Perp Imbalance Zones • Pro (clean)USD Premium (perp vs spot) → (Perp − Spot) / Spot.

Imbalance (z-score of that premium) → how extreme the current premium is relative to its own history over lenPrem bars.

Hysteresis state machine → flips to a SHORT bias when perp-long pressure is extreme; flips to LONG bias when perp-short pressure is extreme. It exits only after the imbalance cools (prevents whipsaw).

Price stretch filter (±σ) → optional Bollinger check so signals only fire when price is already stretched.

HTF confirmation (optional) → require higher-timeframe imbalance to agree with the current-TF bias.

Gradient visuals → line + background tint deepen as |z| grows (more extreme pressure).

What you see on the pane

A single line (z):

Above 0 = perp richer than spot (perp longs pressing).

Below 0 = perp cheaper than spot (perp shorts pressing).

Guides: dotted levels at ±enterZ (entry) and ±exitZ (cool-off/exit).

Background tint:

Red when state = SHORT bias (perp longs heavy).

Blue when state = LONG bias (perp shorts heavy).

Tint intensity scales with |z| (via hotZ).

Labels (optional): prints when bias flips.

Alerts (optional): “Enter SHORT/LONG bias” and “Exit bias”.

How to use it (playbook)

Attach & set symbols

Put the script on your chart.

Set Spot symbol and Perp symbol to the venue you trade (e.g., BINANCE:BTCUSDT + BINANCE:BTCUSDTPERP).

Read the bias

SHORT bias (red background): perp longs over-extended. Look for short entries if price is at resistance, σ-stretched, or your PA system agrees.

LONG bias (blue background): perp shorts over-extended. Look for long entries at support/σ-stretched down.

Entries

Use the bias flip as a context/confirm. Combine with your structure trigger (OB/level sweep, rejection wick, micro-break in market structure, etc.).

If useSigma=true, only trade when price is already ≥ upper band (shorts) or ≤ lower band (longs).

Exits

Bias auto-exits when |z| falls below exitZ.

You can also take profits at your levels or when the line fades back toward 0 while price mean-reverts to the middle band.

Tuning (what each knob does)

enterZ / exitZ (signal strictness + hysteresis)

Higher enterZ → fewer, cleaner signals (e.g., 1.8–2.2).

exitZ should be lower than enterZ (e.g., 0.6–1.0) to prevent flicker.

lenPrem (context window for z)

Larger (50–100) = steadier baseline, fewer signals.

Smaller (20–30) = more reactive, more signals.

smoothLen (EMA on z)

2–3 = snappier; 5–7 = smoother/laggier but cleaner.

useSigma, bbLen, bbK (price-stretch filter)

On filters chop. Try bbLen=100, bbK=1.0–1.5.

Off if you want more frequent signals or you already gate with your own σ/Keltner.

useHTF, htfTF, htfZmin (trend/confirmation)

Turn on to require higher-TF imbalance agreement (e.g., trading 1H → confirm with 4H htfTF=240, htfZmin≈0.6–1.0).

hotZ (visual intensity)

Lower (2.0–2.5) heats up faster; higher (4.0) is more subtle.

Ready-made presets

Conservative swing (fewer, higher-conviction):

enterZ=2.0, exitZ=1.0, lenPrem=60–80, smoothLen=5, useSigma=true, bbK=1.5, useHTF=true (240/0.8).

Balanced intraday (default feel):

enterZ=1.6–1.8, exitZ=0.8–1.0, lenPrem=50, smoothLen=3–4, useSigma=true, bbK=1.0–1.25, useHTF=false/true depending on trendiness.

Aggressive scalping (more signals):

enterZ=1.2–1.4, exitZ=0.6–0.8, lenPrem=20–30, smoothLen=2–3, useSigma=false, useHTF=false.

Practical tips

Don’t trade the line in isolation. Use it to time trades into your levels: VWAP bands, Monday high/low, prior POC/VAH/VAL, order blocks, etc.

Perp-led reversals often snap—be ready to scale out quickly back to mid-bands.

Venue matters. Keep spot & perp from the same exchange family to avoid cross-venue quirks.

Alerts: enable after you’ve tuned thresholds for your timeframe so you only get high-quality pings.

Recherche dans les scripts pour "股价在8元左右净利润为正市值小于80亿的热门股票有哪些"

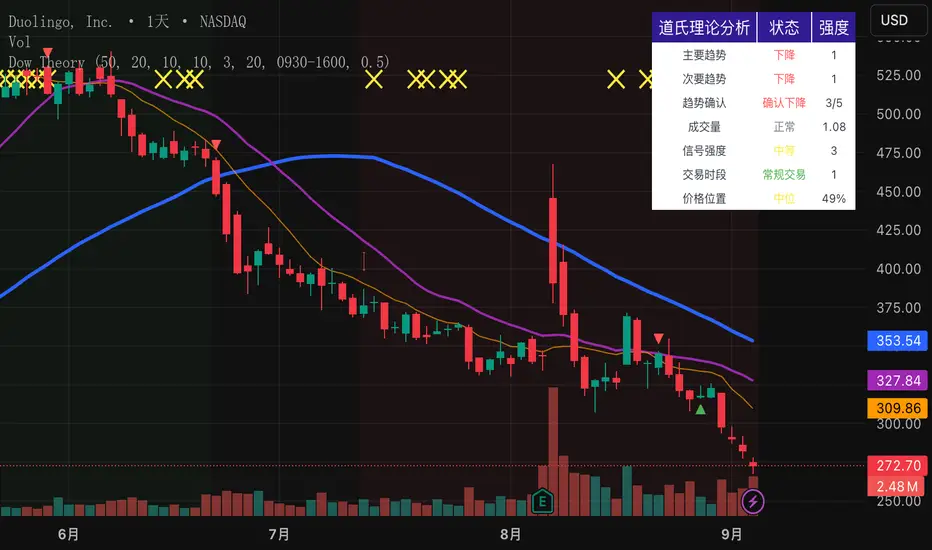

Dow Theory Indicator## 🎯 Key Features of the Indicator

### 📈 Complete Implementation of Dow Theory

- Three-tier trend structure: primary trend (50 periods), secondary trend (20 periods), and minor trend (10 periods).

- Swing point analysis: automatically detects critical swing highs and lows.

- Trend confirmation mechanism: strict confirmation logic based on consecutive higher highs/higher lows or lower highs/lower lows.

- Volume confirmation: ensures price moves are supported by trading volume.

### 🕐 Flexible Timeframe Parameters

All key parameters are adjustable, making it especially suitable for U.S. equities:

Trend analysis parameters:

- Primary trend period: 20–200 (default 50; recommended 50–100 for U.S. stocks).

- Secondary trend period: 10–100 (default 20; recommended 15–30 for U.S. stocks).

- Minor trend period: 5–50 (default 10; recommended 5–15 for U.S. stocks).

Dow Theory parameters:

- Swing high/low lookback: 5–50 (default 10).

- Trend confirmation bar count: 1–10 (default 3).

- Volume confirmation period: 10–100 (default 20).

### 🇺🇸 U.S. Market Optimizations

- Session awareness: distinguishes Regular Trading Hours (9:30–16:00 EST) from pre-market and after-hours.

- Pre/post-market weighting: adjustable weighting factor for signals during extended hours.

- Earnings season filter: automatically adjusts sensitivity during earnings periods.

- U.S.-optimized default parameters.

## 🎨 Visualization

1. Trend lines: three differently colored trend lines.

2. Background fill: green (uptrend) / red (downtrend) / gray (neutral).

3. Signal markers: arrows, labels, and warning icons.

4. Swing point markers: small triangles at key turning points.

5. Info panel: real-time display of eight key metrics.

## 🚨 Alert System

- Trend turning to up/down.

- Strong bullish/bearish signals (dual confirmation).

- Volume divergence warning.

- New swing high/low formed.

## 📋 How to Use

1. Open the Pine Editor in TradingView.

2. Copy the contents of dow_theory_indicator.pine.

3. Paste and click “Add to chart.”

4. Adjust parameters based on trading style:

- Long-term investing: increase all period parameters.

- Swing trading: use the default parameters.

- Short-term trading: decrease all period parameters.

## 💡 Parameter Tips for U.S. Stocks

- Large-cap blue chips (AAPL, MSFT): primary 60–80, secondary 25–30.

- Mid-cap growth stocks: primary 40–60, secondary 18–25.

- Small-cap high-volatility stocks: primary 30–50, secondary 15–20.

RSI Crossover AlertRSI Crossover Alert Indicator - User Guide

The RSI Crossover Alert Indicator is a comprehensive technical analysis tool that detects multiple types of RSI crossovers and generates real-time alerts. It combines traditional RSI analysis with signal lines, divergence detection, and multi-level crossing alerts.

1. Multiple Crossover Detection

- RSI/Signal Line Cross: Signals a primary trend change.

- RSI/Second Signal Cross: Confirmation signals for stronger trends.

- Level Crossings: Crosses of Overbought 70, Oversold 30, and Midline 50.

- Divergence Detection: Hidden and regular divergences for reversal signals.

2. Alert Types

- Alert: RSI > Signal

Description: Bullish momentum is building.

Signal: Consider long positions.

- Alert: RSI < Signal

Description: Bearish momentum is building.

Signal: Consider short positions.

- Alert: RSI > 70

Description: Entering the overbought zone.

Signal: Prepare for a potential reversal.

- Alert: RSI < 30

Description: Entering the oversold zone.

Signal: Watch for a bounce opportunity.

- Alert: RSI crosses 50

Description: A shift in momentum.

Signal: Trend confirmation.

3. Visual Components

- Lines: RSI blue, Signal orange, Second Signal purple

- Histogram: Visualizes momentum by showing the difference between RSI and the Signal line.

- Background Zones: Red overbought, Green oversold

- Markers: Up/down triangles to indicate crossovers.

- Info Table: Real-time RSI values and status.

Strategy 1: Classic Crossover

- Entry Long: RSI crosses above the Signal Line AND RSI is below 50.

- Entry Short: RSI crosses below the Signal Line AND RSI is above 50.

- Take Profit: On the opposite signal.

- Stop Loss: At the recent swing high/low.

Strategy 2: Extreme Zone Reversal

- Entry Long: RSI is below 30 and crosses above the Signal Line.

- Entry Short: RSI is above 70 and crosses below the Signal Line.

- Risk Management: Higher win rate but fewer signals. Use a minimum 2:1 risk-reward ratio.

Strategy 3: Divergence Trading

- Setup: Enable divergence alerts and look for price/RSI divergence. Wait for an RSI crossover for confirmation.

- Entry: Enter on the crossover after the divergence appears. Place the stop loss beyond the starting point of the divergence.

Strategy 4: Multi-Timeframe Confirmation

1. Check the higher timeframe e.g. Daily to identify the main trend.

2. Use the current timeframe e.g. 4H/1H for your entry.

3. Only enter in the direction of the main trend.

4. Use the RSI crossover as the entry trigger.

Optimal Settings by Market

- Forex Major Pairs

RSI Length: 14, Signal Length: 9, Overbought/Oversold: 70/30

- Crypto High Volatility

RSI Length: 10-12, Signal Length: 6-8, Overbought/Oversold: 75/25

- Stocks Trending

RSI Length: 14-21, Signal Length: 9-12, Overbought/Oversold: 70/30

- Commodities

RSI Length: 14, Signal Length: 9, Overbought/Oversold: 80/20

Risk Management Rules

1. Position Sizing: Never risk more than 1-2% on a single trade. Reduce size in ranging markets.

2. Stop Loss Placement: Place stops beyond the recent swing high/low for crossovers. Using an ATR-based stop is also effective.

3. Profit Taking: Take partial profits at a 1:1 risk-reward ratio. Switch to a trailing stop after reaching 2:1.

1. Filtering Signals

- Combine with volume indicators.

- Confirm the trend on a higher timeframe.

- Wait for candlestick pattern confirmation.

2. Avoid Common Mistakes

- Don't trade every single crossover.

- Avoid taking signals against a strong trend.

- Do not ignore risk management.

3. Market Conditions

- Trending Market: Focus on midline 50 crosses.

- Ranging Market: Look for reversals from overbought/oversold levels.

- Volatile Market: Widen the overbought/oversold levels.

- If you get too many false signals:

Increase the signal line period, add other confirmation indicators, or use a higher timeframe.

- If you are missing major moves:

Decrease the RSI length, shorten the signal line period, or check your alert settings.

Recommended Combinations

1. RSI + MACD: For dual momentum confirmation.

2. RSI + Bollinger Bands: For volatility-adjusted signals.

3. RSI + Volume: To confirm the strength of a signal.

4. RSI + Moving Averages: To use as a trend filter.

This indicator provides a comprehensive RSI analysis. Success depends on proper configuration, risk management, and combining signals with the overall market context. Start with the default settings, then optimize based on your trading style and market conditions.

Martingale Strategy Simulator [BackQuant]Martingale Strategy Simulator

Purpose

This indicator lets you study how a martingale-style position sizing rule interacts with a simple long or short trading signal. It computes an equity curve from bar-to-bar returns, adapts position size after losing streaks, caps exposure at a user limit, and summarizes risk with portfolio metrics. An optional Monte Carlo module projects possible future equity paths from your realized daily returns.

What a martingale is

A martingale sizing rule increases stake after losses and resets after a win. In its classical form from gambling, you double the bet after each loss so that a single win recovers all prior losses plus one unit of profit. In markets there is no fixed “even-money” payout and returns are multiplicative, so an exact recovery guarantee does not exist. The core idea is unchanged:

Lose one leg → increase next position size

Lose again → increase again

Win → reset to the base size

The expectation of your strategy still depends on the signal’s edge. Sizing does not create positive expectancy on its own. A martingale raises variance and tail risk by concentrating more capital as a losing streak develops.

What it plots

Equity – simulated portfolio equity including compounding

Buy & Hold – equity from holding the chart symbol for context

Optional helpers – last trade outcome, current streak length, current allocation fraction

Optional diagnostics – daily portfolio return, rolling drawdown, metrics table

Optional Monte Carlo probability cone – p5, p16, p50, p84, p95 aggregate bands

Model assumptions

Bar-close execution with no slippage or commissions

Shorting allowed and frictionless

No margin interest, borrow fees, or position limits

No intrabar moves or gaps within a bar (returns are close-to-close)

Sizing applies to equity fraction only and is capped by your setting

All results are hypothetical and for education only.

How the simulator applies it

1) Directional signal

You pick a simple directional rule that produces +1 for long or −1 for short each bar. Options include 100 HMA slope, RSI above or below 50, EMA or SMA crosses, CCI and other oscillators, ATR move, BB basis, and more. The stance is evaluated bar by bar. When the stance flips, the current trade ends and the next one starts.

2) Sizing after losses and wins

Position size is a fraction of equity:

Initial allocation – the starting fraction, for example 0.15 means 15 percent of equity

Increase after loss – multiply the next allocation by your factor after a losing leg, for example 2.00 to double

Reset after win – return to the initial allocation

Max allocation cap – hard ceiling to prevent runaway growth

At a high level the size after k consecutive losses is

alloc(k) = min( cap , base × factor^k ) .

In practice the simulator changes size only when a leg ends and its PnL is known.

3) Equity update

Let r_t = close_t / close_{t-1} − 1 be the symbol’s bar return, d_{t−1} ∈ {+1, −1} the prior bar stance, and a_{t−1} the prior bar allocation fraction. The simulator compounds:

eq_t = eq_{t−1} × (1 + a_{t−1} × d_{t−1} × r_t) .

This is bar-based and avoids intrabar lookahead. Costs, slippage, and borrowing costs are not modeled.

Why traders experiment with martingale sizing

Mean-reversion contexts – if the signal often snaps back after a string of losses, adding size near the tail of a move can pull the average entry closer to the turn

Behavioral or microstructure edges – some rules have modest edge but frequent small whipsaws; size escalation may shorten time-to-recovery when the edge manifests

Exploration and stress testing – studying the relationship between streaks, caps, and drawdowns is instructive even if you do not deploy martingale sizing live

Why martingale is dangerous

Martingale concentrates capital when the strategy is performing worst. The main risks are structural, not cosmetic:

Loss streaks are inevitable – even with a 55 percent win rate you should expect multi-loss runs. The probability of at least one k-loss streak in N trades rises quickly with N.

Size explodes geometrically – with factor 2.0 and base 10 percent, the sequence is 10, 20, 40, 80, 100 (capped) after five losses. Without a strict cap, required size becomes infeasible.

No fixed payout – in gambling, one win at even odds resets PnL. In markets, there is no guaranteed bounce nor fixed profit multiple. Trends can extend and gaps can skip levels.

Correlation of losses – losses cluster in trends and in volatility bursts. A martingale tends to be largest just when volatility is highest.

Margin and liquidity constraints – leverage limits, margin calls, position limits, and widening spreads can force liquidation before a mean reversion occurs.

Fat tails and regime shifts – assumptions of independent, Gaussian returns can understate tail risk. Structural breaks can keep the signal wrong for much longer than expected.

The simulator exposes these dynamics in the equity curve, Max Drawdown, VaR and CVaR, and via Monte Carlo sketches of forward uncertainty.

Interpreting losing streaks with numbers

A rough intuition: if your per-trade win probability is p and loss probability is q=1−p , the chance of a specific run of k consecutive losses is q^k . Over many trades, the chance that at least one k-loss run occurs grows with the number of opportunities. As a sanity check:

If p=0.55 , then q=0.45 . A 6-loss run has probability q^6 ≈ 0.008 on any six-trade window. Across hundreds of trades, a 6 to 8-loss run is not rare.

If your size factor is 1.5 and your base is 10 percent, after 8 losses the requested size is 10% × 1.5^8 ≈ 25.6% . With factor 2.0 it would try to be 10% × 2^8 = 256% but your cap will stop it. The equity curve will still wear the compounded drawdown from the sequence that led to the cap.

This is why the cap setting is central. It does not remove tail risk, but it prevents the sizing rule from demanding impossible positions

Note: The p and q math is illustrative. In live data the win rate and distribution can drift over time, so real streaks can be longer or shorter than the simple q^k intuition suggests..

Using the simulator productively

Parameter studies

Start with conservative settings. Increase one element at a time and watch how the equity, Max Drawdown, and CVaR respond.

