LibTmFrLibrary "LibTmFr"

This is a utility library for handling timeframes and

multi-timeframe (MTF) analysis in Pine Script. It provides a

collection of functions designed to handle common tasks related

to period detection, session alignment, timeframe construction,

and time calculations, forming a foundation for

MTF indicators.

Key Capabilities:

1. **MTF Period Engine:** The library includes functions for

managing higher-timeframe (HTF) periods.

- **Period Detection (`isNewPeriod`):** Detects the first bar

of a given timeframe. It includes custom logic to handle

multi-month and multi-year intervals where

`timeframe.change()` may not be sufficient.

- **Bar Counting (`sinceNewPeriod`):** Counts the number of

bars that have passed in the current HTF period or

returns the final count for a completed historical period.

2. **Automatic Timeframe Selection:** Offers functions for building

a top-down analysis framework:

- **Automatic HTF (`autoHTF`):** Suggests a higher timeframe

(HTF) for broader context based on the current timeframe.

- **Automatic LTF (`autoLTF`):** Suggests an appropriate lower

timeframe (LTF) for granular intra-bar analysis.

3. **Timeframe Manipulation and Comparison:** Includes tools for

working with timeframe strings:

- **Build & Split (`buildTF`, `splitTF`):** Functions to

programmatically construct valid Pine Script timeframe

strings (e.g., "4H") and parse them back into their

numeric and unit components.

- **Comparison (`isHigherTF`, `isActiveTF`, `isLowerTF`):**

A set of functions to check if a given timeframe is

higher, lower, or the same as the script's active timeframe.

- **Multiple Validation (`isMultipleTF`):** Checks if a

higher timeframe is a practical multiple of the current

timeframe. This is based on the assumption that checking

if recent, completed HTF periods contained more than one

bar is a valid proxy for preventing data gaps.

4. **Timestamp Interpolation:** Contains an `interpTimestamp()`

function that calculates an absolute timestamp by

interpolating at a given percentage across a specified

range of bars (e.g., 50% of the way through the last

20 bars), enabling time calculations at a resolution

finer than the chart's native bars.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

buildTF(quantity, unit)

Builds a Pine Script timeframe string from a numeric quantity and a unit enum.

The resulting string can be used with `request.security()` or `input.timeframe`.

Parameters:

quantity (int) : series int Number to specifie how many `unit` the timeframe spans.

unit (series TFUnit) : series TFUnit The size category for the bars.

Returns: series string A Pine-style timeframe identifier, e.g.

"5S" → 5-seconds bars

"30" → 30-minute bars

"120" → 2-hour bars

"1D" → daily bars

"3M" → 3-month bars

"24M" → 2-year bars

splitTF(tf)

Splits a Pine‑timeframe identifier into numeric quantity and unit (TFUnit).

Parameters:

tf (string) : series string Timeframe string, e.g.

"5S", "30", "120", "1D", "3M", "24M".

Returns:

quantity series int The numeric value of the timeframe (e.g., 15 for "15", 3 for "3M").

unit series TFUnit The unit of the timeframe (e.g., TFUnit.minutes, TFUnit.months).

Notes on strings without a suffix:

• Pure digits are minutes; if divisible by 60, they are treated as hours.

• An "M" suffix is months; if divisible by 12, it is converted to years.

autoHTF(tf)

Picks an appropriate **higher timeframe (HTF)** relative to the selected timeframe.

It steps up along a coarse ladder to produce sensible jumps for top‑down analysis.

Mapping → chosen HTF:

≤ 1 min → 60 (1h) ≈ ×60

≤ 3 min → 180 (3h) ≈ ×60

≤ 5 min → 240 (4h) ≈ ×48

≤ 15 min → D (1 day) ≈ ×26–×32 (regular session 6.5–8 h)

> 15 min → W (1 week) ≈ ×64–×80 for 30m; varies with input

≤ 1 h → W (1 week) ≈ ×32–×40

≤ 4 h → M (1 month) ≈ ×36–×44 (~22 trading days / month)

> 4 h → 3M (3 months) ≈ ×36–×66 (e.g., 12h→×36–×44; 8h→×53–×66)

≤ 1 day → 3M (3 months) ≈ ×60–×66 (~20–22 trading days / month)

> 1 day → 12M (1 year) ≈ ×(252–264)/quantity

≤ 1 week → 12M (1 year) ≈ ×52

> 1 week → 48M (4 years) ≈ ×(208)/quantity

= 1 M → 48M (4 years) ≈ ×48

> 1 M → error ("HTF too big")

any → error ("HTF too big")

Notes:

• Inputs in months or years are restricted: only 1M is allowed; larger months/any years throw.

• Returns a Pine timeframe string usable in `request.security()` and `input.timeframe`.

Parameters:

tf (string) : series string Selected timeframe (e.g., "D", "240", or `timeframe.period`).

Returns: series string Suggested higher timeframe.

autoLTF(tf)

Selects an appropriate **lower timeframe LTF)** for intra‑bar evaluation

based on the selected timeframe. The goal is to keep intra‑bar

loops performant while providing enough granularity.

Mapping → chosen LTF:

≤ 1 min → 1S ≈ ×60

≤ 5 min → 5S ≈ ×60

≤ 15 min → 15S ≈ ×60

≤ 30 min → 30S ≈ ×60

> 30 min → 60S (1m) ≈ ×31–×59 (for 31–59 minute charts)

≤ 1 h → 1 (1m) ≈ ×60

≤ 2 h → 2 (2m) ≈ ×60

≤ 4 h → 5 (5m) ≈ ×48

> 4 h → 15 (15m) ≈ ×24–×48 (e.g., 6h→×24, 8h→×32, 12h→×48)

≤ 1 day → 15 (15m) ≈ ×26–×32 (regular sessions ~6.5–8h)

> 1 day → 60 (60m) ≈ ×(26–32) per day × quantity

≤ 1 week → 60 (60m) ≈ ×32–×40 (≈5 sessions of ~6.5–8h)

> 1 week → 240 (4h) ≈ ×(8–10) per week × quantity

≤ 1 M → 240 (4h) ≈ ×33–×44 (~20–22 sessions × 6.5–8h / 4h)

≤ 3 M → D (1d) ≈ ×(20–22) per month × quantity

> 3 M → W (1w) ≈ ×(4–5) per month × quantity

≤ 1 Y → W (1w) ≈ ×52

> 1 Y → M (1M) ≈ ×12 per year × quantity

Notes:

• Ratios for D/W/M are given as ranges because they depend on

**regular session length** (typically ~6.5–8h, not 24h).

• Returned strings can be used with `request.security()` and `input.timeframe`.

Parameters:

tf (string) : series string Selected timeframe (e.g., "D", "240", or timeframe.period).

Returns: series string Suggested lower TF to use for intra‑bar work.

isNewPeriod(tf, offset)

Returns `true` when a new session-aligned period begins, or on the Nth bar of that period.

Parameters:

tf (string) : series string Target higher timeframe (e.g., "D", "W", "M").

offset (simple int) : simple int 0 → checks for the first bar of the new period.

1+ → checks for the N-th bar of the period.

Returns: series bool `true` if the condition is met.

sinceNewPeriod(tf, offset)

Counts how many bars have passed within a higher timeframe (HTF) period.

For daily, weekly, and monthly resolutions, the period is aligned with the trading session.

Parameters:

tf (string) : series string Target parent timeframe (e.g., "60", "D").

offset (simple int) : simple int 0 → Running count for the current period.

1+ → Finalized count for the Nth most recent *completed* period.

Returns: series int Number of bars.

isHigherTF(tf, main)

Returns `true` when the selected timeframe represents a

higher resolution than the active timeframe.

Parameters:

tf (string) : series string Selected timeframe.

main (bool) : series bool When `true`, the comparison is made against the chart's main timeframe

instead of the script's active timeframe. Optional. Defaults to `false`.

Returns: series bool `true` if `tf` > active TF; otherwise `false`.

isActiveTF(tf, main)

Returns `true` when the selected timeframe represents the

exact resolution of the active timeframe.

Parameters:

tf (string) : series string Selected timeframe.

main (bool) : series bool When `true`, the comparison is made against the chart's main timeframe

instead of the script's active timeframe. Optional. Defaults to `false`.

Returns: series bool `true` if `tf` == active TF; otherwise `false`.

isLowerTF(tf, main)

Returns `true` when the selected timeframe represents a

lower resolution than the active timeframe.

Parameters:

tf (string) : series string Selected timeframe.

main (bool) : series bool When `true`, the comparison is made against the chart's main timeframe

instead of the script's active timeframe. Optional. Defaults to `false`.

Returns: series bool `true` if `tf` < active TF; otherwise `false`.

isMultipleTF(tf)

Returns `true` if the selected timeframe (`tf`) is a practical multiple

of the active skript's timeframe. It verifies this by checking if `tf` is a higher timeframe

that has consistently contained more than one bar of the skript's timeframe in recent periods.

The period detection is session-aware.

Parameters:

tf (string) : series string The higher timeframe to check.

Returns: series bool `true` if `tf` is a practical multiple; otherwise `false`.

interpTimestamp(offStart, offEnd, pct)

Calculates a precise absolute timestamp by interpolating within a bar range based on a percentage.

This version works with RELATIVE bar offsets from the current bar.

Parameters:

offStart (int) : series int The relative offset of the starting bar (e.g., 10 for 10 bars ago).

offEnd (int) : series int The relative offset of the ending bar (e.g., 1 for 1 bar ago). Must be <= offStart.

pct (float) : series float The percentage of the bar range to measure (e.g., 50.5 for 50.5%).

Values are clamped to the range.

Returns: series int The calculated, interpolated absolute Unix timestamp in milliseconds.

Recherche dans les scripts pour "bar"

Anchored VWAP Polyline [CHE] Anchored VWAP Polyline — Anchored VWAP drawn as a polyline from a user-defined bar count with last-bar updates and optional labels

Summary

This indicator renders an anchored Volume-Weighted Average Price as a continuous polyline starting from a user-selected anchor point a specified number of bars back. It accumulates price multiplied by volume only from the anchor forward and resets cleanly when the anchor moves. Drawing is object-based (polyline and labels) and updated on the most recent bar only, which reduces flicker and avoids excessive redraws. Optional labels mark the anchor and, conditionally, a delta label when the current close is below the historical close at the anchor offset.

Motivation: Why this design?

Anchored VWAP is often used to track fair value after a specific event such as a swing, breakout, or session start. Traditional plot-based lines can repaint during live updates or incur overhead when frequently redrawn. This implementation focuses on explicit state management, last-bar rendering, and object recycling so the line stays stable while remaining responsive when the anchor changes. The design emphasizes deterministic updates and simple session gating from the anchor.

What’s different vs. standard approaches?

Baseline: Classic VWAP lines plotted from session open or full history.

Architecture differences:

Anchor defined by a fixed bar offset rather than session or day boundaries.

Object-centric drawing via `polyline` with an array of `chart.point` objects.

Last-bar update pattern with deletion and replacement of the polyline to apply all points cleanly.

Conditional labels: an anchor marker and an optional delta label only when the current close is below the historical close at the offset.

Practical effect: You get a visually continuous anchored VWAP that resets when the anchor shifts and remains clean on chart refreshes. The labels act as lightweight diagnostics without clutter.

How it works (technical)

The anchor index is computed as the latest bar index minus the user-defined bar count.

A session flag turns true from the anchor forward; prior bars are excluded.

Two persistent accumulators track the running sum of price multiplied by volume and the running sum of volume; they reset when the session flag turns from false to true.

The anchored VWAP is the running sum divided by the running volume whenever both are valid and the volume is not zero.

Points are appended to an array only when the anchored VWAP is valid. On the most recent bar, any existing polyline is deleted and replaced with a new one built from the point array.

Labels are refreshed on the most recent bar:

A yellow warning label appears when there are not enough bars to compute the reference values.

The anchor label marks the anchor bar.

The delta label appears only when the current close is below the close at the anchor offset; otherwise it is suppressed.

No higher-timeframe requests are used; repaint is limited to normal live-bar behavior.

Parameter Guide

Bars back — Sets the anchor offset in bars; default two hundred thirty-three; minimum one. Larger values extend the anchored period and increase stability but respond more slowly to regime changes.

Labels — Toggles all labels; default enabled. Disable to keep the chart clean when using multiple instances.

Reading & Interpretation

The polyline represents the anchored VWAP from the chosen anchor to the current bar. Price above the line suggests strength relative to the anchored baseline; price below suggests weakness.

The anchor label shows where the accumulation starts.

The delta label appears only when today’s close is below the historical close at the offset; it provides a quick context for negative drift relative to that reference.

A yellow message at the current bar indicates the chart does not have enough history to compute the reference comparison yet.

Practical Workflows & Combinations

Trend following: Anchor after a breakout bar or a swing confirmation. Use the anchored VWAP as dynamic support or resistance; look for clean retests and holds for continuation.

Mean reversion: Anchor at a local extreme and watch for approaches back toward the line; require structure confirmation to avoid early entries.

Session or event studies: Re-set the anchor around earnings, macro releases, or session opens by adjusting the bar offset.

Combinations: Pair with structure tools such as swing highs and lows, or with volatility measures to filter chop. The labels can be disabled when combining multiple instances to maintain chart clarity.

Behavior, Constraints & Performance

Repaint and confirmation: The line is updated on the most recent bar only; historical values do not rely on future bars. Normal live-bar movement applies until the bar closes.

No higher timeframe: There is no `security` call; repaint paths related to higher-timeframe lookahead do not apply here.

Resources: Uses one polyline object that is rebuilt on the most recent bar, plus two labels when conditions are met. `max_bars_back` is two thousand. Arrays store points from the anchor forward; extremely long anchors or very long charts increase memory usage.

Known limits: With very thin volume, the VWAP can be unavailable for some bars. Very large anchors reduce responsiveness. Labels use ATR for vertical placement; extreme gaps can place them close to extremes.

Sensible Defaults & Quick Tuning

Starting point: Bars back two hundred thirty-three with Labels enabled works well on many assets and timeframes.

Too noisy around the line: Increase Bars back to extend the accumulation window.

Too sluggish after regime changes: Decrease Bars back to focus on a shorter anchored period.

Chart clutter with multiple instances: Disable Labels while keeping the polyline visible.

What this indicator is—and isn’t

This is a visualization of an anchored VWAP with optional diagnostics. It is not a full trading system and does not include entries, exits, or position management. Use it alongside clear market structure, risk controls, and a plan for trade management. It does not predict future prices.

Inputs with defaults

Bars back: two hundred thirty-three bars, minimum one.

Labels: enabled or disabled toggle, default enabled.

Pine version: v6

Overlay: true

Primary outputs: one polyline, optional labels (anchor, conditional delta, and a warning when insufficient bars).

Metrics and functions: volume, ATR for label offset, object drawing via polyline and chart points, last-bar update pattern.

Special techniques: session gating from the anchor, persistent state, object recycling, explicit guards against unavailable values and zero volume.

Compatibility and assets: Designed for standard candlestick or bar charts across liquid assets and common timeframes.

Diagnostics: Yellow warning label when history is insufficient.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

MERV: Market Entropy & Rhythm Visualizer [BullByte]The MERV (Market Entropy & Rhythm Visualizer) indicator analyzes market conditions by measuring entropy (randomness vs. trend), tradeability (volatility/momentum), and cyclical rhythm. It provides traders with an easy-to-read dashboard and oscillator to understand when markets are structured or choppy, and when trading conditions are optimal.

Purpose of the Indicator

MERV’s goal is to help traders identify different market regimes. It quantifies how structured or random recent price action is (entropy), how strong and volatile the movement is (tradeability), and whether a repeating cycle exists. By visualizing these together, MERV highlights trending vs. choppy environments and flags when conditions are favorable for entering trades. For example, a low entropy value means prices are following a clear trend line, whereas high entropy indicates a lot of noise or sideways action. The indicator’s combination of measures is original: it fuses statistical trend-fit (entropy), volatility trends (ATR and slope), and cycle analysis to give a comprehensive view of market behavior.

Why a Trader Should Use It

Traders often need to know when a market trend is reliable vs. when it is just noise. MERV helps in several ways: it shows when the market has a strong direction (low entropy, high tradeability) and when it’s ranging (high entropy). This can prevent entering trend-following strategies during choppy periods, or help catch breakouts early. The “Optimal Regime” marker (a star) highlights moments when entropy is very low and tradeability is very high, typically the best conditions for trend trades. By using MERV, a trader gains an empirical “go/no-go” signal based on price history, rather than guessing from price alone. It’s also adaptable: you can apply it to stocks, forex, crypto, etc., on any timeframe. For example, during a bullish phase of a stock, MERV will turn green (Trending Mode) and often show a star, signaling good follow-through. If the market later grinds sideways, MERV will shift to magenta (Choppy Mode), warning you that trend-following is now risky.

Why These Components Were Chosen

Market Entropy (via R²) : This measures how well recent prices fit a straight line. We compute a linear regression on the last len_entropy bars and calculate R². Entropy = 1 - R², so entropy is low when prices follow a trend (R² near 1) and high when price action is erratic (R² near 0). This single number captures trend strength vs noise.

Tradeability (ATR + Slope) : We combine two familiar measures: the Average True Range (ATR) (normalized by price) and the absolute slope of the regression line (scaled by ATR). Together they reflect how active and directional the market is. A high ATR or strong slope means big moves, making a trend more “tradeable.” We take a simple average of the normalized ATR and slope to get tradeability_raw. Then we convert it to a percentile rank over the lookback window so it’s stable between 0 and 1.

Percentile Ranks : To make entropy and tradeability values easy to interpret, we convert each to a 0–100 rank based on the past len_entropy periods. This turns raw metrics into a consistent scale. (For example, an entropy rank of 90 means current entropy is higher than 90% of recent values.) We then divide by 100 to plot them on a 0–1 scale.

Market Mode (Regime) : Based on those ranks, MERV classifies the market:

Trending (Green) : Low entropy rank (<40%) and high tradeability rank (>60%). This means the market is structurally trending with high activity.

Choppy (Magenta) : High entropy rank (>60%) and low tradeability rank (<40%). This is a mostly random, low-momentum market.

Neutral (Cyan) : All other cases. This covers mixed regimes not strongly trending or choppy.

The mode is shown as a colored bar at the bottom: green for trending, magenta for choppy, cyan for neutral.

Optimal Regime Signal : Separately, we mark an “optimal” condition when entropy_norm < 0.3 and tradeability > 0.7 (both normalized 0–1). When this is true, a ★ star appears on the bottom line. This star is colored white when truly optimal, gold when only tradeability is high (but entropy not quite low enough), and black when neither condition holds. This gives a quick visual cue for very favorable conditions.

What Makes MERV Stand Out

Holistic View : Unlike a single-oscillator, MERV combines trend, volatility, and cycle analysis in one tool. This multi-faceted approach is unique.

Visual Dashboard : The fixed on-chart dashboard (shown at your chosen corner) summarizes all metrics in bar/gauge form. Even a non-technical user can glance at it: more “█” blocks = a higher value, colors match the plots. This is more intuitive than raw numbers.

Adaptive Thresholds : Using percentile ranks means MERV auto-adjusts to each market’s character, rather than requiring fixed thresholds.

Cycle Insight : The rhythm plot adds information rarely found in indicators – it shows if there’s a repeating cycle (and its period in bars) and how strong it is. This can hint at natural bounce or reversal intervals.

Modern Look : The neon color scheme and glow effects make the lines easy to distinguish (blue/pink for entropy, green/orange for tradeability, etc.) and the filled area between them highlights when one dominates the other.

Recommended Timeframes

MERV can be applied to any timeframe, but it will be more reliable on higher timeframes. The default len_entropy = 50 and len_rhythm = 30 mean we use 30–50 bars of history, so on a daily chart that’s ~2–3 months of data; on a 1-hour chart it’s about 2–3 days. In practice:

Swing/Position traders might prefer Daily or 4H charts, where the calculations smooth out small noise. Entropy and cycles are more meaningful on longer trends.

Day trader s could use 15m or 1H charts if they adjust the inputs (e.g. shorter windows). This provides more sensitivity to intraday cycles.

Scalpers might find MERV too “slow” unless input lengths are set very low.

In summary, the indicator works anywhere, but the defaults are tuned for capturing medium-term trends. Users can adjust len_entropy and len_rhythm to match their chart’s volatility. The dashboard position can also be moved (top-left, bottom-right, etc.) so it doesn’t cover important chart areas.

How the Scoring/Logic Works (Step-by-Step)

Compute Entropy : A linear regression line is fit to the last len_entropy closes. We compute R² (goodness of fit). Entropy = 1 – R². So a strong straight-line trend gives low entropy; a flat/noisy set of points gives high entropy.

Compute Tradeability : We get ATR over len_entropy bars, normalize it by price (so it’s a fraction of price). We also calculate the regression slope (difference between the predicted close and last close). We scale |slope| by ATR to get a dimensionless measure. We average these (ATR% and slope%) to get tradeability_raw. This represents how big and directional price moves are.

Convert to Percentiles : Each new entropy and tradeability value is inserted into a rolling array of the last 50 values. We then compute the percentile rank of the current value in that array (0–100%) using a simple loop. This tells us where the current bar stands relative to history. We then divide by 100 to plot on .

Determine Modes and Signal : Based on these normalized metrics: if entropy < 0.4 and tradeability > 0.6 (40% and 60% thresholds), we set mode = Trending (1). If entropy > 0.6 and tradeability < 0.4, mode = Choppy (-1). Otherwise mode = Neutral (0). Separately, if entropy_norm < 0.3 and tradeability > 0.7, we set an optimal flag. These conditions trigger the colored mode bars and the star line.

Rhythm Detection : Every bar, if we have enough data, we take the last len_rhythm closes and compute the mean and standard deviation. Then for lags from 5 up to len_rhythm, we calculate a normalized autocorrelation coefficient. We track the lag that gives the maximum correlation (best match). This “best lag” divided by len_rhythm is plotted (a value between 0 and 1). Its color changes with the correlation strength. We also smooth the best correlation value over 5 bars to plot as “Cycle Strength” (also 0 to 1). This shows if there is a consistent cycle length in recent price action.

Heatmap (Optional) : The background color behind the oscillator panel can change with entropy. If “Neon Rainbow” style is on, low entropy is blue and high entropy is pink (via a custom color function), otherwise a classic green-to-red gradient can be used. This visually reinforces the entropy value.

Volume Regime (Dashboard Only) : We compute vol_norm = volume / sma(volume, len_entropy). If this is above 1.5, it’s considered high volume (neon orange); below 0.7 is low (blue); otherwise normal (green). The dashboard shows this as a bar gauge and percentage. This is for context only.

Oscillator Plot – How to Read It

The main panel (oscillator) has multiple colored lines on a 0–1 vertical scale, with horizontal markers at 0.2 (Low), 0.5 (Mid), and 0.8 (High). Here’s each element:

Entropy Line (Blue→Pink) : This line (and its glow) shows normalized entropy (0 = very low, 1 = very high). It is blue/green when entropy is low (strong trend) and pink/purple when entropy is high (choppy). A value near 0.0 (below 0.2 line) indicates a very well-defined trend. A value near 1.0 (above 0.8 line) means the market is very random. Watch for it dipping near 0: that suggests a strong trend has formed.

Tradeability Line (Green→Yellow) : This represents normalized tradeability. It is colored bright green when tradeability is low, transitioning to yellow as tradeability increases. Higher values (approaching 1) mean big moves and strong slopes. Typically in a market rally or crash, this line will rise. A crossing above ~0.7 often coincides with good trend strength.

Filled Area (Orange Shade) : The orange-ish fill between the entropy and tradeability lines highlights when one dominates the other. If the area is large, the two metrics diverge; if small, they are similar. This is mostly aesthetic but can catch the eye when the lines cross over or remain close.

Rhythm (Cycle) Line : This is plotted as (best_lag / len_rhythm). It indicates the relative period of the strongest cycle. For example, a value of 0.5 means the strongest cycle was about half the window length. The line’s color (green, orange, or pink) reflects how strong that cycle is (green = strong). If no clear cycle is found, this line may be flat or near zero.

Cycle Strength Line : Plotted on the same scale, this shows the autocorrelation strength (0–1). A high value (e.g. above 0.7, shown in green) means the cycle is very pronounced. Low values (pink) mean any cycle is weak and unreliable.

Mode Bars (Bottom) : Below the main oscillator, thick colored bars appear: a green bar means Trending Mode, magenta means Choppy Mode, and cyan means Neutral. These bars all have a fixed height (–0.1) and make it very easy to see the current regime.

Optimal Regime Line (Bottom) : Just below the mode bars is a thick horizontal line at –0.18. Its color indicates regime quality: White (★) means “Optimal Regime” (very low entropy and high tradeability). Gold (★) means not quite optimal (high tradeability but entropy not low enough). Black means neither condition. This star line quickly tells you when conditions are ideal (white star) or simply good (gold star).

Horizontal Guides : The dotted lines at 0.2 (Low), 0.5 (Mid), and 0.8 (High) serve as reference lines. For example, an entropy or tradeability reading above 0.8 is “High,” and below 0.2 is “Low,” as labeled on the chart. These help you gauge values at a glance.

Dashboard (Fixed Corner Panel)

MERV also includes a compact table (dashboard) that can be positioned in any corner. It summarizes key values each bar. Here is how to read its rows:

Entropy : Shows a bar of blocks (█ and ░). More █ blocks = higher entropy. It also gives a percentage (rounded). A full bar (10 blocks) with a high % means very chaotic market. The text is colored similarly (blue-green for low, pink for high).

Rhythm : Shows the best cycle period in bars (e.g. “15 bars”). If no calculation yet, it shows “n/a.” The text color matches the rhythm line.

Cycle Strength : Gives the cycle correlation as a percentage (smoothed, as shown on chart). Higher % (green) means a strong cycle.

Tradeability : Displays a 10-block gauge for tradeability. More blocks = more tradeable market. It also shows “gauge” text colored green→yellow accordingly.

Market Mode : Simply shows “Trending”, “Choppy”, or “Neutral” (cyan text) to match the mode bar color.

Volume Regime : Similar to tradeability, shows blocks for current volume vs. average. Above-average volume gives orange blocks, below-average gives blue blocks. A % value indicates current volume relative to average. This row helps see if volume is abnormally high or low.

Optimal Status (Large Row) : In bold, either “★ Optimal Regime” (white text) if the star condition is met, “★ High Tradeability” (gold text) if tradeability alone is high, or “— Not Optimal” (gray text) otherwise. This large row catches your eye when conditions are ripe.

In short, the dashboard turns the numeric state into an easy read: filled bars, colors, and text let you see current conditions without reading the plot. For instance, five blue blocks under Entropy and “25%” tells you entropy is low (good), and a row showing “Trending” in green confirms a trend state.

Real-Life Example

Example : Consider a daily chart of a trending stock (e.g. “AAPL, 1D”). During a strong uptrend, recent prices fit a clear upward line, so Entropy would be low (blue line near bottom, perhaps below the 0.2 line). Volatility and slope are high, so Tradeability is high (green-yellow line near top). In the dashboard, Entropy might show only 1–2 blocks (e.g. 10%) and Tradeability nearly full (e.g. 90%). The Market Mode bar turns green (Trending), and you might see a white ★ on the optimal line if conditions are very good. The Volume row might light orange if volume is above average during the rally. In contrast, imagine the same stock later in a tight range: Entropy will rise (pink line up, more blocks in dashboard), Tradeability falls (fewer blocks), and the Mode bar turns magenta (Choppy). No star appears in that case.

Consolidated Use Case : Suppose on XYZ stock the dashboard reads “Entropy: █░░░░░░░░ 20%”, “Tradeability: ██████████ 80%”, Mode = Trending (green), and “★ Optimal Regime.” This tells the trader that the market is in a strong, low-noise trend, and it might be a good time to follow the trend (with appropriate risk controls). If instead it reads “Entropy: ████████░░ 80%”, “Tradeability: ███▒▒▒▒▒▒ 30%”, Mode = Choppy (magenta), the trader knows the market is random and low-momentum—likely best to sit out until conditions improve.

Example: How It Looks in Action

Screenshot 1: Trending Market with High Tradeability (SOLUSD, 30m)

What it means:

The market is in a clear, strong trend with excellent conditions for trading. Both trend-following and active strategies are favored, supported by high tradeability and strong volume.

Screenshot 2: Optimal Regime, Strong Trend (ETHUSD, 1h)

What it means:

This is an ideal environment for trend trading. The market is highly organized, tradeability is excellent, and volume supports the move. This is when the indicator signals the highest probability for success.

Screenshot 3: Choppy Market with High Volume (BTC Perpetual, 5m)

What it means:

The market is highly random and choppy, despite a surge in volume. This is a high-risk, low-reward environment, avoid trend strategies, and be cautious even with mean-reversion or scalping.

Settings and Inputs

The script is fully open-source; here are key inputs the user can adjust:

Entropy Window (len_entropy) : Number of bars used for entropy and tradeability (default 50). Larger = smoother, more lag; smaller = more sensitivity.

Rhythm Window (len_rhythm ): Bars used for cycle detection (default 30). This limits the longest cycle we detect.

Dashboard Position : Choose any corner (Top Right default) so it doesn’t cover chart action.

Show Heatmap : Toggles the entropy background coloring on/off.

Heatmap Style : “Neon Rainbow” (colorful) or “Classic” (green→red).

Show Mode Bar : Turn the bottom mode bar on/off.

Show Dashboard : Turn the fixed table panel on/off.

Each setting has a tooltip explaining its effect. In the description we will mention typical settings (e.g. default window sizes) and that the user can move the dashboard corner as desired.

Oscillator Interpretation (Recap)

Lines : Blue/Pink = Entropy (low=trend, high=chop); Green/Yellow = Tradeability (low=quiet, high=volatile).

Fill : Orange tinted area between them (for visual emphasis).

Bars : Green=Trending, Magenta=Choppy, Cyan=Neutral (at bottom).

Star Line : White star = ideal conditions, Gold = good but not ideal.

Horizontal Guides : 0.2 and 0.8 lines mark low/high thresholds for each metric.

Using the chart, a coder or trader can see exactly what each output represents and make decisions accordingly.

Disclaimer

This indicator is provided as-is for educational and analytical purposes only. It does not guarantee any particular trading outcome. Past market patterns may not repeat in the future. Users should apply their own judgment and risk management; do not rely solely on this tool for trading decisions. Remember, TradingView scripts are tools for market analysis, not personalized financial advice. We encourage users to test and combine MERV with other analysis and to trade responsibly.

-BullByte

FA_PA_LIBLibrary "FA_PA_LIB"

A collection of custom tools & utility functions commonly used for coding Dr Al Brooks, Price Action System with my scripts

getBodySize()

Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize()

Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getTopWickPercent()

Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: Percent of total candle width that is occupied by the upper wick

getBottomWickSize()

Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBottomWickPercent()

Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: Percent of total candle width that is occupied by the lower wick

getBarMidPoint()

Gets the current candle's midpoint wick to wick

Returns: The current candle's mid point

getBodyPercent()

Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage (00.00)

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

isBr()

Checks if the current bar is a Bear Bar

Returns: A boolean - true if the current bar is bear candle

isBl()

Checks if the current bar is a Bull Bar

Returns: A boolean - true if the current bar is Bull candle

isTrendBar()

Checks if the current bar is a Trend Bar. Candle that its body size is greater than 50% of entire candle size

Returns: A boolean - true if the current bar is Trend candle

isBlTrendBar()

Checks if the current bar is a Bull Trend Bar. Bullish candle that its body size is greater than 50% of entire candle size

Returns: A boolean - true if the current bar is Bull Trend candle

isBrTrendBar()

Checks if the current bar is a Bull Trend Bar. Bullish candle that its body size is greater than 50% of entire candle size

Returns: A boolean - true if the current bar is Bull Trend candle

isBlRevB()

Checks if the current bar is a Bull Reversal Bar. Bullish candle that closes on upper half of candle body

Returns: A boolean - true if the current bar is Bull Reversal candle

isBrRevB()

Checks if the current bar is a Bear Reversal Bar. BulBearish candle that closes on lower half of candle body

Returns: A boolean - true if the current bar is Bear Reversal candle

isDoji(wickSize, bodySize)

Checks if the current bar is a doji candle based on the given parameters

Parameters:

wickSize (float) : (default=2) The maximum top wick size compared to the bottom (and vice versa)

bodySize (float) : (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isHammer(fib, colorMatch)

Checks if the current bar is a hammer candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=true) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(fib, colorMatch)

Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isBlOB()

Detects Bullish outside bars(OB)

Returns: Returns true if the current bar is a bull outside bar

isBrOB()

Detects Bearish outside bars(OB)

Returns: Returns true if the current bar is a bear outside bar

NextBarColorNextBarColor

This is two-bars pattern search/matching indicator.

This indicator compares multiple values:

current bar high with previous bar open

current bar high with previous bar close

current bar high with previous bar high

current bar high with previous bar low

current bar low with previous bar open

current bar low with previous bar close

current bar low with previous bar high

current bar low with previous bar low

current bar close/current_price with previous bar high

current bar close/current_price with previous bar low

current bar close/current_price with previous bar open

current bar close/current_price with previous bar close

and searches for the same combination of 2 bars (current and previous) in the past.

Then shows as % value how many times the next bar went up or down.

Grey bar compares ups and downs with all results, including cases when price did not move.

My testing is showing better results when current and previous bars colors are also used in the search.

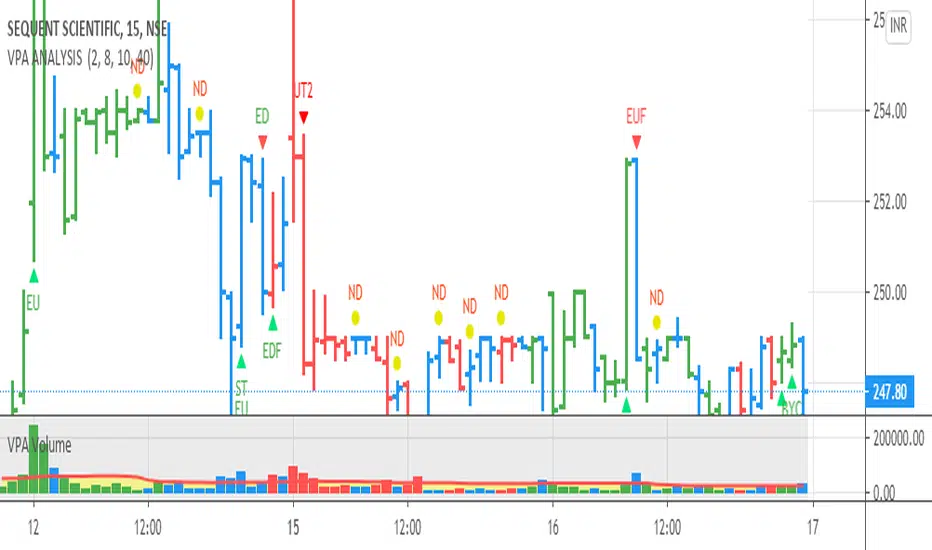

Volume Spread Analysis [TANHEF]Volume Spread Analysis: Understanding Market Intentions through the Interpretation of Volume and Price Movements.

█ Simple Explanation:

The Volume Spread Analysis (VSA) indicator is a comprehensive tool that helps traders identify key market patterns and trends based on volume and spread data. This indicator highlights significant VSA patterns and provides insights into market behavior through color-coded volume/spread bars and identification of bars indicating strength, weakness, and neutrality between buyers and sellers. It also includes powerful volume and spread forecasting capabilities.

█ Laws of Volume Spread Analysis (VSA):

The origin of VSA begins with Richard Wyckoff, a pivotal figure in its development. Wyckoff made significant contributions to trading theory, including the formulation of three basic laws:

The Law of Supply and Demand: This fundamental law states that supply and demand balance each other over time. High demand and low supply lead to rising prices until demand falls to a level where supply can meet it. Conversely, low demand and high supply cause prices to fall until demand increases enough to absorb the excess supply.

The Law of Cause and Effect: This law assumes that a 'cause' will result in an 'effect' proportional to the 'cause'. A strong 'cause' will lead to a strong trend (effect), while a weak 'cause' will lead to a weak trend.

The Law of Effort vs. Result: This law asserts that the result should reflect the effort exerted. In trading terms, a large volume should result in a significant price move (spread). If the spread is small, the volume should also be small. Any deviation from this pattern is considered an anomaly.

█ Volume and Spread Analysis Bars:

Display: Volume and/or spread bars that consist of color coded levels. If both of these are displayed, the number of spread bars can be limited for visual appeal and understanding, with the spread bars scaled to match the volume bars. While automatic calculation of the number of visual bars for auto scaling is possible, it is avoided to prevent the indicator from reloading whenever the number of visual price bars on the chart is adjusted, ensuring uninterrupted analysis. A displayable table (Legend) of bar colors and levels can give context and clarify to each volume/spread bar.

Calculation: Levels are calculated using multipliers applied to moving averages to represent key levels based on historical data: low, normal, high, ultra. This method smooths out short-term fluctuations and focuses on longer-term trends.

Low Level: Indicates reduced volatility and market interest.

Normal Level: Reflects typical market activity and volatility.

High Level: Indicates increased activity and volatility.

Ultra Level: Identifies extreme levels of activity and volatility.

This illustrates the appearance of Volume and Spread bars when scaled and plotted together:

█ Forecasting Capabilities:

Display: Forecasted volume and spread levels using predictive models.

Calculation: Volume and Spread prediction calculations differ as volume is linear and spread is non-linear.

Volume Forecast (Linear Forecasting): Predicts future volume based on current volume rate and bar time till close.

Spread Forecast (Non-Linear Dynamic Forecasting): Predicts future spread using a dynamic multiplier, less near midpoint (consolidation) and more near low or high (trending), reflecting non-linear expansion.

Moving Averages: In forecasting, moving averages utilize forecasted levels instead of actual levels to ensure the correct level is forecasted (low, normal, high, or ultra).

The following compares forecasted volume with actual resulting volume, highlighting the power of early identifying increased volume through forecasted levels:

█ VSA Patterns:

Criteria and descriptions for each VSA pattern are available as tooltips beside them within the indicator’s settings. These tooltips provide explanations of potential developments based on the volume and spread data.

Signs of Strength (🟢): Patterns indicating strong buying pressure and potential market upturns.

Down Thrust

Selling Climax

No Effort → Bearish Result

Bearish Effort → No Result

Inverse Down Thrust

Failed Selling Climax

Bull Outside Reversal

End of Falling Market (Bag Holder)

Pseudo Down Thrust

No Supply

Signs of Weakness (🔴): Patterns indicating strong selling pressure and potential market downturns.

Up Thrust

Buying Climax

No Effort → Bullish Result

Bullish Effort → No Result

Inverse Up Thrust

Failed Buying Climax

Bear Outside Reversal

End of Rising Market (Bag Seller)

Pseudo Up Thrust

No Demand

Neutral Patterns (🔵): Patterns indicating market indecision and potential for continuation or reversal.

Quiet Doji

Balanced Doji

Strong Doji

Quiet Spinning Top

Balanced Spinning Top

Strong Spinning Top

Quiet High Wave

Balanced High Wave

Strong High Wave

Consolidation

Bar Patterns (🟡): Common candlestick patterns that offer insights into market sentiment. These are required in some VSA patterns and can also be displayed independently.

Bull Pin Bar

Bear Pin Bar

Doji

Spinning Top

High Wave

Consolidation

This demonstrates the acronym and descriptive options for displaying bar patterns, with the ability to hover over text to reveal the descriptive text along with what type of pattern:

█ Alerts:

VSA Pattern Alerts: Notifications for identified VSA patterns at bar close.

Volume and Spread Alerts: Alerts for confirmed and forecasted volume/spread levels (Low, High, Ultra).

Forecasted Volume and Spread Alerts: Alerts for forecasted volume/spread levels (High, Ultra) include a minimum percent time elapsed input to reduce false early signals by ensuring sufficient bar time has passed.

█ Inputs and Settings:

Display Volume and/or Spread: Choose between displaying volume bars, spread bars, or both with different lookback periods.

Indicator Bar Color: Select color schemes for bars (Normal, Detail, Levels).

Indicator Moving Average Color: Select schemes for bars (Fill, Lines, None).

Price Bar Colors: Options to color price bars based on VSA patterns and volume levels.

Legend: Display a table of bar colors and levels for context and clarity of volume/spread bars.

Forecast: Configure forecast display and prediction details for volume and spread.

Average Multipliers: Define multipliers for different levels (Low, High, Ultra) to refine the analysis.

Moving Average: Set volume and spread moving average settings.

VSA: Select the VSA patterns to be calculated and displayed (Strength, Weakness, Neutral).

Bar Patterns: Criteria for bar patterns used in VSA (Doji, Bull Pin Bar, Bear Pin Bar, Spinning Top, Consolidation, High Wave).

Colors: Set exact colors used for indicator bars, indicator moving averages, and price bars.

More Display Options: Specify how VSA pattern text is displayed (Acronym, Descriptive), positioning, and sizes.

Alerts: Configure alerts for VSA patterns, volume, and spread levels, including forecasted levels.

█ Usage:

The Volume Spread Analysis indicator is a helpful tool for leveraging volume spread analysis to make informed trading decisions. It offers comprehensive visual and textual cues on the chart, making it easier to identify market conditions, potential reversals, and continuations. Whether analyzing historical data or forecasting future trends, this indicator provides insights into the underlying factors driving market movements.

Delta ZigZag [LuxAlgo]The Delta ZigZag indicator is focused on volume analysis during the development of ZigZag lines. Volume data can be retrieved from a Lower timeframe (LTF) or real-time Tick data.

Our Delta ZigZag publication can be helpful in detecting indications of a trend reversal or potential weakening/strengthening of the trend.

This indicator by its very nature backpaints, meaning that the displayed components are offset in the past.

🔶 USAGE

The ZigZag line is formed by connecting Swings , which can be set by adjusting the Left and Right settings.

Left is the number of bars for evaluation at the left of the evaluated point.

Right is the number of bars for evaluation at the right of the evaluated point.

A valid Swing is a value higher or lower than the bars at the left/right .

A higher Left or Right set number will generally create broader ZigZag ( ZZ ) lines, while the drawing of the ZZ line will be delayed (especially when Right is set higher). On the other hand, when Right is set at 0, ZZ line are drawn quickly. However, this results in a hyperactive switching of the ZZ direction.

To ensure maximum visibility of values, we recommend using " Bars " from the " Bar's style " menu.

🔹 Volume examination

The script provides two options for Volume examination :

Examination per ZigZag line

Examination per bar

Bullish Volume is volume associated with a green bar ( close > open )

Bearish Volume is volume associated with a red bar ( close < open )

Neutral Volume (volume on a " close == open" bar) is not included in this publication.

🔹 Examination per ZigZag line

As long as the price moves in the same direction, the present ZZ line will continue. When the direction of the price changes, the bull/bear volume of the previous ZZ line is evaluated and drawn on the chart.

The ZZ line is divided into two parts: a bullish green line and a bearish red line.

The intercept of these two lines will depend on the ratio of bullish/bearish volume

This ratio is displayed at the intercept as % bullish volume (Settings -> Show % Bullish Volume)

* Note that we cannot draw between 2 bars. Therefore, if a ZZ line is only 1 bar long, the intercept will be at one of those 2 bars and not in between. The percentage can be helpful in interpreting bull/bear volume.

In the example above (2 most right labels), you can see that an overlap of 2 labels is prevented, ensuring the ability to evaluate the bullish % volume of the ZZ line .

The percentage will be colored green when more than 50%, red otherwise. The color will fade when the direction is contradictory; for example, 40% when the ZZ line goes up or 70% when the ZZ line falls.

More details can be visualized by enabling " Show " and choosing 1 of 3 options:

Average Volume Delta/bar

Average Volume/bar

Normalised Volume Delta

For both 'averages', the sum of " Volume "/" Volume Delta " of every bar on the ZZ line is divided by the number of bars (per ZZ line ).

The " Normalised Volume Delta " is calculated by dividing the sum of " Delta Volume " by the sum of " Volume " (neutral volume not included), which is displayed as a percentage.

All three options will display a label at the last point of the ZZ line and be coloured similarly: green when the ratio bullish/bearish volume of the ZZ line is bullish and red otherwise. Here, the colour also fades when it is bullish, but the ZZ line falls or when it is bearish with a rising ZZ line .

A tooltip at each label hints at the chosen option.

You can pick one of the options or combine them together.

🔹 Examination per bar

Besides information about what's happening during the ZZ line , information per bar can be visualized by enabling " Show Details " in Settings .

Split Volume per bar : show the sum of bullish (upV) and bearish (dnV) volume per bar

Volume (bar) : Total Volume per bar (bullish + bearish volume, neutral volume not included)

Δ Volume (bar) : Show Delta Volume (bullish - bearish volume)

🔹 Using Lower Timeframe Data

The ZigZag lines using LTF data are colored brighter. Also note the vertical line where the LTF data starts and the gap between ZZ lines with LTF data and without.

When " LTF " is chosen for the " Data from: " option in Settings , data is retrieved from Lower Timeframe bars (default 1 minute). When the LTF setting is higher than the current chart timeframe, the LTF period will automatically be adjusted to the current timeframe to prevent errors.

As there is a 100K limit to the number of LTF intrabars that can be analyzed by a script, this implies the higher the difference between LTF and current TF; the fewer ZZ lines will be seen.

🔹 Using real-time tick data

The principles are mostly the same as those of LTF data. However, in contrast with LTF data, where you already have LTF ZZ lines when loading the script, real-time tick data-based ZZ lines will only start after loading the chart.

Changing the settings of a ticker will reset everything. However, returning to the same settings/ticker would show the cached data again.

Here, you can see that changing settings reset everything, but returning after 2 minutes to the initial settings shows the cached data. Don't expect it to be cached for hours or days, though.

🔶 DETAILS

The timeframe used for LTF data should always be the same or lower than the current TF; otherwise, an error occurs. This snippet prevents the error and adjusts the LTF to the current TF when LTF is too high:

res = input.timeframe('1')

res := timeframe.from_seconds( math.min( timeframe.in_seconds(timeframe.period), timeframe.in_seconds(res) ) )

🔶 SETTINGS

Data from: LTF (Lower TimeFrame) or Ticks (Real-time ticks)

Res: Lower TimeFrame (only applicable when choosing LTF )

Option: choose " high/low " or " close " for Swing detection

🔹 ZigZag

Left: Lookback period for Swings

Right: Confirmation period after potential Swing

🔹 ZigZag Delta

Show % Bullish Volume : % bullish volume against total volume during the ZZ line

Show:

Average Volume Delta/bar

Average Volume/bar

Normalised Volume Delta

See USAGE for more information

🔹 Bar Data

Split Volume per bar: shows the sum of bullish ( upV ) and bearish ( dnV ) volume per bar

Volume (bar): Total Volume per bar (bullish + bearish volume, neutral volume not included)

Δ Volume (bar): Show Volume Delta (bullish - bearish volume)

LYGLibraryLibrary "LYGLibrary"

A collection of custom tools & utility functions commonly used with my scripts

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

toWhole(number)

Converts pips into whole numbers

Parameters:

number (float)

Returns: The converted number

toPips(number)

Converts whole numbers back into pips

Parameters:

number (float)

Returns: The converted number

getPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period

Parameters:

value1 (float)

value2 (float)

lookback (int)

av_getPositionSize(balance, risk, stopPoints, conversionRate)

Calculates OANDA forex position size for AutoView based on the given parameters

Parameters:

balance (float)

risk (float)

stopPoints (float)

conversionRate (float)

Returns: The calculated position size (in units - only compatible with OANDA)

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(length, maType)

Gets a Moving Average based on type (MUST BE CALLED ON EVERY CALCULATION)

Parameters:

length (simple int)

maType (string)

Returns: A moving average with the given parameters

getEAP(atr)

Performs EAP stop loss size calculation (eg. ATR >= 20.0 and ATR < 30, returns 20)

Parameters:

atr (float)

Returns: The EAP SL converted ATR size

getEAP2(atr)

Performs secondary EAP stop loss size calculation (eg. ATR < 40, add 5 pips, ATR between 40-50, add 10 pips etc)

Parameters:

atr (float)

Returns: The EAP SL converted ATR size

barsAboveMA(lookback, ma)

Counts how many candles are above the MA

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(lookback, ma)

Counts how many candles are below the MA

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many times price recently crossed the EMA

getPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

lookback (int)

direction (int)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize()

Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize()

Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize()

Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent()

Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(fib, colorMatch)

Checks if the current bar is a hammer candle based on the given parameters

Parameters:

fib (float)

colorMatch (bool)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(fib, colorMatch)

Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

fib (float)

colorMatch (bool)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(wickSize, bodySize)

Checks if the current bar is a doji candle based on the given parameters

Parameters:

wickSize (float)

bodySize (float)

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bullish engulfing candle

Parameters:

allowance (float)

rejectionWickSize (float)

engulfWick (bool)

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bearish engulfing candle

Parameters:

allowance (float)

rejectionWickSize (float)

engulfWick (bool)

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

isInsideBar()

Detects inside bars

Returns: Returns true if the current bar is an inside bar

isOutsideBar()

Detects outside bars

Returns: Returns true if the current bar is an outside bar

barInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls within the given time session

barOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls outside the given time session

dateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range

Parameters:

startTime (int)

endTime (int)

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze

Parameters:

monday (bool)

tuesday (bool)

wednesday (bool)

thursday (bool)

friday (bool)

saturday (bool)

sunday (bool)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter(atrValue, maxSize)

Parameters:

atrValue (float)

maxSize (float)

fillCell(tableID, column, row, title, value, bgcolor, txtcolor)

This updates the given table's cell with the given values

Parameters:

tableID (table)

column (int)

row (int)

title (string)

value (string)

bgcolor (color)

txtcolor (color)

Returns: A boolean - true if the current bar falls within the given dates

CVD - Cumulative Volume Delta (Chart)█ OVERVIEW

This indicator displays cumulative volume delta (CVD) as an on-chart oscillator. It uses intrabar analysis to obtain more precise volume delta information compared to methods that only use the chart's timeframe.

The core concepts in this script come from our first CVD indicator , which displays CVD values as plot candles in a separate indicator pane. In this script, CVD values are scaled according to price ranges and represented on the main chart pane.

█ CONCEPTS

Bar polarity

Bar polarity refers to the position of the close price relative to the open price. In other words, bar polarity is the direction of price change.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 bars at the lower timeframe of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script utilizes a LTF to analyze intrabars, or price changes within a chart bar. The lower the LTF, the more intrabars are analyzed, but the less chart bars can display information due to the limited number of intrabars that can be analyzed.

Volume delta

Volume delta is a measure that separates volume into "up" and "down" parts, then takes the difference to estimate the net demand for the asset. This approach gives traders a more detailed insight when analyzing volume and market sentiment. There are several methods for determining whether an asset's volume belongs in the "up" or "down" category. Some indicators, such as On Balance Volume and the Klinger Oscillator , use the change in price between bars to assign volume values to the appropriate category. Others, such as Chaikin Money Flow , make assumptions based on open, high, low, and close prices. The most accurate method involves using tick data to determine whether each transaction occurred at the bid or ask price and assigning the volume value to the appropriate category accordingly. However, this method requires a large amount of data on historical bars, which can limit the historical depth of charts and the number of symbols for which tick data is available.

In the context where historical tick data is not yet available on TradingView, intrabar analysis is the most precise technique to calculate volume delta on historical bars on our charts. This indicator uses intrabar analysis to achieve a compromise between simplicity and accuracy in calculating volume delta on historical bars. Our Volume Profile indicators use it as well. Other volume delta indicators in our Community Scripts , such as the Realtime 5D Profile , use real-time chart updates to achieve more precise volume delta calculations. However, these indicators aren't suitable for analyzing historical bars since they only work for real-time analysis.

This is the logic we use to assign intrabar volume to the "up" or "down" category:

• If the intrabar's open and close values are different, their relative position is used.

• If the intrabar's open and close values are the same, the difference between the intrabar's close and the previous intrabar's close is used.

• As a last resort, when there is no movement during an intrabar and it closes at the same price as the previous intrabar, the last known polarity is used.

Once all intrabars comprising a chart bar are analyzed, we calculate the net difference between "up" and "down" intrabar volume to produce the volume delta for the chart bar.

█ FEATURES

CVD resets

The "cumulative" part of the indicator's name stems from the fact that calculations accumulate during a period of time. By periodically resetting the volume delta accumulation, we can analyze the progression of volume delta across manageable chunks, which is often more useful than looking at volume delta accumulated from the beginning of a chart's history.

You can configure the reset period using the "CVD Resets" input, which offers the following selections:

• None : Calculations do not reset.

• On a fixed higher timeframe : Calculations reset on the higher timeframe you select in the "Fixed higher timeframe" field.

• At a fixed time that you specify.

• At the beginning of the regular session .

• On trend changes : Calculations reset on the direction change of either the Aroon indicator, Parabolic SAR , or Supertrend .

• On a stepped higher timeframe : Calculations reset on a higher timeframe automatically stepped using the chart's timeframe and following these rules:

Chart TF HTF

< 1min 1H

< 3H 1D

<= 12H 1W

< 1W 1M

>= 1W 1Y

Specifying intrabar precision

Ten options are included in the script to control the number of intrabars used per chart bar for calculations. The greater the number of intrabars per chart bar, the fewer chart bars can be analyzed.

The first five options allow users to specify the approximate amount of chart bars to be covered:

• Least Precise (Most chart bars) : Covers all chart bars by dividing the current timeframe by four.

This ensures the highest level of intrabar precision while achieving complete coverage for the dataset.

• Less Precise (Some chart bars) & More Precise (Less chart bars) : These options calculate a stepped LTF in relation to the current chart's timeframe.

• Very precise (2min intrabars) : Uses the second highest quantity of intrabars possible with the 2min LTF.

• Most precise (1min intrabars) : Uses the maximum quantity of intrabars possible with the 1min LTF.

The stepped lower timeframe for "Less Precise" and "More Precise" options is calculated from the current chart's timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

The last five options allow users to specify an approximate fixed number of intrabars to analyze per chart bar. The available choices are 12, 24, 50, 100, and 250. The script will calculate the LTF which most closely approximates the specified number of intrabars per chart bar. Keep in mind that due to factors such as the length of a ticker's sessions and rounding of the LTF, it is not always possible to produce the exact number specified. However, the script will do its best to get as close to the value as possible.

As there is a limit to the number of intrabars that can be analyzed by a script, a tradeoff occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

Display

This script displays raw or cumulative volume delta values on the chart as either line or histogram oscillator zones scaled according to the price chart, allowing traders to visualize volume activity on each bar or cumulatively over time. The indicator's background shows where CVD resets occur, demarcating the beginning of new zones. The vertical axis of each oscillator zone is scaled relative to the one with the highest price range, and the oscillator values are scaled relative to the highest volume delta. A vertical offset is applied to each oscillator zone so that the highest oscillator value aligns with the lowest price. This method ensures an accurate, intuitive visual comparison of volume activity within zones, as the scale is consistent across the chart, and oscillator values sit below prices. The vertical scale of oscillator zones can be adjusted using the "Zone Height" input in the script settings.

This script displays labels at the highest and lowest oscillator values in each zone, which can be enabled using the "Hi/Lo Labels" input in the "Visuals" section of the script settings. Additionally, the oscillator's value on a chart bar is displayed as a tooltip when a user hovers over the bar, which can be enabled using the "Value Tooltips" input.

Divergences occur when the polarity of volume delta does not match that of the chart bar. The script displays divergences as bar colors and background colors that can be enabled using the "Color bars on divergences" and "Color background on divergences" inputs.

An information box in the lower-left corner of the indicator displays the HTF used for resets, the LTF used for intrabars, the average quantity of intrabars per chart bar, and the number of chart bars for which there is LTF data. This is enabled using the "Show information box" input in the "Visuals" section of the script settings.

FOR Pine Script™ CODERS

• This script utilizes `ltf()` and `ltfStats()` from the lower_tf library.

The `ltf()` function determines the appropriate lower timeframe from the selected calculation mode and chart timeframe, and returns it in a format that can be used with request.security_lower_tf() .

The `ltfStats()` function, on the other hand, is used to compute and display statistical information about the lower timeframe in an information box.

• The script utilizes display.data_window and display.status_line to restrict the display of certain plots.

These new built-ins allow coders to fine-tune where a script’s plot values are displayed.

• The newly added session.isfirstbar_regular built-in allows for resetting the CVD segments at the start of the regular session.

• The VisibleChart library developed by our resident PineCoders team leverages the chart.left_visible_bar_time and chart.right_visible_bar_time variables to optimize the performance of this script.

These variables identify the opening time of the leftmost and rightmost visible bars on the chart, allowing the script to recalculate and draw objects only within the range of visible bars as the user scrolls.

This functionality also enables the scaling of the oscillator zones.

These variables are just a couple of the many new built-ins available in the chart.* namespace.

For more information, check out this blog post or look them up by typing "chart." in the Pine Script™ Reference Manual .

• Our ta library has undergone significant updates recently, including the incorporation of the `aroon()` indicator used as a method for resetting CVD segments within this script.

Revisit the library to see more of the newly added content!

Look first. Then leap.

Intrabar Efficiency Ratio█ OVERVIEW

This indicator displays a directional variant of Perry Kaufman's Efficiency Ratio, designed to gauge the "efficiency" of intrabar price movement by comparing the sum of movements of the lower timeframe bars composing a chart bar with the respective bar's movement on an average basis.

█ CONCEPTS

Efficiency Ratio (ER)

Efficiency Ratio was first introduced by Perry Kaufman in his 1995 book, titled "Smarter Trading". It is the ratio of absolute price change to the sum of absolute changes on each bar over a period. This tells us how strong the period's trend is relative to the underlying noise. Simply put, it's a measure of price movement efficiency. This ratio is the modulator utilized in Kaufman's Adaptive Moving Average (KAMA), which is essentially an Exponential Moving Average (EMA) that adapts its responsiveness to movement efficiency.

ER's output is bounded between 0 and 1. A value of 0 indicates that the starting price equals the ending price for the period, which suggests that price movement was maximally inefficient. A value of 1 indicates that price had travelled no more than the distance between the starting price and the ending price for the period, which suggests that price movement was maximally efficient. A value between 0 and 1 indicates that price had travelled a distance greater than the distance between the starting price and the ending price for the period. In other words, some degree of noise was present which resulted in reduced efficiency over the period.

As an example, let's say that the price of an asset had moved from $15 to $14 by the end of a period, but the sum of absolute changes for each bar of data was $4. ER would be calculated like so:

ER = abs(14 - 15)/4 = 0.25

This suggests that the trend was only 25% efficient over the period, as the total distanced travelled by price was four times what was required to achieve the change over the period.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 intrabars at the LTF of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script determines which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed, but fewer chart bars can display indicator information because there is a limit to the total number of intrabars that can be analyzed.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. As there is a 100K limit to the number of intrabars that can be analyzed by a script, a trade-off occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

Intrabar Efficiency Ratio (IER)