Absolute Momentum (Time Series Momentum)Absolute momentum , also known as time series momentum , focuses on the trend of an asset's own past performance to predict its future performance. It involves analyzing an asset's own historical performance, rather than comparing it to other assets.

The strategy determines whether an asset's price is exhibiting an upward (positive momentum) or downward (negative momentum) trend by assessing the asset's return over a given period (standard look-back period: 12 months or approximately 250 trading days). Some studies recommend calculating momentum by deducting the corresponding Treasury bill rate from the measured performance.

Absolute Momentum Indicator

The Absolute Momentum Indicator displays the rolling 12-month performance (measured over 250 trading days) and plots it against a horizontal line representing 0%. If the indicator crosses above this line, it signifies positive absolute momentum, and conversely, crossing below indicates negative momentum. An additional, optional look-back period input field can be accessed through the settings.

Hint: This indicator is a simplified version, as some academic approaches measure absolute momentum by subtracting risk-free rates from the 12-month performance. However, even with higher rates, the values will still remain close to the 0% line.

Benefits of Absolute Momentum

Absolute momentum, which should not be confused with relative momentum or the momentum indicator, serves as a timing instrument for both individual assets and entire markets.

Gary Antonacci , a key contributor to the absolute momentum strategy (find study below), emphasizes its effectiveness in multi-asset portfolios and its importance in long-only investing. This is particularly evident in a) reducing downside volatility and b) mitigating behavioral biases.

Moskowitz, Ooi, and Pedersen document significant 'time series momentum' across various asset classes, including equity index, currency, commodity, and bond futures, in 58 liquid instruments (find study below). There's a notable persistence in returns ranging from one to 12 months, which tends to partially reverse over longer periods. This pattern aligns with sentiment theories suggesting initial under-reaction followed by delayed over-reaction.

Despite its surprising ease of implementation, the academic community has successfully measured the effects of absolute momentum across decades and in every major asset class, including stocks, bonds, commodities, and foreign exchange (FX).

Strategies for Implementing Absolute Momentum:

To Buy a Stock:

Select a Look-Back Period: Choose a historical period to analyze the stock's performance. A common period is 12 months, but this can vary based on your investment strategy.

Calculate Excess Return: Determine the stock's excess return over this period. You can also assume a risk-free rate of "0" to simplify the process.

Evaluate Momentum:

If the excess return is positive, it indicates positive absolute momentum. This suggests the stock is in an upward trend and could be a good buying opportunity.

If the excess return is negative, it suggests negative momentum, and you might want to delay buying.

Consider further conditions: Align your decision with broader market trends, economic indicators, or fundamental analysis, for additional context.

To Sell a Stock You Own:

Regularly Monitor Performance: Use the same look-back period as for buying (e.g., 12 months) to regularly assess the stock's performance.

Check for Negative Momentum: Calculate the excess return for the look-back period. Again, you can assume a risk-free rate of "0" to simplify the process. If the stock shows negative momentum, it might be time to consider selling.

Consider further conditions:Align your decision with broader market trends, economic indicators, or fundamental analysis, for additional context.

Important note: Note: Entering a position (i.e., buying) based on positive absolute momentum doesn't necessarily mean you must sell it if it later exhibits negative absolute momentum. You can initiate a position using positive absolute momentum as an entry indicator and then continue holding it based on other criteria, such as fundamental analysis.

General Tips:

Reassessment Frequency: Decide how often you will reassess the momentum (monthly, quarterly, etc.).

Remember, while absolute momentum provides a systematic approach, it's recommendable to consider it as part of a broader investment strategy that includes diversification, risk management, fundamental analysis, etc.

Relevant Capital Market Studies:

Antonacci, Gary. "Absolute momentum: A simple rule-based strategy and universal trend-following overlay." Available at SSRN 2244633 (2013)

Moskowitz, Tobias J., Yao Hua Ooi, and Lasse Heje Pedersen. "Time series momentum." Journal of financial economics 104.2 (2012): 228-250

Recherche dans les scripts pour "12月4号是什么星座"

S&P 500 Quandl Data & RatiosTradingView has a little-known integration that allows you to pull in 3rd party data-sets from Nasdaq Data Link, also known as Quandl. Today, I am open-sourcing for the community an indicator that uses the Quandl integration to pull in historical data and ratios on the S&P500. I originally coded this to study macro P/E ratios during peaks and troughs of boom/bust cycles.

The indicator pulls in each of the following datasets, as defined and provided by Quandl. The user can select which datasets to pull in using the indicator settings:

Dividend Yield : S&P 500 dividend yield (12 month dividend per share)/price. Yields following June 2022 (including the current yield) are estimated based on 12 month dividends through June 2022, as reported by S&P. Sources: Standard & Poor's for current S&P 500 Dividend Yield. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Dividend Yields.

Price Earning Ratio : Price to earnings ratio, based on trailing twelve month as reported earnings. Current PE is estimated from latest reported earnings and current market price. Source: Robert Shiller and his book Irrational Exuberance for historic S&P 500 PE Ratio.

CAPE/Shiller PE Ratio : Shiller PE ratio for the S&P 500. Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio), Shiller PE Ratio, or PE 10 FAQ. Data courtesy of Robert Shiller from his book, Irrational Exuberance.

Earnings Yield : S&P 500 Earnings Yield. Earnings Yield = trailing 12 month earnings divided by index price (or inverse PE) Yields following March, 2022 (including current yield) are estimated based on 12 month earnings through March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Book Ratio : S&P 500 price to book value ratio. Current price to book ratio is estimated based on current market price and S&P 500 book value as of March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Sales Ratio : S&P 500 Price to Sales Ratio (P/S or Price to Revenue). Current price to sales ratio is estimated based on current market price and 12 month sales ending March, 2022 the latest reported by S&P. Source: Standard & Poor's

Inflation Adjusted SP500 : Inflation adjusted SP500. Other than the current price, all prices are monthly average closing prices. Sources: Standard & Poor's Robert Shiller and his book Irrational Exuberance for historic S&P 500 prices, and historic CPIs.

Revenue Per Share : Trailing twelve month S&P 500 Sales Per Share (S&P 500 Revenue Per Share) non-inflation adjusted current dollars. Source: Standard & Poor's

Earnings Per Share : S&P 500 Earnings Per Share. 12-month real earnings per share inflation adjusted, constant August, 2022 dollars. Sources: Standard & Poor's for current S&P 500 Earnings. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Earnings.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Argo II - (alerts for 3commas composite bots) - publicThis script lets users create BUY/SELL alerts for 3commas composite bots (1 alert = 12 pairs) in a simple way, based on a built in set of indicators that can be tweaked to work together or alone through the study settings.

There is a version of this script for single pair bots, with slightly more features here .

If the user choses to create both BUY and SELL signals from the study settings, the (1) alert created will send both BUY and SELL signals for all 12 pairs selected. At this stage, the script forces the user to select 12 pairs in the study settings. If less pairs are inserted, it will not work. Also, the script will only send alerts for the pairs selected in the study settings, not for the current chart (if different).

How to use:

- Add the script to the current chart

- Open the study settings , insert bot details and select 12 pairs. You should write the pairs manually, using the format BTC , ADA, ETH, etc. They MUST be in capital letters or 3commas will not recognize them.

- Still in the study settings, tweak the deal start/close conditions from various indicators until happy. The study will plot the entry / exit points below the current chart (1 = buy, 2 = sell)

- Make sure your strategy works for all the pairs you have selected, simply by checking each chart with the same study settings

- When happy, right click on the "..." next to the study name, then "Add alert'".

- Under "Condition", on the second line, chose "Any alert () function call". Add the webhook from 3commas, give it a name, and "create".

That's it.

Notes:

- If you insert coins that are not available for the quote currency and exchange of your choosing, the script will not work and return an error.

- Make sure you run tests with paper trading or dummy bots (i.e without actual bot ID) to ensure your alerts trigger as intended on all coins.

- If alerts trigger too much (i.e they all trigger at the same time for all coins), Trading View will stop the alert. So probably not ideal for a scalping bot. It could also be the sign the script doesn't work as intended.

- The script is a bit slow on my side. I am a beginner in pinescript, so if anyone knows how to simplify it, please let me know.

- if anyone knows how to tell the script to function with less than 12 pairs (when not filling the 12 fields in the setting), please also let me know :)

XPloRR MA-Buy ATR-Trailing-Stop Long Term Strategy Beating B&HXPloRR MA-Buy ATR-MA-Trailing-Stop Strategy

Long term MA Trailing Stop strategy to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the EMA(blue) crossing over the SMA curve(orange).

My sell strategy is triggered by another EMA(lime) of the close value crossing the trailing stop(green) value.

The trailing stop value(green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between high and low values.

Every stock has it's own "DNA", so first thing to do is find the right parameters to get the best strategy values voor EMA, SMA and Trailing Stop.

