FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

Stocks

Script_Algo - ORB Strategy with Filters🔍 Core Concept: This strategy combines three powerful technical analysis tools: Range Breakout, the SuperTrend indicator, and a volume filter. Additionally, it features precise customization of the number of candles used to construct the breakout range, enabling optimized performance for specific assets.

🎯 How It Works:

The strategy defines a trading range at the beginning of the trading session based on a selected number of candles.

It waits for a breakout above the upper or below the lower boundary of this range, requiring a candle close.

It filters signals using the SuperTrend indicator for trend confirmation.

It utilizes trading volume to filter out false breakouts.

⚡ Strategy Features

📈 Entry Points:

Long: Candle close above the upper range boundary + SuperTrend confirmation

Short: Candle close below the lower range boundary + SuperTrend confirmation

🛡️ Risk Management:

Stop-Loss: Set at the opposite range boundary.

Take-Profit: Calculated based on a risk/reward ratio (3:1 by default).

Position Size: 10 contracts (configurable).

⚠️ IMPORTANT SETTINGS

🕐 Time Parameters:

Set the correct time and time zone!

❕ATTENTION: The strategy works ONLY with correct time settings! Set the time corresponding to your location and trading session.

📊 This strategy is optimized for trading TESLA stock!

Parameters are tailored to TESLA's volatility, and trading volumes are adequate for signal filtering. Trading time corresponds to the American session.

📈 If you look at the backtesting results, you can see that the strategy could potentially have generated about 70 percent profit on Tesla stock over six months on 5m timeframe. However, this does not guarantee that results will be repeated in the future; remain vigilant.

⚠️ For other assets, the following is required:

Testing and parameter optimization

Adjustment of time intervals and the number of candles forming the range

Calibration of stop-loss and take-profit levels

⚠️ Limitations and Drawbacks

🔗 Automation Constraints:

❌ Cannot be directly connected via Webhook to CFD brokers!

Additional IT solutions are required for automation, thus only manual trading based on signals is possible.

📉 Risk Management:

Do not risk more than 2-3% of your account per trade.

Test on historical data before live use.

Start with a demo account.

💪 Strategy Advantages

✅ Combined approach – multiple signal filters

✅ Clear entry and exit rules

✅ Visual signals on the chart

✅ Volume-based false breakout filtering

✅ Automatic position management

🎯 Usage Recommendations

Always test the strategy on historical data.

Start with small trading volumes.

Ensure time settings are correct.

Adapt parameters to current market volatility.

Use only for stocks – futures and Forex require adaptation.

📚 Suitable Timeframes - M1-M15

Only highly liquid stocks

🍀 I wish all subscribers good luck in trading and steady profits!

📈 May your charts move in the right direction!

⚠️ Remember: Trading involves risk. Do not invest money you cannot afford to lose!

[SHORT ONLY] 10 Bar Low Pullback█ STRATEGY DESCRIPTION

The "10 Bar Low Pullback" strategy is a contrarian short trading system designed to capture pullbacks after a new 10‐bar low is made. it identifies a potential short opportunity when the current bar’s low breaks below the lowest low of the previous 10 bars, provided that the bar exhibits strong internal momentum as measured by its IBS value. An optional trend filter further refines entries by requiring that the close is below a 200-period EMA.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

ibs = (close - low) / (high - low)

- Low IBS (≤ 0.2): Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8): Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current bar’s low is below the lowest low of the past X bars (default: 10).

The bar’s IBS is greater than the specified threshold (default: 0.85).

The signal occurs within the defined trading window (between Start Time and End Time).

If the EMA Filter is enabled, the close must be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

Lookback Period: Defines the number of bars (default is 10) over which the lowest low is calculated.

IBS Threshold: Sets the minimum required IBS value (default is 0.85) to qualify as a pullback.

Trading Window: Trades are only executed between the user-defined Start Time and End Time.

EMA Filter (Optional): When enabled, short entries are only considered if the current close is below the 200-period EMA, with the EMA period being adjustable (default is 200).

█ PERFORMANCE OVERVIEW

Designed for shorting opportunities, this strategy aims to capture pullbacks following an aggressive 10-bar low break.

It leverages a combination of a lookback low and IBS measurement to identify overextended bullish moves that may revert.

The optional EMA filter helps confirm a bearish market environment by ensuring the price remains under the trend line.

Suitable for use on various assets, including stocks and ETFs, on daily or similar timeframes.

Backtesting and parameter optimization are recommended to tailor the strategy to specific market conditions.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

