Open Interest Z-Score [BackQuant]Open Interest Z-Score

A standardized pressure gauge for futures positioning that turns multi venue open interest into a Z score, so you can see how extreme current positioning is relative to its own history and where leverage is stretched, decompressing, or quietly re loading.

What this is

This indicator builds a single synthetic open interest series by aggregating futures OI across major derivatives venues, then standardises that aggregated OI into a rolling Z score. Instead of looking at raw OI or a simple change, you get a normalized signal that says "how many standard deviations away from normal is positioning right now", with optional smoothing, reference bands, and divergence detection against price.

You can render the Z score in several plotting modes:

Line for a clean, classic oscillator.

Colored line that encodes both sign and momentum of OI Z.

Oscillator histogram that makes impulses and compressions obvious.

The script also includes:

Aggregated open interest across Binance, Bybit, OKX, Bitget, Kraken, HTX, and Deribit, using multiple contract suffixes where applicable.

Choice of OI units, either coin based or converted to USD notional.

Standard deviation reference lines and adaptive extreme bands.

A flexible smoothing layer with multiple moving average types.

Automatic detection of regular and hidden divergences between price and OI Z.

Alerts for zero line and ±2 sigma crosses.

Aggregated open interest source

At the core is the same multi venue OI aggregation engine as in the OI RSI tool, adapted from NoveltyTrade's work and extended for this use case. The indicator:

Anchors on the current chart symbol and its base currency.

Loops over a set of exchanges, gated by user toggles:

Binance.

Bybit.

OKX.

Bitget.

Kraken.

HTX.

Deribit.

For each exchange, loops over several contract suffixes such as USDT.P, USD.P, USDC.P, USD.PM to cover the common perp and margin styles.

Requests OI candles for each exchange plus suffix pair into a small custom OI type that carries open, high, low and close of open interest.

Converts each OI stream into a common unit via the sw method:

In COIN mode, OI is normalized relative to the coin.

In USD mode, OI is scaled by price to approximate notional.

Exchange specific scaling factors are applied where needed to match contract multipliers.

Accumulates all valid OI candles into a single combined OI "candle" by summing open, high, low and close across venues.

The result is oiClose , a synthetic close for aggregated OI that represents cross venue positioning. If there is no valid OI data for the symbol after this process, the script throws a clear runtime error so you know the market is unsupported rather than quietly plotting nonsense.

How the Z score is computed

Once the aggregated OI close is available, the indicator computes a rolling Z score over a configurable lookback:

Define subject as the aggregated OI close.

Compute a rolling mean of this subject with EMA over Z Score Lookback Period .

Compute a rolling standard deviation over the same length.

Subtract the mean from the current OI and divide by the standard deviation.

This gives a raw Z score:

oi_z_raw = (subject − mean) ÷ stdDev .

Instead of plotting this raw value directly, the script passes it through a smoothing layer:

You pick a Smoothing Type and Smoothing Period .

Choices include SMA, HMA, EMA, WMA, DEMA, RMA, linear regression, ALMA, TEMA, and T3.

The helper ma function applies the chosen smoother to the raw Z score.

The result is oi_z , a smoothed Z score of aggregated open interest. A separate EMA with EMA Period is then applied on oi_z to create a signal line ma that can be used for crossovers and trend reads.

Plotting modes

The Plotting Type input controls how this Z score is rendered:

1) Line

In line mode:

The smoothed OI Z score is plotted as a single line using Base Line Color .

The EMA overlay is optionally plotted if Show EMA is enabled.

This is the cleanest view when you want to treat OI Z like a standard oscillator, watching for zero line crosses, swings, and divergences.

2) Colored Line

Colored line mode adds conditional color logic to the Z score:

If the Z score is above zero and rising, it is bright green, representing positive and strengthening positioning pressure.

If the Z score is above zero and falling, it shifts to a cooler cyan, representing positive but weakening pressure.

If the Z score is below zero and falling, it is bright red, representing negative and strengthening pressure (growing net de risking or shorting).

If the Z score is below zero and rising, it is dark red, representing negative but recovering pressure.

This mapping makes it easy to see not only whether OI is above or below its historical mean, but also whether that deviation is intensifying or fading.

3) Oscillator

Oscillator mode turns the Z score into a histogram:

The smoothed Z score is plotted as vertical columns around zero.

Column colors use the same conditional palette as colored line mode, based on sign and change direction.

The histogram base is zero, so bars extend up into positive Z and down into negative Z.

Oscillator mode is useful when you care about impulses in positioning, for example sharp jumps into positive Z that coincide with fast builds in leverage, or deep spikes into negative Z that show aggressive flushes.

4) None

If you only want reference lines, extreme bands, divergences, or alerts without the base oscillator, you can set plotting to None and keep the rest of the tooling active.

The EMA overlay respects plotting mode and only appears when a visible Z score line or histogram is present.

Reference lines and standard deviation levels

The Select Reference Lines input offers two styles:

Standard Deviation Levels

Plots small markers at zero.

Draws thin horizontal lines at +1, +2, −1 and −2 Z.

Acts like a classic Z score ladder, zero as mean, ±1 as normal band, ±2 as outer band.

This mode is ideal if you want a textbook statistical framing, using ±1 and ±2 sigma as standard levels for "normal" versus "extended" positioning.

Extreme Bands

Extreme bands build on the same ±1 and ±2 lines, then add:

Upper outer band between +3 and +4 Z.

Lower outer band between −3 and −4 Z.

Dynamic fill colors inside these bands:

If the Z score is positive, the upper band fill turns red with an alpha that scales with the magnitude of |Z|, capped at a chosen max strength. Stronger deviations towards +4 produce more opaque red fills.

If the Z score is negative, the lower band fill turns green with the same adaptive alpha logic, highlighting deep negative deviations.

Opposite side bands remain a faint neutral white when not in use, so they still provide structural context without shouting.

This creates a visual "danger zone" for position crowding. When the Z score enters these outer bands, open interest is many standard deviations away from its mean and you are dealing with rare but highly loaded positioning states.

Z score as a positioning pressure gauge

Because this is a Z score of aggregated open interest, it measures how unusual current positioning is relative to its own recent history, not just whether OI is rising or falling:

Z near zero means total OI is roughly in line with normal conditions for your lookback window.

Positive Z means OI is above its recent mean. The further above zero, the more "crowded" or extended positioning is.

Negative Z means OI is below its recent mean. Deep negatives often mark post flush environments where leverage has been cleared and the market is under positioned.

The smoothing options help control how much noise you want in the signal:

Short Z score lookback and short smoothing will react quickly, suited for short term traders watching intraday positioning shocks.

Longer Z score lookback with smoother MA types (EMA, RMA, T3) give a slower, more structural view of where the crowd sits over days to weeks.

Divergences between price and OI Z

The indicator includes automatic divergence detection on the Z score versus price, using pivot highs and lows:

You configure Pivot Lookback Left and Pivot Lookback Right to control swing sensitivity.

Pivots are detected on the OI Z series.

For each eligible pivot, the script compares OI Z and price at the last two pivots.

It looks for four patterns:

Regular Bullish – price makes a lower low, OI Z makes a higher low. This can indicate selling exhaustion in positioning even as price washes out. These are marked with a line and a label "ℝ" below the oscillator, in the bullish color.

Hidden Bullish – price makes a higher low, OI Z makes a lower low. This suggests continuation potential where price holds up while positioning resets. Marked with "ℍ" in the bullish color.

Regular Bearish – price makes a higher high, OI Z makes a lower high. This is a classic warning sign of trend exhaustion, where price pushes higher while OI Z fails to confirm. Marked with "ℝ" in the bearish color.

Hidden Bearish – price makes a lower high, OI Z makes a higher high. This is often seen in pullbacks within downtrends, where price retraces but positioning stretches again in the direction of the prevailing move. Marked with "ℍ" in the bearish color.

Each divergence type can be toggled globally via Show Detected Divergences . Internally, the script restricts how far back it will connect pivots, so you do not get stray signals linking very old structures to current bars.

Trading applications

Crowding and squeeze risk

Z scores are a natural way to talk about crowding:

High positive Z in aggregated OI means the market is running high leverage compared to its own norm. If price is also extended, the risk of a squeeze or sharp unwind rises.

