CandleCandle: A Comprehensive Pine Script™ Library for Candlestick Analysis

Overview

The Candle library, developed in Pine Script™, provides traders and developers with a robust toolkit for analyzing candlestick data. By offering easy access to fundamental candlestick components like open, high, low, and close prices, along with advanced derived metrics such as body-to-wick ratios, percentage calculations, and volatility analysis, this library enables detailed insights into market behavior.

This library is ideal for creating custom indicators, trading strategies, and backtesting frameworks, making it a powerful resource for any Pine Script™ developer.

Key Features

1. Core Candlestick Data

• Open : Access the opening price of the current candle.

• High : Retrieve the highest price.

• Low : Retrieve the lowest price.

• Close : Access the closing price.

2. Candle Metrics

• Full Size : Calculates the total range of the candle (high - low).

• Body Size : Computes the size of the candle’s body (open - close).

• Wick Size : Provides the combined size of the upper and lower wicks.

3. Wick and Body Ratios

• Upper Wick Size and Lower Wick Size .

• Body-to-Wick Ratio and Wick-to-Body Ratio .

4. Percentage Calculations

• Upper Wick Percentage : The proportion of the upper wick size relative to the full candle size.

• Lower Wick Percentage : The proportion of the lower wick size relative to the full candle size.

• Body Percentage and Wick Percentage relative to the candle’s range.

5. Candle Direction Analysis

• Determines if a candle is "Bullish" or "Bearish" based on its closing and opening prices.

6. Price Metrics

• Average Price : The mean of the open, high, low, and close prices.

• Midpoint Price : The midpoint between the high and low prices.

7. Volatility Measurement

• Calculates the standard deviation of the OHLC prices, providing a volatility metric for the current candle.

Code Architecture

Example Functionality

The library employs a modular structure, exporting various functions that can be used independently or in combination. For instance:

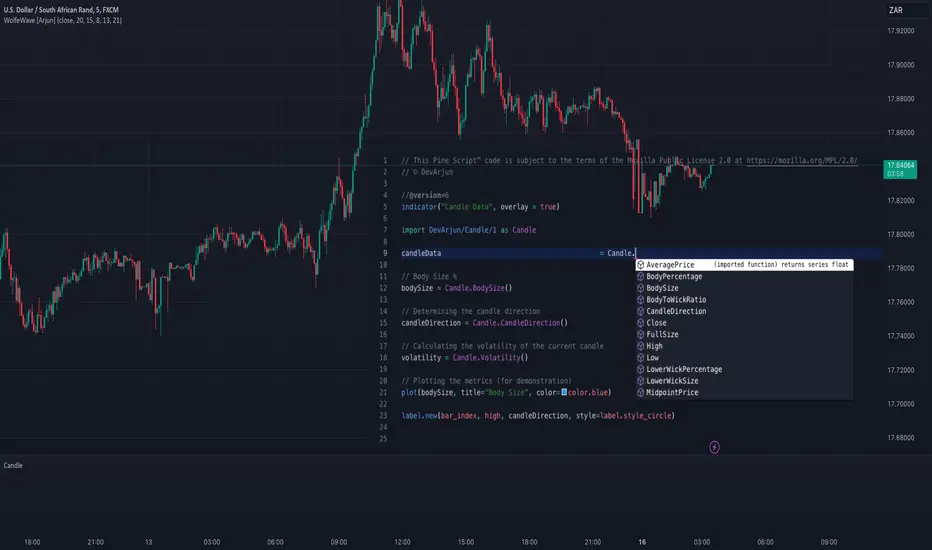

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © DevArjun

//@version=6

indicator("Candle Data", overlay = true)

import DevArjun/Candle/1 as Candle

// Body Size %

bodySize = Candle.BodySize()

// Determining the candle direction

candleDirection = Candle.CandleDirection()

// Calculating the volatility of the current candle

volatility = Candle.Volatility()

// Plotting the metrics (for demonstration)

plot(bodySize, title="Body Size", color=color.blue)

label.new(bar_index, high, candleDirection, style=label.style_circle)

Scalability

The modularity of the Candle library allows seamless integration into more extensive trading systems. Functions can be mixed and matched to suit specific analytical or strategic needs.

Use Cases

Trading Strategies

Developers can use the library to create strategies based on candle properties such as:

• Identifying long-bodied candles (momentum signals).

• Detecting wicks as potential reversal zones.

• Filtering trades based on candle ratios.

Visualization

Plotting components like body size, wick size, and directional labels helps visualize market behavior and identify patterns.

Backtesting

By incorporating volatility and ratio metrics, traders can design and test strategies on historical data, ensuring robust performance before live trading.

Education

This library is a great tool for teaching candlestick analysis and how each component contributes to market behavior.

Portfolio Highlights

Project Objective

To create a Pine Script™ library that simplifies candlestick analysis by providing comprehensive metrics and insights, empowering traders and developers with advanced tools for market analysis.

Development Challenges and Solutions

• Challenge : Achieving high precision in calculating ratios and percentages.

• Solution : Implemented robust mathematical operations and safeguarded against division-by-zero errors.

• Challenge : Ensuring modularity and scalability.

• Solution : Designed functions as independent modules, allowing flexible integration.

Impact

• Efficiency : The library reduces the time required to calculate complex candlestick metrics.

• Versatility : Supports various trading styles, from scalping to swing trading.

• Clarity : Clean code and detailed documentation ensure usability for developers of all levels.

Conclusion

The Candle library exemplifies the power of Pine Script™ in simplifying and enhancing candlestick analysis. By including this project in your portfolio, you showcase your expertise in:

• Financial data analysis.

• Pine Script™ development.

• Creating tools that solve real-world trading challenges.

This project demonstrates both technical proficiency and a keen understanding of market analysis, making it an excellent addition to your professional portfolio.

Library "Candle"

A comprehensive library to access and analyze the basic components of a candlestick, including open, high, low, close prices, and various derived metrics such as full size, body size, wick sizes, ratios, percentages, and additional analysis metrics.

Open()

Open

@description Returns the opening price of the current candle.

Returns: float - The opening price of the current candle.

High()

High

@description Returns the highest price of the current candle.

Returns: float - The highest price of the current candle.

Low()

Low

@description Returns the lowest price of the current candle.

Returns: float - The lowest price of the current candle.

Close()

Close

@description Returns the closing price of the current candle.

Returns: float - The closing price of the current candle.

FullSize()

FullSize

@description Returns the full size (range) of the current candle (high - low).

Returns: float - The full size of the current candle.

BodySize()

BodySize

@description Returns the body size of the current candle (open - close).

Returns: float - The body size of the current candle.

WickSize()

WickSize

@description Returns the size of the wicks of the current candle (full size - body size).

Returns: float - The size of the wicks of the current candle.

UpperWickSize()

UpperWickSize

@description Returns the size of the upper wick of the current candle.

Returns: float - The size of the upper wick of the current candle.

LowerWickSize()

LowerWickSize

@description Returns the size of the lower wick of the current candle.

Returns: float - The size of the lower wick of the current candle.

BodyToWickRatio()

BodyToWickRatio

@description Returns the ratio of the body size to the wick size of the current candle.

Returns: float - The body to wick ratio of the current candle.

UpperWickPercentage()

UpperWickPercentage

@description Returns the percentage of the upper wick size relative to the full size of the current candle.

Returns: float - The percentage of the upper wick size relative to the full size of the current candle.

LowerWickPercentage()

LowerWickPercentage

@description Returns the percentage of the lower wick size relative to the full size of the current candle.

Returns: float - The percentage of the lower wick size relative to the full size of the current candle.

WickToBodyRatio()

WickToBodyRatio

@description Returns the ratio of the wick size to the body size of the current candle.

Returns: float - The wick to body ratio of the current candle.

BodyPercentage()

BodyPercentage

@description Returns the percentage of the body size relative to the full size of the current candle.

Returns: float - The percentage of the body size relative to the full size of the current candle.

WickPercentage()

WickPercentage

@description Returns the percentage of the wick size relative to the full size of the current candle.

Returns: float - The percentage of the wick size relative to the full size of the current candle.

CandleDirection()

CandleDirection

@description Returns the direction of the current candle.

Returns: string - "Bullish" if the candle is bullish, "Bearish" if the candle is bearish.

AveragePrice()

AveragePrice

@description Returns the average price of the current candle (mean of open, high, low, and close).

Returns: float - The average price of the current candle.

MidpointPrice()

MidpointPrice

@description Returns the midpoint price of the current candle (mean of high and low).

Returns: float - The midpoint price of the current candle.

Volatility()

Volatility

@description Returns the standard deviation of the OHLC prices of the current candle.

Returns: float - The volatility of the current candle.

Indicateurs et stratégies

ToolsFluentLibrary "ToolsFluent"

Fluent data holder object with retrieval and modification functions

set(fluent, key, value)

Returns Fluent object after setting related fluent value

Parameters:

fluent (Fluent) : Fluent Fluent object

key (string) : string|int Key to be set

value (int) : int|float|bool|string|color Value to be set

Returns: Fluent

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (string)

value (float)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (string)

value (bool)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (string)

value (string)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (string)

value (color)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (int)

value (int)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (int)

value (float)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (int)

value (bool)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (int)

value (string)

set(fluent, key, value)

Parameters:

fluent (Fluent)

key (int)

value (color)

get(fluent, key, default)

Returns Fluent object key's value or default value when key not found

Parameters:

fluent (Fluent) : Fluent object

key (string)

default (int) : int|float|bool|string|color Value to be returned when key not exists

Returns: int|float|bool|string|color

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (string)

default (float)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (string)

default (bool)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (string)

default (string)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (string)

default (color)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (int)

default (int)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (int)

default (float)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (int)

default (bool)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (int)

default (string)

get(fluent, key, default)

Parameters:

fluent (Fluent)

key (int)

default (color)

Fluent

Fluent - General purpose data holder object

Fields:

msi (map) : map String key, integer value info holder map. Default: na

msf (map) : map String key, float value info holder map. Default: na

msb (map) : map String key, boolean value info holder map. Default: na

mss (map) : map String key, string value info holder map. Default: na

msc (map) : map String key, color value info holder map. Default: na

mii (map) : map Integer key, integer value info holder map. Default: na

mif (map) : map Integer key, float value info holder map. Default: na

mib (map) : map Integer key, boolean value info holder map. Default: na

mis (map) : map Integer key, string value info holder map. Default: na

mic (map) : map Integer key, color value info holder map. Default: na

ToolsPosLibrary "ToolsPos"

Library for general purpose position helpers

new_pos(state, price, when, index)

Returns new PosInfo object

Parameters:

state (series PosState) : Position state

price (float) : float Entry price

when (int) : int Entry bar time UNIX. Default: time

index (int) : int Entry bar index. Default: bar_index

Returns: PosInfo

new_tp(pos, price, when, index, info)

Returns PosInfo object with new take profit info object

Parameters:

pos (PosInfo) : PosInfo object

price (float) : float Entry price

when (int) : int Entry bar time UNIX. Default: time

index (int) : int Entry bar index. Default: bar_index

info (Info type from aybarsm/Tools/14) : Info holder object. Default: na

Returns: PosInfo

new_re(pos, price, when, index, info)

Returns PosInfo object with new re-entry info object

Parameters:

pos (PosInfo) : PosInfo object

price (float) : float Entry price

when (int) : int Entry bar time UNIX. Default: time

index (int) : int Entry bar index. Default: bar_index

info (Info type from aybarsm/Tools/14) : Info holder object. Default: na

Returns: PosInfo

PosTPInfo

PosTPInfo - Position Take Profit info object

Fields:

price (series float) : float Take profit price

when (series int) : int Take profit bar time UNIX. Default: time

index (series int) : int Take profit bar index. Default: bar_index

info (Info type from aybarsm/Tools/14) : Info holder object

PosREInfo

PosREInfo - Position Re-Entry info object

Fields:

price (series float) : float Re-entry price

when (series int) : int Re-entry bar time UNIX. Default: time

index (series int) : int Take profit bar index. Default: bar_index

info (Info type from aybarsm/Tools/14) : Info holder object

PosInfo

PosInfo - Position info object

Fields:

state (series PosState) : Position state

price (series float) : float Entry price

when (series int) : int Entry bar time UNIX. Default: time

index (series int) : int Entry bar index. Default: bar_index

tp (array) : PosTPInfo Take profit info. Default: na

re (array) : PosREInfo Re-entry info. Default: na

info (Info type from aybarsm/Tools/14) : Info holder object

ToolsCollectionLibrary "ToolsCollection"

Helper functions for collection (map/array) type operations

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (string) : Key to be checked

default (bool) : Default return value when key not found. Default: false

Returns: bool

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (string) : Key to be checked

default (int) : Default return value when key not found. Default: -1

Returns: int

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (string) : Key to be checked

default (float) : Default return value when key not found. Default: -1

Returns: float

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (string) : Key to be checked

default (string) : Default return value when key not found. Default: ''

