Crowding model ║ BullVision🔬 Overview

The Crypto Crowding Model Pro is a sophisticated analytical tool designed to visualize and quantify market conditions across multiple cryptocurrencies. By leveraging Relative Strength Index (RSI) and Z-score calculations, this indicator provides traders with an intuitive and detailed snapshot of current crypto market dynamics, highlighting areas of extreme momentum, crowded trades, and potential reversal points.

⚙️ Key Concepts

📊 RSI and Z-Score Analysis

RSI (Relative Strength Index) evaluates the momentum and strength of each cryptocurrency, identifying overbought or oversold conditions.

Z-Score Normalization measures each asset's current price deviation relative to its historical average, identifying statistically significant extremes.

🎯 Crowding Analytics

An integrated analytics panel provides real-time crowding metrics, quantifying market sentiment into four distinct categories:

🔥 FOMO (Fear of Missing Out): High momentum, potential exhaustion.

❄️ Fear: Low momentum, potential reversal or consolidation.

📈 Recovery: Moderate upward momentum after a downward trend.

💪 Strength: Stable bullish conditions with sustained momentum.

🖥️ Visual Scatter Plot

Assets are plotted on a dynamic scatter plot, positioning each cryptocurrency according to its RSI and Z-score.

Color coding, symbol shapes, and sizes help quickly identify main market segments (BTC, ETH, TOTAL, OTHERS) and individual asset conditions.

🧩 Quadrant Classification

Assets are categorized into four quadrants based on their momentum and deviation:

Overbought Extended: High RSI and positive Z-score.

Recovery Phase: Low RSI but positive Z-score.

Oversold Compressed: Low RSI and negative Z-score.

Strong Consolidation: High RSI but negative Z-score.

🔧 User Customization

🎨 Visual Settings

Bar Scale: Adjust the scatter plot visual scale.

Asset Visibility: Optionally display key market benchmarks (TOTAL, BTC, ETH, OTHERS).

Gradient Background: Enhances visual interpretation of asset clusters.

Crowding Analytics Panel: Toggle the analytics panel on/off.

📊 Indicator Parameters

RSI Length: Defines the calculation period for RSI.

Z-score Lookback: Historical lookback period for normalization.

Crowding Alert Threshold: Sets alert sensitivity for crowded market conditions.

🎯 Zone Settings

Quadrant Labels: Displays descriptive labels for each quadrant.

Danger Zones: Highlights extreme RSI levels indicative of heightened market risk.

📈 Visual Output

Dynamic Scatter Plot: Visualizes asset positioning clearly and intuitively.

Gradient and Grid: Professional gridlines and subtle gradient backgrounds assist visual assessment.

Danger Zone Highlights: Visually indicates RSI extremes to warn of potential market turning points.

Crowding Analytics Panel: Real-time summary of market sentiment and asset distribution.

🔍 Use Cases

This indicator is particularly beneficial for traders and analysts looking to:

Identify crowded trades and potential reversal points.

Quickly assess overall market sentiment and individual asset strength.

Integrate a robust momentum analysis into broader technical or fundamental strategies.

Enhance market timing and improve risk management decisions.

⚠️ Important Notes

This indicator does not provide explicit buy or sell signals.

It is intended solely for informational, analytical, and educational purposes.

Past performance and signals are not indicative of future market results.

Always combine with additional tools and analysis as part of comprehensive decision-making.

Indicateurs et stratégies

Dynamic Gap Probability ToolDynamic Gap Probability Tool measures the percentage gap between price and a chosen moving average, then analyzes your chart history to estimate the likelihood of the next candle moving up or down. It dynamically adjusts its sample size to ensure statistical robustness while focusing on the exact deviation level.

Originality and Value:

• Combines gap-based analysis with dynamic sample aggregation to balance precision and reliability.

• Automatically extends the sample when exact matches are scarce, avoiding misleading signals on rare extreme moves.

• Provides real “next-candle” probabilities based on historical occurrences rather than fixed thresholds or untested heuristics.

• Adds value by giving traders an evidence-based edge: you see how similar past deviations actually played out.

How It Works:

1. Calculate gap = (close – moving average) / moving average * 100.

2. Round the absolute gap to nearest percent (X%).

3. Count historical bars where gap ≥ X% above or ≤ –X% below.

4. If exact X% count is below the minimum occurrences threshold, include gaps at X+1%, X+2%, etc., until threshold is reached.

5. Compute “next-candle” green vs. red probabilities from the aggregated sample.

6. Display current gap, sample size, green probability, and red probability in a table.

Inputs:

• Moving Average Type (SMA, EMA, WMA, VWMA, HMA, SMMA, TMA)

• Moving Average Period (default 200)

• Minimum Occurrences Threshold (default 50)

• Table position and styling options

Examples:

• If price is 3% above the 200-period SMA and 120 occurrences ≥3% are found, with 84 green next candles (70%) and 36 red (30%), the script displays “3% | 120 | 70% green | 30% red.”

• If price is 8% below the SMA but only 20 exact matches exist, the script will include 9% and 10% gaps until it reaches 50 samples, then calculate probabilities from that broader set.

Why It’s Useful:

• Mean-reversion traders see green-probability signals at extreme overbought or oversold levels.

• Trend-followers identify continuation likelihood when red probability is high.

• Risk managers gauge reliability by inspecting sample size before acting on any signal.

Limitations:

• Historical probabilities do not guarantee future performance.

• Results depend on timeframe and symbol, backtest with your data before trading.

• Use realistic slippage and commission when overlaying on strategy scripts.

EVaR Indicator and Position SizingThe Problem:

Financial markets consistently show "fat-tailed" distributions where extreme events occur with higher frequency than predicted by normal distributions (Gaussian or even log-normal). These fat tails manifest in sudden price crashes, volatility spikes, and black swan events that traditional risk measures like volatility can underestimate. Standard deviation and conventional VaR calculations assume normally distributed returns, leaving traders vulnerable to severe drawdowns during market stress.

Cryptocurrencies and volatile instruments display particularly pronounced fat-tailed behavior, with extreme moves occurring 5-10 times more frequently than normal distribution models would predict. This reality demands a more sophisticated approach to risk measurement and position sizing.

The Solution: Entropic Value at Risk (EVAR)

EVaR addresses these limitations by incorporating principles from statistical mechanics and information theory through Tsallis entropy. This advanced approach captures the non-linear dependencies and power-law distributions characteristic of real financial markets.

Entropy is more adaptive than standard deviations and volatility measures.

I was inspired to create this indicator after reading the paper " The End of Mean-Variance? Tsallis Entropy Revolutionises Portfolio Optimisation in Cryptocurrencies " by by Sana Gaied Chortane and Kamel Naoui.

Key advantages of EVAR over traditional risk measures:

Superior tail risk capture: More accurately quantifies the probability of extreme market moves

Adaptability to market regimes: Self-calibrates to changing volatility environments

Non-parametric flexibility: Makes less assumptions about the underlying return distribution

Forward-looking risk assessment: Better anticipates potential market changes (just look at the charts :)

Mathematically, EVAR is defined as:

EVAR_α(X) = inf_{z>0} {z * log(1/α * M_X(1/z))}

Where the moment-generating function is calculated using q-exponentials rather than conventional exponentials, allowing precise modeling of fat-tailed behavior.

