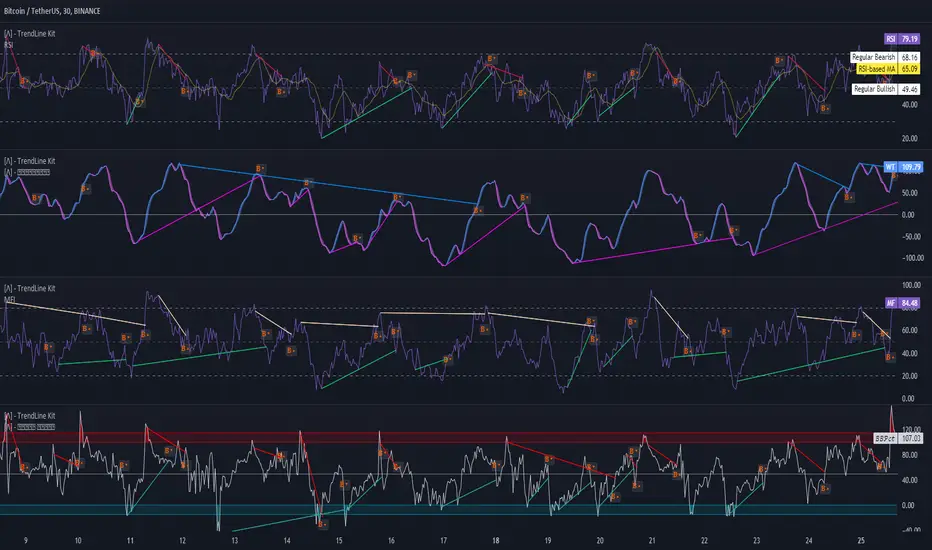

TrendLine Toolkit w/ Breaks (Real-Time)The TrendLine Toolkit script introduces an innovating capability by extending the conventional use of trendlines beyond price action to include oscillators and other technical indicators. This tool allows traders to automatically detect and display trendlines on any TradingView built-in oscillator or community-built script, offering a versatile approach to trend analysis. With breakout detection and real-time alerts, this script enhances the way traders interpret trends in various indicators.

🔲 Methodology

Trendlines are a fundamental tool in technical analysis used to identify and visualize the direction and strength of a price trend. They are drawn by connecting two or more significant points on a price chart, typically the highs or lows of consecutive price movements (pivots).

Drawing Trendlines:

Uptrend Line - Connects a series of higher lows. It signals an upward price trend.

Downtrend Line - Connects a series of lower highs. It indicates a downward price trend.

Support and Resistance:

Support Line - A trendline drawn under rising prices, indicating a level where buying interest is historically strong.

Resistance Line - A trendline drawn above falling prices, showing a level where selling interest historically prevails.

Identification of Trends:

Uptrend - Prices making higher highs and higher lows.

Downtrend - Prices making lower highs and lower lows.

Sideways (or Range-bound) - Prices moving within a horizontal range.

A trendline helps confirm the existence and direction of a trend, providing guidance in aligning with the prevailing market sentiment. Additionally, they are usually paired with breakout analysis, a breakout occurs when the price breaches a trendline. This signals a potential change in trend direction or an acceleration of the existing trend.

The script adapts this methodology to oscillators and other indicators. Instead of relying on price pivots, which can only be detected in retrospect, the script utilizes a trailing stop on the oscillator to identify potential swings in real-time, you may find more info about it here (SuperTrend toolkit) . We detect swings or pivots simply by testing for crosses between the indicator and its trailing stop.

type oscillator

float o = Oscillator Value

float s = Trailing Stop Value

oscillator osc = oscillator.new()

bool l = ta.crossunder(osc.o, osc.s) => Utilized as a formed high

bool h = ta.crossover (osc.o, osc.s) => Utilized as a formed low

This approach enables the algorithm to detect trendlines between consecutive pivot highs or lows on the oscillator itself, providing a dynamic and immediate representation of trend dynamics.

🔲 Breakout Detection

The script goes beyond trendline creation by incorporating breakout detection directly within the oscillator. After identifying a trendline, the algorithm continuously monitors the oscillator for potential breakouts, signaling shifts in market sentiment.

🔲 Setup Guide

A simple example on one of my public scripts, Z-Score Heikin-Ashi Transformed

🔲 Settings

Source - Choose an oscillator source of which to base the Toolkit on.

Zeroing - The Mid-Line value of the oscillator, for example RSI & MFI use 50.

Sensitivity - Calibrates the Sensitivity of which TrendLines are detected, higher values result in more detections.

🔲 Alerts

Bearish TrendLine

Bullish TrendLine

Bearish Breakout

Bullish Breakout

As well as the option to trigger 'any alert' call.

By integrating trendline analysis into oscillators, this Toolkit enhances the capabilities of technical analysis, bringing a dynamic and comprehensive approach to identifying trends, support/resistance levels, and breakout signals across various indicators.

Recherche dans les scripts pour "algo"

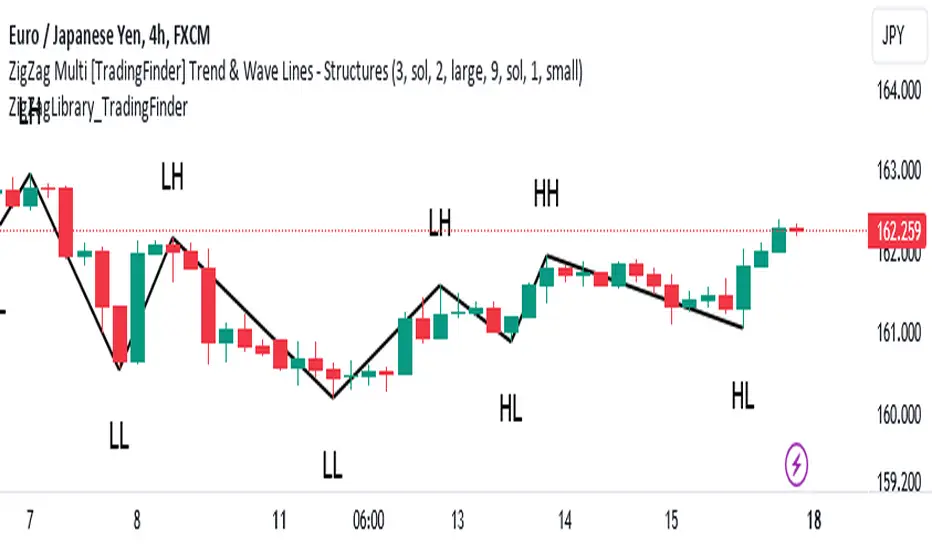

ZigZag Library [TradingFinder]🔵 Introduction

The "Zig Zag" indicator is an analytical tool that emerges from pricing changes. Essentially, it connects consecutive high and low points in an oscillatory manner. This method helps decipher price changes and can also be useful in identifying traditional patterns.

By sifting through partial price changes, "Zig Zag" can effectively pinpoint price fluctuations within defined time intervals.

🔵 Key Features

1. Drawing the Zig Zag based on Pivot points :

The algorithm is based on pivots that operate consecutively and alternately (switch between high and low swing). In this way, zigzag lines are connected from a swing high to a swing low and from a swing low to a swing high.

Also, with a very low probability, it is possible to have both low pivots and high pivots in one candle. In these cases, the algorithm tries to make the best decision to make the most suitable choice.

You can control what period these decisions are based on through the "PiPe" parameter.

2.Naming and labeling each pivot based on its position as "Higher High" (HH), "Lower Low" (LL), "Higher Low" (HL), and "Lower High" (LH).

Additionally, classic patterns such as HH, LH, LL, and HL can be recognized. All traders analyzing financial markets using classic patterns and Elliot Waves can benefit from the "zigzag" indicator to facilitate their analysis.

" HH ": When the price is higher than the previous peak (Higher High).

" HL ": When the price is higher than the previous low (Higher Low).

" LH ": When the price is lower than the previous peak (Lower High).

" LL ": When the price is lower than the previous low (Lower Low).

🔵 How to Use

First, you can add the library to your code as shown in the example below.

import TFlab/ZigZagLibrary_TradingFinder/1 as ZZ

Function "ZigZag" Parameters :

🟣 Logical Parameters

1. HIGH : You should place the "high" value here. High is a float variable.

2. LOW : You should place the "low" value here. Low is a float variable.

3. BAR_INDEX : You should place the "bar_index" value here. Bar_index is an integer variable.

4. PiPe : The desired pivot period for plotting Zig Zag is placed in this parameter. For example, if you intend to draw a Zig Zag with a Swing Period of 5, you should input 5.

PiPe is an integer variable.

Important :

Apart from the "PiPe" indicator, which is part of the customization capabilities of this indicator, you can create a multi-time frame mode for the indicator using 3 parameters "High", "Low" and "BAR_INDEX". In this way, instead of the data of the current time frame, use the data of other time frames.

Note that it is better to use the current time frame data, because using the multi-time frame mode is associated with challenges that may cause bugs in your code.

🟣 Setting Parameters

5. SHOW_LINE : It's a boolean variable. When true, the Zig Zag line is displayed, and when false, the Zig Zag line display is disabled.

6. STYLE_LINE : In this variable, you can determine the style of the Zig Zag line. You can input one of the 3 options: line.style_solid, line.style_dotted, line.style_dashed. STYLE_LINE is a constant string variable.

7. COLOR_LINE : This variable takes the input of the line color.

8. WIDTH_LINE : The input for this variable is a number from 1 to 3, which is used to adjust the thickness of the line that draws the Zig Zag. WIDTH_LINE is an integer variable.

9. SHOW_LABEL : It's a boolean variable. When true, labels are displayed, and when false, label display is disabled.

10. COLOR_LABEL : The color of the labels is set in this variable.

11. SIZE_LABEL : The size of the labels is set in this variable. You should input one of the following options: size.auto, size.tiny, size.small, size.normal, size.large, size.huge.

12. Show_Support : It's a boolean variable that, when true, plots the last support line, and when false, disables its plotting.

13. Show_Resistance : It's a boolean variable that, when true, plots the last resistance line, and when false, disables its plotting.

Suggestion :

You can use the following code snippet to import Zig Zag into your code for time efficiency.

//import Library

import TFlab/ZigZagLibrary_TradingFinder/1 as ZZ

// Input and Setting

// Zig Zag Line

ShZ = input.bool(true , 'Show Zig Zag Line', group = 'Zig Zag') //Show Zig Zag

PPZ = input.int(5 ,'Pivot Period Zig Zag Line' , group = 'Zig Zag') //Pivot Period Zig Zag

ZLS = input.string(line.style_dashed , 'Zig Zag Line Style' , options = , group = 'Zig Zag' )

//Zig Zag Line Style

ZLC = input.color(color.rgb(0, 0, 0) , 'Zig Zag Line Color' , group = 'Zig Zag') //Zig Zag Line Color

ZLW = input.int(1 , 'Zig Zag Line Width' , group = 'Zig Zag')//Zig Zag Line Width

// Label

ShL = input.bool(true , 'Label', group = 'Label') //Show Label

LC = input.color(color.rgb(0, 0, 0) , 'Label Color' , group = 'Label')//Label Color

LS = input.string(size.tiny , 'Label size' , options = , group = 'Label' )//Label size

Show_Support= input.bool(false, 'Show Last Support',

tooltip = 'Last Support' , group = 'Support and Resistance')

Show_Resistance = input.bool(false, 'Show Last Resistance',

tooltip = 'Last Resistance' , group = 'Support and Resistance')

//Call Function

ZZ.ZigZag(high ,low ,bar_index ,PPZ , ShZ ,ZLS , ZLC, ZLW ,ShL , LC , LS , Show_Support , Show_Resistance )

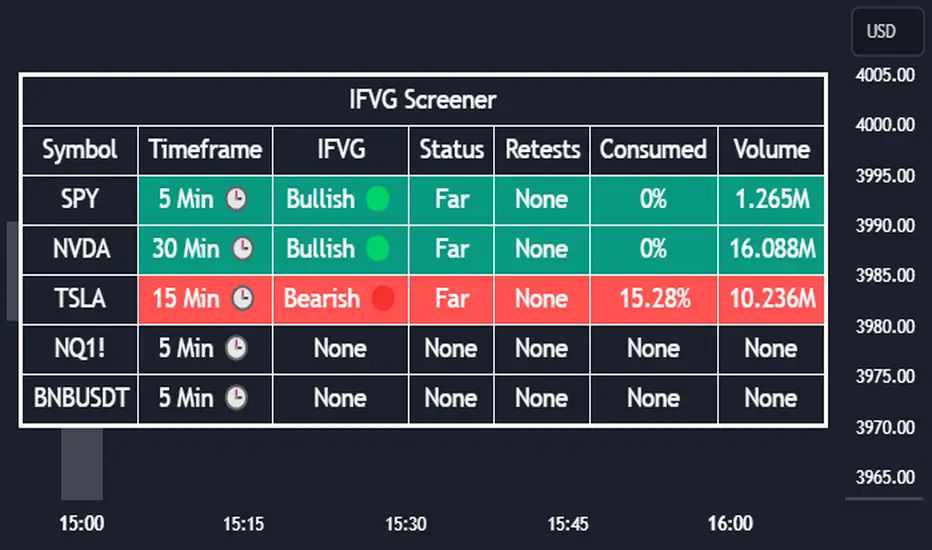

Inversion Fair Value Gap Screener | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Inverse Fair Value Gap Screener! This screener can provide information about the latest Inverse Fair Value Gaps in up to 5 tickers. You can also customize the algorithm that finds the Inverse Fair Value Gaps and the styling of the screener.

Features of the new Inverse Fair Value Gap (IFVG) Screener :

Find Latest Inverse Fair Value Gaps Across 5 Tickers

Shows Their Information Of :

Latest Status

Number Of Retests

Consumption Percent

Volume

Customizable Algorithm / Styling

📌 HOW DOES IT WORK ?

A Fair Value Gap generally occur when there is an imbalance in the market. They can be detected by specific formations within the chart. An Inverse Fair Value Gap is when a FVG becomes invalidated, thus reversing the direction of the FVG.

IFVGs get consumed when a Close / Wick enters the IFVG zone. Check this example:

This screener then finds Fair Value Gaps across 5 different tickers, and shows the latest information about them.

Status ->

Far -> The current price is far away from the IFVG.

Approaching ⬆️/⬇️ -> The current price is approaching the IFVG, and the direction it's approaching from.

Inside -> The price is currently inside the IFVG.

Retests -> Retest means the price tried to invalidate the IFVG, but failed to do so. Here you can see how many times the price retested the IFVG.

Consumed -> IFVGs get consumed when a Close / Wick enters the IFVG zone. For example, if the price hits the middle of the IFVG zone, the zone is considered 50% consumed.

Volume -> Volume of a IFVG is essentially the volume of the bar that broke the original FVG that formed it.

🚩UNIQUENESS

This screener can detect latest Inverse Fair Value Gaps and give information about them for up to 5 tickers. This saves the user time by showing them all in a dashboard at the same time. The screener also uniquely shows information about the number of retests and the consumed percent of the IFVG, as well as it's volume. We believe that this extra information will help you spot reliable IFVGs easier.

⚙️SETTINGS

1. Tickers

You can set up to 5 tickers for the screener to scan Fair Value Gaps here. You can also enable / disable them and set their individual timeframes.

2. General Configuration

FVG Zone Invalidation -> Select between Wick & Close price for FVG Zone Invalidation.

IFVG Zone Invalidation -> Select between Wick & Close price for IFVG Zone Invalidation. This setting also switches the type for IFVG consumption.

Zone Filtering -> With "Average Range" selected, algorithm will find FVG zones in comparison with average range of last bars in the chart. With the "Volume Threshold" option, you may select a Volume Threshold % to spot FVGs with a larger total volume than average.

FVG Detection -> With the "Same Type" option, all 3 bars that formed the FVG should be the same type. (Bullish / Bearish). If the "All" option is selected, bar types may vary between Bullish / Bearish.

Detection Sensitivity -> You may select between Low, Normal or High FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivities resulting in spotting bigger FVGs, and higher sensitivities resulting in spotting all sizes of FVGs.

Composite Trend Oscillator [ChartPrime]CODE DUELLO:

Have you ever stopped to wonder what the underlying filters contained within complex algorithms are actually providing for you? Wouldn't it be nice to actually visually inspect for that? Those would require some kind of wild west styled quick draw duel or some comparison method as a proper 'code duello'. Then it can be determined which filter can 'draw' the quickest from it's computational holster with the least amount of lag and smoothness.

In Pine we can do so, discovering how beneficial that would be. This can be accomplished by quickly switching from one filter to another by input() back and forth, requiring visual memory. A better way could be done by placing two indicators added to the chart and then eventually placed into one indicator pane on top of each other.

By adding a filter() helper function that calls other moving average functions chosen for comparison, it can put to the test which moving average is the best drawing filter suited to our expected needs. PhiSmoother was formerly debuted and now it is utilized in a more complex environment in a multitude of ways along side other commonly utilized filters. Now, you the reader, get to judge for yourself...

FILTER VERSATILITY:

Having the capability to adjust between various smoothing methods such as PhiSmoother, TEMA, DEMA, WMA, EMA, and SMA on historical market data within the code provides an advantage. Each of these filter methods offers distinct advantages and hinderances. PhiSmoother stands out often by having superb noise rejection, while also being able to manipulate the fine-tuning of the phase or lag of the indicator, enhancing responsiveness to price movements.

The following are more well-known classic filters. TEMA (Triple Exponential Moving Average) and DEMA (Double Exponential Moving Average) offer reduced transient response times to price changes fluctuations. WMA (Weighted Moving Average) assigns more weight to recent data points, making it particularly useful for reduced lag. EMA (Exponential Moving Average) strikes a balance between responsiveness and computational efficiency, making it a popular choice. SMA (Simple Moving Average) provides a straightforward calculation based on the arithmetic mean of the data. VWMA and RMA have both been excluded for varying reasons, both being unworthy of having explanation here.

By allowing for adjustment refinements between these filter methods, traders may garner the flexibility to adapt their analysis to different market dynamics, optimizing their algorithms for improved decision-making and performance on demand.

INDICATOR INTRODUCTION:

ChartPrime's Composite Trend Oscillator operates as an oscillator based on the concept of a moving average ribbon. It utilizes up to 32 filters with progressively longer periods to assess trend direction and strength. Embedded within this indicator is an alternative view that utilizes the separation of the ribbon filaments to assess volatility. Both versions are excellent candidates for trend and momentum, both offering visualization of polarity, directional coloring, and filter crossings. Anyone who has former experience using RSI or stochastics may have ease of understanding applying this to their chart.

COMPOSITE CLUSTER MODES EXPLAINED:

In Trend Strength mode, the oscillator behavior signifies market direction and movement strength. When the oscillator is rising and above zero, the market is within a bullish phase, and visa versa. If the signal filter crosses the composite trend, this indicates a potential dynamic shift signaling a possible reversal. When the oscillator is teetering on its extremities, the market is more inclined to reverse later.

With Volatility mode, the oscillator undergoes a transformation, displaying an unbounded oscillator driven by market volatility. While it still employs the same scoring mechanism, it is now scaled according to the strength of the market move. This can aid with identification of ranging scenarios. However, one side effect is that the oscillator no longer has minimum or maximum boundaries. This can still be advantageous when considering divergences.

NOTEWORTHY SETTINGS FEATURES:

The following input settings described offer comprehensive control over the indicator's behavior and visualization.

Common Controls:

Price Source Selection - The indicator offers flexibility in choosing the price source for analysis. Traders can select from multiple options.

Composite Cluster Mode - Choose between "Trend Strength" and "Volatility" modes, providing insights into trend directionality or volatility weighting.

Cluster Filter and Length - Selects a filter for the cluster composition. This includes a length parameter adjustment.

Cluster Options:

Cluster Dispersion - Users can adjust the separation between moving averages in the cluster, influencing the sensitivity of the analysis.

Cluster Trimming - By modifying upper and lower trim parameters, traders can adjust the sensitivity of the moving averages within the cluster, enhancing its adaptability.

PostSmooth Filter and Length - Choose a filter to refine the composite cluster's post-smoothing with a length parameter adjustment.

Signal Filter and Length - Users can select a filter for the lagging signal plot, also having a length parameter adjustment.

Transition Easing - Sensitivity adjustment to influence the transition between bullish and bearish colors.

Enjoy

Machine Learning: Multiple Logistic Regression

Multiple Logistic Regression Indicator

The Logistic Regression Indicator for TradingView is a versatile tool that employs multiple logistic regression based on various technical indicators to generate potential buy and sell signals. By utilizing key indicators such as RSI, CCI, DMI, Aroon, EMA, and SuperTrend, the indicator aims to provide a systematic approach to decision-making in financial markets.

How It Works:

Technical Indicators:

The script uses multiple technical indicators such as RSI, CCI, DMI, Aroon, EMA, and SuperTrend as input variables for the logistic regression model.

These indicators are normalized to create categorical variables, providing a consistent scale for the model.

Logistic Regression:

The logistic regression function is applied to the normalized input variables (x1 to x6) with user-defined coefficients (b0 to b6).

The logistic regression model predicts the probability of a binary outcome, with values closer to 1 indicating a bullish signal and values closer to 0 indicating a bearish signal.

Loss Function (Cross-Entropy Loss):

The cross-entropy loss function is calculated to quantify the difference between the predicted probability and the actual outcome.

The goal is to minimize this loss, which essentially measures the model's accuracy.

// Error Function (cross-entropy loss)

loss(y, p) =>

-y * math.log(p) - (1 - y) * math.log(1 - p)

// y - depended variable

// p - multiple logistic regression

Gradient Descent:

Gradient descent is an optimization algorithm used to minimize the loss function by adjusting the weights of the logistic regression model.

The script iteratively updates the weights (b1 to b6) based on the negative gradient of the loss function with respect to each weight.

// Adjusting model weights using gradient descent

b1 -= lr * (p + loss) * x1

b2 -= lr * (p + loss) * x2

b3 -= lr * (p + loss) * x3

b4 -= lr * (p + loss) * x4

b5 -= lr * (p + loss) * x5

b6 -= lr * (p + loss) * x6

// lr - learning rate or step of learning

// p - multiple logistic regression

// x_n - variables

Learning Rate:

The learning rate (lr) determines the step size in the weight adjustment process. It prevents the algorithm from overshooting the minimum of the loss function.

Users can set the learning rate to control the speed and stability of the optimization process.

Visualization:

The script visualizes the output of the logistic regression model by coloring the SMA.

Arrows are plotted at crossover and crossunder points, indicating potential buy and sell signals.

Lables are showing logistic regression values from 1 to 0 above and below bars

Table Display:

A table is displayed on the chart, providing real-time information about the input variables, their values, and the learned coefficients.

This allows traders to monitor the model's interpretation of the technical indicators and observe how the coefficients change over time.

How to Use:

Parameter Adjustment:

Users can adjust the length of technical indicators (rsi_length, cci_length, etc.) and the Z score length based on their preference and market characteristics.

Set the initial values for the regression coefficients (b0 to b6) and the learning rate (lr) according to your trading strategy.

Signal Interpretation:

Buy signals are indicated by an upward arrow (▲), and sell signals are indicated by a downward arrow (▼).

The color-coded SMA provides a visual representation of the logistic regression output by color.

Table Information:

Monitor the table for real-time information on the input variables, their values, and the learned coefficients.

Keep an eye on the learning rate to ensure a balance between model adjustment speed and stability.

Backtesting and Validation:

Before using the script in live trading, conduct thorough backtesting to evaluate its performance under different market conditions.

Validate the model against historical data to ensure its reliability.

Shadow Range IndexShadow Range Index (SRI) introduces a new concept to calculate momentum, shadow range.

What is range?

Traditionally, True Range (TR) is the current high minus the current low of each bar in the timeframe. This is often used successfully on its own in indicators, or as a moving average in ATR (Average True Range).

To calculate range, SRI uses an innovative calculation of current bar range that also considers the previous bar. It calculates the difference between its maximum upward and maximum downward values over the number of bars the user chooses (by adjusting ‘Range lookback’).

What is shadow range?

True Range (TR) uses elements in its calculation (the highs and lows of the bar) that are also visible on the chart bars. Shadow range does not, though.

SRI calculates shadow range in a similar formula to range, except that this time it works out the difference between the minimum upward and minimum downward movement. This movement is by its nature less than the maximums, hence a shadow of it. Although more subtle, shadow range is significant, because it is quantifiable, and goes in one direction or another.

Finally, SRI smoothes shadow range and plots it as a histogram, and also smoothes and plots range as a signal line. Useful up and down triangles show trend changes, which optionally colour the chart bars.

Here’s an example of a long trade setup:

In summary, Shadow Range Index identifies and traces maximum and minimum bar range movement both up and down, and plots them as centred oscillators. The dynamics between the two can provide insights into the chart's performance and future direction.

Credit to these authors, whose MA or filters form part of this script:

@balipour - Super Smoother MA

@cheatcountry - Hann window smoothing

@AlgoAlpha - Gaussian filter

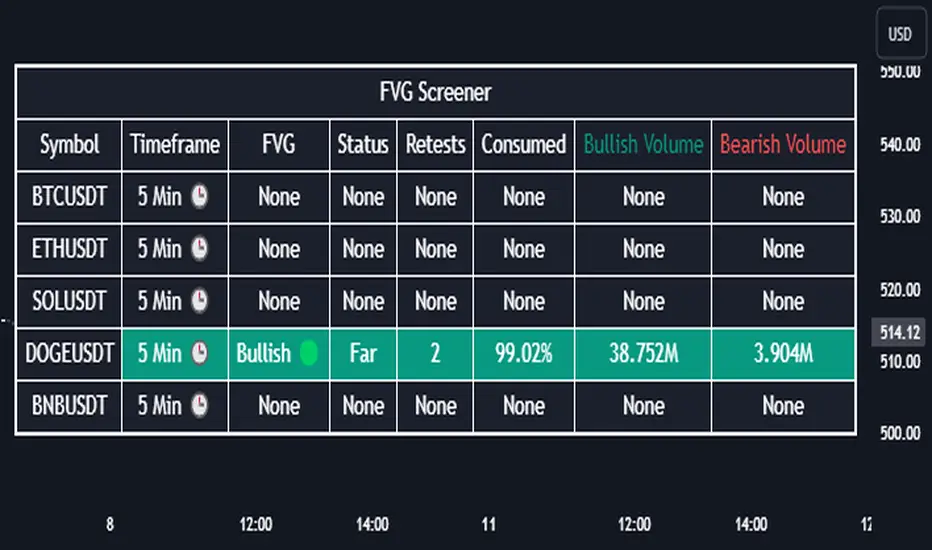

Fair Value Gap Screener | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Fair Value Gap Screener! This screener can provide information about the latest Fair Value Gaps in up to 5 tickers. You can also customize the algorithm that finds the Fair Value Gaps and the styling of the screener.

Features of the new Fair Value Gap (FVG) Screener :

Find Latest Fair Value Gaps Accross 5 Tickers

Shows Their Information Of :

Latest Status

Number Of Retests

Consumption Percent

Bullish & Bearish Volume

Customizable Algoritm / Styling

📌 HOW DOES IT WORK ?

A Fair Value Gap generally occur when there is an imbalance in the market. They can be detected by specific formations within the chart. This screener then finds Fair Value Gaps accross 5 different tickers, and shows the latest information about them.

Status ->

Far -> The current price is far away from the FVG.

Approaching ⬆️/⬇️ -> The current price is approaching the FVG, and the direction it's approaching from.

Inside -> The price is currently inside the FVG.

Retests -> Retest means the price tried to invalidate the FVG, but failed to do so. Here you can see how many times the price retested the FVG.

Consumed -> FVGs get consumed when a Close / Wick enters the FVG zone. For example, if the price hits the middle of the FVG zone, the zone is considered 50% consumed.

Bullish / Bearish Volume -> Bullish & Bearish volume of a FVG is calculated by analyzing the bars that formed it. For example in a bullish FVG, the bullish volume is the total volume of the first 2 bars forming the FVG, and the bearish volume is the volume of the 3rd bar that forms it.

🚩UNIQUENESS

This screener can detect latest Fair Value Gaps and give information about them for up to 5 tickers. This saves the user time by showing them all in a dashboard at the same time. The screener also uniquely shows information about the number of retests and the consumed percent of the FVG, as well as it's bullish & bearish volume. We believe that this extra information will help you spot reliable FVGs easier.

⚙️SETTINGS

1. Tickers

You can set up to 5 tickers for the screener to scan Fair Value Gaps here. You can also enable / disable them and set their individual timeframes.

2. General Configuration

Zone Invalidation -> Select between Wick & Close price for FVG Zone Invalidation.

Zone Filtering -> With "Average Range" selected, algorithm will find FVG zones in comparison with average range of last bars in the chart. With the "Volume Threshold" option, you may select a Volume Threshold % to spot FVGs with a larger total volume than average.

FVG Detection -> With the "Same Type" option, all 3 bars that formed the FVG should be the same type. (Bullish / Bearish). If the "All" option is selected, bar types may vary between Bullish / Bearish.

Detection Sensitivity -> You may select between Low, Normal or High FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivies resulting in spotting bigger FVGs, and higher sensitivies resulting in spotting all sizes of FVGs.

Relative Strength Scoring SystemRelative Strength Scoring System :

Important prerequisite :

This indicator can be loaded on any forex chart, i.e. a currency pair, but must not be loaded on any other asset due to certain market closures.

The chart timeframe must be less than or equal to the trading timeframe, which is the indicator's first parameter. A timeframe equal to that of the "Trading Timeframe" parameter is preferable.

Introduction :

This indicator measures the relative strength of a currency against all other currencies using spread formulas. It gives an indication of which currencies are bullish, neutral or bearish. The ultimate aim of this indicator is to find out which pair will generate a higher probability of gain than the others by pairing the most bullish pair with the most bearish pair.

Spread formulas :

To find the relative strength of a currency compared with others, we use the following spreads formulas :

USD = (FX:USDJPY/100+SAXO:USDEUR+FX:USDCHF+SAXO:USDGBP+FX:USDCAD+SAXO:USDAUD+FX_IDC:USDNZD)/7

JPY = (SAXO:JPYUSD/100+FX_IDC:JPYAUD/100+FX_IDC:JPYCAD/100+FX_IDC:JPYNZD/100+FX_IDC:JPYCHF/100+SAXO:JPYEUR/100+FX_IDC:JPYGBP/100)/7

CHF = (FX:CHFJPY/100+SAXO:CHFUSD+SAXO:CHFEUR+FX_IDC:CHFGBP+FX_IDC:CHFCAD+SAXO:CHFAUD+FX_IDC:CHFNZD)/7

EUR = (FX:EURJPY/100+FX:EURUSD+FX:EURCHF+FX:EURGBP+FX:EURCAD+FX:EURAUD+FX:EURNZD)/7

GBP = (FX:GBPJPY/100+FX:GBPUSD+FX:GBPCHF+SAXO:GBPEUR+FX:GBPCAD+FX:GBPAUD+FX:GBPNZD)/7

CAD = (FX:CADJPY/100+SAXO:CADUSD+FX:CADCHF+FX_IDC:CADGBP+SAXO:CADEUR+FX_IDC:CADAUD+FX_IDC:CADNZD)/7

AUD = (FX:AUDJPY/100+FX:AUDUSD+FX:AUDCHF+SAXO:AUDGBP+FX:AUDCAD+SAXO:AUDEUR+FX:AUDNZD)/7

NZD = (FX:NZDJPY/100+FX:NZDUSD+FX:NZDCHF+SAXO:NZDGBP+FX:NZDCAD+SAXO:NZDAUD+SAXO:NZDEUR)/7

CRYPTO = (BITSTAMP:BTCUSD+BITSTAMP:ETHUSD+BITSTAMP:LTCUSD+BITSTAMP:BCHUSD)/4

Timeframes :

As mentioned in the prerequisites, the chart timeframe must not be greater than the trading timeframe. The latter corresponds to the timeframe chosen by the trader to enter a position, and is the indicator's first parameter. Once this has been chosen, the algorithm selects the timeframes of the "Trend" and "Velocity" charts. Here's how it allocates them :

Trading TF => ("Velocity TF", "Trend TF")

"5min" => ("15min ", "60min")

"15min" => ("60min ", "4h")

"30min" => ("2h ", "8h")

"60min" => ("4h ", "12h")

"4h" => ("12h", "1D")

"6h" => ("1D", "3D")

"8h" => ("1D", "4D")

"12h" => ("2D", "1W")

"1D" => ("3D", "1W")

Trend Scoring System :

When the timeframe of the trend graph has been allocated, the algorithm will establish this graph's score using three criteria :

Trend chart pivot points: if the last two pivots, high and low, are increasing, the score is 1; if they are decreasing, the score is -1; else the score is 0.

SMA: if its slope is increasing with a candle strictly above the SMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

MACD: if the MACD is positive, the score is 1, if it is negative, the score is -1; else it's 0.

We then sum the scores of these three criteria to find the trend score.

Velocity Scoring System :

In the same way, we analyze the score of the "velocity" graph with its corresponding timeframe using three criteria :

The EMA: if its slope is increasing with a candle strictly above the EMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

The RSI: if the RSI's EMA has an increasing slope with an RSI strictly greater than the value of this EMA, the score is 1; and if the RSI's EMA has a decreasing slope with an RSI strictly less than this EMA, the score is -1; otherwise it is 0.

SAR parabolic: if the SAR is below the price, the score is 1; if it is above the price, the score is -1.

We then sum the scores of these three criteria to find the velocity score.

Relative Strength Scoring System :

Once the trend score and velocity score have been calculated, we determine the relative strength score of each currency using the following algorithm :

If trend score >=2 and velocity score >=2, the currency is bullish.

If trend score <=2 and velocity score <=2, currency is bearish

If (trendScore>=2 or velocityScore>=2) and (trendScore=1 or velocityScore=1) the currency is not yet bullish

If (trendScore<=2 or velocityScore<=2) and (trendScore=-1 or velocityScore=-1) the currency is not yet bearish.

Otherwise the currency is neutral

Parameters :

Trading Timeframe: the trading timeframe chosen by the trader for which he makes his position entry and exit decisions. Default is 1h

Pivot Legs: Parameter used for the chart "Trend" setting the pivot strength to the right and left of high/low. Default is 2

SMA Length: SMA length of the chart "Trend". Default is 20

MACD Fast Length: Length of the MACD fast SMA calculated on the chart "Trend". Default is 12

MACD Slow Length: Length of the MACD slow SMA calculated on the chart "Trend". Default is 26

MACD Signal Length: Length of the MACD signal SMA calculated on the chart "Trend". Default is 9

EMA Length: EMA length of the "Velocity" graph. Default is 13

RSI Length: RSI length of the "Velocity" graph. Default is 14

RSI EMA Length: Length of the RSI EMA. Default is 9

Parabolic SAR Start: Start of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Increment: Increment of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Max: Maximum of the SAR parabola in the "Velocity" graph. Default is 0.2

Conclusion :

This indicator has been designed to determine the relative strength of the major currencies against each other. The aim is to know which pair to trade at the right time in order to maximize the probability of a successful trade. For example, if the USD is bullish and the NZD bearish, we'll short the NZDUSD pair.

Enjoy this indicator and don't forget to take the trade ;)

Vo-S-Di-T-I - Volatility Scaled Directional Trend IndicatorThis code represents just the foundation for what's to come. It lays the groundwork for a more sophisticated quant trading model, offering a glimpse into the potential of future developments. I hope my contribution to this community will be valued. I'm here for idea exchanges and coding together, with the key emphasis on ensuring everything we do is grounded on a solid statistical basis.

----------------------------------------------------------------------------------------------------------------------

The developed code is based on a rigorous quantitative approach for analyzing price trends in the equity sector, utilizing advanced statistical methodology to scale returns based on the volatility observed over predefined periods of 20 and 50 days. This technique for normalizing returns allows us to eliminate distortions due to the intrinsic variability of prices and focus on the underlying structure of price behavior. The primary goal of the code is not to speculatively predict future market movements but rather to identify potential reversal trend signals through price dynamics analysis, within an optimized risk and return context.

Our approach is distinguished by the use of statistical decomposition techniques and time series analysis to interpret price variations as indicators of possible shifts in market behavior. This allows distinguishing between random or short-term price movements and true trend changes, providing a solid foundation for more informed investment decisions.

The current code represents the initial phase of a broader project that envisages the integration of machine learning algorithms to further refine the ability to detect significant changes in price trends. Through the application of predictive models and machine learning techniques, we intend to explore complex patterns in historical price data that may precede trend reversals, always respecting the principles of rigorous statistical analysis and risk management. This development and learning path will allow us to continuously improve investment strategies, leveraging the analytical capabilities of modern data science algorithms applied to the financial sector.

HOW TO READ

Simply put, Z values above 0 indicate an uptrend, while values below indicate a downtrend. IMPORTANT: It is not necessary to consider any crosses between Z-Short and Z-Long, but only potential crosses with 0.

The initial values are set at 20 and 50, but everyone is free to choose the most suitable periods, as long as all choices have valid statistical significance. My advice is to use R or MatLab to explore the best correlation between N and price movements. The reason I have set two values for N (Short and Long) is because it's interesting to assess short-term and medium-to-long-term trends to understand if price movements can lead to reversals only in the short term or also in the medium to long term. This idea came to me because I believe all other trend determination systems have too much lag and unpredictability.

Flags and Pennants [Trendoscope®]🎲 An extension to Chart Patterns based on Trend Line Pairs - Flags and Pennants

After exploring Algorithmic Identification and Classification of Chart Patterns and developing Auto Chart Patterns Indicator , we now delve into extensions of these patterns, focusing on Flag and Pennant Chart Patterns. These patterns evolve from basic trend line pair-based structures, often influenced by preceding market impulses.

🎲 Identification rules for the Extension Patterns

🎯 Identify the existence of Base Chart Patterns

Before identifying the flag and pennant patterns, we first need to identify the existence of following base trend line pair based converging or parallel patterns.

Ascending Channel

Descending Channel

Rising Wedge (Contracting)

Falling Wedge (Contracting)

Converging Triangle

Descending Triangle (Contracting)

Ascending Triangle (Contracting)

🎯 Identifying Extension Patterns.

The key to pinpointing these patterns lies in spotting a strong impulsive wave – akin to a flagpole – preceding a base pattern. This setup suggests potential for an extension pattern:

A Bullish Flag emerges from a positive impulse followed by a descending channel or a falling wedge

A Bearish Flag appears after a negative impulse leading to an ascending channel or a rising wedge.

A Bullish Pennant is indicated by a positive thrust preceding a converging triangle or ascending triangle.

A Bearish Pennant follows a negative impulse and a converging or descending triangle.

🎲 Pattern Classifications and Characteristics

🎯 Bullish Flag Pattern

Characteristics of Bullish Flag Pattern are as follows

Starts with a positive impulse wave

Immediately followed by either a short descending channel or a falling wedge

Here is an example of Bullish Flag Pattern

🎯 Bearish Flag Pattern

Characteristics of Bearish Flag Pattern are as follows

Starts with a negative impulse wave

Immediately followed by either a short ascending channel or a rising wedge

Here is an example of Bearish Flag Pattern

🎯 Bullish Pennant Pattern

Characteristics of Bullish Pennant Pattern are as follows

Starts with a positive impulse wave

Immediately followed by either a converging triangle or ascending triangle pattern.

Here is an example of Bullish Pennant Pattern

🎯 Bearish Pennant Pattern

Characteristics of Bearish Pennant Pattern are as follows

Starts with a negative impulse wave

Immediately followed by either a converging triangle or a descending converging triangle pattern.

Here is an example of Bearish Pennant Pattern

🎲 Trading Extension Patterns

In a strong market trend, it's common to see temporary periods of consolidation, forming patterns that either converge or range, often counter to the ongoing trend direction. Such pauses may lay the groundwork for the continuation of the trend post-breakout. The assumption that the trend will resume shapes the underlying bias of Flag and Pennant patterns

It's important, however, not to base decisions solely on past trends. Conducting personal back testing is crucial to ascertain the most effective entry and exit strategies for these patterns. Remember, the behavior of these patterns can vary significantly with the volatility of the asset and the specific timeframe being analyzed.

Approach the interpretation of these patterns with prudence, considering that market dynamics are subject to a wide array of influencing factors that might deviate from expected outcomes. For investors and traders, it's essential to engage in thorough back testing, establishing entry points, stop-loss orders, and target goals that align with your individual trading style and risk appetite. This step is key to assessing the viability of these patterns in line with your personal trading strategies and goals.

It's fairly common to witness a breakout followed by a swift price reversal after these patterns have formed. Additionally, there's room for innovation in trading by going against the bias if the breakout occurs in the opposite direction, specially when the trend before the formation of the pattern is in against the pattern bias.

🎲 Cheat Sheet

🎲 Indicator Settings

Custom Source : Enables users to set custom OHLC - this means, the indicator can also be applied on oscillators and other indicators having OHLC values.

Zigzag Settings : Allows users to enable different zigzag base and set length and depth for each zigzag.

Scanning Settings : Pattern scanning settings set some parameters that define the pattern recognition process.

Display Settings : Determine the display of indicators including colors, lines, labels etc.

Backtest Settings : Allows users to set a predetermined back test bars so that the indicator will not time out while trying to run for all available bars.

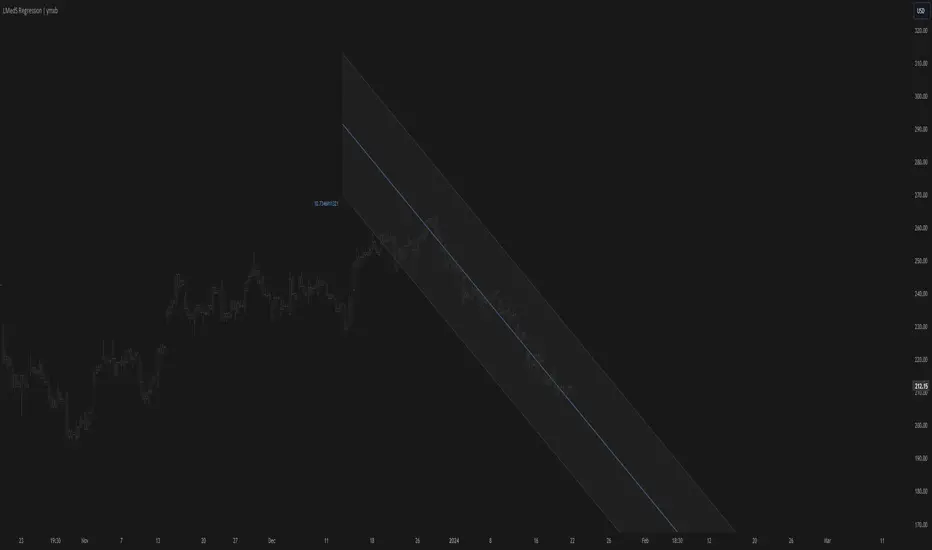

Least Median of Squares Regression | ymxbThe Least Median of Squares (LMedS) is a robust statistical method predominantly used in the context of regression analysis. This technique is designed to fit a model to a dataset in a way that is resistant to outliers. Developed as an alternative to more traditional methods like Ordinary Least Squares (OLS) regression, LMedS is distinguished by its focus on minimizing the median of the squares of the residuals rather than their mean. Residuals are the differences between observed and predicted values.

The key advantage of LMedS is its robustness against outliers. In contrast to methods that minimize the mean squared residuals, the median is less influenced by extreme values, making LMedS more reliable in datasets where outliers are present. This is particularly useful in linear regression, where it identifies the line that minimizes the median of the squared residuals, ensuring that the line is not overly influenced by anomalies.

STATISTICAL PROPERTIES

A critical feature of the LMedS method is its robustness, particularly its resilience to outliers. The method boasts a high breakdown point, which is a measure of an estimator's capacity to handle outliers. In the context of LMedS, this breakdown point is approximately 50%, indicating that it can tolerate corruption of up to half of the input data points without a significant degradation in accuracy. This robustness makes LMedS particularly valuable in real-world data analysis scenarios, where outliers are common and can severely skew the results of less robust methods.

Rousseeuw, Peter J.. “Least Median of Squares Regression.” Journal of the American Statistical Association 79 (1984): 871-880.

The LMedS estimator is also characterized by its equivariance under linear transformations of the response variable. This means that whether you transform the data first and then apply LMedS, or apply LMedS first and then transform the data, the end result remains consistent. However, it's important to note that LMedS is not equivariant under affine transformations of both the predictor and response variables.

ALGORITHM

The algorithm randomly selects pairs of points, calculates the slope (m) and intercept (b) of the line, and then evaluates the median squared deviation (mr2) from this line. The line minimizing this median squared deviation is considered the best fit.

DISCLAIMER

In the LMedS approach, a subset of the data is randomly selected to compute potential models (e.g., lines in linear regression). The method then evaluates these models based on the median of the squared residuals. Since the selection of data points is random, different runs may select different subsets, leading to variability in the computed models.

Qu_Trend+

composition

- Consists of a thick trend line and a thin yellow line.

- The largest (green/red) lines indicate rising and falling markets.

- This line represents the 13-candle moving average of Tilson T3.

- The reason for 13 candles is because it best matches the recent market price based on Bitcoin.

- This value cannot be changed, so if you need it, please modify the public code and use it.

- The yellow line is the MA20 line, the ‘Bollinger Band center line’

(UI will show whether this line has been breakout)

- The same algorithm as 20 of the basic moving average (close standard) is applied.

- The algorithm for breakthrough is calculated based on real-time prices, not based on closing prices.

An additional short-term SMA is created, and whether it crosses the SMA is classified as a breakout/resistance.

How to use it

- If the trend line becomes gentle, it may indicate a change in trend when + MA20 is broken.

- While the slope of the trend line is steep, it indicates that the trend is difficult to change.

(If the trend changes at this time, it is likely to move sideways)

- If the trend changes continuously, it is a sideways market.

At this time, watch out for the movement of the end point where the sideways trend ends.

Multi-Timeframe Recursive Zigzag [Trendoscope®]🎲 Welcome to the Advanced World of Zigzag Analysis

Embark on a journey through the most comprehensive and feature-rich Zigzag implementation you’ll ever encounter. Our Multi-Timeframe Recursive Zigzag Indicator is not just another tool; it's a groundbreaking advancement in technical analysis.

🎯 Key Features

Multi Time-Frame Support - One of the rare open-source Zigzag indicators with robust multi-timeframe capabilities, this feature sets our tool apart, enabling a broader and more dynamic market analysis.

Innovative Recursive Zigzag Algorithm - At its core is our unique Recursive Zigzag Algorithm, a pioneering development that powers multiple Zigzag levels, offering an intricate view of market movements. This proprietary algorithm is the backbone of our advanced pattern recognition indicators.

Sub-Waves and Micro-Waves Analysis - Dive deeper into market trends with our Sub-Waves and Micro-Waves feature. Sub-Waves reveal the interconnectedness of various Zigzag levels, while Micro-Waves offer insight into the fundamental waves at the base level.

Enhanced Indicator Tracking - Integrate and track your custom indicators or oscillators with the zigzag, capturing their values at each Zigzag level, complete with retracement ratios. This offers a comprehensive view of market dynamics.

Curved Zigzag Visualization - Experience a new way of visualizing market movements with our Curved Zigzag Display, employing Pine Script’s polyline feature for a more intuitive and visually appealing representation.

Built-in Customizable Alerts - Stay ahead with built-in alerts that can be customized via user input settings.

🎯 Practical Applications

Our Zigzag Indicator is designed with an understanding of its inherent nature - the last unconfirmed pivot that consistently repaints. This characteristic, while by design, directs its usage more towards pattern recognition rather than direct identification of market tops and bottoms. Here's how you can leverage the Zigzag Indicator:

Harmonic Patterns - Ideal for those familiar with harmonic patterns, this tool simplifies the manual spotting of complex XABCD, ABC, and ABCD patterns on charts.

Chart Patterns - Effortlessly identify patterns like Double/Triple Taps, Head and Shoulders, Inverse Head and Shoulders, and Cup and Handle patterns with enhanced clarity. Navigate through challenging patterns such as Triangles, Wedges, Flags, and Price Channels, where the Zigzag Indicator adds a layer of precision to your breakout strategy.

Elliott Wave Components - The indicator's detailed pivot highlighting aids in identifying key Elliott Wave components, enhancing your wave analysis and decision-making process.

🎲 Deep Dive into Indicator Features

Join us as we explore the intricate features of our indicator in more detail.

🎯 Multi-Timeframe Capability

Our indicator comes equipped with an input option for selecting the desired resolution. This unique feature allows users to view higher timeframe Zigzag patterns directly on their lower timeframe charts.

🎯 Recursive Multi Level Zigzag

Our advanced recursive approach creates multi-level Zigzags from lower-level data. For instance, the level 0 Zigzag forms the base, calculated from specified length and depth parameters, while level 1 Zigzag is derived using level 0 as its foundation, and so forth.

The indicator not only displays multiple Zigzag levels but also offers settings to emphasize specific levels for more detailed analysis.

🎯 Sub-Components and Micro-Components of Zigzag Wave

Sub-components within a Zigzag wave consist of the previous level's Zigzag pivots. Meanwhile, the micro-components are composed of the base level (Level 0) Zigzag pivots encapsulated within the wave.

🎯 Curved Zigzag

Experience a new perspective with our curved Zigzag display. This innovative feature utilizes the polyline curved option to automatically generate sinusoidal waves based on multiple points.

🎯 Indicator Tracking

Default indicators such as RSI, MFI, and OBV are included, alongside the ability to track one external indicator at each Zigzag pivot.

🎯 Customizable Alerts

Our indicator employs the `alert()` function for alert creation. While this means the absence of a customization text box in the alert settings, we've included a custom text area for users to create their own alert templates.

Template placeholders include:

{alertType} - type of alert. Either Confirmed Pivot Update or Last Pivot Update. Depends on the alert type selected in the inputs.

When Last Pivot Update type is selected, the alerts are triggered whenever there is a new Zigzag Pivot. This may also be a repaint of last unconfirmed pivot.

When Confirmed Pivot Update type is selected, the alerts are triggered only when a pivot becomes a confirmed pivot.

{level} - Zigzag level on which the alert is triggered.

{pivot} - Details of the last pivot or confirmed pivot including price, ratio, indicator values and ratios, subcomponent and micro-component pivots.

🎲 User Settings Overview

🎯 Zigzag and Generic Settings

This involves some generic zigzag calculation settings such as length, depth, and timeframe. And few display options such as theme, Highlight Level and Curved Zigzag. By default, zigzag calculation is done based on the latest real time bar. An option is provided to disable this and use only confirmed bars for the calculation.

Indicator Settings

Allows users to track one or more oscillators or volume indicators. Option to add any indicator via external input is provided.

🎯 Alert Settings

Has input fields required to select and customize alerts.

SuperTrend ToolkitThe SuperTrend Toolkit (Super Kit) introduces a versatile approach to trend analysis by extending the application of the SuperTrend indicator to a wide array of @TradingView's built-in or Community Scripts . This tool facilitates the integration of the SuperTrend algorithm with various indicators, including oscillators, moving averages, overlays, and channels.

Methodology:

The SuperTrend, at its core, calculates a trend-following indicator based on the Average-True-Range (ATR) and price action. It creates dynamic support and resistance levels, adjusting to changing market conditions, and aiding in trend identification.

pine_st(simple float factor = 3., simple int length = 10) =>

float atr = ta.atr(length)

float up = hl2 + factor * atr

up := up < nz(up ) or close > nz(up ) ? up : nz(up )

float lo = hl2 - factor * atr

lo := lo > nz(lo ) or close < nz(lo ) ? lo : nz(lo )

int dir = na

float st = na

if na(atr )

dir := 1

else if st == nz(up )

dir := close > up ? -1 : 1

else

dir := close < lo ? 1 : -1

st := dir == -1 ? lo : up

@TradingView's native SuperTrend lacks the flexibility to incorporate different price sources into its calculation.

Community scripts, addressed the limitation by implementing the option to input different price sources, for example, one of the most popular publications, @KivancOzbilgic's SuperTrend script.

In May 2023, @TradingView introduced an update allowing the passing of another indicator's plot as a source value via the input.source() function. However, the built-in ta.atr function still relied on the chart's price data, limiting the formerly mentioned scripts to the chart's price data alone.

Unique Approach -

This script addresses the aforementioned limitations by processing the data differently.

Firstly we create a User-Defined-Type (UDT) replicating a bar's open, high, low, close (OHLC) values.

type bar

float o = open

float h = high

float l = low

float c = close

We then use this type to store the external input data.

src = input.source(close, "External Source")

bar b = bar.new(

nz(src ) , open 𝘷𝘢𝘭𝘶𝘦

math.max(nz(src ), src), high 𝘷𝘢𝘭𝘶𝘦

math.min(nz(src ), src), low 𝘷𝘢𝘭𝘶𝘦

src ) close 𝘷𝘢𝘭𝘶𝘦

Finally, we pass the data into our custom built SuperTrend with ATR functions to derive the external source's version of the SuperTrend indicator.

supertrend st = b.st(mlt, len)

- Setup Guide -

Utility and Use Cases:

Universal Compatibility - Apply SuperTrend to any built-in indicator or script, expanding its use beyond traditional price data.

- A simple example on one of my own public scripts -

Trend Analysis - Gain additional trend insights into otherwise mainly mean reverting or volume indicators.

- Alerts Setup Guide -

The Super Kit empowers traders and analysts with a tool that adapts the robust SuperTrend algorithm to a myriad of indicators, allowing comprehensive trend analysis and strategy development.

Multi-TF AI SuperTrend with ADX - Strategy [PresentTrading]

## █ Introduction and How it is Different

The trading strategy in question is an enhanced version of the SuperTrend indicator, combined with AI elements and an ADX filter. It's a multi-timeframe strategy that incorporates two SuperTrends from different timeframes and utilizes a k-nearest neighbors (KNN) algorithm for trend prediction. It's different from traditional SuperTrend indicators because of its AI-based predictive capabilities and the addition of the ADX filter for trend strength.

BTC 8hr Performance

ETH 8hr Performance

## █ Strategy, How it Works: Detailed Explanation (Revised)

### Multi-Timeframe Approach

The strategy leverages the power of multiple timeframes by incorporating two SuperTrend indicators, each calculated on a different timeframe. This multi-timeframe approach provides a holistic view of the market's trend. For example, a 8-hour timeframe might capture the medium-term trend, while a daily timeframe could capture the longer-term trend. When both SuperTrends align, the strategy confirms a more robust trend.

### K-Nearest Neighbors (KNN)

The KNN algorithm is used to classify the direction of the trend based on historical SuperTrend values. It uses weighted voting of the 'k' nearest data points. For each point, it looks at its 'k' closest neighbors and takes a weighted average of their labels to predict the current label. The KNN algorithm is applied separately to each timeframe's SuperTrend data.

### SuperTrend Indicators

Two SuperTrend indicators are used, each from a different timeframe. They are calculated using different moving averages and ATR lengths as per user settings. The SuperTrend values are then smoothed to make them suitable for KNN-based prediction.

### ADX and DMI Filters

The ADX filter is used to eliminate weak trends. Only when the ADX is above 20 and the directional movement index (DMI) confirms the trend direction, does the strategy signal a buy or sell.

### Combining Elements

A trade signal is generated only when both SuperTrends and the ADX filter confirm the trend direction. This multi-timeframe, multi-indicator approach reduces false positives and increases the robustness of the strategy.

By considering multiple timeframes and using machine learning for trend classification, the strategy aims to provide more accurate and reliable trade signals.

BTC 8hr Performance (Zoom-in)

## █ Trade Direction

The strategy allows users to specify the trade direction as 'Long', 'Short', or 'Both'. This is useful for traders who have a specific market bias. For instance, in a bullish market, one might choose to only take 'Long' trades.

## █ Usage

Parameters: Adjust the number of neighbors, data points, and moving averages according to the asset and market conditions.

Trade Direction: Choose your preferred trading direction based on your market outlook.

ADX Filter: Optionally, enable the ADX filter to avoid trading in a sideways market.

Risk Management: Use the trailing stop-loss feature to manage risks.

## █ Default Settings

Neighbors (K): 3

Data points for KNN: 12

SuperTrend Length: 10 and 5 for the two different SuperTrends

ATR Multiplier: 3.0 for both

ADX Length: 21

ADX Time Frame: 240

Default trading direction: Both

By customizing these settings, traders can tailor the strategy to fit various trading styles and assets.

[Library] VAccThis is the library version of VAcc (Velocity & Acceleration), a momentum indicator published by Scott Cong in Stocks & Commodities V. 41:09 (8–15). It applies concepts from physics, namely velocity and acceleration, to financial markets. VAcc functions similarly to the popular MACD (Moving Average Convergence Divergence) indicator when using a longer lookback period, but produces more responsive results. With shorter periods, VAcc exhibits characteristics reminiscent of the stochastic oscillator.

The indicator version of this algorithm is linked below:

🟠 Algorithm

The average velocity over the past n periods is defined as

((C - C_n) / n + (C - C_{n-1}) / (n - 1) + … + (C - C_i) / i + (C - C_1) / 1) / n

At its core, the velocity is a weighted average of the rate of change over the past n periods.

The calculation of the acceleration follows a similar process, where it’s defined as

((V - V_n) / n + (V - V_{n - 1}) / (n - 1) + … + (V - V_i) / i + (V - V_1) / 1) / n

🟠 Comparison with MACD

A comparison of VAcc and MACD on the daily Nasdaq 100 (NDX) chart from August 2022 helps demonstrate VAcc's improved sensitivity. Both indicators utilized a lookback period of 26 days and smoothing of 9 periods.

The VAcc histogram clearly shows a divergence forming, with momentum weakening as prices reached new highs. In contrast, the corresponding MACD histogram significantly lagged in confirming the divergence, highlighting VAcc's ability to identify subtle shifts in trend momentum more immediately than the traditional MACD.

AI SuperTrend - Strategy [presentTrading]

█ Introduction and How it is Different

The AI Supertrend Strategy is a unique hybrid approach that employs both traditional technical indicators and machine learning techniques. Unlike standard strategies that rely solely on traditional indicators or mathematical models, this strategy integrates the power of k-Nearest Neighbors (KNN), a machine learning algorithm, with the tried-and-true SuperTrend indicator. This blend aims to provide traders with more accurate, responsive, and context-aware trading signals.

*The KNN part is mainly referred from @Zeiierman.

BTCUSD 8hr performance

ETHUSD 8hr performance

█ Strategy, How it Works: Detailed Explanation

SuperTrend Calculation

Volume-Weighted Moving Average (VWMA): A VWMA of the close price is calculated based on the user-defined length (len). This serves as the central line around which the upper and lower bands are calculated.

Average True Range (ATR): ATR is calculated over a period defined by len. It measures the market's volatility.

Upper and Lower Bands: The upper band is calculated as VWMA + (factor * ATR) and the lower band as VWMA - (factor * ATR). The factor is a user-defined multiplier that decides how wide the bands should be.

KNN Algorithm

Data Collection: An array (data) is populated with recent n SuperTrend values. Corresponding labels (labels) are determined by whether the weighted moving average price (price) is greater than the weighted moving average of the SuperTrend (sT).

Distance Calculation: The absolute distance between each data point and the current SuperTrend value is calculated.

Sorting & Weighting: The distances are sorted in ascending order, and the closest k points are selected. Each point is weighted by the inverse of its distance to the current point.

Classification: A weighted sum of the labels of the k closest points is calculated. If the sum is closer to 1, the trend is predicted as bullish; if closer to 0, bearish.

Signal Generation

Start of Trend: A new bullish trend (Start_TrendUp) is considered to have started if the current trend color is bullish and the previous was not bullish. Similarly for bearish trends (Start_TrendDn).

Trend Continuation: A bullish trend (TrendUp) is considered to be continuing if the direction is negative and the KNN prediction is 1. Similarly for bearish trends (TrendDn).

Trading Logic

Long Condition: If Start_TrendUp or TrendUp is true, a long position is entered.

Short Condition: If Start_TrendDn or TrendDn is true, a short position is entered.

Exit Condition: Dynamic trailing stops are used for exits. If the trend does not continue as indicated by the KNN prediction and SuperTrend direction, an exit signal is generated.

The synergy between SuperTrend and KNN aims to filter out noise and produce more reliable trading signals. While SuperTrend provides a broad sense of the market direction, KNN refines this by predicting short-term price movements, leading to a more nuanced trading strategy.

Local picture

█ Trade Direction

The strategy allows traders to choose between taking only long positions, only short positions, or both. This is particularly useful for adapting to different market conditions.

█ Usage

ToolTips: Explains what each parameter does and how to adjust them.

Inputs: Customize values like the number of neighbors in KNN, ATR multiplier, and moving average type.

Plotting: Visual cues on the chart to indicate bullish or bearish trends.

Order Execution: Based on the generated signals, the strategy will execute buy/sell orders.

█ Default Settings

The default settings are selected to provide a balanced approach, but they can be modified for different trading styles and asset classes.

Initial Capital: $10,000

Default Quantity Type: 10% of equity

Commission: 0.1%

Slippage: 1

Currency: USD

By combining both machine learning and traditional technical analysis, this strategy offers a sophisticated and adaptive trading solution.

Elliott Wave with Supertrend Exit - Strategy [presentTrading]## Introduction and How it is Different

The Elliott Wave with Supertrend Exit provides automated detection and validation of Elliott Wave patterns for algorithmic trading. It is designed to objectively identify high-probability wave formations and signal entries based on confirmed impulsive and corrective patterns.

* The Elliott part is mostly referenced from Elliott Wave by @LuxAlgo

Key advantages compared to discretionary Elliott Wave analysis:

- Wave Labeling and Counting: The strategy programmatically identifies swing pivot highs/lows with the Zigzag indicator and analyzes the waves between them. It labels the potential impulsive and corrective patterns as they form. This removes the subjectivity of manual wave counting.

- Pattern Validation: A rules-based engine confirms valid impulsive and corrective patterns by checking relative size relationships and fib ratios. Only confirmed wave counts are plotted and traded.

- Objective Entry Signals: Trades are entered systematically on the start of new impulsive waves in the direction of the trend. Pattern failures invalidate setups and stop out positions.

- Automated Trade Management: The strategy defines specific rules for profit targets at fib extensions, trailing stops at swing points, and exits on Supertrend reversals. This automates the entire trade lifecycle.

- Adaptability: The waveform recognition engine can be tuned by adjusting parameters like Zigzag depth and Supertrend settings. It adapts to evolving market conditions.

ETH 1hr chart

In summary, the strategy brings automation, objectivity and adaptability to Elliott Wave trading - removing subjective interpretation errors and emotional trading biases. It implements a rules-based, algorithmic approach for systematically trading Elliott Wave patterns across markets and timeframes.

## Trading Logic and Rules

The strategy follows specific trading rules based on the detected and validated Elliott Wave patterns.

Entry Rules

- Long entry when a new impulsive bullish (5-wave) pattern forms

- Short entry when a new impulsive bearish (5-wave) pattern forms

The key is entering on the start of a new potential trend wave rather than chasing.

Exit Rules

- Invalidation of wave pattern stops out the trade

- Close long trades on Supertrend downturn

- Close short trades on Supertrend upturn

- Use a stop loss of 10% of entry price (configurable)

Trade Management

- Scale out partial profits at Fibonacci levels

- Move stop to breakeven when price reaches 1.618 extension

- Trail stops below key swing points

- Target exits at next Fibonacci projection level

Risk Management

- Use stop losses on all trades

- Trade only highest probability setups

- Size positions according to chart timeframe

- Avoid overtrading when no clear patterns emerge

## Strategy - How it Works

The core logic follows these steps:

1. Find swing highs/lows with Zigzag indicator

2. Analyze pivot points to detect impulsive 5-wave patterns:

- Waves 1, 3, and 5 should not overlap

- Waves 3 and 5 must be longer than wave 1

- Confirm relative size relationships between waves

3. Validate corrective 3-wave patterns:

- Look for overlapping, choppy waves that retrace the prior impulsive wave

4. Plot validated waves and Fibonacci retracement levels

5. Signal entries when a new impulsive wave pattern forms

6. Manage exits based on pattern failures and Supertrend reversals

Impulsive Wave Validation

The strategy checks relative size relationships to confirm valid impulsive waves.

For uptrends, it ensures:

```

Copy code- Wave 3 is longer than wave 1

- Wave 5 is longer than wave 2

- Waves do not overlap

```

Corrective Wave Validation

The strategy identifies overlapping corrective patterns that retrace the prior impulsive wave within Fibonacci levels.

Pattern Failure Invalidation

If waves fail validation tests, the strategy invalidates the pattern and stops signaling trades.

## Trade Direction

The strategy detects impulsive and corrective patterns in both uptrends and downtrends. Entries are signaled in the direction of the validated wave pattern.

## Usage

- Use on charts showing clear Elliott Wave patterns

- Start with daily or weekly timeframes to gauge overall trend

- Optimize Zigzag and Supertrend settings as needed

- Consider combining with other indicators for confirmation

## Default Settings

- Zigzag Length: 4 bars

- Supertrend Length: 10 bars

- Supertrend Multiplier: 3

- Stop Loss: 10% of entry price

- Trading Direction: Both

Pullback AnalyzerPullback Analyzer - a trailing stop helper.

This indicator measures the biggest pullback encountered during an up or down move.

You can use the reported percentages to fine-tune your trailing stop.

The reporting is very precise: On higher timeframes, the pullback size can sometimes not be determined exactly from the candles.

In this case, the script displays a lower and upper bound for this number.

I suggest that you use the upper bound as your trailing stop callback rate (plus some safety margin if you like).

The size of the move itself is always reported as a lower bound.

The biggest pullback within each move is marked with a gray dotted line.

There is only one parameter, "lookback"' (or lookback limit), which determines how many bars a single move can comprise. A value of 50 was found to be a nice default. If you lower the lookback, long moves will be split up into multiple moves, each being at or below the lookback limit. Conversely, you can capture longer moves in one piece by raising the lookback limit.

The algorithm automatically ignores small moves and trading ranges near a bigger move. (We may add a parameter to control this behavior more precisely in the future.)

How the algorithm works

There is a central class called MoveFinder which scans the candle feed for the biggest possible move in a certain direction (up or down).

Two instances of this class are used, one for each direction, to find the biggest next up and down move simultaneously (upFinder and downFinder).

Additionally, each of these main MoveFinders contains two more MoveFinders. These are used to find pullbacks within the move. (This comes from the observation that finding a pullback is fundamentally the exact same operation as finding a move, just with opposing direction and limited to the time between the move's beginning and end.)

Why two nested MoveFinders per parent (for a total of 6 in the program)? Well, one of them runs in "lower bound" and one runs in "upper bound" mode, so we can print the detected pullback size as an exact interval (lower bound <= real pullback <= upper bound). I am a mathematician. I like precision.

Moves as well as pullbacks that have been found are stored as instances of class Move which simply stores start and end bar index as well as start and end price.

REVE Cohorts - Range Extension Volume Expansion CohortsREVE Cohorts stands for Range Extensions Volume Expansions Cohorts.

Volume is divided in four cohorts, these are depicted in the middle band with colors and histogram spikes.

0-80 percent i.e. low volumes; these get a green color and a narrow histogram bar

80-120 percent, normal volumes, these get a blue color and a narrow histogram bar

120-200 percent, high volume, these get an orange color and a wide histogram bar

200 and more percent is extreme volume, maroon color and wide bar.

All histogram bars have the same length. They point to the exact candle where the volume occurs.

Range is divided in two cohorts, these are depicted as candles above and below the middle band.

0-120 percent: small and normal range, depicted as single size, square candles

120 percent and more, wide range depicted as double size, rectangular candles.

The range candles are placed and colored according to the Advanced Price Algorithm (published script). If the trend is up, the candles are in the uptrend area, which is above the volume band, , downtrend candles below in the downtrend area. Dark blue candles depict a price movement which confirms the uptrend, these are of course in the uptrend area. In this area are also light red candles with a blue border, these depict a faltering price movement countering the uptrend. In the downtrend area, which is below the volume band, are red candles which depict a price movement confirming the downtrend and light blue candles with a red border depicting price movement countering the downtrend. A trend in the Advanced Price Algorithm is in equal to the direction of a simple moving average with the same lookback. The indicator has the same lagging.as this SMA.

Signals are placed in the vacated spaces, e.g. during an uptrend the downtrend area is vacated.

There are six signals, which arise as follows:

1 Two blue triangles up on top of each other: high or extreme volume in combination with wide range confirming uptrend. This indicates strong and effective up pressure in uptrend

2 Two pink tringles down on top of each other: high or extreme volume in combination with wide range down confirming downtrend. This indicates strong and effective down pressure in downtrend

3 Blue square above pink down triangle down: extreme volume in combination with wide range countering uptrend. This indicates a change of heart, down trend is imminent, e.g. during a reversal pattern. Down Pressure in uptrend

4 Pink square below blue triangle up: extreme volume in combination with wide range countering downtrend. This indicates a change of heart, reversal to uptrend is imminent. Up Pressure in downtrend

5 single blue square: a. extreme volume in combination with small range confirming uptrend, b. extreme volume in combination with small range countering downtrend, c. high volume in combination with wide range countering uptrend. This indicates halting upward price movement, occurs often at tops or during distribution periods. Unresolved pressure in uptrend

6 Single pink square: a extreme volume in combination with small range confirming downtrend, b extreme volume in combination with small range countering uptrend, c high volume in combination with wide range countering downtrend. This indicated halting downward price movement. Occurs often at bottoms or during accumulation periods. Unresolved pressure in downtrend.

The signals 5 and 6 are introduced to prevent flipping of signals into their opposite when the lookback is changed. Now signals may only change from unresolved in directional or vice versa. Signals 3 and 4 were introduced to make sure that all occurrences of extreme volume will result in a signal. Occurrences of wide volume only partly lead to a signal.

Use of REVE Cohorts.

This is the indicator for volume-range analyses that I always wanted to have. Now that I managed to create it, I put it in all my charts, it is often the first part I look at, In my momentum investment system I use it primarily in the layout for following open positions. It helps me a lot to decide whether to close or hold a position. The advantage over my previous attempts to create a REVE indicator (published scripts), is that this version is concise because it reports and classifies all possible volumes and ranges, you see periods of drying out of volume, sequences of falter candles, occurrences of high morning volume, warning and confirming signals.. The assessment by script whether some volume should be considered low, normal, high or extreme gives an edge over using the standard volume bars.

Settings of REVE Cohorts

The default setting for lookback is ‘script sets lookback’ I put this in my indicators because I want them harmonized, the script sets lookback according to timeframe. The tooltip informs which lookback will be set at which timeframe, you can enable a feedback label to show the current lookback. If you switch ‘script sets lookback’ off, you can set your own preferred user lookback. The script self-adapts its settings in such a way that it will show up from the very first bar of historical chart data, it adds volume starting at the fourth bar.

You can switch off volume cohorts, only range candles will show while the middle band disappears. Signals will remain if volume is present in the data. Some Instruments have no volume data, e.g. SPX-S&P 500 Index,, then only range candles will be shown.

Colors can be adapted in the inputs. Because the script calculates matching colors with more transparency it is advised to use 100 percent opacity in these settings.

Take care, Eykpunter

28 Levels V0.1V 0.1

Daily, weekly and monthly important key levels for trading options.

FYI: Not fully functional. It will take ongoing effort to complete the algo.

Trend Momentum SynthesizerBy analyzing the MACD (Moving Average Convergence Divergence) and Squeeze Momentum indicators, this indicator helps identify potential bullish, bearish, or undecided market conditions.

The algorithm within considers the positions of the MACD and Squeeze Momentum indicators to determine the overall market sentiment. When the indicators align and indicate a bullish market condition, the indicator's plot color will be either dark green, green, yellow, or lime, indicating a potential bullish trend. Conversely, if the indicators align and indicate a bearish market condition, the plot color will be maroon or red, denoting a potential bearish trend. When the indicators are inconclusive, the plot color will be orange, suggesting an undecided market.

The ADX is an addon component of this indicator, helping to assess the strength of a trend. By analyzing the ADX, the indicator determines whether a trend is strong enough, providing additional confirmation for potential trade signals. The ADX smoothing and DI (Directional Index) length parameters can be customized to suit individual trading preferences.

By combining these indicators, the algorithm provides traders with a comprehensive view of the market, helping them make informed trading decisions. It aims to assist traders in identifying potential market opportunities and aligns with the objective of maximizing trading performance.

How to use the indicator:

Note: I used back-testing for fine tuning do not base your trades on signals from the testing framework.

Simple ICT Market Structure by toodegreesThis Simple ICT Market Structure is based on the teachings of ICT, specifically in his episode 12 of the Public 2022 Mentorship.