Returns: string

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (string) : Key to be checked

default (color) : Default return value when key not found. Default: color.white

Returns: color

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (int) : Key to be checked

default (bool) : Default return value when key not found. Default: false

Returns: bool

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (int) : Key to be checked

default (int) : Default return value when key not found. Default: -1

Returns: int

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (int) : Key to be checked

default (float) : Default return value when key not found. Default: -1

Returns: float

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (int) : Key to be checked

default (string) : Default return value when key not found. Default: ''

Returns: string

get(container, key, default)

Returns Map key's value with default return value option

Parameters:

container (map) : Map object

key (int) : Key to be checked

default (color) : Default return value when key not found. Default: color.white

Returns: color

get(container, key, default)

Returns Array key's value with default return value option

Parameters:

container (array) : Array object

key (int) : Key to be checked

default (bool) : Default return value when key not found. Default: false

Returns: bool

get(container, key, default)

Returns Array key's value with default return value option

Parameters:

container (array) : Array object

key (int) : Key to be checked

default (int) : Default return value when key not found. Default: -1

Returns: bool

get(container, key, default)

Returns Array key's value with default return value option

Parameters:

container (array) : Array object

key (int) : Key to be checked

default (float) : Default return value when key not found. Default: -1

Returns: bool

get(container, key, default)

Returns Array key's value with default return value option

Parameters:

container (array) : Array object

key (int) : Key to be checked

default (string) : Default return value when key not found. Default: ''

Returns: bool

get(container, key, default)

Returns Array key's value with default return value option

Parameters:

container (array) : Array object

key (int) : Key to be checked

default (color) : Default return value when key not found. Default: color.white

Returns: bool

DynamicPeriodPublicDynamic Period Calculation Library

This library provides tools for adaptive period determination, useful for creating indicators or strategies that automatically adjust to market conditions.

Overview

The Dynamic Period Library calculates adaptive periods based on pivot points, enabling the creation of responsive indicators and strategies that adjust to market volatility.

Key Features

Dynamic Periods: Computes periods using distances between pivot highs and lows.

Customizable Parameters: Users can adjust detection settings and period constraints.

Robust Handling: Includes fallback mechanisms for cases with insufficient pivot data.

Use Cases

Adaptive Indicators: Build tools that respond to market volatility by adjusting their periods dynamically.

Dynamic Strategies: Enhance trading strategies by integrating pivot-based period adjustments.

Function: `dynamic_period`

Description

Calculates a dynamic period based on the average distances between pivot highs and lows.

Parameters

`left` (default: 5): Number of left-hand bars for pivot detection.

`right` (default: 5): Number of right-hand bars for pivot detection.

`numPivots` (default: 5): Minimum pivots required for calculation.

`minPeriod` (default: 2): Minimum allowed period.

`maxPeriod` (default: 50): Maximum allowed period.

`defaultPeriod` (default: 14): Fallback period if no pivots are found.

Returns

A dynamic period calculated based on pivot distances, constrained by `minPeriod` and `maxPeriod`.

Example

//@version=6

import CrimsonVault/DynamicPeriodPublic/1

left = input.int(5, "Left bars", minval = 1)

right = input.int(5, "Right bars", minval = 1)

numPivots = input.int(5, "Number of Pivots", minval = 2)

period = DynamicPeriodPublic.dynamic_period(left, right, numPivots)

plot(period, title = "Dynamic Period", color = color.blue)

Implementation Notes

Pivot Detection: Requires sufficient historical data to identify pivots accurately.

Edge Cases: Ensures a default period is applied when pivots are insufficient.

Constraints: Limits period values to a user-defined range for stability.

IndicatorsLibrary "Indicators"

cmf(lookback, n_to_smooth)

Calculates the Chaikin's Money Flow.

Parameters:

lookback (simple int)

n_to_smooth (simple int)

Returns: float The Money Flow value.

cmma(lookback, atr_length)

Calculates the CMMA (Close Minus Moving Average) indicator.

Parameters:

lookback (simple int)

atr_length (simple int)

Returns: float The CMMA value.

macd(fast_length, slow_length, n_to_smooth)

Calculates the normalized and scaled MACD.

Parameters:

fast_length (simple int)

slow_length (simple int)

n_to_smooth (simple int)

Returns: A tuple containing .

stochK(length, n_to_smooth)

Calculates a simplified Stochastic Oscillator.

Uses: 100 * ta.sma((close - lowest_low) / (highest_high - lowest_low), n_to_smooth)

Parameters:

length (simple int)

n_to_smooth (simple int)

Returns: float The Stochastic %K value.

williamsR(length)

Calculates the Williams %R using the stochK function.

Uses: -1 * (100 - stoch(length, 1))

Parameters:

length (simple int)

Returns: float The Williams %R value.

Alerts█ OVERVIEW

This library is a Pine Script™ programmers tool that provides functions to simplify the creation of compound conditions and alert messages. With these functions, scripts can use comma-separated "string" lists to specify condition groups from arbitrarily large "bool" arrays , offering a convenient way to provide highly flexible alert creation to script users without requiring numerous inputs in the "Settings/Inputs" menu.

█ CONCEPTS

Compound conditions

Compound conditions are essentially groups of two or more conditions, where each required condition must occur to produce a `true` result. Traders often combine conditions, including signals from various indicators, to drive and reinforce trade decisions. Similarly, programmers use compound conditions in logical operations to create scripts that respond dynamically to groups of events.

Condition conundrum

Providing flexible condition combinations to script users for signals and alerts often poses a significant challenge: input complexity . Conventionally, such flexibility comes at the cost of an extensive list of separate inputs for toggling individual conditions and customizing their properties, often resulting in complicated input menus that are difficult for users to navigate effectively. Furthermore, managing all those inputs usually entails tediously handling many extra variables and logical expressions, making such projects more complex for programmers.

Condensing complexity

This library introduces a technique using parsed strings to reference groups of elements from "bool" arrays , helping to simplify and streamline the construction of compound conditions and alert messages. With this approach, programmers can provide one or more "string" inputs in their scripts where users can list numbers corresponding to the conditions they want to combine.

For example, suppose you have a script that creates alert triggers based on a combination of up to 20 individual conditions, and you want to make inputs for users to choose which conditions to combine. Instead of creating 20 separate checkboxes in the "Settings/Inputs" tab and manually adding associated logic for each one, you can store the conditional values in arrays, make one or more "string" inputs that accept values listing the array item locations (e.g., "1,4,8,11"), and then pass the inputs to these functions to determine the compound conditions formed by the specified groups.

This approach condenses the input space, improving navigability and utility. Additionally, it helps provide high-level simplicity to complex conditional code, making it easier to maintain and expand over time.

█ CALCULATIONS AND USE

This library contains three functions for evaluating compound conditions: `getCompoundConditon()`, `getCompoundConditionsArray()`, and `compoundAlertMessage()`. Each function has two overloads that evaluate compound conditions based on groups of items from one or two "bool" arrays . The sections below explain the functions' calculations and how to use them.

Referencing conditions using "string" index lists

Each function processes "string" values containing comma-separated lists of numerals representing the indices of the "bool" array items to use in its calculations (e.g., "4, 8, 12"). The functions split each supplied "string" list by its commas, then iterate over those specified indices in the "bool" arrays to determine each group's combined `true` or `false` state.

For convenience, the numbers in the "string" lists can represent zero-based indices (where the first item is at index 0) or one-based indices (where the first item is at index 1), depending on the function's `zeroIndex` parameter. For example, an index list of "0, 2, 4" with a `zeroIndex` value of `true` specifies that the condition group uses the first , third , and fifth "bool" values in the array, ignoring all others. If the `zeroIndex` value is `false`, the list "1, 3, 5" also refers to those same elements.

Zero-based indexing is convenient for programmers because Pine arrays always use this index format. However, one-based indexing is often more convenient and familiar for script users, especially non-programmers.

Evaluating one or many condition groups

The `getCompoundCondition()` function evaluates singular condition groups determined by its `indexList` parameter, returning `true` values whenever the specified array elements are `true`. This function is helpful when a script has to evaluate specific groups of conditions and does not require many combinations.

In contrast, the `getCompoundConditionsArray()` function can evaluate numerous condition groups, one for each "string" included in its `indexLists` argument. It returns arrays containing `true` or `false` states for each listed group. This function is helpful when a script requires multiple condition combinations in additional calculations or logic.

The `compoundAlertMessage()` function is similar to the `getCompoundConditionsArray()` function. It also evaluates a separate compound condition group for each "string" in its `indexLists` array, but it returns "string" values containing the marker (name) of each group with a `true` result. You can use these returned values as the `message` argument in alert() calls, display them in labels and other drawing objects, or even use them in additional calculations and logic.

Directional condition pairs

The first overload of each function operates on a single `conditions` array, returning values representing one or more compound conditions from groups in that array. These functions are ideal for general-purpose condition groups that may or may not represent direction information.

The second overloads accept two arrays representing upward and downward conditions separately: `upConditions` and `downConditions`. These overloads evaluate opposing directional conditions in pairs (e.g., RSI is above/below a level) and return upward and downward condition information separately in a tuple .

When using the directional overloads, ensure the `upConditions` and `downConditions` arrays are the same size, with the intended condition pairs at the same indices . For instance, if you have a specific upward RSI condition's value at the first index in the `upConditions` array, include the opposing downward RSI condition's value at that same index in the `downConditions` array. If a condition can apply to both directions (e.g., rising volume), include its value at the same index in both arrays.

Group markers

To simplify the generation of informative alert messages, the `compoundAlertMessage()` function assigns "string" markers to each condition group, where "marker" refers to the group's name. The `groupMarkers` parameter allows you to assign custom markers to each listed group. If not specified, the function generates default group markers in the format "M", where "M" is short for "Marker" and "" represents the group number starting from 1. For example, the default marker for the first group specified in the `indexLists` array is "M1".

The function's returned "string" values contain a comma-separated list with markers for each activated condition group (e.g., "M1, M4"). The function's second overload, which processes directional pairs of conditions, also appends extra characters to the markers to signify the direction. The default for upward groups is "▲" (e.g., "M1▲") and the default for downward ones is "▼" (e.g., "M1▼"). You can customize these appended characters with the `upChar` and `downChar` parameters.

Designing customizable alerts

We recommend following these primary steps when using this library to design flexible alerts for script users:

1. Create text inputs for users to specify comma-separated lists of conditions with the input.string() or input.text_area() functions, and then collect all the input values in a "string" array . Note that each separate "string" in the array will represent a distinct condition group.

2. Create arrays of "bool" values representing the possible conditions to choose from. If your script will process pairs of upward and downward conditions, ensure the related elements in the arrays align at the same indices.

3. Call `compoundAlertMessage()` using the arrays from steps 1 and 2 as arguments to get the alert message text. If your script will use the text for alerts only, not historical display or calculation purposes, the call is necessary only on realtime bars .

4. Pass the calculated "string" values as the `message` argument in alert() calls. We recommend calling the function only when the "string" is not empty (i.e., `messageText != ""`). To avoid repainting alerts on open bars, use barstate.isconfirmed in the condition to allow alert triggers only on each bar's close .

5. Test the alerts. Open the "Create Alert" dialog box and select "Any alert() function call" in the "Condition" field. It is also helpful to inspect the strings with Pine Logs .

NOTE: Because the techniques in this library use lists of numbers to specify conditions, we recommend including a tooltip for the "string" inputs that lists the available numbers and the conditions they represent. This tooltip provides a legend for script users, making it simple to understand and utilize. To create the tooltip, declare a "const string" listing the options and pass it to the `input.*()` call's `tooltip` parameter. See the library's example code for a simple demonstration.

█ EXAMPLE CODE

This library's example code demonstrates one possible way to offer a selection of compound conditions with "string" inputs and these functions. It uses three input.string() calls, each accepting a comma-separated list representing a distinct condition group. The title of each input represents the default group marker that appears in the label and alert text. The code collects these three input values in a `conditionGroups` array for use with the `compoundAlertMessage()` function.

In this code, we created two "bool" arrays to store six arbitrary condition pairs for demonstration:

1. Bar up/down: The bar's close price must be above the open price for upward conditions, and vice versa for downward conditions.

2. Fast EMA above/below slow EMA : The 9-period Exponential Moving Average of close prices must be above the 21-period EMA for upward conditions, and vice versa for downward conditions.

3. Volume above average : The bar's volume must exceed its 20-bar average to activate an upward or downward condition.

4. Volume rising : The volume must exceed that of the previous bar to activate an upward or downward condition.

5. RSI trending up/down : The 14-period Relative Strength Index of close prices must be between 50 and 70 for upward conditions, and between 30 and 50 for downward conditions.

6. High volatility : The 7-period Average True Range (ATR) must be above the 40-period ATR to activate an upward or downward condition.

We included a `tooltip` argument for the third input.string() call that displays the condition numbers and titles, where 1 is the first condition number.

The `bullConditions` array contains the `true` or `false` states of all individual upward conditions, and the `bearConditions` array contains all downward condition states. For the conditions that filter either direction because they are non-directional, such as "High volatility", both arrays contain the condition's `true` or `false` value at the same index. If you use these conditions alone, they activate upward and downward alert conditions simultaneously.

The example code calls `compoundAlertMessage()` using the `bullConditions`, `bearConditions`, and `conditionGroups` arrays to create a tuple of strings containing the directional markers for each activated group. On confirmed bars, it displays non-empty strings in labels and uses them in alert() calls. For the text shown in the labels, we used str.replace_all() to replace commas with newline characters, aligning the markers vertically in the display.

Look first. Then leap.

█ FUNCTIONS

This library exports the following functions:

getCompoundCondition(conditions, indexList, minRequired, zeroIndex)

(Overload 1 of 2) Determines a compound condition based on selected elements from a `conditions` array.

Parameters:

conditions (array) : (array) An array containing the possible "bool" values to use in the compound condition.

indexList (string) : (series string) A "string" containing a comma-separated list of whole numbers representing the group of `conditions` elements to use in the compound condition. For example, if the value is `"0, 2, 4"`, and `minRequired` is `na`, the function returns `true` only if the `conditions` elements at index 0, 2, and 4 are all `true`. If the value is an empty "string", the function returns `false`.

minRequired (int) : (series int) Optional. Determines the minimum number of selected conditions required to activate the compound condition. For example, if the value is 2, the function returns `true` if at least two of the specified `conditions` elements are `true`. If the value is `na`, the function returns `true` only if all specified elements are `true`. The default is `na`.

zeroIndex (bool) : (series bool) Optional. Specifies whether the `indexList` represents zero-based array indices. If `true`, a value of "0" in the list represents the first array index. If `false`, a `value` of "1" represents the first index. The default is `true`.

Returns: (bool) `true` if `conditions` elements in the group specified by the `indexList` are `true`, `false` otherwise.

getCompoundCondition(upConditions, downConditions, indexList, minRequired, allowUp, allowDown, zeroIndex)

(Overload 2 of 2) Determines upward and downward compound conditions based on selected elements from `upConditions` and `downConditions` arrays.

Parameters:

upConditions (array) : (array) An array containing the possible "bool" values to use in the upward compound condition.

downConditions (array) : (array) An array containing the possible "bool" values to use in the downward compound condition.

indexList (string) : (series string) A "string" containing a comma-separated list of whole numbers representing the `upConditions` and `downConditions` elements to use in the compound conditions. For example, if the value is `"0, 2, 4"` and `minRequired` is `na`, the function returns `true` for the first value only if the `upConditions` elements at index 0, 2, and 4 are all `true`. If the value is an empty "string", the function returns ` `.

minRequired (int) : (series int) Optional. Determines the minimum number of selected conditions required to activate either compound condition. For example, if the value is 2, the function returns `true` for its first value if at least two of the specified `upConditions` elements are `true`. If the value is `na`, the function returns `true` only if all specified elements are `true`. The default is `na`.

allowUp (bool) : (series bool) Optional. Controls whether the function considers upward compound conditions. If `false`, the function ignores the `upConditions` array, and the first item in the returned tuple is `false`. The default is `true`.

allowDown (bool) : (series bool) Optional. Controls whether the function considers downward compound conditions. If `false`, the function ignores the `downConditions` array, and the second item in the returned tuple is `false`. The default is `true`.

zeroIndex (bool) : (series bool) Optional. Specifies whether the `indexList` represents zero-based array indices. If `true`, a value of "0" in the list represents the first array index. If `false`, a value of "1" represents the first index. The default is `true`.

Returns: ( ) A tuple containing two "bool" values representing the upward and downward compound condition states, respectively.

getCompoundConditionsArray(conditions, indexLists, zeroIndex)

(Overload 1 of 2) Creates an array of "bool" values representing compound conditions formed by selected elements from a `conditions` array.

Parameters:

conditions (array) : (array) An array containing the possible "bool" values to use in each compound condition.

indexLists (array) : (array) An array of strings containing comma-separated lists of whole numbers representing the `conditions` elements to use in each compound condition. For example, if an item is `"0, 2, 4"`, the corresponding item in the returned array is `true` only if the `conditions` elements at index 0, 2, and 4 are all `true`. If an item is an empty "string", the item in the returned array is `false`.

zeroIndex (bool) : (series bool) Optional. Specifies whether the "string" lists in the `indexLists` represent zero-based array indices. If `true`, a value of "0" in a list represents the first array index. If `false`, a value of "1" represents the first index. The default is `true`.

Returns: (array) An array of "bool" values representing compound condition states for each condition group. An item in the array is `true` only if all the `conditions` elements specified by the corresponding `indexLists` item are `true`. Otherwise, the item is `false`.

getCompoundConditionsArray(upConditions, downConditions, indexLists, allowUp, allowDown, zeroIndex)

(Overload 2 of 2) Creates two arrays of "bool" values representing compound upward and

downward conditions formed by selected elements from `upConditions` and `downConditions` arrays.

Parameters:

upConditions (array) : (array) An array containing the possible "bool" values to use in each upward compound condition.

downConditions (array) : (array) An array containing the possible "bool" values to use in each downward compound condition.

indexLists (array) : (array) An array of strings containing comma-separated lists of whole numbers representing the `upConditions` and `downConditions` elements to use in each compound condition. For example, if an item is `"0, 2, 4"`, the corresponding item in the first returned array is `true` only if the `upConditions` elements at index 0, 2, and 4 are all `true`. If an item is an empty "string", the items in both returned arrays are `false`.

allowUp (bool) : (series bool) Optional. Controls whether the function considers upward compound conditions. If `false`, the function ignores the `upConditions` array, and all elements in the first returned array are `false`. The default is `true`.

allowDown (bool) : (series bool) Optional. Controls whether the function considers downward compound conditions. If `false`, the function ignores the `downConditions` array, and all elements in the second returned array are `false`. The default is `true`.

zeroIndex (bool) : (series bool) Optional. Specifies whether the "string" lists in the `indexLists` represent zero-based array indices. If `true`, a value of "0" in a list represents the first array index. If `false`, a value of "1" represents the first index. The default is `true`.

Returns: ( ) A tuple containing two "bool" arrays:

- The first array contains values representing upward compound condition states determined using the `upConditions`.

- The second array contains values representing downward compound condition states determined using the `downConditions`.

compoundAlertMessage(conditions, indexLists, zeroIndex, groupMarkers)

(Overload 1 of 2) Creates a "string" message containing a comma-separated list of markers representing active compound conditions formed by specified element groups from a `conditions` array.

Parameters:

conditions (array) : (array) An array containing the possible "bool" values to use in each compound condition.

indexLists (array) : (array) An array of strings containing comma-separated lists of whole numbers representing the `conditions` elements to use in each compound condition. For example, if an item is `"0, 2, 4"`, the corresponding marker for that item appears in the returned "string" only if the `conditions` elements at index 0, 2, and 4 are all `true`.

zeroIndex (bool) : (series bool) Optional. Specifies whether the "string" lists in the `indexLists` represent zero-based array indices. If `true`, a value of "0" in a list represents the first array index. If `false`, a value of "1" represents the first index. The default is `true`.

groupMarkers (array) : (array) Optional. If specified, sets the marker (name) for each condition group specified in the `indexLists` array. If `na`, the function uses the format `"M"` for each group, where "M" is short for "Marker" and `` represents the one-based index for the group (e.g., the marker for the first listed group is "M1"). The default is `na`.

Returns: (string) A "string" containing a list of markers corresponding to each active compound condition.

compoundAlertMessage(upConditions, downConditions, indexLists, allowUp, allowDown, zeroIndex, groupMarkers, upChar, downChar)

(Overload 2 of 2) Creates two "string" messages containing comma-separated lists of markers representing active upward and downward compound conditions formed by specified element groups from `upConditions` and `downConditions` arrays.

Parameters:

upConditions (array) An array containing the possible "bool" values to use in each upward compound condition.

downConditions (array) An array containing the possible "bool" values to use in each downward compound condition.

indexLists (array) An array of strings containing comma-separated lists of whole numbers representing the `upConditions` and `downConditions` element groups to use in each compound condition. For example, if an item is `"0, 2, 4"`, the corresponding group marker for that item appears in the first returned "string" only if the `upConditions` elements at index 0, 2, and 4 are all `true`.

allowUp (bool) Optional. Controls whether the function considers upward compound conditions. If `false`, the function ignores the `upConditions` array and returns an empty "string" for the first tuple element. The default is `true`.

allowDown (bool) Optional. Controls whether the function considers downward compound conditions. If `false`, the function ignores the `downConditions` array and returns an empty "string" for the second tuple element. The default is `true`.

zeroIndex (bool) Optional. Specifies whether the "string" lists in the `indexLists` represent zero-based array indices. If `true`, a value of "0" in a list represents the first array index. If `false`, a value of "1" represents the first index. The default is `true`.

groupMarkers (array) Optional. If specified, sets the name (marker) of each condition group specified in the `indexLists` array. If `na`, the function uses the format `"M"` for each group, where "M" is short for "Marker" and `` represents the one-based index for the group (e.g., the marker for the first listed group is "M1"). The default is `na`.

upChar (string) Optional. A "string" appended to all group markers for upward conditions to signify direction. The default is "▲".

downChar (string) Optional. A "string" appended to all group markers for downward conditions to signify direction. The default is "▼".

Returns: ( ): A tuple of "string" values containing lists of markers corresponding to active upward and downward compound conditions, respectively.

supertrendLibrary "supertrend"

supertrend : Library dedicated to different variations of supertrend

supertrend_atr(length, multiplier, atrMaType, source, highSource, lowSource, waitForClose, delayed)

supertrend_atr: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

length (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

delayed (simple bool) : : if set to true lags supertrend atr stop based on target levels.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_bands(bandType, maType, length, multiplier, source, highSource, lowSource, waitForClose, useTrueRange, useAlternateSource, alternateSource, sticky)

supertrend_bands: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

bandType (simple string) : : Type of band used - can be bb, kc or dc

maType (simple string) : : Moving Average type for Bands. This can be sma, ema, hma, rma, wma, vwma, swma

length (simple int) : : Band Length

multiplier (float) : : Std deviation or ATR multiplier for Bollinger Bands and Keltner Channel

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

useTrueRange (simple bool) : : Used for Keltner channel. If set to false, then high-low is used as range instead of true range

useAlternateSource (simple bool) : - Custom source is used for Donchian Chanbel only if useAlternateSource is set to true

alternateSource (float) : - Custom source for Donchian channel

sticky (simple bool) : : if set to true borders change only when price is beyond borders.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_zigzag(length, history, useAlternativeSource, alternativeSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType)

supertrend_zigzag: Zigzag pivot based supertrend

Parameters:

length (simple int) : : Zigzag Length

history (simple int) : : number of historical pivots to consider

useAlternativeSource (simple bool)

alternativeSource (float)

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

zupertrend(length, history, useAlternativeSource, alternativeSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType)

zupertrend: Zigzag pivot based supertrend

Parameters:

length (simple int) : : Zigzag Length

history (simple int) : : number of historical pivots to consider

useAlternativeSource (simple bool)

alternativeSource (float)

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

zsupertrend(zigzagpivots, history, source, highSource, lowSource, waitForClose, atrMaType, atrlength, multiplier)

zsupertrend: Same as zigzag supertrend. But, works on already calculated array rather than Calculating fresh zigzag

Parameters:

zigzagpivots (array) : : Precalculated zigzag pivots

history (simple int) : : number of historical pivots to consider

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

taLibrary "ta"

Collection of all custom and enhanced TA indicators

ma(source, maType, length)

returns custom moving averages

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: moving average for the given type and length

atr(maType, length)

returns ATR with custom moving average

Parameters:

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: ATR for the given moving average type and length

atrpercent(maType, length)

returns ATR as percentage of close price

Parameters:

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: ATR as percentage of close price for the given moving average type and length

bb(source, maType, length, multiplier, sticky)

returns Bollinger band for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger band with custom moving average for given source, length and multiplier

bbw(source, maType, length, multiplier, sticky)

returns Bollinger bandwidth for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger Bandwidth for custom moving average for given source, length and multiplier

bpercentb(source, maType, length, multiplier, sticky)

returns Bollinger Percent B for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger Percent B for custom moving average for given source, length and multiplier

kc(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Channel for custom moving average for given souce, length and multiplier

kcw(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel Width with custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Channel Width for custom moving average

kpercentk(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel Percent K Width with custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Percent K for given moving average, source, length and multiplier

dc(length, useAlternateSource, alternateSource, sticky)

returns Custom Donchian Channel

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel

dcw(length, useAlternateSource, alternateSource, sticky)

returns Donchian Channel Width

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel width

dpercentd(length, useAlternateSource, alternateSource, sticky)

returns Donchian Channel Percent of price

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel Percent D

oscillatorRange(source, method, highlowLength, rangeLength, sticky)

oscillatorRange - returns Custom overbought/oversold areas for an oscillator input

Parameters:

source (float) : - Osillator source such as RSI, COG etc.

method (simple string) : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

rangeLength (simple int) : - length used for calculating oversold/overbought range - usually same as oscillator length

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

Returns: Dynamic overbought and oversold range for oscillator input

oscillator(type, length, shortLength, longLength, source, highSource, lowSource, method, highlowLength, sticky)

oscillator - returns Choice of oscillator with custom overbought/oversold range

Parameters:

type (simple string) : - oscillator type. Valid values : cci, cmo, cog, mfi, roc, rsi, stoch, tsi, wpr

length (simple int) : - Oscillator length - not used for TSI

shortLength (simple int) : - shortLength only used for TSI

longLength (simple int) : - longLength only used for TSI

source (float) : - custom source if required

highSource (float) : - custom high source for stochastic oscillator

lowSource (float) : - custom low source for stochastic oscillator

method (simple string) : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

Returns: Oscillator value along with dynamic overbought and oversold range for oscillator input

lib_kernelLibrary "lib_kernel"

Library "lib_kernel"

This is a tool / library for developers, that contains several common and adapted kernel functions as well as a kernel regression function and enum to easily select and embed a list into the settings dialog.

How to Choose and Modify Kernels in Practice

Compact Support Kernels (e.g., Epanechnikov, Triangular): Use for localized smoothing and emphasizing nearby data.

Oscillatory Kernels (e.g., Wave, Cosine): Ideal for detecting periodic patterns or mean-reverting behavior.

Smooth Tapering Kernels (e.g., Gaussian, Logistic): Use for smoothing long-term trends or identifying global price behavior.

kernel_Epanechnikov(u)

Parameters:

u (float)

kernel_Epanechnikov_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Triangular(u)

Parameters:

u (float)

kernel_Triangular_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Rectangular(u)

Parameters:

u (float)

kernel_Uniform(u)

Parameters:

u (float)

kernel_Uniform_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Logistic(u)

Parameters:

u (float)

kernel_Logistic_alt(u)

Parameters:

u (float)

kernel_Logistic_alt2(u, sigmoid_steepness)

Parameters:

u (float)

sigmoid_steepness (float)

kernel_Gaussian(u)

Parameters:

u (float)

kernel_Gaussian_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Silverman(u)

Parameters:

u (float)

kernel_Quartic(u)

Parameters:

u (float)

kernel_Quartic_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Biweight(u)

Parameters:

u (float)

kernel_Triweight(u)

Parameters:

u (float)

kernel_Sinc(u)

Parameters:

u (float)

kernel_Wave(u)

Parameters:

u (float)

kernel_Wave_alt(u)

Parameters:

u (float)

kernel_Cosine(u)

Parameters:

u (float)

kernel_Cosine_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel(u, select, alt_modificator)

wrapper for all standard kernel functions, see enum Kernel comments and function descriptions for usage szenarios and parameters

Parameters:

u (float)

select (series Kernel)

alt_modificator (float)

kernel_regression(src, bandwidth, kernel, exponential_distance, alt_modificator)

wrapper for kernel regression with all standard kernel functions, see enum Kernel comments for usage szenarios. performance optimized version using fixed bandwidth and target

Parameters:

src (float) : input data series

bandwidth (simple int) : sample window of nearest neighbours for the kernel to process

kernel (simple Kernel) : type of Kernel to use for processing, see Kernel enum or respective functions for more details

exponential_distance (simple bool) : if true this puts more emphasis on local / more recent values

alt_modificator (float) : see kernel functions for parameter descriptions. Mostly used to pronounce emphasis on local values or introduce a decay/dampening to the kernel output

ManipulationLegHelperLibraryLibrary "ManipulationLegHelperLibrary"

TODO: add library description here

devToArray(dev)

Parameters:

dev (string)

getDev(d, bull, h, l)

Parameters:

d (float)

bull (bool)

h (float)

l (float)

getBearLeg(sweeps, minLegSize, drawLegBox, boxColor)

Parameters:

sweeps (int)

minLegSize (float)

drawLegBox (bool)

boxColor (color)

getBullLeg(sweeps, minSize, drawBox, boxColor)

Parameters:

sweeps (int)

minSize (float)

drawBox (bool)

boxColor (color)

leg

Fields:

time (series int)

low (series float)

high (series float)

edge (series bool)

edge_price (series float)

validated (series int)

sweeps (series int)

barC (series int)

bx (series box)

GapDetectGap Severity Analysis Library

This library, GapDetect , simplifies the identification and evaluation of overnight gaps by leveraging statistical metrics such as standard deviation and percentage moves. It is ideal for detecting large abnormal gaps which may be used to modify how strategies may decide to enter or exit.

Key Features:

Overnight Gap Detection

Provides two core functions:

today : Computes the value of today's overnight gap.

todayPercent : Computes the percentage change for today's overnight gap.

Volatility Analysis

Includes functions for statistical gap analysis:

normal : Calculates the normal daily standard deviation of the overnight gap, filtering outliers using customizable thresholds.

normalPercent : Similar to normal , but for percentage-based gap moves.

Gap Severity Metric

severity : a positive or negative value that represents the ratio of the current overnight move compared to the standard deviation of previous ones.

Customizable Parameters

Supports custom session specifications, resolutions, and outlier thresholds.

PitchforkLibrary "Pitchfork"

Pitchfork class

method tostring(this)

Converts PitchforkTypes/Fork object to string representation

Namespace types: Fork

Parameters:

this (Fork) : PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork

method tostring(this)

Converts Array of PitchforkTypes/Fork object to string representation

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork array

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkProperties object to string representation

Namespace types: PitchforkProperties

Parameters:

this (PitchforkProperties) : PitchforkTypes/PitchforkProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkDrawingProperties object to string representation

Namespace types: PitchforkDrawingProperties

Parameters:

this (PitchforkDrawingProperties) : PitchforkTypes/PitchforkDrawingProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkDrawingProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/Pitchfork object to string representation

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/Pitchfork

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing from PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/PitchforkDrawing object created

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing array from PitchforkTypes/Pitchfork array of objects