Technical Implementation

This indicator implements EVAR through a q-exponential approach from Tsallis statistics:

Returns Calculation: Price returns are calculated over the lookback period

Moment Generating Function: Approximated using q-exponentials to account for fat tails

EVAR Computation: Derived from the MGF and confidence parameter

Normalization: Scaled to for intuitive visualization

Position Sizing: Inversely modulated based on normalized EVAR

The q-parameter controls tail sensitivity—higher values (1.5-2.0) increase the weighting of extreme events in the calculation, making the model more conservative during potentially turbulent conditions.

Indicator Components

1. EVAR Risk Visualization

Dynamic EVAR Plot: Color-coded from red to green normalized risk measurement (0-1)

Risk Thresholds: Reference lines at 0.3, 0.5, and 0.7 delineating risk zones

2. Position Sizing Matrix

Risk Assessment: Current risk level and raw EVAR value

Position Recommendations: Percentage allocation, dollar value, and quantity

Stop Parameters: Mathematically derived stop price with percentage distance

Drawdown Projection: Maximum theoretical loss if stop is triggered

Interpretation and Application

The normalized EVAR reading provides a probabilistic risk assessment:

< 0.3: Low risk environment with minimal tail concerns

0.3-0.5: Moderate risk with standard tail behavior

0.5-0.7: Elevated risk with increased probability of significant moves

> 0.7: High risk environment with substantial tail risk present

Position sizing is automatically calculated using an inverse relationship to EVAR, contracting during high-risk periods and expanding during low-risk conditions. This is a counter-cyclical approach that ensures consistent risk exposure across varying market regimes, especially when the market is hyped or overheated.

Parameter Optimization

For optimal risk assessment across market conditions:

Lookback Period: Determines the historical window for risk calculation

Q Parameter: Controls tail sensitivity (higher values increase conservatism)

Confidence Level: Sets the statistical threshold for risk assessment

For cryptocurrencies and highly volatile instruments, a q-parameter between 1.5-2.0 typically provides the most accurate risk assessment because it helps capturing the fat-tailed behavior characteristic of these markets. You can also increase the q-parameter for more conservative approaches.

Practical Applications

Adaptive Risk Management: Quantify and respond to changing tail risk conditions

Volatility-Normalized Positioning: Maintain consistent exposure across market regimes

Black Swan Detection: Early identification of potential extreme market conditions

Portfolio Construction: Apply consistent risk-based sizing across diverse instruments

This indicator is my own approach to entropy-based risk measures as an alterative to volatility and standard deviations and it helps with fat-tailed markets.

Enjoy!

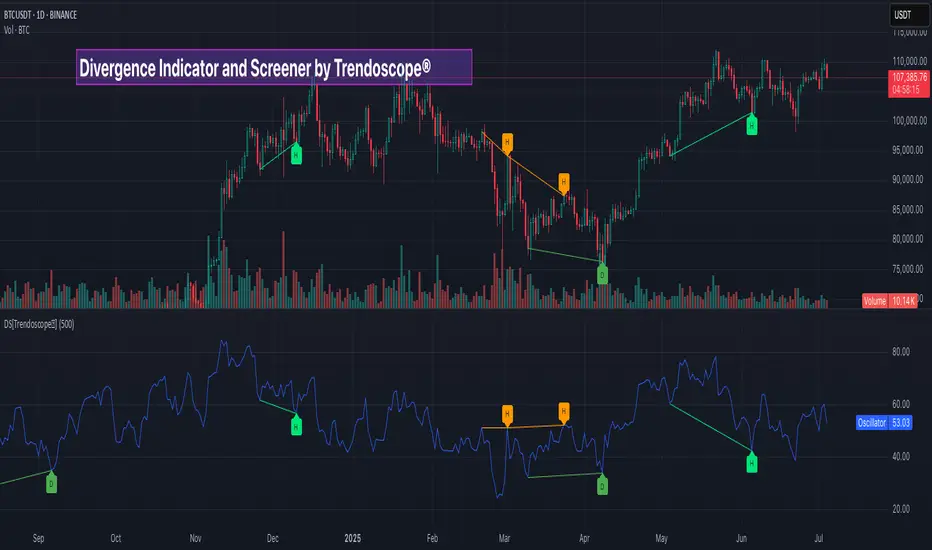

Divergence Screener [Trendoscope®]🎲Overview

The Divergence Screener is a powerful TradingView indicator designed to detect and visualize bullish and bearish divergences, including hidden divergences, between price action and a user-selected oscillator. Built with flexibility in mind, it allows traders to customize the oscillator type, trend detection method, and other parameters to suit various trading strategies. The indicator is non-overlay, displaying divergence signals directly on the oscillator plot, with visual cues such as lines and labels on the chart for easy identification.

This indicator is ideal for traders seeking to identify potential reversal or continuation signals based on price-oscillator divergences. It supports multiple oscillators, trend detection methods, and alert configurations, making it versatile for different markets and timeframes.

🎲Features

🎯Customizable Oscillator Selection

Built-in Oscillators : Choose from a variety of oscillators including RSI, CCI, CMO, COG, MFI, ROC, Stochastic, and WPR.

External Oscillator Support : Users can input an external oscillator source, allowing integration with custom or third-party indicators.

Configurable Length : Adjust the oscillator’s period (e.g., 14 for RSI) to fine-tune sensitivity.

🎯Divergence Detection

The screener identifies four types of divergences:

Bullish Divergence : Price forms a lower low, but the oscillator forms a higher low, signaling potential upward reversal.

Bearish Divergence : Price forms a higher high, but the oscillator forms a lower high, indicating potential downward reversal.

Bullish Hidden Divergence : Price forms a higher low, but the oscillator forms a lower low, suggesting trend continuation in an uptrend.

Bearish Hidden Divergence : Price forms a lower high, but the oscillator forms a higher high, suggesting trend continuation in a downtrend.

🎯Flexible Trend Detection

The indicator offers three methods to determine the trend context for divergence detection:

Zigzag : Uses zigzag pivots to identify trends based on higher highs (HH), higher lows (HL), lower highs (LH), and lower lows (LL).

MA Difference : Calculates the trend based on the difference in a moving average (e.g., SMA, EMA) between divergence pivots.

External Trend Signal : Allows users to input an external trend signal (positive for uptrend, negative for downtrend) for custom trend analysis.

🎯Zigzag-Based Pivot Analysis

Customizable Zigzag Length : Adjust the zigzag length (default: 13) to control the sensitivity of pivot detection.

Repaint Option : Choose whether divergence lines repaint based on the latest data or wait for confirmed pivots, balancing responsiveness and reliability.

🎯Visual and Alert Features

Divergence Visualization : Divergence lines are drawn between price pivots and oscillator pivots, color-coded for easy identification:

Bullish Divergence : Green

Bearish Divergence : Red

Bullish Hidden Divergence : Lime

Bearish Hidden Divergence : Orange

Labels and Tooltips : Labels (e.g., “D” for divergence, “H” for hidden) appear on price and oscillator pivots, with tooltips providing detailed information such as price/oscillator values, ratios, and pivot directions.

Alerts : Configurable alerts for each divergence type (bullish, bearish, bullish hidden, bearish hidden) trigger on bar close, ensuring timely notifications.

🎲 How It Works

🎯Oscillator Calculation

The indicator calculates the selected oscillator (or uses an external source) and plots it on the chart.

Oscillator values are stored in a map for reference during divergence calculations.

🎯Pivot Detection

A zigzag algorithm identifies pivots in the oscillator data, with configurable length and repainting options.

Price and oscillator pivots are compared to detect divergences based on their direction and ratio.

🎯Divergence Identification

The indicator compares price and oscillator pivot directions (HH, HL, LH, LL) to identify divergences.

Trend context is determined using the selected method (Zigzag, MA Difference, or External).

Divergences are classified as bullish, bearish, bullish hidden, or bearish hidden based on price-oscillator relationships and trend direction.

🎯Visualization and Alerts

Valid divergences are drawn as lines connecting price and oscillator pivots, with corresponding labels.

Alerts are triggered for allowed divergence types, providing detailed information via tooltips.

🎯Validation

Divergence lines are validated to ensure no intermediate bars violate the divergence condition, enhancing signal reliability.

🎲 Usage Instructions as Indicator

🎯Add to Chart:

Add the “Divergence Screener ” to your TradingView chart.

The indicator appears in a separate pane below the price chart, plotting the oscillator and divergence signals.

🎯Configure Settings:

Adjust the oscillator type and length to match your trading style.

Select a trend detection method and configure related parameters (e.g., MA type/length or external signal).

Set the zigzag length and repainting preference.

Enable/disable alerts for specific divergence types.

I🎯nterpret Signals:

Bullish Divergence (Green) : Look for potential buy opportunities in a downtrend.

Bearish Divergence (Red) : Consider sell opportunities in an uptrend.

Bullish Hidden Divergence (Lime) : Confirm continuation in an uptrend.

Bearish Hidden Divergence (Orange): Confirm continuation in a downtrend.

Use tooltips on labels to review detailed pivot and divergence information.

🎯Set Alerts:

Create alerts for each divergence type to receive notifications via TradingView’s alert system.

Alerts include detailed text with price, oscillator, and divergence information.

🎲 Example Scenarios as Indicator

🎯 With External Oscillator (Use MACD Histogram as Oscillator)

In order to use MACD as an oscillator for divergence signal instead of the built in options, follow these steps.

Load MACD Indicator from Indicator library

From Indicator settings of Divergence Screener, set Use External Oscillator and select MACD Histograme from the dropdown

You can now see that the oscillator pane shows the data of selected MACD histogram and divergence signals are generated based on the external MACD histogram data.

🎯 With External Trend Signal (Supertrend Ladder ATR)

Now let's demonstrate how to use external direction signals using Supertrend Ladder ATR indicator. Please note that in order to use the indicator as trend source, the indicator should return positive integer for uptrend and negative integer for downtrend. Steps are as follows:

Load the desired trend indicator. In this example, we are using Supertrend Ladder ATR

From the settings of Divergence Screener, select "External" as Trend Detection Method

Select the trend detection plot Direction from the dropdown. You can now see that the divergence signals will rely on the new trend settings rather than the built in options.

🎲 Using the Script with Pine Screener

The primary purpose of the Divergence Screener is to enable traders to scan multiple instruments (e.g., stocks, ETFs, forex pairs) for divergence signals using TradingView’s Pine Screener, facilitating efficient comparison and identification of trading opportunities.

To use the Divergence Screener as a screener, follow these steps:

Add to Favorites : Add the Divergence Screener to your TradingView favorites to make it available in the Pine Screener.

Create a Watchlist : Build a watchlist containing the instruments (e.g., stocks, ETFs, or forex pairs) you want to scan for divergences.

Access Pine Screener : Navigate to the Pine Screener via TradingView’s main menu: Products -> Screeners -> Pine, or directly visit tradingview.com/pine-screener/.

Select Watchlist : Choose the watchlist you created from the Watchlist dropdown in the Pine Screener interface.

Choose Indicator : Select Divergence Screener from the Choose Indicator dropdown.

Configure Settings : Set the desired timeframe (e.g., 1 hour, 1 day) and adjust indicator settings such as oscillator type, zigzag length, or trend detection method as needed.

Select Filter Criteria : Select the condition on which the watchlist items needs to be filtered. Filtering can only be done on the plots defined in the script.

Run Scan : Press the Scan button to display divergence signals across the selected instruments. The screener will show which instruments exhibit bullish, bearish, bullish hidden, or bearish hidden divergences based on the configured settings.

🎲 Limitations and Possible Future Enhancements

Limitations are

Custom input for oscillator and trend detection cannot be used in pine screener.

Pine screener has max 500 bars available.

Repaint option is by default enabled. When in repaint mode expect the early signal but the signals are prone to repaint.

Possible future enhancements

Add more built-in options for oscillators and trend detection methods so that dependency on external indicators is limited

Multi level zigzag support

Logarithmic Moving Average (LMA) [QuantAlgo]🟢 Overview

The Logarithmic Moving Average (LMA) uses advanced logarithmic weighting to create a dynamic trend-following indicator that prioritizes recent price action while maintaining statistical significance. Unlike traditional moving averages that use linear or exponential weights, this indicator employs logarithmic decay functions to create a more sophisticated price averaging system that adapts to market volatility and momentum conditions.

The indicator displays a smoothed signal line that oscillates around zero, with positive values indicating bullish momentum and negative values indicating bearish momentum. The signal incorporates trend quality assessment, momentum confirmation, and multiple filtering mechanisms to help traders and investors identify trend continuation and reversal opportunities across different timeframes and asset classes.

🟢 How It Works

The indicator's core innovation lies in its logarithmic weighting system, where weights are calculated using the formula: w = 1.0 / math.pow(math.log(i + steepness), 2) The steepness parameter controls how aggressively recent data is prioritized over historical data, creating a dynamic weight decay that can be fine-tuned for different trading styles. This logarithmic approach provides more nuanced weight distribution compared to exponential moving averages, offering better responsiveness while maintaining stability.

The LMA calculation combines multiple sophisticated components. First, it calculates the logarithmic weighted average of closing prices. Then it measures the slope of this average over a 10-period lookback: lmaSlope = (lma - lma ) / lma * 100 The system also incorporates trend quality assessment using R-squared correlation analysis of log-transformed prices, measuring how well the price data fits a linear trend model over the specified period.

The final signal generation uses the formula: signal = lmaSlope * (0.5 + rSquared * 0.5) which combines the LMA slope with trend quality weighting. When momentum confirmation is enabled, the indicator calculates annualized log-return momentum and applies a multiplier when the momentum direction aligns with the signal direction, strengthening confirmed signals while filtering out weak or counter-trend movements.

🟢 How to Use

1. Signal Interpretation and Threshold Zones

Positive Values (Above Zero): LMA slope indicating bullish momentum with upward price trajectory relative to logarithmic baseline

Negative Values (Below Zero): LMA slope indicating bearish momentum with downward price trajectory relative to logarithmic baseline

Zero Line Crosses: Signal transitions between bullish and bearish regimes, indicating potential trend changes

Long Entry Threshold Zone: Area above positive threshold (default 0.5) indicating confirmed bullish signals suitable for long positions

Short Entry Threshold Zone: Area below negative threshold (default -0.5) indicating confirmed bearish signals suitable for short positions

Extreme Values: Signals exceeding ±1.0 represent strong momentum conditions with higher probability of continuation

2. Momentum Confirmation and Visual Analysis

Signal Color Intensity: Gradient coloring shows signal strength, with brighter colors indicating stronger momentum

Bar Coloring: Optional price bar coloring matches signal direction for quick visual trend identification

Position Labels: Real-time position classification (Bullish/Bearish/Neutral) displayed on the latest bar

Momentum Weight Factor: When short-term log-return momentum aligns with LMA signal direction, the signal receives additional weight confirmation

Trend Quality Component: R-squared values weight the signal strength, with higher correlation indicating more reliable trend conditions

3. Examples: Preconfigured Settings

Default: Universally applicable configuration balanced for medium-term investing and general trading across multiple timeframes and asset classes.