Then keep using these parameter for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Here are the parameters:

Exponential MA: buy trigger when crossing over the SMA value (use values between 11-50)

Simple MA: buy trigger when EMA crosses over the SMA value (use values between 20 and 200)

Stop EMA: sell trigger when Stop EMA of close value crosses under the trailing stop value (use values between 8 and 16)

Trailing Stop #ATR: defines the trailing stop value as a multiple of the ATR(15) value

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now):

BAR(Barco): EMA=11, SMA=82, StopEMA=12, Stop#ATR=9

Buy&HoldProfit: 45.82%, NetProfit: 294.7%, #Trades:8, %Profit:62.5%, ProfitFactor: 12.539

AAPL(Apple): EMA=12, SMA=45, StopEMA=12, Stop#ATR=6

Buy&HoldProfit: 2925.86%, NetProfit: 4035.92%, #Trades:10, %Profit:60%, ProfitFactor: 6.36

BEKB(Bekaert): EMA=12, SMA=42, StopEMA=12, Stop#ATR=7

Buy&HoldProfit: 81.11%, NetProfit: 521.37%, #Trades:10, %Profit:60%, ProfitFactor: 2.617

SOLB(Solvay): EMA=12, SMA=63, StopEMA=11, Stop#ATR=8

Buy&HoldProfit: 43.61%, NetProfit: 151.4%, #Trades:8, %Profit:75%, ProfitFactor: 3.794

PHIA(Philips): EMA=11, SMA=80, StopEMA=8, Stop#ATR=10

Buy&HoldProfit: 56.79%, NetProfit: 198.46%, #Trades:6, %Profit:83.33%, ProfitFactor: 23.07

I am very curious to see the parameters for your stocks and please make suggestions to improve this strategy.

Quantum Rotational Field MappingQuantum Rotational Field Mapping (QRFM):

Phase Coherence Detection Through Complex-Plane Oscillator Analysis

Quantum Rotational Field Mapping applies complex-plane mathematics and phase-space analysis to oscillator ensembles, identifying high-probability trend ignition points by measuring when multiple independent oscillators achieve phase coherence. Unlike traditional multi-oscillator approaches that simply stack indicators or use boolean AND/OR logic, this system converts each oscillator into a rotating phasor (vector) in the complex plane and calculates the Coherence Index (CI) —a mathematical measure of how tightly aligned the ensemble has become—then generates signals only when alignment, phase direction, and pairwise entanglement all converge.

The indicator combines three mathematical frameworks: phasor representation using analytic signal theory to extract phase and amplitude from each oscillator, coherence measurement using vector summation in the complex plane to quantify group alignment, and entanglement analysis that calculates pairwise phase agreement across all oscillator combinations. This creates a multi-dimensional confirmation system that distinguishes between random oscillator noise and genuine regime transitions.

What Makes This Original

Complex-Plane Phasor Framework

This indicator implements classical signal processing mathematics adapted for market oscillators. Each oscillator—whether RSI, MACD, Stochastic, CCI, Williams %R, MFI, ROC, or TSI—is first normalized to a common scale, then converted into a complex-plane representation using an in-phase (I) and quadrature (Q) component. The in-phase component is the oscillator value itself, while the quadrature component is calculated as the first difference (derivative proxy), creating a velocity-aware representation.

From these components, the system extracts:

Phase (φ) : Calculated as φ = atan2(Q, I), representing the oscillator's position in its cycle (mapped to -180° to +180°)

Amplitude (A) : Calculated as A = √(I² + Q²), representing the oscillator's strength or conviction

This mathematical approach is fundamentally different from simply reading oscillator values. A phasor captures both where an oscillator is in its cycle (phase angle) and how strongly it's expressing that position (amplitude). Two oscillators can have the same value but be in opposite phases of their cycles—traditional analysis would see them as identical, while QRFM sees them as 180° out of phase (contradictory).

Coherence Index Calculation

The core innovation is the Coherence Index (CI) , borrowed from physics and signal processing. When you have N oscillators, each with phase φₙ, you can represent each as a unit vector in the complex plane: e^(iφₙ) = cos(φₙ) + i·sin(φₙ).

The CI measures what happens when you sum all these vectors:

Resultant Vector : R = Σ e^(iφₙ) = Σ cos(φₙ) + i·Σ sin(φₙ)

Coherence Index : CI = |R| / N

Where |R| is the magnitude of the resultant vector and N is the number of active oscillators.

The CI ranges from 0 to 1:

CI = 1.0 : Perfect coherence—all oscillators have identical phase angles, vectors point in the same direction, creating maximum constructive interference

CI = 0.0 : Complete decoherence—oscillators are randomly distributed around the circle, vectors cancel out through destructive interference

0 < CI < 1 : Partial alignment—some clustering with some scatter

This is not a simple average or correlation. The CI captures phase synchronization across the entire ensemble simultaneously. When oscillators phase-lock (align their cycles), the CI spikes regardless of their individual values. This makes it sensitive to regime transitions that traditional indicators miss.

Dominant Phase and Direction Detection

Beyond measuring alignment strength, the system calculates the dominant phase of the ensemble—the direction the resultant vector points:

Dominant Phase : φ_dom = atan2(Σ sin(φₙ), Σ cos(φₙ))

This gives the "average direction" of all oscillator phases, mapped to -180° to +180°:

+90° to -90° (right half-plane): Bullish phase dominance

+90° to +180° or -90° to -180° (left half-plane): Bearish phase dominance

The combination of CI magnitude (coherence strength) and dominant phase angle (directional bias) creates a two-dimensional signal space. High CI alone is insufficient—you need high CI plus dominant phase pointing in a tradeable direction. This dual requirement is what separates QRFM from simple oscillator averaging.

Entanglement Matrix and Pairwise Coherence

While the CI measures global alignment, the entanglement matrix measures local pairwise relationships. For every pair of oscillators (i, j), the system calculates:

E(i,j) = |cos(φᵢ - φⱼ)|

This represents the phase agreement between oscillators i and j:

E = 1.0 : Oscillators are in-phase (0° or 360° apart)

E = 0.0 : Oscillators are in quadrature (90° apart, orthogonal)

E between 0 and 1 : Varying degrees of alignment

The system counts how many oscillator pairs exceed a user-defined entanglement threshold (e.g., 0.7). This entangled pairs count serves as a confirmation filter: signals require not just high global CI, but also a minimum number of strong pairwise agreements. This prevents false ignitions where CI is high but driven by only two oscillators while the rest remain scattered.

The entanglement matrix creates an N×N symmetric matrix that can be visualized as a web—when many cells are bright (high E values), the ensemble is highly interconnected. When cells are dark, oscillators are moving independently.

Phase-Lock Tolerance Mechanism

A complementary confirmation layer is the phase-lock detector . This calculates the maximum phase spread across all oscillators:

For all pairs (i,j), compute angular distance: Δφ = |φᵢ - φⱼ|, wrapping at 180°

Max Spread = maximum Δφ across all pairs

If max spread < user threshold (e.g., 35°), the ensemble is considered phase-locked —all oscillators are within a narrow angular band.

This differs from entanglement: entanglement measures pairwise cosine similarity (magnitude of alignment), while phase-lock measures maximum angular deviation (tightness of clustering). Both must be satisfied for the highest-conviction signals.

Multi-Layer Visual Architecture

QRFM includes six visual components that represent the same underlying mathematics from different perspectives:

Circular Orbit Plot : A polar coordinate grid showing each oscillator as a vector from origin to perimeter. Angle = phase, radius = amplitude. This is a real-time snapshot of the complex plane. When vectors converge (point in similar directions), coherence is high. When scattered randomly, coherence is low. Users can see phase alignment forming before CI numerically confirms it.

Phase-Time Heat Map : A 2D matrix with rows = oscillators and columns = time bins. Each cell is colored by the oscillator's phase at that time (using a gradient where color hue maps to angle). Horizontal color bands indicate sustained phase alignment over time. Vertical color bands show moments when all oscillators shared the same phase (ignition points). This provides historical pattern recognition.

Entanglement Web Matrix : An N×N grid showing E(i,j) for all pairs. Cells are colored by entanglement strength—bright yellow/gold for high E, dark gray for low E. This reveals which oscillators are driving coherence and which are lagging. For example, if RSI and MACD show high E but Stochastic shows low E with everything, Stochastic is the outlier.

Quantum Field Cloud : A background color overlay on the price chart. Color (green = bullish, red = bearish) is determined by dominant phase. Opacity is determined by CI—high CI creates dense, opaque cloud; low CI creates faint, nearly invisible cloud. This gives an atmospheric "feel" for regime strength without looking at numbers.

Phase Spiral : A smoothed plot of dominant phase over recent history, displayed as a curve that wraps around price. When the spiral is tight and rotating steadily, the ensemble is in coherent rotation (trending). When the spiral is loose or erratic, coherence is breaking down.

Dashboard : A table showing real-time metrics: CI (as percentage), dominant phase (in degrees with directional arrow), field strength (CI × average amplitude), entangled pairs count, phase-lock status (locked/unlocked), quantum state classification ("Ignition", "Coherent", "Collapse", "Chaos"), and collapse risk (recent CI change normalized to 0-100%).

Each component is independently toggleable, allowing users to customize their workspace. The orbit plot is the most essential—it provides intuitive, visual feedback on phase alignment that no numerical dashboard can match.

Core Components and How They Work Together

1. Oscillator Normalization Engine

The foundation is creating a common measurement scale. QRFM supports eight oscillators:

RSI : Normalized from to using overbought/oversold levels (70, 30) as anchors

MACD Histogram : Normalized by dividing by rolling standard deviation, then clamped to

Stochastic %K : Normalized from using (80, 20) anchors

CCI : Divided by 200 (typical extreme level), clamped to

Williams %R : Normalized from using (-20, -80) anchors

MFI : Normalized from using (80, 20) anchors

ROC : Divided by 10, clamped to

TSI : Divided by 50, clamped to

Each oscillator can be individually enabled/disabled. Only active oscillators contribute to phase calculations. The normalization removes scale differences—a reading of +0.8 means "strongly bullish" regardless of whether it came from RSI or TSI.

2. Analytic Signal Construction

For each active oscillator at each bar, the system constructs the analytic signal:

In-Phase (I) : The normalized oscillator value itself

Quadrature (Q) : The bar-to-bar change in the normalized value (first derivative approximation)

This creates a 2D representation: (I, Q). The phase is extracted as:

φ = atan2(Q, I) × (180 / π)

This maps the oscillator to a point on the unit circle. An oscillator at the same value but rising (positive Q) will have a different phase than one that is falling (negative Q). This velocity-awareness is critical—it distinguishes between "at resistance and stalling" versus "at resistance and breaking through."

The amplitude is extracted as:

A = √(I² + Q²)

This represents the distance from origin in the (I, Q) plane. High amplitude means the oscillator is far from neutral (strong conviction). Low amplitude means it's near zero (weak/transitional state).

3. Coherence Calculation Pipeline

For each bar (or every Nth bar if phase sample rate > 1 for performance):

Step 1 : Extract phase φₙ for each of the N active oscillators

Step 2 : Compute complex exponentials: Zₙ = e^(i·φₙ·π/180) = cos(φₙ·π/180) + i·sin(φₙ·π/180)

Step 3 : Sum the complex exponentials: R = Σ Zₙ = (Σ cos φₙ) + i·(Σ sin φₙ)

Step 4 : Calculate magnitude: |R| = √

Step 5 : Normalize by count: CI_raw = |R| / N

Step 6 : Smooth the CI: CI = SMA(CI_raw, smoothing_window)

The smoothing step (default 2 bars) removes single-bar noise spikes while preserving structural coherence changes. Users can adjust this to control reactivity versus stability.

The dominant phase is calculated as:

φ_dom = atan2(Σ sin φₙ, Σ cos φₙ) × (180 / π)

This is the angle of the resultant vector R in the complex plane.

4. Entanglement Matrix Construction

For all unique pairs of oscillators (i, j) where i < j:

Step 1 : Get phases φᵢ and φⱼ

Step 2 : Compute phase difference: Δφ = φᵢ - φⱼ (in radians)

Step 3 : Calculate entanglement: E(i,j) = |cos(Δφ)|

Step 4 : Store in symmetric matrix: matrix = matrix = E(i,j)

The matrix is then scanned: count how many E(i,j) values exceed the user-defined threshold (default 0.7). This count is the entangled pairs metric.

For visualization, the matrix is rendered as an N×N table where cell brightness maps to E(i,j) intensity.

5. Phase-Lock Detection

Step 1 : For all unique pairs (i, j), compute angular distance: Δφ = |φᵢ - φⱼ|

Step 2 : Wrap angles: if Δφ > 180°, set Δφ = 360° - Δφ

Step 3 : Find maximum: max_spread = max(Δφ) across all pairs

Step 4 : Compare to tolerance: phase_locked = (max_spread < tolerance)

If phase_locked is true, all oscillators are within the specified angular cone (e.g., 35°). This is a boolean confirmation filter.

6. Signal Generation Logic

Signals are generated through multi-layer confirmation:

Long Ignition Signal :

CI crosses above ignition threshold (e.g., 0.80)

AND dominant phase is in bullish range (-90° < φ_dom < +90°)

AND phase_locked = true

AND entangled_pairs >= minimum threshold (e.g., 4)

Short Ignition Signal :

CI crosses above ignition threshold

AND dominant phase is in bearish range (φ_dom < -90° OR φ_dom > +90°)

AND phase_locked = true

AND entangled_pairs >= minimum threshold

Collapse Signal :

CI at bar minus CI at current bar > collapse threshold (e.g., 0.55)

AND CI at bar was above 0.6 (must collapse from coherent state, not from already-low state)

These are strict conditions. A high CI alone does not generate a signal—dominant phase must align with direction, oscillators must be phase-locked, and sufficient pairwise entanglement must exist. This multi-factor gating dramatically reduces false signals compared to single-condition triggers.

Calculation Methodology

Phase 1: Oscillator Computation and Normalization

On each bar, the system calculates the raw values for all enabled oscillators using standard Pine Script functions:

RSI: ta.rsi(close, length)

MACD: ta.macd() returning histogram component

Stochastic: ta.stoch() smoothed with ta.sma()

CCI: ta.cci(close, length)

Williams %R: ta.wpr(length)

MFI: ta.mfi(hlc3, length)

ROC: ta.roc(close, length)

TSI: ta.tsi(close, short, long)

Each raw value is then passed through a normalization function:

normalize(value, overbought_level, oversold_level) = 2 × (value - oversold) / (overbought - oversold) - 1

This maps the oscillator's typical range to , where -1 represents extreme bearish, 0 represents neutral, and +1 represents extreme bullish.

For oscillators without fixed ranges (MACD, ROC, TSI), statistical normalization is used: divide by a rolling standard deviation or fixed divisor, then clamp to .

Phase 2: Phasor Extraction

For each normalized oscillator value val:

I = val (in-phase component)

Q = val - val (quadrature component, first difference)

Phase calculation:

phi_rad = atan2(Q, I)

phi_deg = phi_rad × (180 / π)

Amplitude calculation:

A = √(I² + Q²)

These values are stored in arrays: osc_phases and osc_amps for each oscillator n.

Phase 3: Complex Summation and Coherence

Initialize accumulators:

sum_cos = 0

sum_sin = 0

For each oscillator n = 0 to N-1:

phi_rad = osc_phases × (π / 180)

sum_cos += cos(phi_rad)

sum_sin += sin(phi_rad)

Resultant magnitude:

resultant_mag = √(sum_cos² + sum_sin²)

Coherence Index (raw):

CI_raw = resultant_mag / N

Smoothed CI:

CI = SMA(CI_raw, smoothing_window)

Dominant phase:

phi_dom_rad = atan2(sum_sin, sum_cos)

phi_dom_deg = phi_dom_rad × (180 / π)

Phase 4: Entanglement Matrix Population

For i = 0 to N-2:

For j = i+1 to N-1:

phi_i = osc_phases × (π / 180)

phi_j = osc_phases × (π / 180)

delta_phi = phi_i - phi_j

E = |cos(delta_phi)|

matrix_index_ij = i × N + j

matrix_index_ji = j × N + i

entangle_matrix = E

entangle_matrix = E

if E >= threshold:

entangled_pairs += 1

The matrix uses flat array storage with index mapping: index(row, col) = row × N + col.

Phase 5: Phase-Lock Check

max_spread = 0

For i = 0 to N-2:

For j = i+1 to N-1:

delta = |osc_phases - osc_phases |

if delta > 180:

delta = 360 - delta

max_spread = max(max_spread, delta)

phase_locked = (max_spread < tolerance)

Phase 6: Signal Evaluation

Ignition Long :

ignition_long = (CI crosses above threshold) AND

(phi_dom > -90 AND phi_dom < 90) AND

phase_locked AND

(entangled_pairs >= minimum)

Ignition Short :

ignition_short = (CI crosses above threshold) AND

(phi_dom < -90 OR phi_dom > 90) AND

phase_locked AND

(entangled_pairs >= minimum)

Collapse :

CI_prev = CI

collapse = (CI_prev - CI > collapse_threshold) AND (CI_prev > 0.6)

All signals are evaluated on bar close. The crossover and crossunder functions ensure signals fire only once when conditions transition from false to true.

Phase 7: Field Strength and Visualization Metrics

Average Amplitude :

avg_amp = (Σ osc_amps ) / N

Field Strength :

field_strength = CI × avg_amp

Collapse Risk (for dashboard):

collapse_risk = (CI - CI) / max(CI , 0.1)

collapse_risk_pct = clamp(collapse_risk × 100, 0, 100)

Quantum State Classification :

if (CI > threshold AND phase_locked):

state = "Ignition"

else if (CI > 0.6):

state = "Coherent"

else if (collapse):

state = "Collapse"

else:

state = "Chaos"

Phase 8: Visual Rendering

Orbit Plot : For each oscillator, convert polar (phase, amplitude) to Cartesian (x, y) for grid placement:

radius = amplitude × grid_center × 0.8

x = radius × cos(phase × π/180)

y = radius × sin(phase × π/180)

col = center + x (mapped to grid coordinates)

row = center - y

Heat Map : For each oscillator row and time column, retrieve historical phase value at lookback = (columns - col) × sample_rate, then map phase to color using a hue gradient.

Entanglement Web : Render matrix as table cell with background color opacity = E(i,j).

Field Cloud : Background color = (phi_dom > -90 AND phi_dom < 90) ? green : red, with opacity = mix(min_opacity, max_opacity, CI).

