NY Open 5 minute Range (5m Box Extended)Draws a box around the first 5 minute candle for the New York session.

Volatilité

Luxy BIG beautiful Dynamic ORBThis is an advanced Opening Range Breakout (ORB) indicator that tracks price breakouts from the first 5, 15, 30, and 60 minutes of the trading session. It provides complete trade management including entry signals, stop-loss placement, take-profit targets, and position sizing calculations.

The ORB strategy is based on the concept that the opening range of a trading session often acts as support/resistance, and breakouts from this range tend to lead to significant moves.

What Makes This Different?

Most ORB indicators simply draw horizontal lines and leave you to figure out the rest. This indicator goes several steps further:

Multi-Stage Tracking

Instead of just one ORB timeframe, this tracks FOUR simultaneously (5min, 15min, 30min, 60min). Each stage builds on the previous one, giving you multiple trading opportunities throughout the session.

Active Trade Management

When a breakout occurs, the indicator automatically calculates and displays entry price, stop-loss, and multiple take-profit targets. These lines extend forward and update in real-time until the trade completes.

Cycle Detection

Unlike indicators that only show the first breakout, this tracks the complete cycle: Breakout → Retest → Re-breakout. You can see when price returns to test the ORB level after breaking out (potential re-entry).

Failed Breakout Warning

If price breaks out but quickly returns inside the range (within a few bars), the label changes to "FAILED BREAK" - warning you to exit or avoid the trade.

Position Sizing Calculator

Built-in risk management that tells you exactly how many shares to buy based on your account size and risk tolerance. No more guessing or manual calculations.

Advanced Filtering

Optional filters for volume confirmation, trend alignment, and Fair Value Gaps (FVG) to reduce false signals and improve win rate.

Core Features Explained

### 1. Multi-Stage ORB Levels

The indicator builds four separate Opening Range levels:

ORB 5 - First 5 minutes (fastest signals, most volatile)

ORB 15 - First 15 minutes (balanced, most popular)

ORB 30 - First 30 minutes (slower, more reliable)

ORB 60 - First 60 minutes (slowest, most confirmed)

Each level is drawn as a horizontal range on your chart. As time progresses, the ranges expand to include more price action. You can enable or disable any stage and assign custom colors to each.

How it works: During the opening minutes, the indicator tracks the highest high and lowest low. Once the time period completes, those levels become your ORB high and low for that stage.

### 2. Breakout Detection

When price closes outside the ORB range, a label appears:

BREAK UP (green label above price) - Price closed above ORB High

BREAK DOWN (red label below price) - Price closed below ORB Low

The label shows which ORB stage triggered (ORB5, ORB15, etc.) and the cycle number if tracking multiple breakouts.

Important: Signals appear on bar close only - no repainting. What you see is what you get.

### 3. Retest Detection

After price breaks out and moves away, if it returns to test the ORB level, a "RETEST" label appears (orange). This indicates:

The original breakout level is now acting as support/resistance

Potential re-entry opportunity if you missed the first breakout

Confirmation that the level is significant

The indicator requires price to move a minimum distance away before considering it a valid retest (configurable in settings).

### 4. Failed Breakout Detection

If price breaks out but returns inside the ORB range within a few bars (before the breakout is "committed"), the original label changes to "FAILED BREAK" in orange.

This warns you:

The breakout lacked conviction

Consider exiting if already in the trade

Wait for better setup

Committed Breakout: The indicator tracks how many bars price stays outside the range. Only after staying outside for the minimum number of bars does it become a committed breakout that can be retested.

### 5. TP/SL Lines (Trade Management)

When a breakout occurs, colored horizontal lines appear showing:

Entry Line (cyan for long, orange for short) - Your entry price (the ORB level)

Stop Loss Line (red) - Where to exit if trade goes against you

TP1, TP2, TP3 Lines (same color as entry) - Profit targets at 1R, 2R, 3R

These lines extend forward as new bars form, making it easy to track your trade. When a target is hit, the line turns green and the label shows a checkmark.

Lines freeze (stop updating) when:

Stop loss is hit

The final enabled take-profit is hit

End of trading session (optional setting)

### 6. Position Sizing Dashboard

The dashboard (bottom-left corner by default) shows real-time information:

Current ORB stage and range size

Breakout status (Inside Range / Break Up / Break Down)

Volume confirmation (if filter enabled)

Trend alignment (if filter enabled)

Entry and Stop Loss prices

All enabled Take Profit levels with percentages

Risk/Reward ratio

Position sizing: Max shares to buy and total risk amount

Position Sizing Example:

If your account is $25,000 and you risk 1% per trade ($250), and the distance from entry to stop loss is $0.50, the calculator shows you can buy 500 shares (250 / 0.50 = 500).

### 7. FVG Filter (Fair Value Gap)

Fair Value Gaps are price inefficiencies - gaps left by strong momentum where one candle's high doesn't overlap with a previous candle's low (or vice versa).

When enabled, this filter:

Detects bullish and bearish FVGs

Draws semi-transparent boxes around these gaps

Only allows breakout signals if there's an FVG near the breakout level

Why this helps: FVGs indicate institutional activity. Breakouts through FVGs tend to be stronger and more reliable.

Proximity setting: Controls how close the FVG must be to the ORB level. 2.0x means the breakout can be within 2 times the FVG size - a reasonable default.

### 8. Volume & Trend Filters

Volume Filter:

Requires current volume to be above average (customizable multiplier). High volume breakouts are more likely to sustain.

Set minimum multiplier (e.g., 1.5x = 50% above average)

Set "strong volume" multiplier (e.g., 2.5x) that bypasses other filters

Dashboard shows current volume ratio

Trend Filter:

Only shows breakouts aligned with a higher timeframe trend. Choose from:

VWAP - Price above/below volume-weighted average

EMA - Price above/below exponential moving average

SuperTrend - ATR-based trend indicator

Combined modes (VWAP+EMA, VWAP+SuperTrend) for stricter filtering

### 9. Pullback Filter (Advanced)

Purpose:

Waits for price to pull back slightly after initial breakout before confirming the signal.

This reduces false breakouts from immediate reversals.