Scalping: Highly responsive setup with shorter period and higher steepness for ultra-short-term trades on 1-15 minute charts, optimized for quick momentum shifts.

Swing Trading: Extended period with moderate steepness and increased smoothing for multi-day positions, designed to filter noise while capturing larger price swings on 1-4 hour and daily charts.

Trend Following: Maximum smoothing with lower steepness for established trend identification, generating fewer but more reliable signals optimal for daily and weekly timeframes.

Mean Reversion: Shorter period with high steepness for counter-trend strategies, more sensitive to extreme moves and reversal opportunities in ranging market conditions.

Volumatic Support/Resistance Levels [BigBeluga]🔵 OVERVIEW

A smart volume-powered tool for identifying key support and resistance zones—enhanced with real-time volume histogram fills and high-volume markers.

Volumatic Support/Resistance Levels detects structural levels from swing highs and lows, and wraps them in dynamic histograms that reflect the relative volume strength around those zones. It highlights the strongest price levels not just by structure—but by the weight of market participation.

🔵 CONCEPTS

Price Zones: Support and resistance levels are drawn from recent price pivots, while volume is used to visually enhance these zones with filled histograms and highlight moments of peak activity using markers.

Histogram Fill = Activity Zone: The width and intensity of each filled zone adjusts to recent volume bursts.

High-Volume Alerts: Circle markers highlight moments of volume dominance directly on the levels—revealing pressure points of support/resistance.

Clean Visual Encoding: Red = resistance zones, green = support zones, orange = high-volume bars.

🔵 FEATURES

Detects pivot-based resistance (highs) and support (lows) using a customizable range length.

Wraps these levels in volume-weighted bands that expand/contract based on percentile volume.

Color fill intensity increases with rising volume pressure, creating a live histogram feel.

When volume > user-defined threshold , the indicator adds circle markers at the top and bottom of that price level zone.

Bar coloring highlights the candles that generated this high-volume behavior (orange by default).

Adjustable settings for all thresholds and colors, so traders can dial in volume sensitivity.

🔵 HOW TO USE

Identify volume-confirmed resistance and support zones for potential reversal or breakout setups.

Focus on levels with intense histogram fill and circle markers —they indicate strong participation.

Use bar coloring to track when key activity started and align it with broader market context.

Works well in combination with order blocks, trend indicators, or liquidity zones.

Ideal for day traders, scalpers, and volume-sensitive setups.

🔵 CONCLUSION

Volumatic Support/Resistance Levels elevates traditional support and resistance logic by anchoring it in volume context. Instead of relying solely on price action, it gives traders insight into where real conviction lies—by mapping how aggressively the market defended or rejected key levels. It's a visual, reactive, and volume-conscious upgrade to your structural toolkit.

True Close – Institutional Trading Sessions (Zeiierman)█ Overview

True Close – Institutional Trading Sessions (Zeiierman) is a professional-grade session mapping tool designed to help traders align with how institutions perceive the market’s true close. Unlike the textbook “daily close” used by retail traders, institutional desks often anchor their risk management, execution benchmarks, and exposure metrics to the first hour of the next session.

This indicator visualizes that logic directly on your chart — drawing session boxes, true close levels, and time-aligned labels across Sydney, Tokyo, London, and New York. It highlights the first hour of each session, projects the institutional closing price, and builds a live dashboard that tells you which sessions are active, which are in the critical opening phase, and what levels matter most right now.

More than just a visual tool, this indicator embeds institutional rhythm directly into your workflow — giving you a window into where big players finalize yesterday’s business, rebalance exposure, and execute delayed orders. It’s not just about painting sessions on your chart — it’s about adopting the mindset of those who truly move the market. Institutions don’t settle risk at the bell; they complete it in the next session. This tool lets you see that transition in real time, giving you an edge that goes beyond candles and indicators.

█ How It Works

⚪ Session Detection Engine

Each session is identified by its own time block (e.g., 09:00–17:30 for London). Once a session opens:

A full-session box is drawn to track its range.

The first hour is highlighted separately.

Once the first hour completes, the true close line is plotted, representing the price institutions often treat as the "real" close of the prior day.

⚪ Institutional True Close Logic

The script captures the close of the first hour, not the end of the day.

This line becomes a static reference across your chart, letting you visualize how price interacts with that institutional anchor:

Rejections from it show where yesterday's flow is respected.

Breaks through it may indicate that today's flows are rewriting the narrative.

⚪ Dynamic Dashboard Table

A live table appears in the corner of your screen, showing:

Each session's active status

Whether we’re inside the first hour

The current “true close” price if available

Each cell comes with advanced tooltips giving institutional context, flow dynamics, and market microstructure insights — from rebalancing spillovers to VWAP/TWAP lag effects.

█ How to Use

⚪ Use the First-Hour Line as Your Institutional Anchor

Treat it like the price level that big funds care about. Watch how the price behaves around level. Fades, re-tests, or continuation moves often occur as the market finishes recapping yesterday’s leftover orders.

⚪ Structure Entries Around the Session Context

Are you inside the first hour? Expect more volatility, more decisive flow. After the first session hour, expect fading liquidity as the market slows down and awaits the next session to open.

█ Settings

UTC Offset – Select your preferred time zone; all sessions adjust accordingly.

Session Toggles – Enable/disable Sydney, Tokyo, London, or NY.

Box Display Options – Show/hide session background, first-hour fill, borders.

True Close Line Controls – Enable line, label, and customize width & color.

Execution Hour Labels – Optional toggle for first-hour label placement.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

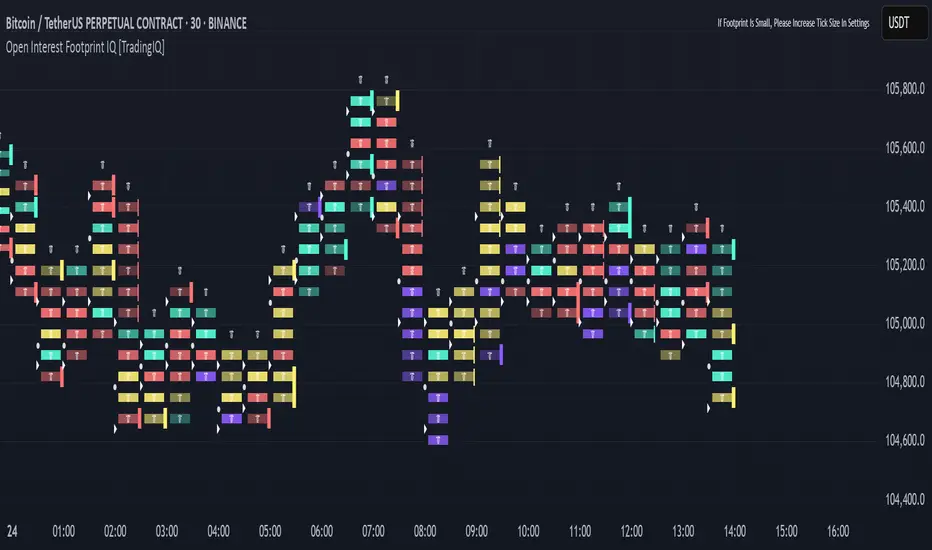

Open Interest Footprint IQ [TradingIQ]Hello Traders!

Th e Open Interest Footprint IQ indicator is an advanced visualization tool designed for cryptocurrency markets. It provides a granular, real-time breakdown of open interest changes across different price levels, allowing traders to see how aggressive market participation is distributed within each bar.

