EUR RSCEUR Relative Strength Comparison to the basket of other major currencies.

eur = (eurusd + eurgbp + eurjpy/100 + eurcad + eurchf + euraud + eurnzd)/7

Recherche dans les scripts pour "deep股票代码"

AUD RSCAUD Relative Strength Comparison to the basket of other major currencies.

aud = (audusd + audjpy/100 + audcad + audchf + 1/euraud + 1/gbpaud + audnzd)/7

CHF RSCCHF Relative Strength Comparison to the basket of other major currencies.

chf = (1/usdchf + chfjpy/100 + 1/cadchf + 1/gbpchf + 1/eurchf + 1/audchf + 1/nzdchf)/7

CAD RSCCAD Relative Strength Comparison to the basket of other major currencies.

cad = (1/usdcad + cadjpy/100 + cadchf + 1/eurcad + 1/gbpcad + 1/audcad + 1/nzdcad)/7

JPY RSCJPY Relative Strength Comparison to the basket of other major currencies.

jpy = (1/usdjpy + 1/cadjpy + 1/chfjpy + 1/eurjpy + 1/gbpjpy + 1/audjpy + 1/nzdjpy)/0.07

GBP RSCGBP Relative Strength Comparison to the basket of other major currencies.

gbp = (gbpusd + gbpjpy/100 + gbpcad + 1/eurgbp + gbpchf + gbpaud + gbpnzd)/7

USD Relative Strength Comparison (RSC)Simple indicator implementing relative strength against the equally weighted basket of major currencies. Perhaps I will coin it the Equally Weighted Index (EWI) and trademark it like ICE did with DXY.

usd = (usdjpy/100 + usdcad + 1/gbpusd + 1/eurusd + usdchf + 1/audusd + 1/nzdusd)/7

DXY is hard to compare against other indices because of it's weightening. Secondly it does not compare against all majors and includes SEK which is not a major currency. Source: Wikipedia .

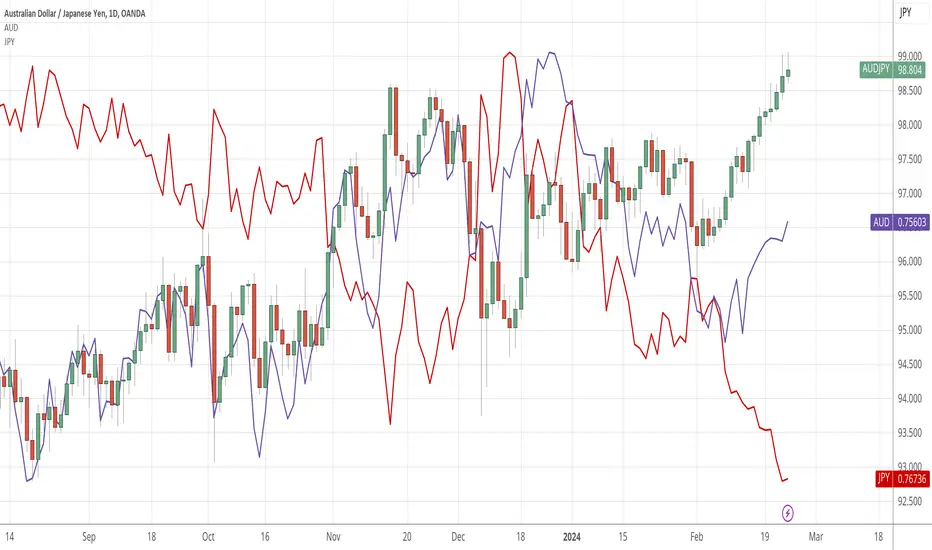

In this chart it becomes more clear why GU is in an uptrend. From April 25th USD has been consolidating against the basket of majors while GBP has gained in strength against the same basket.

gbp = (gbpusd + gbpjpy/100 + gbpcad + 1/eurgbp + gbpchf + gbpaud + gbpnzd)/7

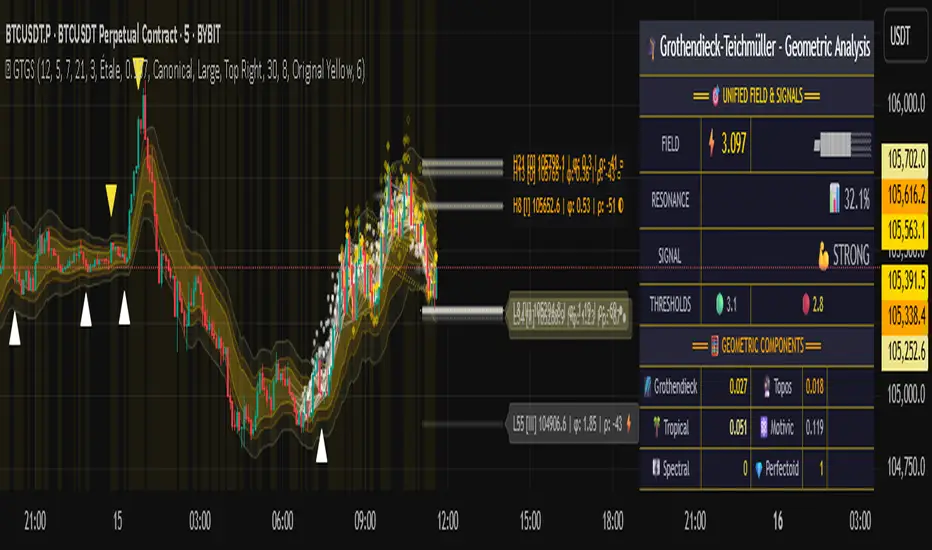

Grothendieck-Teichmüller Geometric SynthesisDskyz's Grothendieck-Teichmüller Geometric Synthesis (GTGS)

THEORETICAL FOUNDATION: A SYMPHONY OF GEOMETRIES

The 🎓 GTGS is built upon a revolutionary premise: that market dynamics can be modeled as geometric and topological structures. While not a literal academic implementation—such a task would demand computational power far beyond current trading platforms—it leverages core ideas from advanced mathematical theories as powerful analogies and frameworks for its algorithms. Each component translates an abstract concept into a practical market calculation, distinguishing GTGS by identifying deeper structural patterns rather than relying on standard statistical measures.

1. Grothendieck-Teichmüller Theory: Deforming Market Structure

The Theory : Studies symmetries and deformations of geometric objects, focusing on the "absolute" structure of mathematical spaces.

Indicator Analogy : The calculate_grothendieck_field function models price action as a "deformation" from its immediate state. Using the nth root of price ratios (math.pow(price_ratio, 1.0/prime)), it measures market "shape" stretching or compression, revealing underlying tensions and potential shifts.

2. Topos Theory & Sheaf Cohomology: From Local to Global Patterns

The Theory : A framework for assembling local properties into a global picture, with cohomology measuring "obstructions" to consistency.

Indicator Analogy : The calculate_topos_coherence function uses sine waves (math.sin) to represent local price "sections." Summing these yields a "cohomology" value, quantifying price action consistency. High values indicate coherent trends; low values signal conflict and uncertainty.

3. Tropical Geometry: Simplifying Complexity

The Theory : Transforms complex multiplicative problems into simpler, additive, piecewise-linear ones using min(a, b) for addition and a + b for multiplication.

Indicator Analogy : The calculate_tropical_metric function applies tropical_add(a, b) => math.min(a, b) to identify the "lowest energy" state among recent price points, pinpointing critical support levels non-linearly.

4. Motivic Cohomology & Non-Commutative Geometry

The Theory : Studies deep arithmetic and quantum-like properties of geometric spaces.

Indicator Analogy : The motivic_rank and spectral_triple functions compute weighted sums of historical prices to capture market "arithmetic complexity" and "spectral signature." Higher values reflect structured, harmonic price movements.

5. Perfectoid Spaces & Homotopy Type Theory

The Theory : Abstract fields dealing with p-adic numbers and logical foundations of mathematics.

Indicator Analogy : The perfectoid_conv and type_coherence functions analyze price convergence and path identity, assessing the "fractal dust" of price differences and price path cohesion, adding fractal and logical analysis.

The Combination is Key : No single theory dominates. GTGS ’s Unified Field synthesizes all seven perspectives into a comprehensive score, ensuring signals reflect deep structural alignment across mathematical domains.

