EC_2024_Q4_SPLibrary "EC_2024_Q4_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

Indicateurs et stratégies

EC_2024_Q3_SPLibrary "EC_2024_Q3_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q4_ENLibrary "EC_2024_Q4_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q3_ENLibrary "EC_2024_Q3_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q2_ENLibrary "EC_2024_Q2_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q2_SPLibrary "EC_2024_Q2_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q1_SPLibrary "EC_2024_Q1_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q1_ENLibrary "EC_2024_Q1_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q4_SPLibrary "EC_2023_Q4_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q3_SPLibrary "EC_2023_Q3_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q2_SPLibrary "EC_2023_Q2_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q1_SPLibrary "EC_2023_Q1_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q4_ENLibrary "EC_2023_Q4_EN"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q3_ENLibrary "EC_2023_Q3_EN"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q2_ENLibrary "EC_2023_Q2_EN"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q1_ENLibrary "EC_2023_Q1_EN"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

Sessions KillZones Library [TradingFinder]🔵 Introduction

"The Forex Trading Sessions" highlight the active periods across different markets where significant trading volume and influence on the forex market are evident. The primary trading sessions globally include the "Asian Session," "London Session," and "New York Session."

A "Kill Zone" refers to a segment within a session characterized by high trading volume and notably sharper price movements. Consequently, there's a higher probability of encountering price action setups within these zones. Traders capitalize on this phenomenon in pursuit of more successful trading outcomes.

If you aim to integrate sessions or kill zones into your indicators or strategies, utilizing this library can amplify the precision and efficiency of your Python script development.

🔵 How to Use

First, you can add the library to your code as shown in the example below:

import TFlab/SessionAndKillZoneLibrary_TradingFinder/1

🟣 Parameters

SessionDetector(Session_Name, Session_Time, KillZone_Time, Session_Show, KillZone_Show, AreaUpdate, MoreInfo, Session_Color, Info_Color) =>

Parameters:

•Session_Name (string)

•Session_Time (string)

•KillZone_Time (string)

•Session_Show (bool)

•KillZone_Show (bool)

•AreaUpdate (string)

•MoreInfo (bool)

•Session_Color (color)

•Info_Color (color)

Session_Name : You must enter the session name in this parameter.

Session_Time : Enter here the start and end time of the session, which should be based on the UTC time zone.

KillZone_Time : Enter the start and end times of the kill zone, which should be based on the UTC time zone, here.

Session_Show : You can control whether or not to show the session using this entry. You must set true to display and false to not display.

KillZone_Show : Using this input you can control whether the kill zone is displayed or not. You must set true to display and false to not display.

AreaUpdate : If you want the session to be determined based on the time and high and low of the session itself, you must enter "Session" and if you want the area to be determined based on the time and high and low of the kill zone, you must enter "Kill Zone".

MoreInfo : If you want more information, you should set this entry to true, otherwise set to false. This information includes the number of candles in the area, the length of time in the area and the volume of transactions in the area.

Session_Color : Enter your desired color to display the session at this section. It is recommended to use bright and sharp colors.

Info_Color : Enter your desired color to display more information in this section.

🔵 Function Outputs

The outputs of this function are direct and indirect.

🟣 Indirect outputs

These outputs include session display, kill zone display, and time and volume information of session or kill zone.

🟣 Direct outputs

There are 8 direct outputs, which are:

Session Time : If the Session is active, it outputs 1, and if the Session is inactive, it outputs 0.

Kill Zone Time : If the Kill Zone is active, it outputs 1, and if the Kill Zone is inactive, it outputs 0.

Open : Session opening price.

High : The highest price of the session.

Low : The lowest price of the session.

Close : The last price of the session.

Low Touch Alert : If "Area Update" is in "Kill Zone" mode, if the price reaches the lowest price of the kill zone in the same session after the end of the kill zone, this output will be true. You can use this output to create an alert.

High Touch Alert : If "Area Update" is in "Kill Zone" mode, if the price reaches the highest price of the kill zone in the same session after the end of the kill zone, this output will be true. You can use this output to create an alert.

Important : To use "Open", "High", "Low" and "Close", "Area Update" must be in "Session" mode.

