Liquidity Levels

o Previous Day High

o Previous Day Low

Used as typical stop-liquidity zones.

• Fair Value

o VWAP is used as confirmation that price has returned to a fair value area.

• Trend Filter

o EMA-based trend direction filter to avoid counter-trend trades.

________________________________________

Trading Rules

Trend Filter

• Long trades only when price closes above EMA.

• Short trades only when price closes below EMA.

Liquidity Sweep

• Bullish sweep: Price trades below Previous Day Low.

• Bearish sweep: Price trades above Previous Day High.

Entry Confirmation

• Long

o Sweep below Previous Day Low

o Close back above Previous Day Low

o Close above VWAP

• Short

o Sweep above Previous Day High

o Close back below Previous Day High

o Close below VWAP

________________________________________

Risk Management

• Stop Loss: ATR-based

• Take Profit: ATR-based

• Risk automatically adapts to market volatility.

• All multipliers are user-adjustable.

________________________________________

Preset Profiles

The script includes ready-to-use preset profiles:

• Index – conservative, session-based, one trade per day

• Forex – session-filtered, moderate volatility settings

• Crypto – higher volatility parameters, no session filter

• Custom – fully manual configuration

Presets control EMA length, ATR settings, SL/TP multipliers, session usage, and trade frequency.

________________________________________

Session & Trade Control

• Optional session filter (default: US regular session)

• Optional one trade per day limit to reduce overtrading and noise

________________________________________

Chart Elements

• EMA (trend direction)

• VWAP (fair value)

• Previous Day High / Low (liquidity zones)

________________________________________

Alerts

• Long setup: Liquidity sweep + VWAP reversal

• Short setup: Liquidity sweep + VWAP reversal

________________________________________

Recommended Usage

• Markets: Indices, liquid stocks, Forex majors, crypto

• Timeframes: 5m and 15m

• Parameters should be optimized per market and timeframe.

________________________________________

Disclaimer

This script is for educational and backtesting purposes only.

It does not constitute financial advice.

Performance depends on market conditions, timeframe, fees, and execution.

Tags: Liquidity, VWAP, EMA, Reversal, Sweep, Smart Money, ICT, ATR, Strategy

_mr_beach Liquidity Sweep + VWAP ReversalLiquidity Sweep + VWAP Reversal (Trend Filter, Session, 1 Trade per Day)

Overview

This strategy models a common institutional market behavior: liquidity is taken above the previous day’s high or below the previous day’s low, followed by a return toward fair value (VWAP) and a reversal in the direction of the prevailing trend.

Designed as a TradingView strategy for structured backtesting in the Strategy Tester.

Core Components

Liquidity Levels: Previous Day High / Previous Day Low

Fair Value Reference: VWAP

Trend Filter: EMA (default: 200)

Volatility-Based Risk: ATR

Trading Rules

Trend Filter

Long only when price closes above EMA

Short only when price closes below EMA

Liquidity Sweep

Bullish sweep: Low < Previous Day Low

Bearish sweep: High > Previous Day High

Entry Confirmation

Long: After a sweep below the Previous Day Low, price closes back above the level and above VWAP

Short: After a sweep above the Previous Day High, price closes back below the level and below VWAP

Risk Management

Stop Loss: ATR-based (slATR)

Take Profit: ATR-based (tpATR)

Automatically adapts to changing market volatility

Session & Trade Frequency

Optional session filter (default: 09:30–16:00 exchange time)

Optional one trade per day limit to reduce overtrading

Chart Elements

EMA (trend direction)

VWAP (fair value)

Previous Day High / Low (liquidity zones)

Alerts

Long setup: Liquidity sweep + VWAP reversal

Short setup: Liquidity sweep + VWAP reversal

Recommended Usage

Markets: Indices, liquid stocks, Forex majors, crypto

Timeframes: 5m, 15m

Note: Parameters such as ATR multipliers and session settings should be optimized per market

Disclaimer

This is a backtesting strategy, not financial advice.

Results depend on market conditions, timeframe, fees, and slippage.

Tags: Liquidity, VWAP, EMA, Reversal, Sweep, Smart Money, ICT, ATR, Strategy

Kill Zone Intraday Momentum Strategy"Re-published in full compliance with TradingView House Rules, featuring realistic risk management and backtesting parameters."

This script is an intraday trend-following strategy optimized for the KOSPI market, specifically tested on KODEX 200 Leverage (122630). It utilizes the "Kill Zone" concept to determine the market's directional bias for the day.

### Strategy Logic

The strategy focuses on the first hour of the Korean market opening (09:00 - 10:00 KST).

Directional Identification: The script analyzes the 1-hour candle formed between 09:00 and 10:00.

If the candle is Bullish (Close > Open), it establishes a LONG bias.

If the candle is Bearish (Close < Open), it establishes a SHORT bias.

Entry Timing: At exactly 10:00 AM, the strategy executes an entry based on the identified bias. Users can toggle between the 1H Close or the 15M Close for the entry price.

Exit Strategy (EOD): To mitigate overnight gap risks, all positions are forcibly closed at a user-defined "End of Day" hour (Default: 15:00 KST).

### Realistic Backtesting Parameters

To provide transparent and non-misleading results, this strategy adheres to strict risk management:

Initial Capital: 10,000,000 KRW

Risk Per Trade: 10% of total equity (Sustainable risk management).

Cost Simulation: Includes a 0.04% commission and 2 ticks of slippage to reflect actual exchange conditions.

Tested Symbol: Optimized for 122630 (KODEX 200 Leverage) on a 15-minute timeframe.

### How to Use

Set your chart timezone to Asia/Seoul.

Apply the script to a lower timeframe (e.g., 15 minutes) to see the Kill Zone highlights and labels.

Use the Dashboard on the top right to monitor real-time statistics like Win Rate and Net Profit.

-------

본 스크립트는 KOSPI 시장의 개장 초기 변동성(Kill Zone)을 활용한 일중 추세 추종 전략입니다. KODEX 200 레버리지(122630) 종목에서 자본금 1,000만 원을 기준으로 최적화되었습니다.

9시부터 10시까지의 1시간봉 방향성을 바탕으로 당일의 매수/매도 우위를 판단하며, 장 마감 시점에 모든 포지션을 정리하여 오버나잇 리스크를 배제합니다. 하우스 룰 준수를 위해 자산의 10%만을 진입 수량으로 설정하고 수수료와 슬리피지를 반영하여 현실적인 백테스트 결과를 제공합니다.

ATR# ATR Trailing Stop Multi-Strategy v7 with Pivot & GST

## Overview

A comprehensive multi-indicator trading strategy that combines multiple technical analysis approaches with sophisticated risk management. The strategy uses a confirmation-based system where trades are executed only when multiple indicators agree on the direction.

## Core Strategy Logic

### Signal Confirmation System

- **Entry Condition**: Requires at least 3 confirmation points from different indicators

- **Weighted Indicators**:

- Dow Theory (Weight: 2 points)

- ATR Trailing Stop (Weight: 2 points)

- Gaussian Smooth Trend (Weight: 1 point)

- KAMA (Weight: 1 point)

- VWMA (Weight: 1 point)

- Alligator (Weight: 1 point)

### Exit Conditions

- **Profit Exit**: When opposite signals achieve 3+ confirmation points

- **Stop Loss**: Fixed percentage stop loss (configurable)

- **Filter-Based Exit**: Signals from individual indicators when filters are violated

## Technical Indicators

### 1. Dow Theory Filter

- Analyzes volume and volatility conditions

- Uses SMA 20/50 crossovers for trend direction

- Volume must exceed MA by threshold (default: 1.5x)

- NATR must exceed threshold (default: 1.0%)

### 2. ATR Trailing Stop System

- Three ATR-based trailing lines (Fast/Medium/Slow)

- Fast: ATR(5) × 0.5 multiplier

- Medium: ATR(10) × 1.5 multiplier

- Slow: ATR(20) × 3.0 multiplier

- State changes when medium line crosses slow line

### 3. Gaussian Smooth Trend (GST)

- Advanced smoothing using DEMA, Gaussian filter, and SMMA

- Includes standard deviation bands for volatility filtering

- Multiple color schemes available for visualization

### 4. KAMA (Kaufman Adaptive Moving Average)

- Two KAMA lines with different lengths (10, 24)

- Adaptive smoothing based on market volatility

- Signals generated on crossovers

### 5. VWMA (Volume Weighted Moving Average)

- Price weighted by volume

- Signals on price crossing VWMA

### 6. Alligator Indicator

- Three SMMA lines (Jaw/Teeth/Lips)

- Standard Williams Alligator settings

- Signals based on line alignment and price position

## Entry Block Filters

### ADX Filter (Optional)

- Filters trades based on trend strength

- Configurable min/max values for long and short positions

- Default: ADX between 15-60

### RSI Filter (Optional)

- Additional RSI-based filtering

- Separate ranges for long and short positions

- Default Long: RSI 20-70, Short: RSI 30-80

### NATR Filter (Optional)

- Filters based on normalized ATR

- Ensures minimum volatility for valid signals

- Default Long/Short: NATR 0.5-5.0%

## Additional Filters

### CCI Filter

- Filters signals based on CCI momentum

- Oversold condition for longs: CCI > -100 and rising

- Overbought condition for shorts: CCI < 100 and falling

### Volatility Filter

- Minimum ATR percentage requirement

- Default: 0.3% minimum ATR/price ratio

### Distance Filter

- Minimum distance from Alligator lips in pips

- Ensures sufficient movement before entry

- Default: 10 pips minimum

## Pivot Points Support

- Multiple pivot point calculation methods:

- Traditional

- Fibonacci

- Woodie

- Classic

- DM

- Camarilla

- Multiple timeframe support (Daily, Weekly, Monthly, etc.)

- Visual display of pivot levels and labels

## Risk Management

### Stop Loss

- Configurable percentage-based stop loss

- Default: 2.5%

- Applied immediately on entry

### Position Management

- Single position only (no pyramiding)

- Position tracking with P/L calculation

- Visual exit lines for individual indicator signals

## Visual Features

### Signal Display

- Colored arrows for each indicator signal

- Entry/Exit labels with price information

- Horizontal exit lines for visual confirmation

- All indicators can be toggled on/off

### Color Schemes

- GST with multiple color modes

- Customizable pivot point colors

- Consistent color coding across indicators

## Alerts

- Entry alerts for both long and short positions

- Exit alerts for both profit and stop loss exits

- Individual indicator alerts available

## Settings Overview

### Strategy Settings

- Dow Theory thresholds (Volume, NATR)

- Stop loss percentage

- ATR Trailing parameters

- Indicator toggles and weights

### Filter Settings

- Entry block filters (ADX, RSI, NATR)

- CCI parameters

- Volatility and distance filters

### Visual Settings

- Show/hide indicators

- Arrow and label display

- Color scheme selection

### Pivot Settings

- Calculation method

- Timeframe

- Level colors and visibility

## Usage Recommendations

### Timeframes

- Works on all timeframes

- Pivot points automatically adjust to timeframe

- Recommended: 15-minutes and above

### Market Conditions

- Best in trending markets

- Multiple filters help avoid choppy conditions

- Volume confirmation adds reliability

### Customization

- Adjust confirmation thresholds for more/less aggressive trading

- Modify filters based on market volatility

- Fine-tune stop loss based on risk tolerance

## Performance Notes

- Strategy uses close prices for order execution

- Maximum 500 labels to prevent chart clutter

- All calculations in real-time

- Historical backtesting supported

## Important Notes

- Past performance doesn't guarantee future results

- Test thoroughly before live trading

- Adjust parameters for specific instruments

- Consider commission and slippage in backtesting

Axis-Pro System | Trend Structure + Fibonacci Pullbacks Axis-Pro System is a comprehensive Trend Following strategy designed to trade high-probability pullbacks. Unlike indicators that merely chase price, this system patiently waits for market structure alignment before seeking an entry.

The system is built on the premise of "Quality over Quantity", utilizing volatility and structure filters to avoid choppy markets (ranges) and false breakouts.

🧠 Strategy Logic

The system makes decisions based on a strict 4-step hierarchy:

Higher Timeframe (HTF) Bias:

Analyzes the trend on a higher timeframe to ensure we are trading in the direction of the dominant flow.

Structure & BOS (Break of Structure):

Identifies clear impulses that break previous highs or lows. Once a BOS is confirmed, the system "arms" the trade and waits.

Fibonacci Zone Pullback:

It does not chase the breakout. Instead, it waits for a pullback into the "Discount Zone" (Golden Zone, configurable between 0.382 and 0.618) to improve the Risk/Reward ratio.

Validation & Trigger:

Uses an ATR expansion check to filter out low-volatility periods.

Requires candle confirmation and alignment with fast EMAs before pulling the trigger.

🛡️ Risk Management

The system incorporates advanced position management using a split execution model (50/50):

Dynamic Stop Loss: Automatically calculated using an ATR multiplier or the recent Swing High/Low (whichever offers better protection).

TP1 (Take Profit 1): Closes 50% of the position at a fixed R-multiple (e.g., 1.5R) to lock in profit and moves the Stop Loss to Break-Even.

TP2 (Runner): The remaining 50% is left to run for higher targets (e.g., 3.0R) or until the trend bends, maximizing gains during strong moves.

Trailing Stop: Optional feature to trail price with a fast EMA once the first target is hit.

⚙️ Settings & Features

The script is highly customizable for different assets (Crypto, Forex, Indices):

Date Range Filter: Includes a date selector to perform precise Backtesting on specific periods (e.g., testing specifically during a Bear Market vs. Bull Market).

Auto Trendlines: Automatically draws relevant trendlines for visual support.

Quality Filters: Options to toggle the EMA 200 filter and breakout buffers.

⚠️ Disclaimer

This strategy is a tool for analysis and backtesting purposes. Past performance does not guarantee future results. It is highly recommended to test the strategy on a Demo account first and adjust parameters according to the volatility of the specific asset being traded. Always use responsible risk management.

Lakshmi - Low Volatility Range Breakout (LVRB)⚡️ Overview

The Low Volatility Range Breakout (LVRB) indicator is designed to identify consolidation phases characterized by suppressed volatility and generate actionable signals when price breaks out of these ranges. The underlying premise is rooted in the market principle that periods of low volatility often precede significant directional moves—volatility contraction leads to expansion.

Important Note on Optimization: The default parameter settings of this indicator have been specifically optimized for BTCUSDT on the 2-hour (2H) timeframe. While the indicator can be applied to other instruments and timeframes, users are encouraged to adjust the parameters accordingly to suit different trading conditions and asset characteristics.

This indicator automates the detection of "quiet" accumulation/distribution zones and provides clear visual cues and alerts when a breakout occurs.

⚡️ How to Use

1. Add the indicator to your chart. Default settings are optimized for BTCUSDT 2H.

2. Wait for a gray box to appear—this indicates a qualified low-volatility range is forming.

3. Monitor for breakout signals:

• LONG (green triangle below bar): Price broke above the range. Consider entering a long position.

• SHORT (red triangle above bar): Price broke below the range. Consider entering a short position.

4. Set alerts using "LVRB LONG" or "LVRB SHORT" to receive notifications on confirmed breakouts.

5. Adjust parameters as needed for different instruments or timeframes.

Tip: Combine with volume analysis or trend filters for higher-probability setups.

⚡️ How It Works

1. Low Volatility Bar Detection

A bar is classified as "low volatility" when it meets the following criteria:

• True Range (TR) is at or below the average TR (Simple Moving Average) multiplied by a user-defined threshold.

• (Optional) Candle Body is at or below the average body size multiplied by a separate threshold.

This dual-filter approach helps isolate bars that exhibit genuine compression in both range and directional commitment.

2. Range Box Formation

When consecutive low-volatility bars are detected, the indicator begins constructing a consolidation box:

• The box expands to encompass the high and low of qualifying bars.

• A minimum number of bars and a minimum fraction of low-volatility bars are required for the box to become "qualified" (active).

• A configurable tolerance allows for a limited number of consecutive non-low-vol bars within the sequence, accommodating minor noise without invalidating the range.

• If the box height exceeds a maximum threshold (defined as a multiple of the base ATR at sequence start), the range is invalidated.

3. Breakout Detection

Once a qualified range is established, the indicator monitors for breakouts:

• Wick Mode: Requires both a wick pierce beyond the range boundary AND a close outside the range.

• Close Mode: Requires only a close beyond the range boundary.

• (Optional) Breakout Body Filter: The breakout candle's body must exceed a multiple of the average body size at range formation.

• (Optional) Candle Direction Filter: Bullish breakouts require a green candle; bearish breakouts require a red candle.

Signals are displayed in real-time and confirmed upon bar close.

⚡️ Inputs & Parameters

• Volatility Window: Lookback period for calculating average TR and average body size.

• TR Multiplier: A bar's TR must be ≤ avgTR × this value to qualify as low-vol.

• Body Multiplier: A bar's body must be ≤ avgBody × this value (if body filter is enabled).

• Use Body Filter: Toggle the body size filter on/off.

• Min Bars in Box: Minimum number of bars required for a range to become qualified.

• Min Low-Vol Fraction: Minimum proportion of bars in the sequence that must be low-vol.

• Allowed Consecutive Non-Low-Vol Bars: Tolerance for consecutive bars that do not meet low-vol criteria.

• Max Box Height: Maximum allowed range height as a multiple of the base ATR.

• Breakout Mode: Choose between "Wick" (pierce + close) or "Close" (close only).

• Breakout Body Multiplier: Require breakout candle body ≥ avgBody × this value (1.0 = OFF).

• Require Candle Direction: Enforce green candle for LONG, red candle for SHORT.

⚡️ Visual Features

• Consolidation Boxes: Displayed in neutral (gray) color during formation. Upon a confirmed breakout, the box is colored green for bullish breakouts or red for bearish breakouts.

• Breakout Signals:

• LONG: Green upward triangle displayed below the price bar with "LONG" label.

• SHORT: Red downward triangle displayed above the price bar with "SHORT" label.

• Range Levels: Optional horizontal plots for the active range's high and low.

• Invalidated Boxes: Optionally retained in neutral (gray) color or deleted from the chart.

• Full Customization: Colors, transparency, and border width are all adjustable.

⚡️ Alerts

Two alert conditions are available:

• LVRB LONG: Triggered on a confirmed bullish breakout (bar close).

• LVRB SHORT: Triggered on a confirmed bearish breakout (bar close).

⚡️ Use Cases

• Breakout Trading: Enter positions when price escapes a well-defined low-volatility range.

• Volatility Expansion Plays: Anticipate increased volatility following periods of compression.

• Filtering Choppy Markets: Avoid trading during extended consolidation; wait for confirmed breakouts.

• Multi-Timeframe Analysis: Use on higher timeframes to identify major consolidation zones.

⚡️ Notes

• Best used in conjunction with volume analysis, trend context, or support/resistance levels for confirmation.

• Performance varies across instruments and timeframes; backtesting and parameter optimization are recommended.

⚡️ Credits

Developed by Lakshmi. Inspired by volatility contraction principles and range breakout methodologies.

⚡️ Disclaimer

This indicator is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a guarantee of profits. Trading financial instruments involves substantial risk, and you may lose more than your initial investment. Past performance, whether indicated by backtesting or historical analysis, does not guarantee future results. The use of this indicator does not ensure or promise any profits or protection against losses. Users are solely responsible for their own trading decisions and should conduct their own research and/or consult with a qualified financial advisor before making any investment decisions. By using this indicator, you acknowledge and accept that you bear full responsibility for any trading outcomes.

Ultimate MACD [captainua]Ultimate MACD - Comprehensive MACD Trading System

Overview

This indicator combines traditional MACD calculations with advanced features including divergence detection, volume analysis, histogram analysis tools, regression forecasting, strong top/bottom detection, and multi-timeframe confirmation to provide a comprehensive MACD-based trading system. The script calculates MACD using configurable moving average types (EMA, SMA, RMA, WMA) and applies various smoothing methods to reduce noise while maintaining responsiveness. The combination of these features creates a multi-layered confirmation system that reduces false signals by requiring alignment across multiple indicators and timeframes.

Core Calculations

MACD Calculation:

The script calculates MACD using the standard formula: MACD Line = Fast MA - Slow MA, Signal Line = Moving Average of MACD Line, Histogram = MACD Line - Signal Line. The default parameters are Fast=12, Slow=26, Signal=9, matching the traditional MACD settings. The script supports four moving average types:

- EMA (Exponential Moving Average): Standard and most responsive, default choice

- SMA (Simple Moving Average): Equal weight to all periods

- RMA (Wilder's Moving Average): Smoother, less responsive

- WMA (Weighted Moving Average): Recent prices weighted more heavily

The price source can be configured as Close (standard), Open, High, Low, HL2, HLC3, or OHLC4. Alternative sources provide different sensitivity characteristics for various trading strategies.

Configuration Presets:

The script includes trading style presets that automatically configure MACD parameters:

- Scalping: Fast/Responsive settings (8,18,6 with minimal smoothing)

- Day Trading: Balanced settings (10,22,7 with minimal smoothing)

- Swing Trading: Standard settings (12,26,9 with moderate smoothing)

- Position Trading: Smooth/Conservative settings (15,35,12 with higher smoothing)

- Custom: Full manual control over all parameters

Histogram Smoothing:

The histogram can be smoothed using EMA to reduce noise and filter minor fluctuations. Smoothing length of 1 = raw histogram (no smoothing), higher values (3-5) = smoother histogram. Increased smoothing reduces noise but may delay signals slightly.

Percentage Mode:

MACD values can be converted to percentage of price (MACD/Close*100) for cross-instrument comparison. This is useful when comparing MACD signals across instruments with different price levels (e.g., BTC vs ETH). The percentage mode normalizes MACD values, making them comparable regardless of instrument price.

MACD Scale Factor:

A scale factor multiplier (default 1.0) allows adjusting MACD display size for better visibility. Use 0.3-0.5 if MACD appears too compressed, or 2.0-3.0 if too small.

Dynamic Overbought/Oversold Levels:

Overbought and oversold levels are calculated dynamically based on MACD's mean and standard deviation over a lookback period. The formula: OB = MACD Mean + (StdDev × OB Multiplier), OS = MACD Mean - (StdDev × OS Multiplier). This adapts to current market conditions, widening in volatile markets and narrowing in calm markets. The lookback period (default 20) controls how quickly the levels adapt: longer periods (30-50) = more stable levels, shorter (10-15) = more responsive.

OB/OS Background Coloring:

Optional background coloring can highlight the entire panel when MACD enters overbought or oversold territory, providing prominent visual indication of extreme conditions. The background colors are drawn on top of the main background to ensure visibility.

Divergence Detection

Regular Divergence:

The script uses the MACD line (not histogram) for divergence detection, which provides more reliable signals. Bullish divergence: Price makes a lower low while MACD line makes a higher low. Bearish divergence: Price makes a higher high while MACD line makes a lower high. Divergences often precede reversals and are powerful reversal signals.

Pivot-Based Divergence:

The divergence detection uses actual pivot points (pivotlow/pivothigh) instead of simple lowest/highest comparisons. This provides more accurate divergence detection by identifying significant pivot lows/highs in both price and MACD line. The pivot-based method compares two recent pivot points: for bullish divergence, price makes a lower low while MACD makes a higher low at the pivot points. This method reduces false divergences by requiring actual pivot points rather than just any low/high within a period.

The pivot lookback parameters (left and right) control how many bars on each side of a pivot are required for confirmation. Higher values = more conservative pivot detection.

Hidden Divergence:

Continuation patterns that signal trend continuation rather than reversal. Bullish hidden divergence: Price makes a higher low but MACD makes a lower low. Bearish hidden divergence: Price makes a lower high but MACD makes a higher high. These patterns indicate the trend is likely to continue in the current direction.

Zero-Line Filter:

The "Don't Touch Zero Line" option ensures divergences occur in proper context: for bullish divergence, MACD must stay below zero; for bearish divergence, MACD must stay above zero. This filters out divergences that occur in neutral zones.

Range Filtering:

Minimum and maximum lookback ranges control the time window between pivots to consider for divergence. This helps filter out divergences that are too close together (noise) or too far apart (less relevant).

Volume Confirmation System

Volume threshold filtering requires current volume to exceed the volume SMA multiplied by the threshold factor. The formula: Volume Confirmed = Volume > (Volume SMA × Threshold). If the threshold is set to 1.0 or lower, volume confirmation is effectively disabled (always returns true). This allows you to use the indicator without volume filtering if desired. Volume confirmation significantly increases divergence and signal reliability.

Volume Climax and Dry-Up Detection:

The script can mark bars with extremely high volume (volume climax) or extremely low volume (volume dry-up). Volume climax indicates potential reversal points or strong momentum continuation. Volume dry-up indicates low participation and may produce unreliable signals. These markers use standard deviation multipliers to identify extreme volume conditions.

Zero-Line Cross Detection

MACD zero-line crosses indicate momentum shifts: above zero = bullish momentum, below zero = bearish momentum. The script includes alert conditions for zero-line crosses with cooldown protection to prevent alert spam. Zero-line crosses can provide early warning signals before MACD crosses the signal line.

Histogram Analysis Tools

Histogram Moving Average:

A moving average applied to the histogram itself helps identify histogram trend direction and acts as a signal line for histogram movements. Supports EMA, SMA, RMA, and WMA types. Useful for identifying when histogram momentum is strengthening or weakening.

Histogram Bollinger Bands:

Bollinger Bands are applied to the MACD histogram instead of price. The calculation: Basis = SMA(Histogram, Period), StdDev = stdev(Histogram, Period), Upper = Basis + (StdDev × Deviation Multiplier), Lower = Basis - (StdDev × Deviation Multiplier). This creates dynamic zones around the histogram that adapt to histogram volatility. When the histogram touches or exceeds the bands, it indicates extreme conditions relative to recent histogram behavior.

Stochastic MACD (StochMACD):

Stochastic MACD applies the Stochastic oscillator formula to the MACD histogram instead of price. This normalizes the histogram to a 0-100 scale, making it easier to identify overbought/oversold conditions on the histogram itself. The calculation: %K = ((Histogram - Lowest Histogram) / (Highest Histogram - Lowest Histogram)) × 100. %K is smoothed, and %D is calculated as the moving average of smoothed %K. Standard thresholds are 80 (overbought) and 20 (oversold).

Regression Forecasting

The script includes advanced regression forecasting that predicts future MACD values using mathematical models. This helps anticipate potential MACD movements and provides forward-looking context for trading decisions.

Regression Types:

- Linear: Simple trend line (y = mx + b) - fastest, works well for steady trends