Namespace types: array

Parameters:

this (array) : array of PitchforkTypes/Pitchfork object

Returns: array of PitchforkTypes/PitchforkDrawing object created

method draw(this)

draws from PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object drawn

method delete(this)

deletes PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing of PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/Pitchfork object deleted

method delete(this)

deletes array of PitchforkTypes/PitchforkDrawing objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: Array of PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing in array of PitchforkTypes/Pitchfork objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Pitchfork object

Returns: Array of PitchforkTypes/Pitchfork object deleted

method clear(this)

deletes array of PitchforkTypes/PitchforkDrawing objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: void

method clear(this)

deletes array of PitchforkTypes/Pitchfork objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of Pitchfork/Pitchfork object

Returns: void

PitchforkDrawingProperties

Pitchfork Drawing Properties object

Fields:

extend (series bool) : If set to true, forks are extended towards right. Default is true

fill (series bool) : Fill forklines with transparent color. Default is true

fillTransparency (series int) : Transparency at which fills are made. Only considered when fill is set. Default is 80

forceCommonColor (series bool) : Force use of common color for forks and fills. Default is false

commonColor (series color) : common fill color. Used only if ratio specific fill colors are not available or if forceCommonColor is set to true.

PitchforkDrawing

Pitchfork drawing components

Fields:

medianLine (Line type from Trendoscope/Drawing/2) : Median line of the pitchfork

baseLine (Line type from Trendoscope/Drawing/2) : Base line of the pitchfork

forkLines (array type from Trendoscope/Drawing/2) : fork lines of the pitchfork

linefills (array type from Trendoscope/Drawing/2) : Linefills between forks

Fork

Fork object property

Fields:

ratio (series float) : Fork ratio

forkColor (series color) : color of fork. Default is blue

include (series bool) : flag to include the fork in drawing. Default is true

PitchforkProperties

Pitchfork Properties

Fields:

forks (array) : Array of Fork objects

type (series string) : Pitchfork type. Supported values are "regular", "schiff", "mschiff", Default is regular

inside (series bool) : Flag to identify if to draw inside fork. If set to true, inside fork will be drawn

Pitchfork

Pitchfork object

Fields:

a (chart.point) : Pivot Point A of pitchfork

b (chart.point) : Pivot Point B of pitchfork

c (chart.point) : Pivot Point C of pitchfork

properties (PitchforkProperties) : PitchforkProperties object which determines type and composition of pitchfork

dProperties (PitchforkDrawingProperties) : Drawing properties for pitchfork

lProperties (LineProperties type from Trendoscope/Drawing/2) : Common line properties for Pitchfork lines

drawing (PitchforkDrawing) : PitchforkDrawing object

lib_smcLibrary "lib_smc"

This is an adaptation of LuxAlgo's Smart Money Concepts indicator with numerous changes. Main changes include integration of object based plotting, plenty of performance improvements, live tracking of Order Blocks, integration of volume profiles to refine Order Blocks, and many more.

This is a library for developers, if you want this converted into a working strategy, let me know.

buffer(item, len, force_rotate)

Parameters:

item (float)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (int)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (Profile type from robbatt/lib_profile/32)

len (int)

force_rotate (bool)

swings(len)

INTERNAL: detect swing points (HH and LL) in given range

Parameters:

len (simple int) : range to check for new swing points

Returns: values are the price level where and if a new HH or LL was detected, else na

method init(this)

Namespace types: OrderBlockConfig

Parameters:

this (OrderBlockConfig)

method delete(this)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

method clear_broken(this, broken_buffer)

INTERNAL: delete internal order blocks box coordinates if top/bottom is broken

Namespace types: map

Parameters:

this (map)

broken_buffer (map)

Returns: any_bull_ob_broken, any_bear_ob_broken, broken signals are true if an according order block was broken/mitigated, broken contains the broken block(s)

create_ob(id, mode, start_t, start_i, top, end_t, end_i, bottom, break_price, early_confirmation_price, config, init_plot, force_overlay)

INTERNAL: set internal order block coordinates

Parameters:

id (int)

mode (int) : 1: bullish, -1 bearish block

start_t (int)

start_i (int)

top (float)

end_t (int)

end_i (int)

bottom (float)

break_price (float)

early_confirmation_price (float)

config (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

Returns: signals are true if an according order block was broken/mitigated

method align_to_profile(block, align_edge, align_break_price)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

align_edge (bool)

align_break_price (bool)

method create_profile(block, opens, tops, bottoms, closes, values, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

opens (array)

tops (array)

bottoms (array)

closes (array)

values (array)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

method create_profile(block, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

track_obs(swing_len, hh, ll, top, btm, bull_bos_alert, bull_choch_alert, bear_bos_alert, bear_choch_alert, min_block_size, max_block_size, config_bull, config_bear, init_plot, force_overlay, enabled, extend_blocks, clear_broken_buffer_before, align_edge_to_value_area, align_break_price_to_poc, profile_args_bull, profile_args_bear, use_soft_confirm, soft_confirm_offset, use_retracements_with_FVG_out)

Parameters:

swing_len (int)

hh (float)

ll (float)

top (float)

btm (float)

bull_bos_alert (bool)

bull_choch_alert (bool)

bear_bos_alert (bool)

bear_choch_alert (bool)

min_block_size (float)

max_block_size (float)

config_bull (OrderBlockConfig)

config_bear (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

enabled (bool)

extend_blocks (simple bool)

clear_broken_buffer_before (simple bool)

align_edge_to_value_area (simple bool)

align_break_price_to_poc (simple bool)

profile_args_bull (ProfileArgs type from robbatt/lib_profile/32)

profile_args_bear (ProfileArgs type from robbatt/lib_profile/32)

use_soft_confirm (simple bool)

soft_confirm_offset (float)

use_retracements_with_FVG_out (simple bool)

method draw(this, config, extend_only)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

config (OrderBlockConfig)

extend_only (bool)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: array

Parameters:

blocks (array)

config (OrderBlockConfig)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: map

Parameters:

blocks (map)

config (OrderBlockConfig)

method cleanup(this, ob_bull, ob_bear)

removes all Profiles that are older than the latest OrderBlock from this profile buffer

Namespace types: array

Parameters:

this (array type from robbatt/lib_profile/32)

ob_bull (OrderBlock)

ob_bear (OrderBlock)

_plot_swing_points(mode, x, y, show_swing_points, linecolor_swings, keep_history, show_latest_swings_levels, trail_x, trail_y, trend)

INTERNAL: plot swing points

Parameters:

mode (int) : 1: bullish, -1 bearish block

x (int) : x-coordingate of swing point to plot (bar_index)

y (float) : y-coordingate of swing point to plot (price)