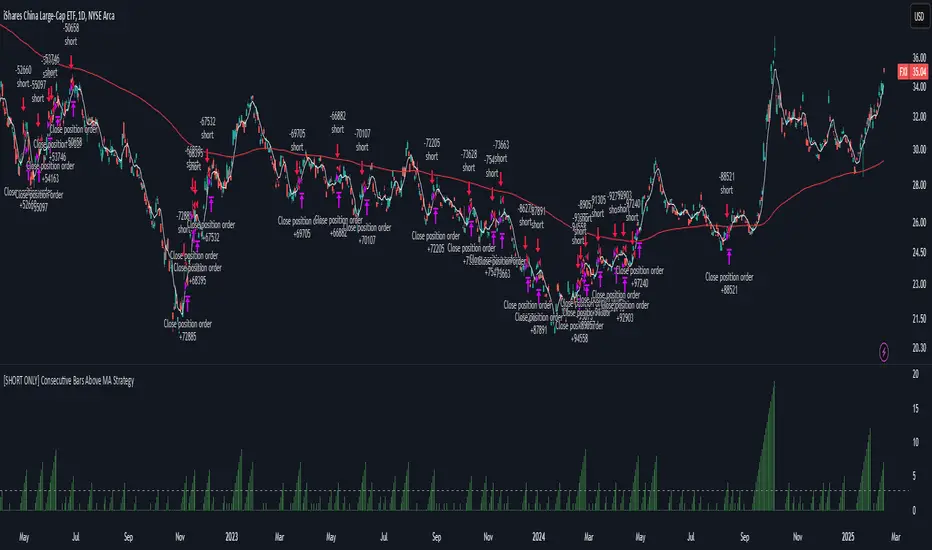

[SHORT ONLY] Consecutive Bars Above MA Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above MA Strategy" is a contrarian trading system aimed at exploiting overextended bullish moves in stocks and ETFs. It monitors the number of consecutive bars that close above a chosen short-term moving average (which can be either a Simple Moving Average or an Exponential Moving Average). Once the count reaches a preset threshold and the current bar’s close exceeds the previous bar’s high within a designated trading window, a short entry is initiated. An optional EMA filter further refines entries by requiring that the current close is below the 200-period EMA, helping to ensure that trades are taken in a bearish environment.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy utilizes a counter variable, `bullCount`, to track consecutive bullish bars based on their relation to the short-term moving average. Here’s how the count is determined:

Initialize the Counter

The counter is initialized at the start:

var int bullCount = na

Bullish Bar Detection

For each bar, if the close is above the selected moving average (either SMA or EMA, based on user input), the counter is incremented:

bullCount := close > signalMa ? (na(bullCount) ? 1 : bullCount + 1) : 0

Reset on Non-Bullish Condition

If the close does not exceed the moving average, the counter resets to zero, indicating a break in the consecutive bullish streak.

█ SIGNAL GENERATION

1. SHORT ENTRY

A short signal is generated when:

The number of consecutive bullish bars (i.e., bars closing above the short-term MA) meets or exceeds the defined threshold (default: 3).

The current bar’s close is higher than the previous bar’s high.

The signal occurs within the specified trading window (between Start Time and End Time).

Additionally, if the EMA filter is enabled, the entry is only executed when the current close is below the 200-period EMA.

2. EXIT CONDITION

An exit signal is triggered when the current close falls below the previous bar’s low, prompting the strategy to close the short position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish bars required to trigger a short entry (default is 3).

Trading Window: The Start Time and End Time inputs define when the strategy is active.

Moving Average Settings: Choose between SMA and EMA, and set the MA length (default is 5), which is used to assess each bar’s bullish condition.

EMA Filter (Optional): When enabled, this filter requires that the current close is below the 200-period EMA, supporting entries in a downtrend.

█ PERFORMANCE OVERVIEW

This strategy is designed for stocks and ETFs and can be applied across various timeframes.

It seeks to capture mean reversion by shorting after a series of bullish bars suggests an overextended move.

The approach employs a contrarian short entry by waiting for a breakout (close > previous high) following consecutive bullish bars.

The adjustable moving average settings and optional EMA filter allow for further optimization based on market conditions.

Comprehensive backtesting is recommended to fine-tune the threshold, moving average parameters, and filter settings for optimal performance.

[SHORT ONLY] Consecutive Close>High[1] Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Consecutive Close > High " Mean Reversion Strategy is a contrarian daily trading system for stocks and ETFs. It identifies potential shorting opportunities by counting consecutive days where the closing price exceeds the previous day's high. When this consecutive day count reaches a predetermined threshold, and if the close is below a 200-period EMA (if enabled), a short entry is triggered, anticipating a corrective pullback.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy uses a counter variable called `bullCount` to track how many consecutive bars meet a bullish condition. Here’s a breakdown of the process:

Initialize the Counter

var int bullCount = 0

Bullish Bar Detection

Every time the close exceeds the previous bar's high, increment the counter:

if close > high

bullCount += 1

Reset on Bearish Bar

When there is a clear bearish reversal, the counter is reset to zero:

if close < low

bullCount := 0

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The count of consecutive bullish closes (where close > high ) reaches or exceeds the defined threshold (default: 3).

The signal occurs within the specified trading window (between Start Time and End Time).

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish closes required to trigger a short entry (default is 3).

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

EMA Filter (Optional): When enabled, short entries are only triggered if the current close is below the 200-period EMA.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs on the Daily timeframe and targets overextended bullish moves.

It aims to capture mean reversion by entering short after a series of consecutive bullish closes.

Further optimization is possible with additional filters (e.g., EMA, volume, or volatility).

Backtesting should be used to fine-tune the threshold and filter settings for specific market conditions.

[SHORT ONLY] Internal Bar Strength (IBS) Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a short position when the IBS indicates overbought conditions and exits when the IBS reaches oversold levels. This strategy is Short-Only and was designed to be used on the Daily timeframe for Stocks and ETFs.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- Low IBS (≤ 0.2) : Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8) : Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The IBS value rises to or above the Upper Threshold (default: 0.9).

The Closing price is greater than the previous bars High (close>high ).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

An exit Signal is generated when the IBS value drops to or below the Lower Threshold (default: 0.3). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy enters trades. Default is 0.9.

Lower Threshold: The IBS level at which the strategy exits short positions. Default is 0.3.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs markets and performs best when prices frequently revert to the mean.

The strategy can be optimized further using additional conditions such as using volume or volatility filters.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

Statistical Arbitrage Pairs Trading - Long-Side OnlyThis strategy implements a simplified statistical arbitrage (" stat arb ") approach focused on mean reversion between two correlated instruments. It identifies opportunities where the spread between their normalized price series (Z-scores) deviates significantly from historical norms, then executes long-only trades anticipating reversion to the mean.