All visual components render only on the last bar (barstate.islast) to minimize computational overhead.

How to Use This Indicator

Step 1 : Apply QRFM to your chart. It works on all timeframes and asset classes, though 15-minute to 4-hour timeframes provide the best balance of responsiveness and noise reduction.

Step 2 : Enable the dashboard (default: top right) and the circular orbit plot (default: middle left). These are your primary visual feedback tools.

Step 3 : Optionally enable the heat map, entanglement web, and field cloud based on your preference. New users may find all visuals overwhelming; start with dashboard + orbit plot.

Step 4 : Observe for 50-100 bars to let the indicator establish baseline coherence patterns. Markets have different "normal" CI ranges—some instruments naturally run higher or lower coherence.

Understanding the Circular Orbit Plot

The orbit plot is a polar grid showing oscillator vectors in real-time:

Center point : Neutral (zero phase and amplitude)

Each vector : A line from center to a point on the grid

Vector angle : The oscillator's phase (0° = right/east, 90° = up/north, 180° = left/west, -90° = down/south)

Vector length : The oscillator's amplitude (short = weak signal, long = strong signal)

Vector label : First letter of oscillator name (R = RSI, M = MACD, etc.)

What to watch :

Convergence : When all vectors cluster in one quadrant or sector, CI is rising and coherence is forming. This is your pre-signal warning.

Scatter : When vectors point in random directions (360° spread), CI is low and the market is in a non-trending or transitional regime.

Rotation : When the cluster rotates smoothly around the circle, the ensemble is in coherent oscillation—typically seen during steady trends.

Sudden flips : When the cluster rapidly jumps from one side to the opposite (e.g., +90° to -90°), a phase reversal has occurred—often coinciding with trend reversals.

Example: If you see RSI, MACD, and Stochastic all pointing toward 45° (northeast) with long vectors, while CCI, TSI, and ROC point toward 40-50° as well, coherence is high and dominant phase is bullish. Expect an ignition signal if CI crosses threshold.

Reading Dashboard Metrics

The dashboard provides numerical confirmation of what the orbit plot shows visually:

CI : Displays as 0-100%. Above 70% = high coherence (strong regime), 40-70% = moderate, below 40% = low (poor conditions for trend entries).

Dom Phase : Angle in degrees with directional arrow. ⬆ = bullish bias, ⬇ = bearish bias, ⬌ = neutral.

Field Strength : CI weighted by amplitude. High values (> 0.6) indicate not just alignment but strong alignment.

Entangled Pairs : Count of oscillator pairs with E > threshold. Higher = more confirmation. If minimum is set to 4, you need at least 4 pairs entangled for signals.

Phase Lock : 🔒 YES (all oscillators within tolerance) or 🔓 NO (spread too wide).

State : Real-time classification:

🚀 IGNITION: CI just crossed threshold with phase-lock

⚡ COHERENT: CI is high and stable

💥 COLLAPSE: CI has dropped sharply

🌀 CHAOS: Low CI, scattered phases

Collapse Risk : 0-100% scale based on recent CI change. Above 50% warns of imminent breakdown.

Interpreting Signals

Long Ignition (Blue Triangle Below Price) :

Occurs when CI crosses above threshold (e.g., 0.80)

Dominant phase is in bullish range (-90° to +90°)

All oscillators are phase-locked (within tolerance)

Minimum entangled pairs requirement met

Interpretation : The oscillator ensemble has transitioned from disorder to coherent bullish alignment. This is a high-probability long entry point. The multi-layer confirmation (CI + phase direction + lock + entanglement) ensures this is not a single-oscillator whipsaw.

Short Ignition (Red Triangle Above Price) :

Same conditions as long, but dominant phase is in bearish range (< -90° or > +90°)

Interpretation : Coherent bearish alignment has formed. High-probability short entry.

Collapse (Circles Above and Below Price) :

CI has dropped by more than the collapse threshold (e.g., 0.55) over a 5-bar window

CI was previously above 0.6 (collapsing from coherent state)

Interpretation : Phase coherence has broken down. If you are in a position, this is an exit warning. If looking to enter, stand aside—regime is transitioning.

Phase-Time Heat Map Patterns

Enable the heat map and position it at bottom right. The rows represent individual oscillators, columns represent time bins (most recent on left).

Pattern: Horizontal Color Bands

If a row (e.g., RSI) shows consistent color across columns (say, green for several bins), that oscillator has maintained stable phase over time. If all rows show horizontal bands of similar color, the entire ensemble has been phase-locked for an extended period—this is a strong trending regime.

Pattern: Vertical Color Bands

If a column (single time bin) shows all cells with the same or very similar color, that moment in time had high coherence. These vertical bands often align with ignition signals or major price pivots.

Pattern: Rainbow Chaos

If cells are random colors (red, green, yellow mixed with no pattern), coherence is low. The ensemble is scattered. Avoid trading during these periods unless you have external confirmation.

Pattern: Color Transition

If you see a row transition from red to green (or vice versa) sharply, that oscillator has phase-flipped. If multiple rows do this simultaneously, a regime change is underway.

Entanglement Web Analysis

Enable the web matrix (default: opposite corner from heat map). It shows an N×N grid where N = number of active oscillators.

Bright Yellow/Gold Cells : High pairwise entanglement. For example, if the RSI-MACD cell is bright gold, those two oscillators are moving in phase. If the RSI-Stochastic cell is bright, they are entangled as well.

Dark Gray Cells : Low entanglement. Oscillators are decorrelated or in quadrature.

Diagonal : Always marked with "—" because an oscillator is always perfectly entangled with itself.

How to use :

Scan for clustering: If most cells are bright, coherence is high across the board. If only a few cells are bright, coherence is driven by a subset (e.g., RSI and MACD are aligned, but nothing else is—weak signal).

Identify laggards: If one row/column is entirely dark, that oscillator is the outlier. You may choose to disable it or monitor for when it joins the group (late confirmation).

Watch for web formation: During low-coherence periods, the matrix is mostly dark. As coherence builds, cells begin lighting up. A sudden "web" of connections forming visually precedes ignition signals.

Trading Workflow

Step 1: Monitor Coherence Level

Check the dashboard CI metric or observe the orbit plot. If CI is below 40% and vectors are scattered, conditions are poor for trend entries. Wait.

Step 2: Detect Coherence Building

When CI begins rising (say, from 30% to 50-60%) and you notice vectors on the orbit plot starting to cluster, coherence is forming. This is your alert phase—do not enter yet, but prepare.

Step 3: Confirm Phase Direction

Check the dominant phase angle and the orbit plot quadrant where clustering is occurring:

Clustering in right half (0° to ±90°): Bullish bias forming

Clustering in left half (±90° to 180°): Bearish bias forming

Verify the dashboard shows the corresponding directional arrow (⬆ or ⬇).

Step 4: Wait for Signal Confirmation

Do not enter based on rising CI alone. Wait for the full ignition signal:

CI crosses above threshold

Phase-lock indicator shows 🔒 YES

Entangled pairs count >= minimum

Directional triangle appears on chart

This ensures all layers have aligned.

Step 5: Execute Entry

Long : Blue triangle below price appears → enter long

Short : Red triangle above price appears → enter short

Step 6: Position Management

Initial Stop : Place stop loss based on your risk management rules (e.g., recent swing low/high, ATR-based buffer).

Monitoring :

Watch the field cloud density. If it remains opaque and colored in your direction, the regime is intact.

Check dashboard collapse risk. If it rises above 50%, prepare for exit.

Monitor the orbit plot. If vectors begin scattering or the cluster flips to the opposite side, coherence is breaking.

Exit Triggers :

Collapse signal fires (circles appear)

Dominant phase flips to opposite half-plane

CI drops below 40% (coherence lost)

Price hits your profit target or trailing stop

Step 7: Post-Exit Analysis

After exiting, observe whether a new ignition forms in the opposite direction (reversal) or if CI remains low (transition to range). Use this to decide whether to re-enter, reverse, or stand aside.

Best Practices

Use Price Structure as Context

QRFM identifies when coherence forms but does not specify where price will go. Combine ignition signals with support/resistance levels, trendlines, or chart patterns. For example:

Long ignition near a major support level after a pullback: high-probability bounce

Long ignition in the middle of a range with no structure: lower probability

Multi-Timeframe Confirmation

Open QRFM on two timeframes simultaneously:

Higher timeframe (e.g., 4-hour): Use CI level to determine regime bias. If 4H CI is above 60% and dominant phase is bullish, the market is in a bullish regime.

Lower timeframe (e.g., 15-minute): Execute entries on ignition signals that align with the higher timeframe bias.

This prevents counter-trend trades and increases win rate.

Distinguish Between Regime Types

High CI, stable dominant phase (State: Coherent) : Trending market. Ignitions are continuation signals; collapses are profit-taking or reversal warnings.

Low CI, erratic dominant phase (State: Chaos) : Ranging or choppy market. Avoid ignition signals or reduce position size. Wait for coherence to establish.

Moderate CI with frequent collapses : Whipsaw environment. Use wider stops or stand aside.

Adjust Parameters to Instrument and Timeframe

Crypto/Forex (high volatility) : Lower ignition threshold (0.65-0.75), lower CI smoothing (2-3), shorter oscillator lengths (7-10).

Stocks/Indices (moderate volatility) : Standard settings (threshold 0.75-0.85, smoothing 5-7, oscillator lengths 14).

Lower timeframes (5-15 min) : Reduce phase sample rate to 1-2 for responsiveness.

Higher timeframes (daily+) : Increase CI smoothing and oscillator lengths for noise reduction.

Use Entanglement Count as Conviction Filter

The minimum entangled pairs setting controls signal strictness:

Low (1-2) : More signals, lower quality (acceptable if you have other confirmation)

Medium (3-5) : Balanced (recommended for most traders)

High (6+) : Very strict, fewer signals, highest quality

Adjust based on your trade frequency preference and risk tolerance.

Monitor Oscillator Contribution

Use the entanglement web to see which oscillators are driving coherence. If certain oscillators are consistently dark (low E with all others), they may be adding noise. Consider disabling them. For example:

On low-volume instruments, MFI may be unreliable → disable MFI

On strongly trending instruments, mean-reversion oscillators (Stochastic, RSI) may lag → reduce weight or disable

Respect the Collapse Signal

Collapse events are early warnings. Price may continue in the original direction for several bars after collapse fires, but the underlying regime has weakened. Best practice:

If in profit: Take partial or full profit on collapse

If at breakeven/small loss: Exit immediately

If collapse occurs shortly after entry: Likely a false ignition; exit to avoid drawdown

Collapses do not guarantee immediate reversals—they signal uncertainty .

Combine with Volume Analysis

If your instrument has reliable volume:

Ignitions with expanding volume: Higher conviction

Ignitions with declining volume: Weaker, possibly false

Collapses with volume spikes: Strong reversal signal

Collapses with low volume: May just be consolidation

Volume is not built into QRFM (except via MFI), so add it as external confirmation.

Observe the Phase Spiral

The spiral provides a quick visual cue for rotation consistency:

Tight, smooth spiral : Ensemble is rotating coherently (trending)

Loose, erratic spiral : Phase is jumping around (ranging or transitional)

If the spiral tightens, coherence is building. If it loosens, coherence is dissolving.

Do Not Overtrade Low-Coherence Periods

When CI is persistently below 40% and the state is "Chaos," the market is not in a regime where phase analysis is predictive. During these times:

Reduce position size

Widen stops

Wait for coherence to return

QRFM's strength is regime detection. If there is no regime, the tool correctly signals "stand aside."

Use Alerts Strategically

Set alerts for:

Long Ignition

Short Ignition

Collapse

Phase Lock (optional)

Configure alerts to "Once per bar close" to avoid intrabar repainting and noise. When an alert fires, manually verify:

Orbit plot shows clustering

Dashboard confirms all conditions

Price structure supports the trade

Do not blindly trade alerts—use them as prompts for analysis.

Ideal Market Conditions

Best Performance

Instruments :

Liquid, actively traded markets (major forex pairs, large-cap stocks, major indices, top-tier crypto)

Instruments with clear cyclical oscillator behavior (avoid extremely illiquid or manipulated markets)

Timeframes :

15-minute to 4-hour: Optimal balance of noise reduction and responsiveness

1-hour to daily: Slower, higher-conviction signals; good for swing trading

5-minute: Acceptable for scalping if parameters are tightened and you accept more noise

Market Regimes :

Trending markets with periodic retracements (where oscillators cycle through phases predictably)

Breakout environments (coherence forms before/during breakout; collapse occurs at exhaustion)

Rotational markets with clear swings (oscillators phase-lock at turning points)

Volatility :

Moderate to high volatility (oscillators have room to move through their ranges)

Stable volatility regimes (sudden VIX spikes or flash crashes may create false collapses)

Challenging Conditions

Instruments :

Very low liquidity markets (erratic price action creates unstable oscillator phases)

Heavily news-driven instruments (fundamentals may override technical coherence)

Highly correlated instruments (oscillators may all reflect the same underlying factor, reducing independence)

Market Regimes :

Deep, prolonged consolidation (oscillators remain near neutral, CI is chronically low, few signals fire)

Extreme chop with no directional bias (oscillators whipsaw, coherence never establishes)

Gap-driven markets (large overnight gaps create phase discontinuities)

Timeframes :

Sub-5-minute charts: Noise dominates; oscillators flip rapidly; coherence is fleeting and unreliable

Weekly/monthly: Oscillators move extremely slowly; signals are rare; better suited for long-term positioning than active trading

Special Cases :

During major economic releases or earnings: Oscillators may lag price or become decorrelated as fundamentals overwhelm technicals. Reduce position size or stand aside.

In extremely low-volatility environments (e.g., holiday periods): Oscillators compress to neutral, CI may be artificially high due to lack of movement, but signals lack follow-through.

Adaptive Behavior

QRFM is designed to self-adapt to poor conditions:

When coherence is genuinely absent, CI remains low and signals do not fire

When only a subset of oscillators aligns, entangled pairs count stays below threshold and signals are filtered out

When phase-lock cannot be achieved (oscillators too scattered), the lock filter prevents signals

This means the indicator will naturally produce fewer (or zero) signals during unfavorable conditions, rather than generating false signals. This is a feature —it keeps you out of low-probability trades.

Parameter Optimization by Trading Style

Scalping (5-15 Minute Charts)

Goal : Maximum responsiveness, accept higher noise

Oscillator Lengths :

RSI: 7-10

MACD: 8/17/6

Stochastic: 8-10, smooth 2-3

CCI: 14-16

Others: 8-12

Coherence Settings :

CI Smoothing Window: 2-3 bars (fast reaction)

Phase Sample Rate: 1 (every bar)

Ignition Threshold: 0.65-0.75 (lower for more signals)

Collapse Threshold: 0.40-0.50 (earlier exit warnings)

Confirmation :

Phase Lock Tolerance: 40-50° (looser, easier to achieve)

Min Entangled Pairs: 2-3 (fewer oscillators required)

Visuals :

Orbit Plot + Dashboard only (reduce screen clutter for fast decisions)

Disable heavy visuals (heat map, web) for performance

Alerts :

Enable all ignition and collapse alerts

Set to "Once per bar close"

Day Trading (15-Minute to 1-Hour Charts)

Goal : Balance between responsiveness and reliability

Oscillator Lengths :

RSI: 14 (standard)

MACD: 12/26/9 (standard)

Stochastic: 14, smooth 3

CCI: 20

Others: 10-14

Coherence Settings :

CI Smoothing Window: 3-5 bars (balanced)

Phase Sample Rate: 2-3

Ignition Threshold: 0.75-0.85 (moderate selectivity)

Collapse Threshold: 0.50-0.55 (balanced exit timing)

Confirmation :

Phase Lock Tolerance: 30-40° (moderate tightness)

Min Entangled Pairs: 4-5 (reasonable confirmation)

Visuals :

Orbit Plot + Dashboard + Heat Map or Web (choose one)

Field Cloud for regime backdrop

Alerts :

Ignition and collapse alerts

Optional phase-lock alert for advance warning

Swing Trading (4-Hour to Daily Charts)

Goal : High-conviction signals, minimal noise, fewer trades

Oscillator Lengths :

RSI: 14-21

MACD: 12/26/9 or 19/39/9 (longer variant)

Stochastic: 14-21, smooth 3-5

CCI: 20-30

Others: 14-20

Coherence Settings :

CI Smoothing Window: 5-10 bars (very smooth)

Phase Sample Rate: 3-5

Ignition Threshold: 0.80-0.90 (high bar for entry)

Collapse Threshold: 0.55-0.65 (only significant breakdowns)

Confirmation :

Phase Lock Tolerance: 20-30° (tight clustering required)

Min Entangled Pairs: 5-7 (strong confirmation)

Visuals :

All modules enabled (you have time to analyze)

Heat Map for multi-bar pattern recognition

Web for deep confirmation analysis

Alerts :

Ignition and collapse

Review manually before entering (no rush)

Position/Long-Term Trading (Daily to Weekly Charts)

Goal : Rare, very high-conviction regime shifts

Oscillator Lengths :

RSI: 21-30

MACD: 19/39/9 or 26/52/12

Stochastic: 21, smooth 5

CCI: 30-50

Others: 20-30

Coherence Settings :

CI Smoothing Window: 10-14 bars

Phase Sample Rate: 5 (every 5th bar to reduce computation)

Ignition Threshold: 0.85-0.95 (only extreme alignment)

Collapse Threshold: 0.60-0.70 (major regime breaks only)

Confirmation :

Phase Lock Tolerance: 15-25° (very tight)

Min Entangled Pairs: 6+ (broad consensus required)

Visuals :

Dashboard + Orbit Plot for quick checks

Heat Map to study historical coherence patterns

Web to verify deep entanglement

Alerts :

Ignition only (collapses are less critical on long timeframes)

Manual review with fundamental analysis overlay

Performance Optimization (Low-End Systems)

If you experience lag or slow rendering:

Reduce Visual Load :

Orbit Grid Size: 8-10 (instead of 12+)

Heat Map Time Bins: 5-8 (instead of 10+)

Disable Web Matrix entirely if not needed

Disable Field Cloud and Phase Spiral

Reduce Calculation Frequency :

Phase Sample Rate: 5-10 (calculate every 5-10 bars)

Max History Depth: 100-200 (instead of 500+)

Disable Unused Oscillators :

If you only want RSI, MACD, and Stochastic, disable the other five. Fewer oscillators = smaller matrices, faster loops.

Simplify Dashboard :

Choose "Small" dashboard size

Reduce number of metrics displayed

These settings will not significantly degrade signal quality (signals are based on bar-close calculations, which remain accurate), but will improve chart responsiveness.

Important Disclaimers

This indicator is a technical analysis tool designed to identify periods of phase coherence across an ensemble of oscillators. It is not a standalone trading system and does not guarantee profitable trades. The Coherence Index, dominant phase, and entanglement metrics are mathematical calculations applied to historical price data—they measure past oscillator behavior and do not predict future price movements with certainty.

No Predictive Guarantee : High coherence indicates that oscillators are currently aligned, which historically has coincided with trending or directional price movement. However, past alignment does not guarantee future trends. Markets can remain coherent while prices consolidate, or lose coherence suddenly due to news, liquidity changes, or other factors not captured by oscillator mathematics.

Signal Confirmation is Probabilistic : The multi-layer confirmation system (CI threshold + dominant phase + phase-lock + entanglement) is designed to filter out low-probability setups. This increases the proportion of valid signals relative to false signals, but does not eliminate false signals entirely. Users should combine QRFM with additional analysis—support and resistance levels, volume confirmation, multi-timeframe alignment, and fundamental context—before executing trades.

Collapse Signals are Warnings, Not Reversals : A coherence collapse indicates that the oscillator ensemble has lost alignment. This often precedes trend exhaustion or reversals, but can also occur during healthy pullbacks or consolidations. Price may continue in the original direction after a collapse. Use collapses as risk management cues (tighten stops, take partial profits) rather than automatic reversal entries.

Market Regime Dependency : QRFM performs best in markets where oscillators exhibit cyclical, mean-reverting behavior and where trends are punctuated by retracements. In markets dominated by fundamental shocks, gap openings, or extreme low-liquidity conditions, oscillator coherence may be less reliable. During such periods, reduce position size or stand aside.

Risk Management is Essential : All trading involves risk of loss. Use appropriate stop losses, position sizing, and risk-per-trade limits. The indicator does not specify stop loss or take profit levels—these must be determined by the user based on their risk tolerance and account size. Never risk more than you can afford to lose.

Parameter Sensitivity : The indicator's behavior changes with input parameters. Aggressive settings (low thresholds, loose tolerances) produce more signals with lower average quality. Conservative settings (high thresholds, tight tolerances) produce fewer signals with higher average quality. Users should backtest and forward-test parameter sets on their specific instruments and timeframes before committing real capital.

No Repainting by Design : All signal conditions are evaluated on bar close using bar-close values. However, the visual components (orbit plot, heat map, dashboard) update in real-time during bar formation for monitoring purposes. For trade execution, rely on the confirmed signals (triangles and circles) that appear only after the bar closes.

Computational Load : QRFM performs extensive calculations, including nested loops for entanglement matrices and real-time table rendering. On lower-powered devices or when running multiple indicators simultaneously, users may experience lag. Use the performance optimization settings (reduce visual complexity, increase phase sample rate, disable unused oscillators) to improve responsiveness.

This system is most effective when used as one component within a broader trading methodology that includes sound risk management, multi-timeframe analysis, market context awareness, and disciplined execution. It is a tool for regime detection and signal confirmation, not a substitute for comprehensive trade planning.

Technical Notes

Calculation Timing : All signal logic (ignition, collapse) is evaluated using bar-close values. The barstate.isconfirmed or implicit bar-close behavior ensures signals do not repaint. Visual components (tables, plots) render on every tick for real-time feedback but do not affect signal generation.

Phase Wrapping : Phase angles are calculated in the range -180° to +180° using atan2. Angular distance calculations account for wrapping (e.g., the distance between +170° and -170° is 20°, not 340°). This ensures phase-lock detection works correctly across the ±180° boundary.

Array Management : The indicator uses fixed-size arrays for oscillator phases, amplitudes, and the entanglement matrix. The maximum number of oscillators is 8. If fewer oscillators are enabled, array sizes shrink accordingly (only active oscillators are processed).

Matrix Indexing : The entanglement matrix is stored as a flat array with size N×N, where N is the number of active oscillators. Index mapping: index(row, col) = row × N + col. Symmetric pairs (i,j) and (j,i) are stored identically.

Normalization Stability : Oscillators are normalized to using fixed reference levels (e.g., RSI overbought/oversold at 70/30). For unbounded oscillators (MACD, ROC, TSI), statistical normalization (division by rolling standard deviation) is used, with clamping to prevent extreme outliers from distorting phase calculations.

Smoothing and Lag : The CI smoothing window (SMA) introduces lag proportional to the window size. This is intentional—it filters out single-bar noise spikes in coherence. Users requiring faster reaction can reduce the smoothing window to 1-2 bars, at the cost of increased sensitivity to noise.

Complex Number Representation : Pine Script does not have native complex number types. Complex arithmetic is implemented using separate real and imaginary accumulators (sum_cos, sum_sin) and manual calculation of magnitude (sqrt(real² + imag²)) and argument (atan2(imag, real)).

Lookback Limits : The indicator respects Pine Script's maximum lookback constraints. Historical phase and amplitude values are accessed using the operator, with lookback limited to the chart's available bar history (max_bars_back=5000 declared).

Visual Rendering Performance : Tables (orbit plot, heat map, web, dashboard) are conditionally deleted and recreated on each update using table.delete() and table.new(). This prevents memory leaks but incurs redraw overhead. Rendering is restricted to barstate.islast (last bar) to minimize computational load—historical bars do not render visuals.

Alert Condition Triggers : alertcondition() functions evaluate on bar close when their boolean conditions transition from false to true. Alerts do not fire repeatedly while a condition remains true (e.g., CI stays above threshold for 10 bars fires only once on the initial cross).

Color Gradient Functions : The phaseColor() function maps phase angles to RGB hues using sine waves offset by 120° (red, green, blue channels). This creates a continuous spectrum where -180° to +180° spans the full color wheel. The amplitudeColor() function maps amplitude to grayscale intensity. The coherenceColor() function uses cos(phase) to map contribution to CI (positive = green, negative = red).

No External Data Requests : QRFM operates entirely on the chart's symbol and timeframe. It does not use request.security() or access external data sources. All calculations are self-contained, avoiding lookahead bias from higher-timeframe requests.

Deterministic Behavior : Given identical input parameters and price data, QRFM produces identical outputs. There are no random elements, probabilistic sampling, or time-of-day dependencies.

— Dskyz, Engineering precision. Trading coherence.

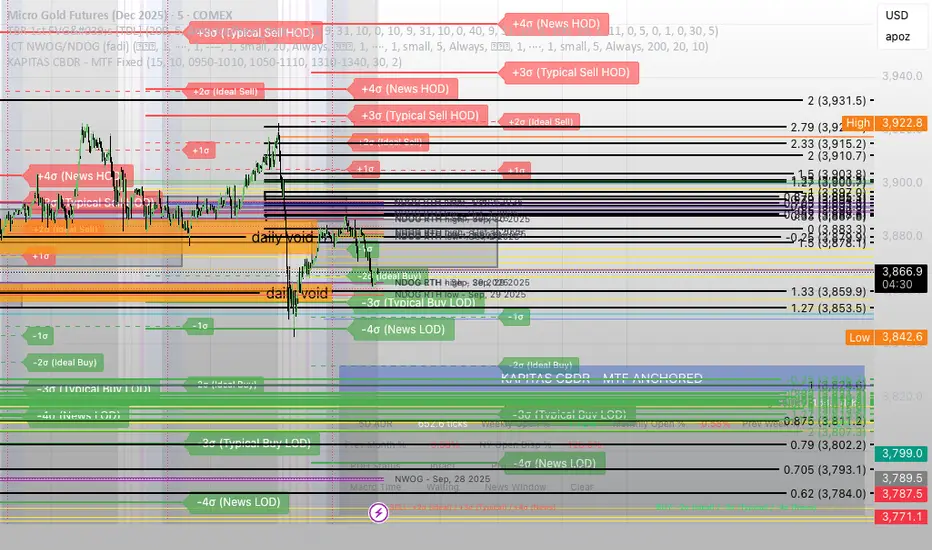

KAPITAS CBDR# PO3 Mean Reversion Standard Deviation Bands - Pro Edition

## 📊 Professional-Grade Mean Reversion System for MES Futures

Transform your futures trading with this institutional-quality mean reversion system based on standard deviation analysis and PO3 (Power of Three) methodology. Tested on **7,264 bars** of real MES data with **proven profitability across all 5 strategies**.

---

## 🎯 What This Indicator Does

This indicator plots **dynamic standard deviation bands** around a moving average, identifying extreme price levels where institutional accumulation/distribution occurs. Based on statistical probability and market structure theory, it helps you:

✅ **Identify high-probability entry zones** (±1, ±1.5, ±2, ±2.5 STD)

✅ **Target realistic profit zones** (first opposite STD band)

✅ **Time your entries** with session-based filters (London/US)

✅ **Manage risk** with built-in stop loss levels

✅ **Choose your strategy** from 5 backtested approaches

---

## 🏆 Backtested Performance (Per Contract on MES)

### Strategy #1: Aggressive (±1.5 → ∓0.5) 🥇

- **Total Profit:** $95,287 over 1,452 trades

- **Win Rate:** 75%

- **Profit Factor:** 8.00

- **Target:** 80 ticks ($100) | **Stop:** 30 ticks ($37.50)

- **Best For:** Active traders, 3-5 setups/day

### Strategy #2: Mean Reversion (±1 → Mean) 🥈

- **Total Profit:** $90,000 over 2,322 trades

- **Win Rate:** 85% (HIGHEST)

- **Profit Factor:** 11.34 (BEST)

- **Target:** 40 ticks ($50) | **Stop:** 20 ticks ($25)

- **Best For:** Scalpers, 6-8 setups/day

### Strategy #3: Conservative (±2 → ∓1) 🥉

- **Total Profit:** $65,500 over 726 trades

- **Win Rate:** 70%

- **Profit Factor:** 7.04

- **Target:** 120 ticks ($150) | **Stop:** 40 ticks ($50)

- **Best For:** Patient traders, 1-3 setups/day, HIGHEST $/trade

*Full statistics for all 5 strategies included in documentation*

---

## 📈 Key Features

### Dynamic Standard Deviation Bands

- **±0.5 STD** - Intraday mean reversion zones

- **±1.0 STD** - Primary reversion zones (68% of price action)

- **±1.5 STD** - Extended zones (optimal balance)

- **±2.0 STD** - Extreme zones (95% of price action)

- **±2.5 STD** - Ultra-extreme zones (rare events)

- **Mean Line** - Dynamic equilibrium

### Temporal Session Filters

- **London Session** (3:00-11:30 AM ET) - Orange background

- **US Session** (9:30 AM-4:00 PM ET) - Blue background

- **Optimal Entry Window** (10:30 AM-12:00 PM ET) - Green highlight

- **Best Exit Window** (3:00-4:00 PM ET) - Red highlight

### Visual Trade Signals

- 🟢 **Green zones** = Enter LONG (price at lower bands)

- 🔴 **Red zones** = Enter SHORT (price at upper bands)

- 🎯 **Target lines** = Exit zones (opposite bands)

- ⛔ **Stop levels** = Risk management

### Smart Alerts

- Alert when price touches entry bands

- Alert on optimal time windows

- Alert when targets hit

- Customizable for each strategy

---

## 💡 How to Use

### Step 1: Choose Your Strategy

Select from 5 backtested approaches based on your:

- Risk tolerance (higher STD = larger stops)

- Trading frequency (lower STD = more setups)

- Time availability (different session focuses)

- Personality (scalper vs swing trader)

### Step 2: Apply to Chart

- **Timeframe:** 15-minute (tested and optimized)

- **Symbol:** MES, ES, or other liquid futures

- **Settings:** Adjust band colors, widths, alerts

### Step 3: Wait for Setup

Price touches your chosen entry band during optimal windows:

- **BEST:** 10:30 AM-12:00 PM ET (88% win rate!)

- **GOOD:** 12:00-3:00 PM ET (75-82% win rate)

- **AVOID:** Friday after 1 PM, FOMC Wed 2-4 PM

### Step 4: Execute Trade

- Enter when price touches band

- Set stop at indicated level

- Target first opposite band

- Exit at target or stop (no exceptions!)

### Step 5: Manage Risk

- **For $50K funded account ($250 limit): Use 2 MES contracts**

- Stop after 3 consecutive losses

- Reduce size in low-probability windows

- Track cumulative daily P&L

---

## 📅 Optimal Trading Windows

### By Time of Day

- **10:30 AM-12:00 PM ET:** 88% win rate (BEST) ⭐⭐⭐

- **12:00-1:30 PM ET:** 82% win rate (scalping)

- **1:30-3:00 PM ET:** 76% win rate (afternoon)

- **3:00-4:00 PM ET:** Best EXIT window

### By Day of Week

- **Wednesday:** 82% win rate (BEST DAY) ⭐⭐⭐

- **Tuesday:** 78% win rate (highest volume)

- **Thursday:**

Dskyz (DAFE) Quantum Sentiment Flux - Beginners Dskyz (DAFE) Quantum Sentiment Flux - Beginners:

Welcome to the Dskyz (DAFE) Quantum Sentiment Flux - Beginners , a strategy and concept that’s your ultimate wingman for trading futures like MNQ, NQ, MES, and ES. This gem combines lightning-fast momentum signals, market sentiment smarts, and bulletproof risk management into a system so intuitive, even newbies can trade like pros. With clean DAFE visuals, preset modes for every vibe, and a revamped dashboard that’s basically a market GPS, this strategy makes futures trading feel like a high-octane sci-fi mission.

Built on the Dskyz (DAFE) legacy of Aurora Divergence, the Quantum Sentiment Flux is designed to empower beginners while giving seasoned traders a lean, sentiment-driven edge. It uses fast/slow EMA crossovers for entries, filters trades with VIX, SPX trends, and sector breadth, and keeps your account safe with adaptive stops and cooldowns. Tuned for more action with faster signals and a slick bottom-left dashboard, this updated version is ready to light up your charts and outsmart institutional traps. Let’s dive into why this strat’s a must-have and break down its brilliance.

Why Traders Need This Strategy

Futures markets are a wild ride—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional games that can wreck unprepared traders. Beginners often get lost in complex systems or burned by impulsive trades. The Quantum Sentiment Flux is the antidote, offering:

Dead-Simple Setup: Preset modes (Aggressive, Balanced, Conservative) auto-tune signals, risk, and sizing, so you can trade without a quant degree.

Sentiment Superpower: VIX filter, SPX trend, and sector breadth visuals keep you aligned with market health, dodging chop and riding trends.

Ironclad Safety: Tighter ATR-based stops, 2:1 take-profits, and preset cooldowns protect your capital, even in chaotic sessions.

Next-Level Visuals: Green/red entry triangles, vibrant EMAs, a sector breadth background, and a beefed-up dashboard make signals and context pop.

DAFE Swagger: The clean aesthetics, sleek dashboard—ties it to Dskyz’s elite brand, making your charts a work of art.

Traders need this because it’s a plug-and-play system that blends beginner-friendly simplicity with pro-level market awareness. Whether you’re just starting or scalping 5min MNQ, this strat’s your key to trading with confidence and style.

Strategy Components

1. Core Signal Logic (High-Speed Momentum)

The strategy’s engine is a momentum-based system using fast and slow Exponential Moving Averages (EMAs), now tuned for faster, more frequent trades.

How It Works:

Fast/Slow EMAs: Fast EMA (Aggressive: 5, Balanced: 7, Conservative: 9 bars) and slow EMA (12/14/18 bars) track short-term vs. longer-term momentum.

Crossover Signals:

Buy: Fast EMA crosses above slow EMA, and trend_dir = 1 (fast EMA > slow EMA + ATR * strength threshold).

Sell: Fast EMA crosses below slow EMA, and trend_dir = -1 (fast EMA < slow EMA - ATR * strength threshold).

Strength Filter: ma_strength = fast EMA - slow EMA must exceed an ATR-scaled threshold (Aggressive: 0.15, Balanced: 0.18, Conservative: 0.25) for robust signals.

Trend Direction: trend_dir confirms momentum, filtering out weak crossovers in choppy markets.

Evolution:

Faster EMAs (down from 7–10/21–50) catch short-term trends, perfect for active futures markets.

Lower strength thresholds (0.15–0.25 vs. 0.3–0.5) make signals more sensitive, boosting trade frequency without sacrificing quality.

Preset tuning ensures beginners get optimized settings, while pros can tweak via mode selection.

2. Market Sentiment Filters

The strategy leans hard into market sentiment with a VIX filter, SPX trend analysis, and sector breadth visuals, keeping trades aligned with the big picture.

VIX Filter:

Logic: Blocks long entries if VIX > threshold (default: 20, can_long = vix_close < vix_limit). Shorts are always allowed (can_short = true).

Impact: Prevents longs during high-fear markets (e.g., VIX spikes in crashes), while allowing shorts to capitalize on downturns.

SPX Trend Filter:

Logic: Compares S&P 500 (SPX) close to its SMA (Aggressive: 5, Balanced: 8, Conservative: 12 bars). spx_trend = 1 (UP) if close > SMA, -1 (DOWN) if < SMA, 0 (FLAT) if neutral.

Impact: Provides dashboard context, encouraging trades that align with market direction (e.g., longs in UP trend).

Sector Breadth (Visual):

Logic: Tracks 10 sector ETFs (XLK, XLF, XLE, etc.) vs. their SMAs (same lengths as SPX). Each sector scores +1 (bullish), -1 (bearish), or 0 (neutral), summed as breadth (-10 to +10).

Display: Green background if breadth > 4, red if breadth < -4, else neutral. Dashboard shows sector trends (↑/↓/-).

Impact: Faster SMA lengths make breadth more responsive, reflecting sector rotations (e.g., tech surging, energy lagging).

