Interactive Compound Interest ProjectorThis indicator is an interactive tool designed for long-term investors and analysts who want to compare an asset's performance against a theoretical compound interest growth curve.

Unlike static tools, this script utilizes the Interactive Anchor feature. This allows you to click on any specific point on the chart (e.g., a market bottom, a specific entry date, or a previous all-time high) to serve as the starting point ("Principal") for the projection.

How to use

Add the indicator to your chart.

Important: Because confirm=true is enabled, the script will wait for you to click on the chart. Click on the specific candle you want to use as the "Start Date".

The Yellow Line will appear starting from that candle.

Open the indicator settings to adjust:

Annual Interest Rate: (Default 6.0%).

Project until Year: (Default 2050).

Use this to visualize if an asset is "beating" a standard benchmark (like a 10% S&P500 average or a 4% risk-free rate) from a specific moment in time.

Disclaimer: This tool is for educational and comparative analysis purposes only and does not guarantee future results.

Recherche dans les scripts pour "curve"

Linear Moments█ OVERVIEW

The Linear Moments indicator, also known as L-moments, is a statistical tool used to estimate the properties of a probability distribution. It is an alternative to conventional moments and is more robust to outliers and extreme values.

█ CONCEPTS

█ Four moments of a distribution

We have mentioned the concept of the Moments of a distribution in one of our previous posts. The method of Linear Moments allows us to calculate more robust measures that describe the shape features of a distribution and are anallougous to those of conventional moments. L-moments therefore provide estimates of the location, scale, skewness, and kurtosis of a probability distribution.

The first L-moment, λ₁, is equivalent to the sample mean and represents the location of the distribution. The second L-moment, λ₂, is a measure of the dispersion of the distribution, similar to the sample standard deviation. The third and fourth L-moments, λ₃ and λ₄, respectively, are the measures of skewness and kurtosis of the distribution. Higher order L-moments can also be calculated to provide more detailed information about the shape of the distribution.

One advantage of using L-moments over conventional moments is that they are less affected by outliers and extreme values. This is because L-moments are based on order statistics, which are more resistant to the influence of outliers. By contrast, conventional moments are based on the deviations of each data point from the sample mean, and outliers can have a disproportionate effect on these deviations, leading to skewed or biased estimates of the distribution parameters.

█ Order Statistics

L-moments are statistical measures that are based on linear combinations of order statistics, which are the sorted values in a dataset. This approach makes L-moments more resistant to the influence of outliers and extreme values. However, the computation of L-moments requires sorting the order statistics, which can lead to a higher computational complexity.

To address this issue, we have implemented an Online Sorting Algorithm that efficiently obtains the sorted dataset of order statistics, reducing the time complexity of the indicator. The Online Sorting Algorithm is an efficient method for sorting large datasets that can be updated incrementally, making it well-suited for use in trading applications where data is often streamed in real-time. By using this algorithm to compute L-moments, we can obtain robust estimates of distribution parameters while minimizing the computational resources required.

█ Bias and efficiency of an estimator

One of the key advantages of L-moments over conventional moments is that they approach their asymptotic normal closer than conventional moments. This means that as the sample size increases, the L-moments provide more accurate estimates of the distribution parameters.

Asymptotic normality is a statistical property that describes the behavior of an estimator as the sample size increases. As the sample size gets larger, the distribution of the estimator approaches a normal distribution, which is a bell-shaped curve. The mean and variance of the estimator are also related to the true mean and variance of the population, and these relationships become more accurate as the sample size increases.

The concept of asymptotic normality is important because it allows us to make inferences about the population based on the properties of the sample. If an estimator is asymptotically normal, we can use the properties of the normal distribution to calculate the probability of observing a particular value of the estimator, given the sample size and other relevant parameters.

In the case of L-moments, the fact that they approach their asymptotic normal more closely than conventional moments means that they provide more accurate estimates of the distribution parameters as the sample size increases. This is especially useful in situations where the sample size is small, such as when working with financial data. By using L-moments to estimate the properties of a distribution, traders can make more informed decisions about their investments and manage their risk more effectively.

Below we can see the empirical dsitributions of the Variance and L-scale estimators. We ran 10000 simulations with a sample size of 100. Here we can clearly see how the L-moment estimator approaches the normal distribution more closely and how such an estimator can be more representative of the underlying population.

█ WAYS TO USE THIS INDICATOR

The Linear Moments indicator can be used to estimate the L-moments of a dataset and provide insights into the underlying probability distribution. By analyzing the L-moments, traders can make inferences about the shape of the distribution, such as whether it is symmetric or skewed, and the degree of its spread and peakedness. This information can be useful in predicting future market movements and developing trading strategies.

One can also compare the L-moments of the dataset at hand with the L-moments of certain commonly used probability distributions. Finance is especially known for the use of certain fat tailed distributions such as Laplace or Student-t. We have built in the theoretical values of L-kurtosis for certain common distributions. In this way a person can compare our observed L-kurtosis with the one of the selected theoretical distribution.

█ FEATURES

Source Settings

Source - Select the source you wish the indicator to calculate on

Source Selection - Selec whether you wish to calculate on the source value or its log return

Moments Settings

Moments Selection - Select the L-moment you wish to be displayed

Lookback - Determine the sample size you wish the L-moments to be calculated with

Theoretical Distribution - This setting is only for investingating the kurtosis of our dataset. One can compare our observed kurtosis with the kurtosis of a selected theoretical distribution.

Relative Strength Heatmap [BackQuant]Relative Strength Heatmap

A multi-horizon RSI matrix that compresses 20 different lookbacks into a single panel, turning raw momentum into a visual “pressure gauge” for overbought and oversold clustering, trend exhaustion, and breadth of participation across time horizons.

What this is

This indicator builds a strip-style heatmap of 20 RSIs, each with a different length, and stacks them vertically as colored tiles in a single pane. Every tile is colored by its RSI value using your chosen palette, so you can see at a glance:

How many “fast” versus “slow” RSIs are overbought or oversold.

Whether momentum is concentrated in the short lookbacks or spread across the whole curve.

When momentum extremes cluster, signalling strong market pressure or exhaustion.

On top of the tiles, the script plots two simple breadth lines:

A white line that counts how many RSIs are above 70 (overbought cluster).

A black line that counts how many RSIs are below 30 (oversold cluster).

This turns a single symbol’s RSI ladder into a compact “market pressure gauge” that shows not only whether RSI is overbought or oversold, but how many different horizons agree at the same time.

Core idea

A single RSI looks at one length and one timescale. Markets, however, are driven by flows that operate on multiple horizons at once. By computing RSI over a ladder of lengths, you approximate a “term structure” of strength:

Short lengths react to immediate swings and very recent impulses.

Medium lengths reflect swing behaviour and local trends.

Long lengths reflect structural bias and higher timeframe regime.

When many lengths agree, for example 10 or more RSIs all above 70, it suggests broad participation and strong directional pressure. When only a few fast lengths stretch to extremes while longer ones stay neutral, the move is more fragile and more likely to mean-revert.

This script makes that structure visible as a heatmap instead of forcing you to run many separate RSI panes.

How it works

1) Generating RSI lengths

You control three parameters in the calculation settings:

RS Period – the base RSI length used for the shortest strip.

RSI Step – the amount added to each successive RSI length.

RSI Multiplier – a global scaling factor applied after the step.

Each of the 20 RSIs uses:

RSI length = round((base_length + step × index) × multiplier) , where the index goes from 0 to 19.

That means:

RSI 1 uses (len + step × 0) × mult.

RSI 2 uses (len + step × 1) × mult.

…

RSI 20 uses (len + step × 19) × mult.

You can keep the ladder dense (small step and multiplier) or stretch it across much longer horizons.

2) Heatmap layout and grouping

Each RSI is plotted as an “area” strip at a fixed vertical level using histbase to stack them:

RSI 1–5 form Group 1.

RSI 6–10 form Group 2.

RSI 11–15 form Group 3.

RSI 16–20 form Group 4.

Each group has a toggle:

Show only Group 1 and 2 if you care mainly about fast and medium horizons.

Show all groups for a full spectrum from very short to very long.

Hide any group that feels redundant for your workflow.

The actual numeric RSI values are not plotted as lines. Instead, each strip is drawn as a horizontal band whose fill color represents the current RSI regime.

3) Palette-based coloring

Each tile’s color is driven by the RSI value and your chosen palette. The script includes several palettes:

Viridis – smooth green to yellow, good for subtle reading.

Jet – strong blue to red sequence with high contrast.

Plasma – purple through orange to yellow.

Custom Heat – cool blues to neutral grey to hot reds.

Gray – grayscale from white to black for minimalistic layouts.

Cividis, Inferno, Magma, Turbo, Rainbow – additional scientific and rainbow-style maps.

Internally, RSI values are bucketed into ranges (for example, below 10, 10–20, …, 90–100). Each bucket maps to a unique colour for that palette. In all schemes, low RSI values are mapped to the “cold” or darker side and high RSI values to the “hot” or brighter side.

The result is a true momentum heatmap:

Cold or dark tiles show low RSI and oversold or compressed conditions.

Mid tones show neutral or mid-range RSI.

Warm or bright tiles show high RSI and overbought or stretched conditions.

4) Bull and bear breadth counts

All 20 RSI values are collected into an array each bar. Two counters are then calculated:

Bull count – how many RSIs are above 70.

Bear count – how many RSIs are below 30.

These are plotted as:

A white line (“RSI > 70 Count”) for the overbought cluster.

A black line (“RSI < 30 Count”) for the oversold cluster.

If you enable the “Show Bull and Bear Count” option, you get an immediate reading of how many of the 20 horizons are stretched at any moment.

5) Cluster alerts and background tagging

Two alert conditions monitor “strong cluster” regimes:

RSI Heatmap Strong Bull – triggers when at least 10 RSIs are above 70.

RSI Heatmap Strong Bear – triggers when at least 10 RSIs are below 30.

When one of these conditions is true, the indicator can tint the background of the chart using a soft version of the current palette. This visually marks stretches where momentum is extreme across many lengths at once, not just on a single RSI.

What it plots

In one oscillator window, the indicator provides:

Up to 20 horizontal RSI strips, each representing a different RSI length.

Color-coded tiles reflecting the current RSI value for each length.

Group toggles to show or hide each block of five RSIs.

An optional white line that counts how many RSIs are above 70.

An optional black line that counts how many RSIs are below 30.

Optional background highlights when the number of overbought or oversold RSIs passes the strong-cluster threshold.

How it measures breadth and pressure

Single-symbol breadth

Breadth is usually defined across a basket of symbols, such as how many stocks advance versus decline. This indicator uses the same concept across time horizons for a single symbol. The question becomes:

“How many different RSI lengths are stretched in the same direction at once?”

Examples:

If only 2 or 3 of the shortest RSIs are above 70, bull count stays low. The move is fast and local, but not yet broadly supported.

If 12 or more RSIs across short, medium and long lengths are above 70, the bull count spikes. The move has broad momentum and strong upside pressure.

If 10 or more RSIs are below 30, bear count spikes and you are in a broad oversold regime.

This is breadth of momentum within one market.

Market pressure gauge

The combination of heatmap tiles and breadth lines acts as a pressure gauge:

High bull count with warm colors across most strips indicates strong upside pressure and crowded long positioning.

High bear count with cold colors across most strips indicates strong downside pressure and capitulation or forced selling.

Low counts with a mixed heatmap indicate neutral pressure, fragmented flows, or range-bound conditions.

You can treat the strong-cluster alerts as “extreme pressure” signals. When they fire, the market is heavily skewed in one direction across many horizons.

How to read the heatmap

Horizontal patterns (through time)

Look along the time axis and watch how the colors evolve:

Persistent hot tiles across many strips show sustained bullish pressure and trend strength.

Persistent cold tiles across many strips show sustained bearish pressure and weak demand.

Frequent flipping between hot and cold colours indicates a choppy or mean-reverting environment.

Vertical structure (across lengths at one bar)

Focus on a single bar and read the column of tiles from top to bottom:

Short RSIs hot, long RSIs neutral or cool: early trend or short-term fomo. Price has moved fast, longer horizons have not caught up.

Short and long RSIs all hot: mature, entrenched uptrend. Broad participation, high pressure, greater risk of blow-off or late-entry vulnerability.

Short RSIs cold but long RSIs mid to high: pullback in a higher timeframe uptrend. Dip-buy and continuation setups are often found here.

Short RSIs high but long RSIs low: countertrend rallies within a broader downtrend. Good hunting ground for fades and short entries after a bounce.

Bull and bear breadth lines

Use the two lines as simple, numeric breadth indicators:

A rising white line shows more RSIs pushing above 70, so bullish pressure is expanding in breadth.

A rising black line shows more RSIs pushing below 30, so bearish pressure is expanding in breadth.

When both lines are low and flat, few horizons are extreme and the market is in mid-range territory.

Cluster zones

When either count crosses the strong threshold (for example 10 out of 20 RSIs in extreme territory):

A strong bull cluster marks a broadly overbought regime. Trend followers may see this as confirmation. Mean-reversion traders may see it as a late-stage or blow-off context.

A strong bear cluster marks a broadly oversold regime. Downtrend traders see strong pressure, but the risk of sharp short-covering bounces also increases.

Trading applications

Trend confirmation

Use the heatmap and breadth lines as a trend filter:

Prefer long setups when the heatmap shows mostly mid to high RSIs and the bull count is rising.

Avoid fresh shorts when there is a strong bull cluster, unless you are specifically trading exhaustion.

Prefer short setups when the heatmap is mostly low RSIs and the bear count is rising.

Avoid aggressive longs when a strong bear cluster is active, unless you are trading reflexive bounces.

Mean-reversion timing

Treat cluster extremes as exhaustion zones:

Look for reversal patterns, failed breakouts, or order flow shifts when bull count is very high and price starts to stall or diverge.

Look for reflexive bounce potential when bear count is very high and price stops making new lows or shows absorption at the lows.

Use the palette and counts together: hot tiles plus a peaking white line can mark blow-off conditions, cold tiles plus a peaking black line can mark capitulation.

Regime detection and risk toggling

Use the overall shape of the ladder over time:

If upper strips stay warm and lower strips stay neutral or warm for extended periods, the market is in an uptrend regime. You can justify higher risk for long-biased strategies.

If upper strips stay cold and lower strips stay neutral or cold, the market is in a downtrend regime. You can justify higher risk for short-biased strategies or defensive positioning.

If colours and counts flip frequently, you are likely in a range or choppy regime. Consider reducing size or using more tactical, short-term strategies.

Multi-horizon synchronization

You can think of each RSI length as a proxy for a different “speed” of the same market:

When only fast RSIs are stretched, the move is local and less robust.

When fast, medium and slow RSIs align, the move has multi-horizon confirmation.

You can require a minimum bull or bear count before allowing your main strategy to engage.

Spotting hidden shifts

Sometimes price appears flat or drifting, but the heatmap quietly cools or warms:

If price is sideways while many hot tiles fade toward neutral, momentum is decaying under the surface and trend risk is increasing.

If price is sideways while many cold tiles climb back toward neutral, selling pressure is decaying and the tape is repairing itself.

Settings overview

Calculation Settings

RS Period – base RSI length for the shortest strip.

RSI Step – the increment added to each successive RSI length.

RSI Multiplier – scales all generated RSI lengths.

Calculation Source – the input series, such as close, hlc3 or others.

Plotting and Coloring Settings

Heatmap Color Palette – choose between Viridis, Jet, Plasma, Custom Heat, Gray, Cividis, Inferno, Magma, Turbo or Rainbow.

Show Group 1 – toggles RSI 1–5.

Show Group 2 – toggles RSI 6–10.

Show Group 3 – toggles RSI 11–15.

Show Group 4 – toggles RSI 16–20.

Show Bull and Bear Count – enables or disables the two breadth lines.

Alerts

RSI Heatmap Strong Bull – fires when the number of RSIs above 70 reaches or exceeds the configured threshold (default 10).

RSI Heatmap Strong Bear – fires when the number of RSIs below 30 reaches or exceeds the configured threshold (default 10).

Tuning guidance

Fast, tactical configurations

Use a small base RS Period, for example 2 to 5.

Use a small RSI Step, for tight clustering around the fast horizon.

Keep the multiplier near 1.0 to avoid extreme long lengths.

Focus on Group 1 and Group 2 for intraday and short-term trading.

Swing and position configurations

Use a mid-range RS Period, for example 7 to 14.

Use a moderate RSI Step to fan out into slower horizons.

Optionally use a multiplier slightly above 1.0.

Keep all four groups enabled for a full view from fast to slow.

Macro or higher timeframe configurations

Use a larger base RS Period.

Use a larger RSI Step so the top of the ladder reaches very slow lengths.

Focus on Group 3 and Group 4 to see structural momentum.

Treat clusters as regime markers rather than frequent trading signals.

Notes

This indicator is a contextual tool, not a standalone trading system. It does not model execution, spreads, slippage or fundamental drivers. Use it to:

Understand whether momentum is narrow or broad across horizons.