Unlike standard footprint charts that rely solely on volume, this indicator offers unique insights by focusing on the interaction between price action and changes in open interest (OI) — a leading metric often used to infer trader intent and positioning.

How it works

The Open Interest Footprint IQ processes lower timeframe price and open interest data to build a footprint-style chart that shows how traders are positioning themselves within each candle.

Here’s a breakdown of the process:

1. Granular OI & Price Sampling

The script retrieves lower-timeframe data (1-minute, 1-second, or 1-tick, based on your setting).

For each candle, it captures:

High and low prices

Price change direction

Change in open interest (OI)

2. Classifying Trader Behavior

For each lower-timeframe segment, the indicator determines the type of positioning occurring based on price movement and OI change:

If price is moving up and open interest is increasing, it suggests that long positions are being opened. This is considered a "Longs Opening" event, labeled as UU (Up/Up).

If price is moving up but open interest is decreasing, it indicates that short positions are being closed. This is referred to as UD (Up/Down), or "Shorts Closing."

If price is moving down and open interest is increasing, it signals that short positions are being opened. This is known as DU (Down/Up), or "Shorts Opening."

If price is moving down while open interest is also decreasing, it means that long positions are being closed. This is labeled as DD (Down/Down), or "Longs Closing."

These are stored in separate arrays and displayed at specific price levels.

It is particularly useful for identifying:

Where longs or shorts are opening/closing positions

Stacked imbalances (indicative of potential absorption or exhaustion)

Value area zones and POC (Point of Control) based on OI, not volume

This footprint runs on your choice of sub-bar granularity and is ideal for high-frequency trading, scalping, and entries based on order flow dynamics.

Key Features

Footprint Visualization

At each price level within a candle:

Long/short opening and closing behavior is broken down.

Delta (net open interest change) is displayed both numerically and color-coded.

Optional gradient coloring shows intensity and type of flow (longs/shorts opened/closed).

Cumulative or per-bar reset modes allow you to track OI evolution over time.

The image above explains the information that each Footprint box shows across a candlestick!

Each footprint box shows:

OI Delta

OI Delta %

Longs Opened (LO)

Longs Closed (LC)

Shorts Opened (SO)

Shorts Closed (SC)

The image above explains the color-coding feature of the indicator.

Boxes are color coded to show which position action

dominated at the price area.

For this example:

Green boxes = Long positions being opened dominated

Purple boxes = Long positions being closed dominated

Red boxes = Short positions being opened dominated

Yellow boxes = Short positions being closed dominated

All colors are customizable.

Additionally, for traders who are only interested in whether OI increased/decreased, a "two-color" option is available in the settings.

For the two-color option, footprint boxes can be one of two colors. Showing whether OI increased or decreased at the level.

Cumulative Levels

Open Interest Footprint IQ contains a "Cumulative Levels" feature that tracks/stores open interest change at tick levels over time, rather than resetting per bar.

With the "Cumulative Levels" feature enabled, traders can see open interest changes persist across all candlesticks. This feature is useful for determining whether longs opening, longs closing, shorts opening, or shorts closing are dominating at particular price areas over time rather than on a single bar.

A useful feature to see if shorts/longs are favoring certain price throughout the day, week, month, etc.

Input Settings Explained

Granularity (Dropdown: Granularity)

Options: 1-Minute, 1-Second, 1-Tick

Determines how finely the script samples the lower timeframe data to construct the footprint.

For precision:

1-Tick = Highest accuracy, but more resource-intensive.

1-Second/1-Minute = Suitable for broader or more zoomed-out analysis.

Tick Level Distance (Tick Level Distance (0 = Auto))

Defines the vertical spacing between levels in the footprint chart.

If 0, the script uses an automatic calculation based on ATR to adapt to volatility.

Set a manual value (e.g., 5) to control the height granularity of each level in ticks.

Cumulative Levels (Toggle)

If enabled, the footprint builds cumulatively over time, rather than resetting per candle.

Use case: Visualize ongoing buildup of OI activity across a session or day.

Cumulative Levels Reset TF (Timeframe)

Sets the reset interval for the cumulative view (e.g., reset daily, hourly, etc.)

Works only when Cumulative Levels is enabled.

Delta Box Display Settings

Show Delta Percentage

Toggles the display of the percentage change in OI across the footprint level.

Helpful to gauge how aggressive positioning is relative to total OI at that level.

Show Longs/Shorts (Opened/Closed)

Show Longs Opened: Displays OI increase in up candles (price ↑, OI ↑).

Show Longs Closed: Displays OI decrease in down candles (price ↓, OI ↓).

Show Shorts Opened: OI increase in down candles (price ↓, OI ↑).

Show Shorts Closed: OI decrease in up candles (price ↑, OI ↓).

These behaviors are color-coded to give traders instant context:

Blue-green for longs opening.

Purple for longs closing.

Red for shorts opening.

Yellow for shorts closing.

Value Area & POC

Value Area % (Value Area %)

Controls how much cumulative open interest is used to define the value area.

Example: 70% means the smallest range of prices that contains 70% of total OI in that bar will be marked.

Helps identify zones of interest, support/resistance, and institutional levels.

The image above explains how to identify the VAH/VAL/POC shown by Open Interest Footprint IQ.

VAH = Upper 🞂

POC = ●

VAL = Lower 🞂

Imbalances

Imbalance Percentage

Defines the minimum delta % required at a level to be marked as an imbalance.

If the net open interest change at a level exceeds this threshold, a visual marker appears.

Stacked Imbalance Count

If the number of consecutive imbalance levels meets this count, a “Stacked Imbalance” alert will trigger.

This can signal aggressive buying or selling pressure, potential breakout zones, or institutional absorption.

Color Settings

Longs Opened / Closed, Shorts Opened / Closed

Customize the color palette for each order flow behavior.

These colors appear in the background gradient of the footprint boxes.

Up/Down Only Mode

Toggle to override all behavior-based colors with a single Up Color and Down Color.

Useful if you prefer a simple bull/bear view.

Up Color / Down Color

If "Up/Down Only" is enabled, these two colors are used to represent all net positive or negative deltas.

Special Notes

Crypto only: This script works only with crypto tickers on TradingView.

For other assets (stocks, futures), a warning message will appear instead.

OI data must be available from the exchange (many perpetual pairs support this).

If the footprint is too small or invisible, increase your tick level spacing in the settings.

Alerts

When a stacked imbalance is detected, an alert is fired ("Stacked Imbalance").

This feature is useful for automated systems, bots, or simply staying informed of potential trade setups.

And that's all for now!

If you have any questions or features you'd like to see feel free to share them in the comments below!

Thank you traders!

Zigzag CandlesCan't deny that I am obsessed with zigzags. Been doing some crazy experiments with it and have many more in pipeline. I believe zigzag can be used to derive better trend following methods. Here is an attempt to visualize zigzag as candlesticks. Next steps probably to derive moving average, atr (although there was an attempt of AZR made earlier) and probably supertrend too ;)

Input parameters include ZigzagLength (to calculate zigzag) and CandleSize (number of zigzag pivots in each candle)

CandleSize can be 3 or more. Every time we collect pivots which are equal to CandleSize, we derive one candle. And when we derive a candle, we remove all old pivots except the last one. Becauase, the last pivot acts as open to the next bar and is required.

Body of the candle tells the start and end zigzag pivot in the range. And Wicks signify highest and lowest pivots in the range. High and Low wicks are placed at the pivot where high and lows are formed. Hence, you can see them at different positions each time.

Thanks to @RicardoSantos for suggesting boxes for candles - while I was trying to achieve this with plotbar

MathStatisticsKernelFunctionsLibrary "MathStatisticsKernelFunctions"

TODO: add library description here

uniform(distance, bandwidth) Uniform kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

triangular(distance, bandwidth) Triangular kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

epanechnikov(distance, bandwidth) Epanechnikov kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

quartic(distance, bandwidth) Quartic kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

triweight(distance, bandwidth) Triweight kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

tricubic(distance, bandwidth) Tricubic kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

gaussian(distance, bandwidth) Gaussian kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

cosine(distance, bandwidth) Cosine kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

logistic(distance, bandwidth) logistic kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

sigmoid(distance, bandwidth) Sigmoid kernel.

Parameters:

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

select(kernel, distance, bandwidth) Kernel selection method.

Parameters:

kernel : string, kernel to select. (options="uniform", "triangle", "epanechnikov", "quartic", "triweight", "tricubic", "gaussian", "cosine", "logistic", "sigmoid")

distance : float, distance to kernel origin.

bandwidth : float, default=1.0, bandwidth limiter to weight the kernel.

Returns: float.

MathConstantsLibrary "MathConstants"

Mathematical Constants

E() The number e

Log2E() The number log (e)

Log10E() The number log (e)

Ln2() The number log (2)

Ln10() The number log (10)

LnPi() The number log (pi)

Ln2PiOver2() The number log (2*pi)/2

InvE() The number 1/e

SqrtE() The number sqrt(e)

Sqrt2() The number sqrt(2)

Sqrt3() The number sqrt(3)

Sqrt1Over2() The number sqrt(1/2) = 1/sqrt(2) = sqrt(2)/2

HalfSqrt3() The number sqrt(3)/2

Pi() The number pi

Pi2() The number pi*2

PiOver2() The number pi/2

Pi3Over2() The number pi*3/2

PiOver4() The number pi/4

SqrtPi() The number sqrt(pi)

Sqrt2Pi() The number sqrt(2pi)

SqrtPiOver2() The number sqrt(pi/2)

Sqrt2PiE() The number sqrt(2*pi*e)

LogSqrt2Pi() The number log(sqrt(2*pi))

LogSqrt2PiE() The number log(sqrt(2*pi*e))

LogTwoSqrtEOverPi() The number log(2 * sqrt(e / pi))

InvPi() The number 1/pi

TwoInvPi() The number 2/pi

InvSqrtPi() The number 1/sqrt(pi)

InvSqrt2Pi() The number 1/sqrt(2pi)

TwoInvSqrtPi() The number 2/sqrt(pi)

TwoSqrtEOverPi() The number 2 * sqrt(e / pi)

Degree() The number (pi)/180 - factor to convert from Degree (deg) to Radians (rad).

Grad() The number (pi)/200 - factor to convert from NewGrad (grad) to Radians (rad).

PowerDecibel() The number ln(10)/20 - factor to convert from Power Decibel (dB) to Neper (Np). Use this version when the Decibel represent a power gain but the compared values are not powers (e.g. amplitude, current, voltage).

NeutralDecibel() The number ln(10)/10 - factor to convert from Neutral Decibel (dB) to Neper (Np). Use this version when either both or neither of the Decibel and the compared values represent powers.

Catalan() The Catalan constant

Sum(k=0 -> inf){ (-1)^k/(2*k + 1)2 }

EulerMascheroni() The Euler-Mascheroni constant

lim(n -> inf){ Sum(k=1 -> n) { 1/k - log(n) } }

GoldenRatio() The number (1+sqrt(5))/2, also known as the golden ratio

Glaisher() The Glaisher constant

e^(1/12 - Zeta(-1))

Khinchin() The Khinchin constant

prod(k=1 -> inf){1+1/(k*(k+2))^log(k,2)}

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

dema2(src, length)

An alternate Double Exponential Moving Average (Dema) function to `dema()`, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `src`.

dm(length)

Calculates the value of the "Demarker" indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

ema2(src, length)

An alternate ema function to the `ta.ema()` built-in, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Number of bars (length).

Returns: (float) The exponentially weighted moving average of the `src`.

eom(length, div)

Calculates the value of the Ease of Movement indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

div (simple int) : (simple int) Divisor used for normalzing values. Optional. The default is 10000.

Returns: (float) The oscillator value.

frama(source, length)

The Fractal Adaptive Moving Average (FRAMA), developed by John Ehlers, is an adaptive moving average that dynamically adjusts its lookback period based on fractal geometry.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The fractal adaptive moving average of the `source`.

ft(source, length)

Calculates the value of the Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

ht(source)

Calculates the value of the Hilbert Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

ichimoku(conLength, baseLength, senkouLength)

Calculates values of the Ichimoku Cloud indicator, including tenkan, kijun, senkouSpan1, senkouSpan2, and chikou. NOTE: offsets forward or backward can be done using the `offset` argument in `plot()`.

Parameters:

conLength (int) : (series int) Length for the Conversion Line (Tenkan). The default is 9 periods, which returns the mid-point of the 9 period Donchian Channel.

baseLength (int) : (series int) Length for the Base Line (Kijun-sen). The default is 26 periods, which returns the mid-point of the 26 period Donchian Channel.

senkouLength (int) : (series int) Length for the Senkou Span 2 (Leading Span B). The default is 52 periods, which returns the mid-point of the 52 period Donchian Channel.

Returns: ( [float, float, float, float, float ]) A tuple of the Tenkan, Kijun, Senkou Span 1, Senkou Span 2, and Chikou Span values. NOTE: by default, the senkouSpan1 and senkouSpan2 should be plotted 26 periods in the future, and the Chikou Span plotted 26 days in the past.

ift(source)

Calculates the value of the Inverse Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

kvo(fastLen, slowLen, trigLen)

Calculates the values of the Klinger Volume Oscillator.

Parameters:

fastLen (simple int) : (simple int) Length for the fast moving average smoothing parameter calculation.

slowLen (simple int) : (simple int) Length for the slow moving average smoothing parameter calculation.

trigLen (simple int) : (simple int) Length for the trigger moving average smoothing parameter calculation.

Returns: ( [float, float ]) A tuple of the KVO value, and the trigger value.

pzo(length)

Calculates the value of the Price Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

rms(source, length)

Calculates the Root Mean Square of the `source` over the `length`.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The RMS value.

rwi(length)

Calculates the values of the Random Walk Index.

Parameters:

length (simple int) : (simple int) Lookback and ATR smoothing parameter length.

Returns: ( [float, float ]) A tuple of the `rwiHigh` and `rwiLow` values.

stc(source, fast, slow, cycle, d1, d2)

Calculates the value of the Schaff Trend Cycle indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

fast (simple int) : (simple int) Length for the MACD fast smoothing parameter calculation.

slow (simple int) : (simple int) Length for the MACD slow smoothing parameter calculation.

cycle (simple int) : (simple int) Number of bars for the Stochastic values (length).

d1 (simple int) : (simple int) Length for the initial %D smoothing parameter calculation.

d2 (simple int) : (simple int) Length for the final %D smoothing parameter calculation.

Returns: (float) The oscillator value.

stochFull(periodK, smoothK, periodD)

Calculates the %K and %D values of the Full Stochastic indicator.

Parameters:

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

stochRsi(lengthRsi, periodK, smoothK, periodD, source)

Calculates the %K and %D values of the Stochastic RSI indicator.

Parameters:

lengthRsi (simple int) : (simple int) Length for the RSI smoothing parameter calculation.

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

source (float) : (series int/float) Series of values to process. Optional. The default is `close`.

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

supertrend(factor, atrLength, wicks)

Calculates the values of the SuperTrend indicator with the ability to take candle wicks into account, rather than only the closing price.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is false.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

szo(source, length)

Calculates the value of the Sentiment Zone Oscillator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

t3(source, length, vf)

Calculates the value of the Tilson Moving Average (T3).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

t3Alt(source, length, vf)

An alternate Tilson Moving Average (T3) function to `t3()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

tema(source, length)

Calculates the value of the Triple Exponential Moving Average (TEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

tema2(source, length)

An alternate Triple Exponential Moving Average (TEMA) function to `tema()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

trima(source, length)

Calculates the value of the Triangular Moving Average (TRIMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `source`.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a "series int" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `src`.

trix(source, length, signalLength, exponential)

Calculates the values of the TRIX indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

signalLength (simple int) : (simple int) Length for smoothing the signal line.

exponential (simple bool) : (simple bool) Condition to determine whether exponential or simple smoothing is used. Optional. The default is `true` (exponential smoothing).

Returns: ( [float, float, float ]) A tuple of the TRIX value, the signal value, and the histogram.

uo(fastLen, midLen, slowLen)

Calculates the value of the Ultimate Oscillator.

Parameters:

fastLen (simple int) : (series int) Number of bars for the fast smoothing average (length).

midLen (simple int) : (series int) Number of bars for the middle smoothing average (length).

slowLen (simple int) : (series int) Number of bars for the slow smoothing average (length).

Returns: (float) The oscillator value.

vhf(source, length)

Calculates the value of the Vertical Horizontal Filter.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

vi(length)

Calculates the values of the Vortex Indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the viPlus and viMinus values.

vzo(length)

Calculates the value of the Volume Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

williamsFractal(period)

Detects Williams Fractals.

Parameters:

period (int) : (series int) Number of bars (length).

Returns: ( [bool, bool ]) A tuple of an up fractal and down fractal. Variables are true when detected.

wpo(length)

Calculates the value of the Wave Period Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

█ v7, Nov. 2, 2023

This version includes the following new and updated functions:

atr2(length)

An alternate ATR function to the `ta.atr()` built-in, which allows a "series float" `length` argument.

Parameters:

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The ATR value.

changePercent(newValue, oldValue)

Calculates the percentage difference between two distinct values.

Parameters:

newValue (float) : (series int/float) The current value.

oldValue (float) : (series int/float) The previous value.

Returns: (float) The percentage change from the `oldValue` to the `newValue`.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

highestSince(cond, source)

Tracks the highest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the highest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `high`.

Returns: (float) The highest `source` value since the last time the `cond` was `true`.

lowestSince(cond, source)

Tracks the lowest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the lowest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `low`.

Returns: (float) The lowest `source` value since the last time the `cond` was `true`.

relativeVolume(length, anchorTimeframe, isCumulative, adjustRealtime)

Calculates the volume since the last change in the time value from the `anchorTimeframe`, the historical average volume using bars from past periods that have the same relative time offset as the current bar from the start of its period, and the ratio of these volumes. The volume values are cumulative by default, but can be adjusted to non-accumulated with the `isCumulative` parameter.

Parameters:

length (simple int) : (simple int) The number of periods to use for the historical average calculation.

anchorTimeframe (simple string) : (simple string) The anchor timeframe used in the calculation. Optional. Default is "D".

isCumulative (simple bool) : (simple bool) If `true`, the volume values will be accumulated since the start of the last `anchorTimeframe`. If `false`, values will be used without accumulation. Optional. The default is `true`.

adjustRealtime (simple bool) : (simple bool) If `true`, estimates the cumulative value on unclosed bars based on the data since the last `anchor` condition. Optional. The default is `false`.

Returns: ( [float, float, float ]) A tuple of three float values. The first element is the current volume. The second is the average of volumes at equivalent time offsets from past anchors over the specified number of periods. The third is the ratio of the current volume to the historical average volume.

rma2(source, length)

An alternate RMA function to the `ta.rma()` built-in, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The rolling moving average of the `source`.

supertrend2(factor, atrLength, wicks)

An alternate SuperTrend function to `supertrend()`, which allows a "series float" `atrLength` argument.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is `false`.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

vStop(source, atrLength, atrFactor)

Calculates an ATR-based stop value that trails behind the `source`. Can serve as a possible stop-loss guide and trend identifier.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

vStop2(source, atrLength, atrFactor)

An alternate Volatility Stop function to `vStop()`, which allows a "series float" `atrLength` argument.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

Removed Functions:

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a

"series int" length argument.

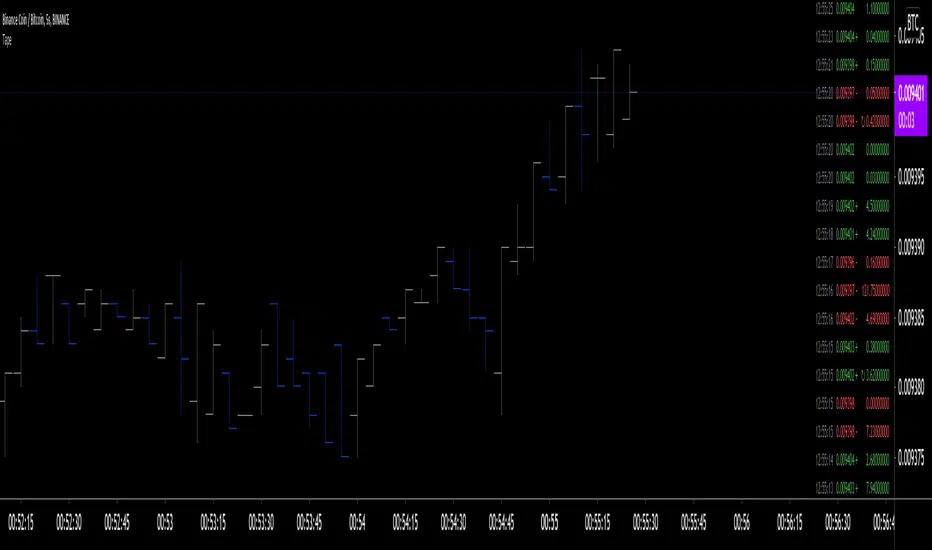

Tape [LucF]█ OVERVIEW

This script prints an ersatz of a trading console's "tape" section to the right of your chart. It displays the time, price and volume of each update of the chart's feed. It also calculates volume delta for the bar. As it calculates from realtime information, it will not display information on historical bars.

█ FEATURES

Calculations

Each new line in the tape displays the last price/volume update from the TradingView feed that's building your chart. These updates do not necessarily correspond to ticks from the originating broker/exchange's matching engine. Multiple broker/exchange ticks are often aggregated in one chart update.

The script first determines if price has moved up or down since the last update. The polarity of the price change, in turn, determines the polarity of the volume for that specific update. If price does not move between consecutive updates, then the last known polarity is used. Using this method, we can calculate a running volume delta accumulation for the bar, which becomes the bar's final volume delta value when the bar closes (you can inspect values of elapsed realtime bars in the Data Window or the indicator's values). Note that these values will all reset if the script re-executes because of a change in inputs or a chart refresh.

While this method of calculating volume delta is not perfect, it is currently the most precise way of calculating volume delta available on TradingView at the moment. Calculating more precise results would require scripts to have access to bid/ask levels from any chart timeframe. Charts at seconds timeframes do use exchange/broker ticks when the feeds you are using allow for it, and this indicator will run on them, but tick data is not yet available from higher timeframes, for now. Also note that the method used in this script is far superior to the intrabar inspection technique used on historical bars in my other "Delta Volume" indicators. This is because volume delta here is calculated from many more realtime updates than the available intrabars in history.

Inputs

You can use the script's inputs to configure:

• The number of lines displayed in the tape.

• If new lines appear at the top or bottom.

• If you want to hide lines with low volume.

• The precision of volume values.

• The size of the text and the colors used to highlight either the tape's text or background.

• The position where you want the tape on your chart.

• Conditions triggering three different markers.

Display

Deltas are shown at the bottom of the tape. They are reset on each bar. Time delta displays the time elapsed since the beginning of the bar, on intraday timeframes only. Contrary to the price change display by TradingView at the top left of charts, which is calculated from the close of the previous bar, the price delta in the tape is calculated from the bar's open, because that's the information used in the calculation of volume delta. The time will become orange when volume delta's polarity diverges from that of the bar. The volume delta value represents the current, cumulative value for the bar. Its color reflects its polarity.

When new realtime bars appear on the chart, a ↻ symbol will appear before the volume value in tape lines.

Markers

There are three types of markers you can choose to display:

• Marker 1 on volume bumps. A bump is defined as two consecutive and increasing/decreasing plus/minus delta volume values,

when no divergence between the polarity of delta volume and the bar occurs on the second bar.

• Marker 2 on volume delta for the bar exceeding a limit of your choice when there is no divergence between the polarity of delta volume and the bar. These trigger at the bar's close.

• Marker 3 on tape lines with volume exceeding a threshold. These trigger in realtime. Be sure to set a threshold high enough so that it doesn't generate too many alerts.

These markers will only display briefly under the bar, but another marker appears next to the relevant line in the tape.

The marker conditions are used to trigger alerts configured on the script. Alert messages will mention the marker(s) that triggered the specific alert event, along with the relevant volume value that triggered the marker. If more than one marker triggers a single alert, they will overprint under the bar, which can make it difficult to distinguish them.

For more detailed on-chart analysis of realtime volume delta, see my Delta Volume Realtime Action .

█ NOTES FOR CODERS

This script showcases two new Pine features:

• Tables, which allow Pine programmers to display tabular information in fixed locations of the chart. The tape uses this feature.

See the Pine User Manual's page on Tables for more information.

• varip -type variables which we can use to save values between realtime updates.

See the " Using `varip` variables " publication by PineCoders for more information.

Dominance Pie ChartA different type of charting, the pie chart,

here for showing the available dominance on one chart,

together with the total % dominance per ticker and between brackets

the % rise/fall.

Can be used in every timeframe

(It is normal it takes some time to be loaded)

Cheers!

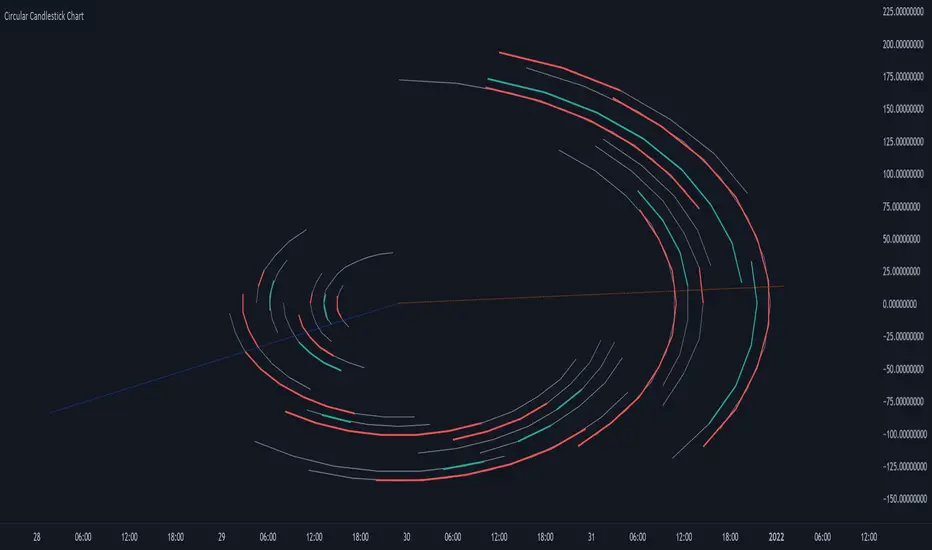

Circular Candlestick ChartAn original (but impractical) way to represent a candlestick chart using circles arc.

The most recent candles are further away from the circle origin. Note that OHLC values follow a clockwise direction. A higher arc length would indicate candles with a higher body or wick range.

The Length settings determine the number of past candles to be included in the circular candlestick chart. The Width setting control the width of the circular chart. The Spacing setting controls the space between each arcs. Finally, the Precision settings allow obtaining a more precise representation of candles, with lower values returning more precise results, however, more precision requires a higher amount of lines. Settings are quite hard to adjust, using a higher length might require a lower spacing value.

Additionally, the script includes two pointers indicating the location of the 75 (in blue) and 25 (in orange) percentiles. This allows obtaining an estimate of the current market sentiment, with the most recent arcs laying closer to the 75 percentile pointer indicating an up-trend.

This new way to represent candlesticks might be useful to more easily identify candles clusters or to find new price patterns. Who knows, we know that new ways to see prices always stimulate traders imagination.

See you next year.

Color█ OVERVIEW

This library is a Pine Script® programming tool for advanced color processing. It provides a comprehensive set of functions for specifying and analyzing colors in various color spaces, mixing and manipulating colors, calculating custom gradients and schemes, detecting contrast, and converting colors to or from hexadecimal strings.

█ CONCEPTS

Color

Color refers to how we interpret light of different wavelengths in the visible spectrum . The colors we see from an object represent the light wavelengths that it reflects, emits, or transmits toward our eyes. Some colors, such as blue and red, correspond directly to parts of the spectrum. Others, such as magenta, arise from a combination of wavelengths to which our minds assign a single color.

The human interpretation of color lends itself to many uses in our world. In the context of financial data analysis, the effective use of color helps transform raw data into insights that users can understand at a glance. For example, colors can categorize series, signal market conditions and sessions, and emphasize patterns or relationships in data.

Color models and spaces

A color model is a general mathematical framework that describes colors using sets of numbers. A color space is an implementation of a specific color model that defines an exact range (gamut) of reproducible colors based on a set of primary colors , a reference white point , and sometimes additional parameters such as viewing conditions.

There are numerous different color spaces — each describing the characteristics of color in unique ways. Different spaces carry different advantages, depending on the application. Below, we provide a brief overview of the concepts underlying the color spaces supported by this library.

RGB

RGB is one of the most well-known color models. It represents color as an additive mixture of three primary colors — red, green, and blue lights — with various intensities. Each cone cell in the human eye responds more strongly to one of the three primaries, and the average person interprets the combination of these lights as a distinct color (e.g., pure red + pure green = yellow).

The sRGB color space is the most common RGB implementation. Developed by HP and Microsoft in the 1990s, sRGB provided a standardized baseline for representing color across CRT monitors of the era, which produced brightness levels that did not increase linearly with the input signal. To match displays and optimize brightness encoding for human sensitivity, sRGB applied a nonlinear transformation to linear RGB signals, often referred to as gamma correction . The result produced more visually pleasing outputs while maintaining a simple encoding. As such, sRGB quickly became a standard for digital color representation across devices and the web. To this day, it remains the default color space for most web-based content.