ATR Movement Percentage from Daily (Bal)Script Description: ATR Movement Percentage from Daily

The script titled "ATR Movement Percentage from Daily" is designed to help traders analyze the price movement of an asset in relation to its daily volatility, as represented by the Average True Range (ATR). Here's a breakdown of how the script works:

Key Features of the Script:

ATR Calculation:

The script allows the user to input the length of the ATR calculation (default is 14 periods).

It retrieves the daily ATR value using the request.security function, ensuring that the ATR is based on the daily timeframe, regardless of the current chart's timeframe.

Price Movement Calculation:

It calculates the opening price of the current day using request.security to ensure it is aligned with the daily timeframe.

It retrieves the current closing price and computes the price change from the opening price.

Movement Percentage:

The percentage of price movement relative to the daily ATR is calculated. This value helps traders understand how significant the current price movement is compared to the expected volatility for the day.

Direction of Movement:

The script determines the direction of the price movement (upward or downward) based on whether the price change is positive or negative.

Dynamic Label Display:

A label is created and updated to show the movement percentage and direction on the chart.

If the price movement is upward, the label is displayed in green; if downward, it is shown in red.

The label position updates with each new bar, keeping it relevant to the current price action.

Plotting Daily ATR:

The daily ATR value is plotted on the chart as a blue line, providing a visual reference for traders to see the volatility levels in relation to price movements.

Conclusion:

This script is particularly useful for traders who want to assess market conditions based on volatility. By understanding how much the price has moved in relation to the daily ATR, traders can make informed decisions about entry and exit points, and adjust their risk management strategies accordingly. The dynamic labeling feature enhances the usability of the script, allowing for quick visual assessments of market behavior.

Recherche dans les scripts pour "the script"

Set Alarm for Closed Codes [Mr_Rakun]Set Alarm for Closed Codes

This Pine Script code is designed to set up alerts based on two types of conditions: Crossover or Greater-Lesser thresholds. The script's most significant feature is its ability to set alerts using external sources that the user defines for long and short positions. These sources can be any other indicator or value on the chart, giving traders maximum flexibility in choosing their alert triggers.

Crossover Condition: The script triggers an alert when the closing price crosses above or below the user-defined external sources for long and short signals.

Greater-Lesser Condition: It also allows triggering alerts when the defined input values (like 70 for greater, 30 for lesser) are crossed by the external sources.

Users can input the message for buy and sell signals (such as "BUY" or "SELL") and set custom thresholds to create more flexible alerts based on market behavior. The code also visually plots the user-selected entry sources on the chart, with the short entry source being displayed in red for easier identification.

In summary, the key feature of this script is its ability to set alerts based on external sources defined by the user, making it highly versatile for traders who want to automate alerts for specific price movements or indicator-based conditions.

--------------------------------------------------

Türkçe Açıklama

Bu Pine Script kodu, iki farklı koşula dayalı olarak alarm kurmayı amaçlar: Kesişim veya Büyük-Küçük eşikleri. Kodun en önemli özelliği, uzun ve kısa pozisyonlar için kullanıcı tarafından tanımlanan dış kaynaklar kullanılarak alarm kurulabilmesidir. Bu kaynaklar, grafikteki herhangi bir gösterge veya değer olabilir, bu da yatırımcılara alarm tetikleyicilerini seçmede maksimum esneklik sağlar.

Kesişim Koşulu: Kapanış fiyatı, kullanıcı tarafından tanımlanan dış kaynakları geçtiğinde uzun veya kısa sinyaller için alarm tetiklenir.

Büyük-Küçük Koşulu: Ayrıca, belirlenen giriş değerlerinin (örneğin, büyük için 70, küçük için 30) dış kaynaklarla kesişmesi durumunda alarm tetiklenir.

Kullanıcılar, alış ve satış sinyalleri için mesajlar (örneğin, "AL" veya "SAT") girebilir ve piyasa hareketlerine dayalı olarak daha esnek alarmlar oluşturmak için özel eşikler belirleyebilir. Kod, ayrıca grafik üzerinde kullanıcı tarafından seçilen giriş kaynaklarını da çizer; kısa giriş kaynağı kırmızı renkte gösterilir, böylece kolayca tanımlanabilir.

Özetle, bu scriptin ana özelliği, kullanıcı tarafından tanımlanan dış kaynaklara dayalı alarm kurabilme yeteneği olup, belirli fiyat hareketleri veya gösterge tabanlı koşullar için alarm kurmak isteyen yatırımcılar için oldukça esnektir.

ATR Bands with ATR Cross + InfoTableOverview

This Pine Script™ indicator is designed to enhance traders' ability to analyze market volatility, trend direction, and position sizing directly on their TradingView charts. By plotting Average True Range (ATR) bands anchored at the OHLC4 price, displaying crossover labels, and providing a comprehensive information table, this tool offers a multifaceted approach to technical analysis.

Key Features:

ATR Bands Anchored at OHLC4: Visual representation of short-term and long-term volatility bands centered around the average price.

OHLC4 Dotted Line: A dotted line representing the average of Open, High, Low, and Close prices.

ATR Cross Labels: Visual cues indicating when short-term volatility exceeds long-term volatility and vice versa.

Information Table: Displays real-time data on market volatility, calculated position size based on risk parameters, and trend direction relative to the 20-period Smoothed Moving Average (SMMA).

Purpose

The primary purpose of this indicator is to:

Assess Market Volatility: By comparing short-term and long-term ATR values, traders can gauge the current volatility environment.

Determine Optimal Position Sizing: A calculated position size based on user-defined risk parameters helps in effective risk management.

Identify Trend Direction: Comparing the current price to the 20-period SMMA assists in determining the prevailing market trend.

Enhance Decision-Making: Visual cues and real-time data enable traders to make informed trading decisions with greater confidence.

How It Works

1. ATR Bands Anchored at OHLC4

Average True Range (ATR) Calculations

Short-Term ATR (SA): Calculated over a 9-period using ta.atr(9).

Long-Term ATR (LA): Calculated over a 21-period using ta.atr(21).

Plotting the Bands

OHLC4 Dotted Line: Plotted using small circles to simulate a dotted line due to Pine Script limitations.

ATR(9) Bands: Plotted in blue with semi-transparent shading.

ATR(21) Bands: Plotted in orange with semi-transparent shading.

Overlap: Bands can overlap, providing visual insights into changes in volatility.

2. ATR Cross Labels

Crossover Detection:

SA > LA: Indicates increasing short-term volatility.

Detected using ta.crossover(SA, LA).

A green upward label "SA>LA" is plotted below the bar.

SA < LA: Indicates decreasing short-term volatility.

Detected using ta.crossunder(SA, LA).

A red downward label "SA LA, then the market is considered volatile.

Display: Shows "Yes" or "No" based on the comparison.

b. Position Size Calculation

Risk Total Amount: User-defined input representing the total capital at risk.

Risk per 1 Stock: User-defined input representing the risk associated with one unit of the asset.

Purpose: Helps traders determine the appropriate position size based on their risk tolerance and current market volatility.

c. Is Price > 20 SMMA?

SMMA Calculation:

Calculated using a 20-period Smoothed Moving Average with ta.rma(close, 20).

Logic: If the current close price is above the SMMA, the trend is considered upward.

Display: Shows "Yes" or "No" based on the comparison.

How to Use

Step 1: Add the Indicator to Your Chart

Copy the Script: Copy the entire Pine Script code into the TradingView Pine Editor.

Save and Apply: Save the script and click "Add to Chart."

Step 2: Configure Inputs

Risk Parameters: Adjust the "Risk Total Amount" and "Risk per 1 Stock" in the indicator settings to match your personal risk management strategy.

Step 3: Interpret the Visuals

ATR Bands

Width of Bands: Wider bands indicate higher volatility; narrower bands indicate lower volatility.

Band Overlap: Pay attention to areas where the blue and orange bands diverge or converge.

