8 SMA Bands (Points)The "8 SMA Bands (Points)" indicator creates a set of eight Simple Moving Average (SMA) bands with adjustable offsets, overlaid on a price chart.

Here’s a breakdown:

Purpose: It tracks price trends using multiple SMAs of varying lengths (default 25, 50, 100, 200, 400, 800, 1600 periods) and adds upper and lower bands around each SMA based on point offsets, helping identify potential support, resistance, and trend strength.

Key Components:

SMAs: Eight SMAs are calculated using closing prices with lengths ranging from 25 to 1600 periods. Each SMA is plotted with a distinct color and line thickness (e.g., MA 1 is blue, MA 8 is white with thicker lines).

Bands: For each SMA, upper and lower bands are created by adding or subtracting a point-based offset (suggestions are to use default Murray Math based numbers e.g., 0.305176 for MA 1, 39.062528 for MA 8) multiplied by a global multiplier (default 1.0). These offsets define the band width and are customizable.

Customization: Users can adjust SMA lengths, offset points, colors, and the global multiplier via input settings grouped by each MA.

Visuals: SMAs are plotted as solid lines with increasing thickness for longer periods (e.g., MA 6–8 use thicker lines or circles).

Bands are plotted as semi-transparent lines matching the SMA color, with longer-term bands (MA 6–7) using a different style for emphasis.

Usage: The indicator helps traders visualize trend direction (upward if price is above most SMAs, downward if below) and potential reversal zones where price interacts with band boundaries.

The flattening or crossing of bands can signal momentum shifts. The coming together of multiple envelope tops/bottoms can signal reversal zones of various degrees based on how many envelopes come together. More envelopes converging mean a more significant top or bottom.

This indicator is particularly useful for identifying multi-timeframe trends and volatility zones on assets like Gold Futures, with flexibility to fine-tune based on market conditions.

Cycles

SuperTrend Optimizer Remastered[CHE] SuperTrend Optimizer Remastered — Grid-ranked SuperTrend with additive or multiplicative scoring

Summary

This indicator evaluates a fixed grid of one hundred and two SuperTrend parameter pairs and ranks them by a simple flip-to-flip return model. It auto-selects the currently best-scoring combination and renders its SuperTrend in real time, with optional gradient coloring for faster visual parsing. The original concept is by KioseffTrading Thanks a lot for it.

For years I wanted to shorten the roughly two thousand three hundred seventy-one lines; I have now reduced the core to about three hundred eighty lines without triggering script errors. The simplification is generalizable to other indicators. A multiplicative return mode was added alongside the existing additive aggregation, enabling different rankings and often more realistic compounding behavior.

Motivation: Why this design?

SuperTrend is sensitive to its factor and period. Picking a single pair statically can underperform across regimes. This design sweeps a compact parameter grid around user-defined lower bounds, measures flip-to-flip outcomes, and promotes the combination with the strongest cumulative return. The approach keeps the visual footprint familiar while removing manual trial-and-error. The multiplicative mode captures compounding effects; the additive mode remains available for linear aggregation.

Originally (by KioseffTrading)

Very long script (~2,371 lines), monolithic structure.

SuperTrend optimization with additive (cumulative percentage-sum) scoring only.

Heavier use of repetitive code; limited modularity and fewer UI conveniences.

No explicit multiplicative compounding option; rankings did not reflect sequence-sensitive equity growth.

Now (remastered by CHE)

Compact core (~380 lines) with the same functional intent, no compile errors.

Adds multiplicative (compounding) scoring alongside additive, changing rankings to reflect real equity paths and penalize drawdown sequences.

Fixed 34×3 grid sweep, live ranking, gradient-based bar/wick/line visuals, top-table display, and an optional override plot.

Cleaner arrays/state handling, last-bar table updates, and reusable simplification pattern that can be applied to other indicators.

What’s different vs. standard approaches?

Baseline: A single SuperTrend with hand-picked inputs.

Architecture differences:

Fixed grid of thirty-four factor offsets across three ATR offsets.

Per-combination flip-to-flip backtest with additive or multiplicative aggregation.

Live ranking with optional “Best” or “Worst” table output.

Gradient bar, wick, and line coloring driven by consecutive trend counts.

Optional override plot to force a specific SuperTrend independent of ranking.

Practical effect: Charts show the currently best-scoring SuperTrend, not a static choice, plus an on-chart table of top performers for transparency.

How it works (technical)

For each parameter pair, the script computes SuperTrend value and direction. It monitors direction transitions and treats a change from up to down as a long entry and the reverse as an exit, measuring the move between entry and exit using close prices. Results are aggregated per pair either by summing percentage changes or by compounding return factors and then converting to percent for comparison. On the last bar, open trades are included as unrealized contributions to ranking. The best combination’s line is plotted, with separate styling for up and down regimes. Consecutive regime counts are normalized within a rolling window and mapped to gradients for bars, wicks, and lines. A two-column table reports the best or worst performers, with an optional row describing the parameter sweep.

Parameter Guide

Factor (Lower Bound) — Starting SuperTrend factor; the grid adds offsets between zero and three point three. Default three point zero. Higher raises distance to price and reduces flips.

ATR Period (Lower Bound) — Starting ATR length; the grid adds zero, one, and two. Default ten. Longer reduces noise at the cost of responsiveness.

Best vs Worst — Ranks by top or bottom cumulative return. Default Best. Use Worst for stress tests.

Calculation Mode — Additive sums percents; Multiplicative compounds returns. Multiplicative is closer to equity growth and can change the leaderboard.

Show in Table — “Top Three” or “All”. Fewer rows keep charts clean.

Show “Parameters Tested” Label — Displays the effective sweep ranges for auditability.

Plot Override SuperTrend — If enabled, the override factor and ATR are plotted instead of the ranked winner.

Override Factor / ATR Period — Values used when override is on.

Light Mode (for Table) — Adjusts table colors for bright charts.

Gradient/Coloring controls — Toggles for gradient bars and wick coloring, window length for normalization, gamma for contrast, and transparency settings. Use these to emphasize or tone down visual intensity.

Table Position and Text Size — Places the table and sets typography.

Reading & Interpretation

The auto SuperTrend plots one line for up regimes and one for down regimes. Color intensity reflects consecutive trend persistence within the chosen window. A small square at the bottom encodes the same gradient as a compact status channel. Optional wick coloring uses the same gradient for maximum contrast. The performance table lists parameter pairs and their cumulative return under the chosen aggregation; positive values are tinted with the up color, negative with the down color. “Long” labels mark flips that open a long in the simplified model.

Practical Workflows & Combinations

Trend following: Use the auto line as your primary bias. Enter on flips aligned with structure such as higher highs and higher lows. Filter with higher-timeframe trend or volatility contraction.

Exits/Stops: Consider conservative exits when color intensity fades or when the opposite line is approached. Aggressive traders can trail near the plotted line.

Override mode: When you want stability across instruments, enable override and standardize factor and ATR; keep the table visible for sanity checks.

Multi-asset/Multi-TF: Defaults travel well on liquid instruments and intraday to daily timeframes. Heavier assets may prefer larger lower bounds or multiplicative mode.

Behavior, Constraints & Performance

Repaint/confirmation: Signals are based on SuperTrend direction; confirmation is best assessed on closed bars to avoid mid-bar oscillation. No higher-timeframe requests are used.

Resources: One hundred and two SuperTrend evaluations per bar, arrays for state, and a last-bar table render. This is efficient for the grid size but avoid stacking many instances.