Confirm or filter existing signals from your primary strategy.

Identify environments where the market is crowded into one side.

Distinguish between isolated spikes and truly broad pressure moves.

The Relative Strength Heatmap is designed to answer a simple but powerful question:

“How many versions of RSI agree with what I am seeing on the chart?”

By compressing those answers into a single panel with clear colour coding and breadth lines, it becomes a practical, visual gauge of momentum breadth and market pressure that you can overlay on any trading framework.

Filter Volume1. Indicator Name

Filter Volume

2. One-line Introduction

A regression-based trend filter that quantifies and visualizes market direction and strength using price behavior.

3. Overall Description

Filter Volume+ is a trend-detection indicator that uses linear regression to evaluate the dominant direction of price movement over a given period.

It compares historical regression values to determine whether the market is in a bullish, bearish, or neutral state.

The indicator applies a percentage threshold to filter out weak or indecisive trends, highlighting only significant movements.

Each trend state is visualized through distinct colors: bullish (greenish), bearish (reddish), and neutral (gray), with intensity reflecting trend strength.

To reduce noise and create smooth visual signals, a three-step smoothing process is applied to the raw trend intensity.

Users can customize the regression source, lookback period, and sensitivity, allowing the indicator to adapt to various assets and timeframes.

This tool is especially useful in filtering entry signals based on clear directional bias, making it suitable for trend-following or confirmation strategies.

4. Key Benefits (Title + Description)

✅ Quantified Trend Strength

Only displays trend signals when a statistically significant direction is detected using linear regression comparisons.

✅ Visual Clarity with Color Coding

Each market state (bullish, bearish, neutral) is represented with distinct colors and transparency, enabling fast interpretation.

✅ Custom Regression Source

Users can define the data input (e.g., close, open, indicator output) for regression calculation, increasing strategic flexibility.

✅ Multi-Level Smoothing

Applies three layers of smoothing (via moving averages) to eliminate noise and produce a stable, flowing trend curve.

✅ Area Fill Visualization

Plots a colored band between the trend value and zero-line, helping users quickly gauge the market's dominant force.

✅ Adjustable Sensitivity Settings

Includes tolerance and lookback controls, allowing traders to fine-tune how reactive or conservative the trend detection should be.

5. Indicator User Guide

📌 Basic Concept

Filter Volume+ assesses the direction of price by comparing regression values over a selected period.

If the percentage of upward comparisons exceeds a threshold, a bullish state is shown; if downward comparisons dominate, it shows a bearish state.

⚙️ Settings Overview

Lookback Period (n): The number of bars to compare for trend analysis

Range Tolerance (%): Minimum threshold for declaring a strong trend

Regression Source: The data used for regression (e.g., close, open)

Linear Regression Length: Number of bars used to compute each regression value

Bull/Bear Color: Custom colors for bullish and bearish trends

📈 Example Timing

When the trend line stays above zero and the green color intensity increases → trend gaining strength

After a neutral phase (gray), the color shifts quickly to greenish → early trend reversal

📉 Example Timing

When the trend line stays below zero with deepening red color → strong bearish continuation

Sudden change from bullish to bearish color with rising intensity

🧪 Recommended Use

Use as a trend confirmation filter alongside entry/exit strategies

Ideal for swing or position trades in trending markets

Combine with oscillators like RSI or MACD for improved signal validation

🔒 Cautions

In ranging (sideways) markets, the color may change frequently – avoid relying solely on this indicator in those zones.

Low-intensity colors (faded) suggest weak trends – better to stay on the sidelines.

A short lookback period may cause over-sensitivity and false signals.

When using non-price regression sources, expect the indicator to behave differently – test before deploying.

+++

Market Breadth - [JTCAPITAL]Market Breadth - is a comprehensive crypto market strength and sentiment indicator designed to visualize the overall bullish or bearish alignment across 40 major cryptocurrencies. By combining multi-asset Exponential Moving Average (EMA) comparisons and smoothing techniques, it offers a clean, aggregated view of the broader market trend—helping traders quickly assess whether the market is dominated by bullish momentum or bearish pressure.

The indicator works by calculating in the following steps:

Symbol Selection and Data Retrieval

The script monitors 40 leading cryptocurrencies based on Market Cap. Each asset’s daily close price is requested using a 1D timeframe. This ensures that every data point reflects the same temporal resolution, allowing the indicator to evaluate global crypto strength rather than individual token volatility.

EMA Comparison per Asset

For each asset, two Exponential Moving Averages (EMAs) are calculated:

A short-term EMA with period emalength (default 10).

A long-term EMA with period emalength2 (default 20).

Each coin receives a score of +1 when the short-term EMA is greater than the long-term EMA (indicating bullish structure), or -1 when it is below (indicating bearish structure). This binary scoring system effectively converts individual price action into a directional sentiment measure.

Market Breadth Aggregation

All 40 individual scores are summed into a single composite value called scores .

If many assets have bullish EMA alignment, the total score becomes strongly positive.

If the majority show bearish alignment, the total score turns negative.

This step transforms scattered price data into one unified market breadth metric—quantifying how many assets participate in the same directional trend.

Smoothing the Breadth Line

To reduce short-term noise and isolate trend direction, the aggregated score is smoothed using an EMA of length = smoothlen (default 15). The resulting smoothed line helps identify sustained shifts in collective sentiment rather than temporary fluctuations.

Visualization and Color Coding

When scores > 0 , the market breadth is bullish and the histogram is colored blue.

When scores < 0 , the breadth turns bearish and the histogram is purple.

The same logic applies to the smoothed line and background color, offering an instant visual cue of market mood transitions.

Buy and Sell Conditions:

The indicator itself does not trigger direct buy/sell signals but rather acts as a market regime filter . Traders can use it as follows:

Buy Filter: When the smoothed value is above zero and rising, the majority of assets confirm an uptrend — this favors long setups or trend continuation entries.

Sell Filter: When the smoothed value is below zero and falling, bearish alignment dominates — ideal for short setups or defensive risk management.

Optional filters could include combining this with RSI or volume-weighted momentum indicators to confirm breadth-based reversals.

Features and Parameters:

emalength – Defines the short-term EMA length used for individual asset trend detection (default 10).

emalength2 – Defines the long-term EMA length (default 20).

smoothlen – Defines the smoothing EMA length for the total market breadth line (default 15).

40 asset inputs – User-editable symbols allow full customization of which cryptos are tracked.

Dynamic color backgrounds – Visual distinction between bullish and bearish phases.

Specifications:

Exponential Moving Average (EMA)

EMA is a type of moving average that places more weight on recent price data, responding faster to market changes compared to SMA. By comparing a short-term and long-term EMA, the indicator captures momentum shifts across each asset individually. The crossover logic (EMA10 > EMA20) signals bullish conditions, while the opposite indicates bearish momentum.

Market Breadth

Market Breadth quantifies how many assets are participating in a directional move. Instead of tracking a single coin’s trend, breadth analysis measures collective sentiment. When most coins’ short-term EMAs are above long-term EMAs, the market shows healthy bullish breadth. Conversely, when most are below, weakness dominates.

Smoothing (EMA on Scores)

After summing the breadth score, the result is smoothed with an additional EMA to mitigate the inherent volatility caused by individual coin reversals. This second-level smoothing transforms raw fluctuations into a readable, trend-consistent curve.

Color Visualization

Visual cues are integral for intuitive interpretation.

Blue Shades: Indicate bullish alignment and collective upward momentum.

Purple Shades: Indicate bearish conditions and potential risk-off phases.

The background tint reinforces visual clarity even when the indicator is overlaid on price charts.

Background Logic

By applying the same color logic to the chart’s background, users can instantly recognize the prevailing market phase.

Use Cases

As a trend confirmation filter for other indicators (e.g., trade only in the direction of positive breadth).

As a divergence tool : when price rises but breadth weakens, it may signal a topping market.

As a macro sentiment monitor : perfect for assessing when the crypto market as a whole transitions from bearish to bullish structure.

Summary

“ Market Breadth - ” transforms the chaotic price movements of 40 cryptocurrencies into a single, powerful visual representation of overall market health. By merging EMA cross analysis with market-wide aggregation and smoothing , it provides traders with a deep understanding of when bullish or bearish forces dominate the ecosystem.

It’s a clean, data-driven approach to identifying shifts in crypto market sentiment — a perfect companion for trend-following, macro analysis, and timing portfolio exposure.

Enjoy!

Alpha-Weighted RSIDescription:

The Alpha-Weighted RSI is a next-generation momentum oscillator that redefines the classic RSI by incorporating the mathematical principles of Lévy Flight. This advanced adaptation applies non-linear weighting to price changes, making the indicator more sensitive to significant market moves and less reactive to minor noise. It is designed for traders seeking a clearer, more powerful view of momentum and potential reversal zones.

🔍 Key Features & Innovations:

Lévy Flight Alpha Weighting: At the core of this indicator is the Alpha parameter (1.0-2.0), which controls the sensitivity to price changes.

Lower Alpha (e.g., 1.2): Makes the indicator highly responsive to recent price movements, ideal for capturing early trend shifts.

Higher Alpha (e.g., 1.8): Creates a smoother, more conservative output that filters out noise, focusing on stronger momentum.

Customizable Smoothing: The raw Lévy-RSI is smoothed by a user-selectable moving average (8 MA types supported: SMA, EMA, SMMA, etc.), allowing for further customization of responsiveness.

Intuitive Centered Oscillator: The RSI is centered around a zero line, providing a clean visual separation between bullish and bearish territory.

Dynamic Gradient Zones: Subtle, colour coded gradient fills in the overbought (>+25) and oversold (<-25) regions enhance visual clarity without cluttering the chart.

Modern Histogram Display: Momentum is plotted as a sleek histogram that changes color between bright cyan (bullish) and magenta (bearish) based on its position relative to the zero line.

🎯 How to Use & Interpret:

Zero-Line Crossovers: The most basic signals. A crossover above the zero line indicates building bullish momentum, while a crossover below suggests growing bearish momentum.

Overbought/Oversold Levels: Use the +25/-25 and +35/-35 levels as dynamic zones. A reading above +25 suggests strong bullish momentum (overbought), while a reading below -25 indicates strong bearish momentum (oversold).

Divergence Detection: Look for divergences between the Alpha-Weighted RSI and price action. For example, if price makes a new low but the RSI forms a higher low, it can signal a potential bullish reversal.

Alpha Tuning: Adjust the Alpha parameter to match market volatility. In choppy markets, increase alpha to reduce noise. In trending markets, decrease alpha to become more responsive.

⚙️ Input Parameters:

RSI Settings: Standard RSI inputs for Length and Calculation Source.

Lévy Flight Settings: The crucial Alpha factor for response control.

MA Settings: MA Type and MA Length for smoothing the final output.

By applying Lévy Flight dynamics, this indicator offers a nuanced perspective on momentum, helping you stay ahead of the curve. Feedback is always welcome!

Better DEMAThe Better DEMA is a new tool designed to recreate the classical moving average DEMA, into a smoother, more reliable tool. Combining many methodologies, this script offers users a unique insight into market behavior.

How does it work?

First, to get a smoother signal, we need to calculate the Gaussian filter. A Gaussian filter is a smoothing filter that reduces noise and detail by averaging data with weights following a Gaussian (bell-shaped) curve.

Now that we have the source, we will calculate the following:

n2 = n/2 (half of the user defined length)

a = 2/(1+n)

ns

Now that we have that out of the way, it is time to get into the core.

Now we calculate 2 EMAs:

slow EMA => EMA over n

fast EMA => EMA over n2 period

Rather then now doing this:

DEMA = fast EMA * 2 - slow EMA

I found this to be better:

DEMA = slow EMA * (1-a) + fast EMA * a

As a last touch I took a little something from the HMA, and used a EMA with period of √n to smooth the entire the thing.

The Trend condition at base is the following (but feel free to FAFO with it):

Long = dema > dema yesterday and dema < src

Short = dema < dema yesterday and dema > src

Methodology

While the DEMA is an amazing tool used in many great indicators, it can be far too noisy.

This made me test out many filters, out of which the Gaussian performed best.

Then I tried out the non subtractive approach and that worked too, as it made it smoother.

Compacting on all I learned and smoothing it bit by bit, I think I can say this is worth looking into :).

Use cases:

Following Trends => classic, effective :)

Smoothing sources for other indicators => if done well enough, could be useful :)

Easy trend visualization => Added extra options for that.

Strategy development => Yes

Another good thing is it does not a high lookback period, so it should be better and less overfit.

That is all for today Gs,

Have fun and enjoy!

True Single Line Fusion [by TitikSona]🧠 Full Description

True Single Line Fusion by TitikSona is an open-source oscillator that unifies Fast Stochastic, Slow Stochastic, and RSI into a single smooth momentum line.

It simplifies multi-oscillator analysis into one clear visual — helping traders recognize potential momentum shifts, exhaustion, and reversal zones.

⚙️ Core Logic

The indicator calculates:

Fast Stochastic (12,3,3) → short-term swing sensitivity

Slow Stochastic (100,8,8) → broad trend context

RSI (26) → overall strength and directional bias

All three are normalized (0–100) and averaged to form the Fusion Line, creating a single unified momentum curve.

A Signal Line (SMA-9) and Histogram are added to highlight short-term acceleration or deceleration.

Formula: Fusion = (FastK + SlowK + RSI) / 3

🔍 Interpretation

Fusion Line rising → momentum strengthening upward

Fusion Line falling → momentum weakening

Histogram color (green/red) shows the direction and intensity of the move

Background highlights identify potential extremes:

🟩 Green = potential oversold region

🟥 Red = potential overbought region

💡 How to Use

Works on any symbol and timeframe.

Use the Fusion Line’s direction and slope as momentum context, not as direct buy/sell signals.

Combine with price structure, support/resistance, or volume analysis to confirm potential reversals.

Example:

Fusion Line turning upward from green zone → possible bullish momentum shift

Fusion Line turning downward from red zone → possible bearish exhaustion

📘 Notes

Ideal for identifying turning points in ranging or consolidating markets.

Does not generate automated signals or predictions.

Open-source for learning, modification, and educational use.

Designed for clarity, low lag, and clean visualization.

🧩 Developed and shared by TitikSona — made to unify oscillators into one adaptive momentum tool.

RSI VWAP v1 [JopAlgo]RSI VWAP v1.1 made stronger by volume-aware!

We know there's nothing new and the original RSI already does an excellent job. We're just working on small, practical improvements – here's our take: The same basic idea, clearer display, and a single, specially developed rolling line: a VWAP of the RSI that incorporates volume (participation) into the calculation.

Do you prefer the pure classic?

You can still use Wilder or Cutler engines –

but the star here is the VW-RSI + rolling line.

This RSI also offers the possibility of illustrating a possible

POC (Point of Control - or the HAL or VAL) level.

However, the indicator does NOT plot any of these levels itself.

We have included an illustration in the chart for this!

We hope this version makes your decision-making easier.

What you’ll see

The RSI line with a 50 midline and optional bands: either static 70/30 or adaptive μ±k·σ of the Rolling Line.

One smoothing concept only: the Rolling Line (light blue) = VWAP of RSI.

Shadow shading between RSI and the Rolling Line (green when RSI > line, red when RSI < line).

A lighter tint only on the parts of that shadow that sit above the upper band or below the lower band (quick overbought/oversold context).

Simple divergence lines drawn from RSI pivots (green for regular bullish, red for regular bearish). No labels, no buy/sell text—kept deliberately clean.

What’s new, and why it helps

VW-RSI engine (default):

RSI can be computed from volume-weighted up/down moves, so momentum reflects how much traded when price moved—not just the direction.

Rolling Line (VWAP of RSI) with pure VWAP adaptation:

Low volume: blends toward a faster VWAP so early, thin starts aren’t missed.

Volume spikes: blends toward a slower VWAP so a single heavy bar doesn’t whip the curve.

You can reveal the Base Rolling (pre-adaptation) line to see exactly how much adaptation is happening.

Adaptive bands (optional):

Instead of fixed 70/30, use mean ± k·stdev of the Rolling Line over a lookback. Levels breathe with the market—useful in strong trends where static bounds stay pinned.

Minimal, readable panel:

One smoothing, one story. The shadow tells you who’s in control; the lighter highlight shows stretch beyond your lines.

How to read it (fast)

Bias: RSI above 50 (and a rising Rolling Line) → bullish bias; below 50 → bearish bias.

Trigger: RSI crossing the Rolling Line with the bias (e.g., above 50 and crossing up).

Stretch: Near/above the upper band, avoid chasing; near/below the lower band, avoid panic—prefer a cross back through the line.

Divergence lines: Use as context, not as standalone signals. They often help you wait for the next cross or avoid late entries into exhaustion.

Settings that actually matter

RSI Engine: VW-RSI (default), Wilder, or Cutler.

Rolling Line Length: the VWAP length on RSI (higher = calmer, lower = earlier).

Adaptive behavior (pure VWAP):

Speed-up on Low Volume → blends toward fast VWAP (factor of your length).

Dampen Spikes (volume z-score) → blends toward slow VWAP.

Fast/Slow Factors → how far those fast/slow variants sit from the base length.

Bands: choose Static 70/30 or Adaptive μ±k·σ (set the lookback and k).

Visuals: show/hide Base Rolling (ref), main shadow, and highlight beyond bands.

Signal gating: optional “ignore first bars” per day/session if you dislike open noise.

Starter presets

Scalp (1–5m): RSI 9–12, Rolling 12–18, FastFactor ~0.5, SlowFactor ~2.0, Adaptive on.

Intraday (15m–1H): RSI 10–14, Rolling 18–26, Bands k = 1.0–1.4.

Swing (4H–1D): RSI 14–20, Rolling 26–40, Bands k = 1.2–1.8, Adaptive on.

Where it shines (and limits)

Best: liquid markets where volume structure matters (majors, indices, large caps).

Works elsewhere: even with imperfect volume, the shadow + bands remain useful.

Limits: very thin/illiquid assets reduce the benefit of volume-weighting—lengthen settings if needed.

Attribution & License

Based on the concept and baseline implementation of the “Relative Strength Index” by TradingView (Pine v6 built-in).

Released as Open-source (MPL-2.0). Please keep the license header and attribution intact.

Disclaimer

For educational purposes only; not financial advice. Markets carry risk. Test first, use clear levels, and manage risk. This project is independent and not affiliated with or endorsed by TradingView.

TTM Squeeze Screener [Pineify]TTM Squeeze Screener for Multiple Crypto Assets and Timeframes

This advanced TradingView Pine script, TTM Squeeze Screener, helps traders scan multiple crypto symbols and timeframes simultaneously, unlocking new dimensions in momentum and volatility analysis.

Key Features

Screen up to 8 crypto symbols across 4 different timeframes in one pane

TTM Squeeze indicator detects volatility contraction and expansion (“squeeze”) phases

Momentum filter reveals potential breakout direction and strength

Visual screener table for intuitive multi-asset monitoring

Fully customizable for symbols and timeframes

How It Works

The heart of this screener is the TTM Squeeze algorithm—a hybrid volatility and momentum indicator leveraging Bollinger Bands, Keltner Channels, and linear momentum analysis. The script checks whether Bollinger Bands are “squeezed” inside Keltner Channels, flagging periods of low volatility primed for expansion. Once a squeeze is released, the included momentum calculation suggests the likely breakout direction.

For each selected symbol and timeframe, the screener runs the TTM Squeeze logic, outputs “SQUEEZE” or “NO SQZ”, and tags momentum values. A table layout organizes the results, allowing rapid pattern recognition across symbols.

Trading Ideas and Insights

Spot multi-symbol volatility clusters—ideal for finding synchronized market moves

Assess breakout potential and direction before entering trades

Scalping and swing trading decisions are enhanced by cross-timeframe momentum filtering

Portfolio managers can quickly identify which assets are about to move

How Multiple Indicators Work Together

This screener unites three essential concepts:

Bollinger Bands : Measure volatility using standard deviation of price

Keltner Channels : Define expected price range based on average true range (ATR)

Momentum : Linear regression calculation to evaluate the direction and intensity after a squeeze

By combining these, the indicator not only signals when volatility compresses and releases, but also adds directional context—filtering false signals and helping traders time entries and exits more precisely.

Unique Aspects

Multi-symbol, multi-timeframe architecture—optimized for crypto traders and market scanners

Advanced table visualization—see all signals at a glance, minimizing cognitive overload

Modular calculation functions—easy to adapt and extend for other asset classes or strategies

Real-time, low-latency screening—built for actionable alerts on fast-moving markets

How to Use

Add the script to a TradingView chart (works on custom layouts)

Select up to 8 symbols and 4 timeframes using input fields (defaults to BTCUSD, ETHUSD, etc.)

Monitor the screener table; “SQUEEZE” highlights assets in potential breakout phase

Use momentum values to judge if the squeeze is likely bullish or bearish

Combine screener insights with manual chart analysis for optimal results

Customization

Symbols: Easily set any ticker for deep market scanning

Timeframes: Adjust to match your trading horizon (scalping, swing, long-term)

Indicator parameters: Refine Bollinger/Keltner/Momentum settings for sensitivity

Visuals: Personalize table layout, color codes, and formatting for clarity

Conclusion

In summary, the TTM Squeeze Screener is a robust, original TradingView indicator designed for crypto traders who demand a sophisticated multi-symbol, multi-timeframe edge. Its combination of volatility and momentum analytics makes it ideal for catching explosive breakouts, managing risk, and scanning the market efficiently. Whether you’re a scalper or swing trader, this screener provides the insights needed to stay ahead of the curve.

MACD Forecast [Titans_Invest]MACD Forecast — The Future of MACD in Trading

The MACD has always been one of the most powerful tools in technical analysis.

But what if you could see where it’s going, instead of just reacting to what has already happened?

Introducing MACD Forecast — the natural evolution of the MACD Full , now taken to the next level. It’s the world’s first MACD designed not only to analyze the present but also to predict the future behavior of momentum.

By combining the classic MACD structure with projections powered by Linear Regression, this indicator gives traders an anticipatory, predictive view, redefining what’s possible in technical analysis.

Forget lagging indicators.

This is the smartest, most advanced, and most accurate MACD ever created.

🍟 WHY MACD FORECAST IS REVOLUTIONARY

Unlike the traditional MACD, which only reflects current and past price dynamics, the MACD Forecast uses regression-based projection models to anticipate where the MACD line, signal line, and histogram are heading.

This means traders can:

• See MACD crossovers before they happen.

• Spot trend reversals earlier than most.

• Gain an unprecedented timing advantage in both discretionary and automated trading.

In other words: this indicator lets you trade ahead of time.

🔮 FORECAST ENGINE — POWERED BY LINEAR REGRESSION

At its core, the MACD Forecast integrates Linear Regression (ta.linreg) to project the MACD’s future behavior with exceptional accuracy.

Projection Modes:

• Flat Projection: Assumes trend continuity at the current level.

• LinReg Projection: Applies linear regression across N periods to mathematically forecast momentum shifts.

This dual system offers both a conservative and adaptive view of market direction.

📐 ACCURACY WITH FULL CUSTOMIZATION

Just like the MACD Full, this new version comes with 20 customizable buy-entry conditions and 20 sell-entry conditions — now enhanced with forecast-based rules that anticipate crossovers and trend reversals.

You’re not just reacting — you’re strategizing ahead of time.

⯁ HOW TO USE MACD FORECAST❓

The MACD Forecast is built on the same foundation as the classic MACD, but with predictive capabilities.

Step 1 — Spot Predicted Crossovers:

Watch for forecasted bullish or bearish crossovers. These signals anticipate when the MACD line will cross the signal line in the future, letting you prepare trades before the move.

Step 2 — Confirm with Histogram Projection:

Use the projected histogram to validate momentum direction. A rising histogram signals strengthening bullish momentum, while a falling projection points to weakening or bearish conditions.

Step 3 — Combine with Multi-Timeframe Analysis:

Use forecasts across multiple timeframes to confirm signal strength (e.g., a 1h forecast aligned with a 4h forecast).

Step 4 — Set Entry Conditions & Automation:

Customize your buy/sell rules with the 20 forecast-based conditions and enable automation for bots or alerts.

Step 5 — Trade Ahead of the Market:

By preparing for future momentum shifts instead of reacting to the past, you’ll always stay one step ahead of lagging traders.

🤖 BUILT FOR AUTOMATION AND BOTS 🤖

Whether for manual trading, quantitative strategies, or advanced algorithms, the MACD Forecast was designed to integrate seamlessly with automated systems.

With predictive logic at its core, your strategies can finally react to what’s coming, not just what already happened.

🥇 WHY THIS INDICATOR IS UNIQUE 🥇

• World’s first MACD with Linear Regression Forecasting

• Predictive Crossovers (before they appear on the chart)

• Maximum flexibility with Long & Short combinations — 20+ fully configurable conditions for tailor-made strategies

• Fully automatable for quantitative systems and advanced bots

This isn’t just an update.

It’s the final evolution of the MACD.

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 MACD > Signal Smoothing

🔹 MACD < Signal Smoothing

🔹 Histogram > 0

🔹 Histogram < 0

🔹 Histogram Positive

🔹 Histogram Negative

🔹 MACD > 0

🔹 MACD < 0

🔹 Signal > 0

🔹 Signal < 0

🔹 MACD > Histogram

🔹 MACD < Histogram

🔹 Signal > Histogram

🔹 Signal < Histogram

🔹 MACD (Crossover) Signal

🔹 MACD (Crossunder) Signal

🔹 MACD (Crossover) 0

🔹 MACD (Crossunder) 0

🔹 Signal (Crossover) 0

🔹 Signal (Crossunder) 0

🔮 MACD (Crossover) Signal Forecast

🔮 MACD (Crossunder) Signal Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 MACD > Signal Smoothing

🔸 MACD < Signal Smoothing

🔸 Histogram > 0

🔸 Histogram < 0

🔸 Histogram Positive

🔸 Histogram Negative

🔸 MACD > 0

🔸 MACD < 0

🔸 Signal > 0

🔸 Signal < 0

🔸 MACD > Histogram

🔸 MACD < Histogram

🔸 Signal > Histogram

🔸 Signal < Histogram

🔸 MACD (Crossover) Signal

🔸 MACD (Crossunder) Signal

🔸 MACD (Crossover) 0

🔸 MACD (Crossunder) 0

🔸 Signal (Crossover) 0

🔸 Signal (Crossunder) 0

🔮 MACD (Crossover) Signal Forecast

🔮 MACD (Crossunder) Signal Forecast

______________________________________________________

______________________________________________________

🔮 Linear Regression Function 🔮

______________________________________________________

• Our indicator includes MACD forecasts powered by linear regression.

Forecast Types:

• Flat: Assumes prices will stay the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset : Offset.

• return: Linear regression curve.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : MACD Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

🎗️ In memory of João Guilherme — your light will live on forever.

CMC Macro Regime PanelOverview (what it is):

A macro‑regime gate built entirely from TradingView-native symbols (CRYPTOCAP, FRED, DXY/VIX, HYG/LQD). It aggregates central‑bank liquidity (Fed balance sheet − RRP − Treasury General Account), USD strength, credit conditions, stablecoin flows/dominance, tech beta and BTC–NDX co‑move into one normalized score (CLRC). The panel outputs Risk‑ON/OFF regimes, an Early 3/5 pre‑signal, and an automatic BTC vs ETH vs ALTs preference. It is intentionally scoped to Daily & Weekly reads (no intraday timing). Publish with a clean chart and a clear description as per TradingView rules.

TradingView

Why we also use other TradingView screens (and why that is compliant)

This script pulls data via request.security() from official TV symbols only; users often want to open the raw series on separate charts to sanity‑check:

CRYPTOCAP indices: TOTAL, TOTAL2, TOTAL3 (market cap aggregates) and dominance tickers like BTC.D, USDT.D. Helpful for regime & rotation (ALTs vs BTC). TradingView provides definitions for crypto market cap and dominance symbols.

TradingView

+3

TradingView

+3

TradingView

+3

FRED releases: WALCL (Fed assets, weekly), RRPONTSYD (ON RRP, daily), WTREGEN (TGA, weekly), M2SL (M2, monthly). These are the official macro sources exposed on TV.

FRED

+3

FRED

+3

FRED

+3

Risk proxies: TVC:DXY (USD index), TVC:VIX (implied vol), AMEX:HYG/AMEX:LQD (credit), NASDAQ:NDX (tech beta), BINANCE:ETHBTC. VIX/NDX relationship is well-documented; VIX measures 30‑day expected S&P500 vol.

TradingView

+2

TradingView

+2

Compliance note: Using multiple screens is optional for users, but it explains/justifies how components work together (a requirement for public scripts). Keep publication chart clean; use extra screens only to illustrate in the description.

TradingView

How it works (high level)

Liquidity block (Weekly/Monthly)

Net Liquidity = WALCL − RRPONTSYD − WTREGEN (YoY z‑score). WALCL is weekly (as of Wednesday) via H.4.1; RRP is daily; TGA is a Fed liability series. M2 YoY is monthly.

FRED

+3

FRED

+3

FRED

+3

Risk conditions (Daily)

DXY 3‑month momentum (inverted), VIX level (inverted), Credit (HYG/LQD ratio or HY OAS). VIX is a 30‑day constant‑maturity implied vol index per Cboe methodology.

Cboe

+1

Crypto‑internal (Daily)

Stablecoins (USDT+USDC+DAI 30‑day log change), USDT dominance (20‑day, inverted), TOTAL3 (63‑day momentum). Dominance symbols on TV follow a documented formula.

TradingView

Beta & co‑move (Daily)

NDX 63‑day momentum, BTC↔NDX 90‑day correlation.

All components become z‑scores (optionally clipped), weighted, missing inputs drop and weights renormalize. We never use lookahead; we confirm on bar close to avoid repainting per Pine docs (barstate.isconfirmed, multi‑TF).

TradingView

+2

TradingView

+2

What you see on the chart

White line (CLRC) = macro regime score.

Background: Green = Risk‑ON, Red = Risk‑OFF, Teal = Early 3/5 (pre‑signal).

Table: shows each component’s z‑score and the Preference: BTC / ETH / ALTs / Mixed.

Signals & interpretation

Designed for Daily (1D) and Weekly (1W) only.

Regime gates (default Fast preset):

Enter ON: CLRC ≥ +0.8; Hold ON while ≥ +0.5.

Enter OFF: CLRC ≤ −1.0; Hold OFF while ≤ −0.5.

0 / ±1 reading: CLRC is a standardized composite.

~0 = neutral baseline (no macro edge).

≥ +1 = strong macro tailwind (≈ +1σ).

≤ −1 = strong headwind (≈ −1σ).

Early 3/5 (teal): a fast pre‑signal when at least 3 of 5 daily checks align: USDT.D↓, DXY↓, VIX↓, HYG/LQD↑, ETHBTC↑ or TOTAL3↑. It often precedes a full ON flip—use for pre‑positioning rather than full sizing.

BTC/ETH/ALTs selector (only when ON):

ALTs when BTC.D↓ and (ETHBTC↑ or TOTAL3↑) ⇒ rotate down the risk curve.

BTC when BTC.D↑ and ETHBTC↓ ⇒ keep it concentrated.

ETH when ETHBTC↑ while BTC.D flat/up ⇒ add ETH beta.

(Dominance mechanics are documented by TV.)

TradingView

Dissonance (incompatibility) rules — when to stand down

Use these overrides to avoid false comfort:

CLRC > +1 but USDT.D↑ and/or VIX spikes day‑over‑day → downgrade to Neutral; wait for USDT.D to stabilize and VIX to cool (VIX is a fear gauge of 30‑day expectation).

Cboe Global Markets

CLRC > +1 but DXY↑ sharply (USD squeeze) → size below normal; require DXY momentum to roll over.

CLRC < −1 but Early 3/5 = true two days in a row → start reducing underweights; look for ON flip within a few bars.

NetLiq improving (W) but credit (HYG/LQD) deteriorating (D) → treat as mixed regime; prefer BTC over ALTs.

How to use (step‑by‑step)

A. Read on Daily (1D) — main regime

Open CRYPTOCAP:TOTAL3, 1D (panel applied).

Wait for bar close (use alerts on confirmed bar). Pine docs recommend barstate.isconfirmed to avoid repainting on realtime bars.

TradingView

If ON, check Preference (BTC / ETH / ALTs).

Then drop to 4H on your trading pair for micro entries (this indicator itself is not for intraday timing).

B. Confirm weekly macro (1W) — once per week)

Review WALCL/RRP/TGA after the H.4.1 release on Thursdays ~4:30 pm ET. WALCL is “Weekly, as of Wednesday”; M2 is Monthly—so do not expect daily responsiveness from these.

Federal Reserve

+2

FRED

+2

Recommended check times (practical schedule)

Daily regime read: right after your chart’s daily close (confirmed bar). For consistent timing across crypto, many users set chart timezone to UTC and read ~00:05 UTC; you can change chart timezone in TV’s settings.

TradingView

In‑day monitoring: optional spot checks 16:00 & 20:00 UTC (DXY/VIX move during US hours), but act only after the daily bar confirms.

Weekly macro pass: Thu 21:30–22:30 UTC (after H.4.1 4:30 pm ET) or Fri after daily close, to let weekly FRED series propagate.

Federal Reserve

Limitations & data latency (be explicit)

Higher‑TF data & confirmation: FRED weekly/monthly series will not reflect intraday risk in crypto; we aggregate them for regime, not for entry timing.

Repainting 101: Realtime bars move until close. This script does not use lookahead and follows Pine guidance on multi‑TF series; still, always act on confirmed bars.

TradingView

+1

Public‑library compliance: Title EN‑only; description starts in EN; clean chart; justify component mash‑up; no lookahead; no unrealistic claims.

TradingView

Alerts you can use

“Macro Risk‑ON (entry)” — fires on ON flip (confirmed bar).

“Macro Risk‑OFF (entry)” — fires on OFF flip.

“Early 3/5” — fires when the teal pre‑signal appears (not a regime flip).

“Preference change” — BTC/ETH/ALTs toggles while ON.

Publish note: Alerts are fine; just avoid implying guaranteed accuracy/performance.

TradingView

Background research (why these inputs matter)

Liquidity → Crypto: Fed H.4.1 timing and series definitions (WALCL, RRP, TGA) formalize the “net liquidity” concept used here.

FRED

+3

Federal Reserve

+3

FRED

+3

Stablecoins ↔ Non‑stable crypto: empirical work shows bi‑directional causality between stablecoin market cap and non‑stable crypto cap; stablecoin growth co‑moves with broader crypto activity.

Global liquidity link: world liquidity positively relates to total crypto market cap; lagged effects are observed at monthly horizons.

VIX/Uncertainty effect: fear shocks impair BTC’s “safe haven” behavior; VIX is a meaningful risk‑off read.

RSI MA Cross + Divergence Signal (V2) Core Logic

RSI + Moving Average

The script calculates a standard RSI (default 14).

It then overlays a moving average (SMA/EMA/WMA, default 9).

When RSI crosses above its MA → bullish momentum.

When RSI crosses below its MA → bearish momentum.

Divergence Filter

Signals are only valid if there’s confirmed divergence:

Bullish divergence: Price makes a lower low, RSI makes a higher low.

Bearish divergence: Price makes a higher high, RSI makes a lower high.

Overbought / Oversold Filter

Optional extra:

Bullish signals only valid if RSI ≤ 30 (oversold).

Bearish signals only valid if RSI ≥ 70 (overbought).

This ensures signals happen in “stretched” conditions.

Risk & Trade Management

Entries taken only when all conditions align.

Exits can be managed with ATR stops, partial take-profits, breakeven moves, and trailing stops (we coded these in the strategy version).

Cooldown, session filters, and daily loss guard to keep risk tight.

🔹 Strengths

✅ High selectivity: Combining RSI cross + divergence + OB/OS means signals are rare but higher quality.

✅ Great at catching reversals: Divergence highlights where price may be running out of steam.

✅ Risk management baked in: ATR stops + partial exits smooth out equity curve.

✅ Works across markets: ES, FX, crypto — anywhere RSI divergences are respected.

✅ Flexible: You can loosen/tighten filters depending on aggressiveness.

🔹 Weaknesses

❌ Lag from pivots: Divergence only confirms after a few bars → you enter late sometimes.

❌ Choppy in ranges: In sideways markets, RSI divergences appear often and whipsaw.

❌ Filters reduce signals: With all filters ON (divergence + OB/OS + trend + session), signals can be very rare — may under-trade.

❌ Not standalone: Needs higher-timeframe context (trend, liquidity pools) to avoid counter-trend entries.

🔹 Best Ways to Trade It

Use Higher Timeframe Bias

Run the strategy on 15m/1H, but only trade in direction of higher timeframe trend (e.g., 4H EMA).

Example: If daily is bullish → only take bullish divergences.

Pair With Structure

Look for signals at key zones: HTF support/resistance, VWAP, or FVGs.

Divergence + RSI cross inside an FVG is a strong entry trigger.

Adjust OB/OS for Volatility

For crypto/FX: use 35/65 instead of 30/70 (markets trend harder).

For ES/S&P: 30/70 works fine.

Risk Management Is King

Use partial exits: take profit at 1R, trail rest.

Size by % of equity (we coded this into the strategy).

Avoid News Spikes

Divergences break down around CPI, NFP, Fed announcements — stay flat.

🔹 When It Shines

Trending markets that make extended pushes → clean divergences.

Reversal zones (oversold → bullish bounce, overbought → bearish fade).

Swing trading (15m–4H) — less noise than 1m/5m scalping.

🔹 When to Avoid

Low volatility chop → lots of false divergences.

During high-impact news → RSI swings wildly.

In strong one-way trends without pullbacks — divergence keeps calling tops/bottoms too early.

✅ Summary:

This is a reversal-focused RSI divergence strategy with strict filters. It’s powerful when combined with higher-timeframe bias + structure confluence, but weak if traded blindly in choppy or news-driven conditions. Best to treat it as a precision entry trigger, not a full system — layer it on top of your FVG/ORB framework for maximum edge.

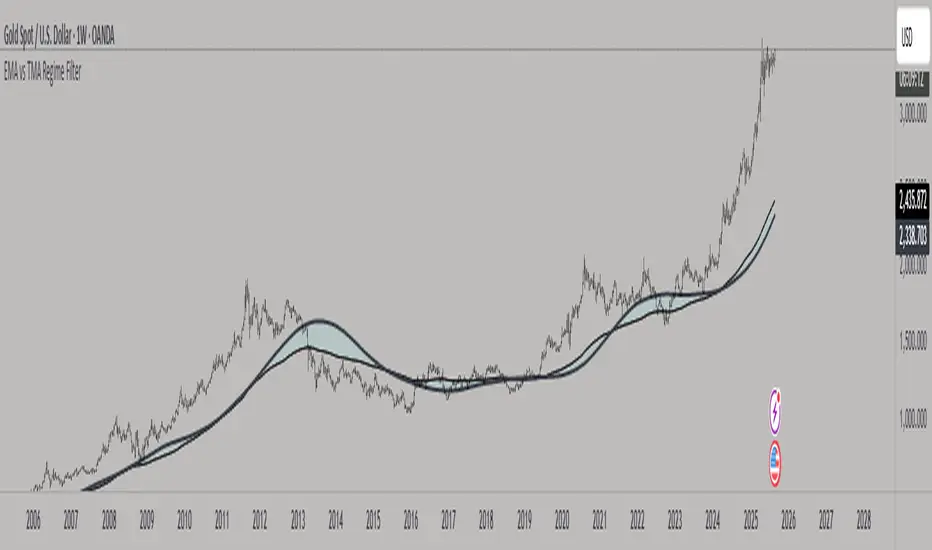

EMA vs TMA Regime FilterEMA vs TMA Regime Filter

This indicator is built as a visual study tool to compare the behavior of the Exponential Moving Average (EMA) and the Triangular Moving Average (TMA).

The EMA applies an exponential weighting to price data, giving stronger importance to the most recent values. This makes it a faster, more responsive line that reflects short-term momentum. The TMA, by contrast, applies a double-smoothing process (or in the “True TMA” option, a split SMA sequence), which produces a much slower curve. The TMA emphasizes balance over reactivity, often used for filtering noise and observing longer-term structure.

When both are plotted on the same chart, their differences become clear. The shaded region between them highlights times when short-term price dynamics diverge from longer-term smoothing. This is where the idea of “regime” comes in — not as a trading signal, but as a descriptive way of seeing whether market action is currently dominated by speed or by stability.

Users can customize:

Line styles, widths, and colors.

Cloud transparency for visual clarity.

Whether to color bars based on relative position (optional, purely visual).

The goal is not to create a system, but to help traders experiment, observe, and learn how different smoothing techniques can emphasize different aspects of price. By switching between the legacy and true TMA, or adjusting lengths, users can study how each approach interprets the same data differently.

Adaptive Valuation [BackQuant]Adaptive Valuation

What this is

A composite, zero-centered oscillator that standardizes several classic indicators and blends them into one “valuation” line. It computes RSI, CCI, Demarker, and the Price Zone Oscillator, converts each to a rolling z-score, then forms a weighted average. Optional smoothing, dynamic overbought and oversold bands, and an on-chart table make the inputs and the final score easy to inspect.

How it works

Components

• RSI with its own lookback.

• CCI with its own lookback.

• DM (Demarker) with its own lookback.

• PZO (Price Zone Oscillator) with its own lookback.

Standardization via z-score

Each component is transformed using a rolling z-score over lookback bars:

z = (value − mean) ÷ stdev , where the mean is an EMA and the stdev is rolling.

This puts all inputs on a comparable scale measured in standard deviations.

Weighted blend

The z-scores are combined with user weights w_rsi, w_cci, w_dm, w_pzo to produce a single valuation series. If desired, it is then smoothed with a selected moving average (SMA, EMA, WMA, HMA, RMA, DEMA, TEMA, LINREG, ALMA, T3). ALMA’s sigma input shapes its curve.

Dynamic thresholds (optional)

Two ways to set overbought and oversold:

• Static : fixed levels at ob_thres and os_thres .

• Dynamic : ±k·σ bands, where σ is the rolling standard deviation of the valuation over dynLen .

Bands can be centered at zero or around the valuation’s rolling mean ( centerZero ).

Visualization and UI

• Zero line at 0 with gradient fill that darkens as the valuation moves away from 0.

• Optional plotting of band lines and background highlights when OB or OS is active.

• Optional candle and background coloring driven by the valuation.

• Summary table showing each component’s current z-score, the final score, and a compact status.

How it can be used

• Bias filter : treat crosses above 0 as bullish bias and below 0 as bearish bias.

• Mean-reversion context : look for exhaustion when the valuation enters the OB or OS region, then watch for exits from those regions or a return toward 0.

• Signal confirmation : use the final score to confirm setups from structure or price action.

• Adaptive banding : with dynamic thresholds, OB and OS adjust to prevailing variability rather than relying on fixed lines.

• Component tuning : change weights to emphasize trend (raise DM, reduce RSI/CCI) or range behavior (raise RSI/CCI, reduce DM). PZO can help in swing environments.

Why z-score blending helps

Indicators often live on different scales. Z-scoring places them on a common, unitless axis, so a one-sigma move in RSI has comparable influence to a one-sigma move in CCI. This reduces scale bias and allows transparent weighting. It also facilitates regime-aware thresholds because the dynamic bands scale with recent dispersion.

Inputs to know

• Component lookbacks : rsilb, ccilb, dmlb, pzolb control each raw signal.

• Standardization window : lookback sets the z-score memory. Longer smooths, shorter reacts.

• Weights : w_rsi, w_cci, w_dm, w_pzo determine each component’s influence.

• Smoothing : maType, smoothP, sig govern optional post-blend smoothing.

• Dynamic bands : dyn_thres, dynLen, thres_k, centerZero configure the adaptive OB/OS logic.

• UI : toggle the plot, table, candle coloring, and threshold lines.

Reading the plot

• Above 0 : composite pressure is positive.

• Below 0 : composite pressure is negative.

• OB region : valuation above the chosen OB line. Risk of mean reversion rises and momentum continuation needs evidence.

• OS region : mirror logic on the downside.

• Band exits : leaving OB or OS can serve as a normalization cue.

Strengths

• Normalizes heterogeneous signals into one interpretable series.

• Adjustable component weights to match instrument behavior.

• Dynamic thresholds adapt to changing volatility and drift.

• Transparent diagnostics from the on-chart table.

• Flexible smoothing choices, including ALMA and T3.

Limitations and cautions

• Z-scores assume a reasonably stationary window. Sharp regime shifts can make recent bands unrepresentative.

• Highly correlated components can overweight the same effect. Consider adjusting weights to avoid double counting.

• More smoothing adds lag. Less smoothing adds noise.

• Dynamic bands recalibrate with dynLen ; if set too short, bands may swing excessively. If too long, bands can be slow to adapt.

Practical tuning tips

• Trending symbols: increase w_dm , use a modest smoother like EMA or T3, and use centerZero dynamic bands.

• Choppy symbols: increase w_rsi and w_cci , consider ALMA with a higher sigma , and widen bands with a larger thres_k .

• Multiday swing charts: lengthen lookback and dynLen to stabilize the scale.

• Lower timeframes: shorten component lookbacks slightly and reduce smoothing to keep signals timely.

Alerts

• Enter and exit of Overbought and Oversold, based on the active band choice.

• Bullish and bearish zero crosses.

Use alerts as prompts to review context rather than as stand-alone trade commands.

Final Remarks

We created this to show people a different way of making indicators & trading.

You can process normal indicators in multiple ways to enhance or change the signal, especially with this you can utilise machine learning to optimise the weights, then trade accordingly.

All of the different components were selected to give some sort of signal, its made out of simple components yet is effective. As long as the user calibrates it to their Trading/ investing style you can find good results. Do not use anything standalone, ensure you are backtesting and creating a proper system.

BPS Multi-MA 5 — 22/30, SMA/WMA/EMA# Multi-MA 5 — 22/30 base, SMA/WMA/EMA

**What it is**

A lightweight 5-line moving-average ribbon for fast visual bias and trend/mean-reversion reads. You can switch the MA type (SMA/WMA/EMA) and choose between two ways of setting lengths: by monthly “session-based” base (22 or 30) with multipliers, or by entering exact lengths manually. An optional info table shows the effective settings in real time.

---

## How it works

* Calculates five moving averages from the selected price source.

* Lengths are either:

* **Multipliers mode:** `Base × Multiplier` (e.g., base 22 → 22/44/66/88/110), or

* **Manual mode:** any five exact lengths (e.g., 10/22/50/100/200).

* Plots five lines with fixed legend titles (MA1…MA5); the **info table** displays the actual type and lengths.

---

## Inputs

**Length Mode**

* **Multipliers** — choose a **Base** of **22** (≈ trading sessions per month) or **30** (calendar-style, smoother) and set **×1…×5** multipliers.

* **Manual** — enter **Len1…Len5** directly.

**MA Settings**

* **MA Type:** SMA / WMA / EMA

* **Source:** any series (e.g., `close`, `hlc3`, etc.)

* **Use true close (ignore Heikin Ashi):** when enabled, the MA is computed from the underlying instrument’s real `close`, not HA candles.

* **Show info table:** toggles the on-chart table with the current mode, type, base, and lengths.

---

## Quick start

1. Add the indicator to your chart.

2. Pick **MA Type** (e.g., **WMA** for faster response, **SMA** for smoother).

3. Choose **Length Mode**:

* **Multipliers:** set **Base = 22** for session-based monthly lengths (stocks/FX), or **30** for heavier smoothing.

* **Manual:** enter your exact lengths (e.g., 10/22/50/100/200).

4. (Optional) On **Heikin Ashi** charts, enable **Use true close** if you want the lines based on the instrument’s real close.

---

## Tips & notes

* **1 month ≈ 21–22 sessions.** Using 30 as “monthly” yields a smoother, more delayed curve.

* **WMA** reacts faster than **SMA** at the same length; expect earlier signals but more whipsaws in chop.

* **Len = 1** makes the MA track the chosen source (e.g., `close`) almost exactly.

* If changing lengths doesn’t move the lines, ensure you’re editing fields for the **active Length Mode** (Multipliers vs Manual).

* For clean comparisons, use the **same timeframe**. If you later wrap this in MTF logic, keep `lookahead_off` and handle gaps appropriately.

---

## Use cases

* Trend ribbon and dynamic bias zones

* Pullback entries to the mid/slow lines

* Crossovers (fast vs slow) for confirmation

* Volatility filtering by spreading lengths (e.g., 22/44/88/132/176)

---

**Credits:** Built for clarity and speed; designed around session-based “monthly” lengths (22) or smoother calendar-style (30).

Machine Learning BBPct [BackQuant]Machine Learning BBPct

What this is (in one line)

A Bollinger Band %B oscillator enhanced with a simplified K-Nearest Neighbors (KNN) pattern matcher. The model compares today’s context (volatility, momentum, volume, and position inside the bands) to similar situations in recent history and blends that historical consensus back into the raw %B to reduce noise and improve context awareness. It is informational and diagnostic—designed to describe market state, not to sell a trading system.

Background: %B in plain terms

Bollinger %B measures where price sits inside its dynamic envelope: 0 at the lower band, 1 at the upper band, ~ 0.5 near the basis (the moving average). Readings toward 1 indicate pressure near the envelope’s upper edge (often strength or stretch), while readings toward 0 indicate pressure near the lower edge (often weakness or stretch). Because bands adapt to volatility, %B is naturally comparable across regimes.

Why add (simplified) KNN?

Classic %B is reactive and can be whippy in fast regimes. The simplified KNN layer builds a “nearest-neighbor memory” of recent market states and asks: “When the market looked like this before, where did %B tend to be next bar?” It then blends that estimate with the current %B. Key ideas:

• Feature vector . Each bar is summarized by up to five normalized features:

– %B itself (normalized)

– Band width (volatility proxy)

– Price momentum (ROC)

– Volume momentum (ROC of volume)

– Price position within the bands

• Distance metric . Euclidean distance ranks the most similar recent bars.

• Prediction . Average the neighbors’ prior %B (lagged to avoid lookahead), inverse-weighted by distance.

• Blend . Linearly combine raw %B and KNN-predicted %B with a configurable weight; optional filtering then adapts to confidence.

This remains “simplified” KNN: no training/validation split, no KD-trees, no scaling beyond windowed min-max, and no probabilistic calibration.