Key Mechanics:

1. Spread Calculation: The strategy computes Z-scores for both instruments to normalize price movements, then tracks the spread between these Z-scores.

2. Modified Z-Score: Uses a robust measure combining the median and Median Absolute Deviation (MAD) to reduce outlier sensitivity.

3. Entry Signal: A long position is triggered when the spread’s modified Z-score falls below a user-defined threshold (e.g., -1.0), indicating extreme undervaluation of the main instrument relative to its pair.

4. Exit Signal: The position closes automatically when the spread reverts to its historical mean (Z-score ≥ 0).

Risk management:

Trades are sized as a percentage of equity (default: 10%).

Includes commissions and slippage for realistic backtesting.

Bearish Wick Reversal█ STRATEGY OVERVIEW

The "Bearish Wick Reversal Strategy" identifies potential bullish reversals following significant bearish price rejection (long lower wicks). This counter-trend approach enters long positions when bearish candles show exaggerated downside wicks relative to closing prices, then exits on bullish confirmation signals. Includes optional EMA trend filtering for improved reliability.

█ What is a Bearish Wick?

A price rejection pattern where:

Bearish candle (close < open) forms with extended lower wick

Wick represents failed selloff: Low drops significantly below close

Measured as: (Low - Close)/Close × 100 (Negative percentage indicates downward extension)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Bearish candle forms with close < open

Lower wick exceeds user-defined threshold (Default: -1% of close price)

The signal occurs within the specified time window

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average)

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: Volatile instruments with frequent price rejections

Key Risk: False signals in sustained bearish trends

Optimization Tip: Test various thresholds

Filter Impact: EMA reduces trades but improves win rate and reduces drawdown

Gap Down Reversal Strategy█ STRATEGY OVERVIEW

The "Gap Down Reversal Strategy" capitalizes on price recovery patterns following bearish gap-down openings. This mean-reversion approach enters long positions on confirmed intraday recoveries and exits when prices breach previous session highs. This strategy is NOT optimized.

█ What is a Gap Down Reversal?

A gap down reversal occurs when:

An instrument opens significantly below its prior session's low (price gap)

Selling pressure exhausts itself during the session

Buyers regain control, pushing price back above the opening level

Creates a candlestick with:

• Open < Prior Session Low (true gap)

• Close > Open (bullish reversal candle)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Previous candle closes BELOW its opening price (bearish candle)

Current session opens BELOW prior candle's low (gap down)

Current candle closes ABOVE its opening price (bullish reversal)

Executes market order at session close

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: High volatility instruments with frequent gaps

Key Risk: False reversals in sustained downtrends

Optimization Tip: Test varying gap thresholds (1-3% ranges)

3 Down, 3 Up Strategy█ STRATEGY DESCRIPTION

The "3 Down, 3 Up Strategy" is a mean-reversion strategy designed to capitalize on short-term price reversals. It enters a long position after consecutive bearish closes and exits after consecutive bullish closes. This strategy is NOT optimized and can be used on any timeframes.

█ WHAT ARE CONSECUTIVE DOWN/UP CLOSES?

- Consecutive Down Closes: A sequence of trading bars where each close is lower than the previous close.

- Consecutive Up Closes: A sequence of trading bars where each close is higher than the previous close.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The price closes lower than the previous close for Consecutive Down Closes for Entry (default: 3) consecutive bars.

The signal occurs within the specified time window (between Start Time and End Time).

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average).

2. EXIT CONDITION

A Sell Signal is generated when the price closes higher than the previous close for Consecutive Up Closes for Exit (default: 3) consecutive bars.

█ ADDITIONAL SETTINGS

Consecutive Down Closes for Entry: Number of consecutive lower closes required to trigger a buy. Default = 3.

Consecutive Up Closes for Exit: Number of consecutive higher closes required to exit. Default = 3.

EMA Filter: Optional 200-period EMA filter to confirm long entries in bullish trends. Default = disabled.

Start Time and End Time: Restrict trading to specific dates (default: 2014-2099).

█ PERFORMANCE OVERVIEW

Designed for volatile markets with frequent short-term reversals.

Performs best when price oscillates between clear support/resistance levels.

The EMA filter improves reliability in trending markets but may reduce trade frequency.

Backtest to optimize consecutive close thresholds and EMA period for specific instruments.

Internal Bar Strength (IBS) Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a long position when the IBS indicates oversold conditions and exits when the IBS reaches overbought levels. This strategy was designed to be used on the daily timeframe.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- **Low IBS (≤ 0.2)**: Indicates the close is near the bar's low, suggesting oversold conditions.

- **High IBS (≥ 0.8)**: Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The IBS value drops below the Lower Threshold (default: 0.2).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the IBS value rises to or above the Upper Threshold (default: 0.8). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy exits trades. Default is 0.8.

Lower Threshold: The IBS level at which the strategy enters long positions. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for ranging markets and performs best when prices frequently revert to the mean.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

Buy on 5 day low Strategy█ STRATEGY DESCRIPTION

The "Buy on 5 Day Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous five days. It enters a long position when specific conditions are met and exits when the price exceeds the high of the previous day. This strategy is optimized for use on daily or higher timeframes.

█ WHAT IS THE 5-DAY LOW?

The 5-Day Low is the lowest price observed over the last five days. This level is used as a reference to identify potential oversold conditions and reversal points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous five days (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous day (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support levels.

It is sensitive to oversold conditions, as indicated by the 5-Day Low, and overbought conditions, as indicated by the previous day's high.

Backtesting results should be analyzed to optimize the strategy for specific instruments and market conditions.

3-Bar Low Strategy█ STRATEGY DESCRIPTION

The "3-Bar Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous three bars. It enters a long position when specific conditions are met and exits when the price exceeds the highest high of the previous seven bars. This strategy is suitable for use on various timeframes.

█ WHAT IS THE 3-BAR LOW?

The 3-Bar Low is the lowest price observed over the last three bars. This level is used as a reference to identify potential oversold conditions and reversal points.

█ WHAT IS THE 7-BAR HIGH?

The 7-Bar High is the highest price observed over the last seven bars. This level is used as a reference to identify potential overbought conditions and exit points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous three bars (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

If the EMA Filter is enabled, the close price must also be above the 200-period Exponential Moving Average (EMA).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

MA Period: The lookback period for the 200-period EMA used in the EMA Filter. Default is 200.

Use EMA Filter: Enables or disables the EMA Filter for long entries. Default is disabled.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support and resistance levels.

It is sensitive to oversold conditions, as indicated by the 3-Bar Low, and overbought conditions, as indicated by the 7-Bar High.

Backtesting results should be analyzed to optimize the MA Period and EMA Filter settings for specific instruments.

Bollinger Bands Reversal + IBS Strategy█ STRATEGY DESCRIPTION

The "Bollinger Bands Reversal Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price deviates below the lower Bollinger Band and the Internal Bar Strength (IBS) indicates oversold conditions. It enters a long position when specific conditions are met and exits when the IBS indicates overbought conditions. This strategy is suitable for use on various timeframes.

█ WHAT ARE BOLLINGER BANDS?

Bollinger Bands consist of three lines:

- **Basis**: A Simple Moving Average (SMA) of the price over a specified period.

- **Upper Band**: The basis plus a multiple of the standard deviation of the price.

- **Lower Band**: The basis minus a multiple of the standard deviation of the price.

Bollinger Bands help identify periods of high volatility and potential reversal points.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) is a measure of where the closing price is relative to the high and low of the bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

A low IBS value (e.g., below 0.2) indicates that the close is near the low of the bar, suggesting oversold conditions. A high IBS value (e.g., above 0.8) indicates that the close is near the high of the bar, suggesting overbought conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The IBS value is below 0.2, indicating oversold conditions.

The close price is below the lower Bollinger Band.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the IBS value exceeds 0.8, indicating overbought conditions. This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Length: The lookback period for calculating the Bollinger Bands. Default is 20.

Multiplier: The number of standard deviations used to calculate the upper and lower Bollinger Bands. Default is 2.0.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently deviates from the Bollinger Bands.

It is sensitive to oversold and overbought conditions, as indicated by the IBS, which helps to identify potential reversals.

Backtesting results should be analyzed to optimize the Length and Multiplier parameters for specific instruments.

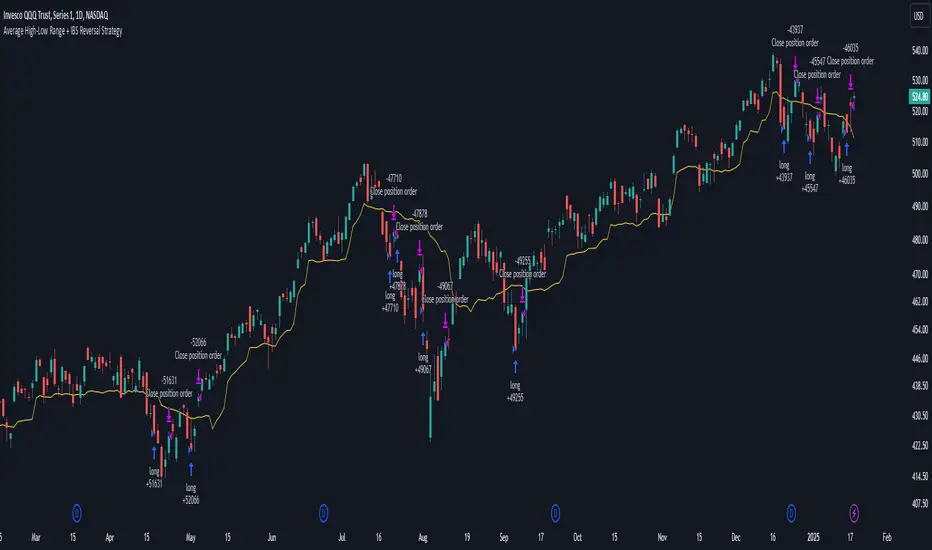

Average High-Low Range + IBS Reversal Strategy█ STRATEGY DESCRIPTION

The "Average High-Low Range + IBS Reversal Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price deviates significantly from its average high-low range and the Internal Bar Strength (IBS) indicates oversold conditions. It enters a long position when specific conditions are met and exits when the price shows strength by exceeding the previous bar's high. This strategy is suitable for use on various timeframes.

█ WHAT IS THE AVERAGE HIGH-LOW RANGE?

The Average High-Low Range is calculated as the Simple Moving Average (SMA) of the difference between the high and low prices over a specified period. It helps identify periods of increased volatility and potential reversal points.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) is a measure of where the closing price is relative to the high and low of the bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

A low IBS value (e.g., below 0.2) indicates that the close is near the low of the bar, suggesting oversold conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been below the buy threshold (calculated as `upper - (2.5 * hl_avg)`) for a specified number of consecutive bars (`bars_below_threshold`).

The IBS value is below the specified buy threshold (`ibs_buy_treshold`).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Length: The lookback period for calculating the average high-low range. Default is 20.

Bars Below Threshold: The number of consecutive bars the price must remain below the buy threshold to trigger a Buy Signal. Default is 2.