Initial allocation – lower base reduces volatility and drawdowns across the board

Increase factor – set modestly above 1.0 if you want the effect at all; doubling is aggressive

Max cap – the most important brake; many users keep it between 20 and 50 percent

Signal selection

Keep sizing fixed and rotate signals to see how streak patterns differ. Trend-following signals tend to produce long wrong-way streaks in choppy ranges. Mean-reversion signals do the opposite. Martingale sizing interacts very differently with each.

Diagnostics to watch

Use the built-in metrics to quantify risk:

Max Drawdown – worst peak-to-trough equity loss

Sharpe and Sortino – volatility and downside-adjusted return

VaR 95 percent and CVaR – tail risk measures from the realized distribution

Alpha and Beta – relationship to your chosen benchmark

If you would like to check out the original performance metrics script with multiple assets with a better explanation on all metrics please see

Monte Carlo exploration

When enabled, the forecast draws many synthetic paths from your realized daily returns:

Choose a horizon and a number of runs

Review the bands: p5 to p95 for a wide risk envelope; p16 to p84 for a narrower range; p50 as the median path

Use the table to read the expected return over the horizon and the tail outcomes

Remember it is a sketch based on your recent distribution, not a predictor

Concrete examples

Example A: Modest martingale

Base 10 percent, factor 1.25, cap 40 percent, RSI>50 signal. You will see small escalations on 2 to 4 loss runs and frequent resets. The equity curve usually remains smooth unless the signal enters a prolonged wrong-way regime. Max DD may rise moderately versus fixed sizing.

Example B: Aggressive martingale

Base 15 percent, factor 2.0, cap 60 percent, EMA cross signal. The curve can look stellar during favorable regimes, then a single extended streak pushes allocation to the cap, and a few more losses drive deep drawdown. CVaR and Max DD jump sharply. This is a textbook case of high tail risk.

Strengths

Bar-by-bar, transparent computation of equity from stance and size

Explicit handling of wins, losses, streaks, and caps

Portable signal inputs so you can A–B test ideas quickly

Risk diagnostics and forward uncertainty visualization in one place

Example, Rolling Max Drawdown

Limitations and important notes

Martingale sizing can escalate drawdowns rapidly. The cap limits position size but not the possibility of extended adverse runs.

No commissions, slippage, margin interest, borrow costs, or liquidity limits are modeled.

Signals are evaluated on closes. Real execution and fills will differ.

Monte Carlo assumes independent draws from your recent return distribution. Markets often have serial correlation, fat tails, and regime changes.

All results are hypothetical. Use this as an educational tool, not a production risk engine.

Practical tips

Prefer gentle factors such as 1.1 to 1.3. Doubling is usually excessive outside of toy examples.

Keep a strict cap. Many users cap between 20 and 40 percent of equity per leg.

Stress test with different start dates and subperiods. Long flat or trending regimes are where martingale weaknesses appear.

Compare to an anti-martingale (increase after wins, cut after losses) to understand the other side of the trade-off.

If you deploy sizing live, add external guardrails such as a daily loss cut, volatility filters, and a global max drawdown stop.

Settings recap

Backtest start date and initial capital

Initial allocation, increase-after-loss factor, max allocation cap

Signal source selector

Trading days per year and risk-free rate

Benchmark symbol for Alpha and Beta

UI toggles for equity, buy and hold, labels, metrics, PnL, and drawdown

Monte Carlo controls for enable, runs, horizon, and result table

Final thoughts

A martingale is not a free lunch. It is a way to tilt capital allocation toward losing streaks. If the signal has a real edge and mean reversion is common, careful and capped escalation can reduce time-to-recovery. If the signal lacks edge or regimes shift, the same rule can magnify losses at the worst possible moment. This simulator makes those trade-offs visible so you can calibrate parameters, understand tail risk, and decide whether the approach belongs anywhere in your research workflow.

Ultra Volume DetectorNative Volume — Auto Levels + Ultra Label

What it does

This indicator classifies volume bars into four categories — Low, Medium, High, and Ultra — using rolling percentile thresholds. Instead of fixed cutoffs, it adapts dynamically to recent market activity, making it useful across different symbols and timeframes. Ultra-high volume bars are highlighted with labels showing compacted values (K/M/B/T) and the appropriate unit (shares, contracts, ticks, etc.).

Core Logic

Dynamic thresholds: Calculates percentile levels (e.g., 50th, 80th, 98th) over a user-defined window of bars.

Categorization: Bars are colored by category (Low/Med/High/Ultra).

Ultra labeling: Only Ultra bars are labeled, preventing chart clutter.

Optional MA: A moving average of raw volume can be plotted for context.

Alerts: Supports both alert condition for Ultra events and dynamic alert() messages that include the actual volume value at bar close.

How to use

Adjust window size: Larger windows (e.g., 200+) provide stable thresholds; smaller windows react more quickly.

Set percentiles: Typical defaults are 50 for Medium, 80 for High, and 98 for Ultra. Lower the Ultra percentile to see more frequent signals, or raise it to isolate only extreme events.

Read chart signals:

Bar colors show the category.

Labels appear only on Ultra bars.

Alerts can be set up for automatic notification when Ultra volume occurs.

Why it’s unique

Adaptive: Uses rolling statistics, not static thresholds.

Cross-asset ready: Adjusts units automatically depending on instrument type.

Efficient visualization: Focuses labels only on the most significant events, reducing noise.

⚠️ Disclaimer: This tool is for educational and analytical purposes only. It does not provide financial advice. Always test and manage risk before trading live

BTC Power-Law Decay Channel Oscillator (0–100)🟠 BTC Power-Law Decay Channel Oscillator (0–100)

This indicator calculates Bitcoin’s position inside its long-term power-law decay channel and normalizes it into an easy-to-read 0–100 oscillator.

🔎 Concept

Bitcoin’s long-term price trajectory can be modeled by a log-log power-law channel.

A baseline is fitted, then an upper band (excess/euphoria) and a lower band (capitulation/fear).

The oscillator shows where the current price sits between those bands:

0 = near the lower band (historical bottoms)

100 = near the upper band (historical tops)

📊 How to Read

Oscillator > 80 → euphoric excess, often cycle tops

Oscillator < 20 → capitulation, often cycle bottoms

Works best on weekly or bi-weekly timeframes.

⚙️ Adjustable Parameters

Anchor date: starting point for the power-law fit (default: 2011).

Smoothing days: moving average applied to log-price (default: 365 days).

Upper / Lower multipliers: scale the bands to align with historical highs and lows.

✅ Best Use

Combine with other cycle signals (dominance ratios, macro indicators, sentiment).

Designed for long-term cycle analysis, not intraday trading.

Full Stochastic (TC2000-style EMA 5,3,3)Full Stochastic (TC2000-style EMA 5,3,3) computes a Full Stochastic oscillator matching TC2000’s settings with Average Type = Exponential.

Raw %K is calculated over K=5, then smoothed by an EMA with Slowing=3 to form the Full %K, and %D is an EMA of Full %K with D=3.

Plots:

%K in black, %D in red, with 80/20 overbought/oversold levels in green.

This setup emphasizes momentum shifts while applying EMA smoothing at both stages to reduce noise and maintain responsiveness. Inputs are adjustable to suit different symbols and timeframes.

Radial Basis Kernel RSI for LoopRadial Basis Kernel RSI for Loop

What it is

An RSI-style oscillator that uses a radial basis function (RBF) kernel to compute a similarity-weighted average of gains and losses across many lookback lengths and kernel widths (γ). By averaging dozens of RSI estimates—each built with different parameters—it aims to deliver a smoother, more robust momentum signal that adapts to changing market conditions.

How it works

The script measures up/down price changes from your chosen Source (default: close).

For each combination of RSI length and Gamma (γ) in your ranges, it builds an RSI where recent bars that look most similar (by price behavior) get more weight via an RBF kernel.

It averages all those RSIs into a single value, then smooths it with your selected Moving Average type (SMA, EMA, WMA, HMA, DEMA) and a light regression-based filter for stability.

Inputs you can tune

Min/Max RSI Kernel Length & Step: Range of RSI lookbacks to include in the ensemble (e.g., 20→40 by 1) or (e.g., 30→50 by 1).

Min/Max Gamma & Step: Controls the RBF “width.” Lower γ = broader similarity (smoother); higher γ = more selective (snappier).

Source: Price series to analyze.

Overbought / Oversold levels: Defaults 70 / 30, with a midline at 50. Shaded regions help visualize extremes.

MA Type & Period (Confluence): Final smoothing on the averaged RSI line (e.g., DEMA(44) by default).

Red “OB” labels when the line crosses down from extreme highs (~80) → potential overbought fade/exit areas.

Green “OS” labels when the line crosses up from extreme lows (~20) → potential oversold bounce/entry areas.

How to use it

Treat it like RSI, but expect fewer whipsaws thanks to the ensemble and kernel weighting.

Common approaches:

Look for crosses back inside the bands (e.g., down from >70 or up from <30).

Use the 50 midline for directional bias (above = bullish momentum tilt; below = bearish).

Combine with trend filters (e.g., your chart MA) for higher-probability signals.

Performance note: This is really heavy and depending on how much time your subscription allows you could experience this timing out. Increasing the step size is the easiest way to reduce the load time.

Works on any symbol or timeframe. Like any oscillator, best used alongside price action and risk management rather than in isolation.

ForecastForecast (FC), indicator documentation

Type: Study, not a strategy

Primary timeframe: 1D chart, most plots and the on-chart table only render on daily bars

Inspiration: Robert Carver’s “forecast” concept from Advanced Futures Trading Strategies, using normalized, capped signals for comparability across markets

⸻

What the indicator does

FC builds a volatility-normalized momentum forecast for a chosen symbol, optionally versus a benchmark. It combines an EWMAC composite with a channel breakout composite, then caps the result to a common scale. You can run it in three data modes:

• Absolute: Forecast of the selected symbol

• Relative: Forecast of the ratio symbol / benchmark

• Combined: Average of Absolute and Relative

A compact table can summarize the current forecast, short-term direction on the forecast EMAs, correlation versus the benchmark, and ATR-scaled distances to common price EMAs.

⸻

PineScreener, relative-strength screening

This indicator is excellent for screening on relative strength in PineScreener, since the forecast is volatility-normalized and capped on a common scale.

Available PineScreener columns

PineScreener reads the plotted series. You will see at least these columns:

• FC, the capped forecast

• from EMA20, (price − EMA20) / ATR in ATR multiples

• from EMA50, (price − EMA50) / ATR in ATR multiples

• ATR, ATR as a percent of price

• Corr, weekly correlation with the chosen benchmark

Relative mode and Combined mode are recommended for cross-sectional screens. In Relative mode the calculation uses symbol / benchmark, so ensure the ratio ticker exists for your data source.

⸻

How it works, step by step

1. Volatility model

Compute exponentially weighted mean and variance of daily percent returns on D, annualize, optionally blend with a long lookback using 10y %, then convert to a price-scaled sigma.

2. EWMAC momentum, three legs

Daily legs: EMA(8) − EMA(32), EMA(16) − EMA(64), EMA(32) − EMA(128).

Divide by price-scaled sigma, multiply by leg scalars, cap to Cap = 20, average, then apply a small FDM factor.

3. Breakout momentum, three channels

Smoothed position inside 40, 80, and 160 day channels, each scaled, then averaged.

4. Composite forecast

Average the EWMAC composite and the breakout composite, then cap to ±20.

Relative mode runs the same logic on symbol / benchmark.

Combined mode averages Absolute and Relative composites.

5. Weekly correlation

Pearson correlation between weekly closes of the asset and the benchmark over a user-set length.

6. Direction overlay

Two EMAs on the forecast series plus optional green or red background by sign, and optional horizontal level shading around 0, ±5, ±10, ±15, ±20.

⸻

Plots

• FC, capped forecast on the daily chart

• 8-32 Abs, 8-32 Rel, single-leg EWMAC plus breakout view

• 8-32-128 Abs, 8-32-128 Rel, three-leg composite views

• from EMA20, from EMA50, (price − EMA) / ATR

• ATR, ATR as a percent of price

• Corr, weekly correlation with the benchmark

• Forecast EMA1 and EMA2, EMAs of the forecast with an optional fill

• Backgrounds and guide lines, optional sign-based background, optional 0, ±5, ±10, ±15, ±20 guides

Most plots and the table are gated by timeframe.isdaily. Set the chart to 1D to see them.

⸻

Inputs

Symbol selection

• Absolute, Relative, Combined

• Vs. benchmark for Relative mode and correlation, choices: SPY, QQQ, XLE, GLD

• Ticker or Freeform, for Freeform use full TradingView notation, for example NASDAQ:AAPL

Engine selection

• Include:

• 8-32-128, three EWMAC legs plus three breakouts

• 8-32, simplified view based on the 8-32 leg plus a 40-day breakout

EMA, applied to the forecast

• EMA1, EMA2, with line-width controls, plus color and opacity

Volatility

• Span, EW volatility span for daily returns

• 10y %, blend of long-run volatility

• Thresh, Too volatile, placeholders in this version

Background

• Horizontal bg, level shading, enabled by default

• Long BG, Hedge BG, colors and opacities

Show

• Table, Header, Direction, Gain, Extension

• Corr, Length for correlation row

Table settings

• Position, background, opacity, text size, text color

Lines

• 0-lines, 10-lines, 5-lines, level guides

⸻

Reading the outputs

• Forecast > 0, bullish tilt; Forecast < 0, bearish or hedge tilt

• ±10 and ±20 indicate strength on a uniform scale

• EMA1 vs EMA2 on the forecast, EMA1 above EMA2 suggests improving momentum

• Table rows, label colored by sign, current forecast value plus a green or red dot for the forecast EMA cross, optional daily return percent, weekly correlation, and ATR-scaled EMA9, EMA20, EMA50 distances

⸻

Data handling, repainting, and performance

• Daily and weekly series are fetched with request.security().

• Calculations use closed bars, values can update until the bar closes.

• No lookahead, historical values do not repaint.

• Weekly correlation updates during the week, it finalizes on weekly close.

• On intraday charts most visuals are hidden by design.

⸻

Good practice and limitations

• This is a research indicator, not a trading system.

• The fixed Cap = 20 keeps a common scale, extreme moves will be clipped.

• Relative mode depends on the ratio symbol / benchmark, ensure both legs have data for your feed.

⸻

Credits

Concept inspired by Robert Carver’s forecast methodology in Advanced Futures Trading Strategies. Implementation details, parameters, and visuals are specific to this script.

⸻

Changelog

• First version

⸻

Disclaimer

For education and research only, not financial advice. Always test on your market and data feed, consider costs and slippage before using any indicator in live decisions.

Market Imbalance Tracker (Inefficient Candle + FVG)# 📊 Overview

This indicator combines two imbalance concepts:

• **Squared Up Points (SUP)** – midpoints of large, "inefficient" candles that often attract price back.

• **Fair Value Gaps (FVG)** – 3-candle gaps created by strong impulse moves that often get "filled."

Use them separately or together. Confluence between a SUP line and an FVG boundary/midpoint is high-value.

---

# ⚡ Quick Start (2 minutes)

1. **Add to chart** → keep defaults (Percentile method, 80th percentile, 100-bar lookback).

2. **Watch** for dashed SUP lines to print after large candles.

3. **Toggle Show FVG** → see green/red boxes where gaps exist.

4. **Turn on alerts** → New SUP created, SUP touched, New FVG.

5. **Trade the reaction** → look for confluence (SUP + FVG + S/R), then manage risk.

---

# 🛠 Features

## 🔹 Squared Up Points (SUP)

• **Purpose:** Midpoint of a large candle → potential support/resistance magnet.

• **Detection:** Choose *Percentile* (adaptive) or *ATR Multiple* (absolute).

• **Validation:** Only plots if the preceding candle does not touch the midpoint (with tolerance).

• **Lifecycle:** Line auto-extends into the future; it's removed when touched or aged out.

• **Visual:** Horizontal dashed line (color/width configurable; style fixed to dashed if not exposed).

## 🔹 Fair Value Gaps (FVG)

• **Purpose:** 3-candle gaps from an impulse; price often revisits to "fill."

• **Detection:** Requires a strong directional candle (Marubozu threshold) creating a gap.

• **Types:**

- **Bullish FVG (Green):** Gap below; expectation is downward fill.

- **Bearish FVG (Red):** Gap above; expectation is upward fill.

• **Close Rules (if implemented):**

- *Full Fill:* Gap closes when the opposite boundary is tagged.

- *Midpoint Fill:* Gap closes when its midpoint is tagged.

• **Visual:** Colored boxes; optional split-coloring to emphasize the midpoint.

> **Note:** If a listed FVG option isn't visible in Inputs, you're on a lighter build; use the available switches.

---

# ⚙️ Settings

## SUP Settings

• **Candle Size Method:** Percentile (top X% of recent ranges) or ATR Multiple.

• **Candle Size Percentile:** e.g., 80 → top 20% largest candles.

• **ATR Multiple & Period:** e.g., 1.5 × ATR(14).

• **Percentile Lookback:** Bars used to compute percentile.

• **Lookback Period:** How long SUP lines remain eligible before auto-cleanup.

• **Touch Tolerance (%):** Buffer based on the inefficient candle's range (0% = exact touch).

## Line Appearance

• **Line Color / Width:** Customizable.

• **Style:** Dashed (fixed unless you expose a style input).

## FVG Settings (if present in your build)

• **Show FVG:** On/Off.

• **Close Method:** Full Fill or Midpoint.

• **Marubozu Wick Tolerance:** Max wick % of the impulse bar.

• **Use Split Coloring:** Two-tone box halves around midpoint.

• **Colors:** Bullish/Bearish, and upper/lower halves (if split).

• **Max FVG Age:** Auto-remove older gaps.

---

# 📈 How to Use

## Trading Applications

• **SUP Lines:** Expect reaction on first touch; use as S/R or profit-taking magnets.

• **FVG Fills:** Price frequently tags the midpoint/boundary before continuing.

• **Confluence:** SUP at an FVG midpoint/boundary + higher-timeframe S/R = higher quality.

• **Bias:** Clusters of unfilled FVGs can hint at path of least resistance.

## Best Practices

• **Timeframe:** HTFs for swing levels, LTFs for execution.

• **Volume:** High volume at level = stronger signal.

• **Context:** Trade with broader trend or at least avoid counter-trend without confirmation.

• **Risk:** Always pre-define invalidation; structures fail in chop.

---

# 🔔 Alerts

• **New SUP Created** – When a qualifying inefficient candle prints a SUP midpoint.

• **SUP Touched/Invalidated** – When price touches within tolerance.

• **New FVG Detected** – When a valid gap forms per your rules.

> **Tip:** Set alerts *Once Per Bar Close* on HTFs; *Once* on LTFs to avoid noise.

---

# 🧑💻 Technical Notes

• **Percentile vs ATR:** Percentile adapts to volatility; ATR gives consistency for backtesting.

• **FVG Direction Logic:** Gap above price = bearish (expect up-fill); below = bullish (expect down-fill).

• **Performance:** Limits on lines/boxes and auto-aging keep things snappy.

---

# ⚠️ Limitations

• Imbalances are **context tools**, not signals by themselves.

• Works best with trend or clear impulses; expect noise in narrow ranges.

• Lower-timeframe gaps can be plentiful and lower quality.

---

# 📌 Version & Requirements

• **Pine Script v6**

• Heavy drawings may require **TradingView Pro** or higher (object limits).

---

*For best results, combine with your existing trading strategy and proper risk management.*

Renko WPR Color ChangerChanges color when williams percent R is between 0 and -20 or when between -80 and -100. Works with renko, HA and regular candles. Can change color.

Guitar Hero [theUltimator5]The Guitar Hero indicator transforms traditional oscillator signals into a visually engaging, game-like display reminiscent of the popular Guitar Hero video game. Instead of standard line plots, this indicator presents oscillator values as colored segments or blocks, making it easier to quickly identify market conditions at a glance.

Choose from 8 different technical oscillators:

RSI (Relative Strength Index)

Stochastic %K

Stochastic %D

Williams %R

CCI (Commodity Channel Index)

MFI (Money Flow Index)

TSI (True Strength Index)

Ultimate Oscillator

Visual Display Modes

1) Boxes Mode : Creates distinct rectangular boxes for each bar, providing a clean, segmented appearance. (default)

This visual display is limited by the amount of box plots that TradingView allows on each indictor, so it will only plot a limited history. If you want to view a similar visual display that has minor breaks between boxes, then use the fill mode.

2) Fill Mode : Uses filled areas between plot boundaries.

Use this mode when you want to view the plots further back in history without the strict drawing limitations.

Five-Level Color-Coded System

The indicator normalizes all oscillator values to a 0-100 scale and categorizes them into five distinct levels:

Level 1 (Red): Very Oversold (0-19)

Level 2 (Orange): Oversold (20-29)

Level 3 (Yellow): Neutral (30-70)

Level 4 (Aqua): Overbought (71-80)

Level 5 (Lime): Very Overbought (81-100)

Customization Options

Signal Parameters

Signal Length: Primary period for oscillator calculation (default: 14)

Signal Length 2: Secondary period for Stochastic %D and TSI (default: 3)

Signal Length 3: Tertiary period for TSI calculation (default: 25)

Display Controls

Show Horizontal Reference Lines: Toggle grid lines for better level identification

Show Information Table: Display current signal type, value, and normalized value

Table Position: Choose from 9 different screen positions for the info table

Display Mode: Switch between Boxes and Fills visualization

Max Bars to Display: Control how many historical bars to show (50-450 range)

Normalization Process

The indicator automatically normalizes different oscillator ranges to a consistent 0-100 scale:

Williams %R: Converts from -100/0 range to 0-100

CCI: Maps typical -300/+300 range to 0-100

TSI: Transforms -100/+100 range to 0-100

Other oscillators: Already use 0-100 scale (RSI, Stochastic, MFI, Ultimate Oscillator)

This was designed as an educational tool

The gamified approach makes learning about oscillators more engaging for new traders.

Six Meridian Divine Swords [theUltimator5]The Six Meridian Divine Sword is a legendary martial arts technique in the classic wuxia novel “Demi-Gods and Semi-Devils” (天龙八部) by Jin Yong (金庸). The technique uses powerful internal energy (qi) to shoot invisible sword-like energy beams from the six meridians of the hand. Each of the six fingers/meridians corresponds to a “sword,” giving six different sword energies.

The Six Meridian Divine Swords indicator is a compact “signal dashboard” that fuses six classic indicators (fingers)—MACD, KDJ, RSI, LWR (Williams %R), BBI, and MTM—into one pane. Each row is a traffic-light dot (green/bullish, red/bearish, gray/neutral). When all six align, the script draws a confirmation line (“All Bullish” or “All Bearish”). It’s designed for quick consensus reads across trend, momentum, and overbought/oversold conditions.

How to Read the Dashboard

The pane has 6 horizontal rows (explained in depth later):

MACD

KDJ

RSI

LWR (Larry Williams %R)

BBI (Bull & Bear Index)

MTM (Momentum)

Each tick in the row is a dot, with sentiment identified by a color.

Green = bullish condition met

Red = bearish condition met

Gray = inside a neutral band (filtering chop), shown when Use Neutral (Gray) Colors is ON

There are two lines that track the dots on the top or bottom of the pane.

All Bullish Signal Line: appears only if all 6 are strongly bullish (default color = white)

All Bearish Signal Line: appears only if all 6 are strongly bearish (default color = fuchsia)

The Six Meridians (Indicators) — What They Mean:

1) MACD — Trend & Momentum

What it is: A trend-following momentum indicator based on the relationship between two moving averages (typically 12-EMA and 26-EMA)

Logic used: Classic MACD line (EMA12−EMA26) vs its 9-EMA signal.

Bullish: MACD > Signal and |MACD−Signal| > Neutral Threshold

Bearish: MACD < Signal and |diff| > threshold

Neutral: |diff| ≤ threshold

Why: Small crosses can whipsaw. The neutral band ignores tiny separations to reduce noise.

Inputs: Fast/Slow/Signal lengths, Neutral Threshold.

2) KDJ — Stochastic with J-line boost

What it is: A variation of the stochastic oscillator popular in Chinese trading systems

Logic used: K = SMA(Stochastic, smooth), D = SMA(K, smooth), J = 3K − 2D.

Bullish: K > D and |K−D| > 2

Bearish: K < D and |K−D| > 2

Neutral: |K−D| ≤ 2

Why: K–D separation filters tiny wiggles; J offers an “extreme” early-warning context in the value label.

Inputs: Length, Smoothing.

3) RSI — Momentum balance (0–100)

What it is: A momentum oscillator measuring speed and magnitude of price changes (0–100)

Logic used: RSI(N).

Bullish: RSI > 50 + Neutral Zone

Bearish: RSI < 50 − Neutral Zone

Neutral: Between those bands

Why: Centerline/adaptive bands (around 50) give a directional bias without relying on fixed 70/30.

Inputs: Length, Neutral Zone (± around 50).

4) LWR (Williams %R) — Overbought/Oversold

What it is: An oscillator similar to stochastic, measuring how close the close is to the high-low range over N periods

Logic used: %R over N bars (0 to −100).

Bullish: %R > −50 + Neutral Zone

Bearish: %R < −50 − Neutral Zone

Neutral: Between those bands

Why: Uses a centered band around −50 instead of only −20/−80, making it act like a directional filter.

Inputs: Length, Neutral Zone (± around −50).

5) BBI (Bull & Bear Index) — Smoothed trend bias

What it is: A composite moving average, essentially the average of several different moving averages (often 3, 6, 12, 24 periods)

Logic used: Average of 4 SMAs (3/6/12/24 by default):

BBI = (MA3 + MA6 + MA12 + MA24) / 4

Bullish: Close > BBI and |Close−BBI| > 0.2% of BBI

Bearish: Close < BBI and |diff| > threshold

Neutral: |diff| ≤ threshold

Why: Multiple MAs blended together reduce single-MA whipsaw. A dynamic 0.2% band ignores tiny drift.

Inputs: 4 lengths (default 3/6/12/24). Threshold is auto-scaled at 0.2% of BBI.

6) MTM (Momentum) — Rate of change in price

What it is: A simple measure of rate of change

Logic used: MTM = Close − Close

Bullish: MTM > 0.5% of Close

Bearish: MTM < −0.5% of Close

Neutral: |MTM| ≤ threshold

Why: A percent-based gate adapts across prices (e.g., $5 vs $500) and mutes insignificant moves.

Inputs: Length. Threshold auto-scaled to 0.5% of current Close.

Display & Inputs You Can Tweak

🎨 Use Neutral (Gray) Colors

ON (default): 3-color mode with clear “no-trade”/“weak” states.

OFF: classic binary (green/red) without neutral filtering.

Capiba Custom RSI with Divergences v2

🇬🇧 English

Summary

This indicator is an enhanced and customizable version of the classic RSI, designed to provide clearer and more powerful trading signals. It combines an alternative, more price-sensitive RSI calculation with an automatic divergence detection, which is one of the most effective tools for predicting trend reversals and finding high-probability entry and exit points.

Built upon the compilation of knowledge and open-source codes from the community, this script has been refined to be an all-in-one tool for traders who base their strategies on momentum and trend exhaustion.

Key Features and How to Use

Ultimate RSI and Signal Line (Momentum)

What it is: The main indicator (white line) is an RSI variation that reacts more dynamically to changes in price volatility. It is accompanied by a signal line (orange, by default), which is a moving average of the RSI itself, serving to smooth the indicator and generate crossover signals.

How to use for Entries/Exits:

Buy Signal (Short-Term): Crossover of the RSI line (white) above the signal line (orange).

Sell Signal (Short-Term): Crossover of the RSI line (white) below the signal line (orange). These are momentum signals, ideal for confirming a trend or for scalping.

Automatic Divergence Detection (Reversal Signals) This is the most powerful feature of the indicator. A divergence occurs when the price moves in one direction and the momentum indicator moves in the opposite direction, signaling a likely exhaustion of the current trend.

Bullish Divergence (Green Line):

What it is: The price makes a lower low, but the RSI makes a higher low.

Meaning: Selling pressure is decreasing. It is a strong signal of a potential market bottom and an excellent entry opportunity for a long position.

Bearish Divergence (Red Line):

What it is: The price makes a higher high, but the RSI makes a lower high.

Meaning: Buying pressure is losing strength. It is a strong signal of a potential market top and an excellent exit opportunity for a long position or an entry for a short position.

Customizable Overbought & Oversold Levels

The horizontal lines (default 80 and 20) and the colored areas show when the asset is overextended to the upside (overbought) or downside (oversold), helping to contextualize the divergence and crossover signals.

Recommended Strategy

For maximum effectiveness, combine the signals:

High-Probability Entry (Buy): Look for a Bullish Divergence (green line) forming in the oversold zone. Confirm the entry when the RSI line crosses above its signal line.

High-Probability Exit (Sell): Look for a Bearish Divergence (red line) forming in the overbought zone. Confirm the exit or new short entry when the RSI line crosses below its signal line.

Acknowledgements

This indicator was developed by compiling and customizing excellent open-source ideas and codes shared by the TradingView community. Special thanks to everyone who contributes to the advancement of technical analysis.

Extended CANSLIM Indicator❖ Extended CANSLIM Indicator.

The Extended CANSLIM indicator is an indicator that concentrates all the tools usually used by CANSLIM traders.

It shows a table where all the stock fundamental information is shown at once first for the last quarter and then up to 5 years back.

The fundamental data is checked against well known CANSLIM validation criteria and is shown over 4 state levels.

1. Good = Value is CANSLIM Compliant.

2. Acceptable = Value is not CANSLIM compliant but still good. value is shown with a lighter background color.

3. Warning = Value deserves special attention. Value is shown over orange background color.

3. Stop = Value is non CANSLIM compliant or indicates a stop trading condition. Value is shown over red background color.

The indicator has also a set of technical tools calculated on price or index and shown directly on the chart.

❖ Fundamental data shown in the table.

The table is arranged in 4 sets of data:

1. Table Header, showing Indicator and Company data.

2. CANSLIM.

3. 3Rs: RS Rating, Revenue and ROE.

4. Extra Data: Piotroski score, ATR, Trend Days, D to E, Avg Vol and Vol today.

Sets 3 and 4 can be hidden from the table.

❖ Indicator and Compay Data.

The table header shows, Indicator name and version.

It then displays Company Name, sector and industry, human size and its capitalization.

❖ CANSLIM Data.

Displays either genuine CANSLIM data from TradinView or custom data as best effort when that data cannot be obtained in TV.

C = EPS diluted growth, Quarterly YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

A = EPS diluted growth, Annual YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

N = New High as best effort (Cust).

Always Good

S = Float shares as best effort.

Always Good

L = One year performance relative to S&P 500 (Cust),

Positive : 0% .. 50% = Neutral, 50%+ = Leader, 80%+ = Leader+, 100%+ = Leader++

Negative : 0% .. -10% = Laggard, -10% .. -30% = Laggard+, -30%+ = Laggard++

>= 50% = Good, >= 0% = Acceptable, >= -10% Warning, < -10% = Stop

I = Accumulation/Distribution days over last 25 days as a clue for institutional support (Cust).

A delta is calculated by subtracting Distribution to Accumulation days.

> 0 = Good, = 0 = Acceptable, < 0 = Warning, < -5 = Stop

M = Market direction and exposure measured on S&500 closing between averages (Cust).

Varies from 0% Full Bear to 100% Full Bull

>= 80% = Good, >= 60% = Acceptable, >= 40% = Warning, < 40% = Stop

❖ Extra non CANSLIM Data.

RS = RS Rating.

>= 90 = Good, >= 80 = Accept, >= 50 = Warning, < 50 = Stop

Rev. = Revenue Growth Quarterly YoY.

>= 0% = Good, <0% = Stop

ROE = Return on Equity, Quarterly YoY.

>= 17% = Good, >= 0% = Acceptable, < 0% = Stop

Piotr. = Piotroski Score, www.investopedia.com (TV)

>= 7 = Good, >= 4 = Acceptable, < 4 = Stop

ATR = Average True Range over the last 20 days (Cust).

0% - 2% = Acceptable, 2% - 4% = Ideal, 4% - 6% = Warning, 5%+ = Stop.

Trend Days = Days since EMA150 is over EMA200 (Cust).

Always Good

D. to E. = Days left before Earnings. Maybe not a good idea buying just before earnings (Cust).

>= 28 = Good, >= 21 = Acceptable, >= 14 = Warning, < 14 = Stop

Avg Vol. = 50d Average Volume (Cust).

>= 100K = Good, < 100K = Acceptable

Vol. Today = Today's percentage volume compared to 50d average (Cust).

Always Good.

❖ Historical Data.

Optionally selectable historical data can be displayed for C, A, Revenue and ROE up to 20 quarters if available.

Quarterly numbers can also be displayed for A, C and Revenue.

Information can be shown in Chronological or Reverse Chronological order (default).

Increasing growth quarters are shown in white, while diminuing ones are shown in Yellow.

Transition from Losing to Profitable quarters are shown with an exclamation mark ‘!’

Finally, losing quarters are shown between parenthesis.

❖ MAs on chart.

Displays 200, 100, 50 and 20 days MAs on chart.

The MAs are also automatically scaled in the 1W time frame.

❖ New 52 Week High on chart.

A sun is shown on the chart the first time that a new 52 week high is reached.

The N cell shows a filled sun when a 52 week high is no older than a month, an lighter sun when it’s no older than a quarter or a moon otherwise.

❖ Pocket Pivots on chart.

Small triangles below the price are signaling pocket pivots.

❖ Bases on chart, formerly Darvas Boxes.

Draw bases as defined by Darvas boxes, both top or bottom of bases can be selected to be shown in order to only show resistance or support.

❖ Market exposure/direction indicator.

When charting S&P500 (SPX), Nasdaq 100 Index (NDX), Nasdaq composite (IXIC) or Dow Jownes Index (DJIA), the indicator switches to Market Exposure indicator, showing also Accumulation/Distribution days when volume information is available. This indication which varies from 0% to 100% is what is shown under the M letter in the CANSLIM table which is calculated on the S&P500.

❖ Follow Through Days indicator.

If you are an adept of the Low-cheat entry, then you will be highly interested by the Follow Through days indicator as measured in the S&P 500 and shown as diamonds on the chart.

The follow-through days are calculated on S&P500 but shown in current stock chart so you don’t need to chart the S&P 500 to know that a follow through day occurred.

Follow Through days show correctly on Daily time frame and most are also shown on the Weekly time frame as well.

They are also classified according to the market zone in which they occur:

0%-5% from peak = Pullback : FT day is not shown.

5%-10% from peak = Minor Correction : Minor FT days is shown.

10%-20% from peak = Correction : Intermediate FT days us shown

20+% from peak = Bear Market : Makor FT days is shown

❖ RS Line and Rating indicator.

A RS Line and Rating indicator can be added to the chart.

Relative Strength Rating Accuracy.

Please note that the RS Rating is not 100% accurate when compared to IBD values.

❖ Earning Line indicator.

An Earning Line indicator can be added to the chart.

❖ ATR Bands and ATR Trade calculator.

The motivation for this calculator came from my own need to enter trades on volatile stocks where the simple 7% Stop Loss rule doest not work.

It simply calculates the number of shares you can buy at any moment based on current stock price and using the lower ATR band as a stop loss.

A few words about the ATR Bands.

On this indicator the ATR bands are not drawn as a classical channel that follows the price.

The lower band is drawn as a support until it’s broken on a closing basis. It can’t be in a down trend.

The upper band is drawn as a resistance until it’s broken on a closing basis. It can’t be in an up trend.

The idea is that when price starts to fall down from a peak, it should not violate its lower band ATR and that means that we can use that level as a Stop Loss.

You must look back for the stock volatility and find out which ATR multiplier works well meaning that the ATR bands are not violated on normal pullbacks. By default, the indicator uses 5x multiplier.

❖ Extra things, visual features and default settings.

The first square cell of current quarter displays a check mark ‘V’ if the CANSLIM criteria is OK or acceptable or a cross ‘X’ otherwise.

The first square cell of historical C and Rev show respectively the count of last consecutive positive quarters.

There are different color themes from “Forest” to “Space” you can chose from to best fit your eyes.

You also have different table sizes going from “Micro” to “Huge” for better adjustment to the size of your display.

The default settings view show: Pocket Pivots, FT Days, MA50, RS Line and ATR Bands.

That's all, Enjoy!

Chart-Only Scanner — Pro Table v2.5.1Chart-Only Scanner — Pro Table v2.5

User Manual (Pine Script v6)

What this tool does (in one line)

A compact, on-chart table that scores the current chart symbol (or an optional override) using momentum, volume, trend, volatility, and pattern checks—so you can quickly decide UP, DOWN, or WAIT.

Quick Start (90 seconds)

Add the indicator to any chart and timeframe (1m…1M).

Leave “Override chart symbol” = OFF to auto-use the chart’s symbol.

Choose your layout:

Row (wide horizontal strip), or Grid (title + labeled cells).

Pick a size preset (Micro, Small, Medium, Large, Mobile).

Optional: turn on “Use Higher TF (EMA 20/50)” and set HTF Multiplier (e.g., 4 ⇒ if chart is 15m, HTF is 60m).

Watch the table:

DIR (↑/↓/→), ROC%, MOM, VOL, EMA stack, HTF, REV, SCORE, ACT.

Add an alert if you want: the script fires when |SCORE| ≥ Action threshold.

What to expect

A small table appears on the chart corner you choose, updating each bar (or only at bar close if you keep default smart-update).

The ACT cell shows 🔥 (strong), 👀 (medium), or ⏳ (weak).

Panels & Settings (every option explained)

Core

Momentum Period: Lookback for rate-of-change (ROC%). Shorter = more reactive; longer = smoother.

ROC% Threshold: Minimum absolute ROC% to call direction UP (↑) or DOWN (↓); otherwise →.

Require Volume Confirmation: If ON and VOL ≤ 1.0, the SCORE is forced to 0 (prevents low-volume false positives).

Override chart symbol + Custom symbol: By default, the indicator uses the chart’s symbol. Turn this ON to lock to a specific ticker (e.g., a perpetual).

Higher TF

Use Higher TF (EMA 20/50): Compares EMA20 vs EMA50 on a higher timeframe.

HTF Multiplier: Higher TF = (chart TF × multiplier).

Example: on 3H chart with multiplier 2 ⇒ HTF = 6H.

Volatility & Oscillators

ATR Length: Used to show ATR% (ATR relative to price).

RSI Length: Standard RSI; colors: green ≤30 (oversold), red ≥70 (overbought).

Stoch %K Length: With %D = SMA(%K, 3).

MACD Fast/Slow/Signal: Standard MACD values; we display Line, Signal, Histogram (L/S/H).

ADX Length (Wilder): Wilder’s smoothing (internal derivation); also shows +DI / −DI if you enable the ADX column.

EMAs / Trend

EMA Fast/Mid/Slow: We compute EMA(20/50/200) by default (editable).

EMA Stack: Bull if Fast > Mid > Slow; Bear if Fast < Mid < Slow; Flat otherwise.

Benchmark (optional, OFF by default)

Show Relative Strength vs Benchmark: Displays RS% = ROC(symbol) − ROC(benchmark) over the Momentum Period.

Benchmark Symbol: Ticker used for comparison (e.g., BTCUSDT as a market proxy).

Columns (show/hide)

Toggle which fields appear in the table. Hiding unused fields keeps the layout clean (especially on mobile).

Display

Layout Mode:

Row = a single two-row strip; each column is a metric.

Grid = a title row plus labeled pairs (label/value) arranged in rows.

Size Preset: Micro, Small, Medium, Large, Mobile change text size and the grid density.

Table Corner: Where the panel sits (e.g., Top Right).

Opaque Table Background: ON = dark card; OFF = transparent(ish).

Update Every Bar: ON = update intra-bar; OFF = smart update (last bar / real-time / confirmed history).

Action threshold (|score|): The cutoff for 🔥 and alert firing (default 70).

How to read each field

CHART: The active symbol name (or your custom override).

DIR: ↑ (ROC% > threshold), ↓ (ROC% < −threshold), → otherwise.

ROC%: Rate of change over Momentum Period.

Formula: (Close − Close ) / Close × 100.

MOM: A scaled momentum score: min(100, |ROC%| × 10).

VOL: Volume ratio vs 20-bar SMA: Volume / SMA(Volume,20).

1.5 highlights as yellow (significant participation).

ATR%: (ATR / Close) × 100 (volatility relative to price).

RSI: Colored for extremes: ≤30 green, ≥70 red.

Stoch K/D: %K and %D numbers.

MACD L/S/H: Line, Signal, Histogram. Histogram color reflects sign (green > 0, red < 0).

ADX, +DI, −DI: Trend strength and directional components (Wilder). ADX ≥ 25 is highlighted.

EMA 20/50/200: Current EMA values (editable lengths).

STACK: Bull/Bear/Flat as defined above.

VWAP%: (Close − VWAP) / Close × 100 (premium/discount to VWAP).

HTF: ▲ if HTF EMA20 > EMA50; ▼ if <; · if flat/off.

RS%: Symbol’s ROC% − Benchmark ROC% (positive = outperforming).

REV (reversal):

🟢 Eng/Pin = bullish engulfing or bullish pin detected,

🔴 Eng/Pin = bearish engulfing or bearish pin,

· = none.

SCORE (absolute shown as a number; sign shown via DIR and ACT):

Components:

base = MOM × 0.4

volBonus = VOL > 1.5 ? 20 : VOL × 13.33

htfBonus = use_mtf ? (HTF == DIR ? 30 : HTF == 0 ? 15 : 0) : 0

trendBonus = (STACK == DIR) ? 10 : 0

macdBonus = 0 (placeholder for future versions)

scoreRaw = base + volBonus + htfBonus + trendBonus + macdBonus

SCORE = DIR ≥ 0 ? scoreRaw : −scoreRaw

If Require Volume Confirmation and VOL ≤ 1.0 ⇒ SCORE = 0.

ACT:

🔥 if |SCORE| ≥ threshold

👀 if 50 < |SCORE| < threshold

⏳ otherwise

Practical examples

Strong long (trend + participation)

DIR = ↑, ROC% = +3.2, MOM ≈ 32, VOL = 1.9, STACK = Bull, HTF = ▲, REV = 🟢

SCORE: base(12.8) + volBonus(20) + htfBonus(30) + trend(10) ≈ 73 → ACT = 🔥

Action idea: look for longs on pullbacks; confirm risk with ATR%.

Weak long (no volume)

DIR = ↑, ROC% = +1.0, but VOL = 0.8 and Require Volume Confirmation = ON

SCORE forced to 0 → ACT = ⏳

Action: wait for volume > 1.0 or turn off confirmation knowingly.

Bearish reversal warning

DIR = →, REV = 🔴 (bearish engulfing), RSI = 68, HTF = ▼

SCORE may be mid-range; ACT = 👀

Action: watch for breakdown and rising VOL.

Alerts (how to use)

The script calls alert() whenever |SCORE| ≥ Action threshold.

To receive pop-ups, sounds, or emails: click “⏰ Alerts” in TradingView, choose this indicator, and pick “Any alert() function call.”

The alert message includes: symbol, |SCORE|, DIR.

Layout, Size, and Corner tips

Row is best when you want a compact status ribbon across the top.

Grid is clearer on big screens or when you enable many columns.

Size:

Mobile = one pair per row (tall, readable)

Micro/Small = dense; good for many fields

Large = presentation/screenshots

Corner: If the table overlaps price, change the corner or set Opaque Background = OFF.

Repaint & timeframe behavior

Default smart update prefers stability (last bar / live / confirmed history).

For a stricter, “close-only” behavior (less repaint): turn Update Every Bar = OFF and avoid Heikin Ashi when you want raw market OHLC (HA modifies price inputs).

HTF logic is derived from a clean, integer multiple of your chart timeframe (via multiplier). It works with 3H/4H and any TF.

Performance notes

The script analyzes one symbol (chart or override) with multiple metrics using efficient tuple requests.

If you later want a multi-symbol grid, do it with pages (10–15 per page + rotate) to stay within platform limits (recommended future add-on).

Troubleshooting

No table visible

Ensure the indicator is added and not hidden.

Try toggling Opaque Background or switch Corner (it might be behind other drawings).

Keep Columns count reasonable for the chosen Size.

If you turned ON Override, verify the Custom symbol exists on your data provider.

Numbers look different on HA candles

Heikin Ashi modifies OHLC; switch to regular candles if you need raw price metrics.

3H/4H issues

Use integer HTF Multiplier (e.g., 2, 4). The tool builds the correct string internally; no manual timeframe strings needed.

Power user tips

Volume gating: keeping Require Volume Confirmation = ON filters most fake moves; if you’re a scalper, reduce strictness or turn it off.

Action threshold: 60–80 is typical. Higher = fewer but stronger signals.

Benchmark RS%: great for spotting leaders/laggards; positive RS% = outperformance vs benchmark.

Change policy & safety

This version doesn’t alter your historical logic you tested (no radical changes).

Any future “radical” change (score weights, HTF logic, UI hiding data) will ship with a toggle and an Impact Statement so you can keep old behavior if you prefer.

Glossary (quick)

ROC%: Percent change over N bars.

MOM: Scaled momentum (0–100).

VOL ratio: Volume vs 20-bar average.

ATR%: ATR as % of price.

ADX/DI: Trend strength / direction components (Wilder).

EMA stack: Relationship between EMAs (bullish/bearish/flat).

VWAP%: Premium/discount to VWAP.

RS%: Relative strength vs benchmark.

Becak I-series: Indicator Floating Panels v.80Becak I-series: Floating Panels v.80th (Indonesia Independence Days)

What it does:

This indicator creates three floating overlay panels that display MACD, RSI, and Stochastic oscillators directly on your price chart. Unlike traditional separate panes, these panels hover over your chart with customizable positioning and transparency, providing a clean, space-efficient way to monitor multiple technical indicators simultaneously.

When to use:

When you need to monitor momentum, trend strength, and overbought/oversold conditions without cluttering your workspace

Perfect for traders who want quick visual access to multiple oscillators while maintaining focus on price action

Ideal for any timeframe and asset class (stocks, crypto, forex, commodities)

How it works:

The script calculates standard MACD (12,26,9), RSI (14), and Stochastic (14,3,3) values, then renders them as floating panels with:

MACD Panel: Shows MACD line (blue), Signal line (orange), and histogram (green/red bars)

RSI Panel: Displays RSI line (purple) with overbought (70) and oversold (30) reference levels

Stochastic Panel: Shows %K (blue) and %D (orange) lines with optional buy/sell signals and highlighted overbought/oversold zones

Customization options:

Position: Choose Top, Bottom, or Auto-Center placement

Size: Adjust panel height (15-35% of chart) and spacing between panels

Positioning: Fine-tune vertical center offset and horizontal positioning

Appearance: Toggle panel backgrounds and adjust transparency (50-95%)

Parameters: Modify all indicator lengths and overbought/oversold levels

Signals: Enable/disable Stochastic crossover signals

Display: Control lookback period (30-100 bars) and right margin spacing

Universal compatibility: Works seamlessly across all asset types with automatic range detection and scaling.

DIRGAHAYU HARI KEMERDEKAAN KE 80 - INDONESIA ... MERDEKA!!!!!

CleanBreak Lines (Break + First Retest)CleanBreak lines draws one robust support line (green) from swing lows and one robust resistance line (red) from swing highs, then optionally signals a confirmed break and the first clean retest back to that line. Lines are scored with a transparent W-Score (0–100) so traders can judge quality at a glance. The script is non-repainting and uses only confirmed bar data.

What it does

Auto-builds two trendlines that aim to represent meaningful support and resistance.

Uses a median-based slope so outliers and single spikes do not distort the line.

Computes a W-Score per line from three things: touches, span (how long it held), and respect (staying on the correct side).

Optionally triggers a single, tightly-gated signal on Break + First Retest.

How it works (plain English)

Detect recent swing highs and swing lows.

Fit one line through highs and one through lows using a robust, median-style slope estimate.

Score each line: more clean touches and longer span raise the W-Score; frequent violations lower it.

A break requires a candle close beyond the line by a small ATR margin.

A first retest requires price to come back to the line within a limited number of bars and hold on close.

A single arrow may print on that confirmed retest, with optional alerts.

What it is not

Not a prediction model and not a promises-of-profit tool.

Not a multi-signal spammer: by design it aims to allow one retest entry per break.

Not a regression channel or machine-learning system.

How to use

At a glance: treat the green line as candidate support and the red line as candidate resistance.

Conservative approach: wait for a break on close and then the first retest to hold; use the arrow as a prompt, not a command.

Context-only mode: hide arrows in Style if you want the lines and W-Score only.

Inputs (brief)

Core: Swing Length, Max Pivots, Min Touches, Min Span Bars.

Scoring: Touches Max (cap), Weights for touches vs span, Min W-Score to arm.

Break and Retest: Break Margin x ATR, Retest Tolerance x ATR, Retest Window (bars).

Visuals: Show Labels, Show Table, Line Width, Fade When Refit.

Recommended presets

Cleaner, fewer signals: Min Touches 4–5, Min Span Bars 100–150, Min W-Score 70–80, Break Margin 0.40–0.60 ATR, Retest Tolerance 0.10–0.15 ATR, Retest Window 8–12 bars.

Lines-only: keep defaults and uncheck the two plotshapes in Style.

Alerts

CB Long Retest: break above the red line and first retest holds.

CB Short Retest: break below the green line and first retest holds.

Use “Once per bar close” for consistency.

On-chart table (if enabled)

RES / SUP: W-Score and distance from price in ATR terms.

Status: “Waiting Long RT”, “Waiting Short RT”, or “Idle”.

Thresholds: MinScore and Retest bars for quick context.

Timeframes

Works well on 1h to 1D. On very low timeframes, raise Break Margin x ATR to reduce whipsaw effects. On higher timeframes, increase Min Touches and Min Span Bars.

Non-repainting policy

All logic uses confirmed pivots and confirmed bar closes.

Breaks and retests are validated on close; alerts reference only confirmed conditions.

No lookahead in any request.security call.

Original implementation focused on a median-based robust slope for auto trendlines, plus a transparent W-Score and a single retest gate.

Disclosure

This script is for education and charting. It does not guarantee outcomes, and past behavior does not imply future results. Always validate on historical data and practice risk management.

Egg vs Tennis Ball — Drop/Rebound StrengthEgg vs Tennis Ball — Drop/Rebound Meter

What it does

Classifies selloffs as either:

Eggs — dead‑cat, no bounce

Tennis Balls — fast, decisive rebound

Core features

Detects swing drops from a Pivot High (PH) to a Pivot Low (PL)

Requires drops to be meaningful (volatility‑aware, ATR‑scaled)

Draws a bounce threshold line and a deadline

Decides outcome based on speed and extent of rebound

Tracks scores and win rates across multiple lookback windows

Includes a color‑coded meter and current streak display

Visuals at a glance

Gray diagonal — drop from PH to PL

Teal dotted horizontal — bounce threshold, from PH to the deadline

Solid green — Tennis Ball (bounce line broken before the deadline)

Solid red — Egg (deadline expired before the bounce)

Optional PH / PL labels for clarity

How the decision is made

1) Find pivots — symmetric pivots using Pivot Left / Right; PL confirms after Right bars.

2) Qualify the drop — Drop Size = PH − PL; must be ≥ (Drop Threshold × ATR at PL).

3) Define the bounce line — PL + (Bounce Multiple × Drop Size). 1.00× = full retrace to PH; up to 2.00× for overshoot.

4) Set the deadline — Drop Bars = PL index − PH index; Deadline = Drop Bars × Recovery Factor; timer starts from PH or PL.

5) Resolve — Tennis Ball if price hits the bounce line before the deadline; Egg if the deadline passes first.

Scoring system (−100 to +100)

+100 = perfect Tennis Ball (fastest possible + full overshoot)

−100 = perfect Egg (no recovery)

In between: scored by rebound speed and extent, shaped by your weight settings

Meter Table

Columns (toggle on/off)

All (off by default)

Last N1 (default 5)

Last N2 (default 10)

Last N3 (default 20)

Rows

Tennis / Eggs — counts

% Tennis — win rate

Avg Score — normalized quality from −100 to +100

Streak — overall (not windowed), e.g., +3 = 3 Tennis Balls in a row, −4 = 4 Eggs in a row

Alerts

Tennis Ball – Fast Rebound — triggers when the bounce line is broken in time

Egg – Window Expired — triggers when the deadline passes without a bounce

Inputs

① Drop Detection

Pivot Left / Right

ATR Length

Drop Threshold × ATR

② Bounce Requirement

Bounce Multiple × Drop Size (0.10–2.00×)

③ Timing

Timer Start — PH or PL

Recovery Factor × Drop Bars

Break Trigger — Close or High

④ Display

Show Pivot/Outcome Labels

Line Width

Table Position (corner)

⑤ Meter Columns

Show All (off by default)

Show N1 / N2 / N3 (5, 10, 20 by default)

⑥ Scoring Weights

Tennis — Base, Speed, Extent

Egg — Base, Strength

How to use it

Pick strictness — start with Drop Threshold = 2.0 ATR, Bounce Multiple = 1.0×, Recovery Factor = 3.0×; adjust to timeframe and volatility.

Watch the dotted line — it ends at the deadline; turns solid green (Tennis) if broken in time, solid red (Egg) if it expires.

Read the meter — short windows (5–10) show current behavior; Avg Score captures quality; Streak shows momentum.

Blend with your system — combine with trend filters, volume, or regime detection.

Tips

Close vs High trigger: Close is stricter; High is more responsive.

PH vs PL timer start: PH measures round‑trip; PL measures recovery only.

Increase pivot strength for fewer, more reliable signals.

Higher timeframes generally produce cleaner patterns.

Defaults

Pivot L/R: 5 / 5

ATR Length: 14

Drop Threshold: 2.0× ATR

Bounce Multiple: 1.00×

Recovery Factor: 3.0×

Break Trigger: Close

Windows: Last 5, 10, 20 (All off)

Interpreting results

Tennis‑y: Avg Score +30 to +70, %Tennis > 55%

Mixed: Avg Score near 0

Egg‑y: Avg Score −30 to −80, %Tennis < 45%

Wolf Exit Oscillator Enhanced

# Wolf Exit Oscillator Enhanced

## What it is (quick take)

**Wolf Exit Oscillator Enhanced** is a clean, rules-first **exit timing tool** built on the **True Strength Index (TSI)** with two optional safeguards:

1. **Signal-line crossover** (to avoid bailing on shallow dips), and

2. **EMA confirmation** (price-based “is the trend actually weakening/strengthening?” check).

Use it to standardize when you **take profits, cut losers, or scale out**—especially after momentum runs hot or cold.

> Works best **paired** with:

>

> * **ABS NR — Fail-Safe Confirm (v4.2.2)** for entries

> * **ABS Companion Oscillator — Trend / Exhaustion / New Trend** for trend/exhaustion context

---

## How to use it (operational workflow)

1. **Set your bands**

* `exitHigh` and `exitLow` mark “overcooked” zones on the TSI scale (default: +60 / –60).