🎛️ INPUTS: CONFIGURING THE GEOMETRIC ENGINE

The GTGS offers a suite of customizable inputs, allowing traders to tailor its behavior to specific timeframes, market sectors, and trading styles. Below is a detailed breakdown of key input groups, their functionality, and optimization strategies, leveraging provided tooltips for precision.

Grothendieck-Teichmüller Theory Inputs

🧬 Deformation Depth (Absolute Galois) :

What It Is : Controls the depth of Galois group deformations analyzed in market structure.

How It Works : Measures price action deformations under automorphisms of the absolute Galois group, capturing market symmetries.

Optimization :

Higher Values (15-20) : Captures deeper symmetries, ideal for major trends in swing trading (4H-1D).

Lower Values (3-8) : Responsive to local deformations, suited for scalping (1-5min).

Timeframes :

Scalping (1-5min) : 3-6 for quick local shifts.

Day Trading (15min-1H) : 8-12 for balanced analysis.

Swing Trading (4H-1D) : 12-20 for deep structural trends.

Sectors :

Stocks : Use 8-12 for stable trends.

Crypto : 3-8 for volatile, short-term moves.

Forex : 12-15 for smooth, cyclical patterns.

Pro Tip : Increase in trending markets to filter noise; decrease in choppy markets for sensitivity.

🗼 Teichmüller Tower Height :

What It Is : Determines the height of the Teichmüller modular tower for hierarchical pattern detection.

How It Works : Builds modular levels to identify nested market patterns.

Optimization :

Higher Values (6-8) : Detects complex fractals, ideal for swing trading.

Lower Values (2-4) : Focuses on primary patterns, faster for scalping.

Timeframes :

Scalping : 2-3 for speed.

Day Trading : 4-5 for balanced patterns.

Swing Trading : 5-8 for deep fractals.

Sectors :

Indices : 5-8 for robust, long-term patterns.

Crypto : 2-4 for rapid shifts.

Commodities : 4-6 for cyclical trends.

Pro Tip : Higher towers reveal hidden fractals but may slow computation; adjust based on hardware.

🔢 Galois Prime Base :

What It Is : Sets the prime base for Galois field computations.

How It Works : Defines the field extension characteristic for market analysis.

Optimization :

Prime Characteristics :

2 : Binary markets (up/down).

3 : Ternary states (bull/bear/neutral).

5 : Pentagonal symmetry (Elliott waves).

7 : Heptagonal cycles (weekly patterns).

11,13,17,19 : Higher-order patterns.

Timeframes :

Scalping/Day Trading : 2 or 3 for simplicity.

Swing Trading : 5 or 7 for wave or cycle detection.

Sectors :

Forex : 5 for Elliott wave alignment.

Stocks : 7 for weekly cycle consistency.

Crypto : 3 for volatile state shifts.

Pro Tip : Use 7 for most markets; 5 for Elliott wave traders.

Topos Theory & Sheaf Cohomology Inputs

🏛️ Temporal Site Size :

What It Is : Defines the number of time points in the topological site.

How It Works : Sets the local neighborhood for sheaf computations, affecting cohomology smoothness.

Optimization :

Higher Values (30-50) : Smoother cohomology, better for trends in swing trading.

Lower Values (5-15) : Responsive, ideal for reversals in scalping.

Timeframes :

Scalping : 5-10 for quick responses.

Day Trading : 15-25 for balanced analysis.

Swing Trading : 25-50 for smooth trends.

Sectors :

Stocks : 25-35 for stable trends.

Crypto : 5-15 for volatility.

Forex : 20-30 for smooth cycles.

Pro Tip : Match site size to your average holding period in bars for optimal coherence.

📐 Sheaf Cohomology Degree :

What It Is : Sets the maximum degree of cohomology groups computed.

How It Works : Higher degrees capture complex topological obstructions.

Optimization :

Degree Meanings :

1 : Simple obstructions (basic support/resistance).

2 : Cohomological pairs (double tops/bottoms).

3 : Triple intersections (complex patterns).

4-5 : Higher-order structures (rare events).

Timeframes :

Scalping/Day Trading : 1-2 for simplicity.

Swing Trading : 3 for complex patterns.

Sectors :

Indices : 2-3 for robust patterns.

Crypto : 1-2 for rapid shifts.

Commodities : 3-4 for cyclical events.

Pro Tip : Degree 3 is optimal for most trading; higher degrees for research or rare event detection.

🌐 Grothendieck Topology :

What It Is : Chooses the Grothendieck topology for the site.

How It Works : Affects how local data integrates into global patterns.

Optimization :

Topology Characteristics :

Étale : Finest topology, captures local-global principles.

Nisnevich : A1-invariant, good for trends.

Zariski : Coarse but robust, filters noise.

Fpqc : Faithfully flat, highly sensitive.

Sectors :

Stocks : Zariski for stability.

Crypto : Étale for sensitivity.

Forex : Nisnevich for smooth trends.

Indices : Zariski for robustness.

Timeframes :

Scalping : Étale for precision.

Swing Trading : Nisnevich or Zariski for reliability.

Pro Tip : Start with Étale for precision; switch to Zariski in noisy markets.

Unified Field Configuration Inputs

⚛️ Field Coupling Constant :

What It Is : Sets the interaction strength between geometric components.

How It Works : Controls signal amplification in the unified field equation.

Optimization :

Higher Values (0.5-1.0) : Strong coupling, amplified signals for ranging markets.

Lower Values (0.001-0.1) : Subtle signals for trending markets.

Timeframes :

Scalping : 0.5-0.8 for quick, strong signals.

Swing Trading : 0.1-0.3 for trend confirmation.

Sectors :

Crypto : 0.5-1.0 for volatility.

Stocks : 0.1-0.3 for stability.

Forex : 0.3-0.5 for balance.

Pro Tip : Default 0.137 (fine structure constant) is a balanced starting point; adjust up in choppy markets.

📐 Geometric Weighting Scheme :

What It Is : Determines the framework for combining geometric components.

How It Works : Adjusts emphasis on different mathematical structures.

Optimization :

Scheme Characteristics :

Canonical : Equal weighting, balanced.

Derived : Emphasizes higher-order structures.

Motivic : Prioritizes arithmetic properties.

Spectral : Focuses on frequency domain.

Sectors :

Stocks : Canonical for balance.

Crypto : Spectral for volatility.

Forex : Derived for structured moves.

Indices : Motivic for arithmetic cycles.

Timeframes :

Day Trading : Canonical or Derived for flexibility.

Swing Trading : Motivic for long-term cycles.

Pro Tip : Start with Canonical; experiment with Spectral in volatile markets.

Dashboard and Visual Configuration Inputs

📋 Show Enhanced Dashboard, 📏 Size, 📍 Position :

What They Are : Control dashboard visibility, size, and placement.

How They Work : Display key metrics like Unified Field , Resonance , and Signal Quality .

Optimization :

Scalping : Small size, Bottom Right for minimal chart obstruction.

Swing Trading : Large size, Top Right for detailed analysis.

Sectors : Universal across markets; adjust size based on screen setup.

Pro Tip : Use Large for analysis, Small for live trading.

📐 Show Motivic Cohomology Bands, 🌊 Morphism Flow, 🔮 Future Projection, 🔷 Holographic Mesh, ⚛️ Spectral Flow :

What They Are : Toggle visual elements representing mathematical calculations.

How They Work : Provide intuitive representations of market dynamics.

Optimization :

Timeframes :

Scalping : Enable Morphism Flow and Spectral Flow for momentum.

Swing Trading : Enable all for comprehensive analysis.

Sectors :

Crypto : Emphasize Morphism Flow and Future Projection for volatility.

Stocks : Focus on Cohomology Bands for stable trends.

Pro Tip : Disable non-essential visuals in fast markets to reduce clutter.

🌫️ Field Transparency, 🔄 Web Recursion Depth, 🎨 Mesh Color Scheme :

What They Are : Adjust visual clarity, complexity, and color.

How They Work : Enhance interpretability of visual elements.

Optimization :

Transparency : 30-50 for balanced visibility; lower for analysis.

Recursion Depth : 6-8 for balanced detail; lower for older hardware.

Color Scheme :

Purple/Blue : Analytical focus.

Green/Orange : Trading momentum.

Pro Tip : Use Neon Purple for deep analysis; Neon Green for active trading.

⏱️ Minimum Bars Between Signals :

What It Is : Minimum number of bars required between consecutive signals.

How It Works : Prevents signal clustering by enforcing a cooldown period.

Optimization :

Higher Values (10-20) : Fewer signals, avoids whipsaws, suited for swing trading.