OHLC4 Dotted Line

Serves as a central reference point for the ATR bands.

Helps visualize the average price around which volatility is measured.

ATR Cross Labels

"SA>LA" Label:

Indicates short-term volatility is increasing relative to long-term volatility.

May signal potential breakout or trend acceleration.

"SA 20 SMMA?

Use this to confirm trend direction before entering or exiting trades.

Practical Example

Imagine you are analyzing a stock and notice the following:

ATR(9) Crosses Above ATR(21):

A green "SA>LA" label appears.

The info table shows "Yes" for "Is ATR-based price volatile."

Position Size:

Based on your risk parameters, the position size is calculated.

Price Above 20 SMMA:

The info table shows "Yes" for "Is price > 20 SMMA."

Interpretation:

The market is experiencing increasing short-term volatility.

The trend is upward, as the price is above the 20 SMMA.

You may consider entering a long position, using the calculated position size to manage risk.

Customization

Colors and Transparency:

Adjust the colors of the bands and labels to suit your preferences.

Risk Parameters:

Modify the default values for risk amounts in the inputs.

Moving Average Period:

Change the SMMA period if desired.

Limitations and Considerations

Lagging Indicators: ATR and SMMA are lagging indicators and may not predict future price movements.

Market Conditions: The effectiveness of this indicator may vary across different assets and market conditions.

Risk of Overfitting: Relying solely on this indicator without considering other factors may lead to suboptimal trading decisions.

Conclusion

This indicator combines essential elements of technical analysis to provide a comprehensive tool for traders. By visualizing ATR bands anchored at the OHLC4, indicating volatility crossovers, and providing real-time data on position sizing and trend direction, it aids in making informed trading decisions.

Whether you're a novice trader looking to understand market volatility or an experienced trader seeking to refine your strategy, this indicator offers valuable insights directly on your TradingView charts.

Code Summary

The script is written in Pine Script™ version 5 and includes:

Calculations for OHLC4, ATRs, Bands, SMMA:

Uses built-in functions like ta.atr() and ta.rma() for calculations.

Plotting Functions:

plotshape() for the OHLC4 dotted line.

plot() and fill() for the ATR bands.

Crossover Detection:

ta.crossover() and ta.crossunder() for detecting ATR crosses.

Labeling Crossovers:

label.new() to place informative labels on the chart.

Information Table Creation:

table.new() to create the table.

table.cell() to populate it with data.

Acknowledgments

ATR and SMMA Concepts: Built upon standard technical analysis concepts widely used in trading.

Pine Script™: Leveraged the capabilities of Pine Script™ version 5 for advanced charting and analysis.

Note: Always test any indicator thoroughly and consider combining it with other forms of analysis before making trading decisions. Trading involves risk, and past performance is not indicative of future results.

Happy Trading!

EV Calculator [CHE]EV Calculator with Adjustable Boxes and Custom Colors for TradingView

Introduction:

As a trader, one of the key metrics you need to evaluate is the Expected Value (EV) of your trading strategy. Understanding EV helps you gauge whether your trades will be profitable in the long run. This TradingView script allows you to visualize your EV alongside customizable win rates and risk-to-reward ratios. With adjustable visual components, you can quickly determine whether your trading strategy has a positive or negative EV, and make informed decisions.

Features of the Script:

1. Customizable Inputs:

- Win Rate: Set your win probability (0.0 to 1.0), which represents how often your strategy is successful.

- Risk and Reward: Define how much you're risking and the potential reward for each trade.

2. Visual Representation:

- The script creates colored boxes representing different EV scenarios:

- Green Box: Indicates a good EV (>2), suggesting a highly profitable strategy.

- Yellow Box: Represents a neutral EV (between 0 and 2), where the strategy could work but is not optimal.

- Red Box: Shows a negative EV (<0), signaling that the strategy may lead to losses.

3. Adjustable Box Size:

- You can modify the width and height of the boxes to fit your chart display preferences, giving you better visual clarity based on your screen or chart style.

4. Dynamic Labels:

- Each bar in the chart includes dynamic labels showing:

- Win Rate: Displays the percentage chance of success.

- EV Value: Shows the calculated expected value based on the win rate and risk-reward ratio.

- Guide: Explains what each colored box means so that you can easily interpret the chart.

5. Scalability and Flexibility:

- The script only keeps a maximum of 20 recent entries, ensuring that your chart stays clean and organized.

- Both the number of labels and boxes adjust automatically to match your preferred settings, enhancing usability.

How the EV Calculation Works:

The formula for EV is based on a standard risk-to-reward model:

EV = (Win\ Rate \times Reward) - (Loss\ Probability \times Risk)

For example:

- If your win rate is 60% and your risk-to-reward ratio is 1:3, the script will calculate whether this strategy is expected to yield positive returns or result in long-term losses.

Example Use Case:

Let's say you are trading with a 60% win rate, risking 1 unit to gain 3 units. The script calculates that your EV is positive and represents this with a Green Box, showing you that your strategy has a high likelihood of being profitable. If your strategy slips and the win rate drops, the EV calculation will adjust, and you may see Yellow or Red Boxes, signaling a need for adjustment.

Final Thoughts:

This script is designed for traders who want to take their analysis beyond the basics. By providing real-time visualization of your EV, you can better assess whether your strategy is sound and make adjustments as needed.

How to Use:

- Adjust the input parameters for Win Rate, Risk, and Reward to match your trading strategy.

- Observe the colored boxes and labels to quickly understand if your current strategy is in a healthy EV zone.

- Use this visual feedback to refine your approach and stay on track towards profitability.

This tool simplifies the complex calculations behind EV and turns it into an intuitive and powerful decision-making aid for traders.

Now you're ready to integrate the EV Calculator with Adjustable Boxes and Custom Colors into your trading routine and start optimizing your strategies for long-term success!

Happy Trading and best regards Chervolino

Options Series - P_SAR And Supertrend

The provided PineScript combines two well-known indicators—Parabolic SAR (P_SAR) and Supertrend—to create a comprehensive trading tool. Here are some powerful insights and the importance of this script:

⭐ 1. Supertrend Indicator:

What it does: The Supertrend indicator is based on the Average True Range (ATR) and is used to identify trend direction. When the price is above the Supertrend line, it suggests an uptrend, and when below, a downtrend.

Insights:

Trend Following: By adjusting the ATR length (atrPeriod) and the multiplier (factor), you can fine-tune the sensitivity of the Supertrend. A smaller ATR or factor results in more frequent trend changes, whereas larger values make the indicator more robust but slower to react.

Trend Visualization: The script highlights trends with the help of green and red lines, offering a clear visual cue for traders. The uptrend is filled with a translucent green and the downtrend with red, allowing quick identification of market momentum.

⭐ 2. Parabolic SAR (P_SAR):

What it does: The Parabolic SAR is a time/price-based indicator that helps identify potential reversals in the market. The dots (SAR) follow the price and move closer to it as the trend progresses.

Insights:

Trailing Stops: This is commonly used by traders to trail stop losses, as the SAR moves closer to price as the trend strengthens.

Combining with Supertrend: The SAR dots in this script act as an additional confirmation for trend direction. For instance, when the price is above both the SAR and Supertrend, it strongly suggests an uptrend.

⭐ 3. Bar Coloring Based on Trend Confirmation:

What it does: The script calculates conditions based on whether the price is above or below both the Supertrend and SAR values.

Insights:

Bullish/Bearish Confirmation: The combination of these two indicators provides a stronger confirmation of trend direction compared to using either one alone. For example:

Green Bars: If the price is above both the Supertrend and SAR, it signals a strong uptrend (bullish).

Red Bars: If the price is below both, it suggests a strong downtrend (bearish).

Visual Alerts: The candle colors are adjusted based on these conditions, providing a quick visual alert for traders to take action.