IBS Buy Threshold: The IBS value below which a Buy Signal is triggered. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently deviates from its average high-low range.

It is sensitive to oversold conditions, as indicated by the IBS, which helps to identify potential reversals.

Backtesting results should be analyzed to optimize the Length, Bars Below Threshold, and IBS Buy Threshold parameters for specific instruments.

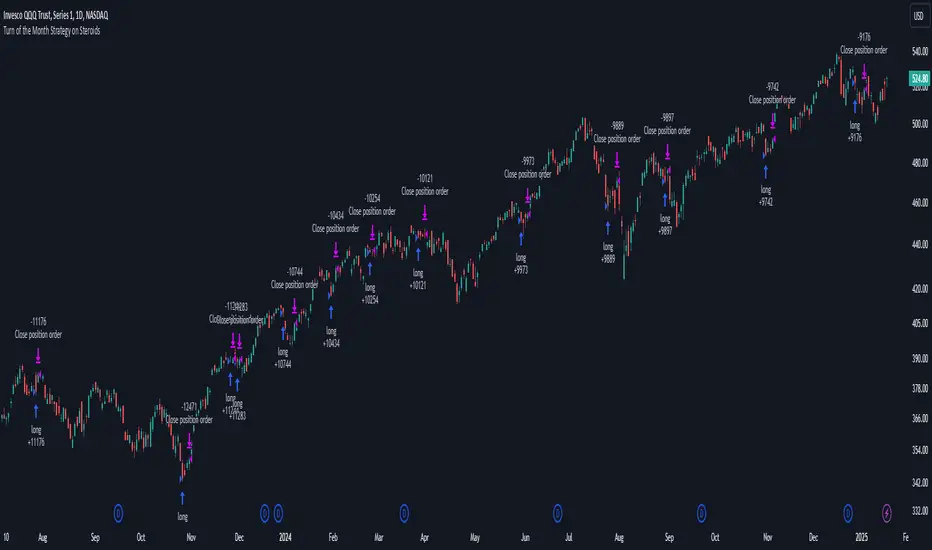

Turn of the Month Strategy on Steroids█ STRATEGY DESCRIPTION

The "Turn of the Month Strategy on Steroids" is a seasonal mean-reversion strategy designed to capitalize on price movements around the end of the month. It enters a long position when specific conditions are met and exits when the Relative Strength Index (RSI) indicates overbought conditions. This strategy is optimized for use on daily or higher timeframes.

█ WHAT IS THE TURN OF THE MONTH EFFECT?

The Turn of the Month effect refers to the observed tendency of stock prices to rise around the end of the month. This strategy leverages this phenomenon by entering long positions when the price shows signs of a reversal during this period.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The current day of the month is greater than or equal to the specified `dayOfMonth` threshold (default is 25).

The close price is lower than the previous day's close (`close < close `).

The previous day's close is also lower than the close two days ago (`close < close `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

There is no existing open position (`strategy.position_size == 0`).

2. EXIT CONDITION

A Sell Signal is generated when the 2-period RSI exceeds 65, indicating overbought conditions. This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Day of Month: The day of the month threshold for triggering a Buy Signal. Default is 25.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed to exploit seasonal price patterns around the end of the month.

It performs best in markets where the Turn of the Month effect is pronounced.

Backtesting results should be analyzed to optimize the `dayOfMonth` threshold and RSI parameters for specific instruments.

Consecutive Bearish Candle Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bearish Candle Strategy" is a momentum-based strategy designed to identify potential reversals after a sustained bearish move. It enters a long position when a specific number of consecutive bearish candles occur and exits when the price shows strength by exceeding the previous bar's high. This strategy is optimized for use on various timeframes and instruments.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been lower than the previous close for at least `Lookback` consecutive bars. This indicates a sustained bearish move, suggesting a potential reversal.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Lookback: The number of consecutive bearish bars required to trigger a Buy Signal. Default is 3.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for markets with frequent momentum shifts.

It performs best in volatile conditions where price movements are significant.

Backtesting results should be analysed to optimize the `Lookback` parameter for specific instruments.

4 Bar Momentum Reversal strategy█ STRATEGY DESCRIPTION

The "4 Bar Momentum Reversal Strategy" is a mean-reversion strategy designed to identify price reversals following a sustained downward move. It enters a long position when a reversal condition is met and exits when the price shows strength by exceeding the previous bar's high. This strategy is optimized for indices and stocks on the daily timeframe.

█ WHAT IS THE REFERENCE CLOSE?

The Reference Close is the closing price from X bars ago, where X is determined by the Lookback period. Think of it as a moving benchmark that helps the strategy assess whether prices are trending upwards or downwards relative to past performance. For example, if the Lookback is set to 4, the Reference Close is the closing price 4 bars ago (`close `).

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been lower than the Reference Close for at least `Buy Threshold` consecutive bars. This indicates a sustained downward move, suggesting a potential reversal.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Buy Threshold: The number of consecutive bearish bars needed to trigger a Buy Signal. Default is 4.

Lookback: The number of bars ago used to calculate the Reference Close. Default is 4.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for trending markets with frequent reversals.

It performs best in volatile conditions where price movements are significant.

Backtesting results should be analysed to optimize the Buy Threshold and Lookback parameters for specific instruments.

Simple RSI stock Strategy [1D] The "Simple RSI Stock Strategy " is designed to long-term traders. Strategy uses a daily time frame to capitalize on signals generated by the Relative Strength Index (RSI) and the Simple Moving Average (SMA). This strategy is suitable for low-leverage trading environments and focuses on identifying potential buy opportunities when the market is oversold, while incorporating strong risk management with both dynamic and static Stop Loss mechanisms.

This strategy is recommended for use with a relatively small amount of capital and is best applied by diversifying across multiple stocks in a strong uptrend, particularly in the S&P 500 stock market. It is specifically designed for equities, and may not perform well in other markets such as commodities, forex, or cryptocurrencies, where different market dynamics and volatility patterns apply.

Indicators Used in the Strategy:

1. RSI (Relative Strength Index):

- The RSI is a momentum oscillator used to identify overbought and oversold conditions in the market.

- This strategy enters long positions when the RSI drops below the oversold level (default: 30), indicating a potential buying opportunity.

- It focuses on oversold conditions but uses a filter (SMA 200) to ensure trades are only made in the context of an overall uptrend.

2. SMA 200 (Simple Moving Average):

- The 200-period SMA serves as a trend filter, ensuring that trades are only executed when the price is above the SMA, signaling a bullish market.

- This filter helps to avoid entering trades in a downtrend, thereby reducing the risk of holding positions in a declining market.

3. ATR (Average True Range):

- The ATR is used to measure market volatility and is instrumental in setting the Stop Loss.

- By multiplying the ATR value by a custom multiplier (default: 1.5), the strategy dynamically adjusts the Stop Loss level based on market volatility, allowing for flexibility in risk management.

How the Strategy Works:

Entry Signals:

The strategy opens long positions when RSI indicates that the market is oversold (below 30), and the price is above the 200-period SMA. This ensures that the strategy buys into potential market bottoms within the context of a long-term uptrend.

Take Profit Levels:

The strategy defines three distinct Take Profit (TP) levels:

TP 1: A 5% from the entry price.

TP 2: A 10% from the entry price.

TP 3: A 15% from the entry price.

As each TP level is reached, the strategy closes portions of the position to secure profits: 33% of the position is closed at TP 1, 66% at TP 2, and 100% at TP 3.

Visualizing Target Points:

The strategy provides visual feedback by plotting plotshapes at each Take Profit level (TP 1, TP 2, TP 3). This allows traders to easily see the target profit levels on the chart, making it easier to monitor and manage positions as they approach key profit-taking areas.

Stop Loss Mechanism:

The strategy uses a dual Stop Loss system to effectively manage risk:

ATR Trailing Stop: This dynamic Stop Loss adjusts based on the ATR value and trails the price as the position moves in the trader’s favor. If a price reversal occurs and the market begins to trend downward, the trailing stop closes the position, locking in gains or minimizing losses.

Basic Stop Loss: Additionally, a fixed Stop Loss is set at 25%, limiting potential losses. This basic Stop Loss serves as a safeguard, automatically closing the position if the price drops 25% from the entry point. This higher Stop Loss is designed specifically for low-leverage trading, allowing more room for market fluctuations without prematurely closing positions.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

Together, these mechanisms ensure that the strategy dynamically manages risk while offering robust protection against significant losses in case of sharp market downturns.

The position size has been estimated by me at 75% of the total capital. For optimal capital allocation, a recommended value based on the Kelly Criterion, which is calculated to be 59.13% of the total capital per trade, can also be considered.

Enjoy !

Unlock the Power of Seasonality: Monthly Performance StrategyThe Monthly Performance Strategy leverages the power of seasonality—those cyclical patterns that emerge in financial markets at specific times of the year. From tax deadlines to industry-specific events and global holidays, historical data shows that certain months can offer strong opportunities for trading. This strategy was designed to help traders capture those opportunities and take advantage of recurring market patterns through an automated and highly customizable approach.

The Inspiration Behind the Strategy:

This strategy began with the idea that market performance is often influenced by seasonal factors. Historically, certain months outperform others due to a variety of reasons, like earnings reports, holiday shopping, or fiscal year-end events. By identifying these periods, traders can better time their market entries and exits, giving them an advantage over those who solely rely on technical indicators or news events.

The Monthly Performance Strategy was built to take this concept and automate it. Instead of manually analyzing market data for each month, this strategy enables you to select which months you want to focus on and then executes trades based on predefined rules, saving you time and optimizing the performance of your trades.

Key Features:

Customizable Month Selection: The strategy allows traders to choose specific months to test or trade on. You can select any combination of months—for example, January, July, and December—to focus on based on historical trends. Whether you’re targeting the historically strong months like December (often driven by the 'Santa Rally') or analyzing quieter months for low volatility trades, this strategy gives you full control.

Automated Monthly Entries and Exits: The strategy automatically enters a long position on the first day of your selected month(s) and exits the trade at the beginning of the next month. This makes it perfect for traders who want to benefit from seasonal patterns without manually monitoring the market. It ensures precision in entering and exiting trades based on pre-set timeframes.

Re-entry on Stop Loss or Take Profit: One of the standout features of this strategy is its ability to re-enter a trade if a position hits the stop loss (SL) or take profit (TP) level during the selected month. If your trade reaches either a SL or TP before the month ends, the strategy will automatically re-enter a new trade the next trading day. This feature ensures that you capture multiple trading opportunities within the same month, instead of exiting entirely after a successful or unsuccessful trade. Essentially, it keeps your capital working for you throughout the entire month, not just when conditions align perfectly at the beginning.

Built-in Risk Management: Risk management is a vital part of this strategy. It incorporates an Average True Range (ATR)-based stop loss and take profit system. The ATR helps set dynamic levels based on the market’s volatility, ensuring that your stops and targets adjust to changing market conditions. This not only helps limit potential losses but also maximizes profit potential by adapting to market behavior.

Historical Performance Testing: You can backtest this strategy on any period by setting the start year. This allows traders to analyze past market data and optimize their strategy based on historical performance. You can fine-tune which months to trade based on years of data, helping you identify trends and patterns that provide the best trading results.

Versatility Across Asset Classes: While this strategy can be particularly effective for stock market indices and sector rotation, it’s versatile enough to apply to other asset classes like forex, commodities, and even cryptocurrencies. Each asset class may exhibit different seasonal behaviors, allowing you to explore opportunities across various markets with this strategy.

How It Works:

The trader selects which months to test or trade, for example, January, April, and October.

The strategy will automatically open a long position on the first trading day of each selected month.

If the trade hits either the take profit or stop loss within the month, the strategy will close the current position and re-enter a new trade on the next trading day, provided the month has not yet ended. This ensures that the strategy continues to capture any potential gains throughout the month, rather than stopping after one successful trade.

At the start of the next month, the position is closed, and if the next month is also selected, a new trade is initiated following the same process.

Risk Management and Dynamic Adjustments:

Incorporating risk management with this strategy is as easy as turning on the ATR-based system. The strategy will automatically calculate stop loss and take profit levels based on the market’s current volatility, adjusting dynamically to the conditions. This ensures that the risk is controlled while allowing for flexibility in capturing profits during both high and low volatility periods.

Maximizing the Seasonal Edge:

By automating entries and exits based on specific months and combining that with dynamic risk management, the Ultimate Monthly Performance Strategy takes advantage of seasonal patterns without requiring constant monitoring. The added re-entry feature after hitting a stop loss or take profit ensures that you are always in the game, maximizing your chances to capture profitable trades during favorable seasonal periods.

Who Can Benefit from This Strategy?

This strategy is perfect for traders who:

Want to exploit the predictable, recurring patterns that occur during specific months of the year.

Prefer a hands-off, automated trading approach that allows them to focus on other aspects of their portfolio or life.

Seek to manage risk effectively with ATR-based stop losses and take profits that adjust to market conditions.

Appreciate the ability to re-enter trades when a take profit or stop loss is hit within the month, ensuring that they don't miss out on multiple opportunities during a favorable period.

In summary, the Ultimate Monthly Performance Strategy provides traders with a comprehensive tool to capitalize on seasonal trends, optimize their trading opportunities throughout the year, and manage risk effectively. The built-in re-entry system ensures you continue to benefit from the market even after hitting targets within the same month, making it a robust strategy for traders looking to maximize their edge in any market.

Risk Disclaimer:

Trading financial markets involves significant risk and may not be suitable for all investors. The Monthly Performance Strategy is designed to help traders identify seasonal trends, but past performance does not guarantee future results. It is important to carefully consider your risk tolerance, financial situation, and trading goals before using any strategy. Always use appropriate risk management and consult with a professional financial advisor if necessary. The use of this strategy does not eliminate the risk of losses, and traders should be prepared for the possibility of losing their entire investment. Be sure to test the strategy on a demo account before applying it in live markets.

Multi-Step FlexiSuperTrend - Strategy [presentTrading]At the heart of this endeavor is a passion for continuous improvement in the art of trading

█ Introduction and How it is Different

The "Multi-Step FlexiSuperTrend - Strategy " is an advanced trading strategy that integrates the well-known SuperTrend indicator with a nuanced and dynamic approach to market trend analysis. Unlike conventional SuperTrend strategies that rely on static thresholds and fixed parameters, this strategy introduces multi-step take profit mechanisms that allow traders to capitalize on varying market conditions in a more controlled and systematic manner.

What sets this strategy apart is its ability to dynamically adjust to market volatility through the use of an incremental factor applied to the SuperTrend calculation. This adjustment ensures that the strategy remains responsive to both minor and major market shifts, providing a more accurate signal for entries and exits. Additionally, the integration of multi-step take profit levels offers traders the flexibility to scale out of positions, locking in profits progressively as the market moves in their favor.

BTC 6hr Long/Short Performance

█ Strategy, How it Works: Detailed Explanation

The Multi-Step FlexiSuperTrend strategy operates on the foundation of the SuperTrend indicator, but with several enhancements that make it more adaptable to varying market conditions. The key components of this strategy include the SuperTrend Polyfactor Oscillator, a dynamic normalization process, and multi-step take profit levels.

🔶 SuperTrend Polyfactor Oscillator

The SuperTrend Polyfactor Oscillator is the heart of this strategy. It is calculated by applying a series of SuperTrend calculations with varying factors, starting from a defined "Starting Factor" and incrementing by a specified "Increment Factor." The indicator length and the chosen price source (e.g., HLC3, HL2) are inputs to the oscillator.

The SuperTrend formula typically calculates an upper and lower band based on the average true range (ATR) and a multiplier (the factor). These bands determine the trend direction. In the FlexiSuperTrend strategy, the oscillator is enhanced by iteratively applying the SuperTrend calculation across different factors. The iterative process allows the strategy to capture both minor and significant trend changes.

For each iteration (indexed by `i`), the following calculations are performed:

1. ATR Calculation: The Average True Range (ATR) is calculated over the specified `indicatorLength`:

ATR_i = ATR(indicatorLength)

2. Upper and Lower Bands Calculation: The upper and lower bands are calculated using the ATR and the current factor:

Upper Band_i = hl2 + (ATR_i * Factor_i)

Lower Band_i = hl2 - (ATR_i * Factor_i)

Here, `Factor_i` starts from `startingFactor` and is incremented by `incrementFactor` in each iteration.

3. Trend Determination: The trend is determined by comparing the indicator source with the upper and lower bands:

Trend_i = 1 (uptrend) if IndicatorSource > Upper Band_i

Trend_i = 0 (downtrend) if IndicatorSource < Lower Band_i

Otherwise, the trend remains unchanged from the previous value.

4. Output Calculation: The output of each iteration is determined based on the trend:

Output_i = Lower Band_i if Trend_i = 1

Output_i = Upper Band_i if Trend_i = 0

This process is repeated for each iteration (from 0 to 19), creating a series of outputs that reflect different levels of trend sensitivity.

Local

🔶 Normalization Process

To make the oscillator values comparable across different market conditions, the deviations between the indicator source and the SuperTrend outputs are normalized. The normalization method can be one of the following:

1. Max-Min Normalization: The deviations are normalized based on the range of the deviations:

Normalized Value_i = (Deviation_i - Min Deviation) / (Max Deviation - Min Deviation)

2. Absolute Sum Normalization: The deviations are normalized based on the sum of absolute deviations:

Normalized Value_i = Deviation_i / Sum of Absolute Deviations

This normalization ensures that the oscillator values are within a consistent range, facilitating more reliable trend analysis.

For more details:

🔶 Multi-Step Take Profit Mechanism

One of the unique features of this strategy is the multi-step take profit mechanism. This allows traders to lock in profits at multiple levels as the market moves in their favor. The strategy uses three take profit levels, each defined as a percentage increase (for long trades) or decrease (for short trades) from the entry price.

1. First Take Profit Level: Calculated as a percentage increase/decrease from the entry price:

TP_Level1 = Entry Price * (1 + tp_level1 / 100) for long trades

TP_Level1 = Entry Price * (1 - tp_level1 / 100) for short trades

The strategy exits a portion of the position (defined by `tp_percent1`) when this level is reached.

2. Second Take Profit Level: Similar to the first level, but with a higher percentage:

TP_Level2 = Entry Price * (1 + tp_level2 / 100) for long trades

TP_Level2 = Entry Price * (1 - tp_level2 / 100) for short trades

The strategy exits another portion of the position (`tp_percent2`) at this level.

3. Third Take Profit Level: The final take profit level:

TP_Level3 = Entry Price * (1 + tp_level3 / 100) for long trades

TP_Level3 = Entry Price * (1 - tp_level3 / 100) for short trades

The remaining portion of the position (`tp_percent3`) is exited at this level.

This multi-step approach provides a balance between securing profits and allowing the remaining position to benefit from continued favorable market movement.

█ Trade Direction

The strategy allows traders to specify the trade direction through the `tradeDirection` input. The options are:

1. Both: The strategy will take both long and short positions based on the entry signals.

2. Long: The strategy will only take long positions.

3. Short: The strategy will only take short positions.

This flexibility enables traders to tailor the strategy to their market outlook or current trend analysis.

█ Usage

To use the Multi-Step FlexiSuperTrend strategy, traders need to set the input parameters according to their trading style and market conditions. The strategy is designed for versatility, allowing for various market environments, including trending and ranging markets.

Traders can also adjust the multi-step take profit levels and percentages to match their risk management and profit-taking preferences. For example, in highly volatile markets, traders might set wider take profit levels with smaller percentages at each level to capture larger price movements.

The normalization method and the incremental factor can be fine-tuned to adjust the sensitivity of the SuperTrend Polyfactor Oscillator, making the strategy more responsive to minor market shifts or more focused on significant trends.

█ Default Settings

The default settings of the strategy are carefully chosen to provide a balanced approach between risk management and profit potential. Here is a breakdown of the default settings and their effects on performance:

1. Indicator Length (10): This parameter controls the lookback period for the ATR calculation. A shorter length makes the strategy more sensitive to recent price movements, potentially generating more signals. A longer length smooths out the ATR, reducing sensitivity but filtering out noise.

2. Starting Factor (0.618): This is the initial multiplier used in the SuperTrend calculation. A lower starting factor makes the SuperTrend bands closer to the price, generating more frequent trend changes. A higher starting factor places the bands further away, filtering out minor fluctuations.

3. Increment Factor (0.382): This parameter controls how much the factor increases with each iteration of the SuperTrend calculation. A smaller increment factor results in more gradual changes in sensitivity, while a larger increment factor creates a wider range of sensitivity across the iterations.

4. Normalization Method (None): The default is no normalization, meaning the raw deviations are used. Normalization methods like Max-Min or Absolute Sum can make the deviations more consistent across different market conditions, improving the reliability of the oscillator.

5. Take Profit Levels (2%, 8%, 18%): These levels define the thresholds for exiting portions of the position. Lower levels (e.g., 2%) capture smaller profits quickly, while higher levels (e.g., 18%) allow positions to run longer for more significant gains.

6. Take Profit Percentages (30%, 20%, 15%): These percentages determine how much of the position is exited at each take profit level. A higher percentage at the first level locks in more profit early, reducing exposure to market reversals. Lower percentages at higher levels allow for a portion of the position to benefit from extended trends.

USD Liquidity Conditions Index Swing Stock Strategy Original credits goes to @ElDoggo22 www.tradingview.com

I looked in the post created by him, of USD liquidity and I have noticed that if you are going to apply a percentile top and bottom to it, can become an interesting swing strategy for US Stocks.

So in this case I decided to create a 99th percentile for top and 4th percentile for bot with a big length, preferably 100+ candles, for this example i took 150.

Rules for entry :

Long : either bot or top lines are ascending

We exit long either the top line is descending, or we have sudden cross of the moving average with both top and bot within the same candle

Short: we enter short when we have a sudden cross down of the moving average with both top and bot within the same candle

We exit short when we have a cross over of the moving average with both top and bot within the same candle ( or we have a long entry condition)

If there are qny questions, please let me know !