Hyper Squeeze Sniper (Dual Side: Long + Short)Hyper Squeeze Sniper (Dual Side Strategy)

This script is a comprehensive Volatility Breakout System designed to identify and trade explosive price moves following periods of consolidation. It combines the classical "Squeeze" theory with Linear Regression Momentum, Volume Analysis, and an ATR-based Trailing Stop to filter false signals and manage risk effectively.

The script operates on a logic of "Compression -> Explosion -> Trend Following" suitable for both Long and Short positions.

🛠 Detailed Methodology (How it works)

1. The Squeeze Detection (Consolidation) The core concept relies on the relationship between Bollinger Bands (BB) and Keltner Channels (KC).

Condition: When the Bollinger Bands (Standard Deviation) contract and fall inside the Keltner Channels (ATR based), it indicates a period of extremely low volatility (The Squeeze).

Visual: The background turns Gray to indicate "Do Not Trade / Wait Mode".

2. Momentum Confirmation (Linear Regression) Instead of using standard lagging indicators, this script utilizes Linear Regression of the price deviation to determine the direction of the breakout.

If the Linear Regression Slope > 0, the bias is Bullish.

If the Linear Regression Slope < 0, the bias is Bearish.

3. Volume Validation To avoid fake breakouts, a Volume Spike filter is applied. A signal is only valid if the current volume exceeds its moving average by a defined multiplier (Default x1.2).

4. Risk Management: ATR Trailing Stop Once a trade is entered, the script calculates a dynamic Trailing Stop based on the Average True Range (ATR).

- Long: The stop line trails below the price and never moves down.

- Short: The stop line trails above the price and never moves up.

- Exit: The position is closed immediately when the price breaches this volatility-based safety line.

How to Use

1. Wait: Look for the Gray Background. This is the accumulation phase.

2. Entry:

LONG: Wait for a Green Triangle ▲ (Price breaks Upper BB + Vol Spike + Bullish Momentum).

SHORT: Wait for a Red Triangle ▼ (Price breaks Lower BB + Vol Spike + Bearish Momentum).

3. Exit: Close the position when the "X" mark appears or when candles cross the trailing safety line.

Settings

- BB Length/Mult: Adjust the sensitivity of the squeeze detection.

- Vol Spike Factor: Increase this to filter out low-volume breakouts.

- ATR Period/Mult: Adjust the trailing stop distance (Higher = Wider stop for swing trading).

Bands

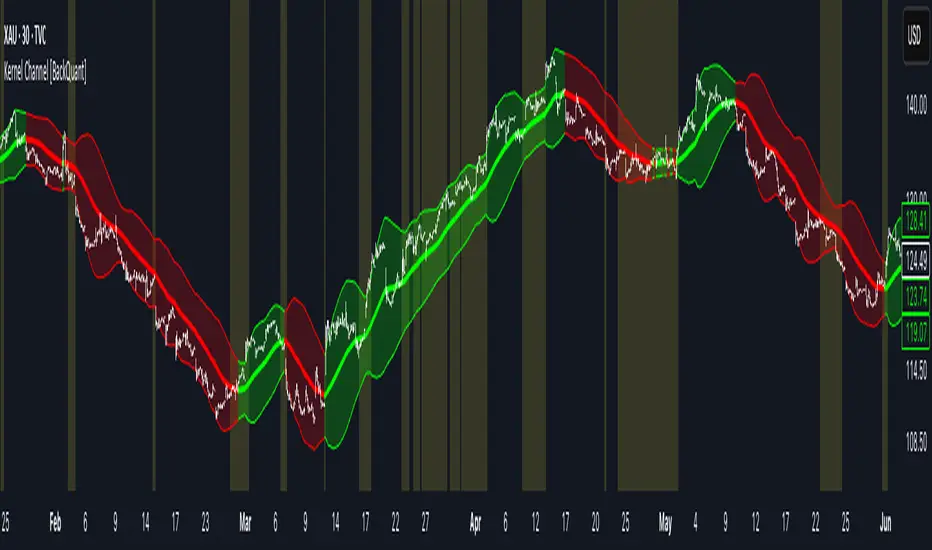

Kernel Channel [BackQuant]Kernel Channel

A non-parametric, kernel-weighted trend channel that adapts to local structure, smooths noise without lagging like moving averages, and highlights volatility compressions, expansions, and directional bias through a flexible choice of kernels, band types, and squeeze logic.

What this is

This indicator builds a full trend channel using kernel regression rather than classical averaging. Instead of a simple moving average or exponential weighting, the midline is computed as a kernel-weighted expectation of past values. This allows it to adapt to local shape, give more weight to nearby bars, and reduce distortion from outliers.

You can think of it as a sliding local smoother where you define both the “window” of influence (Window Length) and the “locality strength” (Bandwidth). The result is a flexible midline with optional upper and lower bands derived from kernel-weighted ATR or kernel-weighted standard deviation, letting you visualize volatility in a structurally consistent way.

Three plotting modes help demonstrate this difference:

When the midline is shown alone, you get a smooth, adaptive baseline that behaves almost like a regression moving average, as shown in this view:

When full channels are enabled, you see how standard deviation reacts to local structure with dynamically widening and tightening bands, a mode illustrated here:

When ATR mode is chosen instead of StdDev, band width reflects breadth of movement rather than variance, creating a volatility-aware envelope like the example here:

Why kernels

Classical moving averages allocate fixed weights. Kernels let the user define weighting shape:

Epanechnikov — emphasizes bars near the current bar, fades fast, stable and smooth.

Triangular — linear decay, simple and responsive.

Laplacian — exponential decay from the current point, sharper reactivity.

Cosine — gentle periodic decay, balanced smoothness for trend filters.

Using these in combination with a bandwidth parameter gives fine control over smoothness vs responsiveness. Smaller bandwidths give sharper local sensitivity, larger bandwidths give smoother curvature.

How it works (core logic)

The indicator computes three building blocks:

1) Kernel-weighted midline

For every bar, a sliding window looks back Window Length bars. Each bar in this window receives a kernel weight depending on:

its index distance from the present

the chosen kernel shape

the bandwidth parameter (locality)

Weights form the denominator, weighted values form the numerator, and the resulting ratio is the kernel regression mean. This midline is the central trend.

2) Kernel-based width

You choose one of two band types:

Kernel ATR — ATR values are kernel-averaged, producing a smooth, volatility-based width that is not dependent on variance. Ideal for directional trend channels and regime separation.

Kernel StdDev — local variance around the midline is computed through kernel weighting. This produces a true statistical envelope that narrows in quiet periods and widens in noisy areas.

Width is scaled using Band Multiplier , controlling how far the envelope extends.

3) Upper and lower channels

Provided midline and width exist, the channel edges are:

Upper = midline + bandMult × width

Lower = midline − bandMult × width

These create smooth structures around price that adapt continuously.

Plotting modes

The indicator supports multiple visual styles depending on what you want to emphasize.

When only the midline is displayed, you get a pure kernel trend: a smooth regression-like curve that reacts to local structure while filtering noise, demonstrated here: This provides a clean read on direction and slope.

With full channels enabled, the behavior of the bands becomes visible. Standard deviation mode creates elastic boundaries that tighten during compressions and widen during turbulence, which you can see in the band-focused demonstration: This helps identify expansion events, volatility clusters, and breakouts.

ATR mode shifts interpretation from statistical variance to raw movement amplitude. This makes channels less sensitive to outliers and more consistent across trend phases, as shown in this ATR variation example: This mode is particularly useful for breakout systems and bar-range regimes.

Regime detection and bar coloring

The slope of the midline defines directional bias:

Up-slope → green

Down-slope → red

Flat → gray

A secondary regime filter compares close to the channel:

Trend Up Strong — close above upper band and midline rising.

Trend Down Strong — close below lower band and midline falling.

Trend Up Weak — close between midline and upper band with rising slope.

Trend Down Weak — close between lower band and midline with falling slope.

Compression mode — squeeze conditions.

Bar coloring is optional and can be toggled for cleaner charts.

Squeeze logic

The indicator includes non-standard squeeze detection based on relative width , defined as:

width / |midline|

This gives a dimensionless measure of how “tight” or “loose” the channel is, normalized for trend level.

A rolling window evaluates the percentile rank of current width relative to past behavior. If the width is in the lowest X% of its last N observations, the script flags a squeeze environment. This highlights compression regions that may precede breakouts or regime shifts.

Deviation highlighting

When using Kernel StdDev mode, you may enable deviation flags that highlight bars where price moves outside the channel:

Above upper band → bullish momentum overextension

Below lower band → bearish momentum overextension

This is turned off in ATR mode because ATR widths do not represent distributional variance.

Alerts included

Kernel Channel Long — midline turns up.

Kernel Channel Short — midline turns down.