Known limits: The flip model ignores costs, slippage, and short exposure. Rapid whipsaws can degrade both aggregation modes. Gradients are cosmetic and do not change logic.

Sensible Defaults & Quick Tuning

Start with the provided lower bounds and “Top Three” table.

Too many flips → raise the lower bound factor or period.

Too sluggish → lower the bounds or switch to additive mode.

Rankings feel unstable → prefer multiplicative mode and extend the normalization window.

Visuals too strong → increase gradient transparency or disable wick coloring.

What this indicator is—and isn’t

This is a parameter-sweep and visualization layer for SuperTrend selection. It is not a complete trading system, not predictive, and does not include position sizing, transaction costs, or risk management. Combine with market structure, higher-timeframe context, and explicit risk controls.

Attribution and refactor note: The original work is by KioseffTrading. The script has been refactored from approximately two thousand three hundred seventy-one lines to about three hundred eighty core lines, retaining behavior without compiler errors. The general simplification pattern is reusable for other indicators.

Metadata

Name/Tag: SuperTrend Optimizer Remastered

Pine version: v6

Overlay or separate pane: true (overlay)

Core idea/principle: Grid-based SuperTrend selection by cumulative flip returns with additive or multiplicative aggregation.

Primary outputs/signals: Auto-selected SuperTrend up and down lines, optional override lines, gradient bar and wick colors, “Long” labels, performance table.

Inputs with defaults: See Parameter Guide above.

Metrics/functions used: SuperTrend, ATR, arrays, barstate checks, windowed normalization, gamma-based contrast adjustment, table API, gradient utilities.

Special techniques: Fixed grid sweep, compounding vs linear aggregation, last-bar UI updates, gradient encoding of persistence.

Performance/constraints: One hundred and two SuperTrend calls, arrays of length one hundred and two, label budget, last-bar table updates, no higher-timeframe requests.

Recommended use-cases/workflows: Trend bias selection, quick parameter audits, override standardization across assets.

Compatibility/assets/timeframes: Standard OHLC charts across intraday to daily; liquid instruments recommended.

Limitations/risks: Costs and slippage omitted; mid-bar instability possible; not suitable for synthetic chart types.

Debug/diagnostics: Ranking table, optional tested-range label; internal counters for consecutive trends.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Total Points Moved by exp3rtsThis lightweight utility tracks the total intraday range of price movement, giving you real-time insight into market activity.

It calculates:

🟩 Bullish Points – Total range from bullish candles (close > open)

🟥 Bearish Points – Total range from bearish candles (close < open)

🔁 Total Points Moved (TPM) – Sum of all high–low ranges for the day

Values are pulled from the 1-second chart for high precision and displayed in a compact tag in the top-right corner.

MTF EMA200 Dashboard (No Trend Column)Show ema200 position on multiple timeframe, so that in run time we can see price strength and weekness

Enhanced Std Dev Oscillator (Z-Score)Enhanced Std Dev Oscillator (Z-Score)

Overview

The Enhanced Std Dev Oscillator (ESDO) is a refined Z-Score indicator that normalizes price deviations from a moving mean using standard deviation, smoothed for clarity and equipped with divergence detection. This oscillator shines in identifying extreme overbought/oversold conditions and potential reversals, making it ideal for mean-reversion strategies in stocks, forex, or crypto. By highlighting when prices stray too far from the norm, it helps traders avoid chasing trends and focus on high-probability pullbacks.

Key Features

Customisable Mean & Deviation: Choose SMA or EMA for the mean (default: SMA, length 14); opt for Population or Sample standard deviation for precise statistical accuracy.

Smoothing for Clarity: Apply a simple moving average (default: 3) to the raw Z-Score, reducing noise without lagging signals excessively.

Zone Highlighting: Background colours flag extreme zones—red tint above +2 (overbought), green below -2 (oversold)—for quick visual scans.

Divergence Alerts: Automatically detects bullish (price lows lower, Z-Score higher) and bearish (price highs higher, Z-Score lower) divergences using pivot points (default length: 5), with labeled shapes for easy spotting.

Built-in Alerts: Notifications for Z-Score crossovers into OB/OS zones and divergence events to keep you informed without constant monitoring.

How It Works

Core Calculation: Computes the mean (SMA/EMA) over the specified length, then standard deviation (Population or adjusted Sample formula for N>1). Z-Score = (Source - Mean) / Std Dev, handling edge cases like zero deviation.

Smoothing: Averages the Z-Score with an SMA to create a cleaner plot oscillating around zero.

Levels & Zones: Plots horizontal lines at ±1 (orange dotted) and ±2 (red dashed) for reference; backgrounds activate in extreme zones.

Divergence Logic: Scans for pivot highs/lows in price and Z-Score; flags divergences when price extremes diverge from oscillator extremes (looking back 2 pivots for confirmation).

Visualisation: Blue line for the smoothed Z-Score; green/red labels for bull/bear divergences.

Usage Tips

Buy Signal: Z-Score crosses below -2 (oversold) or bullish divergence forms—pair with volume spike for confirmation.

Sell Signal: Z-Score crosses above +2 (overbought) or bearish divergence—watch for resistance alignment.

Customisation: Use EMA mean for trendier assets; enable Sample std dev for smaller datasets. Increase pivot length (7-10) in volatile markets to filter false signals.

Timeframes: Excels on daily/4H for swing trades; test smoothing on lower frames to avoid over-smoothing. Always combine with trend filters like a 200-period MA.

This open-source script is licensed under Mozilla Public License 2.0. Backtest thoroughly—past performance isn't indicative of future results. Trade with discipline! 📈

© HighlanderOne

Advanced Directional Stoch RSIAdvanced Directional Stochastic RSI

Overview

The Advanced Directional Stochastic RSI (Adv Stoch RSI Dir) is a powerful oscillator that combines the classic Stochastic RSI with John Ehlers' SuperSmoother filter for ultra-smooth signals and reduced noise. Unlike traditional Stoch RSI, this indicator incorporates directional coloring based on price action relative to a smoothed trend line, helping traders quickly spot bullish or bearish momentum. It's designed for swing traders and scalpers looking for clearer overbought/oversold conditions in volatile markets.

Key Features

Directional Coloring: %K line turns green when price is above the trend MA (bullish) and red when below (bearish), providing instant visual bias.

Multi-Pass SuperSmoothing: Apply Ehlers' SuperSmoother filter up to 5 times for customizable noise reduction—dial in passes (default: 2) to balance responsiveness and smoothness.

Trend-Aware Baseline: Uses a cascaded smoothed moving average (default length: 20) to gauge overall direction, making the oscillator more context-aware.

Classic Stoch RSI Core: Built on RSI (default: 14) and Stochastic (default: 14), with SMA smoothing for %K (3) and %D (3).

Visual Aids: Includes overbought (80), oversold (20), and midline (50) levels, plus a subtle blue fill between OB/OS zones for easy reference.

How It Works

Source Smoothing: The input source (default: close) is passed through the SuperSmoother filter multiple times to create a trend MA.

Stoch RSI Calculation: Computes RSI on the source, then applies Stochastic to the RSI values, followed by SMA smoothing for base %K and %D.

Advanced Smoothing: Extra SuperSmoother layers are applied to %K and %D based on your chosen passes, minimizing whipsaws.

Directional Logic: Compares current close to the trend MA to color %K dynamically.