Lower Values (0-5) : More responsive, allows quick reversals, ideal for scalping.

Timeframes :

Scalping : 0-2 bars for rapid signals.

Day Trading : 3-5 bars for balance.

Swing Trading : 5-10 bars for stability.

Sectors :

Crypto : 0-3 for volatility.

Stocks : 5-10 for trend clarity.

Forex : 3-7 for cyclical moves.

Pro Tip : Increase in choppy markets to filter noise.

Hardcoded Parameters

Tropical, Motivic, Spectral, Perfectoid, Homotopy Inputs : Fixed to optimize performance but influence calculations (e.g., tropical_degree=4 for support levels, perfectoid_prime=5 for convergence).

Optimization : Experiment with codebase modifications if advanced customization is needed, but defaults are robust across markets.

🎨 ADVANCED VISUAL SYSTEM: TRADING IN A GEOMETRIC UNIVERSE

The GTTMTSF ’s visuals are direct representations of its mathematics, designed for intuitive and precise trading decisions.

Motivic Cohomology Bands :

What They Are : Dynamic bands ( H⁰ , H¹ , H² ) representing cohomological support/resistance.

Color & Meaning : Colors reflect energy levels ( H⁰ tightest, H² widest). Breaks into H¹ signal momentum; H² touches suggest reversals.

How to Trade : Use for stop-loss/profit-taking. Band bounces with Dashboard confirmation are high-probability setups.

Morphism Flow (Webbing) :

What It Is : White particle streams visualizing market momentum.

Interpretation : Dense flows indicate strong trends; sparse flows signal consolidation.

How to Trade : Follow dominant flow direction; new flows post-consolidation signal trend starts.

Future Projection Web (Fractal Grid) :

What It Is : Fibonacci-period fractal projections of support/resistance.

Color & Meaning : Three-layer lines (white shadow, glow, colored quantum) with labels showing price, topological class, anomaly strength (φ), resonance (ρ), and obstruction ( H¹ ). ⚡ marks extreme anomalies.

How to Trade : Target ⚡/● levels for entries/exits. High-anomaly levels with weakening Unified Field are reversal setups.

Holographic Mesh & Spectral Flow :

What They Are : Visuals of harmonic interference and spectral energy.

How to Trade : Bright mesh nodes or strong Spectral Flow warn of building pressure before price movement.

📊 THE GEOMETRIC DASHBOARD: YOUR MISSION CONTROL

The Dashboard translates complex mathematics into actionable intelligence.

Unified Field & Signals :

FIELD : Master value (-10 to +10), synthesizing all geometric components. Extreme readings (>5 or <-5) signal structural limits, often preceding reversals or continuations.

RESONANCE : Measures harmony between geometric field and price-volume momentum. Positive amplifies bullish moves; negative amplifies bearish moves.

SIGNAL QUALITY : Confidence meter rating alignment. Trade only STRONG or EXCEPTIONAL signals for high-probability setups.

Geometric Components :

What They Are : Breakdown of seven mathematical engines.

How to Use : Watch for convergence. A strong Unified Field is reliable when components (e.g., Grothendieck , Topos , Motivic ) align. Divergence warns of trend weakening.

Signal Performance :

What It Is : Tracks indicator signal performance.

How to Use : Assesses real-time performance to build confidence and understand system behavior.

🚀 DEVELOPMENT & UNIQUENESS: BEYOND CONVENTIONAL ANALYSIS

The GTTMTSF was developed to analyze markets as evolving geometric objects, not statistical time-series.

Why This Is Unlike Anything Else :

Theoretical Depth : Uses geometry and topology, identifying patterns invisible to statistical tools.

Holistic Synthesis : Integrates seven deep mathematical frameworks into a cohesive Unified Field .

Creative Implementation : Translates PhD-level mathematics into functional Pine Script , blending theory and practice.

Immersive Visualization : Transforms charts into dynamic geometric landscapes for intuitive market understanding.

The GTTMTSF is more than an indicator; it’s a new lens for viewing markets, for traders seeking deeper insight into hidden order within chaos.

" Where there is matter, there is geometry. " - Johannes Kepler

— Dskyz , Trade with insight. Trade with anticipation.

RSI of RSI Deviation (RoRD)RSI of RSI Deviation (RoRD) - Advanced Momentum Acceleration Analysis

What is RSI of RSI Deviation (RoRD)?

RSI of RSI Deviation (RoRD) is a insightful momentum indicator that transcends traditional oscillator analysis by measuring the acceleration of momentum through sophisticated mathematical layering. By calculating RSI on RSI itself (RSI²) and applying advanced statistical deviation analysis with T3 smoothing, RoRD reveals hidden market dynamics that single-layer indicators miss entirely.

This isn't just another RSI variant—it's a complete reimagining of how we measure and visualize momentum dynamics. Where traditional RSI shows momentum, RoRD shows momentum's rate of change . Where others show static overbought/oversold levels, RoRD reveals statistically significant deviations unique to each market's character.

Theoretical Foundation - The Mathematics of Momentum Acceleration

1. RSI² (RSI of RSI) - The Core Innovation

Traditional RSI measures price momentum. RoRD goes deeper:

Primary RSI (RSI₁) : Standard RSI calculation on price

Secondary RSI (RSI²) : RSI calculated on RSI₁ values

This creates a "momentum of momentum" indicator that leads price action

Mathematical Expression:

RSI₁ = 100 - (100 / (1 + RS₁))

RSI² = 100 - (100 / (1 + RS₂))

Where RS₂ = Average Gain of RSI₁ / Average Loss of RSI₁

2. T3 Smoothing - Lag-Free Response

The T3 Moving Average, developed by Tim Tillson, provides:

Superior smoothing with minimal lag

Adaptive response through volume factor (vFactor)

Noise reduction while preserving signal integrity

T3 Formula:

T3 = c1×e6 + c2×e5 + c3×e4 + c4×e3

Where e1...e6 are cascaded EMAs and c1...c4 are volume-factor-based coefficients

3. Statistical Z-Score Deviation

RoRD employs dual-layer Z-score normalization :

Initial Z-Score : (RSI² - SMA) / StDev

Final Z-Score : Z-score of the Z-score for refined extremity detection

This identifies statistically rare events relative to recent market behavior

4. Multi-Timeframe Confluence

Compares current timeframe Z-score with higher timeframe (HTF)

Provides directional confirmation across time horizons

Filters false signals through timeframe alignment

Why RoRD is Different & More Sophisticated

Beyond Traditional Indicators:

Acceleration vs. Velocity : While RSI measures momentum (velocity), RoRD measures momentum's rate of change (acceleration)

Adaptive Thresholds : Z-score analysis adapts to market conditions rather than using fixed 70/30 levels

Statistical Significance : Signals are based on mathematical rarity, not arbitrary levels

Leading Indicator : RSI² often turns before price, providing earlier signals

Reduced Whipsaws : T3 smoothing eliminates noise while maintaining responsiveness

Unique Signal Generation:

Quantum Orbs : Multi-layered visual signals for statistically extreme events

Divergence Detection : Automated identification of price/momentum divergences

Regime Backgrounds : Visual market state classification (Bullish/Bearish/Neutral)

Particle Effects : Dynamic visualization of momentum energy

Visual Design & Interpretation Guide

Color Coding System:

Yellow (#e1ff00) : Neutral/balanced momentum state

Red (#ff0000) : Overbought/extreme bullish acceleration

Green (#2fff00) : Oversold/extreme bearish acceleration

Orange : Z-score visualization

Blue : HTF Z-score comparison

Main Visual Elements:

RSI² Line with Glow Effect

Multi-layer glow creates depth and emphasis

Color dynamically shifts based on momentum state

Line thickness indicates signal strength

Quantum Signal Orbs

Green Orbs Below : Statistically rare oversold conditions

Red Orbs Above : Statistically rare overbought conditions

Multiple layers indicate signal strength

Only appear at Z-score extremes for high-conviction signals

Divergence Markers

Green Circles : Bullish divergence detected

Red Circles : Bearish divergence detected

Plotted at pivot points for precision

Background Regimes

Green Background : Bullish momentum regime

Grey Background : Bearish momentum regime

Blue Background : Neutral/transitioning regime

Particle Effects

Density indicates momentum energy

Color matches current RSI² state

Provides dynamic market "feel"

Dashboard Metrics - Deep Dive

RSI² ANALYSIS Section:

RSI² Value (0-100)

Current smoothed RSI of RSI reading

>70 : Strong bullish acceleration

<30 : Strong bearish acceleration

~50 : Neutral momentum state

RSI¹ Value

Traditional RSI for reference

Compare with RSI² for acceleration/deceleration insights

Z-Score Status

🔥 EXTREME HIGH : Z > threshold, statistically rare bullish

❄️ EXTREME LOW : Z < threshold, statistically rare bearish

📈 HIGH/📉 LOW : Elevated but not extreme

➡️ NEUTRAL : Normal statistical range

MOMENTUM Section:

Velocity Indicator

▲▲▲ : Strong positive acceleration

▼▼▼ : Strong negative acceleration

Shows rate of change in RSI²

Strength Bar

██████░░░░ : Visual power gauge

Filled bars indicate momentum strength

Based on deviation from center line

SIGNALS Section:

Divergence Status

🟢 BULLISH DIV : Price making lows, RSI² making highs

🔴 BEARISH DIV : Price making highs, RSI² making lows

⚪ NO DIVERGENCE : No divergence detected

HTF Comparison

🔥 HTF EXTREME : Higher timeframe confirms extremity

📊 HTF NORMAL : Higher timeframe is neutral

Critical for multi-timeframe confirmation

Trading Application & Strategy

Signal Hierarchy (Highest to Lowest Priority):

Quantum Orb + HTF Alignment + Divergence

Highest conviction reversal signal

Z-score extreme + timeframe confluence + divergence

Quantum Orb + HTF Alignment

Strong reversal signal

Wait for price confirmation

Divergence + Regime Change

Medium-term reversal signal

Monitor for orb confirmation

Threshold Crosses

Traditional overbought/oversold

Use as alert, not entry

Entry Strategies:

For Reversals:

Wait for Quantum Orb signal

Confirm with HTF Z-score direction

Enter on price structure break

Stop beyond recent extreme

For Continuations:

Trade with regime background color

Use RSI² pullbacks to center line

Avoid signals against HTF trend

For Scalping:

Focus on Z-score extremes

Quick entries on orb signals

Exit at center line cross

Risk Management:

Reduce position size when signals conflict with HTF

Avoid trades during regime transitions (blue background)

Tighten stops after divergence completion

Scale out at statistical mean reversion

Development & Uniqueness

RoRD represents months of research into momentum dynamics and statistical analysis. Unlike indicators that simply combine existing tools, RoRD introduces several genuine innovations :

True RSI² Implementation : Not a smoothed RSI, but actual RSI calculated on RSI values

Dual Z-Score Normalization : Unique approach to finding statistical extremes

T3 Integration : First RSI² implementation with T3 smoothing for optimal lag reduction

Quantum Orb Visualization : Revolutionary signal display method

Dynamic Regime Detection : Automatic market state classification

Statistical Adaptability : Thresholds adapt to market volatility

This indicator was built from first principles, with each component carefully selected for its mathematical properties and practical trading utility. The result is a professional-grade tool that provides insights unavailable through traditional momentum analysis.

Best Practices & Tips

Start with default settings - they're optimized for most markets

Always check HTF alignment before taking signals

Use divergences as early warning , orbs as confirmation

Respect regime backgrounds - trade with them, not against

Combine with price action - RoRD shows when, price shows where

Adjust Z-score thresholds based on market volatility

Monitor dashboard metrics for complete market context

Conclusion

RoRD isn't just another indicator—it's a complete momentum analysis system that reveals market dynamics invisible to traditional tools. By combining momentum acceleration, statistical analysis, and multi-timeframe confluence with intuitive visualization, RoRD provides traders with a sophisticated edge in any market condition.

Whether you're scalping rapid reversals or positioning for major trend changes, RoRD's unique approach to momentum analysis will transform how you see and trade market dynamics.

See momentum's future. Trade with statistical edge.

Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

Sentiment OscillatorIn the complex world of trading, understanding market sentiment can be like reading the emotional pulse of financial markets. Our Sentiment Oscillator is designed to be your personal market mood translator, helping you navigate through the noise of price movements and market fluctuations.

Imagine having a sophisticated tool that goes beyond traditional price charts, diving deep into the underlying dynamics of market behavior. This indicator doesn't just show you numbers – it tells you a story about market sentiment, combining multiple financial signals to give you a comprehensive view of potential market directions.

The Sentiment Oscillator acts like a sophisticated emotional barometer for stocks, cryptocurrencies, or any tradable asset. It analyzes price changes, market volatility, trading volume, and long-term trends to generate a unique sentiment score. This score ranges from highly bullish to deeply bearish, providing traders with an intuitive visual representation of market mood.

Green zones indicate positive market sentiment, suggesting potential buying opportunities. Red zones signal caution, hinting at possible downward trends. The oscillator's gray neutral zone helps you identify periods of market uncertainty, allowing for more calculated trading decisions.

What sets this indicator apart is its ability to blend multiple market factors into a single, easy-to-understand indicator. It's not just about current price – it's about understanding the deeper currents moving beneath the surface of market prices.

Traders can use this oscillator to:

- Identify potential trend reversals

- Understand market sentiment beyond price movement

- Spot periods of market strength or weakness

- Complement other technical analysis tools

Whether you're a day trader, swing trader, or long-term investor, the Sentiment Oscillator provides an additional layer of insight to support your trading strategy. Remember, no indicator is a crystal ball, but this tool can help you make more informed decisions in the dynamic world of trading.

Pasrsifal.RegressionTrendStateSummary

The Parsifal.Regression.Trend.State Indicator analyzes the leading coefficients of linear and quadratic regressions of price (against time). It also considers their first- and second-order changes. These features are aggregated into a Trend-State background, shown as a gradient color. In addition, the indicator generates fast and slow signals that can be used as potential entry- or exit triggers.

This tool is designed for advanced trend-following strategies, leveraging information from multiple trendline features.

Background

Trendlines provide insight into the state of a trend or the “trendiness” of a price process. While moving averages or pivot-based lines can serve as envelopes and breakout levels, they are often too lagging for swing traders, who need tools that adapt more closely to price swings, ideally using trendlines, around which the price process swings continuously.

Regression lines address this by cutting directly through the data, making them a natural anchor for observing how price winds around a central trendline within a chosen lookback period.

Regression Trendlines

• Linear Regression:

o Minimizes distance to all closing values over the lookback period.

o The slope represents the short-term linear trend.

o The change of slope indicates trend acceleration or deceleration.

o Linear regression lags during phases of rapid market shifts.

• Quadratic Regression:

o Fits a second-degree polynomial to minimize deviation from closing prices.

o The convexity term (leading coefficient) reflects curvature:

Positive convexity → accelerating uptrend or fading downtrend.

Negative convexity → accelerating downtrend or fading uptrend.

o The change of convexity detects early shifts in momentum and often reacts faster than slope features.

Features Extracted

The indicator evaluates six features:

• Linear features: slope, first derivative of slope, second derivative of slope.

• Quadratic features: convexity term, first derivative of the convexity term, second derivative of the convexity term.

• Linear features: capture broad, background trend behavior.

• Quadratic features: detect deviations, accelerations, and smaller-scale dynamics.

Quadratic terms generally react first to market changes, while linear terms provide stability and context.

Dynamics of Market Moves as seen by linear and quadratic regressions

• At the start of a rapid move:

The change of convexity reacts first, capturing the shift in dynamics before other features. The convexity term then follows, while linear slope features lag further behind. Because convexity measures deviation from linearity, it reflects accelerating momentum more effectively than slope.

• At the end of a rapid move:

Again, the change of convexity responds first to fading momentum, signaling the transition from above-linear to below-linear dynamics. Even while a strong trend persists, the change of convexity may flip sign early, offering a warning of weakening strength. The convexity term itself adjusts more slowly but may still turn before the price process does. Linear features lag the most, typically only flipping after price has already reversed, thereby smoothing out the rapid, more sensitive reactions of quadratic terms.

________________________________________

Parsifal Regression.Trend.State Method

1. Feature Mapping:

Each feature is mapped to a range between -1 and 1, preserving zero-crossings (critical for sign interpretation).

2. Aggregation:

A heuristic linear combination*) produces a background information value, visualized as a gradient color scale:

o Deep green → strong positive trend.

o Deep red → strong negative trend.

o Yellow → neutral or transitional states.

3. Signals:

o Fast signal (oscillator): ranges from -1 to 1, reflecting short-term trend state.

o Slow signal (smoothed): moving average of the fast signal.

o Their interactions (crossovers, zero-crossings) provide actionable trading triggers.

How to Use

The Trend-State background gradient provides intuitive visual feedback on the aggregated regression features (slope, convexity, and their changes). Because these features reflect not only current trend strength but also their acceleration or deceleration, the color transitions help anticipate evolving market states:

• Solid Green: All features near their highs. Indicates a strong, accelerating uptrend. May also reflect explosive or hyperbolic upside moves (including gaps).

• Fading Solid Green: A recently strong uptrend is losing momentum. Price may shift into a slower uptrend, consolidation, or even a reversal.

• Fading Green → Yellow: Often appears as a dirty yellow or a rapidly mixing pattern of green and red. Signals that the uptrend is weakening toward neutrality or beginning to turn negative.

• Yellow → Deepening Red: Two possible scenarios:

o Coming from a strong uptrend → suggests a sharp fade, though the trend may still technically be up.

o Coming from a weaker uptrend or sideways market → suggests the start of an accelerating downtrend.

• Solid Red: All features near their lows. Indicates a strong, accelerating downtrend. May also reflect crash-type conditions or downside gaps.

• Fading Solid Red: A recently strong downtrend is losing strength. Market may move into a slower decline, consolidation, or early reversal upward.

• Fading Red → Yellow : The downtrend is weakening toward neutral, with potential for a bullish shift.

• Yellow → Increasing Green: Two possible scenarios:

o Coming from a strong downtrend, it reflects a sharp fade of bearish momentum, though the market may still technically be trending down.

o Coming from a weaker downtrend or sideways movement, it suggests the start of an accelerating uptrend.

Note: Market evolution does not always follow this neat “color cycle.” It may jump between states, skip stages, or reverse abruptly depending on market conditions. This makes the background coloring particularly valuable as a contextual map of current and evolving price dynamics.

Signal Crossovers:

Although the fast signal is very similar (but not identical) to the background coloring, it provides a numerical representation indicating a bullish interpretation for rising values and bearish for falling.

o High-confidence entries:

Fast signal rising from < -0.7 and crossing above the slow signal → potential long entry.

Fast signal falling from > +0.7 and crossing below the slow signal → potential short entry.

o Low-confidence entries:

Crossovers near zero may still provide a valid trigger but may be noisy and should be confirmed with other signals.

o Zero-crossings:

Indicate broader state changes, useful for conservative positioning or option strategies. For confirmation of a Fast signal 0-crossing, wait for the Slow signal to cross as well.

________________________________________

*) Note on Aggregation

While the indicator currently uses a heuristic linear combination of features, alternatives such as Principal Component Analysis (PCA) could provide a more formal aggregation. However, while in the absence of matrix algebra, the required eigenvalue decomposition can be approximated, its computational expense does not justify the marginal higher insight in this case. The current heuristic approach offers a practical balance of clarity, speed, and accuracy.

Meta-LR ForecastThis indicator builds a forward-looking projection from the current bar by combining twelve time-compressed “mini forecasts.” Each forecast is a linear-regression-based outlook whose contribution is adaptively scaled by trend strength (via ADX) and normalized to each timeframe’s own volatility (via that timeframe’s ATR). The result is a 12-segment polyline that starts at the current price and extends one bar at a time into the future (1× through 12× the chart’s timeframe). Alongside the plotted path, the script computes two summary measures:

* Per-TF Bias% — a directional efficiency × R² score for each micro-forecast, expressed as a percent.

* Meta Bias% — the same score, but applied to the final, accumulated 12-step path. It summarizes how coherent and directional the combined projection is.

This tool is an indicator, not a strategy. It does not place orders. Nothing here is trade advice; it is a visual, quantitative framework to help you assess directional bias and trend context across a ladder of timeframe multiples.

The core engine fits a simple least-squares line on a normalized price series for each small forecast horizon and extrapolates one bar forward. That “trend” forecast is paired with its mirror, an “anti-trend” forecast, constructed around the current normalized price. The model then blends between these two wings according to current trend strength as measured by ADX.

ADX is transformed into a weight (w) in using an adaptive band centered on the rolling mean (μ) with width derived from the standard deviation (σ) of ADX over a configurable lookback. When ADX is deeply below the lower band, the weight approaches -1, favoring anti-trend behavior. Inside the flat band, the weight is near zero, producing neutral behavior. Clearly above the upper band, the weight approaches +1, favoring a trend-following stance. The transitions between these regions are linear so the regime shift is smooth rather than abrupt.

You can shape how quickly the model commits to either wing using two exponents. One exponent controls how aggressively positive weights lean into the trend forecast; the other controls how aggressively negative weights lean into the anti-trend forecast. Raising these exponents makes the response more gradual; lowering them makes the shift more decisive. An optional switch can force full anti-trend behavior when ADX registers a deep-low condition far below the lower tail, if you prefer a categorical stance in very flat markets.

A key design choice is volatility normalization. Every micro-forecast is computed in ATR units of its own timeframe. The script fetches that timeframe’s ATR inside each security call and converts normalized outputs back to price with that exact ATR. This avoids scaling higher-timeframe effects by the chart ATR or by square-root time approximations. Using “ATR-true” for each timeframe keeps the cross-timeframe accumulation consistent and dimensionally correct.

Bias% is defined as directional efficiency multiplied by R², expressed as a percent. Directional efficiency captures how much net progress occurred relative to the total path length; R² captures how well the path aligns with a straight line. If price meanders without net progress, efficiency drops; if the variation is well-explained by a line, R² rises. Multiplying the two penalizes choppy, low-signal paths and rewards sustained, coherent motion.

The forward path is built by converting each per-timeframe Bias% into a small ATR-sized delta, then cumulatively adding those deltas to form a 12-step projection. This produces a polyline anchored at the current close and stepping forward one bar per timeframe multiple. Segment color flips by slope, allowing a quick read of the path’s direction and inflection.

Inputs you can tune include:

* Max Regression Length. Upper bound for each micro-forecast’s regression window. Larger values smooth the trend estimate at the cost of responsiveness; smaller values react faster but can add noise.

* Price Source. The price series analyzed (for example, close or typical price).

* ADX Length. Period used for the DMI/ADX calculation.

* ATR Length (normalization). Window used for ATR; this is applied per timeframe inside each security call.

* Band Lookback (for μ, σ). Lookback used to compute the adaptive ADX band statistics. Larger values stabilize the band; smaller values react more quickly.

* Flat half-width (σ). Width of the neutral band on both sides of μ. Wider flats spend more time neutral; narrower flats switch regimes more readily.

* Tail width beyond flat (σ). Distance from the flat band edge to the extreme trend/anti-trend zone. Larger tails create a longer ramp; smaller tails reach extremes sooner.

* Polyline Width. Visual thickness of the plotted segments.

* Negative Wing Aggression (anti-trend). Exponent shaping for negative weights; higher values soften the tilt into mean reversion.

* Positive Wing Aggression (trend). Exponent shaping for positive weights; lower values make trend commitment stronger and sooner.

* Force FULL Anti-Trend at Deep-Low ADX. Optional hard switch for extremely low ADX conditions.

On the chart you will see:

* A 12-segment forward polyline starting from the current close to bar\_index + 1 … +12, with green segments for up-steps and red for down-steps.

* A small label at the latest bar showing Meta Bias% when available, or “n/a” when insufficient data exists.

Interpreting the readouts:

* Trend-following contexts are characterized by ADX above the adaptive upper band, pushing w toward +1. The blended forecast leans toward the regression extrapolation. A strongly positive Meta Bias% in this environment suggests directional alignment across the ladder of timeframes.

* Mean-reversion contexts occur when ADX is well below the lower tail, pushing w toward -1 (or forcing anti-trend if enabled). After a sharp advance, a negative Meta Bias% may indicate the model projects pullback tendencies.

* Neutral contexts occur when ADX sits inside the flat band; w is near zero, the blended forecast remains close to current price, and Meta Bias% tends to hover near zero.

These are analytical cues, not rules. Always corroborate with your broader process, including market structure, time-of-day behavior, liquidity conditions, and risk limits.

Practical usage patterns include:

* Momentum confirmation. Combine a rising Meta Bias% with higher-timeframe structure (such as higher highs and higher lows) to validate continuation setups. Treat the 12th step’s distance as a coarse sense of potential room rather than as a target.

* Fade filtering. If you prefer fading extremes, require ADX to be near or below the lower ramp before acting on counter-moves, and avoid fades when ADX is decisively above the upper band.

* Position planning. Because per-step deltas are ATR-scaled, the path’s vertical extent can be mentally mapped to typical noise for the instrument, informing stop distance choices. The script itself does not compute orders or size.

* Multi-timeframe alignment. Each step corresponds to a clean multiple of your chart timeframe, so the polyline visualizes how successively larger windows bias price, all referenced to the current bar.

House-rules and repainting disclosures:

* Indicator, not strategy. The script does not execute, manage, or suggest orders. It displays computed paths and bias scores for analysis only.

* No performance claims. Past behavior of any measure, including Meta Bias%, does not guarantee future results. There are no assurances of profitability.

* Higher-timeframe updates. Values obtained via security for higher-timeframe series can update intrabar until the higher-timeframe bar closes. The forward path and Meta Bias% may change during formation of a higher-timeframe candle. If you need confirmed higher-timeframe inputs, consider reading the prior higher-timeframe value or acting only after the higher-timeframe close.

* Data sufficiency. The model requires enough history to compute ATR, ADX statistics, and regression windows. On very young charts or illiquid symbols, parts of the readout can be unavailable until sufficient data accumulates.

* Volatility regimes. ATR normalization helps compare across timeframes, but unusual volatility regimes can make the path look deceptively flat or exaggerated. Judge the vertical scale relative to your instrument’s typical ATR.

Tuning tips:

* Stability versus responsiveness. Increase Max Regression Length to steady the micro-forecasts but accept slower response. If you lower it, consider slightly increasing Band Lookback so regime boundaries are not too jumpy.

* Regime bands. Widen the flat half-width to spend more time neutral, which can reduce over-trading tendencies in chop. Shrink the tail width if you want the model to commit to extremes sooner, at the cost of more false swings.

* Wing shaping. If anti-trend behavior feels too abrupt at low ADX, raise the negative wing exponent. If you want trend bias to kick in more decisively at high ADX, lower the positive wing exponent. Small changes have large effects.

* Forced anti-trend. Enable the deep-low option only if you explicitly want a categorical “markets are flat, fade moves” policy. Many users prefer leaving it off to keep regime decisions continuous.

Troubleshooting:

* Nothing plots or the label shows “n/a.” Ensure the chart has enough history for the ADX band statistics, ATR, and the regression windows. Exotic or illiquid symbols with missing data may starve the higher-timeframe computations. Try a more liquid market or a higher timeframe.

* Path flickers or shifts during the bar. This is expected when any higher-timeframe input is still forming. Wait for the higher-timeframe close for fully confirmed behavior, or modify the code to read prior values from the higher timeframe.

* Polyline looks too flat or too steep. Check the chart’s vertical scale and recent ATR regime. Adjust Max Regression Length, the wing exponents, or the band widths to suit the instrument.

Integration ideas for manual workflows:

* Confluence checklist. Use Meta Bias% as one of several independent checks, alongside structure, session context, and event risk. Act only when multiple cues align.

* Stop and target thinking. Because deltas are ATR-scaled at each timeframe, benchmark your proposed stops and targets against the forward steps’ magnitude. Stops that are much tighter than the prevailing ATR often sit inside normal noise.

* Session context. Consider session hours and microstructure. The same ADX value can imply different tradeability in different sessions, particularly in index futures and FX.

This indicator deliberately avoids:

* Fixed thresholds for buy or sell decisions. Markets vary and fixed numbers invite overfitting. Decide what constitutes “high enough” Meta Bias% for your market and timeframe.

* Automatic risk sizing. Proper sizing depends on account parameters, instrument specifications, and personal risk tolerance. Keep that decision in your risk plan, not in a visual bias tool.

* Claims of edge. These measures summarize path geometry and trend context; they do not ensure a tradable edge on their own.

Summary of how to think about the output:

* The script builds a 12-step forward path by stacking linear-regression micro-forecasts across increasing multiples of the chart timeframe.

* Each micro-forecast is blended between trend and anti-trend using an adaptive ADX band with separate aggression controls for positive and negative regimes.

* All computations are done in ATR-true units for each timeframe before reconversion to price, ensuring dimensional consistency when accumulating steps.

* Bias% (per-timeframe and Meta) condenses directional efficiency and trend fidelity into a compact score.

* The output is designed to serve as an analytical overlay that helps assess whether conditions look trend-friendly, fade-friendly, or neutral, while acknowledging higher-timeframe update behavior and avoiding prescriptive trade rules.

Use this tool as one component within a disciplined process that includes independent confirmation, event awareness, and robust risk management.

Red & Green Zone ReversalOverview

The “Red & Green Zone Reversal” indicator is designed to visually highlight potential reversal zones on your chart by using a combination of Bollinger Bands and the Relative Strength Index (RSI).

It overlays on the chart and provides background color cues—red for oversold conditions and green for overbought conditions—along with corresponding alert triggers.

Key Components

Overlay: The indicator is set to overlay the chart, meaning its visual cues (colored backgrounds) are drawn directly on the price chart.

Bollinger Bands Calculation

Period: A 20-period simple moving average (SMA) is calculated from the closing prices.

Standard Deviation Multiplier: A multiplier of 2.0 is applied.

Bands Defined:

Basis: The 20-period SMA.

Deviation: Calculated as 2 times the standard deviation over the same period.

Upper Band: Basis plus the deviation.

Lower Band: Basis minus the deviation.

RSI Calculation

Period: The RSI is computed over a 14-period span using the closing prices.

Thresholds:

Oversold Threshold: 30 (used for the red zone condition).

Overbought Threshold: 70 (used for the green zone condition).

Zone Conditions

Red Zone (Oversold):

Criteria: The price is below the lower Bollinger Band and the RSI is below 30.

Purpose: Highlights a situation where the asset may be deeply oversold, signaling a potential reversal to the upside.

Green Zone (Overbought):

Criteria: The price is above the upper Bollinger Band and the RSI is above 70.

Purpose: Indicates that the asset may be overbought, potentially signaling a reversal to the downside.

Visual and Alert Components

Background Coloring:

Red Background: Applied when the red zone condition is met (using a semi-transparent red).

Green Background: Applied when the green zone condition is met (using a semi-transparent green).

Alerts:

Red Alert: An alert condition titled “Deep Oversold Alert” is triggered with the message “Deep Oversold Signal triggered!” when the red zone criteria are satisfied.

Green Alert: Similarly, an alert condition titled “Deep Overbought Alert” is triggered with the message “Deep Overbought Signal triggered!” when the green zone criteria are met.

Important Disclaimers

Not Financial Advice:

This indicator is provided for informational and analytical purposes only. It does not constitute trading advice or a recommendation to buy or sell any asset. Traders should use it as one of several tools in their analysis and should perform their own due diligence.

Risk Management:

Trading inherently involves risk. Past performance is not indicative of future results. Always implement appropriate risk management and use stop losses where necessary.

Summary

In summary, the “Red & Green Zone Reversal” indicator uses Bollinger Bands and RSI to detect extreme market conditions. It visually marks oversold (red) and overbought (green) conditions directly on the chart and offers alert conditions to help traders monitor these potential reversal points.

Enjoy!!

Quinn-Fernandes Fourier Transform of Filtered Price [Loxx]Down the Rabbit Hole We Go: A Deep Dive into the Mysteries of Quinn-Fernandes Fast Fourier Transform and Hodrick-Prescott Filtering

In the ever-evolving landscape of financial markets, the ability to accurately identify and exploit underlying market patterns is of paramount importance. As market participants continuously search for innovative tools to gain an edge in their trading and investment strategies, advanced mathematical techniques, such as the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter, have emerged as powerful analytical tools. This comprehensive analysis aims to delve into the rich history and theoretical foundations of these techniques, exploring their applications in financial time series analysis, particularly in the context of a sophisticated trading indicator. Furthermore, we will critically assess the limitations and challenges associated with these transformative tools, while offering practical insights and recommendations for overcoming these hurdles to maximize their potential in the financial domain.

Our investigation will begin with a comprehensive examination of the origins and development of both the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter. We will trace their roots from classical Fourier analysis and time series smoothing to their modern-day adaptive iterations. We will elucidate the key concepts and mathematical underpinnings of these techniques and demonstrate how they are synergistically used in the context of the trading indicator under study.

As we progress, we will carefully consider the potential drawbacks and challenges associated with using the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter as integral components of a trading indicator. By providing a critical evaluation of their computational complexity, sensitivity to input parameters, assumptions about data stationarity, performance in noisy environments, and their nature as lagging indicators, we aim to offer a balanced and comprehensive understanding of these powerful analytical tools.

In conclusion, this in-depth analysis of the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter aims to provide a solid foundation for financial market participants seeking to harness the potential of these advanced techniques in their trading and investment strategies. By shedding light on their history, applications, and limitations, we hope to equip traders and investors with the knowledge and insights necessary to make informed decisions and, ultimately, achieve greater success in the highly competitive world of finance.

█ Fourier Transform and Hodrick-Prescott Filter in Financial Time Series Analysis

Financial time series analysis plays a crucial role in making informed decisions about investments and trading strategies. Among the various methods used in this domain, the Fourier Transform and the Hodrick-Prescott (HP) Filter have emerged as powerful techniques for processing and analyzing financial data. This section aims to provide a comprehensive understanding of these two methodologies, their significance in financial time series analysis, and their combined application to enhance trading strategies.

█ The Quinn-Fernandes Fourier Transform: History, Applications, and Use in Financial Time Series Analysis

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique developed by John J. Quinn and Mauricio A. Fernandes in the early 1990s. It builds upon the classical Fourier Transform by introducing an adaptive approach that improves the identification of dominant frequencies in noisy signals. This section will explore the history of the Quinn-Fernandes Fourier Transform, its applications in various domains, and its specific use in financial time series analysis.

History of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform was introduced in a 1993 paper titled "The Application of Adaptive Estimation to the Interpolation of Missing Values in Noisy Signals." In this paper, Quinn and Fernandes developed an adaptive spectral estimation algorithm to address the limitations of the classical Fourier Transform when analyzing noisy signals.

The classical Fourier Transform is a powerful mathematical tool that decomposes a function or a time series into a sum of sinusoids, making it easier to identify underlying patterns and trends. However, its performance can be negatively impacted by noise and missing data points, leading to inaccurate frequency identification.

Quinn and Fernandes sought to address these issues by developing an adaptive algorithm that could more accurately identify the dominant frequencies in a noisy signal, even when data points were missing. This adaptive algorithm, now known as the Quinn-Fernandes Fourier Transform, employs an iterative approach to refine the frequency estimates, ultimately resulting in improved spectral estimation.

Applications of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform has found applications in various fields, including signal processing, telecommunications, geophysics, and biomedical engineering. Its ability to accurately identify dominant frequencies in noisy signals makes it a valuable tool for analyzing and interpreting data in these domains.

For example, in telecommunications, the Quinn-Fernandes Fourier Transform can be used to analyze the performance of communication systems and identify interference patterns. In geophysics, it can help detect and analyze seismic signals and vibrations, leading to improved understanding of geological processes. In biomedical engineering, the technique can be employed to analyze physiological signals, such as electrocardiograms, leading to more accurate diagnoses and better patient care.

Use of the Quinn-Fernandes Fourier Transform in Financial Time Series Analysis

In financial time series analysis, the Quinn-Fernandes Fourier Transform can be a powerful tool for isolating the dominant cycles and frequencies in asset price data. By more accurately identifying these critical cycles, traders can better understand the underlying dynamics of financial markets and develop more effective trading strategies.

The Quinn-Fernandes Fourier Transform is used in conjunction with the Hodrick-Prescott Filter, a technique that separates the underlying trend from the cyclical component in a time series. By first applying the Hodrick-Prescott Filter to the financial data, short-term fluctuations and noise are removed, resulting in a smoothed representation of the underlying trend. This smoothed data is then subjected to the Quinn-Fernandes Fourier Transform, allowing for more accurate identification of the dominant cycles and frequencies in the asset price data.

By employing the Quinn-Fernandes Fourier Transform in this manner, traders can gain a deeper understanding of the underlying dynamics of financial time series and develop more effective trading strategies. The enhanced knowledge of market cycles and frequencies can lead to improved risk management and ultimately, better investment performance.

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique that has proven valuable in various domains, including financial time series analysis. Its adaptive approach to frequency identification addresses the limitations of the classical Fourier Transform when analyzing noisy signals, leading to more accurate and reliable analysis. By employing the Quinn-Fernandes Fourier Transform in financial time series analysis, traders can gain a deeper understanding of the underlying financial instrument.

Drawbacks to the Quinn-Fernandes algorithm

While the Quinn-Fernandes Fourier Transform is an effective tool for identifying dominant cycles and frequencies in financial time series, it is not without its drawbacks. Some of the limitations and challenges associated with this indicator include:

1. Computational complexity: The adaptive nature of the Quinn-Fernandes Fourier Transform requires iterative calculations, which can lead to increased computational complexity. This can be particularly challenging when analyzing large datasets or when the indicator is used in real-time trading environments.

2. Sensitivity to input parameters: The performance of the Quinn-Fernandes Fourier Transform is dependent on the choice of input parameters, such as the number of harmonic periods, frequency tolerance, and Hodrick-Prescott filter settings. Choosing inappropriate parameter values can lead to inaccurate frequency identification or reduced performance. Finding the optimal parameter settings can be challenging, and may require trial and error or a more sophisticated optimization process.

3. Assumption of stationary data: The Quinn-Fernandes Fourier Transform assumes that the underlying data is stationary, meaning that its statistical properties do not change over time. However, financial time series data is often non-stationary, with changing trends and volatility. This can limit the effectiveness of the indicator and may require additional preprocessing steps, such as detrending or differencing, to ensure the data meets the assumptions of the algorithm.

4. Limitations in noisy environments: Although the Quinn-Fernandes Fourier Transform is designed to handle noisy signals, its performance may still be negatively impacted by significant noise levels. In such cases, the identification of dominant frequencies may become less reliable, leading to suboptimal trading signals or strategies.

5. Lagging indicator: As with many technical analysis tools, the Quinn-Fernandes Fourier Transform is a lagging indicator, meaning that it is based on past data. While it can provide valuable insights into historical market dynamics, its ability to predict future price movements may be limited. This can result in false signals or late entries and exits, potentially reducing the effectiveness of trading strategies based on this indicator.

Despite these drawbacks, the Quinn-Fernandes Fourier Transform remains a valuable tool for financial time series analysis when used appropriately. By being aware of its limitations and adjusting input parameters or preprocessing steps as needed, traders can still benefit from its ability to identify dominant cycles and frequencies in financial data, and use this information to inform their trading strategies.

█ Deep-dive into the Hodrick-Prescott Fitler

The Hodrick-Prescott (HP) filter is a statistical tool used in economics and finance to separate a time series into two components: a trend component and a cyclical component. It is a powerful tool for identifying long-term trends in economic and financial data and is widely used by economists, central banks, and financial institutions around the world.

The HP filter was first introduced in the 1990s by economists Robert Hodrick and Edward Prescott. It is a simple, two-parameter filter that separates a time series into a trend component and a cyclical component. The trend component represents the long-term behavior of the data, while the cyclical component captures the shorter-term fluctuations around the trend.

The HP filter works by minimizing the following objective function:

Minimize: (Sum of Squared Deviations) + λ (Sum of Squared Second Differences)

Where:

1. The first term represents the deviation of the data from the trend.

2. The second term represents the smoothness of the trend.

3. λ is a smoothing parameter that determines the degree of smoothness of the trend.

The smoothing parameter λ is typically set to a value between 100 and 1600, depending on the frequency of the data. Higher values of λ lead to a smoother trend, while lower values lead to a more volatile trend.

The HP filter has several advantages over other smoothing techniques. It is a non-parametric method, meaning that it does not make any assumptions about the underlying distribution of the data. It also allows for easy comparison of trends across different time series and can be used with data of any frequency.

Another significant advantage of the HP Filter is its ability to adapt to changes in the underlying trend. This feature makes it particularly well-suited for analyzing financial time series, which often exhibit non-stationary behavior. By employing the HP Filter to smooth financial data, traders can more accurately identify and analyze the long-term trends that drive asset prices, ultimately leading to better-informed investment decisions.

However, the HP filter also has some limitations. It assumes that the trend is a smooth function, which may not be the case in some situations. It can also be sensitive to changes in the smoothing parameter λ, which may result in different trends for the same data. Additionally, the filter may produce unrealistic trends for very short time series.

Despite these limitations, the HP filter remains a valuable tool for analyzing economic and financial data. It is widely used by central banks and financial institutions to monitor long-term trends in the economy, and it can be used to identify turning points in the business cycle. The filter can also be used to analyze asset prices, exchange rates, and other financial variables.

The Hodrick-Prescott filter is a powerful tool for analyzing economic and financial data. It separates a time series into a trend component and a cyclical component, allowing for easy identification of long-term trends and turning points in the business cycle. While it has some limitations, it remains a valuable tool for economists, central banks, and financial institutions around the world.

█ Combined Application of Fourier Transform and Hodrick-Prescott Filter

The integration of the Fourier Transform and the Hodrick-Prescott Filter in financial time series analysis can offer several benefits. By first applying the HP Filter to the financial data, traders can remove short-term fluctuations and noise, effectively isolating the underlying trend. This smoothed data can then be subjected to the Fourier Transform, allowing for the identification of dominant cycles and frequencies with greater precision.

By combining these two powerful techniques, traders can gain a more comprehensive understanding of the underlying dynamics of financial time series. This enhanced knowledge can lead to the development of more effective trading strategies, better risk management, and ultimately, improved investment performance.

The Fourier Transform and the Hodrick-Prescott Filter are powerful tools for financial time series analysis. Each technique offers unique benefits, with the Fourier Transform being adept at identifying dominant cycles and frequencies, and the HP Filter excelling at isolating long-term trends from short-term noise. By combining these methodologies, traders can develop a deeper understanding of the underlying dynamics of financial time series, leading to more informed investment decisions and improved trading strategies. As the financial markets continue to evolve, the combined application of these techniques will undoubtedly remain an essential aspect of modern financial analysis.

█ Features

Endpointed and Non-repainting

This is an endpointed and non-repainting indicator. These are crucial factors that contribute to its usefulness and reliability in trading and investment strategies. Let us break down these concepts and discuss why they matter in the context of a financial indicator.

1. Endpoint nature: An endpoint indicator uses the most recent data points to calculate its values, ensuring that the output is timely and reflective of the current market conditions. This is in contrast to non-endpoint indicators, which may use earlier data points in their calculations, potentially leading to less timely or less relevant results. By utilizing the most recent data available, the endpoint nature of this indicator ensures that it remains up-to-date and relevant, providing traders and investors with valuable and actionable insights into the market dynamics.

2. Non-repainting characteristic: A non-repainting indicator is one that does not change its values or signals after they have been generated. This means that once a signal or a value has been plotted on the chart, it will remain there, and future data will not affect it. This is crucial for traders and investors, as it offers a sense of consistency and certainty when making decisions based on the indicator's output.

Repainting indicators, on the other hand, can change their values or signals as new data comes in, effectively "repainting" the past. This can be problematic for several reasons:

a. Misleading results: Repainting indicators can create the illusion of a highly accurate or successful trading system when backtesting, as the indicator may adapt its past signals to fit the historical price data. This can lead to overly optimistic performance results that may not hold up in real-time trading.

b. Decision-making uncertainty: When an indicator repaints, it becomes challenging for traders and investors to trust its signals, as the signal that prompted a trade may change or disappear after the fact. This can create confusion and indecision, making it difficult to execute a consistent trading strategy.

The endpoint and non-repainting characteristics of this indicator contribute to its overall reliability and effectiveness as a tool for trading and investment decision-making. By providing timely and consistent information, this indicator helps traders and investors make well-informed decisions that are less likely to be influenced by misleading or shifting data.

Inputs

Source: This input determines the source of the price data to be used for the calculations. Users can select from options like closing price, opening price, high, low, etc., based on their preferences. Changing the source of the price data (e.g., from closing price to opening price) will alter the base data used for calculations, which may lead to different patterns and cycles being identified.

Calculation Bars: This input represents the number of past bars used for the calculation. A higher value will use more historical data for the analysis, while a lower value will focus on more recent price data. Increasing the number of past bars used for calculation will incorporate more historical data into the analysis. This may lead to a more comprehensive understanding of long-term trends but could also result in a slower response to recent price changes. Decreasing this value will focus more on recent data, potentially making the indicator more responsive to short-term fluctuations.

Harmonic Period: This input represents the harmonic period, which is the number of harmonics used in the Fourier Transform. A higher value will result in more harmonics being used, potentially capturing more complex cycles in the price data. Increasing the harmonic period will include more harmonics in the Fourier Transform, potentially capturing more complex cycles in the price data. However, this may also introduce more noise and make it harder to identify clear patterns. Decreasing this value will focus on simpler cycles and may make the analysis clearer, but it might miss out on more complex patterns.

Frequency Tolerance: This input represents the frequency tolerance, which determines how close the frequencies of the harmonics must be to be considered part of the same cycle. A higher value will allow for more variation between harmonics, while a lower value will require the frequencies to be more similar. Increasing the frequency tolerance will allow for more variation between harmonics, potentially capturing a broader range of cycles. However, this may also introduce noise and make it more difficult to identify clear patterns. Decreasing this value will require the frequencies to be more similar, potentially making the analysis clearer, but it might miss out on some cycles.

Number of Bars to Render: This input determines the number of bars to render on the chart. A higher value will result in more historical data being displayed, but it may also slow down the computation due to the increased amount of data being processed. Increasing the number of bars to render on the chart will display more historical data, providing a broader context for the analysis. However, this may also slow down the computation due to the increased amount of data being processed. Decreasing this value will speed up the computation, but it will provide less historical context for the analysis.

Smoothing Mode: This input allows the user to choose between two smoothing modes for the source price data: no smoothing or Hodrick-Prescott (HP) smoothing. The choice depends on the user's preference for how the price data should be processed before the Fourier Transform is applied. Choosing between no smoothing and Hodrick-Prescott (HP) smoothing will affect the preprocessing of the price data. Using HP smoothing will remove some of the short-term fluctuations from the data, potentially making the analysis clearer and more focused on longer-term trends. Not using smoothing will retain the original price fluctuations, which may provide more detail but also introduce noise into the analysis.

Hodrick-Prescott Filter Period: This input represents the Hodrick-Prescott filter period, which is used if the user chooses to apply HP smoothing to the price data. A higher value will result in a smoother curve, while a lower value will retain more of the original price fluctuations. Increasing the Hodrick-Prescott filter period will result in a smoother curve for the price data, emphasizing longer-term trends and minimizing short-term fluctuations. Decreasing this value will retain more of the original price fluctuations, potentially providing more detail but also introducing noise into the analysis.

Alets and signals

This indicator featues alerts, signals and bar coloring. You have to option to turn these on/off in the settings menu.

Maximum Bars Restriction

This indicator requires a large amount of processing power to render on the chart. To reduce overhead, the setting "Number of Bars to Render" is set to 500 bars. You can adjust this to you liking.

█ Related Indicators and Libraries

Goertzel Cycle Composite Wave

Goertzel Browser

Fourier Spectrometer of Price w/ Extrapolation Forecast

Fourier Extrapolator of 'Caterpillar' SSA of Price

Normalized, Variety, Fast Fourier Transform Explorer

Real-Fast Fourier Transform of Price Oscillator

Real-Fast Fourier Transform of Price w/ Linear Regression

Fourier Extrapolation of Variety Moving Averages

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolator of Price w/ Projection Forecast

Fourier Extrapolator of Price

STD-Stepped Fast Cosine Transform Moving Average

Variety RSI of Fast Discrete Cosine Transform

loxfft

harmonicpatterns1Library "harmonicpatterns1"

harmonicpatterns: methods required for calculation of harmonic patterns. Correction for library (missing export in line 303)

isGartleyPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isGartleyPattern: Checks for harmonic pattern Gartley

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Gartley. False otherwise.

isBatPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isBatPattern: Checks for harmonic pattern Bat

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Bat. False otherwise.

isButterflyPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isButterflyPattern: Checks for harmonic pattern Butterfly

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Butterfly. False otherwise.

isCrabPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isCrabPattern: Checks for harmonic pattern Crab

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Crab. False otherwise.

isDeepCrabPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isDeepCrabPattern: Checks for harmonic pattern DeepCrab

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is DeepCrab. False otherwise.

isCypherPattern(xabRatio, axcRatio, xadRatio, err_min, err_max) isCypherPattern: Checks for harmonic pattern Cypher

Parameters:

xabRatio : AB/XA

axcRatio : XC/AX

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Cypher. False otherwise.

isSharkPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isSharkPattern: Checks for harmonic pattern Shark

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Shark. False otherwise.

isNenStarPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isNenStarPattern: Checks for harmonic pattern Nenstar

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold