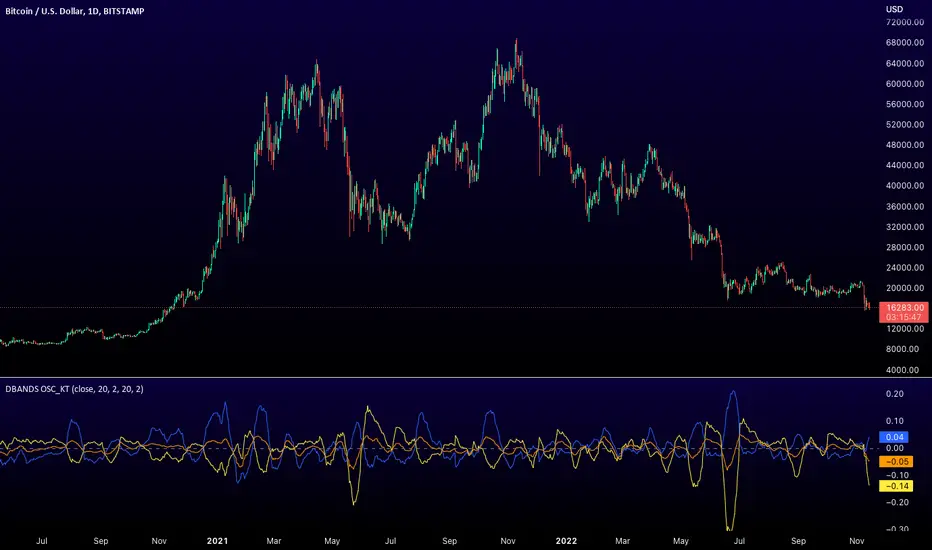

Distance Bands Oscillator_KT █ OVERVIEW

This tool is based on both Bollinger Bands and Keltner Channels, and measures 3 distances between the two, respectively.

Upper Kelt to Upper Bollinger Band

Lower Kelt to Lower Bollinger Band

Kelt Basis to Bollinger Basis Basis

Similar to the Band Width indicator, this can be used as a measure of volatility, and can be used to measure uptrend, downtrend and chop regions on a given chart.

Happy Trading,

ET

Recherche dans les scripts pour "bands"

HMA w/ SSE-Dynamic EWMA Volatility Bands [Loxx]This indicator is for educational purposes to lay the groundwork for future closed/open source indicators. Some of thee future indicators will employ parameter estimation methods described below, others will require complex solvers such as the Nelder-Mead algorithm on log likelihood estimations to derive optimal parameter values for omega, gamma, alpha, and beta for GARCH(1,1) MLE and other volatility metrics. For our purposes here, we estimate the rolling lambda (λ) value used to calculate EWMA by minimizing of the sum of the squared errors minus the long-run variance--a rolling window of the one year mean of squared log-returns. In practice, practitioners will use a λ equal to a standardized value put out by institutions such as JP Morgan. Even simpler than this, others use a ratio of (per - 1) / (per + 1) to derive λ where per is the lookback period for EWMA. Due to computation limits in Pine, we'll likely not see a true GARCH(1,1) MLE on Pine for quite some time, but future closed source indicators will contain some very interesting industry hacks to get close by employing modifications to EWMA. Enjoy!

Exponentially weighted volatility and its relationship to GARCH(1,1)

Exponentially weighted volatility--also called exponentially weighted moving average volatility (EWMA)--puts more weight on more recent observations. EWMA is calculated as follows:

σ*2 = λσ(n - 1)^2 + (1 − λ)u(n - 1)^2

The estimate, σn, of the volatility for day n (made at the end of day n − 1) is calculated from σn −1 (the estimate that was made at the end of day n − 2 of the volatility for day n − 1) and u^n−1 (the most recent daily percentage change).

The EWMA approach has the attractive feature that the data storage requirements are modest. At any given time, we need to remember only the current estimate of the variance rate and the most recent observation on the value of the market variable. When we get a new observation on the value of the market variable, we calculate a new daily percentage change to update our estimate of the variance rate. The old estimate of the variance rate and the old value of the market variable can then be discarded.

The EWMA approach is designed to track changes in the volatility. Suppose there is a big move in the market variable on day n − 1 so that u2n−1 is large. This causes our estimate of the current volatility to move upward. The value of λ governs how responsive the estimate of the daily volatility is to the most recent daily percentage change. A low value of λ leads to a great deal of weight being given to the u(n−1)^2 when σn is calculated. In this case, the estimates produced for the volatility on successive days are themselves highly volatile. A high value of λ (i.e., a value close to 1.0) produces estimates of the daily volatility that respond relatively slowly to new information provided by the daily percentage change.

The RiskMetrics database, which was originally created by JPMorgan and made publicly available in 1994, used the EWMA model with λ = 0.94 for updating daily volatility estimates. The company found that, across a range of different market variables, this value of λ gives forecasts of the variance rate that come closest to the realized variance rate. In 2006, RiskMetrics switched to using a long memory model. This is a model where the weights assigned to the u(n -i)^2 as i increases decline less fast than in EWMA.

GARCH(1,1) Model

The EWMA model is a particular case of GARCH(1,1) where γ = 0, α = 1 − λ, and β = λ. The “(1,1)” in GARCH(1,1) indicates that σ^2 is based on the most recent observation of u^2 and the most recent estimate of the variance rate. The more general GARCH(p, q) model calculates σ^2 from the most recent p observations on u2 and the most recent q estimates of the variance rate.7 GARCH(1,1) is by far the most popular of the GARCH models. Setting ω = γVL, the GARCH(1,1) model can also be written:

σ(n)^2 = ω + αu(n-1)^2 + βσ(n-1)^2

What this indicator does

Calculate log returns log(close/close(1))

Calculates Lambda (λ) dynamically by minimizing the sum of squared errors. I've restricted this to the daily timeframe so as to not bloat the code with additional logic required to derive an annualized EWMA historical volatility metric.

After the Lambda is derived, EWMA is calculated one last time and the result is the daily volatility

This daily volatility is multiplied by the source and the multiplier +/- the HMA to create the volatility bands

Finally, daily volatility is multiplied by the square-root of days per year to derive annualized volatility. Years are trading days for the asset, for most everything but crypto, its 252, for crypto is 365.

Polynomial Regression Bands w/ Extrapolation of Price [Loxx]Polynomial Regression Bands w/ Extrapolation of Price is a moving average built on Polynomial Regression. This indicator paints both a non-repainting moving average and also a projection forecast based on the Polynomial Regression. I've included 33 source types and 38 moving average types to smooth the price input before it's run through the Polynomial Regression algorithm. This indicator only paints X many bars back so as to increase on screen calculation speed. Make sure to read the tooltips to answer any questions you have.

What is Polynomial Regression?

In statistics, polynomial regression is a form of regression analysis in which the relationship between the independent variable x and the dependent variable y is modeled as an nth degree polynomial in x. Polynomial regression fits a nonlinear relationship between the value of x and the corresponding conditional mean of y, denoted E(y |x). Although polynomial regression fits a nonlinear model to the data, as a statistical estimation problem it is linear, in the sense that the regression function E(y | x) is linear in the unknown parameters that are estimated from the data. For this reason, polynomial regression is considered to be a special case of multiple linear regression .

Related indicators

Polynomial-Regression-Fitted Oscillator

Polynomial-Regression-Fitted RSI

PA-Adaptive Polynomial Regression Fitted Moving Average

Poly Cycle

Fourier Extrapolator of Price w/ Projection Forecast

Bitcoin Support BandsSMA and EMA support/resistance bands for Bitcoin. Based on 4 week multiples; 1 month, 3 month, 6 month, 1 year, 2 year, 4 year.

Bollinger Bands SqueezeBollinger Bands set to only display when a squeeze is taking place. Squeeze will be highlighted.

SMA EMA Bands [CraftyChaos]This indicator creates bands for SMA and EMA averages and adds an average of the two with the idea that price often touches one of them at support and resistance levels. Saves indicator space by combining all into one indicator

Greedy MA & Greedy Bollinger Bands This moving average takes all of the moving averages between 1 and 700 and takes the average of them all. It also takes the min/max average (donchian) of every one of those averages. Also included is Bollinger Bands calculated in the same way. One nice feature I have added is the option to use geometric calculations for. I also added regular bb calculations because this can be a major hog. Use this default setting on 1d or 1w. Enjoy!

ps, I call it greedy because the default settings wont work on lower time frames

Mayer Multiple Bands [TXMC]This Bitcoin indicator provides level bands using price distance from the 200 day moving average, also known as the Mayer Multiple.

The percentage levels are based on historical distribution of the Mayer Multiple since Bitcoin's inception, and are meant to inform the user of price action probabilities.

Usage examples:

The 25% line means that 25% of Bitcoin's price history has traded below that distance away from the 200 day moving average.

A value of 95% means that only 5% of Bitcoin's price history has extended that far above the 200 day moving average.

Levels displayed:

5% (5% chance of trading below)

10% (10% chance of trading below)

20%

75%

90% (10% chance of trading above)

95% (5% chance of trading above)

This indicator is for information purposes only . Use at your own discretion.

Accumulation/Distribution Bands & Signals (BTC, 1D, BITSTAMP) This is an accumulation/distribution indicator for BTC/USD (D) based on variations of 1400D and 120D moving averages and logarithmic regression. Yellow plot signals Long Term Accumulation, which is based on 1400D (200W) ALMA, orange plot signals Mid Term Accumulation and is based on 120D ALMA, and finally the red plot signals Long Term Distribution that's based on log regression. It should be noted that for red plot to work BTC 1D BITSTAMP graph must be used, because the function of the logarithmic regression was modified according to the x axis of the BITSTAMP data.

Signal bands have different coefficients; long term accumulation (yellow) and and the log regression (red) plots have the highest coefficients and mid term accumulation (orange) has the lowest coefficients. Coefficients are 6x, 3x and 1.5x for the red (sell) and yellow (buy) plots and 1x, 2x and 3x for the orange (buy) plot. Selling coefficient for the yellow and the orange plots are respectively 2x and 1x. Buy and sell signals are summed up accordingly and plotted at the top of the highest band.

Acknowledgement: Credits for the logarithmic regression function are due @memotyka9009 and Benjamin Cowen

Deviation BandsThis indicator plots the 1, 2 and 3 standard deviations from the mean as bands of color (hot and cold). Useful in identifying likely points of mean reversion.

Default mean is WMA 200 but can be SMA, EMA, VWMA, and VAWMA.

Calculating the standard deviation is done by first cleaning the data of outliers (configurable).

Bands %ABCThe % Bands multitool to keep volatility and reversals under control using quantitative approach and to trade using different signals.

Features

15 well known % bands

4 display modes ( All Lines , Average Line , Breakouts Histogram , Middle Crosses Histogram )

Bands Customization

Readable and optimized code

Implemented bands

Bomar Bands %BOMAR (by Marc Chaikin and Bob Brogan)

Bollinger Bands %B (by John Bollinger)

Apirine Exponential Standard Deviation Bands (by Vitali Apirine)

Standard Error Bands %SEB (by Jon Andersen)

Kirshenbaum Bands %KB (by Paul Kirshenbaum)

Acceleration Bands %A (by Price Headley)

Keltner Channels %KC (by Chester W. Keltner)

Stoller Average Range Channels Bands %STARC (by Manning Stoller)

Donchian Channels %DC (by Richard Donchian)

Interquartile Range Bands %IQR (by Alex Orekhov)

Median Absolute Deviation Bands %MAD (by Alex Orekhov)

Mean Absolute Deviation Bands %MEANAD (by Alex Orekhov)

Vervoort Volatility Bands %VVB (by Sylvain Vervoort)

High Low Bands %HLB

Projection Bands %PB (by Mel Widner)

Bands-Trailing Stop UtilityIntroduction

Bands and trailing stops are important indicators in technical analysis, while we could think that both are different they can be in fact closely related, at least in the way they are made. Bands and trailing stops can be made from a simple central tendency estimator, like a moving average, and from a volatility estimator like standard deviation, atr...etc.

This is why i propose this utility that allow you to make bands and trailing stops from any indicator in the price chart.

How To Use

All you have to do is select the indicator you want to make bands from in the settings, so just open the Bands-Trailing Stop Utility indicator settings and select your indicator in "Source". Make sure your source indicator is not in "hide" mode.

For example here i'am using a moving average as source for the indicator. Mult control how spread the bands are from each others, by default mult = 1, if we use mult = 2 we get :

Mult can be non-integer as well as lower than 1 (when lower than 1 the bands would be closer to each others)

Error/Volatility Estimators

You can choose from a wide variety of volatility estimators, select the estimator from the "Method" scrolling parameter in settings, by default the indicator will use the running mean absolute error (MAE) which don't use length. Other estimators use length, making length = to the period of the source indicator can help get better results.

The root moving averaged squared error (RMASE) is just the square root of the simple moving average of the squared difference between the closing price and the source indicator. length control the period of the moving average of RMASE.

You can also use the average true range with period length. It might work better with low lagging moving averages.

The range is simply the difference between the highest and lowest over length periods of the source indicator.

Stdev is simply the price running standard deviation.

Trailing Stop

When the trailing stop mode is checked the bands will be replaced by a trailing stop, the trailing stop will still depend on every settings of the indicator like mult/volatility estimator...etc.

Conclusion

You might find an use to this tool if you want to make bands/trailing stops from pretty much everything. The indicator used as source for the examples is a smooth exponential averager that i could share if i see interest from peoples.

Thanks for reading !

Bollinger Bands TimeBollinger bands that are fixed to a time interval. The time interval can be set in minutes or days.

Parameters

Daily Interval: If checked then days are used for the interval. If unchecked then minutes will be used.

Interval: The interval to use for the indicator.

Balgat EkibiBands are calculated with the std error and variance of the price actions. So if price cross up or cross down the variance bands, you could expect a reversal movement.

So if price cross up with the bands and after that there is a reversal candle movement, a short position could be taken.

If price cross down to the bands and after that there is a reversal candle movement, a long positon could be taken.

All risk management and money management is up to you.

Pivot-Based Channels & Bands [Misu]█ This Indicator is based on Pivot detection to show bands and channels.

The pivot price is similar to a resistance or support level. If the pivot level is breached, the price should continue in that direction. Or the price could reverse at or near this level.

█ Usages:

Use channels as a support & resistance zone.

Use bands as a support & resistance zone. It is also very powerfull to use it as a breakout.

Use mid bands & mid channels as a trend direction or trade filter as a more usual moving average.

█ Parameters:

Show Pivot Bands: show bands.

Show Pivot Mid Band: show mid bands.

Show Pivot Channels: show channels.

Show Pivot Mid Channel: show mid channels.

Deviation: deviation used to calculate pivot points.

Depth: depth used to calculate pivot points.

HL2 Moving Average with BandsThis indicator is designed to assist traders in identifying potential trade entries and exits for S&P 500 (ES) and Nasdaq-100 (NQ) futures. It calculates a Simple Moving Average (SMA) based on the HL2 value (average of high and low prices) of the current candle over a user-defined lookback period (default: 200 periods). The indicator plots this SMA as a blue line, providing a smoothed reference for price trends.

Additionally, it includes upper and lower bands calculated as a percentage (default: 0.5%) above and below the SMA, plotted as green and red lines, respectively. These bands act as dynamic thresholds to identify overbought or oversold conditions. The indicator generates trade signals based on price action relative to these bands:

Long Entry: A green upward triangle is plotted below the candle when the close crosses above the upper band, signaling a potential buy.

Close Long: A red square is plotted above the candle when the close crosses back below the upper band, indicating an exit for the long position.

Short Entry: A red downward triangle is plotted above the candle when the close crosses below the lower band, signaling a potential sell.

Close Short: A green square is plotted below the candle when the close crosses back above the lower band, indicating an exit for the short position.

The script is customizable, allowing users to adjust the SMA length and band percentage to suit their trading style or market conditions. It is plotted as an overlay on the price chart for easy integration with other technical analysis tools.

Recommended Time Frame and Settings for Trading S&P 500 and Nasdaq-100 Futures

Based on research and market dynamics for S&P 500 (ES) and Nasdaq-100 (NQ) futures, the 5-minute chart is recommended as the optimal time frame for day trading with this indicator. This time frame strikes a balance between capturing intraday trends and filtering out excessive noise, which is critical for futures trading due to their high volatility and leverage. The 5-minute chart aligns well with periods of high liquidity and volatility, such as the U.S. market open (9:30 AM–11:00 AM EST) and the afternoon session (2:00 PM–4:00 PM EST), when institutional traders are most active.

Why 5-minute? It allows traders to react to short-term price movements while avoiding the rapid fluctuations of 1-minute charts, which can be prone to false signals in choppy markets. It also provides enough data points to make the SMA and bands meaningful without the lag associated with longer time frames like 15-minute or hourly charts.

Recommended Settings

SMA Length: Set to 200 periods. This longer lookback period smooths the HL2 data, reducing noise and providing a reliable trend reference for the 5-minute chart. A 200-period SMA helps identify significant trend shifts without being overly sensitive to minor price fluctuations.

Band Percentage: 0.5% is more suitable for the volatility of ES and NQ futures on a 5-minute chart, as it generates fewer but higher-probability signals. Wider bands (e.g., 1%) may miss short-term opportunities, while narrower bands (e.g., 0.1%) may produce excessive false signals.

Trading Session Recommendations

Futures markets for ES and NQ are open nearly 24 hours (Sunday 6:00 PM EST to Friday 5:00 PM EST, with a daily break from 4:00 PM–5:00 PM EST), but not all hours are equally optimal due to varying liquidity and volatility. The best times to trade with this indicator are:

U.S. Market Open (9:30 AM–11:00 AM EST): This period is characterized by high volume and volatility, driven by the opening of U.S. equity markets and economic data releases (e.g., 8:30 AM EST reports like CPI or GDP). The indicator’s signals are more reliable during this window due to strong order flow and price momentum.

Afternoon Session (2:00 PM–4:00 PM EST): After the lunchtime lull, volume picks up as institutional traders return, and news or FOMC announcements often drive price action. The indicator can capture breakout moves as prices test the upper or lower bands.

Pre-Market (7:30 AM–9:30 AM EST): For traders comfortable with lower liquidity, this period can offer opportunities, especially around 8:30 AM EST economic releases. However, use tighter risk management due to wider spreads and potential volatility spikes.

Additional Tips

Avoid Low-Volume Periods: Steer clear of trading during low-liquidity hours, such as the overnight session (11:00 PM–3:00 AM EST), when spreads widen and price movements can be erratic, leading to false signals from the indicator.

Combine with Other Tools: Enhance the indicator’s effectiveness by pairing it with support/resistance levels, Fibonacci retracements, or volume analysis to confirm signals. For example, a long entry signal above the upper band is stronger if it coincides with a breakout above a key resistance level.

Risk Management: Given the leverage in futures (e.g., Micro E-mini contracts require ~$1,200 margin for ES), use tight stop-losses (e.g., below the lower band for longs or above the upper band for shorts) to manage risk. Aim for a risk-reward ratio of at least 1:2.

Test Settings: Backtest the indicator on a demo account to optimize the SMA length and band percentage for your specific trading style and risk tolerance. Micro E-mini contracts (MES for S&P 500, MNQ for Nasdaq-100) are ideal for testing due to their lower capital requirements.

Why These Settings and Time Frame?

The 5-minute chart with a 200-period SMA and 0.5% bands is tailored for the volatility and liquidity of ES and NQ futures during peak trading hours. The longer SMA period ensures the indicator captures meaningful trends, while the 0.5% bands are tight enough to signal actionable breakouts but wide enough to avoid excessive whipsaws. Trading during high-volume sessions maximizes the likelihood of valid signals, as institutional participation drives clearer price action.

By focusing on these settings and time frames, traders can leverage the indicator to capitalize on the dynamic price movements of S&P 500 and Nasdaq-100 futures while managing the inherent risks of these markets.

Adaptive RSI BandsThe RSI Band Optimizer is an innovative technical analysis tool designed to identify and display the most effective Relative Strength Index (RSI) band values for any given trading instrument. This powerful indicator dynamically calculates optimal overbought and oversold levels, moving beyond the traditional static 70/30 or 80/20 bands.

Core Functionality:

Dynamic RSI Band Calculation:

The indicator analyzes historical price data to determine the most effective RSI levels for identifying overbought and oversold conditions specific to the current trading instrument and timeframe.

Adaptive Optimization:

Rather than relying on external factors, the tool uses a proprietary algorithm that focuses solely on the relationship between historical RSI values and subsequent price movements. This pure RSI-based approach ensures that the bands are optimized for the indicator's own dynamics.

Continuous Recalibration:

The optimal RSI bands are continuously recalculated as new price data becomes available, ensuring that the indicator adapts to changing market conditions and remains relevant over time.

Key Inputs:

RSI Length:

Allows users to set the period for the RSI calculation. While the default is typically 14, users can adjust this to suit their trading style and the characteristics of the instrument they're trading.

Optimization Lookback:

Defines the historical period the indicator uses to calculate optimal bands. This balance between recent market behavior and longer-term patterns.

Band Sensitivity:

Enables fine-tuning of how aggressively the indicator adjusts the RSI bands. Higher sensitivity results in more frequent band adjustments, while lower sensitivity provides more stable levels.

What Makes It Unique:

Self-Contained Optimization:

Unlike indicators that rely on external data sources or comparisons, this tool focuses purely on optimizing RSI bands based on the indicator's own historical performance.

Instrument-Specific Bands:

By calculating optimal bands for each specific instrument, the indicator acknowledges that different assets may have different typical RSI ranges and behaviors.

Timeframe Adaptability:

The optimization process adapts to the selected timeframe, recognizing that optimal RSI bands may differ between short-term and long-term charts.

Dynamic Band Adjustment:

The continuous recalibration of bands allows the indicator to adapt to changing market volatility and trends, providing more relevant signals over time.

Enhanced RSI Interpretation:

By providing optimized, asset-specific overbought and oversold levels, the indicator offers a more nuanced and potentially more accurate interpretation of RSI values.

The RSI Band Optimizer represents a significant advancement in the application of the Relative Strength Index. By dynamically calculating optimal band values, it addresses one of the main criticisms of traditional RSI usage – the reliance on static, one-size-fits-all overbought and oversold levels. This tool empowers traders to make more informed decisions based on RSI readings that are truly tailored to the specific characteristics of the asset they're trading.

Supertrend BandsSupertrend Bands

What is the Supertrend indicator?

"The Supertrend indicator is a trend following overlay on your trading chart, much like a moving average, that shows you the current trend direction.

The indicator works well in a trending market but can give false signals when a market is trading in a range.

It uses the ATR (average true range) as part of its calculation which takes into account the volatility of the market. The ATR is adjusted using the multiplier setting which determines how sensitive the indicator is."

"For the basic Supertrend settings, you can adjust period and factor:

- The period setting is the lookback for the ATR calculation

- Factor is the what the ATR is multiplied by to offset the bands from price"

How to use this indicator

This indicator is inspired by a strategy I found. It includes four Supertrend indicators, each with different settings that displays trend strength and support/resistance zones. The default settings are optimal for cryptocurrency but do work quite well for traditional also. I highly recommend you try experimenting with different settings, increasing them to suit the instrument.

The bands are set from low to high, Band 1 being the fastest and Band 4 being the slowest. Band 4 is the one that sets the overall trend so when price is above Band 4, the trend is bullish and vice versa. Trend is strongest when price is above/below Band 1 and gets weaker as it filters through each band. Band 4 provides the strongest support/resistance and if that breaks the trend flips.

In the menu, you will see an option called "Remove Anti Trend?". It is enabled by default and it removes any bearish/resistance bands when the trend is up and any bullish/support bands when the trend is down. When turned off, it will show all Supertrend Bands as they are by default.

Bar Colors

Bar colors are optional and they reflect the current trend strength based on the Supertrend bands.

Alternate ways of using this indicator

You could leave everything as default or you can display individual bands. For instance, because I use many overlay indicators, most of the time I turn off all the bands and only show bar colors:

You can also turn off Bands 1 and 2 and only show the two slowest lengths:

This removes the noise of the two faster Supertrends.

Or just show the two fastest bands:

Any suggestions to improve this indicator are most welcome :)

MorphWave Bands [JOAT]MorphWave Bands - Adaptive Volatility Envelope System

MorphWave Bands create a dynamic price envelope that automatically adjusts its width based on current market conditions. Unlike static Bollinger Bands, this indicator blends ATR and standard deviation with an efficiency ratio to expand during trending conditions and contract during consolidation.

What This Indicator Does

Plots adaptive upper and lower bands around a customizable moving average basis

Automatically adjusts band width using a blend of ATR and standard deviation

Detects volatility squeezes when bands contract to historical lows

Highlights breakouts when price moves beyond the bands

Provides squeeze alerts for anticipating volatility expansion

Adaptive Mechanism

The bands adapt through a multi-step process:

// Blend ATR and Standard Deviation

blendedVol = useAtrBlend ? (atrVal * 0.6 + stdVal * 0.4) : stdVal

// Normalize volatility to its historical range

volNorm = (blendedVol - volLow) / (volHigh - volLow)

// Create adaptive multiplier

adaptMult = baseMult * (0.5 + volNorm * adaptSens)

This creates bands that respond to market regime changes while maintaining stability.

Squeeze Detection

A squeeze is identified when band width drops below a specified percentile of its historical range:

Background highlighting indicates active squeeze conditions

Low percentile readings suggest compressed volatility

Squeeze exits often precede directional moves

Inputs Overview

Band Length — Period for basis calculation (default: 20)

Base Multiplier — Starting band width multiplier (default: 2.0)

MA Type — Choose from SMA, EMA, WMA, VWMA, or HMA

Adaptation Lookback — Historical period for normalization (default: 50)

Adaptation Sensitivity — How much bands respond to volatility changes

Squeeze Threshold — Percentile below which squeeze is detected

Dashboard Information

Current trend direction relative to basis and bands

Band width percentage

Squeeze status (Active or None)

Efficiency ratio

Current adaptive multiplier value

How to Use It

Look for squeeze conditions as potential precursors to breakouts

Use band touches as dynamic support/resistance references

Monitor breakout signals when price closes beyond bands

Combine with momentum indicators for directional confirmation

Alerts

Upper/Lower Breakout — Price exceeds band boundaries

Squeeze Entry/Exit — Volatility compression begins or ends

Basis Crosses — Price crosses the center line

This indicator is provided for educational purposes. It does not constitute financial advice.

— Made with passion by officialjackofalltrades

VFAP Bands: Volume Flow Aggregate Price [NeoButane]What VFAP accomplishes is finishing what VWAP started, which is to find the best liquidity for market makers to profit off the bid/ask spread. What price is the best? Of course, nobody would tell you this. Otherwise it would be easy for bigger market participants to hunt or prevent being hunted.

This is where VFAP comes in: by being able to visualize optimal liquidity zones, you will be able to enter/exit positions at the safest entries, front run the market makers, and get stopped out at the coolest prices.

The bands are consistently wicked into and provide insight to minute timeframe movements. The levels are areas of high volume where traders may be trapped or defending their position.

See here for pricing and more information: medium.com

Pictured below are the true basis bands. In a tightening/nonvolatile range, They are able to pre-define the range by having a modified formula and being sooner to update than the traditional VFAP bands.

Trial version here:

OBV Trend Bands [Alpha Extract]OBV Trend Bands 📊

The OBV Trend Bands indicator leverages On-Balance Volume (OBV) to assess trend strength and potential reversals by plotting a dynamic median line alongside upper and lower bands based on standard deviation. This tool helps traders identify overbought or oversold conditions and visualize OBV momentum relative to historical trends.

🔶 CALCULATION

The indicator calculates OBV, a dynamic median of OBV, and standard deviation bands to measure volume-driven momentum:

• OBV: Cumulative volume that adds or subtracts based on price direction.

• Aggregate Median: A smoothed median of OBV over a user-defined lookback period, adjusted by a minimum lookback for robustness.

• Standard Deviation Bands: Upper and lower bands derived from the scaled aggregate median, adjusted by a multiplier.

• Scaled OBV: OBV divided by a customizable scaling factor for better visualization.

Formula:

• OBV = Cumulative sum of volume (positive if price increases, negative if price decreases)

• Aggregate Median = Average of simple medians over a range from minLookbackPeriod to length

• Upper Band = Aggregate Median / Scaling Factor + StdMultiplier * StdDev

• Lower Band = Aggregate Median / Scaling Factor - StdMultiplier * StdDev

🔶 DETAILS

Visual Features:

• OBV Line (Dynamic Color): Plotted with a color that shifts based on its position—green above the upper band (bullish), red below the lower band (bearish), and white between bands (neutral).

• Upper Band (Green): Represents the overbought threshold, lightly shaded for clarity.

• Lower Band (Red): Indicates the oversold threshold, also lightly shaded.

• Aggregate Median Line (Gray): Acts as the central trend reference.

• Fill Areas: Transparent green fill when OBV exceeds the upper band, transparent red fill when below the lower band, and no fill within the bands.

Interpretation:

• Bullish Signal: OBV rises above the upper band, suggesting strong buying pressure and potential trend continuation.

• Bearish Signal: OBV falls below the lower band, indicating selling pressure and possible trend weakness.

• Neutral Zone: OBV between bands reflects consolidation or indecision in the market.

🔶 EXAMPLES

The chart demonstrates:

• Bullish Momentum: OBV crosses above the upper band with a green line and fill, signaling robust accumulation.

• Bearish Momentum: OBV drops below the lower band with a red line and fill, indicating distribution or selling pressure.

• Reversal Points: Transitions of OBV from below the lower band to above the upper band (or vice versa) suggest potential trend shifts.

Example Snapshots:

• A sustained bullish phase where OBV remains above the upper band with consistent green coloring.

• A bearish trend change where OBV falls below the upper band hinting at weakening momentum leading to a change in trend.

🔶 SETTINGS

Customization Options:

• Median Length (Default: 100): Adjusts the period for calculating the aggregate median, tailoring trend sensitivity.

• Minimum Lookback Period (Default: 30): Sets the shortest period for median aggregation, refining responsiveness.

• Standard Deviation Multiplier (Default: 1.0): Controls the width of the bands—higher values widen them, lower values tighten them.

• Scaling Factor (Default: 100,000): Scales OBV for better chart readability, adjustable based on asset volume.

The OBV Trend Bands indicator is a versatile tool for traders, blending volume analysis with statistical boundaries to effectively pinpoint market extremes and momentum shifts.

AG Ultimate Bollinger BandsWe believe we have really built the ultimate Bollinger Bands! There are so many options with these Bands:

- use an SMA or EMA for the Basis Moving Average

- displaying the Average Highs/Lows (blue lines) to create a Moving Band

- show breakouts of the Upper/Lower Bollinger Bands with arrows for simplicity (no more wondering whether it closed out or not!)

- show a standard deviation of Highs/Lows alongside the traditional Upper/Lower Bollinger Bands.

All options are togglable, for full flexibility and customisation.