How it works:

- After breakout is detected, indicator waits for a small pullback (default 2%)

- Once pullback occurs AND price breaks out again, signal is confirmed

- If no pullback within timeout period (5 bars), signal is issued anyway

Settings:

Enable Pullback Filter: Turn this filter on/off

Pullback %: How much price must pull back (2% is balanced)

Timeout (bars): Max bars to wait for pullback (5 is standard)

When to use:

- Choppy markets with many fake breakouts

- When you want higher quality signals

- Combine with Volume filter for maximum confirmation

Trade-off:

- Better signal quality

- May miss some valid fast moves

- Slight entry delay

How to Use This Indicator

### For Beginners - Simple Setup

Add the indicator to your chart (5-minute or 15-minute timeframe recommended)

Leave all default settings - they work well for most stocks

Watch for BREAK UP or BREAK DOWN labels to appear

Check the dashboard for entry, stop loss, and targets

Use the position sizing to determine how many shares to buy

Basic Trading Plan:

Wait for a clear breakout label

Enter at the ORB level (or next candle open if you're late)

Place stop loss where the red line indicates

Take profit at TP1 (50% of position) and TP2 (remaining 50%)

### For Advanced Traders - Customized Setup

Choose which ORB stages to track (you might only want ORB15 and ORB30)

Enable filters: Volume (stocks) or Trend (trending markets)

Enable FVG filter for institutional confirmation

Set "Track Cycles" mode to catch retests and re-breakouts

Customize stop loss method (ATR for volatile stocks, ORB% for stable ones)

Adjust risk per trade and account size for accurate position sizing

Advanced Strategy Example:

Enable ORB15 only (disable others for cleaner chart)

Turn on Volume filter at 1.5x with Strong at 2.5x

Enable Trend filter using VWAP

Set Signal Mode to "Track Cycles" with Max 3 cycles

Wait for aligned breakouts (Volume + Trend + Direction)

Enter on retest if you missed the initial break

### Timeframe Recommendations

5-minute chart: Scalping, very active trading, crypto

15-minute chart: Day trading, balanced approach (most popular)

30-minute chart: Swing entries, less screen time

60-minute chart: Position trading, longer holds

The indicator works on any intraday timeframe, but ORB is fundamentally a day trading strategy. Daily charts don't make sense for ORB.

DEFAULT CONFIGURATION

ON by Default:

• All 4 ORB stages (5/15/30/60)

• Breakout Detection

• Retest Labels

• All TP levels (1/1.5/2/3)

• TP/SL Lines (Detailed mode)

• Dashboard (Bottom Left, Dark theme)

• Position Size Calculator

OFF by Default (Optional Filters):

• FVG Filter

• Pullback Filter

• Volume Filter

• Trend Filter

• HTF Bias Check

• Alerts

Recommended for Beginners:

• Leave all defaults

• Session Mode: Auto-Detect

• Signal Mode: Track Cycles

• Stop Method: ATR

• Add Volume Filter if trading stocks

Recommended for Advanced:

• Enable ORB15 + ORB30 only (disable 5 & 60)

• Enable: Volume + Trend + FVG

• Signal Mode: Track Cycles, Max 3

• Stop Method: ATR or Safer

• Enable HTF Daily bias check

## Settings Guide

The settings are organized into logical groups. Here's what each section controls:

### ORB COLORS Section

Show Edge Labels: Display "ORB 5", "ORB 15" labels at the right edge of the levels

Background: Fill the area between ORB high/low with color

Transparency: How see-through the background is (95% is nearly invisible)

Enable ORB 5/15/30/60: Turn each stage on or off individually

Colors: Assign colors to each ORB stage for easy identification

### SESSION SETTINGS Section

Session Mode: Choose trading session (Auto-Detect works for most instruments)

Custom Session Hours: Define your own hours if needed (format: HHMM-HHMM)

Auto-Detect uses the instrument's natural hours (stocks use exchange hours, crypto uses 24/7).

### BREAKOUT DETECTION Section

Enable Breakout Detection: Master switch for signals

Show Retest Labels: Display retest signals

Label Size: Visual size for all labels (Small recommended)

Enable FVG Filter: Require Fair Value Gap confirmation

Show FVG Boxes: Display the gap boxes on chart

Signal Mode: "First Only" = one signal per direction per day, "Track Cycles" = multiple signals

Max Cycles: How many breakout-retest cycles to track (6 is balanced)

Breakout Buffer: Extra distance required beyond ORB level (0.1-0.2% recommended)

Min Distance for Retest: How far price must move away before retest is valid (2% recommended)

Min Bars Outside ORB: Bars price must stay outside for committed breakout (2 is balanced)

### TARGETS & RISK Section

Enable Targets & Stop-Loss: Calculate and show trade management

TP1/TP2/TP3 checkboxes: Select which profit targets to display

Stop Method: How to calculate stop loss placement

- ATR: Based on volatility (best for most cases)

- ORB %: Fixed % of ORB range

- Swing: Recent swing high/low

- Safer: Widest of all methods

ATR Length & Multiplier: Controls ATR stop distance (14 period, 1.5x is standard)

ORB Stop %: Percentage beyond ORB for stop (20% is balanced)

Swing Bars: Lookback period for swing high/low (3 is recent)

### TP/SL LINES Section

Show TP/SL Lines: Display horizontal lines on chart

Label Format: "Short" = minimal text, "Detailed" = shows prices

Freeze Lines at EOD: Stop extending lines at session close

### DASHBOARD Section

Show Info Panel: Display the metrics dashboard

Theme: Dark or Light colors

Position: Where to place dashboard on chart

Toggle rows: Show/hide specific information rows

Calculate Position Size: Enable the position sizing calculator

Risk Mode: Risk fixed $ amount or % of account

Account Size: Your total trading capital

Risk %: Percentage to risk per trade (0.5-1% recommended)

### VOLUME FILTER Section

Enable Volume Filter: Require volume confirmation

MA Length: Average period (20 is standard)

Min Volume: Required multiplier (1.5x = 50% above average)

Strong Volume: Multiplier that bypasses other filters (2.5x)

### TREND FILTER Section

Enable Trend Filter: Require trend alignment

Trend Mode: Method to determine trend (VWAP is simple and effective)

Custom EMA Length: If using EMA mode (50 for swing, 20 for day trading)

SuperTrend settings: Period and Multiplier if using SuperTrend mode

### HIGHER TIMEFRAME Section

Check Daily Trend: Display higher timeframe bias in dashboard

Timeframe: What TF to check (D = daily, recommended)

Method: Price vs MA (stable) or Candle Direction (reactive)

MA Period: EMA length for Price vs MA method (20 is balanced)

Min Strength %: Minimum strength threshold for HTF bias to be considered

- For "Price vs MA": Minimum distance (%) from moving average

- For "Candle Direction": Minimum candle body size (%)

- 0.5% is balanced - increase for stricter filtering

- Lower values = more signals, higher values = only strong trends

### ALERTS Section

Enable Alerts: Master switch (must be ON to use any alerts)

Breakout Alerts: Notify on ORB breakouts

Retest Alerts: Notify when price retests after breakout

Failed Break Alerts: Notify on failed breakouts

Stage Complete Alerts: Notify when each ORB stage finishes forming

After enabling desired alert types, click "Create Alert" button, select this indicator, choose "Any alert() function call".

## Tips & Best Practices

### General Trading Tips

ORB works best on liquid instruments (stocks with good volume, major crypto pairs)

First hour of the session is most important - that's when ORB is forming

Breakouts WITH the trend have higher success rates - use the trend filter

Failed breakouts are common - use the "Min Bars Outside" setting to filter weak moves

Not every day produces good ORB setups - be patient and selective

### Position Sizing Best Practices

Never risk more than 1-2% of your account on a single trade

Use the built-in calculator - don't guess your position size

Update your account size monthly as it grows

Smaller accounts: use $ Amount mode for simplicity

Larger accounts: use % of Account mode for scaling

### Take Profit Strategy

Most traders use: 50% at TP1, 50% at TP2

Aggressive: Hold through TP1 for TP2 or TP3

Conservative: Full exit at TP1 (1:1 risk/reward)

After TP1 hits, consider moving stop to breakeven

TP3 rarely hits - only on strong trending days

### Filter Combinations

Maximum Quality: Volume + Trend + FVG (fewest signals, highest quality)

Balanced: Volume + Trend (good quality, reasonable frequency)

Active Trading: No filters or Volume only (many signals, lower quality)

Trending Markets: Trend filter essential (indices, crypto)

Range-Bound: Volume + FVG (avoid trend filter)

### Common Mistakes to Avoid

Chasing breakouts - wait for the bar to close, don't FOMO into wicks

Ignoring the stop loss - always use it, move it manually if needed

Over-leveraging - the calculator shows MAX shares, you can buy less

Trading every signal - quality > quantity, use filters

Not tracking results - keep a journal to see what works for YOU

## Pros and Cons

### Advantages

Complete all-in-one solution - from signal to position sizing

Multiple timeframes tracked simultaneously

Visual clarity - easy to see what's happening

Cycle tracking catches opportunities others miss

Built-in risk management eliminates guesswork

Customizable filters for different trading styles

No repainting - what you see is locked in

Works across multiple markets (stocks, forex, crypto)

### Limitations

Intraday strategy only - doesn't work on daily charts

Requires active monitoring during first 1-2 hours of session

Not suitable for after-hours or extended sessions by default

Can produce many signals in choppy markets (use filters)

Dashboard can be overwhelming for complete beginners

Performance depends on market conditions (trends vs ranges)

Requires understanding of risk management concepts

### Best For

Day traders who can watch the first 1-2 hours of market open

Traders who want systematic entry/exit rules

Those learning proper position sizing and risk management

Active traders comfortable with multiple signals per day

Anyone trading liquid instruments with clear sessions

### Not Ideal For

Swing traders holding multi-day positions

Set-and-forget / passive investors

Traders who can't watch market open

Complete beginners unfamiliar with trading concepts

Low volume / illiquid instruments

## Frequently Asked Questions

Q: Why are no signals appearing?

A: Check that you're on an intraday timeframe (5min, 15min, etc.) and that the current time is within your session hours. Also verify that "Enable Breakout Detection" is ON and at least one ORB stage is enabled. If using filters, they might be blocking signals - try disabling them temporarily.

Q: What's the best ORB stage to use?

A: ORB15 (15 minutes) is most popular and balanced. ORB5 gives faster signals but more noise. ORB30 and ORB60 are slower but more reliable. Many traders use ORB15 + ORB30 together.

Q: Should I enable all the filters?

A: Start with no filters to see all signals. If too many false signals, add Volume filter first (stocks) or Trend filter (trending markets). FVG filter is most restrictive - use for maximum quality but fewer signals.

Q: How do I know which stop loss method to use?

A: ATR works for most cases - it adapts to volatility. Use ORB% if you want predictable stop placement. Swing is for respecting chart structure. Safer gives you the most room but largest risk.

Q: Can I use this for swing trading?

A: Not really - ORB is fundamentally an intraday strategy. The ranges reset each day. For swing trading, look at weekly support/resistance or moving averages instead.

Q: Why do TP/SL lines disappear sometimes?

A: Lines freeze (stop extending) when: stop loss is hit, the last enabled take-profit is hit, or end of session arrives (if "Freeze at EOD" is enabled). This is intentional - the trade is complete.

Q: What's the difference between "First Only" and "Track Cycles"?

A: "First Only" shows one breakout UP and one DOWN per day maximum - clean but might miss opportunities. "Track Cycles" shows breakout-retest-rebreak sequences - more signals but busier chart.

Q: Is position sizing accurate for options/forex?

A: The calculator is designed for shares (stocks). For options, ignore the share count and use the risk amount. For forex, you'll need to adapt the lot size calculation manually.

Q: How much capital do I need to use this?

A: The indicator works for any account size, but practical day trading typically requires $25,000 in the US due to Pattern Day Trader rules. Adjust the "Account Size" setting to match your capital.

Q: Can I backtest this strategy?

A: This is an indicator, not a strategy script, so it doesn't have built-in backtesting. You can visually review historical signals or code a strategy script using similar logic.

Q: Why does the dashboard show different entry price than the breakout label?

A: If you're looking at an old breakout, the ORB levels may have changed when the next stage completed. The dashboard always shows the CURRENT active range and trade setup.

Q: What's a good win rate to expect?

A: ORB strategies typically see 40-60% win rate depending on market conditions and filters used. The strategy relies on positive risk/reward ratios (2:1 or better) to be profitable even with moderate win rates.

Q: Does this work on crypto?

A: Yes, but crypto trades 24/7 so you need to define what "session start" means. Use Session Mode = Custom and set your preferred daily reset time (e.g., 0000-2359 UTC).

## Credits & Transparency

### Development

This indicator was developed with the assistance of AI technology to implement complex ORB trading logic.

The strategy concept, feature specifications, and trading logic were designed by the publisher. The implementation leverages modern development tools to ensure:

Clean, efficient, and maintainable code

Comprehensive error handling and input validation

Detailed documentation and user guidance

Performance optimization

### Trading Concepts

This indicator implements several public domain trading concepts:

Opening Range Breakout (ORB): Trading strategy popularized by Toby Crabel, Mark Fisher and many more talanted traders.

Fair Value Gap (FVG): Price imbalance concept from ICT methodology

SuperTrend: ATR-based trend indicator using public formula

Risk/Reward Ratio: Standard risk management principle

All mathematical formulas and technical concepts used are in the public domain.

### Pine Script

Uses standard TradingView built-in functions:

ta.ema(), ta.atr(), ta.vwap(), ta.highest(), ta.lowest(), request.security()

No external libraries or proprietary code from other authors.

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice.

Trading involves substantial risk of loss and is not suitable for every investor. Past performance shown in examples is not indicative of future results.

The indicator provides signals and calculations, but trading decisions are solely your responsibility. Always:

Test strategies on paper before using real money

Never risk more than you can afford to lose

Understand that all trading involves risk

Consider seeking advice from a licensed financial advisor

The publisher makes no guarantees regarding accuracy, profitability, or performance. Use at your own risk.

---

Version: 3.0

Pine Script Version: v6

Last Updated: October 2024

For support, questions, or suggestions, please comment below or send a private message.

---

Happy trading, and remember: consistent risk management beats perfect entry timing every time.

Risk Leverage ToolRisk Leverage Tool – Calculate Position Size and Required Leverage

This script automatically calculates the optimal position size and the leverage needed based on the amount of capital you are willing to risk on a trade. It is designed for traders who want precise control over their risk management.

The script determines the distance between the entry and stop-loss price, calculates the maximum position size that fits within the defined risk, and derives the notional value of the trade. Based on the available margin, it then calculates the required leverage. It also displays the percentage of margin at risk if the stop-loss is hit.

All results are displayed in a table in the top-right corner of the chart. Additionally, a label appears at the entry price level showing the same data.

To use the tool, simply input your planned entry price, stop-loss price, the maximum risk amount in dollars, and the available margin in the settings menu. The script will update all values automatically in real time.

This tool works with any market where capital risk is expressed in absolute terms (such as USD), including futures, CFDs, and leveraged spot positions. For inverse contracts or percentage-based stops, manual adjustment is required.

Liquidity Levels - PMH/PWH/PDH/HODWhat is it?

An indicator that tracks the main liquidity levels on TradingView, displaying the highs and lows of reference for month, week, previous day and current day.

What's it for?

It identifies price zones where there are many pending orders (liquidity). Traders use it to:

Find support and resistance points

Identify areas where price could bounce or break through

Receive alerts when price touches or breaks these levels

Which levels does it show?

LevelDescriptionColorLinePMH/PMLPrevious month's high and lowPurpleSolidPWH/PWLPrevious week's high and lowBlueSolidPDH/PDLPrevious day's high and lowOrangeSolidHOD/LODCurrent day's high and lowGrayDotted

How to use it?

Apply the indicator to your chart

Customize colors and enable/disable the levels you prefer

Set alerts to receive notifications when price touches or breaks levels

Use the levels to make trading decisions (entry, exit, stop loss)

Perfect for: Scalping, Day Trading, Swing Trading on any asset (forex, crypto, stocks)

THAIT Moving Averages Tight within # ATR EMA SMA convergence

THAIT(tight) indicator is a powerful tool for identifying moving average convergence in price action. This indicator plots four user-defined moving averages (EMA or SMA). It highlights moments when the MAs converge within a user specified number of ATRs, adjusted by the 14-period ATR, signaling potential trend shifts or consolidation.

A convergence is flagged when MA1 is the maximum, the spread between MAs is tight, and the price is above MA1, excluding cases where the longest MA (MA4) is the highest. The indicator alerts and visually marks convergence zones with a shaded green background, making it ideal for traders seeking precise entry or exit points.

Flux AI PullBack System (Hybrid Pro)Flux AI PullBack System (Hybrid Pro)

//Session-Aware | Adaptive Confluence | Grace Confirm Logic//

Overview:

The Flux AI PullBack System (Hybrid Pro v5) is an adaptive, session-aware pullback indicator designed to identify high-probability continuation setups within trending markets. It automatically adjusts between “Classic” and “Enhanced” logic modes based on volatility, volume, and ATR slope, allowing it to perform seamlessly across different market sessions (Asian, London, and New York).

Core Features:

Hybrid Auto Mode — Dynamically switches between Classic (fast-moving) and Enhanced (strict) modes.

Session-Aware Context — Optimized for intraday trading in ES, NQ, and SPY.

Grace Confirmation Logic — Validates pullbacks with a follow-through condition to reduce noise.

Adaptive EMA Zone (38/62) — Highlights pullback areas with dynamic aqua fill and transparency linked to trend strength.

Noise Suppression Filter — Prevents false pullbacks during EMA crossovers or unstable transitions.

Weighted Confluence Model — Combines trend, ATR, volume, and swing structure for confirmation strength.

Pine v6 Compliant Alerts — Constant-string safe, ready for webhooks and automation.

Visual Elements:

Aqua EMA Zone: Displays the “breathing” pullback band (tightens during volatility spikes).

PB↑ / PB↓ Markers: Confirmed pullbacks with subtle transparency and fixed label size.

Bar Highlights: Yellow for pullbacks; ice-blue for confirmed continuation.

Use Cases

Perfect for:

Intraday trend traders

0DTE SPX / ES scalpers

Futures traders (NQ, MNQ, MES)

Algorithmic strategy builders using webhooks

Recommended Timeframes:

1–15 minute charts (scalping / intraday)

Higher timeframes for swing confirmations.

Attribution:

This open-source script was inspired by Chris Moody’s “CM Slingshot System” and JustUncleL’s Pullback Tools, but it was built from scratch using AI-assisted code refinement (ChatGPT).

All logic and enhancements are original, not derived from proprietary software.

License: MIT (Open Source)

© 2025 Ken Anderson — You may modify, use, or redistribute with credit.

Keywords:

Pullback, Reversal, AI Trading, EMA Zone, Session Aware, Futures Trading, SPX, ES, NQ, ATR Filter, Volume Confirmation, Flux System, Pine Script v6, Non-Repainting, Adaptive Trading Indicator.

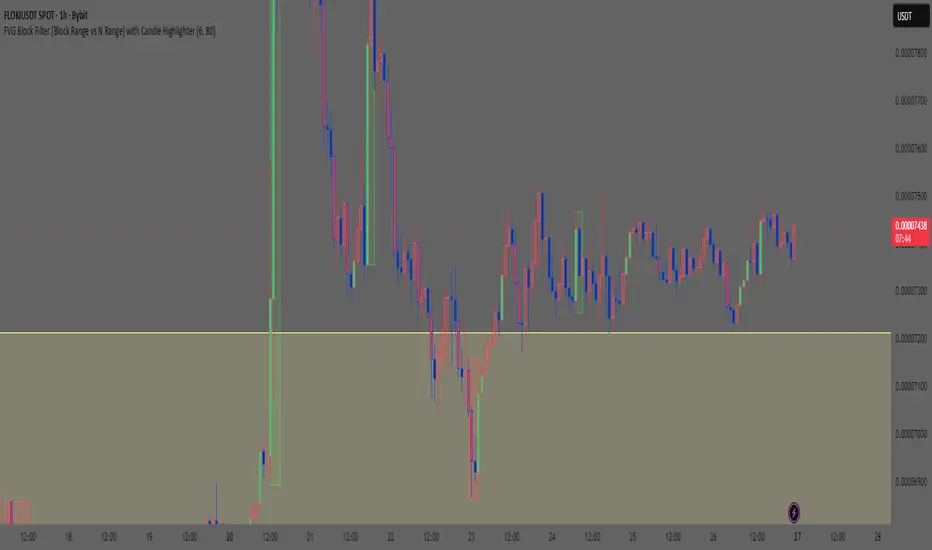

Smart Money Concept: FVG Block Filter Smart Money Concept: FVG Block Filter (FVG Block Range vs N Range) with Candle Highlighter

Summary:

Smart Money Concept (SMC): An advanced indicator designed to visualize and filter Fair Value Gaps (FVG) blocks based on their size (Range) compared to the preceding N Range candle movement. It also includes a customizable Candle Highlighter function that marks the specific candle responsible for creating the FVG. The indicator allows full color customization for both blocks and the highlighter, and features clean, label-free charts by default.

Key Features:

FVG Block Detection: Automatically identifies and groups sequential FVG imbalances to form consolidated FVG blocks.

FVG Block Filtering (N Range): Filters blocks based on a user-defined rule, comparing the block's size (Range) to the range of the preceding N candles (e.g., requiring the FVG block to be larger than the range of the previous 6 candles).

Customizable Candle Highlighter: Marks the central candle (B) within the FVG structure (A-B-C) to highlight the source of the price imbalance. Highlighter colors are fully adjustable via inputs.

Visualization Control: Labels are turned OFF by default to keep the chart clean but can be easily enabled via the indicator settings.

Full Color Customization: Allows independent customization of Bullish and Bearish FVG Block colors, Block Transparency, and Bullish/Bearish Highlighter colors.

Keywords:

Smart Money Concept, SMC, Fair Value Gap, FVG, Imbalance, Block Filter, Candle Highlighter, Range.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

NEURAL FLOW INDEX — Core Energy • Momentum Stream • Pulse SyncNeural Flow Index (NFI) — Advanced Triple-Layer Reversal Framework

The Neural Flow Index (NFI) is a next-generation market oscillator designed to reveal the hidden synchronization between trend energy, cyclical momentum, and internal pulse dynamics.

It merges three powerful analytical layers into a single, normalized view:

Core Energy Curve (based on RSO logic) — captures structural trend bias and volatility expansion.

Momentum Stream (WaveTrend algorithm) — visualizes cyclical motion of price waves.

Pulse Sync (Stochastic RSI adaptation) — measures short-term momentum rhythm and overextension.

Each layer feeds into a unified flow model that adapts to both trend-following and reversal conditions. The goal is not to chase every fluctuation, but to sense where momentum, direction, and volatility converge into true inflection points.

Conceptual Mechanics

The oscillator translates complex market behavior into an elegant, multi-phase signal system:

Core Energy Curve (RSO foundation):

A smoothed dynamic field representing the overall strength and direction of market pressure.

Green energy indicates expansion (bullish dominance); red energy reflects contraction (bearish decay).

Momentum Stream (WaveTrend):

The teal line functions like an electro-wave, oscillating through phases of expansion and exhaustion.

It provides the heartbeat of the market — smooth, rhythmic, and beautifully cyclic.

Pulse Sync (Stochastic RSI):

The purple line acts as the market’s nervous pulse, reacting to micro-momentum changes before the larger trend adjusts.

It identifies micro-tops and micro-bottoms that precede major trend shifts.

When these three forces align, they create high-probability reversal zones known as Neural Nodes — regions where energy, momentum, and rhythm converge.

Trading Logic

Potential Entry Zones:

When the purple Pulse Sync line crosses the green Momentum Stream near the lower or upper bounds of the oscillator, a potential turning point forms.

Yet, these crossovers are only validated when the Core Energy histogram (RSO) simultaneously supports the same direction — confirming that energy and rhythm are synchronized.

Histogram Confirmation:

The histogram is the “voice” of the oscillator.

Rising green volume within the histogram during a Pulse-Momentum crossover suggests a legitimate upward reversal.

Conversely, expanding red energy during an upper-band cross indicates momentum exhaustion and an early short-side opportunity.

Neutral Zones:

When all three layers flatten near the zero line, the market enters an equilibrium phase — no clear trend dominance, ideal for patience and re-entry planning.

| Layer | Representation | Color | Function |

| --------------------- | ------------------- | ----------------- | ------------------------------ |

| **Core Energy Curve** | Area / Histogram | Lime-Red gradient | Trend bias & volatility energy |

| **Momentum Stream** | WaveTrend line | Teal | Cyclical flow of price |

| **Pulse Sync** | Stochastic RSI line | Purple | Short-term momentum rhythm |

Interpretation Summary

Converging Waves: Trend, momentum, and pulse move together → strong continuation.

Diverging Waves: Pulse or Momentum decouple from Core Energy → early reversal warnings.

Histogram Expansion: Confirms direction and strength of the new wave.

Crossovers at Extremes: Potential entries, especially when confirmed by energy alignment.

🪶 Philosophy Behind NFI

The Neural Flow Index is not just a technical indicator — it’s a behavioral visualization system.

Instead of focusing on lagging confirmations, it captures the neural pattern of price motion:

how liquidity flows, contracts, and expands through time.

It bridges the gap between pure mathematics and market intuition — giving traders a cinematic, harmonic view of energy transition inside price structure.

GARCH Range PredictorThis was inspired by deltatrendtrading's video on GARCH models to predict daily trading ranges and identify favorable trading conditions. Based on advanced volatility forecasting techniques, it predicts whether a trading day's true range will exceed a threshold, helping traders decide when to trade or skip a session.

Key Features

GARCH(1,1) Volatility Modeling: Uses log-transformed true ranges with exponential moving average centering

Forward-Looking Predictions: Makes predictions at session start before the day unfolds

Dynamic or Static Thresholds: Choose between fixed dollar thresholds or adaptive 20-day averages

Accuracy Tracking: Monitors prediction accuracy with overall and recent (20-day) hit rates

Visual Session Boxes: Colors trading sessions green (trade) or red (skip) based on predictions

Real-Time Statistics: Displays current predictions, thresholds, and performance metrics

How It Works

Data Transformation: Log-transforms daily true ranges and centers them using an EMA

Variance Modeling: Updates GARCH variance using: σ²ₜ = ω + α(residual²) + β(σ²ₜ₋₁)

Prediction Generation: Back-transforms log predictions to dollar values

Signal Generation: Compares predictions to threshold to generate trade/skip signals

Performance Tracking: Validates predictions against actual outcomes

Parameters

GARCH Parameters (ω, α, β): Control volatility persistence and mean reversion

EMA Period: Smoothing period for log range centering

Threshold Settings: Static dollar amount or dynamic multiplier of recent averages

Session Time: Define regular trading hours for analysis

Best Use Cases

Breakout and momentum strategies that perform better on high-range days

Risk management by avoiding low-volatility sessions

Futures day trading (optimized for MNQ/NQ detection)

Any strategy where daily range impacts profitability

Important Notes

Requires 5+ sessions for initialization and warm-up

Accuracy depends heavily on proper parameter tuning for your specific instrument

Default parameters may need adjustment for different markets

Monitor the hit rate to validate effectiveness on your timeframe

Volume + MA5 & MA10This Volume + MA5 & MA10 (Technical Volume Trend Analysis)

The Volume + MA5 & MA10 indicator provides a precise view of market participation and volume momentum by combining raw volume data with two moving averages (MA5 and MA10). It’s designed for traders who rely on volume-based confirmation to validate price movements, breakouts, and trend reversals.

🔍 Overview

This indicator displays volume bars alongside two smooth volume averages — MA5 (short-term) and MA10 (medium-term) — making it easier to detect shifts in market activity.

When the short-term average crosses above or below the long-term average, it signals a potential change in trading intensity or market sentiment.

⚙️ Key Features

Dual Volume Moving Averages (MA5 & MA10) for short- and medium-term analysis.

Dynamic Bar Coloring based on whether current volume exceeds MA5 or MA10.

Crossover Detection with visual markers for MA5/MA10 intersections.

Alert Conditions to notify you of significant volume trend shifts.

Fully customizable appearance and smoothing options.

📊 How to Interpret

MA5 > MA10 → Increasing short-term volume activity (strengthening momentum).

MA5 < MA10 → Decreasing short-term volume (weakening participation).

Rising volume with price → Confirms trend strength.

Falling volume with rising/falling price → Suggests potential reversal or reduced conviction.

💡 Applications

Confirm breakouts and trend continuations.

Identify momentum divergences between price and volume.

Filter out low-volume or weak-trend setups.

Combine with RSI, MACD, or moving averages for enhanced signal validation.

✅ Advantages

Simple yet powerful structure for clean visual analysis.

Works across all timeframes and markets (crypto, stocks, forex, indices).

No repainting — reliable for both live and historical backtesting.

Use Volume + MA5 & MA10 to strengthen your technical analysis and gain a deeper understanding of how market participation drives price trends.

PG ATM Strike Line with Call & Put PremiumsPine Script: ATM Strike Line with Call & Put Premiums (Simplified)This Pine Script for TradingView displays the At-The-Money (ATM) strike price, futures price, call/put premiums (time value), and two ratios—Premium Ratio (PR) and Volume Ratio (VR)—for a user-selected underlying asset (e.g., NIFTY, BANKNIFTY, or stocks). It helps traders gauge near-term market direction using options data.How the Script WorksInputs:Expiry: Select year (e.g., '25), month (01–12), day (01–31) for option expiry (e.g., '251028').

Timeframe: Choose data timeframe (e.g., Daily, 15-min).

Symbol: Auto-detects chart symbol or select from Indian indices/stocks.

Strike: Auto-ATM (based on futures) or manual strike input.

Interval: Auto (e.g., 100 for NIFTY) or custom strike interval.

Colors: Customizable for ATM line, labels (Futures Price, CPR, PPR, VR, PR).

Calculations:Futures Price (FP): Fetches front-month futures price (e.g., NSE:NIFTY1!).

ATM Strike: Rounds futures price to nearest strike interval.

Option Data: Retrieves Last Traded Price (LTP) and volume for ATM call/put options (e.g., NSE:NIFTY251028C24200).

Call Premium (CPR): Call LTP minus intrinsic value (max(0, FP - Strike)).

Put Premium (PPR): Put LTP minus intrinsic value (max(0, Strike - FP)).

Premium Ratio (PR): PPR / CPR.

Volume Ratio (VR): Put Volume / Call Volume.

Visuals:Draws ATM strike line on chart.

Displays labels: FP (futures price), CPR (call premium), PPR (put premium), VR, PR.

VR/PR labels: Red (≥ 1.25, bearish), Green (≤ 0.75, bullish), Gray (0.75–1.25, neutral).

Updates on last confirmed bar to avoid redraws.

Using PR and VR for Market DirectionPremium Ratio (PR):PR ≥ 1.25 (Red): High put premiums suggest bearish sentiment (expect price drop).

PR ≤ 0.75 (Green): High call premiums suggest bullish sentiment (expect price rise).

0.75 < PR < 1.25 (Gray): Neutral, no clear direction.

Use: High PR favors bearish trades (e.g., buy puts); low PR favors bullish trades (e.g., buy calls).

Volume Ratio (VR):VR ≥ 1.25 (Red): High put volume indicates bearish activity.

VR ≤ 0.75 (Green): High call volume indicates bullish activity.

0.75 < VR < 1.25 (Gray): Neutral trading activity.

Use: High VR suggests bearish moves; low VR suggests bullish moves.

Combined Signals:High PR & VR: Strong bearish signal; consider put buying or call selling.

Low PR & VR: Strong bullish signal; consider call buying or put selling.

Mixed/Neutral: Use price action or support/resistance for confirmation.

Tips:Combine with technical analysis (e.g., trends, levels).

Match timeframe to trading horizon (e.g., 15-min for intraday).

Monitor FP for context; check volatility or news for accuracy.

ExampleNIFTY: FP = 24,237.50, ATM = 24,200, CPR = 120.25, PPR = 180.50, PR = 1.50 (Red), VR = 1.30 (Red).

Insight: High PR/VR suggests bearish bias; consider bearish trades if price nears resistance.

Action: Buy puts or exit longs, confirm with price action.

Conclusion: This script provides a concise tool for options traders, showing ATM strike, premiums, and PR/VR ratios. High PR/VR (≥ 1.25) signals bearish sentiment, low PR/VR (≤ 0.75) signals bullish sentiment, and neutral (0.75–1.25) suggests indecision. Combine with technical analysis for robust trading decisions in the Indian options market.

HV Spike Strategy (HVP + OR Breakout + Reversal + TP/SL Modes)Here is a script that I tried to make it simple, although it has several parameters, I will try to explain, here we go:

Logic: Open Range Breakout: otherwise knows as First Candle Rule, usually used for the first candle in the opening of a market session, in my strategy there is an option to use it even for Crypto that operate 24/7, how to do that? Simply by detecting Volatility from the HVP (Historical Volatility Percentile). Then the ORB logic kicks in and the first candle with high volatility gives the ranges for the trades. The proper HVP Activation Threshold has to be selected for each currency pair/index/crypto in order to have maximum profit.

Enter a trade: when the price goes 100% above/below the First Candle Rule Range. That way it is filtering fake breakouts. Also if the price reverses back into the range the strategy takes the opposite trade.

Exit a trade: SL/TP By percentage or ATR, selection in the input menu.

My intention is to avoid using lagging indicators or guessing of Price Action, purely Bull/Bear indication by the first candle.

I hope you find this helpful! Wishing all successful Trades!

ATR Trailing Stop with Entry Date & First-Day MultiplierATR based trailing stop based on a X post of Aksel Kibar.

Directional EMA - For Loop | Lyro RSDirectional EMA - For Loop | Lyro RS

Introduction

This indicator combines multi-type moving averages, loop-based momentum scoring, and divergence detection for adaptive trend and reversal analysis.

Key Features:

Multiple Moving Average Selection System: Choose from 16 different MA types - HMA, ALMA and JMA etc. To match your style best.

For Loop Based Scoring: Uses a From / To system to calculate cumulative buying/selling pressure across recent price action.

Signal Threshold: Long / Short threshold levels to control the sensitivity for different market conditions.

Divergence Detection: Regular bullish / bearish with clear labels for potential reversal points.

Clean Visuals: Multiple color themes with table and color based indicator line for easy reading.

How It Works:

Core Calculation: The indicator first creates a directional signal by comparing price to your selected moving average, normalized for current volatility.

Loop Analysis: This signal feeds into a for-loop that scores recent price history, generating a cumulative momentum value.

Signal Generation:

Bullish signals trigger when the score crosses above the Upper Threshold

Bearish signals trigger when the score crosses below the Lower Threshold

Divergence Alerts: Automatically detects when price makes new highs/lows that aren't confirmed by the oscillator.

Practical Use:

Trend Identification: The color-coded oscillator and signal table help confirm trend direction.

Reversal Warning: Divergence labels highlight potential trend exhaustion points for careful watch.

Customization:

Adjust MA type and length for sensitivity tuning

Modify loop parameters (From/To) to change analysis depth

Fine-tune threshold levels for signal frequency

Enable/disable divergence detection as needed

⚠️ Disclaimer

This tool is for technical analysis education only. It does not guarantee results or constitute financial advice. Always use proper risk management and combine with other analysis methods. Past performance doesn't predict future results.

Bollinger Band Spread (Dunk)Bollinger Band Width measures the distance between the upper and lower Bollinger Bands. It reflects market volatility—wider bands mean higher volatility, narrower bands mean lower volatility.

When the width contracts to low levels, it can signal price consolidation and potential breakouts. When the width expands, it indicates active markets or strong trends.

Traders use it to spot volatility squeezes, confirm breakouts, and compare relative volatility across assets or timeframes.

[Kpt-Ahab] Assistant: Risk & DCA PlannerScript Description – Assistant: Risk & DCA Planner

The Risk & DCA Planner is a technical assistant for position and risk management.

It automatically calculates, based on volatility (ATR%), swing structure, and your settings:

Stop-Loss (SL) and corresponding Take-Profit targets (TPs) in R-multiples

DCA (Dollar-Cost-Averaging) levels — both price and amount

A market suitability check (based on volatility & volume)

Plus a clear table and summary label displayed on the chart

The script helps you plan risk, scaling, and profit targets consistently and quantitatively.

Core Logic

Risk Profile

Three modes: Low, Normal, High.

These define how reactive the script behaves internally:

Low → conservative, longer lookbacks, tighter analysis

Normal → balanced

High → aggressive, faster reaction, wider stops

Stop-Loss (SL)

Automatically calculated from ATR% and recent swing structure, limited by minimum and maximum thresholds.

The SL percentage defines the R-unit, which all TPs and DCA levels are based on.

Take-Profits (TPs)

Up to six targets, each a multiple of the defined risk (e.g., 1R, 2R, 3R).

Prices are automatically adjusted depending on long or short direction.

DCA Strategy

Optional. Adds scaling levels evenly between Entry and SL or in multiples of the ATR.

Each DCA allocation grows geometrically until the maximum position size is reached.

Suitability Check

Evaluates whether the market is within an appropriate ATR% range and has sufficient volume.

The table displays “OK” or “Caution” depending on volatility and historical consistency.

Visualization

Lines for SL, TPs, and DCA levels

A table with all parameters, prices, and risk data

A chart label summarizing key info (profile, direction, SL%, TPs, DCA, etc.)

XAUUSD Family Scalping (5min)🟡 XAUUSD Family Scalping 5-Min — Momentum Precision Indicator

Overview

This indicator is built for XAUUSD (Gold) on the 5-minute timeframe and is designed for short-term momentum scalping.

It helps traders identify early reversal zones, confirm momentum direction, and detect exhaustion points during high-volatility market moves.

Core Concept

The indicator measures momentum strength and price acceleration using a smoothed oscillator.

It features two adjustable thresholds:

Overbought level: 58

Oversold level: -58

When the momentum line crosses above or below these zones, it signals potential trend continuation or reversal opportunities.

Features

Detects short-term momentum shifts on XAUUSD 5M.

Works with EMA-based trend confirmation (optional).

Adaptive smoothing reduces noise and false reversals.

Highlights overbought/oversold areas visually.

Can be combined with price action or other oscillators for confluence.

Usage

Instrument: XAUUSD (Gold)

Best timeframe: 5-minute (scalping setup)

Use case: Detecting momentum exhaustion and reversal entries.

Sessions: London & New York recommended.

Disclaimer

This indicator is for market analysis and educational purposes.

No indicator guarantees profit — use proper risk management and test before live trading.

VIX Overnight Unch or Up AlertThis indicator alerts when VIX opens the day unchanged or higher on the day. If in fact VIX opens up unchanged or higher, it will display near the first bar of the day, previous day's close time and level and the opening time and level. The close time is typically 16:15 New York Time and the opening time is 09:30 or the first print a few minutes later. I use TVC:VIX instead of CBOT because TVC for me is real time. I also use the 1 minute chart and the script is coded as 1 minute.

Adaptive Volatility Bands | AlphaNattAdaptive Volatility Bands (AVB) | AlphaNatt

Professional-grade dynamic bands that adapt to market volatility and trend strength, featuring smooth gradient visualization for enhanced chart clarity.

🎯 CORE CONCEPT

AVB creates self-adjusting bands around a customizable basis line, expanding during trending markets and contracting during consolidation. The gradient fill provides instant visual feedback on price position within the volatility envelope.

✨ KEY FEATURES

5 Basis Types: Choose between SMA, EMA, ALMA, KAMA, or VWMA for the centerline calculation

Adaptive Band Width: Bands automatically widen in strong trends and tighten in ranging markets

Smooth Gradient Fills: 10-layer gradient on each side for professional depth visualization

Multiple Volatility Metrics: ATR, Standard Deviation, or Range-based calculations

Squeeze Detection: Identifies Bollinger/Keltner squeeze conditions for breakout anticipation

Dynamic Color States: Cyan (#00F1FF) for bullish, Magenta (#FF019A) for bearish conditions

📊 HOW IT WORKS

The basis line is calculated using your selected moving average type

Volatility is measured using ATR, StDev, or Range

Trend strength is quantified via linear regression

Band width adapts based on normalized trend strength (when enabled)

Gradient layers create smooth visual transitions from bands to basis

Color state changes based on price position and basis direction

🔧 PARAMETER GROUPS

Basis Configuration:

Basis Type: Moving average calculation method

Basis Length (20): Period for centerline calculation

ALMA Settings: Offset (0.85) and Sigma (6) for ALMA basis

Volatility Settings:

Volatility Method: ATR, Standard Deviation, or Range

Volatility Length (14): Lookback for volatility calculation

Band Multiplier (2.0): Distance of bands from basis

Adaptive Settings:

Enable Adaptive (true): Toggle dynamic band adjustment

Adaptation Period (50): Trend strength measurement window

Squeeze Detection:

BB/KC Parameters: Settings for squeeze identification

Expansion Threshold: Multiplier for expansion signals

📈 TRADING SIGNALS

Long Conditions:

Price crosses above basis

Basis line is rising

Band color shifts to cyan

Short Conditions:

Price crosses below basis

Basis line is falling

Band color shifts to magenta

💡 USAGE STRATEGIES

Trend Following: Trade with the basis direction when bands are expanding

Mean Reversion: Fade moves to outer bands during squeeze conditions

Breakout Trading: Enter on expansion signals after squeeze periods

Support/Resistance: Use bands as dynamic S/R levels

Position Sizing: Wider bands suggest higher volatility - adjust size accordingly

🎨 VISUAL ELEMENTS

Gradient Fills: 10 opacity layers creating smooth band transitions

Dynamic Colors: State-dependent coloring for instant trend recognition

Basis Line: Bold centerline changes color with trend state

Band Lines: Outer boundaries with matching state colors

⚡ BEST PRACTICES

The AVB indicator works optimally on liquid instruments with consistent volume. The adaptive feature performs best in trending markets but can generate false signals during choppy conditions. Consider using alongside momentum indicators for confirmation. The gradient visualization helps identify price position within the volatility envelope at a glance.

🔔 ALERTS INCLUDED

Long/Short Signals

Squeeze Conditions

Expansion Breakouts

Band Touch Events

Version 6 | Pine Script™ | © AlphaNatt

Sigma Volatility BandsThis indicator models and displays bands of potential future price based on historic realized volatility.

This can be used for finding price target where there is no past price action.

The price bands are derived from Standard Deviations based on input bars back of historic volatility.

More Inputs:

Lookback = Number of bars considered

Forward Bars = Number of bars to project bands forward

There are two display modes:

Forward shifted envelopes = (see below) Draws bands of price from the Standard Deviation

Forward for Anchor Lines = Draws a wedge out number of bars forward

(Vibe coded. Message me for suggested updates and improvements)

DTR & ATR with live zonesThis indicator is designed to help traders gauge the day's volatility in real-time. It compares the current Daily True Range (DTR)—the distance between the session's high and low—to the historical Average True Range (ATR).

The main purpose is to project potential price levels where the market might reach based on its average volatility. These levels (100% ATR, 150%, 200%, etc.) can be used as price targets. For instance, if you're in a long trade, you might consider taking partial or full profits as the price approaches these upper ATR extension levels. The indicator is highly customisable, allowing you to control the appearance of the ATR lines, zones, and labels to fit your charting preferences.

Core Concepts: ATR and DTR

To use this indicator effectively, it's important to understand its two main components:

Average True Range (ATR): This is a classic technical analysis indicator that measures market volatility. It calculates the average range of price movement over a specific period (e.g., 14 days). A higher ATR means the price is, on average, moving more, while a low ATR indicates less volatility. This script uses a higher timeframe ATR (e.g., Daily) to establish a stable volatility baseline for the current trading day.

Daily True Range (DTR): This is simply the difference between the current trading session's highest high and lowest low (session high - session low). It tells you how much the price has actually moved so far today.

The indicator's logic revolves around comparing the live, unfolding DTR to the historical, baseline ATR. An on-screen table conveniently shows this comparison as a percentage, to show how volatile the day has been.

How It Works: The Dynamic & Locked Mechanism

The most clever part of this indicator is how it draws the ATR levels. It operates in two distinct phases during the trading session:

Phase 1: Dynamic Expansion (Before DTR meets ATR)

At the start of the session, the DTR is small. The indicator calculates the remaining range needed to "complete" the 100% ATR level (difference = avg_atr - dtr). It then adds this remaining amount to the session high and subtracts it from the session low. This creates a "floating" 100% ATR range that expands dynamically as the session high or low is extended.

Phase 2: The Lock-in (After DTR meets or exceeds ATR)

Once the day's range (DTR) becomes equal to or greater than the avg_atr, the day has met its "expected" volatility. At this point, the levels lock in place. The indicator intelligently determines the anchor point for the locked range.

Once this primary 100% ATR range is established (either dynamically or locked), the script projects the other levels (150%, 200%, 250%, and 300%) by adding or subtracting multiples of the avg_atr from this base.

How to Use It for Trading

The primary use of this indicator is to set logical, volatility-based price targets.

Setting Profit Targets: If you enter a long position, the upper ATR levels (100%, 150%, 200%) serve as excellent areas to consider taking profits. A move to the 200% or 250% level often signifies an overextended or "exhaustion" move, making it a high-probability exit zone. For short positions, the lower ATR levels serve the same purpose.

Assessing Intraday Momentum: The on-screen table tells you how much of the expected daily range has been used. If it's early in the session and the DTR is only at 30% of the ATR, you can anticipate more significant price movement is likely to come. Conversely, if the DTR is already at 150% of ATR, the bulk of the day's move may already be complete.

Mean Reversion Signals: If the price pushes to an extreme level (e.g., 250% ATR) and shows signs of stalling (e.g., bearish divergence on an oscillator), it could signal a potential reversal or pullback, offering an opportunity for a counter-trend trade.

Key Settings

ATR Length & Smoothing Type: These settings control how the baseline ATR is calculated. The default 14 period and RMA smoothing are standard, but you can adjust them to your preference.

Session Settings: This is crucial. You must set the Market Session and Time Zone to match the primary trading hours of the asset you are analysing (e.g., "0930-1600" for the NYSE session).

Show Lines / Show Labels / Show Zones: The script gives you full control over the visual display. You can toggle each ATR level's lines, labels, and background zones individually to avoid a cluttered chart and focus only on the levels that matter to your strategy.

Nadaraya-Watson Envelope [Dynamic Adaptive Working]LuxAlgo'a kernel channel-based, modified for dynamic stochastic bandwidth adaptation.

Nadaraya-Watson Envelope , "NWE Adaptive (Working)"