Plotting: %K (thick line, colored) and %D (thin orange) oscillate between 0-100, highlighting crossovers and divergences.

Usage Tips

Buy Signal: Green %K crosses above %D below 50, or bounces off oversold (20) in uptrends.

Sell Signal: Red %K crosses below %D above 50, or rejects overbought (80) in downtrends.

Customization: Increase smoothing passes (3-5) for choppy markets; reduce for faster signals. Pair with volume or support/resistance for confirmation.

Timeframes: Best on 1H-4H charts for stocks/crypto; adjust lengths for forex.

This open-source script is licensed under Mozilla Public License 2.0. Backtest thoroughly—past performance isn't indicative of future results. Enjoy trading smarter with less noise! 🚀

© HighlanderOne

Daily Midnight Lines# Daily Midnight Lines

A simple and efficient TradingView indicator that automatically draws vertical lines at the start of each new day.

* *

## Features

✅ **Precise Timing**: Draws lines at exactly 00:00 or on the first bar of the new day

✅ **Calendar Days**: Uses calendar days, not trading sessions

✅ **Customizable Design**: Green color with transparency for comfortable viewing

✅ **High Performance**: Optimized code without unnecessary calculations

✅ **Universal**: Works on all timeframes and instruments

## Settings

- **Line Color**: Green with 30% transparency (customizable)

- **Line Width**: 1 pixel (1 to 3)

- **Mode**: Exactly at 00:00 or first bar of new day

## Applications

- Separating trading days on the chart

- Analyzing price behavior at the start of the day

- Planning trading strategies

- Statistical analysis by days

## Compatibility

- Pine Script v6

- All timeframes (1m - 1M)

- All instruments (stocks, forex, crypto, futures)

- All markets (24/7, daily, night sessions)

Perfect for day traders, scalpers, and analysts who want better chart orientation and intraday pattern analysis.

---

## Ежедневные Полночные Линии

Простой и эффективный индикатор TradingView, который автоматически рисует вертикальные линии в начале каждого нового дня.

## Особенности

✅ **Точное время**: Рисует линии в 00:00 или на первом баре нового дня

✅ **Календарные дни**: Использует календарные дни, а не торговые сессии

✅ **Настраиваемый дизайн**: Зеленый цвет с прозрачностью для комфортного просмотра

✅ **Высокая производительность**: Оптимизированный код без лишних вычислений

✅ **Универсальность**: Работает на всех таймфреймах и инструментах

## Настройки

- **Цвет линий**: Зеленый с прозрачностью 30% (настраивается)

- **Толщина линий**: 1 пиксель (от 1 до 3)

- **Режим**: Точно в 00:00 или первый бар нового дня

## Применение

- Разделение торговых дней на графике

- Анализ поведения цены в начале дня

- Планирование торговых стратегий

- Статистический анализ по дням

## Совместимость

- Pine Script v6

- Все таймфреймы (1м - 1М)

- Все инструменты (акции, форекс, крипто, фьючерсы)

- Все рынки (24/7, дневные, ночные сессии)

Идеально подходит для дневных трейдеров, скальперов и аналитиков, которые хотят лучше ориентироваться на графике и анализировать внутридневные паттерны.

**Pine Script v6** | **Updated: October 2024** | **Обновлено: Октябрь 2024**

FibPulse144 [CHE] FibPulse144 — ADX-gated 13/21 crossover with 144-trend regime and closed-bar labels

Summary

FibPulse144 combines a fast moving-average crossover with a 144-period trend regime and an ADX strength gate. Signals are confirmed on closed bars only and drawn as labels on the price chart, while an ADX line in a separate pane provides context. Color gradients are derived from normalized ADX, so visual intensity reflects trend strength without changing the underlying logic. The approach reduces false flips during weak conditions and keeps entries aligned with the dominant trend.

Motivation: Why this design?

Traditional crossover signals can flip repeatedly during sideways phases and often trigger against the higher-time regime. By requiring alignment with a slower trend proxy and by gating entries through a rising ADX condition, FibPulse144 favors structurally cleaner transitions. Gradient coloring communicates strength visually, helping users temper aggressiveness without additional indicators.

What’s different vs. standard approaches?

Baseline: Classic dual-MA crossover with unconditional signals.

Architecture differences:

Two-bar regime confirmation against a 144-period trend average.

Pending-signal logic that waits for regime and optional ADX approval.

ADX strength gate using the prior reading relative to a user threshold and earlier value.

Gradient colors scaled by an ADX window with gamma controls.

Price-chart labels enforced via overlay on an otherwise pane-based indicator.

Practical effect: Fewer signals during weak or choppy conditions, labels that appear only after a bar closes, and color intensity that mirrors trend quality.

How it works (technical)

The script computes fast and slow moving averages using the selected method and lengths. A separate 144-length average defines the regime using a two-bar confirmation above or below it. Crossovers are observed on the previous bar to avoid intrabar ambiguity; once a prior crossover is detected, it is stored as pending. A pending long requires regime alignment and, if enabled, an ADX condition based on the previous reading being above the threshold and greater than an earlier reading. The state machine holds neutral, long, or short until an exit condition or ADX reset is met. ADX is normalized within a user window, scaled with gamma, and mapped to up and down color palettes to render gradients. Labels on the price panel are forced to overlay, while the ADX line and threshold guide remain in a separate pane.

Parameter Guide

Source — Input data for all calculations. Default: close. Tip: keep consistent with your chart.

MA Type — EMA or SMA. Default: EMA. EMA reacts faster; SMA is smoother.

Fast / Slow — Fast and slow lengths for crossover. Defaults: 13 and 21. Shorter reacts earlier; longer reduces noise.

Trend — Regime average length. Default: 144. Larger values stabilize regime; smaller values increase sensitivity.

Use 144 as trend filter — Enables regime gating. Default: true. Disable to allow raw crossovers.

Use ADX filter — Requires ADX strength. Default: true. Disable to allow signals regardless of strength.

ADX Len — DI and ADX smoothing length. Default: 14. Higher values smooth strength; lower values react faster.

ADX Thresh — Minimum strength for signals. Default: 25. Raise to reduce flips; lower to capture earlier moves.

Entry/Exit labels (price) — Price-panel labels on state changes. Default: true.

Signal labels in ADX pane — Small markers at the ADX value on entries. Default: true.

Label size — tiny, small, normal, large. Default: normal.

Enable barcolor — Optional candle tint by regime and gradient. Default: false.

Enable gradient — Turns on ADX-driven color blending. Default: true.

Window — Bars used to normalize ADX for colors. Default: 100; minimum: 5.

Gamma bars / Gamma plots — Nonlinear scaling for bar and line intensities. Default: 0.80; between 0.30 and 2.00.

Gradient transp (0–90) — Transparency for gradient colors. Default: 0.

MA fill transparency (0–100) — Fill opacity between fast and slow lines. Default: 65.

Palette colors (Up/Down) — Dark and neon endpoints for up and down gradients. Defaults as in the code.

Reading & Interpretation

Fast/Slow lines: When the fast line is above the slow line, the line and fill use the long palette; when below, the short palette is used.

Trend MA (144): Neutral gray line indicating the regime boundary.

Labels on price: “LONG” appears when the state turns long; “SHORT” when it turns short. Labels appear only after the bar closes and conditions are satisfied.

ADX pane: The ADX line shows current strength. The dotted threshold line is the user level for gating. Optional small markers indicate entries at the ADX value.