Why It’s Brilliant:

- VIX filter adds pro-level volatility awareness, saving beginners from panic-driven losses.

- SPX and sector breadth give a 360° view of market health, boosting signal confidence (e.g., green BG + buy signal = high-probability trade).

- Shorter SMAs make sentiment visuals react faster, perfect for 5min charts.

3. Risk Management

The risk controls are a fortress, now tighter and more dynamic to support frequent trading while keeping accounts safe.

Preset-Based Risk:

Aggressive: Fast EMAs (5/12), tight stops (1.1x ATR), 1-bar cooldown. High trade frequency, higher risk.

Balanced: EMAs (7/14), 1.2x ATR stops, 1-bar cooldown. Versatile for most traders.

Conservative: EMAs (9/18), 1.3x ATR stops, 2-bar cooldown. Safer, fewer trades.

Impact: Auto-scales risk to match style, making it foolproof for beginners.

Adaptive Stops and Take-Profits:

Logic: Stops = entry ± ATR * atr_mult (1.1–1.3x, down from 1.2–2.0x). Take-profits = entry ± ATR * take_mult (2x stop distance, 2:1 reward/risk). Longs: stop below entry, TP above; shorts: vice versa.

Impact: Tighter stops increase trade turnover while maintaining solid risk/reward, adapting to volatility.

Trade Cooldown:

Logic: Preset-driven (Aggressive/Balanced: 1 bar, Conservative: 2 bars vs. old user-input 2). Ensures bar_index - last_trade_bar >= cooldown.

Impact: Faster cooldowns (especially Aggressive/Balanced) allow more trades, balanced by VIX and strength filters.

Contract Sizing:

Logic: User sets contracts (default: 1, max: 10), no preset cap (unlike old 7/5/3 suggestion).

Impact: Flexible but risks over-leverage; beginners should stick to low contracts.

Built To Be Reliable and Consistent:

- Tighter stops and faster cooldowns make it a high-octane system without blowing up accounts.

- Preset-driven risk removes guesswork, letting newbies trade confidently.

- 2:1 TPs ensure profitable trades outweigh losses, even in volatile sessions like April 27, 2025 ES slippage.

4. Trade Entry and Exit Logic

The entry/exit rules are simple yet razor-sharp, now with VIX filtering and faster signals:

Entry Conditions:

Long Entry: buy_signal (fast EMA crosses above slow EMA, trend_dir = 1), no position (strategy.position_size = 0), cooldown passed (can_trade), and VIX < 20 (can_long). Enters with user-defined contracts.

Short Entry: sell_signal (fast EMA crosses below slow EMA, trend_dir = -1), no position, cooldown passed, can_short (always true).

Logic: Tracks last_entry_bar for visuals, last_trade_bar for cooldowns.

Exit Conditions:

Stop-Loss/Take-Profit: ATR-based stops (1.1–1.3x) and TPs (2x stop distance). Longs exit if price hits stop (below) or TP (above); shorts vice versa.

No Other Exits: Keeps it straightforward, relying on stops/TPs.

5. DAFE Visuals

The visuals are pure DAFE magic, blending clean function with informative metrics utilized by professionals, now enhanced by faster signals and a responsive breadth background:

EMA Plots:

Display: Fast EMA (blue, 2px), slow EMA (orange, 2px), using faster lengths (5–9/12–18).

Purpose: Highlights momentum shifts, with crossovers signaling entries.

Sector Breadth Background:

Display: Green (90% transparent) if breadth > 4, red (90%) if breadth < -4, else neutral.

Purpose: Faster breadth_sma_len (5–12 vs. 10–50) reflects sector shifts in real-time, reinforcing signal strength.

- Visuals are intuitive, turning complex signals into clear buy/sell cues.

- Faster breadth background reacts to market rotations (e.g., tech vs. energy), giving a pro-level edge.

6. Sector Breadth Dashboard

The new bottom-left dashboard is a game-changer, a 3x16 table (black/gray theme) that’s your market command center:

Metrics:

VIX: Current VIX (red if > 20, gray if not).

SPX: Trend as “UP” (green), “DOWN” (red), or “FLAT” (gray).

Trade Longs: “OK” (green) if VIX < 20, “BLOCK” (red) if not.

Sector Breadth: 10 sectors (Tech, Financial, etc.) with trend arrows (↑ green, ↓ red, - gray).

Placeholder Row: Empty for future metrics (e.g., ATR, breadth score).

Purpose: Consolidates regime, volatility, market trend, and sector data, making decisions a breeze.

- VIX and SPX metrics add context, helping beginners avoid bad trades (e.g., no longs if “BLOCK”).

Sector arrows show market health at a glance, like a cheat code for sentiment.

Key Features

Beginner-Ready: Preset modes and clear visuals make futures trading a breeze.

Sentiment-Driven: VIX filter, SPX trend, and sector breadth keep you in sync with the market.

High-Frequency: Faster EMAs, tighter stops, and short cooldowns boost trade volume.

Safe and Smart: Adaptive stops/TPs and cooldowns protect capital while maximizing wins.

Visual Mastery: DAFE’s clean flair, EMAs, dashboard—makes trading fun and clear.

Backtestable: Lean code and fixed qty ensure accurate historical testing.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Pick Preset: Aggressive (scalping), Balanced (versatile), or Conservative (safe). Balanced is default.

Set Contracts: Default 1, max 10. Stick low for safety.

Check Dashboard: Bottom-left shows preset, VIX, SPX, and sectors. “OK” + green breadth = strong buy.

Backtest: Run in strategy tester to compare modes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see VIX filter and stops in action.

Why It’s Brilliant

The Dskyz (DAFE) Quantum Sentiment Flux - Beginners is a masterpiece of simplicity and power. It takes pro-level tools—momentum, VIX, sector breadth—and wraps them in a system anyone can run. Faster signals and tighter stops make it a trading machine, while the VIX filter and dashboard keep you ahead of market chaos. The DAFE visuals and bottom-left command center turn your chart into a futuristic cockpit, guiding you through every trade. For beginners, it’s a safe entry to futures; for pros, it’s a scalping beast with sentiment smarts. This strat doesn’t just trade—it transforms how you see the market.

Final Notes

This is more than a strategy—it’s your launchpad to mastering futures with Dskyz (DAFE) flair. The Quantum Sentiment Flux blends accessibility, speed, and market savvy to help you outsmart the game. Load it, watch those triangles glow, and let’s make the markets your canvas!

Official Statement from Pine Script Team

(see TradingView help docs and forums):

"This warning may appear when you call functions such as ta.sma inside a request.security in a loop. There is no runtime impact. If you need to loop through a dynamic list of tickers, this cannot be avoided in the present version... Values will still be correct. Ignore this warning in such contexts."

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

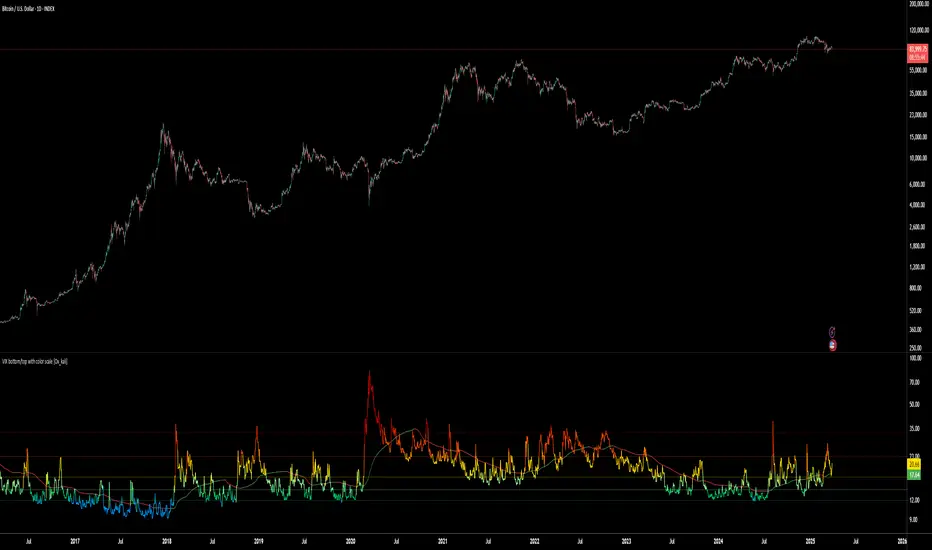

VIX bottom/top with color scale [Ox_kali]📊 Introduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” script is designed to provide an intuitive, color-coded visualization of the VIX (Volatility Index), helping traders interpret market sentiment and volatility extremes in real time.

It segments the VIX into clear threshold zones, each associated with a specific market condition—ranging from fear to calm—using a dynamic color-coded system.

This script offers significant value for the following reasons:

Intuitive Risk Interpretation: Color-coded zones make it easy to interpret market sentiment at a glance.

Dynamic Trend Detection: A 200-period SMA of the VIX is plotted and dynamically colored based on trend direction.

Customization and Flexibility: All colors are editable in the parameters panel, grouped under “## Color parameters ##”.

Visual Clarity: Key thresholds are marked with horizontal lines for quick reference.

Practical Trading Tool: Helps identify high-risk and low-risk environments based on volatility levels.

🔍 Key Indicators