Price Crossed Midline — crossover or crossunder of the midline.

Price Above Upper — early momentum expansion.

Price Below Lower — downward volatility expansion.

These help automate regime changes and breakout detection.

How to use it

Trend identification

The midline acts as a bias filter. Rising midline means trend strength upward, falling midline means downward behavior. The channel width contextualizes confidence.

Breakout anticipation

Kernel StdDev compressions highlight areas where price is coiling. Breakouts often follow narrow relative width. ATR mode provides structural expansion cues that are smooth and robust.

Mean reversion

StdDev mode is suitable for fade setups. Moves to outer bands during low volatility often revert to the midline.

Continuation logic

If price breaks above the upper band while midline is rising, the indicator flags strong directional expansion. Same logic for breakdowns on the lower band.

Volatility characterization

Kernel ATR maps raw bar movements and is excellent for identifying regime shifts in markets where variance is unstable.

Tuning guidance

For smoother long-term trend tracking

Larger window (150–300).

Moderate bandwidth (1.0–2.0).

Epanechnikov or Cosine kernel.

ATR mode for stable envelopes.

For swing trading / short-term structure

Window length around 50–100.

Bandwidth 0.6–1.2.

Triangular for speed, Laplacian for sharper reactions.

StdDev bands for precise volatility compression.

For breakout systems

Smaller bandwidth for sharp local detection.

ATR mode for stable envelopes.

Enable squeeze highlighting for identifying setups early.

For mean-reversion systems

Use StdDev bands.

Moderate window length.

Highlight deviations to locate overextended bars.

Settings overview

Kernel Settings

Source

Window Length

Bandwidth

Kernel Type (Epanechnikov, Triangular, Laplacian, Cosine)

Channel Width

Band Type (Kernel ATR or Kernel StdDev)

Band Multiplier

Visuals

Show Bands

Color Bars By Regime

Highlight Squeeze Periods

Highlight Deviation

Lookback and Percentile settings

Colors for uptrend, downtrend, squeeze, flat

Trading applications

Trend filtering — trade only in direction of the midline slope.

Breakout confirmation — expansion outside the bands while slope agrees.

Squeeze timing — compression periods often precede the next directional leg.

Volatility-aware stops — ATR mode makes channel edges suitable for adaptive stop placement.

Structural swing mapping — StdDev bands help locate midline pullbacks vs distributional extremes.

Bias rotation — bar coloring highlights when regime shifts occur.

Notes

The Kernel Channel is not a signal generator by itself, but a structural map. It helps classify trend direction, volatility environment, distribution shape, and compression cycles. Combine it with your entry and exit framework, risk parameters, and higher-timeframe confirmation.

It is designed to behave consistently across markets, to avoid the bluntness of classical averages, and to reveal subtle curvature in price that traditional channels miss. Adjust kernel type, bandwidth, and band source to match the noise profile of your instrument, then use squeeze logic and deviation highlighting to guide timing.

Damo's Custom EMA Bands 1.0I was making these manually for a long time. They just give me more peace of mind when I'm using EMAs. They feel more like a net catching price. These are easy to make. All they are is 3 EMAs with the Source at High, Low and (H+L)/2 for the midpoint.

I find on a 3-Day chart on BTC the 100 EMA is great for telling what trend we're are in.

i.postimg.cc

McMillan Volatility Bands (MVB) – with Entry Logic// McMillan Volatility Bands (MVB) with signal + entry logic

// Author: ChatGPT for OneRyanAlexander

// Notes:

// - Bands are computed using percentage volatility (log returns), per the Black‑Scholes framing.

// - Inner band (default 3σ) and outer band (default 4σ) are configurable.

// - A setup occurs when price closes outside the outer band, then closes back within the inner band.

// The bar that re‑enters is the "signal bar." We then require price to trade beyond the signal bar's

// extreme by a user‑defined cushion (default 0.34 * signal bar range) to confirm entry.

// - Includes alertconditions for both setups and confirmed entries.

Dynamic Fractal Flow [Alpha Extract]An advanced momentum oscillator that combines fractal market structure analysis with adaptive volatility weighting and multi-derivative calculus to identify high-probability trend reversals and continuation patterns. Utilizing sophisticated noise filtering through choppiness indexing and efficiency ratio analysis, this indicator delivers entries that adapt to changing market regimes while reducing false signals during consolidation via multi-layer confirmation centered on acceleration analysis, statistical band context, and dynamic omega weighting—without any divergence detection.

🔶 Fractal-Based Market Structure Detection

Employs Williams Fractal methodology to identify pivotal market highs and lows, calculating normalized price position within the established fractal range to generate oscillator signals based on structural positioning. The system tracks fractal points dynamically and computes relative positioning with ATR fallback protection, ensuring continuous signal generation even during extended trending periods without fractal formation.

🔶 Dynamic Omega Weighting System

Implements an adaptive weighting algorithm that adjusts signal emphasis based on real-time volatility conditions and volume strength, calculating dynamic omega coefficients ranging from 0.3 to 0.9. The system applies heavier weighting to recent price action during high-conviction moves while reducing sensitivity during low-volume environments, mitigating lag inherent in fixed-period calculations through volatility normalization and volume-strength integration.

🔶 Cascading Robustness Filtering

Features up to five stages of progressive EMA smoothing with user-adjustable robustness steps, each layer systematically filtering microstructure noise while preserving essential trend information. Smoothing periods scale with the chosen fractal length and robustness steps using a fixed smoothing multiplier for consistent, predictable behavior.

🔶 Adaptive Noise Suppression Engine

Integrates dual-component noise filtering combining Choppiness Index calculation with Kaufman’s Efficiency Ratio to detect ranging versus trending market conditions. The system applies dynamic damping that maintains full signal strength during trending environments while suppressing signals during choppy consolidation, aligning output with the prevailing regime.

🔶 Acceleration and Jerk Analysis Framework

Calculates second-derivative acceleration and third-derivative jerk to identify explosive momentum shifts before they fully materialize on traditional indicators. Detects bullish acceleration when both acceleration and jerk turn positive in negative oscillator territory, and bearish acceleration when both turn negative in positive territory, providing early entry signals for high-velocity trend initiation phases.

🔶 Multi-Layer Signal Generation Architecture

Combines three primary signal types with hierarchical validation: acceleration signals, band crossover entries, and threshold momentum signals. Each signal category includes momentum confirmation, trend-state validation, and statistical band context; signals are further conditioned by band squeeze detection to avoid low-probability entries during compression phases. Divergence is intentionally excluded for a purely structure- and momentum-driven approach.

🔶 Dynamic Statistical Band System

Utilizes Bollinger-style standard deviation bands with configurable multiplier and length to create adaptive threshold zones that expand during volatile periods and contract during consolidation. Includes band squeeze detection to identify compression phases that typically precede expansion, with signal suppression during squeezes to prevent premature entries.

🔶 Gradient Color Visualization System

Features color gradient mapping that dynamically adjusts line intensity based on signal strength, transitioning from neutral gray to progressively intense bullish or bearish colors as conviction increases. Includes gradient fills between the signal line and zero with transparency scaling based on oscillator intensity for immediate visual confirmation of trend strength and directional bias.

All analysis provided by Alpha Extract is for educational and informational purposes only. The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations.

CandleFlow — Adaptive-Colored Bollinger BandsEN — What it is

Classic Bollinger Bands with adaptive color. Bands turn green when the basis slope is rising and red when it is falling. Same BB math; only visuals adapt. Two-state only.

Features

• Works on any timeframe; built with daily crypto in mind

• Inputs: Length 20, Multiplier 2.0, MA Type (SMA/EMA/WMA), Slope Length, Up/Down thresholds, Band fill

• Alerts: Trend state turns Up / turns Down

Notes

• Invite-only access. Source code not provided.

• No profit guarantee; this is not financial advice.

KR — 요약

표준 볼린저 계산은 그대로, 기준선이 상승하면 초록/하락하면 빨강으로 자동 색상 전환. 일봉 크립토에 최적화. 입력값(기간 20, 배수 2.0, MA 타입, 기울기 길이, 상/하 임계값, 밴드 채우기), 알림(상승/하락 전환) 제공. 초대전용, 코드 비공개. 수익 보장 없음.

Trademark

Bollinger Bands® is a registered trademark of John Bollinger. Not affiliated or endorsed.

Advanced Candle Compression BollingerColors candles based on Bollinger Band width relative to its average — showing when volatility tightens.

Orange = medium compression

Red = strong compression

Candle color appears only after several consecutive bars meet the condition.

You can adjust thresholds, colors, bar count, and the Bollinger source (default: (High+Low+Close)/3).

Useful to spot low-volatility zones that often precede breakouts.

Market Pressure Differential (MPD) [SharpStrat]Market Pressure Differential (MPD)

Concept & Purpose

The Market Pressure Differential (MPD) is a proprietary indicator designed to measure the internal balance of buying and selling pressure directly on the price chart.

Unlike standard momentum or trend indicators, MPD analyzes the structural behavior of each candle—its body, wicks, and overall range—to determine whether the market is dominated by expansion (buying aggression) or contraction (selling absorption).

This indicator provides a visual overlay of market pressure that adapts dynamically to volatility, helping traders see real-time shifts in participation intensity without using oscillators.

In simple terms:

When MPD expands upward → buyer pressure dominates.

When MPD contracts downward → seller pressure dominates.

Calculation Overview

MPD uses a structural candle formula to compute directional pressure:

Body Ratio = (Close − Open) / (High − Low)

Wick Differential = (Lower Wick − Upper Wick) / (High − Low)

Raw Pressure = (Body Ratio × Body Weight) + (Wick Differential × Wick Weight)

Then it applies:

EMA smoothing (to stabilize short-term noise)

Standard deviation normalization (to maintain consistent scaling)

ATR projection (to adapt the signal visually to volatility)

This produces the MPD projection line and the pressure ribbon, drawn directly on the main chart.

Customizable Inputs

Users can adjust color schemes, EMA smoothing length, ATR parameters, normalization length, and body/wick weighting to adapt the indicator’s sensitivity and aesthetic to different markets or chart themes.

How to Use

The Market Pressure Differential (MPD) visualizes the real-time balance between buying and selling pressure. It should be used as a contextual bias tool, not a standalone signal generator.

The white line represents the MPD projection, showing how market pressure evolves in real time based on candle structure and volatility.

The red line represents the ATR envelope, which defines the market’s expected volatility range.

MPD reacts quickly to candle structure, so trend bias is based on how its projection behaves relative to the ATR envelope:

Above the ATR band → positive pressure and bullish bias.

Below the ATR band → negative pressure and bearish bias.

Hovering near the ATR band → neutral or indecisive conditions.

The MPD percentage in the label represents the normalized strength of pressure relative to recent volatility.

Positive % = buying dominance.

Negative % = selling dominance.

Higher absolute values = stronger momentum compared to volatility.

To trade with MPD:

Watch candle colors and the projection line — green or positive % shows buyer control, red or negative % shows seller control.

Note transitions above or below the ATR level for early signs of momentum shifts.

Combine MPD signals with price structure, key levels, or volume for confirmation.

This helps reveal which side controls the market and whether that pressure is strong enough to overcome typical volatility.

Disclaimer

It introduces a novel structural–pressure approach to visualizing market dynamics.

For educational and analytical purposes only; this does not constitute financial advice.

Aggregated Scores Oscillator [Alpha Extract]A sophisticated risk-adjusted performance measurement system that combines Omega Ratio and Sortino Ratio methodologies to create a comprehensive market assessment oscillator. Utilizing advanced statistical band calculations with expanding and rolling window analysis, this indicator delivers institutional-grade overbought/oversold detection based on risk-adjusted returns rather than traditional price movements. The system's dual-ratio aggregation approach provides superior signal accuracy by incorporating both upside potential and downside risk metrics with dynamic threshold adaptation for varying market conditions.

🔶 Advanced Statistical Framework

Implements dual statistical methodologies using expanding and rolling window calculations to create adaptive threshold bands that evolve with market conditions. The system calculates cumulative statistics alongside rolling averages to provide both historical context and current market regime sensitivity with configurable window parameters for optimal performance across timeframes.

🔶 Dual Ratio Integration System

Combines Omega Ratio analysis measuring excess returns versus deficit returns with Sortino Ratio calculations focusing on downside deviation for comprehensive risk-adjusted performance assessment. The system applies configurable smoothing to both ratios before aggregation, ensuring stable signal generation while maintaining sensitivity to regime changes.

// Omega Ratio Calculation

Excess_Return = sum((Daily_Return > Target_Return ? Daily_Return - Target_Return : 0), Period)

Deficit_Return = sum((Daily_Return < Target_Return ? Target_Return - Daily_Return : 0), Period)

Omega_Ratio = Deficit_Return ≠ 0 ? (Excess_Return / Deficit_Return) : na

// Sortino Ratio Framework

Downside_Deviation = sqrt(sum((Daily_Return < Target_Return ? (Daily_Return - Target_Return)² : 0), Period) / Period)

Sortino_Ratio = (Mean_Return / Downside_Deviation) * sqrt(Annualization_Factor)

// Aggregated Score

Aggregated_Score = SMA(Omega_Ratio, Omega_SMA) + SMA(Sortino_Ratio, Sortino_SMA)

🔶 Dynamic Band Calculation Engine

Features sophisticated threshold determination using both expanding historical statistics and rolling window analysis to create adaptive overbought/oversold levels. The system incorporates configurable multipliers and sensitivity adjustments to optimize signal timing across varying market volatility conditions with automatic band convergence logic.

🔶 Signal Generation Framework

Generates overbought conditions when aggregated score exceeds adjusted upper threshold and oversold conditions below lower threshold, with neutral zone identification for range-bound markets. The system provides clear binary signal states with background zone highlighting and dynamic oscillator coloring for intuitive market condition assessment.

🔶 Enhanced Visual Architecture

Provides modern dark theme visualization with neon color scheme, dynamic oscillator line coloring based on signal states, and gradient band fills for comprehensive market condition visualization. The system includes zero-line reference, statistical band plots, and background zone highlighting with configurable transparency levels.

snapshot

🔶 Risk-Adjusted Performance Analysis

Utilizes target return parameters for customizable risk assessment baselines, enabling traders to evaluate performance relative to specific return objectives. The system's focus on downside deviation through Sortino analysis provides superior risk-adjusted signals compared to traditional volatility-based oscillators that treat upside and downside movements equally.

🔶 Multi-Timeframe Adaptability

Features configurable calculation periods and rolling windows to optimize performance across various timeframes from intraday to long-term analysis. The system's statistical foundation ensures consistent signal quality regardless of timeframe selection while maintaining sensitivity to market regime changes through adaptive band calculations.

🔶 Performance Optimization Framework

Implements efficient statistical calculations with optimized variable management and configurable smoothing parameters to balance responsiveness with signal stability. The system includes automatic band adjustment mechanisms and rolling window management for consistent performance across extended analysis periods.

This indicator delivers sophisticated risk-adjusted market analysis by combining proven statistical ratios in a unified oscillator framework. Unlike traditional overbought/oversold indicators that rely solely on price movements, the ASO incorporates risk-adjusted performance metrics to identify genuine market extremes based on return quality rather than price volatility alone. The system's adaptive statistical bands and dual-ratio methodology provide institutional-grade signal accuracy suitable for systematic trading approaches across cryptocurrency, forex, and equity markets with comprehensive visual feedback and configurable risk parameters for optimal strategy integration.

John Bollinger's Bollinger BandsJapanese below / 日本語説明は下記

This indicator replicates how John Bollinger, the inventor of Bollinger Bands, uses Bollinger Bands, displaying Bollinger Bands, %B and Bandwidth in one indicator with alerts and signals.

Bollinger Bands is created by John Bollinger in 1980s who is an American financial trader and analyst. He introduced %B and Bandwidth 30 years later.

🟦 What's different from other Bollinger Bands indicator?

Unlike the default Bollinger Bands or other custom Bollinger Bands indicators on TradingView, this indicator enables to display three Bollinger Bands tools into a single indicator with signals and alerts capability.

You can plot the classic Bollinger Bands together with either %B or Bandwidth or three tools altogether which requires the specific setting(see below settings).

This makes it easy to quantitatively monitor volatility changes and price position in relation to Bollinger Bands in one place.

🟦 Features:

Plots Bollinger Bands (Upper, Basis, Lower) with fill between bands.

Option to display %B or Bandwidth with Bollinger Bands.

Plots highest and lowest Bandwidth levels over a customizable lookback period.

Adds visual markers when Bandwidth reaches its highest (Bulge) or lowest (Squeeze) value.

Includes ready-to-use alert conditions for Bulge and Squeeze events.

📈Chart

Green triangles and red triangles in the bottom chart mark Bulges and Squeezes respectively.

🟦 Settings:

Length: Number of bars used for Bollinger Band middleline calculation.

Basis MA Type: Choose SMA, EMA, SMMA (RMA), WMA, or VWMA for the midline.

StdDev: Standard deviation multiplier (default = 2.0).

Option: Select "Bandwidth" or "%B" (add the indicator twice if you want to display both).

Period for Squeeze and Bulge: Lookback period for detecting the highest and lowest Bandwidth levels.(default = 125 as specified by John Bollinger )

Style Settings: Colors, line thickness, and transparency can be customized.

📈Chart

The chart below shows an example of three Bollinger Bands tools: Bollinger Band, %B and Bandwidth are in display.

To do this, you need to add this indicator TWICE where you select %B from Option in the first addition of this indicator and Bandwidth from Option in the second addition.

🟦 Usage:

🟠Monitor Volatility:

Watch Bandwidth values to spot volatility contractions (Squeeze) and expansions (Bulge) that often precede strong price moves.

John Bollinger defines Squeeze and Bulge as follows;

Squeeze:

The lowest bandwidth in the past 125 period, where trend is born.

Bulge:

The highest bandwidth in the past 125 period where trend is going to die.

According to John Bollinger, this 125 period can be used in any timeframe.

📈Chart1

Example of Squeeze

You can see uptrends start after squeeze(red triangles)

📈Chart2

Example of Bulge

You can see the trend reversal from downtrend to uptrends at the bulge(green triangles)

📈Chart3

Bulge DOES NOT NECESSARILY mean the beginning of a trend in opposite direction.

For example, you can see a bulge happening in the right side of the chart where green triangles are marked. Nevertheless, uptrend still continues after the bulge.

In this case, the bulge marks the beginning of a consolidation which lead to the continuation of the trend. It means that a phase of the trend highlighted in the light blue box came to an end.

Note: light blue box is not drawn by the indicator.

Like other technical analysis methods or tools, these setups do not guarantee birth of new trends and trend reversals. Traders should be carefully observing these setups along with other factors for making decisions.

🟠Track Price Position:

Use %B to see where price is located in relation to the Bollinger Bands.

If %B is close to 1, the price is near upper band while %B is close to 0, the price is near lower band.

🟠Set Alerts:

Receive alerts when Bandwidth hits highest and lowest values of bandwidth, helping you prepare for potential breakout, ending of trends and trend reversal opportunities.

🟠Combine with Other Tools:

This indicator would work best when combined with price action, trend analysis, or

market environmental analysis.

—————————————————————————————

このインジケーターはボリンジャーバンドの考案者であるジョン・ボリンジャー氏が提唱するボリンジャーバンドの使い方を再現するために、ボリンジャーバンド、%B、バンドウィズ(Bandwidth) の3つを1つのインジケーターで表示可能にしたものです。シグナルやアラートにも対応しています。

ボリンジャーバンドは1980年代にアメリカ人トレーダー兼アナリストのジョン・ボリンジャー氏によって開発されました。彼はその30年後に%Bとバンドウィズを導入しました。

🟦 他のボリンジャーバンドとの違い

TradingView標準のボリンジャーバンドや他のボリンジャーバンドとは異なり、このインジケーターでは3つのボリンジャーバンドツールを1つのインジケーターで表示し、シグナルやアラート機能も利用できるようになっています。

一般的に知られている通常のボリンジャーバンドに加え、%Bやバンドウィズを組み合わせて表示でき、設定次第では3つすべてを同時にモニターすることも可能です。これにより、価格とボリンジャーバンドの位置関係とボラティリティ変化をひと目で、かつ定量的に把握することができます。

🟦 機能:

ボリンジャーバンド(アッパーバンド・基準線・ロワーバンド)を描画し、バンド間を塗りつぶし表示。

オプションで%Bまたはバンドウィズを追加表示可能。

バンドウィズの最高値・最安値を、任意の期間で検出して表示。

バンドウィズが指定期間の最高値(バルジ※)または最安値(スクイーズ)に達した際にシグナルを表示。

※バルジは一般的にボリンジャーバンドで用いられるエクスパンションとほぼ同じ意味ですが、定義が異なります。(下記参照)

バルジおよびスクイーズ発生時のアラート設定が可能。

📈 チャート例

下記チャートの緑の三角と赤の三角は、それぞれバルジとスクイーズを示しています。

🟦 設定:

Length: ボリンジャーバンドの基準線計算に使う期間。

Basis MA Type: SMA, EMA, SMMA (RMA), WMA, VWMAから選択可能。

StdDev: 標準偏差の乗数(デフォルト2.0)。

Option: 「Bandwidth」または「%B」を選択(両方表示するにはこのインジケーターを2回追加)。

Period for Squeeze and Bulge: Bandwidthの最高値・最安値を検出する期間(デフォルトはジョン・ボリンジャー氏が推奨する125)。

Style Settings: 色、線の太さ、透明度などをカスタマイズ可能。

📈 チャート例

下のチャートは「ボリンジャーバンド」「%B」「バンドウィズ」の3つを同時に表示した例です。

この場合、インジケーターを2回追加し、最初に追加した方ではOptionを「%B」に、次に追加した方では「Bandwidth」を選択します。

🟦 使い方:

🟠 ボラティリティを監視する:

バンドウィズの値を見ることで、価格変動の収縮(スクイーズ)や拡大(バルジ)を確認できます。

これらはしばしば強い値動きの前兆となります。

ジョン・ボリンジャー氏はスクイーズとバルジを次のように定義しています:

スクイーズ: 過去125期間の中で最も低いバンドウィズ→ 新しいトレンドが生まれる場所。

バルジ: 過去125期間の中で最も高いバンドウィズ → トレンドが終わりを迎える場所。

この「125期間」はどのタイムフレームでも利用可能とされています。

📈 チャート1

スクイーズの例

赤い三角のスクイーズの後に上昇トレンドが始まっているのが確認できます。

📈 チャート2

バルジの例

緑の三角のバルジの箇所で下降トレンドから上昇トレンドへの反転が見られます。

📈 チャート3

バルジが必ずしも反転を意味しない例

下記のチャート右側の緑の三角で示されたバルジの後も、上昇トレンドが継続しています。

この場合、バルジは反転ではなく「トレンド一時的な調整(レンジ入り)」を示しており、結果的に上昇トレンドが継続しています。

この場合、バルジは水色のボックスで示されたトレンドのフェーズの終わりを示しています。

※水色のボックスはインジケーターが描画したものではありません。

また、他のテクニカル分析と同様に、これらのセットアップは必ず新しいトレンドの発生やトレンド転換を保証するものではありません。トレーダーは他の要素も考慮し、慎重に意思決定する必要があります。

🟠 価格とボリンジャーバンドの位置関係を確認する:

%Bを利用すれば、価格がバンドのどこに位置しているかを簡単に把握できます。

%Bが1に近ければ価格はアッパーバンド付近、0に近ければロワーバンド付近にあります。

🟠 アラートを設定する:

バンドウィズが一定期間の最高値または最安値に到達した際にアラートを設定することで、ブレイクアウトやトレンド終了、反転の可能性に備えることができます。

🟠 他のツールと組み合わせる:

このインジケーターは、プライスアクション、トレンド分析、環境認識などと組み合わせて活用すると最も効果的です。

JLine RZ+|SuperFundedJLINE with Resistance Zone+ — Quick Guide

What it is

This indicator generalizes the classic “JLINE” concept by letting you choose the MA type (SMA / EMA / WMA) and by converting mixed-order phases—when the fast/mid/slow MAs temporarily overlap—into forward-projected horizontal zones. It also shows a status label (current timeframe) and an optional higher-timeframe (HTF) status so you can align entries with broader trend context.

Why this is not a simple mashup

・Structure first: Instead of merely plotting MAs, the script detects mixed-order windows and tracks the max/min envelope formed by the 3 MAs during the overlap, then freezes and extends that range to the right as tradable zones (dynamic S/R derived from regime transitions).

・Context layering: You get a clear “Bullish/Bearish Perfect Order vs Mixed Zone” state, a color-coded MA band, and forward zones that persist beyond the regime change. This provides a workflow (identify structure → watch reactions at projected zones → confirm with status).

・Top-down alignment: The HTF status overlay makes it easy to avoid counter-trend trades or, if you prefer, time mean-reversion only when the current timeframe’s mixed zones line up with HTF conditions.

How it works (concise)

1. Compute fast/mid/slow MAs using your selected type (SMA/EMA/WMA).

2. Define states: Bullish Perfect Order (fast > mid > slow), Bearish Perfect Order (fast < mid < slow), or Mixed Zone (neither).

3. While Mixed, maintain an envelope using the highest/lowest of the three MAs. When the regime exits Mixed, save that envelope as a horizontal box and extend it into the future (older boxes auto-delete to keep the chart clean).

4. Paint an MA band between fast & slow with state-aware shading.

5. Show a corner label with the current state; optionally add the HTF state via request.security.

Parameters (UI mapping)

1. Moving Average Settings

・MA Type: SMA / EMA / WMA.

・Fast/Middle/Slow Period: Default 20/100/200, editable.

・Paint MA Band: Toggle the band fill between fast and slow MA.

2. Resistance Zone Settings

・Show Resistance Zone: Draw horizontal zones from mixed-order windows and extend to the right.

・Max Number of Zones: Cap the count; oldest zones are removed automatically.

・Zone Color: Set zone color/opacity.

3. Status Display Settings

・Show Status Label: On-chart label showing the current state.

・Label Position: Top/Bottom × Left/Right.

4. Multi-Timeframe Settings

・Show Higher Timeframe Status: Display the HTF state in the label.

・Higher Timeframe: Select the HTF (empty = disabled).

Practical usage

・Plan around zones: Treat zones as potential support/resistance derived from regime transitions. Observe how price reacts when it revisits/enters a zone.

・Align with trend: Prefer entries with the PO state (e.g., longs in Bullish PO) and use HTF status to filter. Mean-reversion is still possible, but require clear reaction (wick rejections, engulfings) at a zone.

・Manage clutter: If charts get busy, increase timeframe or lower “Max Number of Zones.”

・Risk first: SL beyond the opposite side of the zone; TPs can target adjacent zones or fixed R-multiples.

Notes & limitations

・Zones reflect MA-structure (mixed) envelopes, not price consolidations per se; they are structural guides, not guarantees.

・HTF readouts rely on request.security and your chosen timeframe; data quality and timing follow TradingView constraints.

Disclaimer

This tool suggests potential reaction areas; it cannot ensure outcomes. Volatility, news and liquidity conditions may invalidate any setup. Use appropriate position sizing and only risk capital you can afford to lose.

SuperFunded invite-only

To obtain access, please contact me via TradingView DM or the link in my profile.

JLINE with Resistance Zone (Advanced) — クイックガイド(日本語)

概要

本インジは、任意のMAタイプ(SMA / EMA / WMA)で高速・中速・低速の3本を描画し、順序が混在する期間(Mixed)で形成された3MAの最大値/最小値の包絡を水平ゾーンとして将来に延長して表示します。さらに、現在の状態ラベルと、任意で上位時間足(HTF)の状態も重ねて表示できます。

新規性(単なる寄せ集めではない点)

・構造を先に特定:MAを出すだけでなく、混在期間を検出→その間の3MA包絡を凍結して水平帯に変換→右に延長。レジーム転換由来のS/Rを作ります。

・文脈レイヤー:Bullish/BearishのパーフェクトオーダーとMixedを明示、MAバンドと将来に残るゾーンで、構造→反応→確認の手順が取りやすい構成。

・トップダウン整合:HTF状態をラベルに併記して、逆行を避けたり、逆張りでも根拠を強めたりできます。

使い方のヒント

ゾーン中心で計画:ゾーンはレジーム転換に基づく潜在的S/R。再訪時のローソク足の反応(ピンバー、包み足など)を確認してからエントリー。

トレンド整合:可能ならPO方向に合わせる。逆張りは明確な反応が条件。

視認性:時間軸を上げるか Max Number of Zones を下げて整理。

リスク管理:損切りは帯の反対側、利確は隣接ゾーンやR倍数で。

免責

ゾーンは反発を保証しません。ニュース・流動性の急変で機能しない場合があります。資金管理の徹底と自己責任でのご利用をお願いします。

SuperFunded招待専用スクリプト

このスクリプトはSuperFundedの参加者専用です。

Quantile Regression Bands [BackQuant]Quantile Regression Bands

Tail-aware trend channeling built from quantiles of real errors, not just standard deviations.

What it does

This indicator fits a simple linear trend over a rolling lookback and then measures how price has actually deviated from that trend during the window. It then places two pairs of bands at user-chosen quantiles of those deviations (inner and outer). Because bands are based on empirical quantiles rather than a symmetric standard deviation, they adapt to skewed and fat-tailed behaviour and often hug price better in trending or asymmetric markets.

Why “quantile” bands instead of Bollinger-style bands?

Bollinger Bands assume a (roughly) symmetric spread around the mean; quantiles don’t—upper and lower bands can sit at different distances if the error distribution is skewed.

Quantiles are robust to outliers; a single shock won’t inflate the bands for many bars.

You can choose tails precisely (e.g., 1%/99% or 5%/95%) to match your risk appetite.

How it works (intuitive)

Center line — a rolling linear regression approximates the local trend.

Residuals — for each bar in the lookback, the indicator looks at the gap between actual price and where the line “expected” price to be.

Quantiles — those gaps are sorted; you select which percentiles become your inner/outer offsets.

Bands — the chosen quantile offsets are added to the current end of the regression line to draw parallel support/resistance rails.

Smoothing — a light EMA can be applied to reduce jitter in the line and bands.

What you see

Center (linear regression) line (optional).

Inner quantile bands (e.g., 25th/75th) with optional translucent fill.

Outer quantile bands (e.g., 1st/99th) with a multi-step gradient to visualise “tail zones.”

Optional bar coloring: bars trend-colored by whether price is rising above or falling below the center line.

Alerts when price crosses the outer bands (upper or lower).

How to read it

Trend & drift — the slope of the center line is your local trend. Persistent closes on the same side of the center line indicate directional drift.

Pullbacks — tags of the inner band often mark routine pullbacks within trend. Reaction back to the center line can be used for continuation entries/partials.

Tails & squeezes — outer-band touches highlight statistically rare excursions for the chosen window. Frequent outer-band activity can signal regime change or volatility expansion.

Asymmetry — if the upper band sits much further from the center than the lower (or vice versa), recent behaviour has been skewed. Trade management can be adjusted accordingly (e.g., wider take-profit upslope than downslope).

A simple trend interpretation can be derived from the bar colouring

Good use-cases

Volatility-aware mean reversion — fade moves into outer bands back toward the center when trend is flat.

Trend participation — buy pullbacks to the inner band above a rising center; flip logic for shorts below a falling center.

Risk framing — set dynamic stops/targets at quantile rails so position sizing respects recent tail behaviour rather than fixed ticks.

Inputs (quick guide)

Source — price input used for the fit (default: close).

Lookback Length — bars in the regression window and residual sample. Longer = smoother, slower bands; shorter = tighter, more reactive.

Inner/Outer Quantiles (τ) — choose your “typical” vs “tail” levels (e.g., 0.25/0.75 inner, 0.01/0.99 outer).

Show toggles — independently toggle center line, inner bands, outer bands, and their fills.

Colors & transparency — customize band and fill appearance; gradient shading highlights the tail zone.

Band Smoothing Length — small EMA on lines to reduce stair-step artefacts without meaningfully changing levels.

Bar Coloring — optional trend tint from the center line’s momentum.

Practical settings

Swing trading — Length 75–150; inner τ = 0.25/0.75, outer τ = 0.05/0.95.

Intraday — Length 50–100 for liquid futures/FX; consider 0.20/0.80 inner and 0.02/0.98 outer in high-vol assets.

Crypto — Because of fat tails, try slightly wider outers (0.01/0.99) and keep smoothing at 2–4 to tame weekend jumps.

Signal ideas

Continuation — in an uptrend, look for pullback into the lower inner band with a close back above the center as a timing cue.

Exhaustion probe — in ranges, first touch of an outer band followed by a rejection candle back inside the inner band often precedes mean-reversion swings.

Regime shift — repeated closes beyond an outer band or a sharp re-tilt in the center line can mark a new trend phase; adjust tactics (stop-following along the opposite inner band).

Alerts included

“Price Crosses Upper Outer Band” — potential overextension or breakout risk.

“Price Crosses Lower Outer Band” — potential capitulation or breakdown risk.

Notes

The fit and quantiles are computed on a fixed rolling window and do not repaint; bands update as the window moves forward.

Quantiles are based on the recent distribution; if conditions change abruptly, expect band widths and skew to adapt over the next few bars.

Parameter choices directly shape behaviour: longer windows favour stability, tighter inner quantiles increase touch frequency, and extreme outer quantiles highlight only the rarest moves.

Final thought

Quantile bands answer a simple question: “How unusual is this move given the current trend and the way price has been missing it lately?” By scoring that question with real, distribution-aware limits rather than one-size-fits-all volatility you get cleaner pullback zones in trends, more honest “extreme” tags in ranges, and a framework for risk that matches the market’s recent personality.

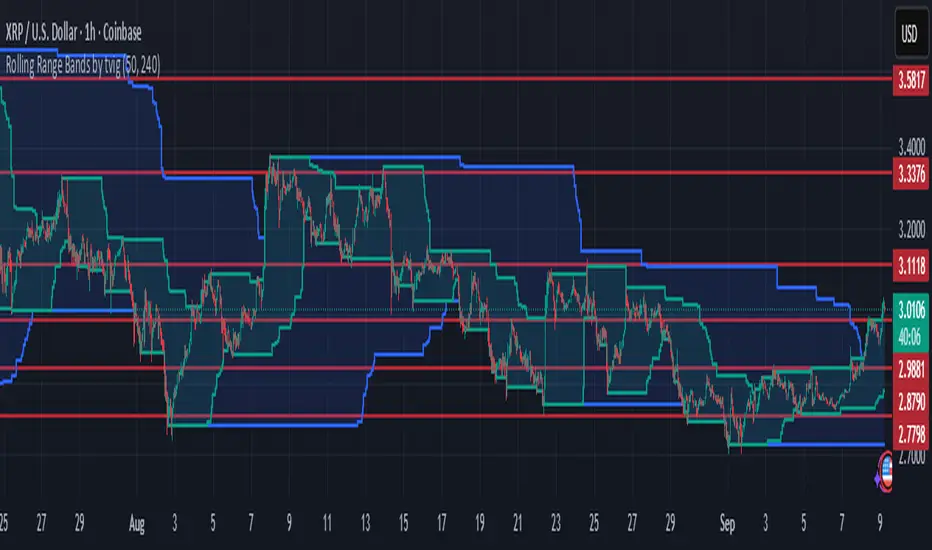

Rolling Range Bands by tvigRolling Range Bands

Plots two dynamic price envelopes that track the highest and lowest prices over a Short and Long lookback. Use them to see near-term vs. broader market structure, evolving support/resistance, and volatility changes at a glance.

What it shows

• Short Bands: recent trading range (fast, more reactive).

• Long Bands: broader range (slow, structural).

• Optional step-line style and shaded zones for clarity.

• Option to use completed bar values to avoid intrabar jitter (no repaint).

How to read

• Price pressing the short high while the long band rises → short-term momentum in a larger uptrend.

• Price riding the short low inside a falling long band → weakness with trend alignment.

• Band squeeze (narrowing) → compression; watch for breakout.

• Band expansion (widening) → rising volatility; expect larger swings.

• Repeated touches/rejections of long bands → potential areas of support/resistance.

Inputs

• Short Window, Long Window (bars)

• Use Close only (vs. High/Low)

• Use completed bar values (stability)

• Step-line style and Band shading

Tips

• Works on any symbol/timeframe; tune windows to your market.

• For consistent scaling, pin the indicator to the same right price scale as the chart.

Not financial advice; combine with trend/volume/RSI or your system for entries/exits.

Adaptive Trend Following Suite [Alpha Extract]A sophisticated multi-filter trend analysis system that combines advanced noise reduction, adaptive moving averages, and intelligent market structure detection to deliver institutional-grade trend following signals. Utilizing cutting-edge mathematical algorithms and dynamic channel adaptation, this indicator provides crystal-clear directional guidance with real-time confidence scoring and market mode classification for professional trading execution.

🔶 Advanced Noise Reduction

Filter Eliminates market noise using sophisticated Gaussian filtering with configurable sigma values and period optimization. The system applies mathematical weight distribution across price data to ensure clean signal generation while preserving critical trend information, automatically adjusting filter strength based on volatility conditions.

advancedNoiseFilter(sourceData, filterLength, sigmaParam) =>

weightSum = 0.0

valueSum = 0.0

centerPoint = (filterLength - 1) / 2

for index = 0 to filterLength - 1

gaussianWeight = math.exp(-0.5 * math.pow((index - centerPoint) / sigmaParam, 2))

weightSum += gaussianWeight

valueSum += sourceData * gaussianWeight

valueSum / weightSum

🔶 Adaptive Moving Average Core Engine

Features revolutionary volatility-responsive averaging that automatically adjusts smoothing parameters based on real-time market conditions. The engine calculates adaptive power factors using logarithmic scaling and bandwidth optimization, ensuring optimal responsiveness during trending markets while maintaining stability during consolidation phases.

// Calculate adaptive parameters

adaptiveLength = (periodLength - 1) / 2

logFactor = math.max(math.log(math.sqrt(adaptiveLength)) / math.log(2) + 2, 0)

powerFactor = math.max(logFactor - 2, 0.5)

relativeVol = avgVolatility != 0 ? volatilityMeasure / avgVolatility : 0

adaptivePower = math.pow(relativeVol, powerFactor)

bandwidthFactor = math.sqrt(adaptiveLength) * logFactor

🔶 Intelligent Market Structure Analysis

Employs fractal dimension calculations to classify market conditions as trending or ranging with mathematical precision. The system analyzes price path complexity using normalized data arrays and geometric path length calculations, providing quantitative market mode identification with configurable threshold sensitivity.

🔶 Multi-Component Momentum Analysis

Integrates RSI and CCI oscillators with advanced Z-score normalization for statistical significance testing. Each momentum component receives independent analysis with customizable periods and significance levels, creating a robust consensus system that filters false signals while maintaining sensitivity to genuine momentum shifts.

// Z-score momentum analysis

rsiAverage = ta.sma(rsiComponent, zAnalysisPeriod)

rsiDeviation = ta.stdev(rsiComponent, zAnalysisPeriod)

rsiZScore = (rsiComponent - rsiAverage) / rsiDeviation

if math.abs(rsiZScore) > zSignificanceLevel

rsiMomentumSignal := rsiComponent > 50 ? 1 : rsiComponent < 50 ? -1 : rsiMomentumSignal

❓How It Works

🔶 Dynamic Channel Configuration

Calculates adaptive channel boundaries using three distinct methodologies: ATR-based volatility, Standard Deviation, and advanced Gaussian Deviation analysis. The system automatically adjusts channel multipliers based on market structure classification, applying tighter channels during trending conditions and wider boundaries during ranging markets for optimal signal accuracy.

dynamicChannelEngine(baselineData, channelLength, methodType) =>

switch methodType

"ATR" => ta.atr(channelLength)

"Standard Deviation" => ta.stdev(baselineData, channelLength)

"Gaussian Deviation" =>

weightArray = array.new_float()

totalWeight = 0.0

for i = 0 to channelLength - 1

gaussWeight = math.exp(-math.pow((i / channelLength) / 2, 2))

weightedVariance += math.pow(deviation, 2) * array.get(weightArray, i)

math.sqrt(weightedVariance / totalWeight)

🔶 Signal Processing Pipeline

Executes a sophisticated 10-step signal generation process including noise filtering, trend reference calculation, structure analysis, momentum component processing, channel boundary determination, trend direction assessment, consensus calculation, confidence scoring, and final signal generation with quality control validation.

🔶 Confidence Transformation System

Applies sigmoid transformation functions to raw confidence scores, providing 0-1 normalized confidence ratings with configurable threshold controls. The system uses steepness parameters and center point adjustments to fine-tune signal sensitivity while maintaining statistical robustness across different market conditions.

🔶 Enhanced Visual Presentation

Features dynamic color-coded trend lines with adaptive channel fills, enhanced candlestick visualization, and intelligent price-trend relationship mapping. The system provides real-time visual feedback through gradient fills and transparency adjustments that immediately communicate trend strength and direction changes.

🔶 Real-Time Information Dashboard

Displays critical trading metrics including market mode classification (Trending/Ranging), structure complexity values, confidence scores, and current signal status. The dashboard updates in real-time with color-coded indicators and numerical precision for instant market condition assessment.

🔶 Intelligent Alert System

Generates three distinct alert types: Bullish Signal alerts for uptrend confirmations, Bearish Signal alerts for downtrend confirmations, and Mode Change alerts for market structure transitions. Each alert includes detailed messaging and timestamp information for comprehensive trade management integration.

🔶 Performance Optimization

Utilizes efficient array management and conditional processing to maintain smooth operation across all timeframes. The system employs strategic variable caching, optimized loop structures, and intelligent update mechanisms to ensure consistent performance even during high-volatility market conditions.

This indicator delivers institutional-grade trend analysis through sophisticated mathematical modelling and multi-stage signal processing. By combining advanced noise reduction, adaptive averaging, intelligent structure analysis, and robust momentum confirmation with dynamic channel adaptation, it provides traders with unparalleled trend following precision. The comprehensive confidence scoring system and real-time market mode classification make it an essential tool for professional traders seeking consistent, high-probability trend following opportunities with mathematical certainty and visual clarity.

Snapfront WCTφ Coherence BandsSnapfront Coherence Bands — WCTφ (v6)

The Snapfront Coherence Bands (SCB) extend classic ATR-style bands with a coherence-driven engine. Instead of simple volatility envelopes, SCB adapt dynamically to market entropy, trend stability, and regime detection.

Core Features:

📊 WCTφ (Weighted Coherence Tracking) to measure entropy & disorder

🔍 Adaptive band width scaling with chaos factor (ATR × coherence)

🎯 Regime coloring:

Trend (lime)

Breakout (aqua)

Mean reversion (yellow)

Exhaustion (orange)

⚡ Squeeze detector with percentile-based compression zones

🟢/🔴 Entry/exit arrows on crossovers (optional)

Use Cases:

Spot high-clarity trend moves vs. noisy ranges

Anticipate volatility squeezes & breakout setups

Filter trades by regime classification

Visualize price stability with adaptive banding

⚠️ Invite-Only Access:

Available exclusively via SnapfrontTech. Subscription required.

ADR H/L + Bull/Bear TargetsThis indicator calculates the Average Daily/Weekly Range over any given period and plots the Bull and Bear targets for that Session Daily/Weekly or both. Classic targets are calculated at ADR/AWR +/- .50 .75 1.00 1.25. Green is for the + and RED is for the - but colors can been changed to suit.

In 'Settings' there is the ability to toggle:

1. How many sessions you want to plotting on your chart.

2. Switching ON/OFF Bull/Bear targets.

3. Line color/thickness

4. Ability to offset Header for ADR/AWR vertically.

5. I've put in there a FIB option as well as Classic. FIB counts are at .382 .50 .618 1.00 of ADR and labelled as such.

Matrix bands by JaeheeMatrix Bands — multi-sigma EMA bands for price dispersion context (no signals)

📌 What it is

Matrix Bands draws an EMA-based central line with multiple standard-deviation envelopes at ±1σ, ±1.618σ, ±2σ, ±2.618σ, ±3σ.

Thin core lines show the precise band levels, while subtle outer “glow” lines improve readability without obscuring candles.

📌 How it works (concept)

Basis: EMA of the selected source (default: close)

Dispersion: Rolling sample standard deviation over the same length

Bands: Basis ± k·σ for k ∈ {1, 1.618, 2, 2.618, 3}

This is not a strategy and does not generate trade signals.

It provides price dispersion context only.

📌 Why these levels together (justification of the combination)

Using multiple σ layers reveals graduated risk zones in one view:

±1σ: routine fluctuation

±1.618σ & ±2σ: extended but still common excursions

±2.618σ & ±3σ: statistically rare extremes, where mean-reversion risk or trend acceleration risk increases

Combining these specific multipliers allows traders to judge positioning vs. volatility instantly, without switching between separate indicators or re-configuring a single band.

📌 How it differs from classic Bollinger Bands

Unlike classic Bollinger Bands, which typically use an SMA basis and only ±2σ envelopes,

Matrix Bands uses an EMA basis for faster trend responsiveness and plots five sigma levels (±1, ±1.618, ±2, ±2.618, ±3).

This design allows traders to visualize market dispersion across multiple statistical thresholds simultaneously, making it more versatile for both trend-following and mean-reversion contexts.

📌 How to read it (context, not signals)

Mean-reversion context: Moves beyond ±2σ may indicate stretched conditions; wait for your own confirmation signals before acting

Trend context: In strong trends, price can “ride” the outer bands; sustained closes near +2σ~+3σ (uptrend) or −2σ~−3σ (downtrend) suggest persistent momentum

Regime observation: Band width expands in high volatility and contracts in quiet regimes; adjust stops and sizing accordingly

📌 Inputs

BB Length: lookback period for EMA and σ (default: 20)

Source: price source for calculations

📌 Design notes

Thin inner lines = exact levels

Soft outer lines = readability “glow” only; no effect on calculations

Overlay display keeps the chart uncluttered

📌 Limitations & good practice

No entry/exit logic; use with your own strategy rules

Volatility interpretation varies by timeframe

Past patterns do not guarantee future outcomes; risk management is essential

📌 Defaults & scope

Works on any symbol with OHLCV

No alerts, no strategy results, no performance claims

Average Daily Range ADR by thSpecial for Amer and ATR testing and some text for description which I will add a little bit later because beatiful tv can't pass my indicator to be published

Volume Weighted Average Price Dynamic Slope [sgbpulse]VWAP Dynamic Slope: A Comprehensive Indicator for Trend Identification and Smart Trading

Introducing VWAP Dynamic Slope, an innovative TradingView indicator that harnesses the power of Volume Weighted Average Price (VWAP) and enhances it with immediate visual feedback. The indicator colors the VWAP line based on its slope, allowing you to quickly and easily identify the direction and strength of the current trend for the asset, providing advanced tools for in-depth analysis.

What is VWAP and Why is it so Important?

VWAP (Volume Weighted Average Price) is an indicator that represents the average price at which an asset has traded, weighted by the volume traded at each price level. Unlike a simple moving average, VWAP gives greater weight to trades executed with high volume, making it a reliable measure of the asset's "true" or "fair" price within a given period. Many institutional traders use VWAP as a central reference point for evaluating the effectiveness of entries and exits. An asset trading above its VWAP is considered to have bullish momentum, and below it – bearish momentum.

How it Works: Dynamic VWAP Slope Analysis

VWAP Dynamic Slope analyzes the inclination of the VWAP line and displays it using an intuitive color scheme:

Positive Slope (Uptrend): When the VWAP points upwards, signaling positive momentum, the default color will be green.

Negative Slope (Downtrend): When the VWAP points downwards, signaling negative momentum, the default color will be orange.

Trend Change (CHG): When a change in the VWAP's trend direction occurs, a "CHG" label will be displayed. The label's color will be green if the change is to an uptrend, and orange if the change is to a downtrend.

Identifying Steep Slopes for Increased Momentum:

The indicator's uniqueness lies in its ability to identify "steep" slopes – rapid and particularly strong changes in the VWAP's direction. This indicates exceptionally strong momentum:

Steep Positive Slope: The VWAP color will change to dark green, indicating significant buying pressure.

Steep Negative Slope: The VWAP color will change to dark red, indicating significant selling pressure.

Dynamic Momentum Strength Label: In situations of steep slope (positive or negative), a dynamic label will be displayed with the change value of the VWAP at that point. This label allows you to monitor momentum strength, intensification, or weakening in real-time.

Advanced Analytical Tools for Complete Control

VWAP Dynamic Slope provides you with unprecedented flexibility through a variety of customizable tools:

Multiple VWAP Anchors and Visual Marking:

Common Time Anchors: Choose whether the VWAP resets at the beginning of each Session (daily), Week, Month, Quarter, Year, Decade, or Century.

Advanced Intraday Anchors: Within the Session, you can choose to calculate VWAP specifically for Pre-Market, Regular Hours, and Post-Market hours. This option is particularly crucial for intraday traders.

Important Event Anchors: The indicator allows for VWAP resets at significant milestones such as Earnings, Dividends, and Splits, for analyzing the market's immediate reaction.

Visual Anchor Marking: To enhance clarity and orientation, a Label ⚓ can be displayed at each selected anchor point, helping to immediately identify the start point of the VWAP calculation in the chosen context.

Customizable Bands (Up to Three on Each Side):

Add up to three Bands above and below the VWAP to identify areas of deviation and excursion from the average price. You have two calculation options:

Standard Deviation: Based on volatility and statistical distance from the VWAP.

Percentage: Defines fixed percentage-based bands from the VWAP.

Key Pre-Market Levels (Pre-Market High/Low):

Display the Pre-Market High and Low levels as separate lines on the chart. These lines often serve as important psychological support and resistance zones, allowing you to see how the VWAP behaves near them.

Full Customization and Precise Control:

VWAP Source Selection: Determine which price data type will be used for the VWAP calculation. The default is HLC3 (average of High, Low, and Close), but any other relevant data source available in TradingView can be selected.

Offset: Set an offset for the VWAP line, allowing you to shift it left or right on the time axis by a chosen number of bars.

Customizable Colors: Choose your preferred colors for each slope state, Pre-Market High/Low lines, and Bands.

Setting the "Steepness" Threshold (Per-mille Price Change Per Minute ‱/min with Auto-Adjustment): Determine the sensitivity for identifying a steep slope by setting the required change threshold in VWAP in terms of per-mille price change per minute (‱/min). The indicator performs smart adjustment for any timeframe you select on the chart (e.g., 30 seconds, 1 minute, 5 minutes, 10 minutes, etc.), ensuring that the "steepness" setting maintains consistency and relevance.

Examples for Setting the Steepness Threshold:

Suppose you set the steepness threshold to 0.3‱/min (per-mille price change per minute).

On a 30-second chart: The indicator will check if the VWAP changed by 0.15 ‱/min (half of the per-minute threshold) within a single bar. If so, the slope will be considered steep. Explanation: Since 30 seconds is half a minute, the indicator looks for a change that is half of the threshold set for a full minute.

On a 1-minute chart: The indicator will check if the VWAP changed by 0.3 ‱/min (the full per-minute threshold) within a single bar. If so, the slope will be considered steep. Explanation: Here, the bar represents a full minute, so we check the full threshold.

On a 5-minute chart: The indicator will check if the VWAP changed by 1.5 ‱/min (5 times the per-minute threshold) within a single bar. If so, the slope will be considered steep. Explanation: A 5-minute bar contains 5 minutes, so the cumulative change in VWAP needs to be 5 times greater to be considered "steep" on the same scale.

In summary, this setting allows you to precisely and uniformly control the sensitivity of steep slope detection across all timeframes, providing immense flexibility in analyzing the asset's momentum.

Advantages of Using Per-mille Price Change Per Minute (‱/min)

Using per-mille price change per minute (‱/min) offers several key advantages for your indicator:

Normalized and Objective Measurement: It provides a uniform scale for the VWAP's rate of change, regardless of the asset's price or nominal value. A 0.1 per-mille change per minute always carries the same relative significance.

Comparison Across Different Asset Prices: Using per-mille allows for direct comparison of VWAP movement strength between assets trading at very different prices (e.g., a $100 asset versus a $1 asset), enabling an understanding of true momentum without bias from the nominal price.

Smart Timeframe Agnostic Adjustment: This is a critical capability. The indicator automatically adjusts the per-mille per minute threshold you set to any chart timeframe (30 seconds, 1 minute, 5 minutes, etc.), maintaining consistency in "steepness" detection without manual recalibration.

Precise Momentum Identification: This measurement precisely identifies when the VWAP's rate of change becomes significant, and when momentum strengthens or weakens, contributing to more informed trading decisions.

In short, per-mille change per minute (‱/min) provides accuracy, consistency, and flexibility in identifying VWAP momentum changes, with smart adaptation across all timeframes.

Who is this Indicator For?

VWAP Dynamic Slope is a powerful tool for:

Intraday Traders: For quick identification of intraday trend directions and momentum across any timeframe, with specific consideration for Pre-Market, Regular Hours, or Post-Market VWAP, and incorporating key pre-market levels.

Swing Traders and Long-Term Investors: For analyzing longer-term trends based on periodic and event-driven VWAP anchors.

Beginner Traders: As an excellent visual aid for understanding the relationship between price, volume, and trend direction, and how different anchor points, pre-market levels, and data sources influence price behavior.

Experienced Traders: For integration with existing strategies, gaining additional confirmation for trend strength identification, and highly precise and flexible parameter calibration.

VWAP Dynamic Slope provides a rich, multi-dimensional layer of information about the VWAP, helping you make more informed trading decisions in real-time, within the context of your chosen asset.

Dynamic Laguerre Filter Bands | OttoThis indicator combines trend-following and volatility analysis by enhancing the traditional Laguerre filter with a dynamic, volatility-adjusted band system. Instead of using fixed thresholds, the bands adapt in real-time to changing market conditions by applying smoothed standard deviation calculations. This design keeps the indicator responsive to significant price movements while effectively filtering out short-term market noise, resulting in more accurate trend identification and breakout signals.

Core Concept

The indicator is built around the following key components:

Laguerre Filter:

The Laguerre filter is designed to smooth out price data by reducing market noise while still being quick enough to detect real changes in price direction. Its goal is to create a clear, smooth trend line that helps traders/investors focus on the overall market trend without getting distracted by small, random price swings.

It uses a parameter called gamma to control how it balances smoothness and responsiveness:

A lower gamma gives more weight to recent price data, making the filter react faster to new price changes. This means the trend line is more sensitive but may also be less smooth and more prone to small fluctuations.

A higher gamma gives more weight to past price data, making the filter smoother and less sensitive to quick changes. This helps reduce noise and produces a steadier trend line, but it also introduces more lag, meaning the filter reacts slower to new price moves.

By adjusting gamma, the Laguerre filter lets you choose the balance between following price changes quickly and having a stable, noise-free trend signal.

Standard Deviation:

shows how much price varies from the mean. In this indicator, it’s used to measure market volatility.

Volatility Bands: The upper and lower bands are based on an EMA-smoothed standard deviation of price. The EMA reduces sudden jumps in volatility, creating smoother and more stable bands that still respond to changing market conditions. These bands are plotted around the Laguerre filter line, expanding and contracting in a controlled way to stay aligned with real market movement while avoiding short-term noise.

Signal Logic:

A long signal is triggered when the close price crosses above the upper band.

A short signal occurs when the close price falls below the lower band.

⚙️ Inputs

Source: Price source used in calculations

Gamma: Adjusts how much the Laguerre filter responds to price changes. Lower gamma values make the filter react more to recent prices, while higher values give more influence to older data, making the line smoother but slower to respond.

Volatility Length: Period used to calculate standard deviation

Volatility Smoothing Length: EMA smoothing length for standard deviation

Multiplier: Scales the width of the bands based on volatility

📈 Visual Output

Laguerre Filter Line: Plots the laguerre filter line, colored dynamically based on signal direction (green for bullish, purple for bearish)

Upper & Lower Bands: Volatility-based bands that adjust with market conditions. (green for bullish, purple for bearish)

Glow Effect: Optional glow layer to enhance visibility of the laguerre filter trend line (green for bullish, purple for bearish)

Bar Coloring: Candlesticks and bar colors reflect the active signal state for fast visual interpretation (green for bullish, purple for bearish)

How to Use

Apply the indicator to your chart and monitor for signal events:

Long Signal: When price closes above the upper band

Short Signal: When price closes below the lower band

🔔 Alerts

This indicator supports optional alert conditions you can enable for:

Long Signal: Close price crossing above the upper band

Short Signal: Close price crossing below the lower band

⚠️ Disclaimer:

This indicator is intended for educational and informational purposes only. Trading/investing involves risk, and past performance does not guarantee future results. Always test and evaluate indicators/strategies before applying them in live markets. Use at your own risk.

Dynamic Flow Ribbons [BigBeluga]🔵 OVERVIEW

A dynamic multi-band trend visualization system that adapts to market volatility and reveals trend momentum with layered ribbon channels.

Dynamic Flow Ribbons transforms price action into flowing trend bands that expand and contract with volatility. It not only shows the active directional bias but also visualizes how strong or weak the trend is through layered ribbons, making it easier to assess trend quality and structure.

🔵 CONCEPTS

Uses an adaptive trend detection system built on a volatility envelope derived from an EMA of the average price (HLC3).

Measures volatility using a long-period average of the high-low range, which scales the envelope width dynamically.

Trend direction flips when the average price crosses above or below these envelopes.

Ribbons form around the trend line to show how far price is stretching or compressing relative to the mean.

🔵 FEATURES

Volatility-Based Trend Line:

A thick, color-coded line tracks the current trend with smoother transitions between phases.

Multi-Layered Flow Ribbons:

Up to 10 bands (5 above and 5 below) radiate outward from the upper and lower envelopes, reflecting volatility strength and direction.

Trend Coloring & Transitions:

Ribbons and candles are dynamically colored based on trend direction— green for bullish , orange for bearish . Transparency fades with distance from the core trend band.

Real-Time Responsiveness:

Ribbon structure and trend shifts update in real time, adapting instantly to fast market changes.

🔵 HOW TO USE

Use the color and thickness of the core trend line to follow directional bias.

When ribbons widen symmetrically, it signals strong trend momentum .

Narrowing or overlapping ribbons can suggest consolidation or transition zones .

Combine with breakout systems or volume tools to confirm impulsive or corrective phases .

Adjust the “Length” (factor) input to tune sensitivity—higher values smooth trends more.

🔵 CONCLUSION

Dynamic Flow Ribbons offers a sleek and insightful view into trend strength and structure. By visualizing volatility expansion with directional flow, it becomes a powerful overlay for momentum traders, swing strategists, and trend followers who want to stay ahead of evolving market flows

Price Imbalance Flow Tracker (PIFT)Price Imbalance Flow Tracker (PIFT)

PIFT is a visual volatility and structure indicator that maps market imbalance zones using dynamic envelope logic. It plots three sets of envelope bands derived from different moving averages — short, medium, and long — with volatility-based offsets scaled by ATR. These envelopes adapt in real time to reflect momentum expansion, compression, and directional pressure.

- The system highlights only the dominant envelope layer at any given moment (short cancels medium/long, medium cancels long) to reduce clutter and help you focus on the most reactive structure.

- There’s also a central yellow zone representing the core trend channel — a tighter band derived from the short MA, helping you track price containment and breakout zones.

- The green and red fills show where price is expanding beyond core levels, acting as pressure zones. These fills compress during consolidations and widen during impulse moves, giving you a clean read on momentum shifts.

You can toggle:

- Full grid view (all envelopes)

- Core channel only

- Price tracks (moving averages)

- Dynamic pressure zones

Use PIFT to:

- Identify clean trend continuation inside the yellow zone

- Spot momentum exhaustion when price rides the outer bands

- Filter false moves when fills contract but price keeps drifting

- See structure shifts before standard indicators like Bollinger Bands react

This isn’t just another moving average overlay. It’s a dynamic envelope hierarchy built for traders who want to read price flow — not just lagging trend direction.

See the following images for a more in-depth breakdown.

1.)

2.)

3.)

4.)

5.)

6.)

7.)

8.)

9.)

10.)

11.)

12.)

13.)

14.)