Bar colors (optional): Candle tint intensity reflects normalized ADX. Higher intensity implies stronger conditions.

Practical Workflows & Combinations

Trend following: Use long entries when fast crosses above slow and price has held above the trend average for two bars, with ADX above threshold. Mirror this for shorts below the trend average.

Exits and stops: Consider reducing exposure when price closes on the opposite side of the trend average for two consecutive bars or when ADX fades below the threshold if the ADX filter is enabled.

Structure confirmation: Combine with higher-timeframe structure such as swing highs and lows or a simple market structure overlay for confirmation.

Multi-asset/Multi-TF: Works across liquid assets. For lower timeframes, consider a slightly lower ADX threshold; for higher timeframes, maintain or raise the threshold to avoid unnecessary flips.

Behavior, Constraints & Performance

Repaint/confirmation: Signals are based on previous-bar crossovers and are confirmed on bar close. No higher-timeframe or security calls are used. Intrabar markers are not relied upon.

Resources: The script declares `max_bars_back` of 2000, uses no loops or arrays, and employs persistent variables for pending signals and state.

Known limits: Crossover systems can lag after sudden reversals. During tight ranges, disabling the ADX filter may increase flips; keeping it enabled may skip early transitions.

Sensible Defaults & Quick Tuning

Starting point: EMA, 13/21/144, ADX length 14, ADX threshold 25, gradients on, barcolor off.

Too many flips: Increase ADX threshold or length; increase trend length; consider SMA instead of EMA.

Too sluggish: Lower ADX threshold slightly; shorten fast and slow lengths; reduce the trend length.

Colors overpowering: Increase gradient transparency or reduce gamma values toward one.

What this indicator is—and isn’t

This is a visualization and signal layer that combines crossover, regime, and strength gating. It does not predict future movements, manage risk, or execute trades. Use it alongside clear structure, risk controls, and a defined position management plan.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Quarter Strength Table (3M) [CHE] Quarter Strength Table (3M) — quarterly seasonality overview for the current symbol

Is there seasonality in certain assets? Some YouTubers claim there is—can you test it yourself?

Summary

This indicator builds a compact table that summarizes quarterly seasonality from three-month bars. It aggregates the simple return of each historical quarter, counts observations, computes the average return and the win rate for each quarter, and flags the historically strongest quarter. The output is a five-column table rendered on the chart, designed for quick comparison rather than signal generation. Because it processes only confirmed higher-timeframe bars, results are stable once a quarter has closed.

Motivation: Why this design?

Seasonality tools often mix intraperiod estimates with live bars, which can lead to misleading flips and inconsistent statistics. The core idea here is to restrict aggregation to completed three-month bars only and to deduplicate events by timestamp. This avoids partial information and double counting, so the table reflects a consistent, closed-bar history.

What’s different vs. standard approaches?

Baseline: Typical seasonality studies that compute monthly or quarterly stats directly on the chart timeframe or update on live higher-timeframe bars.

Architecture differences:

Uses explicit higher-timeframe requests for open, close, time, and calendar month from three-month bars.

Confirms the higher-timeframe bar before recording a sample; deduplicates by the higher-timeframe timestamp.

Keeps fixed arrays of length four for the four quarters; renders a fixed five-by-five table with zebra rows.

Practical effect: Once a quarter closes, counts and averages are stable. The “Best” column marks the highest average quarter so you can quickly identify the historically strongest period.

How it works (technical)

On every chart bar, the script requests three-month open, close, time, and the calendar month derived from that bar’s time. When the three-month bar is confirmed, it computes the simple return for that bar and maps the month to a quarter index between zero and three. A guard stores the last seen three-month timestamp to avoid duplicate writes. Per quarter, it accumulates the sum of returns, the number of samples, and the number of positive samples. From these, it derives average return and win rate. The table header is created once on the first bar; content updates only on the last visible chart bar for efficiency. No forward references are used, and lookahead is disabled in all higher-timeframe requests to avoid peeking.

Parameter Guide

Percent — Formats values as percentages. Default: true. Trade-off: Easier visual comparison; disable if you prefer raw unit returns.

Decimals — Number of digits shown. Default: two. Bounds: zero to six. Trade-off: More digits improve precision but reduce readability.

Show table — Toggles table rendering. Default: true. Trade-off: Disable when space is limited or for batch testing.

Reading & Interpretation

The table shows rows for Q1 through Q4 and columns for Count, Avg Ret, P(win), and Best.

Count: Number of completed three-month bars observed for that quarter.

Avg Ret: Average simple return across all samples in that quarter.

P(win): Share of samples with a positive return.

Best: An asterisk marks the quarter with the highest average return among those with at least one sample.

Use the combination of average and win rate to judge both magnitude and consistency. Low counts signal limited evidence.

Practical Workflows & Combinations

Trend following filter: Favor setups when the upcoming or active quarter historically shows a positive average and a stable win rate. Combine with structure analysis such as higher highs and higher lows to avoid fighting dominant trends.

Exits and risk: When entering during a historically weak quarter, consider tighter risk controls and quicker profit taking.

Multi-asset and multi-timeframe: The default settings work across most liquid symbols. For assets with sparse history, treat results as low confidence due to small sample sizes.

Behavior, Constraints & Performance

Repaint and confirmation: Aggregation occurs only when the three-month bar is confirmed; values do not change afterward for that bar. During an open quarter, no new sample is added.

Higher-timeframe usage: All higher-timeframe requests disable lookahead and rely on confirmation to mitigate repaint.

Resources: Declared `max_bars_back` is two thousand. Arrays are fixed at length four. The script updates the table only on the last visible bar to reduce work.

Known limits: Averages can be affected by outliers and structural market changes. Limited history reduces reliability. Corporate actions and contract rolls may influence returns depending on the symbol’s data source. This is a visualization and not a trading system.

Sensible Defaults & Quick Tuning

Starting values: Percent true; Decimals two; Show table true.

If numbers feel noisy: Decrease decimals to one to reduce visual clutter.

If you need raw values: Turn off Percent to display unit returns.

If the table overlaps price: Toggle Show table off when annotating, or reposition via your chart’s table controls.

What this indicator is—and isn’t

This is a historical summary of quarterly behavior. It visualizes evidence and helps frame expectations. It is not predictive, does not generate trade signals, and does not manage positions or risk. Always combine with market structure, liquidity considerations, and independent risk controls.

Inputs with defaults

Percent: true, boolean.

Decimals: two, integer between zero and six.

Show table: true, boolean.

Pine version: v6

Overlay: true

Primary outputs: Table with five columns and five rows.

Metrics/functions used: Higher-timeframe data requests, table rendering, arrays, bar state checks, month mapping.

Special techniques: Closed-bar aggregation, deduplication by higher-timeframe timestamp, zebra row styling.

Performance/constraints: Two thousand bars back, small fixed loops, higher-timeframe requests without lookahead.

Compatibility/assets/timeframes: Works on time-based charts across most assets with sufficient history.

Limitations/risks: Sample size sensitivity, regime shifts, data differences across venues.

Debug/diagnostics: (Unknown/Optional)

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Vertical Lines at 10:00 & 11:30Sales-Style Description

This script is a simple but powerful TradingView add-on that automatically marks your chart with clear, bold vertical lines at exactly 10:00 AM and 11:30 AM every day. No more manually drawing lines or setting reminders — it does the work for you.

Always on time: It tracks the market clock in real-time and drops a line the moment your chart hits those times.