Deep negative Z means leverage has been cleaned out. While it can be painful to sit through, this environment often sets up cleaner new trends, since there is less one sided positioning to unwind.

The extreme bands at ±3 to ±4 highlight the rare states where crowding is most intense. You can treat these events as regime markers rather than day to day noise.

Trend confirmation and fade selection

Combine Z score with price and trend:

Bull trends with positive and rising Z are supported by fresh leverage, usually more persistent.

Bull trends with flat or falling Z while price keeps grinding up can be more fragile. Divergences and extreme bands can help identify which edges you do not want to fade and which you might.

In downtrends, deep negative Z that stays pinned can mean persistent de risking. Once the Z score starts to mean revert back toward zero, it can mark the early stages of stabilization.

Event and liquidation context

Around major events, you often see:

Rapid spikes in Z as traders rush to position.

Reversal and overshoot as liquidations and forced de risking clear the book.

A move from positive extremes through zero into negative extremes as the market transitions from crowded to under exposed.

The Z score makes that path obvious, especially in oscillator mode, where you see a block of high positive bars before the crash, then a slab of deep negative bars after the flush.

Settings overview

Z Score group

Plotting Type – None, Line, Colored Line, Oscillator.

Z Score Lookback Period – window used for mean and standard deviation on aggregated OI.

Smoothing Type – SMA, HMA, EMA, WMA, DEMA, RMA, linear regression, ALMA, TEMA or T3.

Smoothing Period – length for the selected moving average on the raw Z score.

Moving Average group

Show EMA – toggle EMA overlay on Z score.

EMA Period – EMA length for the signal line.

EMA Color – color of the EMA line.

Thresholds and Reference Lines group

Select Reference Lines – None, Standard Deviation Levels, Extreme Bands.

Standard deviation lines at 0, ±1, ±2 appear in both modes.

Extreme bands add filled zones at ±3 to ±4 with adaptive opacity tied to |Z|.

Extra Plotting and UI

Base Line Color – default color for the simple line mode.

Line Width – thickness of the oscillator line.

Positive Color – positive or bullish condition color.

Negative Color – negative or bearish condition color.

Divergences group

Show Detected Divergences – master toggle for divergence plotting.

Pivot Lookback Left and Pivot Lookback Right – how many bars left and right to define a pivot, controlling divergence sensitivity.

Open Interest Source group

OI Units – COIN or USD.

Exchange toggles for Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit.

Internally, all enabled exchanges and contract suffixes are aggregated into one synthetic OI series.

Alerts included

The indicator defines alert conditions for several key events:

OI Z Score Positive – Z crosses above zero, aggregated OI moves from below mean to above mean.

OI Z Score Negative – Z crosses below zero, aggregated OI moves from above mean to below mean.

OI Z Score Enters +2σ – Z enters the +2 band and above, marking extended positive positioning.

OI Z Score Enters −2σ – Z enters the −2 band and below, marking extended negative positioning.

Tie these into your strategy to be notified when leverage moves from normal to extended states.

Notes

This indicator does not rely on price based oscillators. It is a statistical lens on cross venue open interest, which makes it a complementary tool rather than a replacement for your existing price or volume signals. Use it to:

Quantify how unusual current futures positioning is compared to recent history.

Identify crowded leverage phases that can fuel squeezes.

Spot structural divergences between price and positioning.

Frame risk and opportunity around events and regime shifts.

It is not a complete trading system. Combine it with your own entries, exits and risk rules to get the most out of what the Z score is telling you about positioning pressure under the hood of the market.

Backquant

Open Interest RSI [BackQuant]Open Interest RSI

A multi-venue open interest oscillator that aggregates OI across major derivatives exchanges, converts it to coin or USD terms, and runs an RSI-style engine on that aggregated OI so you can track positioning pressure, crowding, and mean reversion in leverage flows, not just in price.

What this is

This tool is an RSI built on top of aggregated open interest instead of price. It pulls futures OI from several major exchanges, converts it into a unified unit (COIN or USD), sums it into a single synthetic OI candle, then applies RSI and smoothing to that combined series.

You can then render that Open Interest RSI in different visual modes:

Clean line or colored line for classic oscillator-style reads.

Column-style oscillator for impulse and compression views.

Flag mode that fills between OI RSI and its EMA for trend/mean reversion blends. See:

Heatmap mode that paints the panel based on OI RSI extremes, ideal for scanning. See:

On top of that it includes:

Aggregated OI source selection (Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit).

Choice of OI units (COIN or USD).

Reference lines and OB/OS zones.

Extreme highlighting for either trend or mean reversion.

A vertical OI RSI meter that acts as a quick strength gauge.

Aggregated open interest source

Under the hood, the indicator builds a synthetic open interest candle by:

Looping over a list of supported exchanges: Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit.

Looping over multiple contract suffixes (such as USDT.P, USD.P, USDC.P, USD.PM) to capture different contract types on each venue.

Requesting OI candles from each venue + contract combination for the same underlying symbol.

Converting each OI stream into a common unit: In COIN mode, everything is normalized into coin-denominated OI. In USD mode, coin OI is multiplied by price to approximate notional OI.

Summing up open, high, low and close of OI across venues into a single aggregated OI candle.

If no valid OI is available for the current symbol across all sources, the script throws a clear runtime error so you know you are on an unsupported market.

This gives you a single, exchange-agnostic open interest curve instead of being tied to one venue. That aggregated OI is then passed into the RSI logic.

How the OI RSI is calculated

The RSI side is straightforward, but it is applied to the aggregated OI close:

Compute a base RSI of aggregated OI using the Calculation Period .

Apply a simple moving average of length Smoothing Period (SMA) to reduce noise in the raw OI RSI.

Optionally apply an EMA on top of the smoothed OI RSI as a moving average signal line.

Key parameters:

Calculation Period – base RSI length for OI.

Smoothing Period (SMA) – extra smoothing on the RSI value.

EMA Period – EMA length on the smoothed OI RSI.

The result is:

oi_rsi – raw RSI of aggregated OI.

oi_rsi_s – SMA-smoothed OI RSI.

ma – EMA of the smoothed OI RSI.

Thresholds and extremes

You control three core thresholds:

Mid Point – central reference level, typically 50.

Extreme Upper Threshold – high-level OI RSI edge (for example 80).

Extreme Lower Threshold – low-level OI RSI edge (for example 20).

These thresholds are used for:

Reference lines or OB/OS zone fills.

Heatmap gradient bounds.

Background highlighting of extremes.

The Extreme Highlighting mode controls how extremes are interpreted:

None – do nothing special in extreme regions.

Mean-Rev – background turns red on high OI RSI and green on low OI RSI, framing extremes as contrarian zones.

Trend – background turns green on high OI RSI and red on low OI RSI, framing extremes as participation zones aligned with the prevailing move.

Reference lines and OB/OS zones

You can choose:

None – clean plotting without guides.

Basic Reference Lines – mid, upper and lower thresholds as simple gray horizontals.

OB/OS Levels – filled zones between:

Upper OB: from the upper threshold to 100, colored with the short/overbought color.

Lower OS: from 0 to the lower threshold, colored with the long/oversold color.

These guides help visually anchor the OI RSI within "normal" versus "extreme" regions.

Plotting modes

The Plotting Type input controls how OI RSI is drawn. All modes share the same underlying OI and RSI logic, but emphasise different aspects of the signal.

1) Line mode

This is the classic oscillator representation:

Plots the smoothed OI RSI as a simple line using RSI Line Color and RSI Line Width .

Optionally plots the EMA overlay on the same panel.

Works well when you want standard RSI-style signals on leverage flows: crosses of the midline, divergences versus price, and so on.

2) Colored Line mode

In this mode:

The OI RSI is plotted as a line, but its color is dynamic.

If the smoothed OI RSI is above the mid point, it uses the Long/OB Color .

If it is below the mid point, it uses the Short/OS Color .

This creates an instant visual regime switch between "bullish positioning pressure" and "bearish positioning pressure", while retaining the feel of a traditional RSI line.

3) Oscillator mode

Oscillator mode renders OI RSI as vertical columns around the mid level:

The smoothed OI RSI is plotted as columns using plot.style_columns .

The histogram base is fixed at 50, so bars extend above and below the mid line.

Bar color is dynamic, using long or short colors depending on which side of the mid point the value sits.

This representation makes impulse and compression in OI flows more obvious. It is especially useful when you want to focus on how quickly OI RSI is expanding or contracting around its neutral level. See:

4) Flag mode

Flag mode turns OI RSI and its EMA into a two-line band with a filled area between them:

The smoothed OI RSI and its EMA are both plotted.

A fill is drawn between them.

The fill color flips between the long color and the short color depending on whether OI RSI is above or below its EMA.

Black outlines are added to both lines to make the band clear against any background.

This creates a "flag" style region where:

Green fills show OI RSI leading its EMA, suggesting positive positioning momentum.

Red fills show OI RSI trailing below its EMA, suggesting negative positioning momentum.

Crossovers of the two lines can be read as shifts in OI momentum regime.

Flag mode is useful if you want a more structural view that combines both the level and slope behaviour of OI RSI. See:

5) Heatmap mode

Heatmap mode recasts OI RSI as a single-row gradient instead of a line:

A single row at level 1 is plotted using column style.

The color is pulled from a gradient between the lower and upper thresholds: Near the lower threshold it approaches the short/oversold color and near the upper threshold it approaches the long/overbought color.

The EMA overlay and reference lines are disabled in this mode to keep the panel clean.

This is a very compact way to track OI RSI state at a glance, especially when stacking it alongside other indicators. See:

OI RSI vertical meter

Beyond the main plot, the script can draw a small "thermometer" table showing the current OI RSI position from 0 to 100:

The meter is a two-column table with a configurable number of rows.

Row colors form an inverted gradient: red at the top (100) and green at the bottom (0).

The script clamps OI RSI between 0 and 100 and maps it to a row index.

An arrow marker "▶" is drawn next to the row corresponding to the current OI RSI value.

0 and 100 labels are printed at the ends of the scale for orientation.

You control:

Show OI RSI Meter – turn the meter on or off.

OI RSI Blocks – number of vertical blocks (granularity).

OI RSI Meter Position – panel anchor (top/bottom, left/center/right).

The meter is particularly helpful if you keep the main plot in a small panel but still want an intuitive strength gauge.

How to read it as a market pressure gauge

Because this is an RSI built on aggregated open interest, its extremes and regimes speak to positioning pressure rather than price alone:

High OI RSI (near or above the upper threshold) indicates that open interest has been increasing aggressively relative to its recent history. This often coincides with crowded leverage and a buildup of directional pressure.

Low OI RSI (near or below the lower threshold) indicates aggressive de-leveraging or closing of positions, often associated with flushes, forced unwinds or post-liquidation clean-ups.

Values around the mid point indicate more balanced positioning flows.

You can combine this with price action:

Price up with rising OI RSI suggests fresh leverage joining the move, a more persistent trend.

Price up with falling OI RSI suggests shorts covering or longs taking profit, more fragile upside.

Price down with rising OI RSI suggests aggressive new shorts or levered selling.

Price down with falling OI RSI suggests de-leveraging and potential exhaustion of the move.

Trading applications

Trend confirmation on leverage flows

Use OI RSI to confirm or question a price trend:

In an uptrend, rising OI RSI with values above the mid point indicates supportive leverage flows.

In an uptrend, repeated failures to lift OI RSI above mid point or persistent weakness suggest less committed participation.

In a downtrend, strong OI RSI on the downside points to aggressive shorting.

Mean reversion in positioning

Use thresholds and the Mean-Rev highlight mode:

When OI RSI spends extended time above the upper threshold, the crowd is extended on one side. That can set up squeeze risk in the opposite direction.

When OI RSI has been pinned low, it suggests heavy de-leveraging. Once price stabilises, a re-risking phase is often not far away.

Background colours in Mean-Rev mode help visually identify these periods.

Regime mapping with plotting modes

Different plotting modes give different perspectives:

Heatmap mode for dashboard-style use where you just need to know "hot", "neutral" or "cold" on OI flows at a glance.

Oscillator mode for short term impulses and compression reads around the mid line. See:

Flag mode for blending level and trend of OI RSI into a single banded visual. See:

Settings overview

RSI group

Plotting Type – None, Line, Colored Line, Oscillator, Flag, Heatmap.

Calculation Period – base RSI length for OI.

Smoothing Period (SMA) – smoothing on RSI.

Moving Average group

Show EMA – toggle EMA overlay (not used in heatmap).

EMA Period – length of EMA on OI RSI.

EMA Color – colour of EMA line.

Thresholds group

Mid Point – central reference.

Extreme Upper Threshold and Extreme Lower Threshold – OB/OS thresholds.

Select Reference Lines – none, basic lines or OB/OS zone fills.

Extreme Highlighting – None, Mean-Rev, Trend.

Extra Plotting and UI

RSI Line Color and RSI Line Width .

Long/OB Color and Short/OS Color .

Show OI RSI Meter , OI RSI Blocks , OI RSI Meter Position .

Open Interest Source

OI Units – COIN or USD.

Exchange toggles: Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit.

Notes

This is a positioning and pressure tool, not a complete system. It:

Models aggregated futures open interest across multiple centralized exchanges.

Transforms that OI into an RSI-style oscillator for better comparability across regimes.

Offers several visual modes to match different workflows, from detailed analysis to compact dashboards.

Use it to understand how leverage and positioning are evolving behind the price, to gauge when the crowd is stretched, and to decide whether to lean with or against that pressure. Attach it to your existing signals, not in place of them.

Also, please check out @NoveltyTrade for the OI Aggregation logic & pulling the data source!

Here is the original script:

PoC Migration Map [BackQuant]PoC Migration Map

A volume structure tool that builds a side volume profile, extracts rolling Points of Control (PoCs), and maps how those PoCs migrate through time so you can see where value is moving, how volume clusters shift, and how that aligns with trend regime.

What this is

This indicator combines a classic volume profile with a segmented PoC trail. It looks back over a configurable window, splits that window into bins by price, and shows you where volume has concentrated. On top of that, it slices the lookback into fixed bar segments, finds the local PoC in each segment, and plots those PoCs as a chain of nodes across the chart.

The result is a "migration map" of value:

A side volume profile that shows how volume is distributed over the recent price range.

A sequence of PoC nodes that show where local value has been accepted over time.

Lines that connect those PoCs to reveal the path of value migration.

Optional trend coloring based on EMA 12 and EMA 21, so each PoC also encodes trend regime.

Used together, this gives you a structural read on where the market has actually traded size, how "value" is moving, and whether that movement is aligned or fighting the current trend.

Core components

Lookback volume profile - a side histogram built from all closes and volumes in the chosen lookback window.

Segmented PoC trail - rolling PoCs computed over fixed bar segments, plotted as nodes in time.

Trend heatmap - optional color mapping of PoC nodes using EMA 12 versus EMA 21.

PoC labels - optional labels on every Nth PoC for easier reading and referencing.

How it works

1) Global lookback and binning

You choose:

Lookback Bars - how far back to collect data.

Number of Bins - how finely to split the price range.

The script:

Finds the highest high and lowest low in the lookback.

Computes the total price range and divides it into equal binCount slices.

Assigns each bar's close and volume into the appropriate price bin.

This creates a discretized volume distribution across the entire lookback.

2) Side volume profile

If "Show Side Profile" is enabled, a right-hand volume profile is drawn:

Each bin becomes a horizontal bar anchored at a configurable "Right Offset" from the current bar.

The horizontal width of each bar is proportional to that bin's volume relative to the maximum volume bin.

Optionally, volume values and percentages are printed inside the profile bars.

Color and transparency are controlled by:

Base Profile Color and its transparency.

A gradient that uses relative volume to modulate opacity between lower volume and higher volume bins.

Profile Width (%) - how wide the maximum bin can extend in bars.

This gives you an at-a-glance view of the volume landscape for the chosen lookback window.

3) Segmenting for PoC migration

To build the PoC trail, the lookback is divided into segments:

Bars per Segment - bars in each local cluster.

Number of Segments - how many segments you want to see back in time.

For each segment:

The script uses the same price bins and accumulates volume only from bars in that segment.

It finds the bin with the highest volume in that segment, which is the local PoC for that segment.

It sets the PoC price to the center of that bin.

It finds the "mid bar" of the segment and places the PoC node at that time on the chart.

This is repeated for each segment from older to newer, so you get a chain of PoCs that shows how local value has migrated over time.

4) Trend regime and color coding

The indicator precomputes:

EMA 12 (Fast).

EMA 21 (Slow).

For each PoC:

It samples EMA 12 and EMA 21 at the mid bar of that segment.

It computes a simple trend score as fast EMA minus slow EMA.

If trend heatmap is enabled, PoC nodes (and the lines between them) are colored by:

Trend Up Color if EMA 12 is above EMA 21.

Trend Down Color if EMA 12 is below EMA 21.

Trend Flat Color if they are roughly equal.

If the trend heatmap is disabled, PoC color is instead based on PoC migration:

If the current PoC is above the previous PoC, use the Up PoC Color.

If the current PoC is below the previous PoC, use the Down PoC Color.

If unchanged, use the Flat PoC Color.

5) Connecting PoCs and labels

Once PoC prices and times are known:

Each PoC is connected to the previous one with a dotted line, using the PoC's color.

Optional labels are placed next to every Nth PoC:

Label text uses a simple "PoC N" scheme.

Label background uses a configurable label background color.

Label border is colored by the PoC's own color for visual consistency.

This turns the PoCs into a visual path that can be read like a "value trajectory" across the chart.

What it plots

When fully enabled, you will see:

A right-sided volume profile for the chosen lookback window, built from volume by price.

Colored horizontal bars representing each price bin's relative volume.

Optional volume text showing each bin's volume and its percentage of the profile maximum.

A series of PoC nodes spaced across the chart at the mid point of each segment.

Dotted lines connecting those PoCs to show the migration path of value.

Optional PoC labels at each Nth node for easier reference.

Color-coding of PoCs and lines either by EMA 12 / 21 trend regime or by up/down PoC drift.

Reading PoC migration and market pressure

Side profile as a pressure map

The side profile shows where trading has been most active:

Thick, opaque bars represent high volume zones and possible high interest or acceptance areas.

Thin, faint bars represent low volume zones, potential rejection or transition areas.

When price trades near a high volume bin, the market is sitting on an area of prior acceptance and size.

When price moves quickly through low volume bins, it often does so with less friction.

This gives you a static map of where the market has been willing to do business within your lookback.

PoC trail as a value migration map

The PoC chain represents "where value has lived" over time:

An upward sloping PoC trail indicates value migrating higher. Buyers have been willing to transact at increasingly higher prices.

A downward sloping trail indicates value migrating lower and sellers pushing the center of mass down.

A flat or oscillating trail indicates balance or rotational behaviour, with no clear directional acceptance.

Taken together, you can interpret:

Side profile as "where the volume mass sits", a static pressure field.

PoC trail as "how that mass has moved", the dynamic path of value.

Trend heatmap as a regime overlay

When PoCs are colored by the EMA 12 / 21 spread:

Green PoCs mark segments where the faster EMA is above the slower EMA, that is, a local uptrend regime.

Red PoCs mark segments where the faster EMA is below the slower EMA, that is, a local downtrend regime.

Gray PoCs mark flat or ambiguous trend segments.

This lets you answer questions like:

"Is value migrating higher while the trend regime is also up?" (trend confirming value).

"Is value migrating higher but most PoCs are red?" (value against the prevailing trend).

"Has value started to roll over just as PoCs flip from green to red?" (early regime transition).

Key settings

General Settings

Lookback Bars - how many bars back to use for both the global volume profile and segment profiles.

Number of Bins - how many price bins to split the high to low range into.

Profile Settings

Show Side Profile - toggle the right-hand volume profile on or off.

Profile Width (%) - how wide the largest volume bar is allowed to be in terms of bars.

Base Profile Color - the starting color for profile bars, with transparency.

Show Volume Values - if enabled, print volume and percent for each non-zero bin.

Profile Text Color - color for volume text inside the profile.

PoC Migration Settings

Show PoC Migration - toggle the PoC trail plotting.

Bars per Segment - the number of bars contained in each segment.

Number of Segments - how many segments to build backwards from the current bar.

Horizontal Spacing (bars) - spacing between PoC nodes when drawn. (Used to separate PoCs horizontally.)

Label Every Nth PoC - draw labels at every Nth PoC (0 or 1 to suppress labels).

Right Offset (bars) - horizontal offset to anchor the side profile on the right.

Up PoC Color - color used when a PoC is higher than the previous one, if trend heatmap is off.

Down PoC Color - color used when a PoC is lower than the previous one, if trend heatmap is off.

Flat PoC Color - color used when the PoC is unchanged, if trend heatmap is off.

PoC Label Background - background color for PoC labels.

Trend Heatmap Settings

Color PoCs By Trend (EMA 12 / 21) - when enabled, overrides simple up/down coloring and uses EMA-based trend colors.

Fast EMA - length for the fast EMA.

Slow EMA - length for the slow EMA.

Trend Up Color - color for PoCs in a bullish EMA regime.

Trend Down Color - color for PoCs in a bearish EMA regime.

Trend Flat Color - color for neutral or flat EMA regimes.

Trading applications

1) Value migration and trend confirmation

Use the PoC path to see if value is following price or lagging it:

In a healthy uptrend, price, PoCs, and trend regime should all lean higher.

In a weakening trend, price may still move up, but PoCs flatten or start drifting lower, suggesting fewer participants are accepting the new highs.

In a downtrend, persistent downward PoC migration confirms that sellers are winning the value battle.

2) Identifying acceptance and rejection zones

Combine the side profile with PoC locations:

High volume bins near clustered PoCs mark strong acceptance zones, good areas to watch for re-tests and decision points.

PoCs that quickly jump across low volume areas can indicate rejection and fast repricing between value zones.

High volume zones with mixed PoC colors may signal balance or prolonged negotiation.

3) Structuring entries and exits

Use the map to refine trade location:

Fade trades against value migration are higher risk unless you see clear signs of exhaustion or regime change.

Pullbacks into prior PoC zones in the direction of the current PoC slope can offer higher quality entries.

Stops placed beyond major accepted zones (clusters of PoCs and high volume bins) are less likely to be hit by random noise.

4) Regime transitions

Watch how PoCs behave as the EMA regime changes:

A flip in EMA 12 versus EMA 21, coupled with a turn in PoC slope, is a strong signal that value is beginning to move with the new trend.

If EMAs flip but PoC migration does not follow, the trend signal may be early or false.

A weakening PoC path (lower highs in PoCs) while trend colors are still green can warn of a late-stage trend.

Best practices

Start with a moderate lookback such as 200 to 300 bars and a moderate bin count such as 20 to 40. Too many bins can make the profile overly granular and sparse.

Align "Bars per Segment" with your trading horizon. For example, 5 to 10 bars for intraday, 10 to 20 bars for swing.

Use the profile and PoC trail as structural context rather than as a direct buy or sell signal. Combine with your existing setups for timing.

Pay attention to clusters of PoCs at similar prices. Those are areas where the market has repeatedly accepted value, and they often matter on future tests.

Notes

This is a structural volume tool, not a complete trading system. It does not manage execution, position sizing or risk management. Use it to understand:

Where the bulk of trading has occurred in your chosen window.

How the center of volume has migrated over time.

Whether that migration is aligned with or fighting the current trend regime.

By turning PoC evolution into a visible path and adding a trend-aware heatmap, the PoC Migration Map makes it easier to see how value has been moving, where the market is likely to feel "heavy" or "light", and how that structure fits into your trading decisions.

Relative Strength Heatmap [BackQuant]Relative Strength Heatmap

A multi-horizon RSI matrix that compresses 20 different lookbacks into a single panel, turning raw momentum into a visual “pressure gauge” for overbought and oversold clustering, trend exhaustion, and breadth of participation across time horizons.

What this is

This indicator builds a strip-style heatmap of 20 RSIs, each with a different length, and stacks them vertically as colored tiles in a single pane. Every tile is colored by its RSI value using your chosen palette, so you can see at a glance:

How many “fast” versus “slow” RSIs are overbought or oversold.

Whether momentum is concentrated in the short lookbacks or spread across the whole curve.

When momentum extremes cluster, signalling strong market pressure or exhaustion.

On top of the tiles, the script plots two simple breadth lines:

A white line that counts how many RSIs are above 70 (overbought cluster).

A black line that counts how many RSIs are below 30 (oversold cluster).

This turns a single symbol’s RSI ladder into a compact “market pressure gauge” that shows not only whether RSI is overbought or oversold, but how many different horizons agree at the same time.

Core idea

A single RSI looks at one length and one timescale. Markets, however, are driven by flows that operate on multiple horizons at once. By computing RSI over a ladder of lengths, you approximate a “term structure” of strength:

Short lengths react to immediate swings and very recent impulses.

Medium lengths reflect swing behaviour and local trends.

Long lengths reflect structural bias and higher timeframe regime.

When many lengths agree, for example 10 or more RSIs all above 70, it suggests broad participation and strong directional pressure. When only a few fast lengths stretch to extremes while longer ones stay neutral, the move is more fragile and more likely to mean-revert.

This script makes that structure visible as a heatmap instead of forcing you to run many separate RSI panes.

How it works

1) Generating RSI lengths

You control three parameters in the calculation settings:

RS Period – the base RSI length used for the shortest strip.

RSI Step – the amount added to each successive RSI length.

RSI Multiplier – a global scaling factor applied after the step.

Each of the 20 RSIs uses:

RSI length = round((base_length + step × index) × multiplier) , where the index goes from 0 to 19.

That means:

RSI 1 uses (len + step × 0) × mult.

RSI 2 uses (len + step × 1) × mult.

…

RSI 20 uses (len + step × 19) × mult.

You can keep the ladder dense (small step and multiplier) or stretch it across much longer horizons.

2) Heatmap layout and grouping

Each RSI is plotted as an “area” strip at a fixed vertical level using histbase to stack them:

RSI 1–5 form Group 1.

RSI 6–10 form Group 2.

RSI 11–15 form Group 3.

RSI 16–20 form Group 4.

Each group has a toggle:

Show only Group 1 and 2 if you care mainly about fast and medium horizons.

Show all groups for a full spectrum from very short to very long.

Hide any group that feels redundant for your workflow.

The actual numeric RSI values are not plotted as lines. Instead, each strip is drawn as a horizontal band whose fill color represents the current RSI regime.

3) Palette-based coloring

Each tile’s color is driven by the RSI value and your chosen palette. The script includes several palettes:

Viridis – smooth green to yellow, good for subtle reading.

Jet – strong blue to red sequence with high contrast.

Plasma – purple through orange to yellow.

Custom Heat – cool blues to neutral grey to hot reds.

Gray – grayscale from white to black for minimalistic layouts.

Cividis, Inferno, Magma, Turbo, Rainbow – additional scientific and rainbow-style maps.

Internally, RSI values are bucketed into ranges (for example, below 10, 10–20, …, 90–100). Each bucket maps to a unique colour for that palette. In all schemes, low RSI values are mapped to the “cold” or darker side and high RSI values to the “hot” or brighter side.

The result is a true momentum heatmap:

Cold or dark tiles show low RSI and oversold or compressed conditions.

Mid tones show neutral or mid-range RSI.

Warm or bright tiles show high RSI and overbought or stretched conditions.

4) Bull and bear breadth counts

All 20 RSI values are collected into an array each bar. Two counters are then calculated:

Bull count – how many RSIs are above 70.

Bear count – how many RSIs are below 30.

These are plotted as:

A white line (“RSI > 70 Count”) for the overbought cluster.

A black line (“RSI < 30 Count”) for the oversold cluster.

If you enable the “Show Bull and Bear Count” option, you get an immediate reading of how many of the 20 horizons are stretched at any moment.

5) Cluster alerts and background tagging

Two alert conditions monitor “strong cluster” regimes:

RSI Heatmap Strong Bull – triggers when at least 10 RSIs are above 70.

RSI Heatmap Strong Bear – triggers when at least 10 RSIs are below 30.

When one of these conditions is true, the indicator can tint the background of the chart using a soft version of the current palette. This visually marks stretches where momentum is extreme across many lengths at once, not just on a single RSI.

What it plots

In one oscillator window, the indicator provides:

Up to 20 horizontal RSI strips, each representing a different RSI length.

Color-coded tiles reflecting the current RSI value for each length.

Group toggles to show or hide each block of five RSIs.

An optional white line that counts how many RSIs are above 70.

An optional black line that counts how many RSIs are below 30.

Optional background highlights when the number of overbought or oversold RSIs passes the strong-cluster threshold.

How it measures breadth and pressure

Single-symbol breadth

Breadth is usually defined across a basket of symbols, such as how many stocks advance versus decline. This indicator uses the same concept across time horizons for a single symbol. The question becomes:

“How many different RSI lengths are stretched in the same direction at once?”

Examples:

If only 2 or 3 of the shortest RSIs are above 70, bull count stays low. The move is fast and local, but not yet broadly supported.

If 12 or more RSIs across short, medium and long lengths are above 70, the bull count spikes. The move has broad momentum and strong upside pressure.

If 10 or more RSIs are below 30, bear count spikes and you are in a broad oversold regime.

This is breadth of momentum within one market.

Market pressure gauge

The combination of heatmap tiles and breadth lines acts as a pressure gauge:

High bull count with warm colors across most strips indicates strong upside pressure and crowded long positioning.

High bear count with cold colors across most strips indicates strong downside pressure and capitulation or forced selling.

Low counts with a mixed heatmap indicate neutral pressure, fragmented flows, or range-bound conditions.

You can treat the strong-cluster alerts as “extreme pressure” signals. When they fire, the market is heavily skewed in one direction across many horizons.

How to read the heatmap

Horizontal patterns (through time)

Look along the time axis and watch how the colors evolve:

Persistent hot tiles across many strips show sustained bullish pressure and trend strength.

Persistent cold tiles across many strips show sustained bearish pressure and weak demand.

Frequent flipping between hot and cold colours indicates a choppy or mean-reverting environment.

Vertical structure (across lengths at one bar)

Focus on a single bar and read the column of tiles from top to bottom:

Short RSIs hot, long RSIs neutral or cool: early trend or short-term fomo. Price has moved fast, longer horizons have not caught up.

Short and long RSIs all hot: mature, entrenched uptrend. Broad participation, high pressure, greater risk of blow-off or late-entry vulnerability.

Short RSIs cold but long RSIs mid to high: pullback in a higher timeframe uptrend. Dip-buy and continuation setups are often found here.

Short RSIs high but long RSIs low: countertrend rallies within a broader downtrend. Good hunting ground for fades and short entries after a bounce.

Bull and bear breadth lines

Use the two lines as simple, numeric breadth indicators:

A rising white line shows more RSIs pushing above 70, so bullish pressure is expanding in breadth.

A rising black line shows more RSIs pushing below 30, so bearish pressure is expanding in breadth.

When both lines are low and flat, few horizons are extreme and the market is in mid-range territory.

Cluster zones

When either count crosses the strong threshold (for example 10 out of 20 RSIs in extreme territory):

A strong bull cluster marks a broadly overbought regime. Trend followers may see this as confirmation. Mean-reversion traders may see it as a late-stage or blow-off context.

A strong bear cluster marks a broadly oversold regime. Downtrend traders see strong pressure, but the risk of sharp short-covering bounces also increases.

Trading applications

Trend confirmation

Use the heatmap and breadth lines as a trend filter:

Prefer long setups when the heatmap shows mostly mid to high RSIs and the bull count is rising.

Avoid fresh shorts when there is a strong bull cluster, unless you are specifically trading exhaustion.

Prefer short setups when the heatmap is mostly low RSIs and the bear count is rising.

Avoid aggressive longs when a strong bear cluster is active, unless you are trading reflexive bounces.

Mean-reversion timing

Treat cluster extremes as exhaustion zones:

Look for reversal patterns, failed breakouts, or order flow shifts when bull count is very high and price starts to stall or diverge.

Look for reflexive bounce potential when bear count is very high and price stops making new lows or shows absorption at the lows.

Use the palette and counts together: hot tiles plus a peaking white line can mark blow-off conditions, cold tiles plus a peaking black line can mark capitulation.

Regime detection and risk toggling

Use the overall shape of the ladder over time:

If upper strips stay warm and lower strips stay neutral or warm for extended periods, the market is in an uptrend regime. You can justify higher risk for long-biased strategies.

If upper strips stay cold and lower strips stay neutral or cold, the market is in a downtrend regime. You can justify higher risk for short-biased strategies or defensive positioning.

If colours and counts flip frequently, you are likely in a range or choppy regime. Consider reducing size or using more tactical, short-term strategies.

Multi-horizon synchronization

You can think of each RSI length as a proxy for a different “speed” of the same market:

When only fast RSIs are stretched, the move is local and less robust.

When fast, medium and slow RSIs align, the move has multi-horizon confirmation.

You can require a minimum bull or bear count before allowing your main strategy to engage.

Spotting hidden shifts

Sometimes price appears flat or drifting, but the heatmap quietly cools or warms:

If price is sideways while many hot tiles fade toward neutral, momentum is decaying under the surface and trend risk is increasing.

If price is sideways while many cold tiles climb back toward neutral, selling pressure is decaying and the tape is repairing itself.

Settings overview

Calculation Settings

RS Period – base RSI length for the shortest strip.

RSI Step – the increment added to each successive RSI length.

RSI Multiplier – scales all generated RSI lengths.

Calculation Source – the input series, such as close, hlc3 or others.

Plotting and Coloring Settings

Heatmap Color Palette – choose between Viridis, Jet, Plasma, Custom Heat, Gray, Cividis, Inferno, Magma, Turbo or Rainbow.

Show Group 1 – toggles RSI 1–5.

Show Group 2 – toggles RSI 6–10.

Show Group 3 – toggles RSI 11–15.

Show Group 4 – toggles RSI 16–20.

Show Bull and Bear Count – enables or disables the two breadth lines.

Alerts

RSI Heatmap Strong Bull – fires when the number of RSIs above 70 reaches or exceeds the configured threshold (default 10).

RSI Heatmap Strong Bear – fires when the number of RSIs below 30 reaches or exceeds the configured threshold (default 10).

Tuning guidance

Fast, tactical configurations

Use a small base RS Period, for example 2 to 5.

Use a small RSI Step, for tight clustering around the fast horizon.

Keep the multiplier near 1.0 to avoid extreme long lengths.

Focus on Group 1 and Group 2 for intraday and short-term trading.

Swing and position configurations

Use a mid-range RS Period, for example 7 to 14.

Use a moderate RSI Step to fan out into slower horizons.

Optionally use a multiplier slightly above 1.0.

Keep all four groups enabled for a full view from fast to slow.

Macro or higher timeframe configurations

Use a larger base RS Period.

Use a larger RSI Step so the top of the ladder reaches very slow lengths.

Focus on Group 3 and Group 4 to see structural momentum.

Treat clusters as regime markers rather than frequent trading signals.

Notes

This indicator is a contextual tool, not a standalone trading system. It does not model execution, spreads, slippage or fundamental drivers. Use it to:

Understand whether momentum is narrow or broad across horizons.

Confirm or filter existing signals from your primary strategy.

Identify environments where the market is crowded into one side.

Distinguish between isolated spikes and truly broad pressure moves.

The Relative Strength Heatmap is designed to answer a simple but powerful question:

“How many versions of RSI agree with what I am seeing on the chart?”

By compressing those answers into a single panel with clear colour coding and breadth lines, it becomes a practical, visual gauge of momentum breadth and market pressure that you can overlay on any trading framework.

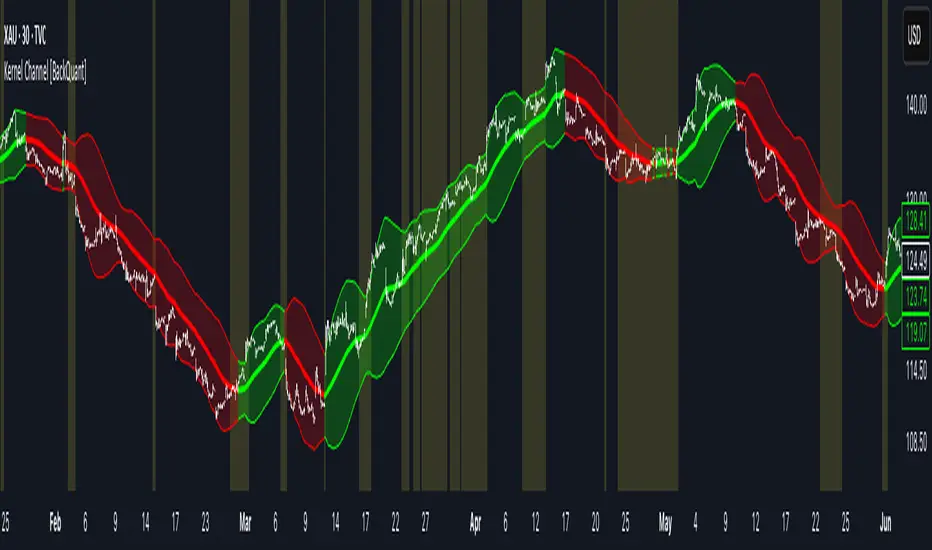

Kernel Channel [BackQuant]Kernel Channel

A non-parametric, kernel-weighted trend channel that adapts to local structure, smooths noise without lagging like moving averages, and highlights volatility compressions, expansions, and directional bias through a flexible choice of kernels, band types, and squeeze logic.

What this is

This indicator builds a full trend channel using kernel regression rather than classical averaging. Instead of a simple moving average or exponential weighting, the midline is computed as a kernel-weighted expectation of past values. This allows it to adapt to local shape, give more weight to nearby bars, and reduce distortion from outliers.

You can think of it as a sliding local smoother where you define both the “window” of influence (Window Length) and the “locality strength” (Bandwidth). The result is a flexible midline with optional upper and lower bands derived from kernel-weighted ATR or kernel-weighted standard deviation, letting you visualize volatility in a structurally consistent way.

Three plotting modes help demonstrate this difference:

When the midline is shown alone, you get a smooth, adaptive baseline that behaves almost like a regression moving average, as shown in this view:

When full channels are enabled, you see how standard deviation reacts to local structure with dynamically widening and tightening bands, a mode illustrated here:

When ATR mode is chosen instead of StdDev, band width reflects breadth of movement rather than variance, creating a volatility-aware envelope like the example here:

Why kernels

Classical moving averages allocate fixed weights. Kernels let the user define weighting shape:

Epanechnikov — emphasizes bars near the current bar, fades fast, stable and smooth.

Triangular — linear decay, simple and responsive.

Laplacian — exponential decay from the current point, sharper reactivity.

Cosine — gentle periodic decay, balanced smoothness for trend filters.

Using these in combination with a bandwidth parameter gives fine control over smoothness vs responsiveness. Smaller bandwidths give sharper local sensitivity, larger bandwidths give smoother curvature.

How it works (core logic)

The indicator computes three building blocks:

1) Kernel-weighted midline

For every bar, a sliding window looks back Window Length bars. Each bar in this window receives a kernel weight depending on:

its index distance from the present

the chosen kernel shape

the bandwidth parameter (locality)

Weights form the denominator, weighted values form the numerator, and the resulting ratio is the kernel regression mean. This midline is the central trend.

2) Kernel-based width

You choose one of two band types:

Kernel ATR — ATR values are kernel-averaged, producing a smooth, volatility-based width that is not dependent on variance. Ideal for directional trend channels and regime separation.

Kernel StdDev — local variance around the midline is computed through kernel weighting. This produces a true statistical envelope that narrows in quiet periods and widens in noisy areas.

Width is scaled using Band Multiplier , controlling how far the envelope extends.

3) Upper and lower channels

Provided midline and width exist, the channel edges are:

Upper = midline + bandMult × width

Lower = midline − bandMult × width

These create smooth structures around price that adapt continuously.

Plotting modes

The indicator supports multiple visual styles depending on what you want to emphasize.

When only the midline is displayed, you get a pure kernel trend: a smooth regression-like curve that reacts to local structure while filtering noise, demonstrated here: This provides a clean read on direction and slope.

With full channels enabled, the behavior of the bands becomes visible. Standard deviation mode creates elastic boundaries that tighten during compressions and widen during turbulence, which you can see in the band-focused demonstration: This helps identify expansion events, volatility clusters, and breakouts.

ATR mode shifts interpretation from statistical variance to raw movement amplitude. This makes channels less sensitive to outliers and more consistent across trend phases, as shown in this ATR variation example: This mode is particularly useful for breakout systems and bar-range regimes.

Regime detection and bar coloring

The slope of the midline defines directional bias:

Up-slope → green

Down-slope → red

Flat → gray

A secondary regime filter compares close to the channel:

Trend Up Strong — close above upper band and midline rising.

Trend Down Strong — close below lower band and midline falling.

Trend Up Weak — close between midline and upper band with rising slope.

Trend Down Weak — close between lower band and midline with falling slope.

Compression mode — squeeze conditions.

Bar coloring is optional and can be toggled for cleaner charts.

Squeeze logic

The indicator includes non-standard squeeze detection based on relative width , defined as:

width / |midline|

This gives a dimensionless measure of how “tight” or “loose” the channel is, normalized for trend level.

A rolling window evaluates the percentile rank of current width relative to past behavior. If the width is in the lowest X% of its last N observations, the script flags a squeeze environment. This highlights compression regions that may precede breakouts or regime shifts.

Deviation highlighting

When using Kernel StdDev mode, you may enable deviation flags that highlight bars where price moves outside the channel:

Above upper band → bullish momentum overextension

Below lower band → bearish momentum overextension

This is turned off in ATR mode because ATR widths do not represent distributional variance.

Alerts included

Kernel Channel Long — midline turns up.

Kernel Channel Short — midline turns down.

Price Crossed Midline — crossover or crossunder of the midline.

Price Above Upper — early momentum expansion.

Price Below Lower — downward volatility expansion.

These help automate regime changes and breakout detection.

How to use it

Trend identification

The midline acts as a bias filter. Rising midline means trend strength upward, falling midline means downward behavior. The channel width contextualizes confidence.

Breakout anticipation

Kernel StdDev compressions highlight areas where price is coiling. Breakouts often follow narrow relative width. ATR mode provides structural expansion cues that are smooth and robust.

Mean reversion

StdDev mode is suitable for fade setups. Moves to outer bands during low volatility often revert to the midline.

Continuation logic

If price breaks above the upper band while midline is rising, the indicator flags strong directional expansion. Same logic for breakdowns on the lower band.

Volatility characterization

Kernel ATR maps raw bar movements and is excellent for identifying regime shifts in markets where variance is unstable.

Tuning guidance

For smoother long-term trend tracking

Larger window (150–300).

Moderate bandwidth (1.0–2.0).

Epanechnikov or Cosine kernel.

ATR mode for stable envelopes.

For swing trading / short-term structure

Window length around 50–100.

Bandwidth 0.6–1.2.

Triangular for speed, Laplacian for sharper reactions.

StdDev bands for precise volatility compression.

For breakout systems

Smaller bandwidth for sharp local detection.

ATR mode for stable envelopes.

Enable squeeze highlighting for identifying setups early.

For mean-reversion systems

Use StdDev bands.

Moderate window length.

Highlight deviations to locate overextended bars.

Settings overview

Kernel Settings

Source

Window Length

Bandwidth

Kernel Type (Epanechnikov, Triangular, Laplacian, Cosine)

Channel Width

Band Type (Kernel ATR or Kernel StdDev)

Band Multiplier

Visuals

Show Bands

Color Bars By Regime

Highlight Squeeze Periods

Highlight Deviation

Lookback and Percentile settings

Colors for uptrend, downtrend, squeeze, flat

Trading applications

Trend filtering — trade only in direction of the midline slope.

Breakout confirmation — expansion outside the bands while slope agrees.

Squeeze timing — compression periods often precede the next directional leg.

Volatility-aware stops — ATR mode makes channel edges suitable for adaptive stop placement.

Structural swing mapping — StdDev bands help locate midline pullbacks vs distributional extremes.

Bias rotation — bar coloring highlights when regime shifts occur.

Notes

The Kernel Channel is not a signal generator by itself, but a structural map. It helps classify trend direction, volatility environment, distribution shape, and compression cycles. Combine it with your entry and exit framework, risk parameters, and higher-timeframe confirmation.

It is designed to behave consistently across markets, to avoid the bluntness of classical averages, and to reveal subtle curvature in price that traditional channels miss. Adjust kernel type, bandwidth, and band source to match the noise profile of your instrument, then use squeeze logic and deviation highlighting to guide timing.

Time-Decay Liquidity Zones [BackQuant]Time-Decay Liquidity Zones

A dynamic liquidity map that turns single-bar exhaustion events into fading, color-graded zones, so you can see where trapped traders and unfinished business still matter, and when those areas have finally stopped pulling price.

What this is

This indicator detects unusually strong impulsive moves into wicks, converts them into supply or demand “zones,” then lets those zones decay over time. Each zone carries a strength score that fades bar by bar. Zones that stop attracting or rejecting price are gradually de-emphasized and eventually removed, while the most relevant areas stay bright and obvious.

Instead of static rectangles that live forever, you get a living liquidity map where:

Zones are born from objective criteria: volatility, wick size, and optional volume spikes.

Zones “age” using a configurable decay factor and maximum lifetime.

Zone color and opacity reflect current relative strength on a unified clear → green → red gradient.

Zones freeze when broken, so you can distinguish “active reaction areas” from “historical levels that have already given way”.

Conceptual idea

Large wicks with strong volatility often mark areas where aggressive orders met hidden liquidity and got absorbed. Price may revisit these areas to test leftover interest or to relieve trapped positions. However, not every wick matters for long. As time passes and more bars print, the market “forgets” some areas.

Time-Decay Liquidity Zones turns that idea into a rule-based system:

Find bars that likely reflect strong aggressive flows into liquidity.

Mark a zone around the wick using ATR-based thickness.

Assign a strength score of 1.0 at birth.

Each bar, reduce that score by a decay factor and remove zones that fall below a threshold or live too long.

Color all surviving zones from weak to strong using a single gradient scale and a visual legend.

How events are detected

Detection lives in the Event Detection group. The script combines range, wick size, and optional volume filters into simple rules.

Volatility filter

ATR Length — computes a rolling ATR over your chosen window. This is the volatility baseline.

Min range in ATRs — bar range (High–Low) must exceed this multiple of ATR for an event to be considered. This avoids tiny bars triggering zones.

Wick filters

For each bar, the script splits the candle into body and wicks:

Upper wick = High minus the max(Open, Close).

Lower wick = min(Open, Close) minus Low.

Then it tests:

Upper wick condition — upper wick must be larger than Min wick size in ATRs × ATR.

Lower wick condition — lower wick must be larger than Min wick size in ATRs × ATR.

Only bars with a sufficiently long wick relative to volatility qualify as candidate “liquidity events”.

Volume filter

Optionally, the script requires a volume spike:

Use volume filter — if enabled, volume must exceed a rolling volume SMA by a configurable multiplier.

Volume SMA length — period for the volume average.

Volume spike multiplier — how many times above the SMA current volume needs to be.

This lets you focus only on “heavy” tests of liquidity and ignore quiet bars.

Event types

Putting it together:

Upper event (potential supply / long liquidation, etc.)

Occurs when:

Upper wick is large in ATR terms.

Full bar range is large in ATR terms.

Volume is above the spike threshold (if enabled).

Lower event (potential demand / short liquidation, etc.)

Symmetric conditions using the lower wick.

How zones are constructed

Zone geometry lives in Zone Geometry .

When an event is detected, the script builds a rectangular box that anchors to the wick and extends in the appropriate direction by an ATR-based thickness.

For upper (supply-type) zones

Bottom of the zone = event bar high.

Top of the zone = event bar high + Zone thickness in ATRs × ATR.

The zone initially spans only the event bar on the x-axis, but is extended to the right as new bars appear while the zone is active.

For lower (demand-type) zones

Top of the zone = event bar low.

Bottom of the zone = event bar low − Zone thickness in ATRs × ATR.

Same extension logic: box starts on the event bar and grows rightward while alive.

The result is a band around the wick that scales with volatility. On high-ATR charts, zones are thicker. On calm charts, they are narrower and more precise.

Zone lifecycle, decay, and removal

All lifecycle logic is controlled by the Decay & Lifetime group.

Each zone carries:

Score — a floating-point “importance” measure, starting at 1.0 when created.

Direction — +1 for upper zones, −1 for lower zones.

Birth index — bar index at creation time.

Active flag — whether the zone is still considered unbroken and extendable.

1) Active vs broken

Each confirmed bar, the script checks:

For an upper zone , the zone is counted as “broken” when the close moves above the top of the zone.

For a lower zone , the zone is counted as “broken” when the close moves below the bottom of the zone.

When a zone breaks:

Its right edge is frozen at the previous bar (no further extension).

The zone remains on the chart, but is no longer updated by price interaction. It still decays in score until removal.

This lets you see where a major level was overrun, while naturally fading its influence over time.

2) Time decay

At each confirmed bar:

Score := Score × Score decay per bar .

A decay value close to 1.0 means very slow decay and long-lived zones.

Lower values (closer to 0.9) mean faster forgetting and more current-focused zones.

You are controlling how quickly the market “forgets” past events.

3) Age and score-based removal

Zones are removed when either:

Age in bars exceeds Max bars a zone can live .

This is a hard lifetime cap.

Score falls below Minimum score before removal .

This trims zones that have decayed into irrelevance even if their age is still within bounds.

When a zone is removed, its box is deleted and all associated state is freed to keep performance and visuals clean.

Unified gradient and color logic

Color control lives in Gradient & Color . The indicator uses a single continuous gradient for all zones, above and below price, so you can read strength at a glance without guessing what palette means what.

Base colors

You set:

Mid strength color (green) — used for mid-level strength zones and as the “anchor” in the gradient.

High strength color (red) — used for the strongest zones.

Max opacity — the maximum visual opacity for the solid part of the gradient. Lower values here mean more solid; higher values mean more transparent.

The script then defines three internal points:

Clear end — same as mid color, but with a high alpha (close to transparent).

Mid end — mid color at the strongest allowed opacity.

High end — high color at the strongest allowed opacity.

Strength normalization

Within each update:

The script finds the maximum score among all existing zones.

Each zone’s strength is computed as its score divided by this maximum.

Strength is clamped into .

This means a zone with strength 1.0 is currently the strongest zone on the chart. Other zones are colored relative to that.

Piecewise gradient

Color is assigned in two stages:

For strength between 0.0 and 0.5: interpolate from “clear” green to solid green.

Weak zones are barely visible, mid-strength zones appear as solid green.

For strength between 0.5 and 1.0: interpolate from solid green to solid red.

The strongest zones shift toward the red anchor, clearly separating them from everything else.

Strength scale legend

To make the gradient readable, the indicator draws a vertical legend on the right side of the chart:

About 15 cells from top (Strong) to bottom (Weak).

Each cell uses the same gradient function as the zones themselves.

Top cell is labeled “Strong”; bottom cell is labeled “Weak”.

This legend acts as a fixed reference so you can instantly map a zone’s color to its approximate strength rank.

What it plots

At a glance, the indicator produces:

Upper liquidity zones above price, built from large upper wick events.

Lower liquidity zones below price, built from large lower wick events.

All zones colored by relative strength using the same gradient.

Zones that freeze when price breaks them, then fade out via decay and removal.

A strength scale legend on the right to interpret the gradient.

There are no extra lines, labels, or clutter. The focus is the evolving structure of liquidity zones and their visual strength.

How to read the zones

Bright red / bright green zones

These are your current “major” liquidity areas. They have high scores relative to other zones and have not yet decayed. Expect meaningful reactions, absorption attempts, or spillover moves when price interacts with them.

Faded zones

Pale, nearly transparent zones are either old, decayed, or minor. They can still matter, but priority is lower. If these are in the middle of a long consolidation, they often become background noise.

Broken but still visible zones

Zones whose extension has stopped have been overrun by closing price. They show where a key level gave way. You can use them as context for regime shifts or failed attempts.

Absence of zones

A chart with few or no zones means that, under your current thresholds, there have not been strong enough liquidity events recently. Either tighten the filters or accept that recent price action has been relatively balanced.

Use cases

1) Intraday liquidity hunting

Run the indicator on lower timeframes (e.g., 1–15 minute) with moderately fast decay.

Use the upper zones as potential sell reaction areas, the lower zones as potential buy reaction areas.

Combine with order flow, CVD, or footprint tools to see whether price is absorbing or rejecting at each zone.

2) Swing trading context

Increase ATR length and range/wick multipliers to focus only on major spikes.

Set slower decay and higher max lifetime so zones persist across multiple sessions.

Use these zones as swing inflection areas for larger setups, for example anticipating re-tests after breakouts.

3) Stop placement and invalidation

For longs, place invalidation beyond a decaying lower zone rather than in the middle of noise.

For shorts, place invalidation beyond strong upper zones.

If price closes through a strong zone and it freezes, treat that as additional evidence your prior bias may be wrong.

4) Identifying trapped flows

Upper zones formed after violent spikes up that quickly fail can mark trapped longs.

Lower zones formed after violent spikes down that quickly reverse can mark trapped shorts.

Watching how price behaves on the next touch of those zones can hint at whether those participants are being rescued or squeezed.

Settings overview

Event Detection

Use volume filter — enable or disable the volume spike requirement.

Volume SMA length — rolling window for average volume.

Volume spike multiplier — how aggressive the volume spike filter is.

ATR length — period for ATR, used in all size comparisons.

Min wick size in ATRs — minimum wick size threshold.

Min range in ATRs — minimum bar range threshold.

Zone Geometry

Zone thickness in ATRs — vertical size of each liquidity zone, scaled by ATR.

Decay & Lifetime

Score decay per bar — multiplicative decay factor for each zone score per bar.

Max bars a zone can live — hard cap on lifetime.

Minimum score before removal — score cut-off at which zones are deleted.

Gradient & Color

Mid strength color (green) — base color for mid-level zones and the lower half of the gradient.

High strength color (red) — target color for the strongest zones.

Max opacity — controls the most solid end of the gradient (0 = fully solid, 100 = fully invisible).

Tuning guidance

Fast, session-only liquidity

Shorter ATR length (e.g., 20–50).

Higher wick and range multipliers to focus only on extreme events.

Decay per bar closer to 0.95–0.98 and moderate max lifetime.

Volume filter enabled with a decent multiplier (e.g., 1.5–2.0).

Slow, structural zones

Longer ATR length (e.g., 100+).

Moderate wick and range thresholds.

Decay per bar very close to 1.0 for slow fading.

Higher max lifetime and slightly higher min score threshold so only very weak zones disappear.

Noisy, high-volatility instruments

Increase wick and range ATR multipliers to avoid over-triggering.

Consider enabling the volume filter with stronger settings.

Keep decay moderate to avoid the chart getting overloaded with old zones.

Notes

This is a structural and contextual tool, not a complete trading system. It does not account for transaction costs, execution slippage, or your specific strategy rules. Use it to:

Highlight where liquidity has recently been tested hard.

Rank these areas by decaying strength.

Guide your attention when layering in separate entry signals, risk management, and higher-timeframe context.

Time-Decay Liquidity Zones is designed to keep your chart focused on where the market has most recently “cared” about price, and to gradually forget what no longer matters. Adjust the detection, geometry, decay, and gradient to fit your product and timeframe, and let the zones show you which parts of the tape still have unfinished business.

Normalised Volume Oscillator [BackQuant]Normalised Volume Oscillator

A refined evolution of the Klinger Volume Oscillator, rebuilt for clarity, precision, and adaptability. This tool normalizes volume-driven momentum into a bounded scale so you can easily identify shifts in accumulation and distribution across any asset or timeframe, while keeping readings comparable between markets.

What this indicator does

The Normalised Volume Oscillator quantifies the balance between buying and selling pressure using the Klinger Volume Oscillator (KVO) as its base, then rescales it dynamically into a normalized range between -0.5 and +0.5. This normalization allows traders to interpret relative strength and exhaustion in volume flow, rather than dealing with raw unbounded values that differ across symbols.

It is a momentum-volume hybrid that reveals the strength of trend participation: when buyers dominate, normalized readings rise toward +0.5; when sellers dominate, they fall toward -0.5. The midline (0) acts as an equilibrium between accumulation and distribution.

Core components

Klinger Volume Oscillator: The foundation of this indicator, combining volume with price trend direction to measure long-term money flow relative to short-term movement.