Useful_lib_publicLibrary "Useful_lib_public"

Useful functions

CountBarsOfDay()

count bars for one for the diffrent time frames

Returns: number of bars for one day

LastBarsOfDay()

Index number for the las bar for one day

Returns: TRUE is that the last bar from day

isTuesday()

TRUE is tuesday

Returns: TRUE is tuesday else FALSE

Rsi(src, len)

RSI calulation

Parameters:

src (float) : RSI Source

len (simple int) : RSI Length

Returns: RSI Value

CalcIndex(netPos, weeks)

Index calulation

Parameters:

netPos (float) : Source

weeks (simple int) : Length

Returns: "COT Index"

RsiStock(src, len, smoothK)

TRUE is tuesday

Parameters:

src (float)

len (simple int)

smoothK (int)

Returns: RSI Stochastik

Offset()

Use Offset for Day time frame

Returns: Offset

PercentChange(Data, LastData)

Calc different in Percent

Parameters:

Data (float)

LastData (float)

Returns: Change in percent

MathOperatorLibrary "MathOperator"

Methods to handle operators.

method add(value_a, value_b)

Add value a to b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method subtract(value_a, value_b)

subtract value b from a.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method multiply(value_a, value_b)

multiply value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method divide(value_a, value_b)

divide value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method remainder(value_a, value_b)

remainder of a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method equal(value_a, value_b)

equality of value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method not_equal(value_a, value_b)

inequality of value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method over(value_a, value_b)

value a is over b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method under(value_a, value_b)

value a is under b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method over_equal(value_a, value_b)

value a is over equal b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method under_equal(value_a, value_b)

value a is under equal b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method and_(value_a, value_b)

logical and of a with b

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method or_(value_a, value_b)

logical or of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method not_(value_a)

logical not of a.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

Returns: bool.

method xor_(value_a, value_b)

logical xor of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method xnor_(value_a, value_b)

logical xnor of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method nand_(value_a, value_b)

logical nand of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method nor_(value_a, value_b)

logical nor of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

strategy_helpersThis library is designed to aid traders and developers in calculating risk metrics efficiently across different asset types like equities, futures, and forex. It includes comprehensive functions that calculate the number of units or contracts to trade, the value at risk, and the total value of the position based on provided entry prices, stop levels, and risk percentages. Whether you're managing a portfolio or developing trading strategies, this library provides essential tools for risk management. Functions also automatically select the appropriate risk calculation method based on asset type, calculate leverage levels, and determine potential liquidation points for leveraged positions. Perfect for enhancing the precision and effectiveness of your trading strategies.

Library "strategy_helpers"

Provides tools for calculating risk metrics across different types of trading strategies including equities, futures, and forex. Functions allow for precise control over risk management by calculating the number of units or contracts to trade, the value at risk, and the total position value based on entry prices, stop levels, and desired risk percentage. Additional utilities include automatic risk calculation based on asset type, leverage level calculations, and determination of liquidation levels for leveraged trades.

calculate_risk(entry, stop_level, stop_range, capital, risk_percent, trade_direction, whole_number_buy)

Calculates risk metrics for equity trades based on entry, stop level, and risk percent

Parameters:

entry (float) : The price at which the position is entered. Use close if you arent adding to a position. Use the original entry price if you are adding to a position.

stop_level (float) : The price level where the stop loss is placed

stop_range (float) : The price range from entry to stop level

capital (float) : The total capital available for trading

risk_percent (float) : The percentage of capital risked on the trade. 100% is represented by 100.

trade_direction (bool) : True for long trades, false for short trades

whole_number_buy (bool) : True to adjust the quantity to whole numbers

Returns: A tuple containing the number of units to trade, the value at risk, and the total value of the position:

calculate_risk_futures(risk_capital, stop_range)

Calculates risk metrics for futures trades based on the risk capital and stop range

Parameters:

risk_capital (float) : The capital allocated for the trade

stop_range (float) : The price range from entry to stop level

Returns: A tuple containing the number of contracts to trade, the value at risk, and the total value of the position:

calculate_risk_forex(entry, stop_level, stop_range, capital, risk_percent, trade_direction)

Calculates risk metrics for forex trades based on entry, stop level, and risk percent

Parameters:

entry (float) : The price at which the position is entered. Use close if you arent adding to a position. Use the original entry price if you are adding to a position.

stop_level (float) : The price level where the stop loss is placed

stop_range (float) : The price range from entry to stop level

capital (float) : The total capital available for trading

risk_percent (float) : The percentage of capital risked on the trade. 100% is represented by 100.

trade_direction (bool) : True for long trades, false for short trades

Returns: A tuple containing the number of lots to trade, the value at risk, and the total value of the position:

calculate_risk_auto(entry, stop_level, stop_range, capital, risk_percent, trade_direction, whole_number_buy)

Automatically selects the risk calculation method based on the asset type and calculates risk metrics

Parameters:

entry (float) : The price at which the position is entered. Use close if you arent adding to a position. Use the original entry price if you are adding to a position.

stop_level (float) : The price level where the stop loss is placed

stop_range (float) : The price range from entry to stop level

capital (float) : The total capital available for trading

risk_percent (float) : The percentage of capital risked on the trade. 100% is represented by 100.

trade_direction (bool) : True for long trades, false for short trades

whole_number_buy (bool) : True to adjust the quantity to whole numbers, applicable only for non-futures and non-forex trades

Returns: A tuple containing the number of units or contracts to trade, the value at risk, and the total value of the position:

leverage_level(account_equity, position_value)

Calculates the leverage level used based on account equity and position value

Parameters:

account_equity (float) : Total equity in the trading account

position_value (float) : Total value of the position taken

Returns: The leverage level used in the trade

calculate_liquidation_level(entry, leverage, trade_direction, maintenance_margine)

Calculates the liquidation price level for a leveraged trade

Parameters:

entry (float) : The price at which the position is entered

leverage (float) : The leverage level used in the trade

trade_direction (bool) : True for long trades, false for short trades

maintenance_margine (float) : The maintenance margin requirement, expressed as a percentage

Returns: The price level at which the position would be liquidated, or na if leverage is zero

WebhookMessageDevLibrary "WebhookMessageDev"

The webhook message library provides several functions for building JSON payloads

method buildWebhookJson(msg)

Builds the final JSON payload from a webhookMessage type.

Namespace types: webhookMessage

Parameters:

msg (webhookMessage) : (webhookMessage) A prepared webhookMessage.

Returns: A JSON Payload.

method buildTakeProfitJson(msg)

Builds the takeProfit JSON message to be used in a webhook message.

Namespace types: takeProfitMessage

Parameters:

msg (takeProfitMessage) : (takeProfitMessage)

Returns: A JSON takeProfit payload.

method buildStopLossJson(msg)

Builds the stopLoss JSON message to be used in a webhook message.

Namespace types: stopLossMessage

Parameters:

msg (stopLossMessage) : (stopLossMessage)

Returns: A JSON stopLoss payload.

webhookMessage

Final webhook message.

Fields:

ticker (series string)

action (series string)

sentiment (series string)

price (series float)

quantity (series int)

takeProfit (series string)

stopLoss (series string)

takeProfitMessage

Take profit message.

Fields:

limitPrice (series float)

percent (series float)

amount (series float)

stopLossMessage

Stop loss message.

Fields:

type (series string)

percent (series float)

amount (series float)

stopPrice (series float)

limitPrice (series float)

trailPrice (series float)

trailPercent (series float)

chrono_utilsLibrary "chrono_utils"

Collection of objects and common functions that are related to datetime windows session days and time

ranges. The main purpose of this library is to handle time-related functionality and make it easy to reason about a

future bar checking if it will be part of a predefined session and/or inside a datetime window. All existing session

functionality I found in the documentation e.g. "not na(time(timeframe, session, timezone))" are not suitable for

strategy scripts, since the execution of the orders is delayed by one bar, due to the script execution happening at

the bar close. Moreover, a history operator with a negative value that looks forward is not allowed in any pinescript

expression. So, a prediction for the next bar using the bars_back argument of "time()"" and "time_close()" was

necessary. Thus, I created this library to overcome this small but very important limitation. In the meantime, I

added useful functionality to handle session-based behavior. An interesting utility that emerged from this

development is the data anomaly detection where a comparison between the prediction and the actual value is happening.

If those two values are different then a data inconsistency happened between the prediction bar and the actual bar

(probably due to a holiday, half session day, a timezone change etc..)

exTimezone(timezone)

exTimezone - Convert extended timezone to timezone string

Parameters:

timezone (simple string) : - The timezone or a special string

Returns: string representing the timezone

nameOfDay(day)

nameOfDay - Convert the day id into a short nameOfDay

Parameters:

day (int) : - The day id to convert

Returns: - The short name of the day

today()

today - Get the day id of this day

Returns: - The day id

nthDayAfter(day, n)

nthDayAfter - Get the day id of n days after the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days after the reference day

nextDayAfter(day)

nextDayAfter - Get the day id of next day after the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the next day after the reference day

nthDayBefore(day, n)

nthDayBefore - Get the day id of n days before the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days before the reference day

prevDayBefore(day)

prevDayBefore - Get the day id of previous day before the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the previous day before the reference day

tomorrow()

tomorrow - Get the day id of the next day

Returns: - The next day day id

normalize(num, min, max)

normalizeHour - Check if number is inthe range of

Parameters:

num (int)

min (int)

max (int)

Returns: - The normalized number

normalizeHour(hourInDay)

normalizeHour - Check if hour is valid and return a noralized hour range from

Parameters:

hourInDay (int)

Returns: - The normalized hour

normalizeMinute(minuteInHour)

normalizeMinute - Check if minute is valid and return a noralized minute from

Parameters:

minuteInHour (int)

Returns: - The normalized minute

monthInMilliseconds(mon)

monthInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Parameters:

mon (int) : - The month of reference to get the miliseconds

Returns: - The number of milliseconds of the month

barInMilliseconds()

barInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Returns: - The number of milliseconds in one bar

method to_string(this)

to_string - Formats the time window into a human-readable string

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The string of the time window

method to_string(this)

to_string - Formats the session days into a human-readable string with short day names

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The string of the session day short names

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_string(this)

to_string - Formats the session into a human-readable string

Namespace types: Session

Parameters:

this (Session) : - The session object with the day and the time range selection

Returns: - The string of the session

method init(this, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, refTimezone, chTimezone, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

refTimezone (simple string) : - The timezone of reference of the 'from' and 'to' dates

chTimezone (simple string) : - The target timezone to convert the 'from' and 'to' dates

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, sun, mon, tue, wed, thu, fri, sat)

init - Initialize the session days object from boolean values of each session day

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sun (bool) : - Is Sunday a trading day?

mon (bool) : - Is Monday a trading day?

tue (bool) : - Is Tuesday a trading day?

wed (bool) : - Is Wednesday a trading day?

thu (bool) : - Is Thursday a trading day?

fri (bool) : - Is Friday a trading day?

sat (bool) : - Is Saturday a trading day?

Returns: - The session days object

method init(this, unixTime)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

unixTime (int) : - The unix time

Returns: - The session time object

method init(this, hourInDay, minuteInHour)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

Returns: - The session time object

method init(this, hourInDay, minuteInHour, refTimezone)

init - Initialize the object from the hour and minute of the session time

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

refTimezone (string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method init(this, startTime, endTime)

init - Initialize the object from the start and end session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTime (SessionTime) : - The time the session begins

endTime (SessionTime) : - The time the session ends

Returns: - The session time range object

method init(this, startTimeHour, startTimeMinute, endTimeHour, endTimeMinute, refTimezone)

init - Initialize the object from the start and end session time

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTimeHour (int) : - The time hour the session begins

startTimeMinute (int) : - The time minute the session begins

endTimeHour (int) : - The time hour the session ends

endTimeMinute (int) : - The time minute the session ends

refTimezone (string)

Returns: - The session time range object

method init(this, days, timeRanges)

init - Initialize the session object from session days and time range

Namespace types: Session

Parameters:

this (Session) : - The session object that will hold the day and the time range selection

days (SessionDays) : - The session days object that defines the days the session is happening

timeRanges (array) : - The array of all the session time ranges during a session day

Returns: - The session object

method init(this, days, timeRanges, names, colors)

init - Initialize the session object from session days and time range

Namespace types: SessionView

Parameters:

this (SessionView) : - The session view object that will hold the session, the names and the color selections

days (SessionDays) : - The session days object that defines the days the session is happening

timeRanges (array) : - The array of all the session time ranges during a session day

names (array) : - The array of the names of the sessions

colors (array) : - The array of the colors of the sessions

Returns: - The session object

method get_size_in_secs(this)

get_size_in_secs - Count the seconds from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of seconds inside the time widow for the given timeframe

method get_size_in_secs(this)

get_size_in_secs - Calculate the seconds inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of seconds inside the session

method get_size_in_bars(this)

get_size_in_bars - Count the bars from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of bars inside the time widow for the given timeframe

method get_size_in_bars(this)

get_size_in_bars - Calculate the bars inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of bars inside the session for the given timeframe

method is_bar_included(this, offset_forward)

is_bar_included - Check if the given bar is between the start and end dates of the window

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

offset_forward (simple int) : - The number of bars forward. Default is 1

Returns: - Whether the current bar is inside the datetime window

method is_bar_included(this, offset_forward)

is_bar_included - Check if the given bar is inside the session as defined by the input params (what "not na(time(timeframe.period, this.to_sess_string()) )" should return if you could write it

Namespace types: Session

Parameters:

this (Session) : - The session with the day and the time range selection

offset_forward (simple int) : - The bar forward to check if it is between the from and to datetimes. Default is 1

Returns: - Whether the current time is inside the session

method to_sess_string(this)

to_sess_string - Formats the session days into a session string with day ids

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object

Returns: - The string of the session day ids

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the session into a session string

Namespace types: Session

Parameters:

this (Session) : - The session object with the day and the time range selection

Returns: - The string of the session

method from_sess_string(this, sess)

from_sess_string - Initialize the session days object from the session string

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sess (string) : - The session string part that represents the days

Returns: - The session days object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

Returns: - The session time object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time object from the session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

refTimezone (simple string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time range object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time range object from the session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method from_sess_string(this, sess)

from_sess_string - Initialize the session object from the session string in exchange timezone (syminfo.timezone)

Namespace types: Session

Parameters:

this (Session) : - The session object that will hold the day and the time range selection

sess (string) : - The session string that represents the session HHmm-HHmm,HHmm-HHmm:ddddddd

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session object from the session string

Namespace types: Session

Parameters:

this (Session) : - The session object that will hold the day and the time range selection

sess (string) : - The session string that represents the session HHmm-HHmm,HHmm-HHmm:ddddddd

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method nth_day_after(this, day, n)

nth_day_after - The nth day after the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week after the given day

method nth_day_before(this, day, n)

nth_day_before - The nth day before the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week before the given day

method next_day(this)

next_day - The next day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the next session day of the week

method previous_day(this)

previous_day - The previous day that is session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the previous session day of the week

method get_sec_in_day(this)

get_sec_in_day - Count the seconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of seconds passed from the start of the day until that session time

method get_ms_in_day(this)

get_ms_in_day - Count the milliseconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of milliseconds passed from the start of the day until that session time

method is_day_included(this, day)

is_day_included - Check if the given day is inside the session days

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day to check if it is a trading day

Returns: - Whether the current day is included in the session days

DateTimeWindow

DateTimeWindow - Object that represents a datetime window with a beginning and an end

Fields:

fromDateTime (series int) : - The beginning of the datetime window

toDateTime (series int) : - The end of the datetime window

SessionDays

SessionDays - Object that represent the trading days of the week

Fields:

days (map) : - The map that contains all days of the week and their session flag

SessionTime

SessionTime - Object that represents the time (hour and minutes)

Fields:

hourInDay (series int) : - The hour of the day that ranges from 0 to 24

minuteInHour (series int) : - The minute of the hour that ranges from 0 to 59

minuteInDay (series int) : - The minute of the day that ranges from 0 to 1440. They will be calculated based on hourInDay and minuteInHour when method is called

SessionTimeRange

SessionTimeRange - Object that represents a range that extends from the start to the end time

Fields:

startTime (SessionTime) : - The beginning of the time range

endTime (SessionTime) : - The end of the time range

isOvernight (series bool) : - Whether or not this is an overnight time range

Session

Session - Object that represents a session

Fields:

days (SessionDays) : - The map of the trading days

timeRanges (array) : - The array with all time ranges of the session during the trading days

SessionView

SessionView - Object that visualize a session

Fields:

sess (Session) : - The Session object to be visualized

names (array) : - The names of the session time ranges

colors (array) : - The colors of the session time ranges

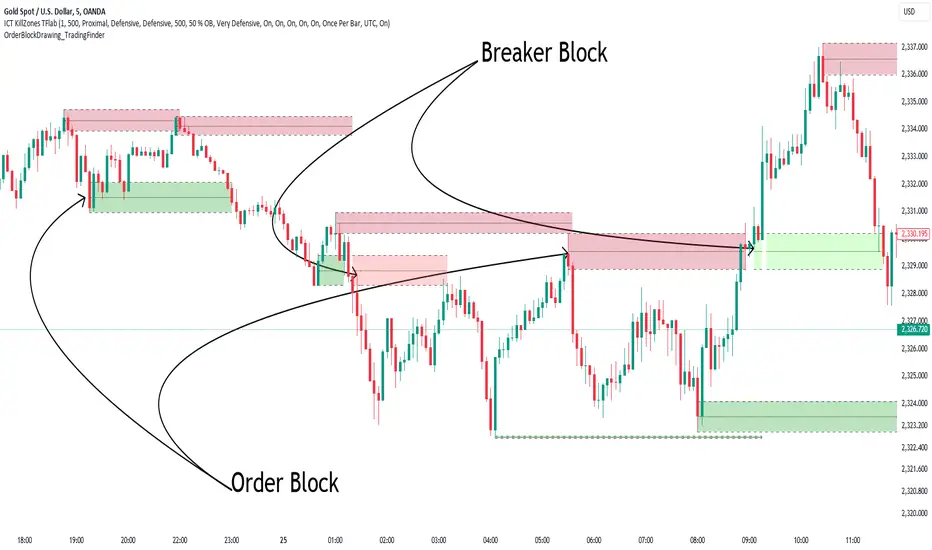

Order Block Drawing [TradingFinder]🔵 Introduction

Perhaps one of the most challenging tasks for Pine script developers (especially beginners) is properly drawing order blocks. While utilizing the latest technical analysis methods for "Price Action," beginners heavily rely on accurately plotting "Supply" and "Demand" zones, following concepts like "Smart Money Concept" and "ICT".

However, drawing "Order Blocks" may pose a challenge for developers. Therefore, to minimize bugs, increase accuracy, and speed up the process of coding order blocks, we have released the "Order Block Drawing" library.

Below, you can read more details about how to use this library.

Important :

This library has direct and indirect outputs. The indirect output includes the ranges of order blocks plotted on the chart. However, the direct output is a "Boolean" value that becomes "true" only when the price touches an order block, colloquially termed as "Mitigate." You can use this output for setting up alerts.

🔵 How to Use

First, you can add the library to your code as shown in the example below.

import TFlab/OrderBlockDrawing_TradingFinder/1

🟣Parameters

OBDrawing(OBType, TriggerCondition, DistalPrice, ProximalPrice, Index, OBValidDis, Show, ColorZone) =>

Parameters:

• OBType (string)

• TriggerCondition (bool)

• DistalPrice (float)

• ProximalPrice (float)

• Index (int)

• OBValidDis (int)

• Show (bool)

• ColorZone (color)

OBType : All order blocks are summarized into two types: "Supply" and "Demand." You should input your order block type in this parameter. Enter "Demand" for drawing demand zones and "Supply" for drawing supply zones.

TriggerCondition : Input the condition under which you want the order block to be drawn in this parameter.

DistalPrice : Generally, if each zone is formed by two lines, the farthest line from the price is termed "Distal." This input receives the price of the "Distal" line.

ProximalPrice : Generally, if each zone is formed by two lines, the nearest line to the price is termed "Proximal" line.

Index : This input receives the value of the "bar_index" at the beginning of the order block. You should store the "bar_index" value at the occurrence of the condition for the order block to be drawn and input it here.

OBValidDis : Order blocks continue to be drawn until a new order block is drawn or the order block is "Mitigate." You can specify how many candles after their initiation order blocks should continue. If you want no limitation, enter the number 4998.

Show : You may need to manage whether to display or hide order blocks. When this input is "On", order blocks are displayed, and when it's "Off", order blocks are not displayed.

ColorZone : You can input your preferred color for drawing order blocks.

🔵 Function Outputs

This function has only one output. This output is of type "Boolean" and becomes "true" only when the price touches an order block. Each order block can be touched only once and then loses its validity. You can use this output for alerts.

= Drawing.OBDrawing('Demand', Condition, Distal, Proximal, Index, 4998, true, Color)