Clean visibility : The lines are bright blue (#2962FF), solid, and drawn with thickness level 3, so they stand out against any background or chart theme.

Automatic housekeeping: It keeps your workspace clean by automatically deleting old lines once you reach a set limit, so your chart never gets cluttered.

Customizable : You can change the time zone, thickness, and the number of days’ worth of lines to keep.

Set it and forget it: Once added to your chart, it runs quietly in the background — you’ll always know when the 10:00 and 11:30 sessions hit without lifting a finger.

Power Hour Breakout Signals [LuxAlgo]The Power Hour Breakout tool helps traders identify key price levels from the Power Hour and spot breakouts from those levels easily. This tool features Power Hour extensions, Fibonacci levels, and session break marks for the trader's convenience.

🔶 USAGE

The Power Hour is defined as the last hour of the trading session and is set by default from 3:00 p.m. to 4:00 p.m. New York time. During this period, volume and volatility enter the market. Traders using higher timeframes may use this period to enter or exit positions by placing MOC (Market on Close) orders.

This tool highlights the Power Hour and the top and bottom price levels. Each time prices break out from these levels, a signal is displayed on the chart.

We can use the Power Hour to gauge market sentiment:

Bullish sentiment: Price trades above the Power Hour.

Mixed sentiment: Price trades within the Power Hour.

Bearish sentiment: Price trades below the Power Hour.

🔹 Displaying Power Hours and Breakouts

By default, all detected Power Hours are displayed. Traders can manually adjust this number by disabling the "Display All" parameter in the Settings panel.

Breakouts are displayed by default, too, but this feature can be disabled as well.

The chart above shows different configurations of these parameters.

🔹 Power Hour Extensions

Traders can use Power Hour extensions as potential targets for breakout signals.

In the settings panel, traders can select the percentage of the Power Hour price range to use for each extension. For example, 100% uses the full range, 200% uses the range twice, and so on.

As seen on the chart, traders can configure different percentages for the top and bottom extensions.

🔹 Fibonacci Levels

Traders can display default or custom Fibonacci levels on the Power Hour range to identify retracement opportunities and evaluate market movement strength. Each level can be enabled or disabled, as well as customized by level, color, and line style.

For example, as we can see on the chart, prices attempt to break out at the Power Hour top level, then retrace to the 0.618 Fibonacci level, and then rise to the 200% Power Hour top extension.

🔶 SETTINGS

Display Last X Power Hours: Select how many Power Hours to display or enable the Display All feature.

Power Hour (NY Time): Choose a custom Power Hour in New York time.

🔹 Breakouts

Breakouts: Enable or disable breakouts.

Bullish Breakout: Select color for bullish breakouts.

Bearish Breakout: Select color for bearish breakouts.

🔹 Extensions

Top Extension: Enable or disable the top extension and choose the percentage of Power Hour to use.

Bottom extension: Enable or disable the bottom extension and choose the percentage of Power Hour to use.

🔹 Fibonacci Levels

Display Fibonacci: Enable or disable Fibonacci levels.

Reverse: Reverse Fibonacci levels.

Levels, Colors & Style

Display Labels: Enable or disable labels and choose text size.

🔹 Style

Power Hour Colors

Extension Transparency: Choose the extension's transparency. 0 is solid, and 100 is fully transparent.

Session Breaks: Enable or disable session breaks.

Seasonal Pattern DecoderSeasonal Pattern Decoder

The Seasonal Pattern Decoder is a powerful tool designed for traders and analysts who want to uncover and leverage seasonal tendencies in financial markets. Instead of cluttering your chart with complex visuals, this indicator presents a clean, intuitive table that summarizes historical monthly performance, allowing you to spot recurring patterns at a glance.

How It Works

The indicator fetches historical monthly data for any symbol and calculates the percentage return for each month over a specified number of years. It then organizes this data into a comprehensive table, providing a clear, year-by-year and month-by-month breakdown of performance.

Key Features

Historical Performance Table: Displays monthly returns for up to a user-defined number of years, making it easy to compare performance across different periods.

Color-Coded Heatmap: Each cell is colored based on the performance of the month. Strong positive returns are shaded in green, while strong negative returns are shaded in red, allowing for immediate visual analysis of monthly strength or weakness.

Annual Summary: A "Σ" column shows the total percentage return for each full calendar year.

AVG Row: Calculates and displays the average return for each month across all the years shown in the table.

WR Row: Shows the "Win Rate" for each month, which is the percentage of time that month had a positive return. This is crucial for identifying high-probability seasonal trends.

How to Use

Add the "Seasonal Pattern Decoder" indicator to your chart. Note that it works best on Daily, Weekly, or Monthly timeframes. A warning message will be displayed on intraday charts.

In the indicator settings, adjust the "Lookback Period" to control how many years of historical data you want to analyze.

Use the "Show Years Descending" option to sort the table from the most recent year to the oldest.

The "Heat Range" setting allows you to adjust the sensitivity of the color-coding to fit the volatility of the asset you are analyzing.

This tool is ideal for confirming trading biases, developing seasonal strategies, or simply gaining a deeper understanding of an asset's typical behavior throughout the year.

## Disclaimer

This indicator is designed as a technical analysis tool and should be used in conjunction with other forms of analysis and proper risk management.

Past performance does not guarantee future results, and traders should thoroughly test any strategy before implementing it with real capital.

Predicted Funding RatesOverview

The Predicted Funding Rates indicator calculates real-time funding rate estimates for perpetual futures contracts on Binance. It uses triangular weighting algorithms on multiple different timeframes to ensure an accurate prediction.

Funding rates are periodic payments between long and short position holders in perpetual futures markets

If positive, longs pay shorts (usually bullish)

If negative, shorts pay longs (usually bearish)

This is a prediction. Actual funding rates depend on the instantaneous premium index, derived from bid/ask impacts of futures. So whilst it may imitate it similarly, it won't be completely accurate.

This only applies currently to Binance funding rates, as HyperLiquid premium data isn't available. Other Exchanges may be added if their premium data is uploaded.

Methods

Method 1: Collects premium 1-minunute data using triangular weighing over 8 hours. This granular method fills in predicted funding for 4h and less recent data

Method 2: Multi-time frame approach. Daily uses 1 hour data in the calculation, 4h + timeframes use 15M data. This dynamic method fills in higher timeframes and parts where there's unavailable premium data on the 1min.

How it works

1) Premium data is collected across multiple timeframes (depending on the timeframe)

2) Triangular weighing is applied to emphasize recent data points linearly

Tri_Weighing = (data *1 + data *2 + data *3 + data *4) / (1+2+3+4)

3) Finally, the funding rate is calculated

FundingRate = Premium + clamp(interest rate - Premium, -0.05, 0.05)

where the interest rate is 0.01% as per Binance

Triangular weighting is calculated on collected premium data, where recent data receives progressively higher weight (1, 2, 3, 4...). This linear weighting scheme provides responsiveness to recent market conditions while maintaining stability, similar to an exponential moving average but with predictable, linear characteristics

A visual representation:

Data points: ──────────────>

Weights: 1 2 3 4 5

Importance: ▂ ▃ ▅ ▆ █

How to use it

For futures traders:

If funding is trending up, the market can be interpreted as being in a bull market

If trending down, the market can be interpreted as being in a bear market

Even used simply, it allows you to gauge roughly how well the market is performing per funding. It can basically be gauged as a sentiment indicator too

For funding rate traders:

If funding is up, it can indicate a long on implied APR values

If funding is down, it can indicate a short on implied APR values

It also includes an underlying APR, which is the annualized funding rate. For Binance, it is current funding * (24/8) * 365

For Position Traders: Monitor predicted funding rates before entering large positions. Extremely high positive rates (>0.05% for 8-hour periods) suggest overleveraged longs and potential reversal risk. Conversely, extreme negative rates indicate shorts dominance

Table:

Funding rate: Gives the predicted funding rate as a percentage

Current premium: Displays the current premium (difference between perpetual futures price and the underlying spot) as a percentage

Funding period: You can choose between 1 hour funding (HyperLiquid usually) and 8 hour funding (Binance)

APR: Underlying annualized funding rate

What makes it original

Whilst some predicted funding scripts exist, some aren't as accurate or have gaps in data. And seeing as funding values are generally missing from TV tickers, this gives traders accessibility to the script when they would have to use other platforms

Notes

Currently only compatible with symbols that have Binance USDT premium indices

Optimal accuracy is found on timeframes that are 4H or less. On higher timeframes, the accuracy drops off

Actual funding rates may differ

Inputs

Funding Period: Choose between "8 Hour" (standard Binance cycle) or "1 Hour" (divides the 8-hour rate by 8 for granular comparison)

Plot Type: Display as "Funding Rate" (percentage per interval) or "APR" (annualized rate calculated as 8-hour rate × 3 × 365)

Table: Toggle the information table showing current funding rate, premium, funding period, and APR in the top-right corner

Positive Colour: Sets the colour for positive funding rates where longs pay shorts (default: #00ffbb turquoise)

Negative Colour: Sets the colour for negative funding rates where shorts pay longs (default: red)

Table Background: Controls the background colour and transparency of the information table (default: transparent dark blue)

Table Text Colour: Sets the colour for all text labels in the information table (default: white)

Table Text Size: Controls font size with options from Tiny to Huge, with Small as the default balance of readability and space

Fractal Strength OscillatorThe Fractal Strength Oscillator Indicator combines the Relative Strength Index (RSI) and Fractal Dimension Index (FDI) to identify market momentum and trend direction. By integrating RSI's momentum signals with FDI's fractal-based trend analysis, this indicator provides clear visual cues for bullish and bearish conditions through colored plots and price bars.

How It Works

RSI Calculation: Computes RSI based on a user-selected price source (default: Close) over a configurable period. Optional smoothing with various moving average types (e.g., SMA, EMA, ALMA) enhances signal clarity.

FDI Calculation: Measures market complexity using a fractal dimension over a user-defined period (default: 20). A threshold (default: 1.45) determines trend strength.

Trend Logic

Bullish Signal: RSI > 55 or FDI < threshold indicates upward momentum

Bearish Signal: RSI < 45 or FDI > threshold indicates downward momentum

Customization & Parameters

RSI Parameters: RSI length, smoothing option , MA type, MA length, ALMA sigma

FDI Parameters: FDI length, trend threshold.

Trading Applications

Momentum Trading: Use RSI and FDI signals for entry/exit points.

Trend Confirmation: Bar coloring aligns with trend signals.

Reversal Detection: Identify shifts when RSI or FDI crosses thresholds

Final Note

The Fractal Strength Oscillator Indicator is a straightforward tool for traders seeking momentum and trend insights. Its combination of RSI, FDI, and visual cues supports informed trading decisions. Backtest thoroughly and use within a broader strategy. This indicator is for educational purposes and not financial advice.

Validated Order Blocks with Fib LevelsThis indicator automatically identifies and displays Smart Money Concepts (SMC) order blocks based on market structure breaks:

How it works:

Bearish Order Blocks (Red): Marks the last bullish candle before a swing high. The OB becomes valid when price breaks below the previous swing low, indicating institutional selling zones. Drawn from the candle's close (body top) to its low (bottom wick).

Bullish Order Blocks (Green): Marks the last bearish candle before a swing low. The OB becomes valid when price breaks above the previous swing high, indicating institutional buying zones. Drawn from the candle's high (top wick) to its close (body bottom).

Features:

Three Fibonacci retracement levels (50%, 75%, 100%) for each order block

Fib 100% faces downward on bearish OBs and upward on bullish OBs

Auto-validation: OBs are removed when price closes through them

Customizable: Adjustable swing detection, timeframe selection, and OB display limits

Optional Break of Structure (BOS) markers to show when OBs activate

Works on any timeframe with HTF analysis support

Perfect for identifying key institutional support/resistance zones and potential reversal areas.

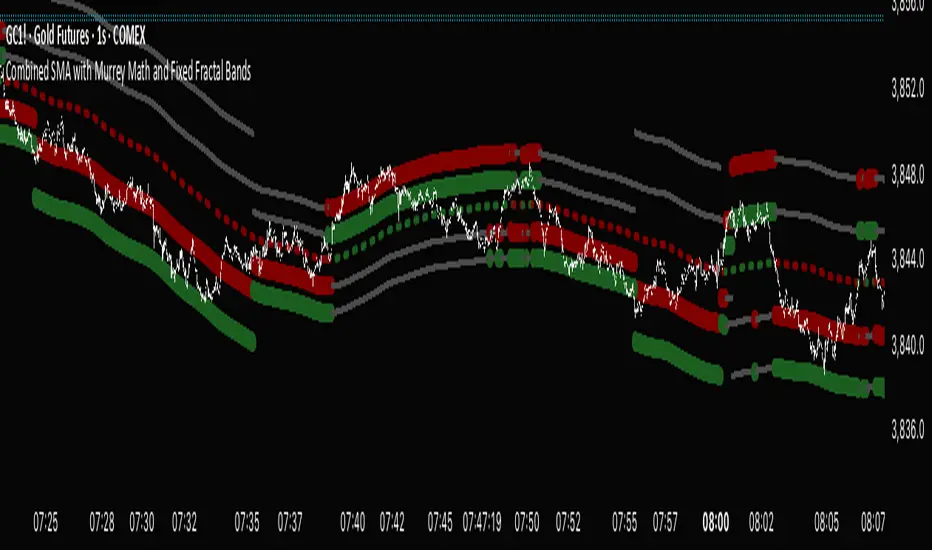

Combined SMA with Murrey Math and Fixed Fractal Bands "Combined SMA with Murrey Math and Fixed Fractal Bands" , overlaying a Simple Moving Average (SMA), Murrey Math (MM) bands, and fixed fractal bands on a price chart. Here's a brief description of its functionality:Inputs:SMA Length: Configurable period for the SMA (default: 180 bars).

Resolution: Optional custom timeframe for data.

Frame Size for MM: Lookback period for Murrey Math calculations (default: 180 bars, adjustable via multiplier).

Ignore Wicks: Option to use open/close prices instead of high/low for MM calculations.

Fixed Fractal Size: Fixed distance in points for fractal bands (default: 1.22).

Shade 3/8-5/8 Overlap: Option to highlight overlapping regions between SMA-centered and absolute MM bands.

Data Source:Uses open, close, high, and low prices from the specified ticker and timeframe.

Optionally ignores wicks (high/low) for MM calculations, using max/min of open/close instead.

SMA Calculation:Computes a Simple Moving Average (SMA) based on the closing price and user-defined length.

Murrey Math Bands:Absolute MM Bands: Calculated using a dynamic range based on the highest/lowest prices over a lookback period, scaled logarithmically to create 13 levels (from -3/8 to +3/8, with 8/8 as the midpoint). These adapt to price action.

SMA-Centered MM Bands: Constructs MM bands relative to the SMA, with levels (0/8 to 8/8) spaced by a calculated increment derived from the absolute MM range.

Colors bands dynamically (green for bullish, red for bearish, gray for neutral) based on changes in the 4/8 level or increment, with labels indicating "Higher," "Lower," or "Same" states.

Fixed Fractal Bands:Plots six fixed-distance bands (±1, ±2, ±3) around the SMA, using a user-defined point value (default: 1.22).

Overlaps and Shading:Detects overlaps between SMA-centered and absolute MM bands at key levels (7/8-8/8, 0/8-1/8, and optionally 3/8-5/8).

Shades overlapping regions with distinct colors (red for 7/8-8/8, green for 0/8-1/8, blue for 3/8-5/8).

Fills specific SMA-centered MM regions (3/8-5/8, 0/8-1/8, 7/8-8/8) for visual emphasis.

Visualization:Plots SMA-centered MM bands, absolute MM bands, and fixed fractal bands as stepped lines with varying colors and transparency.

Displays a table at the bottom-right showing the current MM increment value.

Adds labels when the 4/8 level or increment changes, indicating trend direction.

In summary, this indicator combines a user-defined SMA with Murrey Math bands (both absolute and SMA-centered) and fixed fractal bands to provide a multi-level support/resistance framework. It highlights dynamic price levels, trend direction, and key overlaps, aiding traders in identifying potential reversal or consolidation zones.

Hurst‑Millard FLD Normalized 2.0 – Signals "Hurst-Millard FLD Normalized 2.0 – Signals" indicator. It analyzes price data using a combination of moving averages (MAs) and the Hurst exponent to decompose price movements into trend, swing, and noise components, generating buy and sell signals. Here's a brief overview of its functionality:Inputs and Modes:Offers Auto Mode (cycle-based) and Manual Mode for configuring three moving averages: Long-Term (LT), Mid-Term (MT), and Short-Term (ST).

Auto Mode calculates MA lengths and offsets based on user-defined target cycle lengths (e.g., LT: 400 bars, MT: 100 bars, ST: 25 bars) with predefined offset ratios (0.2, 0.333, 0.5 respectively).

Manual Mode allows direct input of MA lengths and offsets.

Moving Averages:Computes Simple Moving Averages (SMAs) for LT, MT, and ST based on the closing price.

Applies forward-shifting to simulate future price behavior (e.g., maLongFwd shifts the LT MA by the specified offset).

Decomposition:Trend: Derived from the forward-shifted LT MA (maLongFwd).

Swing: Calculated as the difference between MT and LT MAs, scaled as a percentage of the closing price and amplified (using ATR or a manual factor).

Noise: Calculated as the difference between ST and MT MAs, similarly scaled and amplified.

Hurst Exponent:Estimates the Hurst exponent to measure the persistence or mean-reversion of the noise component.

Uses a 50-bar lookback period, smoothed with a 5-period SMA.

Signal Generation:Generates buy signals when the noise component is less than the swing component and their difference is within a user-defined proximity threshold (default: 25% of swing).

Generates sell signals when noise exceeds swing within the same threshold.

Signals are plotted as diamond shapes at the calculated proximity price level.

Visualization:Plots the trend, swing, and noise components as lines with customizable colors and gradient intensity based on their relative strength.

Optional debugging plots for raw forward-shifted MAs and proximity thresholds.

Displays a periodic debug table (every 100 bars) showing key metrics like close price, MAs, trend, swing, noise, Hurst exponent, and more.

Additional Features:Supports ATR-based amplification for scaling swing and noise.

Allows customization of signal colors, diamond offsets, and proximity thresholds.

Includes debugging options to visualize raw MAs and proximity bands.

In summary, this indicator uses cycle-based or manually configured MAs to break down price action into trend, swing, and noise, calculates the Hurst exponent for noise analysis, and generates buy/sell signals based on the relationship between swing and noise within a proximity threshold. It’s designed for traders to identify potential trend reversals or continuations.

Breaout and followthroughThis indicator is designed to identify and highlight a single, powerful entry signal at the beginning of a new trend. It filters for high-volatility breakout bars that show strong directional conviction, helping traders catch the initial momentum of a potential move. It will only paint one bullish or bearish signal after a trend change is detected, preventing repeat signals during a sustained move.

Core Concept

The indicator combines four key concepts to generate high-probability signals:

Trend Direction: It first establishes the overall trend (bullish or bearish) using a configurable Exponential or Simple Moving Average (EMA/SMA).

Volatility Expansion: It looks for bars with a larger-than-average range by comparing the bar's size to the Average True Range (ATR). This helps identify moments of increased market interest.

Closing Strength (IBS): It uses the Internal Bar Strength (IBS) to measure directional conviction. A high IBS (closing near the top) suggests bullish strength, while a low IBS (closing near the bottom) suggests bearish pressure.

Breakout Confirmation: As an optional but powerful filter, it can confirm the signal by ensuring the bar is breaking above the high or below the low of a user-defined number of previous bars.

A signal is only generated on the first bar that meets all these criteria after the price crosses the trend-defining moving average, making it ideal for capturing the start of a new swing.

Features

Bullish Signals (Green): Highlights the first bar in an uptrend that is larger than the ATR, closes with a high IBS (>70), and optionally breaks out above the recent highs.

Bearish Signals (Red): Highlights the first bar in a downtrend that is larger than the ATR, closes with a low IBS (<30), and optionally breaks out below the recent lows.

"First Signal Only" Logic: The script is hard-coded to show only the initial signal in a new trend, filtering out noise and redundant signals.

Fully Customizable Trend Filter:

Choose between EMA or SMA for trend definition.

Set the MA length (default is a short-term 7-period MA).

Option to show or hide the moving average on the chart.

Optional Breakout Filter:

Enable or disable the requirement for the signal bar to break the high/low of previous bars.

Customize the lookback period for the breakout confirmation.

How to Use

This indicator can be used as a primary signal for a trend-following or momentum-based trading system.

Look for a Green Bar (Bullish Signal): This suggests the start of a potential uptrend. Consider it a signal for a long entry. A logical stop-loss could be placed below the low of the highlighted signal bar.

Look for a Red Bar (Bearish Signal): This suggests the start of a potential downtrend. Consider it a signal for a short entry. A logical stop-loss could be placed above the high of the highlighted signal bar.

Adjust Settings: Use the settings menu to configure the indicator to your preferred market and timeframe. A longer Trend MA Length will result in fewer, more long-term signals, while a shorter length will be more responsive.

As with any tool, this indicator is best used in conjunction with other forms of analysis, such as market structure, support/resistance levels, and proper risk management.

M Killzones[by vetrivel]Cool free style Session indicator, Inspired by TJR trader session times and it's easily changeable. Really this session times changes everything. Basic requirement to use this Discipline and Mindset

Dominance Signal Apex [CHE]]Dominance Signal Apex — Triple-confirmed entry markers with stateful guardrails

Summary

This indicator focuses on entry timing by plotting markers only when three conditions align: a closed-bar Heikin-Ashi bias, a monotonic stack of super-smoother filters, and the current HMA slope. A compact state machine provides guardrails: it starts a directional state on closed-bar Heikin-Ashi bias, maintains it only while the smoother stack remains ordered, and renders a marker only if HMA slope agrees. This design aims for selective signals and reduces isolated prints during mixed conditions. Markers fade over time to visualize the age and persistence of the current state.

Motivation: Why this design?

Common triggers flip frequently in noise or react late when regimes shift. The core idea is to gate entry markers through a closed-bar state plus independent filter alignment. The state machine limits premature prints, removes markers when alignment breaks, and uses the HMA as a final directional gate. The result is fewer mixed-context entries and clearer clusters during sustained trends.

What’s different vs. standard approaches?

Reference baseline: Single moving-average slope or classic MA cross signals.

Architecture differences:

Multi-length two-pole super-smoother stack with strict ordering checks.

Closed-bar Heikin-Ashi bias to start a directional state.

HMA slope as a final gate for rendering markers.

Time-based alpha fade to surface state age.

Practical effect: Entry markers appear in clusters during aligned regimes and are suppressed when conditions diverge, improving selectivity.

How it works (technical)

Measurements: Four recursive super-smoother series on price at short to medium horizons. Up regime means each shorter smoother sits below the next longer one; down regime is the inverse.

State machine: On bar close, positive Heikin-Ashi bias starts a bull state and negative bias starts a bear state. The state terminates the moment the smoother ordering breaks relative to the prior bar.

Rendering gate: A marker prints only if the active state agrees with the current HMA slope. The HMA is plotted and colored by slope for context.

Normalization and clamping: Marker transparency transitions from a starting to an ending alpha across a fixed number of bars, clamped within the allowed range.

Initialization: Persistent variables track state and bar-count since state start; Heikin-Ashi open is seeded on the first valid bar.

HTF/security: None used. State updates are closed-bar, which reduces repaint paths.

Bands: Smoothed high, low, centerline, and offset bands are computed but not rendered.

Parameter Guide

Show Markers — Toggle rendering — Default: true — Hides markers without changing logic.

Bull Color / Bear Color — Visual colors — Defaults: bright green / red — Aesthetic only.

Start Alpha / End Alpha — Transparency range — Defaults: one hundred / fifty, within zero to one hundred — Controls initial visibility and fade endpoint.

Steps — Fade length in bars — Default: eight, minimum one — Longer values extend the visual memory of a state.

Smoother Length — Internal band smoothing — Default: twenty-one, minimum two — Affects computed bands only; not drawn.

Band Multiplier — Internal band offset — Default: one point zero — No impact on markers.

Source — Input for HMA — Default: close — Align with your workflow.

Length — HMA length — Default: fifty, minimum one — Larger values reduce flips; smaller values react faster.

Reading & Interpretation

Entry markers:

Bull marker (below bar): Closed-bar Heikin-Ashi bias is positive, smoother stack remains aligned for up regime, and HMA slope is rising.

Bear marker (above bar): Closed-bar Heikin-Ashi bias is negative, smoother stack remains aligned for down regime, and HMA slope is falling.

Fade: Transparency progresses over the configured steps, indicating how long the current state has persisted.

Practical Workflows & Combinations

Trend following: Focus on marker clusters aligned with HMA color. Add structure filters such as higher highs and higher lows or lower highs and lower lows to avoid counter-trend entries.

Exits/Stops: Consider exiting or reducing risk when smoother ordering breaks, when HMA color flips, or when marker cadence thins out.

Multi-asset/Multi-TF: Suitable for liquid crypto, FX, indices, and equities. On lower timeframes, shorten HMA length and fade steps for faster response.

Behavior, Constraints & Performance

Repaint/confirmation: State transitions and marker eligibility are decided on closed bars; live bars do not commit state changes until close.

security()/HTF: Not used.

Resources: Declared max bars back of one thousand five hundred; recursive filters and persistent states; no explicit loops.

Known limits: Some delay around sharp turns; brief states may start in noisy phases but are quickly revoked when alignment fails; HMA gating can miss very early reversals.

Sensible Defaults & Quick Tuning

Start here: Keep defaults.

Too many flips: Increase HMA length and raise fade steps.

Too sluggish: Decrease HMA length and reduce fade steps.

Markers too faint/bold: Adjust start and end alpha toward lower or higher opacity.

What this indicator is—and isn’t

A selective entry-marker layer that prints only under triple confirmation with stateful guardrails. It is not a full system, not predictive, and does not handle risk. Combine with market structure, risk controls, and position management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

ARGT Possible entry and exit points:This is just an observation, and not any type of financial advice.

]To identify key entry and exit points. In addition, this is based on YTD and yearly charts. This is a work in progress.

SuperScript Filtered (Stable)🔎 What This Indicator Does

The indicator is a trend and momentum filter.

It looks at multiple well-known technical tools (T3 moving averages, RSI, TSI, and EMA trend) and assigns a score to the current market condition.

• If most tools are bullish → score goes up.

• If most tools are bearish → score goes down.

• Only when the score is very strong (above +75 or below -75), it prints a Buy or Sell signal.

This helps traders focus only on high-probability setups instead of reacting to every small wiggle in price.

________________________________________

⚙️ How It Works

1. T3 Trend Check

o Compares a fast and slow T3 moving average.

o If the fast T3 is above the slow T3 → bullish signal.

o If it’s below → bearish signal.

2. RSI Check

o Uses the Relative Strength Index.

o If RSI is above 50 → bullish momentum.

o If RSI is below 50 → bearish momentum.

3. TSI Check

o Uses the True Strength Index.

o If TSI is above its signal line → bullish momentum.

o If TSI is below → bearish momentum.

4. EMA Trend Check

o Looks at two exponential moving averages (fast and slow).

o If price is above both → bullish.

o If price is below both → bearish.

5. Score System

o Each condition contributes +25 (bullish) or -25 (bearish).

o The total score can range from -100 to +100.

o Score ≥ +75 → Strong Buy

o Score ≤ -75 → Strong Sell

6. Signal Filtering

o Only one buy is allowed until a sell appears (and vice versa).

o A minimum bar gap is enforced between signals to avoid clutter.

________________________________________

📊 How It Appears on the Chart

• Green “BUY” label below candles → when multiple signals agree and the market is strongly bullish.

• Red “SELL” label above candles → when multiple signals agree and the market is strongly bearish.

• Background softly shaded green or red → highlights bullish or bearish conditions.

No messy tables, no clutter — just clear trend-based entries.

________________________________________

🎯 How Traders Can Use It

This indicator is designed to help traders by:

1. Filtering Noise

o Instead of reacting to every small crossover or RSI blip, it waits until at least 3–4 conditions agree.

o This avoids entering weak trades.

2. Identifying Strong Trend Shifts

o When a Buy or Sell arrow appears, it usually signals a shift in momentum that can lead to a larger move.

3. Reducing Overtrading

o By limiting signals, traders won’t be tempted to jump in and out unnecessarily.

4. Trade Confirmation

o Traders can use the signals as confirmation for their own setups.

o Example: If your strategy says “go long” and the indicator also shows a strong Buy, that trade has more conviction.

5. Alert Automation

o Built-in alerts mean you don’t have to watch the chart all day.

o You’ll be notified only when a strong signal appears.

________________________________________

⚡ When It Helps the Most

• Works best in trending markets (bullish or bearish).

• Very useful on higher timeframes (1h, 4h, daily) for swing trading.

• Can also work on lower timeframes (5m, 15m) if combined with higher timeframe trend filtering.

________________________________________

👉 In short

This indicator is a signal filter + trend detector. It combines four powerful tools into one scoring system, and only tells you to act when the odds are stacked in your favor.

________________________________________