⭐ 4. Importance of Using Both Supertrend and P_SAR:

Multiple Confirmations: Combining the Supertrend and Parabolic SAR increases the accuracy of trend-following strategies. Each indicator has its strengths: Supertrend is good for identifying the overall trend, while the SAR excels at identifying potential reversals.

Risk Management: This script can help you not only identify trends but also manage your positions more effectively. The Parabolic SAR, for example, can serve as a dynamic stop-loss level, while the Supertrend can help you stay in trades longer by smoothing out noise in the market.

⭐ 5. Customizable Inputs:

Adaptability: The user can adjust the ATR period, factor, start, increment, and maximum values, tailoring the script to different market conditions and timeframes. This flexibility is essential, as each asset class or market may require different parameter settings.

⭐ 6. Practical Application in Trading:

Entry and Exit Signals: The script can be used to generate entry and exit signals. For instance:

Buy Signal: When the bar turns green (price is above Supertrend and SAR), it could be a signal to go long.

Sell Signal: When the bar turns red (price is below Supertrend and SAR), it could be a signal to go short or exit a long position.

Stop-Loss Placement: The Parabolic SAR dots can act as trailing stop-loss levels, helping traders lock in profits as trends progress.

Trend Continuation vs. Reversal: The Supertrend provides a broader view of the trend, while the Parabolic SAR provides pinpoint entry/exit signals for reversals.

🚀 Conclusion:

This script is a robust combination of trend-following and reversal indicators, making it a versatile tool for traders. The dual confirmation from Supertrend and Parabolic SAR reduces false signals, and the color-coded bars provide quick insights into market conditions. When used properly, this can greatly improve your ability to catch trends early, exit at the right moment, and manage risk effectively.

[TR] Engulf Patterns by SM

Engulf Pattern by SM

Overview:

The " Engulf Pattern by SM" script is designed to identify bullish and bearish engulfing candlestick patterns on TradingView charts. Engulfing patterns are significant in technical analysis as they often indicate potential reversals in market trends.

Features:

- Bullish Engulfing Pattern Detection: The script identifies bullish engulfing patterns, which occur when a larger bullish candle completely engulfs the body of the previous smaller bearish candle.

- Bearish Engulfing Pattern Detection: Similarly, it detects bearish engulfing patterns, where a larger bearish candle engulfs the body of the preceding smaller bullish candle.

- Body Size Filtering: The script includes a feature to filter patterns based on the size of the candle bodies, allowing for more precise marking of significant patterns.

- Visual Markers: The script plots visual markers on the chart to highlight the detected engulfing patterns, making it easy for traders to spot them.

How It Works:

1. Bullish Engulfing Pattern:

- The script checks for a smaller bearish candle followed by a larger bullish candle.

- The body of the bullish candle must completely cover the body of the bearish candle.

- The size of the bullish candle's body must meet a specified threshold to be considered significant.

2. Bearish Engulfing Pattern:

- The script looks for a smaller bullish candle followed by a larger bearish candle.

- The body of the bearish candle must completely engulf the body of the bullish candle.

- The size of the bearish candle's body must meet a specified threshold to be considered significant.

Usage:

- Add the Script: Apply the " Engulf Pattern by SM" script to your TradingView chart.

- Configure Settings: Customize the script settings to suit your trading strategy, including visual marker styles and body size thresholds.

- Monitor Visual Markers: Keep an eye on the visual markers to identify potential trading opportunities based on engulfing patterns.

Disclaimer:

This script is not intended to be used as a direct entry signal. It should be used as a confluence in your overall trading plan. Always conduct your own analysis and consider multiple factors before making any trading decisions.

Feel free to customize this writeup further to match your specific needs! If you have any other requests or need additional details, just let me know.

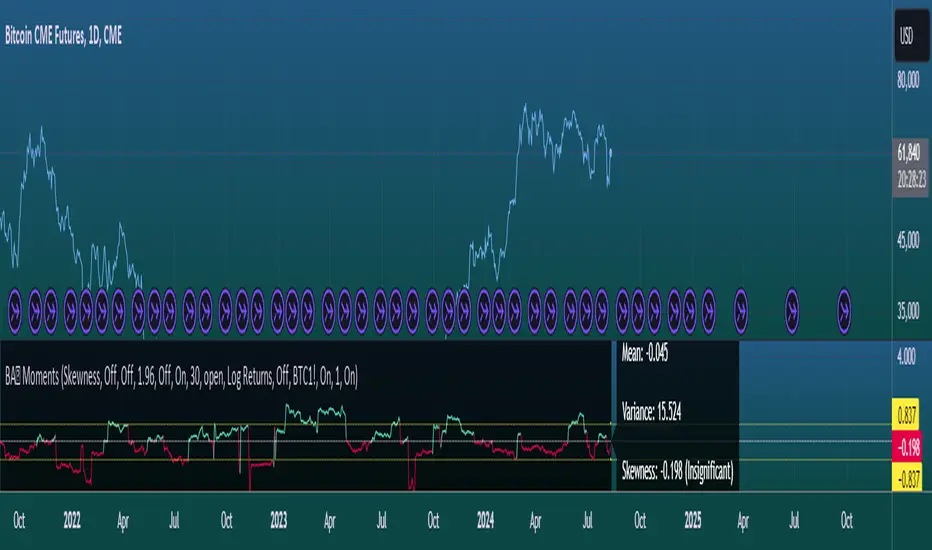

Moments Functions

This script is a TradingView Pine Script (version 5) for calculating and plotting statistical moments of a financial series. Here's a breakdown of what it does:

Script Overview

Purpose:

The script calculates and visualizes moments such as Mean, Variance, Skewness, and Kurtosis of a price series.

It also provides the option to display log returns and various statistical bands.

Inputs:

Moments Selection: Choose from Mean, Variance, Skewness, or Excess Kurtosis.

Source Settings: Define the lookback period and source data (e.g., closing price or log returns).

Plot Settings: Control visibility and styling of plots, bands, and information panels.

Colors Settings: Customize colors for different plot elements.

Functions:

f_va(): Computes sample variance.

f_sd(): Computes sample standard deviation.

f_skew(): Computes sample skewness.

f_kurt(): Computes sample kurtosis.

seskew(): Calculates the standard error of skewness.

sekurt(): Calculates the standard error of kurtosis.

skewcv(): Computes critical values for skewness.

kurtcv(): Computes critical values for kurtosis.

Outputs:

Plots:

Moment values (Mean, Variance, Skewness, Kurtosis).

Log Returns (if selected).

Standard Deviation Bands (if selected).

Critical Values for Skewness and Kurtosis (if selected).

Information Panel: Displays current statistical values and their significance.

Customization:

Users can customize appearance and behavior of the script through various input options, including colors, line thickness, and background settings.

Key Variables and Constants

Constants:

zscoreS and zscoreL: Z-scores for confidence intervals based on sample size.

skewrv and kurtrv: Reference values for skewness and excess kurtosis.

Sample Functions:

f_va() and f_sd(): Custom functions to calculate sample variance and standard deviation.

f_skew() and f_kurt(): Custom functions to calculate skewness and kurtosis.

Critical Values:

Functions skewcv() and kurtcv() calculate critical values used to assess statistical significance of skewness and kurtosis.

Plotting

Plot Types:

Mean, variance, skewness, and excess kurtosis are plotted based on user selection.

Log returns are plotted if enabled.

Standard deviation bands and critical values are plotted if enabled.

Labels:

Information panel labels display mean, variance/standard deviation, skewness, and kurtosis values along with their significance.

Example Usage

To use this script:

Add it to a TradingView chart.

Adjust inputs to configure which statistical moments to display, the source data, and the appearance of the plots.

Review the plotted data and labels to analyze the statistical properties of the selected price series.

This script is useful for traders and analysts looking to perform advanced statistical analysis on financial data directly within TradingView.

When comparing two stock prices over a period of time, the statistical moments—mean, variance, skewness, and kurtosis—can provide a deep insight into the behavior of the stock prices and their distributions. Here’s what each moment signifies in this context:

1. Mean

Definition: The mean (or average) is the sum of the stock prices over the period divided by the number of data points. It represents the central value of the price series.

Interpretation: When comparing two stocks, the mean tells you the average price level of each stock over the period. A higher mean indicates that, on average, the stock price is higher compared to another stock with a lower mean.

Comparison Insight: If Stock A has a higher mean price than Stock B, it implies that Stock A's prices are generally higher than those of Stock B over the given period.

2. Variance

Definition: Variance measures the dispersion or spread of the stock prices around the mean. It is the average of the squared differences from the mean.

Interpretation: A higher variance indicates that the stock prices fluctuate more widely from the mean, implying greater volatility. Conversely, a lower variance indicates more stable and predictable prices.

Comparison Insight: Comparing the variances of two stocks helps in assessing which stock has more price volatility. If Stock A has a higher variance than Stock B, it means Stock A's prices are more volatile and less predictable compared to Stock B.

3. Skewness

Definition: Skewness measures the asymmetry of the distribution of stock prices around the mean. It can be positive, negative, or zero:

Positive Skewness: The distribution has a long right tail, with more frequent small returns and fewer large positive returns.

Negative Skewness: The distribution has a long left tail, with more frequent small returns and fewer large negative returns.

Zero Skewness: The distribution is symmetric around the mean.

Interpretation: Skewness tells you about the direction of outliers in the stock price distribution. Positive skewness means a higher probability of large positive returns, while negative skewness means a higher probability of large negative returns.

Comparison Insight: By comparing skewness, you can understand the nature of extreme returns for two stocks. For example, if Stock A has positive skewness and Stock B has negative skewness, Stock A might have more frequent large gains, whereas Stock B might have more frequent large losses.

4. Kurtosis

Definition: Kurtosis measures the "tailedness" of the distribution of stock prices. It indicates how much of the distribution is in the tails versus the center. High kurtosis means more outliers (extreme returns), while low kurtosis means fewer outliers.

Interpretation:

High Kurtosis: Indicates a higher likelihood of extreme price movements (both high and low) compared to a normal distribution.

Low Kurtosis: Indicates that extreme price movements are less common.

Comparison Insight: Comparing kurtosis between two stocks shows which stock has more extreme returns. If Stock A has higher kurtosis than Stock B, it means Stock A has more frequent extreme price changes, suggesting more risk or opportunities for large gains or losses.

Summary

Mean: Compares average price levels.

Variance: Compares price volatility.

Skewness: Compares the asymmetry of price movements.

Kurtosis: Compares the likelihood of extreme price changes.

By analyzing these statistical moments, you can gain a comprehensive view of how the two stocks behave relative to each other, which can inform investment decisions based on risk, return expectations, and the nature of price movements.

Swing High/Low & EMA Cross AlertScript Description:

This script on TradingView combines the detection of Swing High/Low points with exponential moving average (EMA) crossovers to provide buy and sell alerts and to mark swing points on the chart.

What the Script Does:

Swing High/Low Detection:

Uses the ta.pivothigh function to detect significant high points and the ta.pivotlow function to detect significant low points.

For each detected point, the script checks if it is a new higher high (HH) or lower high (LH) for the highs, and a new lower low (LL) or higher low (HL) for the lows.

Creates visual labels to identify these points on the chart, helping traders to visualize potential reversal points.

EMA Crossover:

Calculates two EMAs: a fast EMA (fastEMA) with a default period of 50 and a slow EMA (slowEMA) with a default period of 200.

Detects bullish crossovers (when fastEMA crosses above slowEMA) and bearish crossunders (when fastEMA crosses below slowEMA).

Generates buy and sell alerts based on these crossovers.

How the Script Works:

EMA Calculation: EMAs are calculated using the closing prices and user-defined periods.

Swing High/Low Detection: Uses the high and low values from the previous length bars to determine the swing points.

Alert Generation: Alerts are triggered when crossovers between the EMAs occur.

How to Use the Script:

Add to Chart: Insert the script into TradingView and apply it to the desired chart.

Configure Parameters:

Adjust the detection period for swing points (length).

Configure the periods for the EMAs (fastLen and slowLen).

Customize the colors for the swing point labels as per your preference.

Monitor Alerts: Use the EMA crossover alerts to make buy or sell decisions. Observe the swing point labels to identify potential trend reversals.

Justification for the Combination:

EMAs: Widely used to identify trend direction. Combining a fast EMA with a slow EMA helps capture both short-term and long-term trend changes.

Swing High/Low: Identifies reversal points in price, which are crucial for determining potential entry and exit points in trades.

Combination:

Combining EMAs and Swing High/Low provides a comprehensive view of price behavior, helping traders to effectively identify trends and reversal points.

This script is useful for traders who want to combine trend analysis (via EMAs) with the identification of reversal points (Swing High/Low), providing a more complete view of price behavior on the chart.

ATR5 Gerchik&CoThis script is designed to calculate and display the Average True Range (ATR) based on the last 5 bars on a daily (D1) chart. The ATR is a key indicator used to measure market volatility by decomposing the entire range of an asset price for that period. Additionally, the script provides a visual representation of the percentage of the current day's range relative to the calculated ATR.

How It Works

Calculation of ATR:

The script calculates the ATR by taking the high and low of each of the last 5 daily bars, computing the range for each bar, and then averaging these values.

The ATR value is then dynamically formatted based on the decimal places relevant to the asset's tick size.

Percentage of Current Day's Range:

The script also calculates the percentage of the current day's range compared to the ATR. This helps traders quickly assess how much of the average range has been covered today.

Visual Display:

The ATR value and the percentage of the current day's range are displayed in the top-right corner of the chart for easy reference.

Usage

Identifying Volatility: The ATR is a widely used indicator to identify periods of high and low volatility in the market. Traders can use this to adjust their strategies accordingly, such as widening or tightening stop-loss levels.

Entry and Exit Points: Knowing the ATR can help traders decide on optimal entry and exit points based on expected market movements.

Risk Management: By understanding the market volatility, traders can better manage their risk by adjusting position sizes and stop-loss levels.

Example

The script shows the ATR calculated over the last 5 days, formatted to match the asset's decimal places.

It also displays the current day's range as a percentage of the ATR, providing immediate insight into the day's volatility relative to the recent average.

How to Use

Apply the Script: Add the script to your TradingView chart.

Analyze the Display: Observe the ATR value and the percentage of the current day's range displayed in the top-right corner.

Make Informed Decisions: Use the information to make informed trading decisions based on the volatility and range of the asset.

Code Explanation

The script uses Pine Script v5 and includes functions to calculate the range of bars, average these ranges, and format the output appropriately. The ATR value and percentage are displayed using the table functionality to ensure clear and precise placement on the chart.

This description should provide users with a clear understanding of what the script does, how it can be used, and the concepts behind its calculations. Let me know if you need any further adjustments or additional details!

Multi-Timeframe MA Levels█ OVERVIEW

This Pine Script is an indicator for displaying multiple moving average (MA) levels from several timeframes on your TradingView charts. At the Realtime Bar (the right-most bar on your chart), it draws a line where the various moving averages currently are.

For example, it will show you where the 8 EMA on the 5 minute timeframe is on your 1-minute timeframe chart.

It derives its look and function from "Lepelle's Key Levels" and focuses on visualizing various moving averages to complement this indicator.

█ FEATURES

1 — Multi-Timeframe Analysis:

• The script allows traders to view moving averages from different timeframes on a single chart.

This multi-timeframe approach helps identify significant levels and trends that might not be apparent when looking at a single timeframe.

2 — Customization and Flexibility:

• Extensive input options for customizing the appearance of the lines (width, style, color) and labels (size, position, distance from price).

This ensures that the indicator can be tailored to individual preferences and charting styles.

3 — Multiple Moving Averages:

• Support for various types of moving averages (8 EMA, 21 EMA, 50 SMA, 100 SMA, 200 SMA).

Each moving average can be individually enabled or disabled for specific timeframes,

providing a flexible tool for technical analysis.

█ SETTINGS

Inputs for Styling:

• Controls the appearance of the lines and labels.

• Includes options for line width, line style, text size, distance from the candlesticks, label position,

and whether to hide prices or use shorthand notation.

Moving Averages Settings:

• Inputs to select different moving averages (8 EMA, 21 EMA, 50 SMA, 100 SMA, 200 SMA) and their corresponding colors.

• Boolean inputs to enable or disable these moving averages on various timeframes (2 min, 5 min, hourly, daily).

█ SUMMARY

In essence, this script provides a comprehensive tool for technical analysis by combining multi-timeframe moving averages into a single, customizable, and user-friendly indicator. It enhances traders' ability to make informed decisions by providing clear visual representations of key moving average levels across different timeframes.

═════════════════════════════════════════════════════════════

█ LIMITATIONS

This script is best used with a short timeframe such as 1-minute or lower because of the limitations of Multi-Timeframe scripts. Basically, the alternate timeframes in use should always be higher than the chart timeframe.

═════════════════════════════════════════════════════════════

█ NOTES

This indicator is intended to complement and be used with "Lepelle's Key Levels" indicator.

In that indictor settings, I recommend turning off the 5 Daily timeframe moving average levels in that script, if using this one.

═════════════════════════════════════════════════════════════

Harmony or Divergence Single CandleThis script is designed for traders who seek to visually identify and analyze patterns of harmony and divergence in the price action of securities directly on their trading charts. The script provides a nuanced approach to understanding market sentiment and potential price movement directions by examining candle sizes and volumes over a specified lookback period.

What the Script Does:

The script overlays indicators on the price chart that highlight periods of harmony and divergence using background colors. These periods are determined based on comparisons between current candle sizes, candle volumes, and their respective simple moving averages (SMAs) over a user-defined lookback period.

Harmony : A state where the candle size and volume are either both above or below their respective averages, indicating a consensus or agreement in market direction.

Divergence : A state where there's a mismatch, such as a larger candle size with lower volume or vice versa, suggesting uncertainty or potential reversal in market trends.

How It Does It:

User Inputs : Traders can customize several parameters, including the lookback period for averages, whether to include wicks in candle size calculations, and preferences for displaying harmony and divergence indicators with specific colors.

Calculations :

- The script calculates the simple moving average (SMA) of volume and candle sizes (with an option to consider the full candle range including wicks or just the body) over the specified lookback period.

- It then compares the current candle's size and volume against these averages to identify states of harmony or divergence.

Visualization :

- Based on the user's input, it colors the background of the chart to reflect identified patterns. Each state (harmony above or below average, divergence with higher volume or larger candle body) can be highlighted with different colors, providing immediate visual cues to the trader.

What Traders Can Do With the Script:

Traders can utilize this script to enhance their technical analysis by:

Identifying Trend Consistency : Harmony indicators can signal strong trends where price action and volume confirm each other, possibly supporting continuation strategies.

Spotting Potential Reversals : Divergence indicators may highlight potential exhaustion points or reversals, especially when price moves significantly without corresponding volume support.

Customizing Analysis : By adjusting the lookback period, candle size consideration (body or including wicks), and visualization options, traders can tailor the analysis to fit their trading style and strategy.

Table to filter trades per dayThis script contains a block of code that allows users to filter the total number of trades, loss trades, win trades and win rate per day in a table. This makes it easier to compare which days were profitable and which were not.

Be aware that this script can only be used in strategy scripts. To use the script, open it and copy every line from "START" to "STOP". Then, paste these lines at the very bottom of the strategy script that you want to attach it to.

The user has the ability to adjust the position of the table and customize the size of the text displayed.

If the user sets "Check when the trade:" to "Opened", the script will monitor when the trade opens and add it to the table once it has been closed. If "Check when the trade:" is set to "Closed", the script will track when the trade is closed and add it to the table once it has been closed.

It is recommended to run the script on the "Exchange" setting for more accurate results, even though a "Set the timezone" option is available. This will prevent discrepancies caused by daylight saving time changes.

Please note that the code will only work properly if you choose a daily timeframe or lower.

IU Support and Resistance How this script works :

1. This script is an indicator script which calculates the support and resistance based on pivot high and pivot low and plot them as zone onto the chart.

2. The first user input is minimum number of touches which indicates how many time pivot high or pivot low should be tested in order to be a valid support or resistance level.

3.The second user input "Set Buffer" check if the user wants to use a custom buffer or not if it's unchanged then the default is 50% of the 1000 period ATR value .

4. If "Set Buffer" is checked meaning if it's set to true then only the third user input will be execute which is the "buffer" which indicates how much price range user wants his zone to have.

5. After the user input part this script create two arrays to store the pivot high and pivot low values every time he have a new value.

6. This script also creates two arrays to store the bar index of the bar where the new pivot high or pivot low is detected those bar index will be later use while creating the support and resistance zones.

7. Then the script creates four more arrays to store the final support and resistance values and their respective bar index which will be use for creating the support and resistance zones.

8. After this the script check that we are at the last bar of our chart if we are then we sort the support and resistance indices by descending order and store them into an new variable after that we sort the support and resistance arrays by descending order, then we loop through the arrays elements and we check if the previous element comes under the zone of the current element if so we increase the "minimum touch" variable by 1, once we have 5 or more count in our variable and we no longer have a valid zone then we store the element value and the sorted index of the element into our final arrays.

9. Finally the script will loop through the final support and resistance arrays and it will create a box for each support and resistance with respect to extending it on both directions.

10.The green zones are the support and the red zones are the resistance.

How user can benifits from this script:

1. User can automatically identify support and resistance zones and he can plan his trade as per that.

2. User can test how different markets reacts with support and resistance zones.

3. User can plan breakout trade on the break of the support or resistance level.

4. User can adjust he stop loss and take profit as per the support and resistance zones.

Linear Reg CandlesThe provided Pine Script is a TradingView script for creating a technical analysis indicator called "Humble LinReg Candles." This script includes features such as linear regression for open, high, low, and close prices, signal smoothing with simple or exponential moving averages, and a trailing stop based on Average True Range (ATR). Additionally, the script contains a screener section to display signals for a list of specified symbols.

Here is a breakdown of the script:

Indicator Settings:

It defines various input parameters such as signal smoothing length, linear regression settings, and options for using simple moving averages.

Linear regression is applied to open, high, low, and close prices based on user-defined settings.

ATR Trailing Stop:

It calculates the Average True Range (ATR) and uses it to determine a trailing stop for buy and sell signals.

Signals are generated based on whether the close price is above or below the ATR trailing stop.

Plotting:

The script plots the calculated signal on the chart using the plot function.

Buy and Sell Conditions:

Buy and sell conditions are defined based on the relationship between the close price and the ATR trailing stop.

Plot shapes and bar colors are used to visually represent buy and sell signals on the chart.

Alerts:

Alerts are triggered when buy or sell conditions are met.

Screener Section:

The script defines a screener section to display a watchlist of symbols with long and short signals.

The watchlist includes a set of predefined symbols with corresponding long and short signals.

Table Theme Settings:

The script allows customization of the table theme, including background color, frame color, and text color.

The size and location of the table on the chart can also be customized.

Screener Function:

A function getSignal is defined to determine long and short signals for each symbol in the watchlist.

The getSym function is used to extract the symbol name from the symbol string.

Dashboard Creation:

The script creates a table (dashboard) to display long and short signals for the symbols in the watchlist.

The table includes headers for "Long Signal" and "Short Signal" and lists the symbols with corresponding signals.

Overall, the script combines technical analysis indicators and a screener to help traders identify potential buy and sell signals for a set of specified symbols.

Kiss Of DeathThis Pine Script code is designed to create a technical indicator on a TradingView chart known as the "Kiss of Death" signal. Here's a description of the script:

The script begins by specifying that it is intended for use with Pine Script version 5 (//@version=5) and sets the indicator's title to "Kiss of Death Signal" with indicator(title="Kiss of Death Signal", overlay=true).

The code calculates a 21-period Exponential Moving Average (EMA) of the closing prices (ema21 = ta.ema(close, 21)). The EMA is a commonly used trend-following indicator.

It also determines the lowest low of the previous two periods (prev_low = ta.lowest(low, 2)). This variable will be used in the signal condition.

The script then defines the signal condition for the "Kiss of Death" pattern. This pattern occurs when:

The current closing price is below the 21-period EMA (close < ema21).

The previous closing price is above or equal to the 21-period EMA (close >= ema21).

The current low is below the lowest low of the previous two periods (low < prev_low).

Next, it uses plot to display the 21-period EMA on the chart (plot(ema21, color=color.blue, title="21 EMA")), using a blue color.

Finally, the script utilizes plotshape to mark the points on the chart where the "Kiss of Death" signal condition is met. It places a red, downward-pointing triangle above the corresponding bars

In summary, this script provides a visual representation of the "Kiss of Death" signal on a TradingView chart, helping traders identify potential bearish reversal points based on the defined conditions. The 21-period EMA is also displayed to provide additional context.

What makes this script unique is that it specifically identifies and visualizes a specific technical pattern known as the "Kiss of Death". The "Kiss of Death" is a bearish reversal pattern that occurs when the current price falls below a specific moving average (in this case, a 21-period Exponential Moving Average or EMA) after previously being above it, and when the current low is below the lowest low of the previous two periods.

This script stands out because it provides a clear and visual representation of this particular pattern on a TradingView chart. By using a red, downward-pointing triangle above the bars, it helps traders quickly identify potential bearish reversal points based on the defined conditions.

The combination of a specific pattern, in this case the "Kiss of Death", along with a visual indicator, sets this script apart and makes it a useful tool for traders looking to identify potential bearish reversal points in their technical analysis.

IU Average move How The Script Works :

1. This script calculate the average movement of the price in a user defined custom session and plot the data in a table from on top left corner of the chart.

2. The script takes highest and lowest value of that custom session and store their difference into an array.

3. Then the script average the array thus gets the average price.

4. Addition to that the script converter the price pip change into percentage in order to calculate the value in percentage form.

5. This script is pure price action based the script only take price value and doesn't take any indicator for calculation.

6. The script works on every type of market.

7. If the session is invalid it returns nothing

8. The background color, text color and transparency is changeable.

How User Can Benefit From This Script:

1. User can understand the volatility of any session that he/she wish to trade.

2. It can be helpful for understanding the average price moment of any tradeble asset.

3. It will give the average price movement both in percentage and points bases.

4. By understanding the volatility user can adjust his stop loss or take profit with respect his risk management.

Naresh CE with 13 62 crossThank you to Lauris, for sharing knowledge and logic for the EMA cross-over (13/62).

The provided Pine Script is a custom script, which is designed to display Chandelier Exit levels on the price chart and generate buy and sell labels based on specific conditions.

Here's a breakdown of the key components and logic of the Pine Script:

Exponential Moving Averages (EMAs):

ema1: The 13-period Exponential Moving Average (EMA) of the closing price.

ema2: The 62-period Exponential Moving Average (EMA) of the closing price.

EMA Plotting:

The script plots the ema1 (13 EMA) and ema2 (62 EMA) lines on the price chart using the plot() function.

Chandelier Exit Calculation:

The Chandelier Exit values are calculated using the Average True Range (ATR).

The script calculates the atr (Average True Range) using the atr() function with the given length.

longStop is calculated as the highest price of the specified length minus the ATR, and shortStop is calculated as the lowest price plus the ATR.

Directional Indicator (dir):

The dir variable is used to determine the direction of the Chandelier Exit based on the comparison of the current close price with the previous long and short stops.

Buy and Sell Signals:

The script generates buy signals when the Chandelier Exit direction changes from short to long (buySignal).

Similarly, sell signals are generated when the Chandelier Exit direction changes from long to short (sellSignal).

The conditions for buy and sell signals are based on the value of dir and its previous value.

Buy and Sell Labels:

Buy and sell labels are plotted on the chart using plotshape() based on the generated buy and sell signals.

The showLabels input parameter controls whether to display the buy and sell labels.

Highlighting States:

The script fills the chart area with color (green for long, red for short) based on the direction of the Chandelier Exit values.

The highlightState input parameter controls whether to apply this highlighting.

Alerts:

The script includes alert conditions based on the direction change (changeCond), buy signal (buySignal), and sell signal (sellSignal) using the alertcondition() function.

The script aims to help traders identify potential buy and sell signals based on the Chandelier Exit levels derived from the 13 EMA and 62 EMA crossovers. The Chandelier Exit values can serve as dynamic stop-loss levels for long and short positions.

120x ticker screener (composite tickers)In specific circumstances, it is possible to extract data, far above the 40 `request.*()` call limit for 1 single script .

The following technique uses composite tickers . Changing tickers needs to be done in the code itself as will be explained further.

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

🔶 PRINCIPLE

Standard example:

c1 = request.security('MTLUSDT' , 'D', close)

This will give the close value from 1 ticker (MTLUSDT); c1 for example is 1.153

Now let's add 2 tickers to MTLUSDT; XMRUSDT and ORNUSDT with, for example, values of 1.153 (I), 143.4 (II) and 0.8242 (III) respectively.

Just adding them up 'MTLUSDT+XMRUSDT+ORNUSDT' would give 145.3772 as a result, which is not something we can use...

Let's multiply ORNUSDT by 100 -> 14340

and multiply MTLUSDT by 1000000000 -> 1153000000 (from now, 10e8 will be used instead of 1000000000)

Then we make the sum.

When we put this in a security call (just the close value) we get:

c1 = request.security('MTLUSDT*10e8+XMRUSDT*100+ORNUSDT', 'D', close)

'MTLUSDT*10e8+XMRUSDT*100+ORNUSDT' -> 1153000000 + 14340 + 0.8242 = 1153014340.8242 (a)

This (a) will be split later on, for example:

1153014330.8242 / 10e8 = 1.1530143408242 -> round -> in this case to 1.153 (I), multiply again by 10e8 -> 1153000000.00 (b)

We subtract this from the initial number:

1153014340.8242 (a)

- 1153000000.0000 (b)

–––––––––––––––––

14340.8242 (c)

Then -> 14340.8242 / 100 = 143.408242 -> round -> 143.4 (II) -> multiply -> 14340.0000 (d)

-> subtract

14340.8242 (c)

- 14340.0000 (d)

––––––––––––

0.8242 (III)

Now we have split the number again into 3 tickers: 1.153 (I), 143.4 (II) and 0.8242 (III)

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

In this publication the function compose_3_() will make a composite ticker of 3 tickers, and the split_3_() function will split these 3 tickers again after passing 1 request.security() call.

In this example:

t46 = 'BINANCE:MTLUSDT', n46 = 10e8 , r46 = 3, t47 = 'BINANCE:XMRUSDT', n47 = 10e1, r47 = 1, t48 = 'BINANCE:ORNUSDT', r48 = 4 // T16

•••

T16= compose_3_(t48, t47, n47, t46, n46)

•••

= request.security(T16, res, )

•••

= split_3_(c16, n46, r46, n47, r47, r48)

🔶 CHANGING TICKERS

If you need to change tickers, you only have to change the first part of the script, USER DEFINED TICKERS

Back to our example, at line 26 in the code, you'll find:

t46 = 'BINANCE:MTLUSDT', n46 = 10e8 , r46 = 3, t47 = 'BINANCE:XMRUSDT', n47 = 10e1, r47 = 1, t48 = 'BINANCE:ORNUSDT', r48 = 4 // T16

( t46 , T16 ,... will be explained later)

You need to figure out how much you need to multiply each ticker, and the number for rounding, to get a good result.

In this case:

'BINANCE:MTLUSDT', multiply number = 10e8, round number is 3 (example value 1.153)

'BINANCE:XMRUSDT', multiply number = 10e1, round number is 1 (example value 143.4)

'BINANCE:ORNUSDT', NO multiply number, round number is 4 (example value 0.8242)

The value with most digits after the decimal point by preference is placed to the right side (ORNUSDT)

If you want to change these 3, how would you do so?

First pick your tickers and look for the round values, for example:

'MATICUSDT', example value = 0.5876 -> round -> 4

'LTCUSDT' , example value = 77.47 -> round -> 2

'ARBUSDT' , example value = 1.0231 -> round -> 4

Value with most digits after the decimal point -> MATIC or ARB, let's pick ARB to go on the right side, LTC at the left of ARB, and MATIC at the most left side.

-> 'MATICUSDT', LTCUSDT', ARBUSDT'

Then check with how much 'LTCUSDT' and 'MATICUSDT' needs to be multiplied to get this: 5876 0 7747 0 1.0231

'MATICUSDT' -> 10e10

'LTCUSDT' -> 10e3

Replace:

t46 = 'BINANCE:MTLUSDT', n46 = 10e8 , r46 = 3, t47 = 'BINANCE:XMRUSDT', n47 = 10e1, r47 = 1, t48 = 'BINANCE:ORNUSDT', r48 = 4 // T16

->

t46 = 'BINANCE:MATICUSDT', n46 = 10e10 , r46 = 4, t47 = 'BINANCE:LTCUSDT', n47 = 10e3, r47 = 2, t48 = 'BINANCE:ARBUSDT', r48 = 4 // T16

DO NOT change anything at t46, n46,... if you don't know what you're doing!

Only

• tickers ('BINANCE:MTLUSDT', 'BINANCE:XMRUSDT', 'BINANCE:ORNUSDT', ...),

• multiply numbers (10e8, 10e1, ...) and

• round numbers (3, 1, 4, ...)

should be changed.

There you go!

🔶 LIMITATIONS

🔹 The composite ticker fails when 1 of the 3 isn't in market in the weekend, while the other 2 are.

That is the reason all tickers are crypto. I think it is possible to combine stock,... tickers, but they have to share the same market hours.

🔹 The number cannot be as large as you want, the limit lays around 15-16 digits.

This means when you have for example 123, 45.67 and 0.000000000089, you'll get issues when composing to this:

-> 123045670.000000000089 (21 digits)

Make sure the numbers are close to each other as possible, with 1 zero (or 2) in between:

-> 1.230045670089 (13 digits by doing -> (123 * 10e-3) + (45.67 * 10e-7) + 0.000000000089)

🔹 This script contains examples of calculated values, % change, SMA, RMA and RSI.

These values need to be calculated from HTF close data at current TF (timeframe).

This gives challenges. For example the SMA / %change is not a problem (same values at 1h TF from Daily data).

RMA , RSI is not so easy though...

Daily values are rather similar on a 2-3h TF, but 1h TF and lower is quite different.

At the moment I haven't figured out why, if someone has an idea, don't hesitate to share.

The main goal of this publication is 'composite tickers ~ request.security()' though.

🔹 When a ticker value changes substantially (x10, x100), the multiply number needs to be adjusted accordingly.

🔶 SETTINGS

SHOW SETS

SET

• Length : length of SMA, RMA and RSI

• HTF : Higher TimeFrame (default Daily)

TABLE

• Size table : \ _ Self-explanatory

• Include exchange name : /

• Sort : If exchange names are shown, the exchanges will be sorted first

COLOURS

• CH%

• RSI

• SMA (RMA)

DEBUG

Remember t46 , T16 ,... ?

This can be used for debugging/checking

ALWAYS DISABLE " sort " when doing so.

Example:

Set string -> T1 (tickers FIL, CAKE, SOL)

(Numbers are slightly different due to time passing by between screen captures)

Placing your tickers at the side panel makes it easy to compare with the printed label below the table (right side, 332201415014.45 ),

together with the line T1 in the script:

t1 = 'BINANCE:FILUSDT' , n1 = 10e10, r1 = 4, t2 = 'BINANCE:CAKEUSDT' , n2 = 10e5 , r2 = 3, t3 = 'BINANCE:SOLUSDT' , r3 = 2 // T1

FIL : 3.322

CAKE: 1.415

SOL : 14.56

Now it is easy to check whether the tickers are placed close enough to each other, with 1-2 zero's in between.

If you want to check a specific ticker, use " Show Ticker" , see out initial example:

Set string -> T16

Show ticker -> 46 (in the code -> t46 = 'BINANCE:MTLUSDT')

(Set at 0 to disable " check string " and NONE to disable " Set string ")

-> Debug/check/set away! 😀

🔶 OTHER TECHNIQUES

• REGEX ( Regular expression ) and str.match() is used to delete the exchange name from the ticker, in other words, everything before ":" is deleted by following regex:

exch(t) => incl_exch ? t : str.match(t, "(?<=:) +")

• To sort, array.sort_indices() is used (line 675 in the code), just as in my first "sort" publication Sort array alphabetically - educational

aSort = arrT.copy()

sort_Indices = array.sort_indices(id= aSort, order= order.ascending)

• Numbers and text colour will adjust automatically when switching between light/dark mode by using chart.fg_color / chart.bg_color

🔹 DISCLAIMER

Please don't ask me for custom screeners, thank you.

JS-TechTrading: VWAP Momentum_Pullback StrategyGeneral Description and Unique Features of this Script

Introducing the VWAP Momentum-Pullback Strategy (long-only) that offers several unique features:

1. Our script/strategy utilizes Mark Minervini's Trend-Template as a qualifier for identifying stocks and other financial securities in confirmed uptrends.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available on TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

2. Our strategy is based on the supply/demand balance in the market, making it timeless and effective across all timeframes. Whether you are day trading using 1- or 5-min charts or swing-trading using daily charts, this strategy can be applied and works very well.

3. We have also integrated technical indicators such as the RSI and the MA / VWAP crossover into this strategy to identify low-risk pullback entries in the context of confirmed uptrends. By doing so, the risk profile of this strategy and drawdowns are being reduced to an absolute minimum.

Minervini’s Trend-Template and the ‘Stage-Analysis’ of the Markets

This strategy is a so-called 'long-only' strategy. This means that we only take long positions, short positions are not considered.

The best market environment for such strategies are periods of stable upward trends in the so-called stage 2 - uptrend.

In stable upward trends, we increase our market exposure and risk.

In sideways markets and downward trends or bear markets, we reduce our exposure very quickly or go 100% to cash and wait for the markets to recover and improve. This allows us to avoid major losses and drawdowns.

This simple rule gives us a significant advantage over most undisciplined traders and amateurs!

'The Trend is your Friend'. This is a very old but true quote.

What's behind it???

• 98% of stocks made their biggest gains in a Phase 2 upward trend.

• If a stock is in a stable uptrend, this is evidence that larger institutions are buying the stock sustainably.

• By focusing on stocks that are in a stable uptrend, the chances of profit are significantly increased.

• In a stable uptrend, investors know exactly what to expect from further price developments. This makes it possible to locate low-risk entry points.

The goal is not to buy at the lowest price – the goal is to buy at the right price!

Each stock goes through the same maturity cycle – it starts at stage 1 and ends at stage 4

Stage 1 – Neglect Phase – Consolidation

Stage 2 – Progressive Phase – Accumulation

Stage 3 – Topping Phase – Distribution

Stage 4 – Downtrend – Capitulation

This strategy focuses on identifying stocks in confirmed stage 2 uptrends. This in itself gives us an advantage over long-term investors and less professional traders.

By focusing on stocks in a stage 2 uptrend, we avoid losses in downtrends (stage 4) or less profitable consolidation phases (stages 1 and 3). We are fully invested and put our money to work for us, and we are fully invested when stocks are in their stage 2 uptrends.

But how can we use technical chart analysis to find stocks that are in a stable stage 2 uptrend?

Mark Minervini has developed the so-called 'trend template' for this purpose. This is an essential part of our JS-TechTrading pullback strategy. For our watchlists, only those individual values that meet the tough requirements of Minervini's trend template are eligible.

The Trend Template

• 200d MA increasing over a period of at least 1 month, better 4-5 months or longer

• 150d MA above 200d MA

• 50d MA above 150d MA and 200d MA

• Course above 50d MA, 150d MA and 200d MA

• Ideally, the 50d MA is increasing over at least 1 month

• Price at least 25% above the 52w low

• Price within 25% of 52w high

• High relative strength according to IBD.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available in TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

This strategy can be applied to all timeframes from 5 min to daily.

The VWAP Momentum-Pullback Strateg y

For the JS-TechTrading VWAP Momentum-Pullback Strategy, only stocks and other financial instruments that meet the selected criteria of Mark Minervini's trend template are recommended for algorithmic trading with this startegy.

A further prerequisite for generating a buy signals is that the individual value is in a short-term oversold state (RSI).

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Stop-loss limits and profit targets can be set variably.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from April 2020 until April 2021 (1 yr)

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The RSI qualifier is highly selective and filters out the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• As a result, traders need to apply this strategy for a full watchlist rather than just one financial security.

TechnicalRating█ OVERVIEW

This library is a Pine Script™ programmer’s tool for incorporating TradingView's well-known technical ratings within their scripts. The ratings produced by this library are the same as those from the speedometers in the technical analysis summary and the "Rating" indicator in the Screener , which use the aggregate biases of 26 technical indicators to calculate their results.

█ CONCEPTS

Ensemble analysis

Ensemble analysis uses multiple weaker models to produce a potentially stronger one. A common form of ensemble analysis in technical analysis is the usage of aggregate indicators together in hopes of gaining further market insight and reinforcing trading decisions.

Technical ratings

Technical ratings provide a simplified way to analyze financial markets by combining signals from an ensemble of indicators into a singular value, allowing traders to assess market sentiment more quickly and conveniently than analyzing each constituent separately. By consolidating the signals from multiple indicators into a single rating, traders can more intuitively and easily interpret the "technical health" of the market.

Calculating the rating value

Using a variety of built-in TA functions and functions from our ta library, this script calculates technical ratings for moving averages, oscillators, and their overall result within the `calcRatingAll()` function.

The function uses the script's `calcRatingMA()` function to calculate the moving average technical rating from an ensemble of 15 moving averages and filters:

• Six Simple Moving Averages and six Exponential Moving Averages with periods of 10, 20, 30, 50, 100, and 200

• A Hull Moving Average with a period of 9

• A Volume-Weighted Moving Average with a period of 20

• An Ichimoku Cloud with a conversion line length of 9, base length of 26, and leading span B length of 52

The function uses the script's `calcRating()` function to calculate the oscillator technical rating from an ensemble of 11 oscillators:

• RSI with a period of 14

• Stochastic with a %K period of 14, a smoothing period of 3, and a %D period of 3

• CCI with a period of 20

• ADX with a DI length of 14 and an ADX smoothing period of 14

• Awesome Oscillator

• Momentum with a period of 10

• MACD with fast, slow, and signal periods of 12, 26, and 9

• Stochastic RSI with an RSI period of 14, a %K period of 14, a smoothing period of 3, and a %D period of 3

• Williams %R with a period of 14

• Bull Bear Power with a period of 50

• Ultimate Oscillator with fast, middle, and slow lengths of 7, 14, and 28

Each indicator is assigned a value of +1, 0, or -1, representing a bullish, neutral, or bearish rating. The moving average rating is the mean of all ratings that use the `calcRatingMA()` function, and the oscillator rating is the mean of all ratings that use the `calcRating()` function. The overall rating is the mean of the moving average and oscillator ratings, which ranges between +1 and -1. This overall rating, along with the separate MA and oscillator ratings, can be used to gain insight into the technical strength of the market. For a more detailed breakdown of the signals and conditions used to calculate the indicators' ratings, consult our Help Center explanation.

Determining rating status

The `ratingStatus()` function produces a string representing the status of a series of ratings. The `strongBound` and `weakBound` parameters, with respective default values of 0.5 and 0.1, define the bounds for "strong" and "weak" ratings.

The rating status is determined as follows:

Rating Value Rating Status

< -strongBound Strong Sell

< -weakBound Sell

-weakBound to weakBound Neutral

> weakBound Buy

> strongBound Strong Buy

By customizing the `strongBound` and `weakBound` values, traders can tailor the `ratingStatus()` function to fit their trading style or strategy, leading to a more personalized approach to evaluating ratings.

Look first. Then leap.

█ FUNCTIONS

This library contains the following functions:

calcRatingAll()

Calculates 3 ratings (ratings total, MA ratings, indicator ratings) using the aggregate biases of 26 different technical indicators.

Returns: A 3-element tuple: ( [(float) ratingTotal, (float) ratingOther, (float) ratingMA ].

countRising(plot)

Calculates the number of times the values in the given series increase in value up to a maximum count of 5.

Parameters:

plot : (series float) The series of values to check for rising values.

Returns: (int) The number of times the values in the series increased in value.

ratingStatus(ratingValue, strongBound, weakBound)

Determines the rating status of a given series based on its values and defined bounds.

Parameters:

ratingValue : (series float) The series of values to determine the rating status for.

strongBound : (series float) The upper bound for a "strong" rating.

weakBound : (series float) The upper bound for a "weak" rating.

Returns: (string) The rating status of the given series ("Strong Buy", "Buy", "Neutral", "Sell", or "Strong Sell").

Oscillator Workbench — Chart [LucF]█ OVERVIEW

This indicator uses an on-chart visual framework to help traders with the interpretation of any oscillator's behavior. The advantage of using this tool is that you do not need to know all the ins and outs of a particular oscillator such as RSI, CCI, Stochastic, etc. Your choice of oscillator and settings in this indicator will change its visuals, which allows you to evaluate different configurations in the context of how the workbench models oscillator behavior. My hope is that by using the workbench, you may come up with an oscillator selection and settings that produce visual cues you find useful in your trading.

The workbench works on any symbol and timeframe. It uses the same presentation engine as my Delta Volume Channels indicator; those already familiar with it will feel right at home here.

█ CONCEPTS

Oscillators

An oscillator is any signal that moves up and down a centerline. The centerline value is often zero or 50. Because the range of oscillator values is different than that of the symbol prices we look at on our charts, it is usually impossible to display an oscillator on the chart, so we typically put oscillators in a separate pane where they live in their own space. Each oscillator has its own profile and properties that dictate its behavior and interpretation. Oscillators can be bounded , meaning their values oscillate between fixed values such as 0 to 100 or +1 to -1, or unbounded when their maximum and minimum values are undefined.

Oscillator weight

How do you display an oscillator's value on a chart showing prices when both values are not on the same scale? The method I use here converts the oscillator's value into a percentage that is used to weigh a reference line. The weight of the oscillator is calculated by maintaining its highest and lowest value above and below its centerline since the beginning of the chart's history. The oscillator's relative position in either of those spaces is then converted to a percentage, yielding a positive or negative value depending on whether the oscillator is above or below its centerline. This method works equally well with bounded and unbounded oscillators.

Oscillator Channel

The oscillator channel is the space between two moving averages: the reference line and a weighted version of that line. The reference line is a moving average of a type, source and length which you select. The weighted line uses the same settings, but it averages the oscillator-weighted price source.

The weight applied to the source of the reference line can also include the relative size of the bar's volume in relation to previous bars. The effect of this is that the oscillator's weight on bars with higher total volume will carry greater weight than those with lesser volume.

The oscillator channel can be in one of four states, each having its corresponding color: