Super Trend LineThe classic and simple Super Trend Line. Enjoy it and have a nice trading

Hashtag_binary ;D

Recherche dans les scripts pour "algo"

Alerta de Cruce de Medias MovilesAlgoritmo que indica el momento en que las EMA de corto y largos periodos se crucen y generen cambio de tendencias- Asi poder identificar cuando comprar y cuando vender.

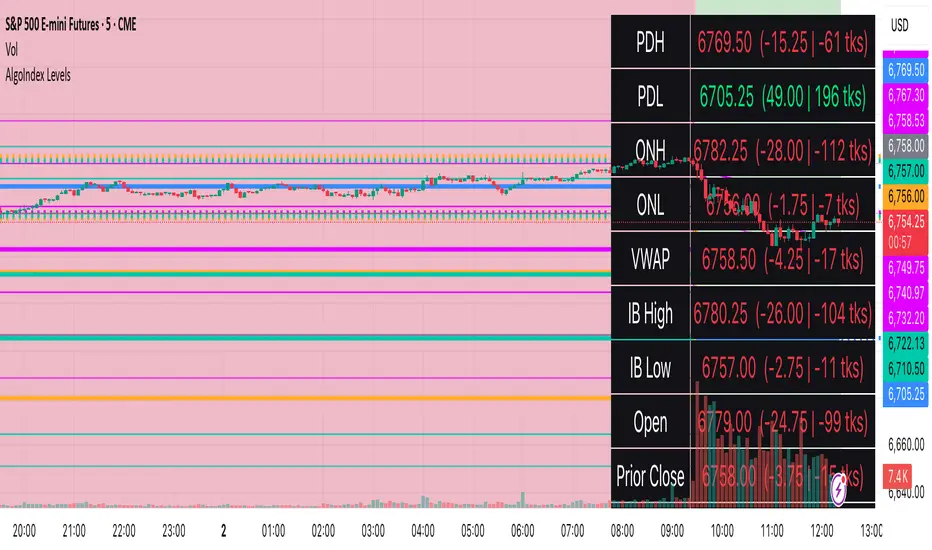

RTH Levels: VWAP + PDH/PDL + ONH/ONL + IBAlgo Index — Levels Pro (ONH/ONL • PDH/PDL • VWAP±Bands • IB • Gaps)

Purpose. A session-aware, non-repainting levels tool for intraday decision-making. Designed for futures and indices, with clean visuals, alerts, and a one-click Minimal Mode for screenshot-ready charts.

What it plots

• PDH/PDL (RTH-only) – Prior Regular Trading Hours high/low, computed intraday and frozen at the RTH close (no 24h mix-ups, no repainting).

• ONH/ONL – Prior Overnight high/low, held throughout RTH.

• RTH VWAP with ±σ bands – Volume-weighted variance, reset each RTH.

• Initial Balance (IB) – First N minutes of RTH, plus 1.5× / 2.0× extensions after IB completes.

• Today’s RTH Open & Prior RTH Close – With gap detection and “gap filled” alert.

• Killzone shading – NY Open (09:30–10:30 ET) and Lunch (11:15–13:30 ET).

• Values panel (top-right) – Each level with live distance in points & ticks.

• Right-edge level tags – With anti-overlap (stagger + vertical jitter).

• Price-scale tags – Native trackprice markers that always “stick” to the axis.

⸻

New in v6.4

• Minimal Mode: one click for a clean look (thinner lines, VWAP bands/IB extensions hidden, on-chart right-edge labels off; price-scale tags remain).

• Theme presets: Dark Hi-Contrast / Light Minimal / Futures Classic / Muted Dark.

• Anti-overlap controls: horizontal staggering, vertical jitter, and baseline offset to keep tags readable even when levels cluster.

⸻

Quick start (2 minutes)

1. Add to chart → keep defaults.

2. Sessions (ET):

• RTH Session default: 09:30–16:00 (US equities cash hours).

• Overnight Session default: 18:00–09:29.

Adjust for your market if you use different “day” hours (e.g., many use 08:20–13:30 ET for COMEX Gold).

3. Theme & Minimal Mode: pick a Theme Preset; enable Minimal Mode for screenshots.

4. Visibility: toggle PD/ON/VWAP/IB/References/Panel to taste.

5. Right-edge labels: turn Show Right-Edge Labels on. If they crowd, tune:

• Anti-overlap: min separation (ticks)

• Horizontal offset per tag (bars)

• Vertical jitter per step (ticks)

• Right-edge baseline offset (bars)

6. Alerts: open Add alert → Condition: and pick the events you want.

⸻

How levels are computed (no repainting)

• PDH/PDL: Intraday H/L are accumulated only while in RTH and saved at RTH close for “yesterday’s” values.

• ONH/ONL: Accumulated across the defined Overnight window and then held during RTH.

• RTH VWAP & ±σ: Volume-weighted mean and standard deviation, reset at the RTH open.

• IB: First N minutes of RTH (default 60). Extensions (1.5×/2.0×) appear after IB completes.

• Gaps: Today’s RTH open vs prior RTH close; “Gap Filled” triggers when price trades back to prior close.

⸻

Practical playbooks (how to trade around the levels)

1) PDH/PDL interactions

• Rejection: Price taps PDH/PDL then closes back inside → mean-reversion toward VWAP/IB.

• Acceptance: Close/hold beyond PDH/PDL with momentum → continuation to next HTF/IB target.

• Alert: PD Touch/Break.

2) ONH/ONL “taken”

• Often one ON extreme is taken during RTH. ONH Taken / ONL Taken → check if it’s a clean break or sweep & reclaim.

• Sweep + reclaim near VWAP can fuel rotations through the ON range.

3) VWAP ±σ framework

• Balanced: First tag of ±1σ often reverts toward VWAP.

• Trend: Persistent trade beyond ±1σ + IB break → target ±2σ/±3σ.

• Alerts: VWAP Cross and VWAP Reject (cross then immediate fail back).

4) IB breaks

• After IB completes, a clean IB break commonly targets 1.5× and sometimes 2.0×.

• Quick return inside IB = possible fade back to the opposite IB edge/VWAP.

• Alerts: IB Break Up / Down.

5) Gaps

• Gap-and-go: Opening drive away from prior close + VWAP support → trend until IB completion.

• Gap-fill: Weak open and VWAP overhead/underfoot → trade toward prior close; manage on Gap Filled alert.

Pro tip: Stack confluences (e.g., ONL sweep + VWAP reclaim + IB hold) and respect your execution rules (e.g., require a 5-minute close in direction, or your order-flow confirmation).

⸻

Inputs you’ll actually touch

• Sessions (ET): Session Timezone, RTH Session, Overnight Session.

• Visibility: toggles for PD/ON/VWAP/IB/Ref/Panel.

• VWAP bands: set σ multipliers (±1/±2/±3).

• IB: duration (minutes) and extension multipliers (1.5× / 2.0×).

• Style & Theme: Theme Preset, Main Line Width, Trackprice, Minimal Mode, and anti-overlap controls.

⸻

Alerts included

• PD Touch/Break — High ≥ PDH or Low ≤ PDL

• ONH Taken / ONL Taken — First in-RTH take of ONH/ONL

• VWAP Cross — Close crosses VWAP

• VWAP Reject — Cross then immediate fail back

• IB Break Up / Down — Break of IB High/Low after IB completes

• Gap Filled — Price trades back to prior RTH close

Setup: Add alert → Condition: Algo Index — Levels Pro → choose event → message → Notify on app/email.

⸻

Panel guide

The top-right panel shows each level plus live distance from last price:

LevelValue (Δpoints | Δticks)

Coloring: green if level is below current price, red if above.

⸻

Styling & screenshot tips

• Use Theme Preset that matches your chart.

• For dark charts, “Dark Hi-Contrast” with Main Line Width = 3 works well.

• Enable Trackprice for crisp axis tags that always stick to the right edge.

• Turn on Minimal Mode for cleaner screenshots (no VWAP bands or IB extensions, on-chart tags off; price-scale tags remain).

• If tags crowd, increase min separation (ticks) to 30–60 and horizontal offset to 3–5; add vertical jitter (4–12 ticks) and/or push tags farther right with baseline offset (bars).

⸻

Behavior & limitations

• Levels are computed incrementally; tables refresh on the last bar for efficiency.

• Right-edge labels are placed at bar_index + offset and do not track extra right-margin scrolling (TradingView limitation). The price-scale tags (from trackprice) do track the axis.

• “RTH” is what you define in inputs. If your market uses different day hours, change the session strings so PDH/PDL reflect your definition of “yesterday’s session.”

⸻

FAQ

Q: My PDH/PDL don’t match the daily chart.

A: By design this uses RTH-only highs/lows, not 24h daily bars. Adjust sessions if you want a different definition.

Q: Right-edge tags overlap or don’t sit at the far right.

A: Increase min separation / horizontal offset / vertical jitter and/or push tags farther with baseline offset. If you want markers that always hug the axis, rely on Trackprice.

Q: Can I change killzones?

A: Yes—edit the session strings in settings or request a version with user inputs for custom windows.

⸻

Disclaimer

Educational use only. This is not financial advice. Always apply your own risk management and confirmation rules.

⸻

Enjoy it? Please ⭐ the script and share screenshots using Minimal Mode + a Theme Preset that fits your style.

[Algo/Fract] CoreAutomate your chart analysis with fractal-based logic and multi-timeframe clarity — built for traders who value clean visual context.

Witness the Framework beneath the Market’s movement.

Every Trend starts with Structure.

Features included are:

Triple Fractal Bands (TFB)

MoneyFlow Diamonds (MFD)

MicroTrend Dots (MTD)

4D Trend Colors (4DTC)

AutoSR Grid (ASRG)

Gain Access at: www.algofract.com

or by visiting our Whop Marketplace: whop.com

Algo ۞ Halo 7MAs WonderA complete trend following and important MA crossing tool.

The indicator is self-explanatory. You decide where you want the triggers to go.

Enjoy!

ALGO 3h, 1h, 2hThis script tracks the crossing of the 10EMA on the 3h timeframe and the 200EMA on the 1h timeframe to open LONGS and SHORTS. Whether those LONGS or SHORTS actually trigger is based on the first 2 EMA's position in relation to a 3rd "controller" EMA.

QuantCodes [Trial]Algorithm showing potential profit with minimal risk for every market signal.

QuantCodes Premium Click Here.

Guided144Algorithm conditions suggested by a friend, works best on daily tf for bitcoin.

simple cycle trading of buy and sell..

A great guide for trading those complicated moves.

X-Trend reversal (PRO) 👑 X-TREND REVERSAL (PRO): Institutional Order Flow Analysis

Look at the results above. This is not luck. This is mathematics. X-Trend PRO is the flagship algorithm of our ecosystem, engineered for traders who have outgrown standard technical analysis. While the Lite version identifies trends, the PRO version sees where the money is.

Unlike 99% of indicators that focus solely on price action, X-Trend PRO analyzes Market Liquidity and Volume Delta (CVD). We have fused market structure with an X-ray view of institutional activity.

💎 EXCLUSIVE PRO FEATURES:

📊 Volume & CVD Fusion: The indicator detects Cumulative Volume Delta divergences. It warns you of reversals when price is still rising, but buyers have already left the market.

📍 Dynamic POC (Point of Control): Automatically identifies "fair price" levels and institutional accumulation zones. You trade from levels defended by market makers.

🛡 Zero Repaint Guarantee: The signal is locked permanently upon bar close. The history you see is the actual real-time performance of the algorithm.

🧠 Smart Filtering: The system filters out "noise" in ranging markets, generating signals only when Trend, Momentum, and Volume align perfectly.

⚠️ IMPORTANT: SYSTEM SYNERGY

While X-Trend PRO is a powerful standalone tool, the author does not recommend using it in isolation. To achieve the "Sniper Efficiency" shown in the screenshots and to ensure deep market confluence, this tool is engineered to work ideally in synergy with the X-Trend Dashboard PRO. Combining these modules provides the ultimate confirmation system.

🔒 HOW TO GET ACCESS (INVITE-ONLY)

This script is a closed-source proprietary tool. Access is granted exclusively through our official channels.

⛔ NOTE: We do NOT respond to access requests in the comment section below. Please use the links above for instant support and license activation.

ORB Strategy - EnhancedThis algo is for setting and forgetting ORB. Does require an understanding of how to tweak trading factors

AlphaSignals Pro🟠OVERVIEW

AlphaSignals Pro™ is a comprehensive trading indicator suite developed by A1TradingHub. The

system combines trend analysis, momentum indicators, and proprietary signal algorithms to identify

high-probability trading opportunities across all market conditions and timeframes.

Core Components

■ Long/Short Signals — Clear entry markers based on trend reversals and momentum shifts

■ Golden Call/Put — Premium signals for high-conviction directional trades

■ Support & Resistance — Dynamic price zones with visual highlighting

■ Moving Averages — Trend direction with color-coded crossover signals

■ Keltner Channels — Volatility bands for breakout and mean-reversion setups

■ Signal Dashboard — Multi-symbol overview with trend and momentum status

🟠Long & Short Entry Signals

The core signal system identifies optimal entry points by analyzing price action, momentum, and

trend structure. LONG signals appear at potential reversal points for upward moves, while SHORT

signals indicate bearish opportunities at resistance.

◆ Green 'LONG' labels mark buy zones at support levels

◆ Red 'SHORT' labels indicate sell zones at resistance

◆ Momentum confirmation filters out false signals

◆ Works across all timeframes (1min to daily)

🟠Trend Direction Arrows

Small directional arrows provide real-time trend feedback. ▲ Green arrows confirm bullish

momentum, ▼ red arrows signal bearish pressure. These micro-signals help traders stay aligned with

the dominant trend.

◆ Green up arrows during bullish momentum phases

◆ Red down arrows indicate bearish momentum shifts

◆ Confirms entry signals and aids trade management

◆ Minimalist design preserves chart clarity

🟠 Golden Put Signal

The Golden Put identifies high-probability short opportunities. Triggers when multiple bearish factors

align: price rejection at resistance, momentum divergence, and volume confirmation. These premium

signals represent the highest-conviction bearish trades.

◆ Triggered at major resistance with momentum divergence

◆ Red 'GOLDEN PUT' label marks premium short entries

◆ Designed for options traders seeking directional plays

◆ Lower frequency, higher accuracy than standard signals

🟠 Golden Call Signal

The Golden Call is the bullish counterpart, identifying premium long opportunities. Appears when

price finds strong support with bullish momentum divergence and institutional volume patterns. Marks

optimal entry points for aggressive upside plays.

◆ Yellow 'GOLDEN CALL' highlights premium buy setups

◆ Triggers at key support with momentum confirmation

◆ Ideal for call options or leveraged positions

◆ Signals typically precede significant advances

🟠 Moving Average System

The dual moving average system provides trend context and dynamic support/resistance. The red

line is the fast MA (shorter period), the green line is the slow MA. Color transitions indicate trend

changes and crossover signals.

◆ Red MA: Fast period for short-term direction

◆ Green MA: Slow period for primary trend

◆ Bullish crossover: Fast crosses above slow

◆ Bearish crossover: Fast crosses below slow

◆ MAs act as dynamic support/resistance

🟠 Keltner Channel Bands

Volatility-based price envelopes that adapt to market conditions. Bands expand during high volatility,

contract during consolidation. Price at outer bands signals mean-reversion opportunities; breakouts

beyond bands may indicate trend continuation.

◆ Upper/lower bands adapt to current volatility

◆ Pink outer bands mark extreme price zones

◆ Cyan middle band shows baseline trend

◆ Band touches signal reversal or breakout setups

◆ Shaded fill visualizes the volatility range

🟠 Support & Resistance Zones

Automatic detection of key price levels with visual highlighting. Green zones mark support where

buying pressure emerges, red zones highlight resistance with selling pressure. Dashed lines show

precise price levels.

◆ Green shaded areas: Support zones (buy interest)

◆ Red shaded areas: Resistance zones (sell interest)

◆ Horizontal dashed lines mark exact levels

◆ Zones update dynamically as new levels form

◆ Essential for targets and stop-loss placement

🟠 Golden Signal Dashboard

Multi-symbol dashboard provides comprehensive market overview. Track multiple instruments with

real-time trend status, momentum readings, active signals, and freshness indicators. Perfect for

scanning opportunities across your watchlist.

◆ SYMBOL: Tracked instruments (SPY, QQQ, IWM, TSLA)

◆ PRICE & CHG%: Current price and daily change

◆ MOMENTUM: Bullish/Bearish classification

◆ SIGNAL: Active Golden Call or Put signals

◆ BARS: Bars since last signal

◆ STATUS: Signal temperature (HOT/WARM/COLD)

🟠 Best Practices

✓ Confirm signals with dominant trend (use MAs)

✓ Prioritize Golden signals — higher probability

✓ Use S/R zones for stop-loss placement

✓ Check dashboard for multi-timeframe confluence

✓ Combine with your own analysis

Triple VWAP: Anchored# Triple VWAP: Anchored + Last 2 Sessions

## 📊 Overview

**Triple VWAP** is a professional-grade Volume Weighted Average Price (VWAP) indicator designed for serious traders who need multi-timeframe volume analysis on a single chart. This indicator combines three powerful VWAP calculations: a custom **Anchored VWAP** from any historical date, a real-time **Current Session VWAP**, and **Previous Session VWAP** reference levels—all with configurable standard deviation bands.

Perfect for intraday traders, swing traders, and institutional-level analysis on Indian markets (Nifty, BankNifty) and global instruments.

***

## ✨ Key Features

### 🎯 Three Independent VWAP Calculations

**📍 Anchored VWAP (Long-term Reference)**

- Anchor VWAP from any specific date and time (year, month, day, hour, minute)

- Ideal for tracking price action from significant market events, earnings, or trend reversals

- Maintains accumulation from your chosen anchor point throughout the entire timeframe

**📅 Current Session VWAP (Real-Time)**

- Automatically resets at the start of each trading day

- Calculates dynamically as new bars form during the session

- Shows institutional trading levels and intraday fair value

**📆 Previous Session VWAP (Reference Levels)**

- Displays yesterday's final VWAP as horizontal reference lines

- Helps identify support/resistance zones from prior session

- Useful for gap analysis and opening range strategies

### 📐 Standard Deviation Bands

Each VWAP calculation includes optional standard deviation bands:

- **±1 SD** - Identifies normal price deviation zones

- **±2 SD** - Marks extreme price movements (high probability reversal zones)

- **±3 SD** - Ultra-extreme levels (rare price extensions)

Configure which SD levels to display for each VWAP type independently.

### 🎨 Customizable Visual Settings

- **Independent Color Schemes**: Assign unique colors to each VWAP type and its SD bands

- **Adjustable Line Widths**: Configure VWAP and SD line thickness (1-5 for VWAP, 1-3 for SD)

- **Plot Styles**: Previous session plots use cross-style for clear differentiation from real-time plots

- **Background Zones**: Optional colored zones when price extends beyond ±2 SD levels

- **Session Labels**: Automatic date labels marking each VWAP anchor point

### 📊 Information Dashboard

Real-time statistics table displaying:

- Current VWAP values for all three calculations

- Live standard deviation values

- ±1 SD levels for quick reference

- Distance from price to each VWAP (percentage format)

- Session tracking counter

- Color-coded proximity indicators

***

## 🔧 How to Use

### For Intraday Trading

1. **Current Session VWAP** acts as dynamic support/resistance—price above VWAP indicates bullish bias, below indicates bearish bias

2. Use **±1 SD bands** for profit targets and stop-loss placement

3. **±2 SD touches** often signal mean reversion opportunities

4. **Previous Session VWAP** provides overnight gap reference levels

### For Swing Trading

1. **Anchored VWAP** from significant events (breakouts, earnings, trend changes) shows institutional cost basis

2. Price trading consistently above/below anchored VWAP confirms trend strength

3. SD band rejections provide high-probability entry zones

### For Multi-Timeframe Analysis

1. Combine all three VWAPs to identify confluence zones

2. When current session VWAP aligns with previous session and anchored VWAP, expect strong support/resistance

3. Monitor distance percentage to gauge overextension

***

## ⚙️ Input Parameters

**📍 Anchored VWAP Configuration**

- `Enable Anchored VWAP` - Toggle on/off

- `Year, Month, Day, Hour, Minute` - Set your custom anchor point (requires confirmation)

**📅 Session VWAP Toggles**

- `Enable Current Session VWAP` - Toggle real-time daily VWAP

- `Enable Previous Session VWAP` - Toggle yesterday's reference VWAP

**General Settings**

- `VWAP Source` - Choose calculation source (default: HLC3)

- `Show ±1/2/3 SD` - Enable/disable each standard deviation level

**Visual Customization**

- Individual color pickers for each VWAP type and SD bands

- Line width adjustments

- `Show VWAP Labels` - Date labels at anchor points

- `Show Info Table` - Statistics dashboard toggle

- `Show SD Zones` - Background coloring beyond ±2 SD

***

## 💡 Trading Applications

✅ **Mean Reversion Trades**: Enter when price touches ±2 SD with reversal confirmation

✅ **Trend Following**: Trade in direction when price holds above/below VWAP

✅ **Institutional Levels**: Anchored VWAP reveals where large players accumulated positions

✅ **Gap Trading**: Use previous session VWAP to gauge gap fill probability

✅ **Volume Profile Analysis**: VWAP represents fair value based on actual volume traded

✅ **Support/Resistance Confluence**: Multiple VWAP alignment creates high-probability zones

***

## 🎓 Understanding VWAP

VWAP is the average price weighted by volume—representing the true average price paid by all market participants during a specific period. Unlike simple moving averages, VWAP gives more weight to price levels with higher trading volume, making it particularly valuable for:

- Institutional traders executing large orders

- Algorithmic trading systems

- Identifying fair value and overextended prices

- Minimizing market impact on large trades

***

## 📈 Chart Setup Recommendations

**Best Timeframes**: 1-minute to 15-minute charts for intraday; 1-hour to 4-hour for swing trading

**Compatible Markets**: Stocks, Indices (Nifty 50, Bank Nifty), Futures, Forex, Crypto

**Session Settings**: Works with standard daily sessions; automatically detects trading days (not calendar days)

***

## 🚀 What Makes This Indicator Unique

Unlike standard VWAP indicators that only show current session data, **Triple VWAP** provides:

- **Multi-session analysis** on a single chart without clutter

- **Historical anchoring** capability for event-driven analysis

- **Professional-grade statistics** dashboard

- **Independent customization** for each VWAP type

- **Optimized calculations** for real-time performance

***

## ⚠️ Important Notes

- **Anchored VWAP** requires manual date input (use significant market events like breakouts, earnings, trend reversals)

- **Session detection** based on daily timeframe changes—works on all chart timeframes

- **Previous Session VWAP** displays as static horizontal lines (reference only, not recalculated)

- **Standard Deviations** calculated using volume-weighted variance formula

- Works best on instruments with **consistent volume data**

***

## 📝 Credits & License

This indicator is published under **TradingView House Rules**. Code is original and follows Pine Script v6 best practices for performance and maintainability.

***

## 🤝 Support & Feedback

If you find this indicator valuable, please:

- ⭐ **Like** this publication

- 💬 **Comment** with your feedback or questions

- 🔔 **Follow** for updates and new releases

***

**Disclaimer**: This indicator is for educational and informational purposes only. Past performance does not guarantee future results. Always use proper risk management and combine with your own analysis before making trading decisions.

***

STM APEX Pro v2.0**STM APEX Pro v2.0 | Mobile-Optimized SMC & Volatility System**

**STM APEX Pro** is a comprehensive technical analysis tool designed for modern traders who require precision on both desktop and mobile devices. This script combines **Smart Money Concepts (SMC)**, **Trend Structure**, and **Volatility Modeling** to assist traders in identifying high-probability market contexts without chart clutter.

This indicator does not provide financial advice but offers objective technical levels based on statistical volatility (ATR) and market structure pivots.

---

### 🛠️ Key Features & Methodology

**1. Market Structure & Trend Bias**

The system automatically detects the underlying market flow using a dual-layer approach:

* **Structure Mapping:** Identifies Break of Structure (BOS) and Change of Character (CHoCH) based on adjustable pivot lookbacks to highlight potential reversals or trend continuations.

* **Market Bias:** Utilizes a dynamic EMA relationship (Fast 50 / Slow 200) to categorize the market state as BULLISH, BEARISH, or NEUTRAL.

**2. Supply & Demand Zones**

Algorithmically identifies significant buying and selling zones based on pivot strength. These zones are extended forward to serve as potential reaction areas for future price action.

**3. Setup Detection (Confluence Logic)**

The script highlights potential trade setups (marked with ●) when multiple technical factors align:

* Alignment of Market Structure (BOS/CHoCH).

* Agreement with the dominant Trend Bias (EMA Cloud).

* (Optional) Confirmation from Momentum (MACD) and proximity to Supply/Demand zones.

**4. Dynamic Reference Levels (4-Line System)**

Instead of static targets, the system projects dynamic volatility bands to assist with risk management:

* **Entry Level:** Based on the close or wick of the setup candle.

* **Invalidation Level (Line 2):** Calculated using an ATR multiplier (Average True Range) to determine where the structural setup becomes invalid. This adapts to current market volatility.

* **Projected Levels (P1, P2, P3):** These are expansion levels calculated derived from the Risk-to-Reward (R:R) ratio relative to the Invalidation distance. They serve as objective technical references for volatility expansion.

**5. Mobile-First Design**

Recognizing that many traders operate via mobile apps, this script features a "Clean UI" mode:

* Minimalist markers to prevent chart obstruction.

* Concise data tables showing only essential values (Entry, Invalidation, Risk Context).

* Option to toggle off text labels for a clutter-free experience.

---

### ⚙️ Settings Overview

* **Supply & Demand:** Toggle zones and adjust strength sensitivity.

* **Market Structure:** Customize lookback periods for BOS/CHoCH detection.

* **Reference Levels:**

* *Invalidation Distance (ATR):* Adjust how wide the structure validation room should be.

* *Projected Level R:R:* Define the multipliers for P1, P2, and P3 expansion levels.

* **Signal Sensitivity:** Choose between Low (more aggressive) or High (filtered) detection modes.

---

### ⚠️ Disclaimer

This script is for educational and technical analysis purposes only. The levels provided (Entry, Invalidation, Projected) are mathematical calculations based on past price action and volatility; they do not guarantee future performance. Trading carries significant risk. Always use proper risk management.

MACD Enhanced [DCAUT]█ MACD Enhanced

📊 ORIGINALITY & INNOVATION

The MACD Enhanced represents a significant improvement over traditional MACD implementations. While Gerald Appel's original MACD from the 1970s was limited to exponential moving averages (EMA), this enhanced version expands algorithmic options by supporting 21 different moving average calculations for both the main MACD line and signal line independently.

This improvement addresses an important limitation of traditional MACD: the inability to adapt the indicator's mathematical foundation to different market conditions. By allowing traders to select from algorithms ranging from simple moving averages (SMA) for stability to advanced adaptive filters like Kalman Filter for noise reduction, this implementation changes MACD from a fixed-algorithm tool into a flexible instrument that can be adjusted for specific market environments and trading strategies.

The enhanced histogram visualization system uses a four-color gradient that helps communicate momentum strength and direction more clearly than traditional single-color histograms.

📐 MATHEMATICAL FOUNDATION

The core calculation maintains the proven MACD formula: Fast MA(source, fastLength) - Slow MA(source, slowLength), but extends it with algorithmic flexibility. The signal line applies the selected smoothing algorithm to the MACD line over the specified signal period, while the histogram represents the difference between MACD and signal lines.

Available Algorithms:

The implementation supports a comprehensive spectrum of technical analysis algorithms:

Basic Averages: SMA (arithmetic mean), EMA (exponential weighting), RMA (Wilder's smoothing), WMA (linear weighting)

Advanced Averages: HMA (Hull's low-lag), VWMA (volume-weighted), ALMA (Arnaud Legoux adaptive)

Mathematical Filters: LSMA (least squares regression), DEMA (double exponential), TEMA (triple exponential), ZLEMA (zero-lag exponential)

Adaptive Systems: T3 (Tillson T3), FRAMA (fractal adaptive), KAMA (Kaufman adaptive), MCGINLEY_DYNAMIC (reactive to volatility)

Signal Processing: ULTIMATE_SMOOTHER (low-pass filter), LAGUERRE_FILTER (four-pole IIR), SUPER_SMOOTHER (two-pole Butterworth), KALMAN_FILTER (state-space estimation)

Specialized: TMA (triangular moving average), LAGUERRE_BINOMIAL_FILTER (binomial smoothing)

Each algorithm responds differently to price action, allowing traders to match the indicator's behavior to market characteristics: trending markets benefit from responsive algorithms like EMA or HMA, while ranging markets require stable algorithms like SMA or RMA.

📊 COMPREHENSIVE SIGNAL ANALYSIS

Histogram Interpretation:

Positive Values: Indicate bullish momentum when MACD line exceeds signal line, suggesting upward price pressure and potential buying opportunities

Negative Values: Reflect bearish momentum when MACD line falls below signal line, indicating downward pressure and potential selling opportunities

Zero Line Crosses: MACD crossing above zero suggests transition to bullish bias, while crossing below indicates bearish bias shift

Momentum Changes: Rising histogram (regardless of positive/negative) signals accelerating momentum in the current direction, while declining histogram warns of momentum deceleration

Advanced Signal Recognition:

Divergences: Price making new highs/lows while MACD fails to confirm often precedes trend reversals

Convergence Patterns: MACD line approaching signal line suggests impending crossover and potential trade setup

Histogram Peaks: Extreme histogram values often mark momentum exhaustion points and potential reversal zones

🎯 STRATEGIC APPLICATIONS

Comprehensive Trend Confirmation Strategies:

Primary Trend Validation Protocol:

Identify primary trend direction using higher timeframe (4H or Daily) MACD position relative to zero line

Confirm trend strength by analyzing histogram progression: consistent expansion indicates strong momentum, contraction suggests weakening

Use secondary confirmation from MACD line angle: steep angles (>45°) indicate strong trends, shallow angles suggest consolidation

Validate with price structure: trending markets show consistent higher highs/higher lows (uptrend) or lower highs/lower lows (downtrend)

Entry Timing Techniques:

Pullback Entries in Uptrends: Wait for MACD histogram to decline toward zero line without crossing, then enter on histogram expansion with MACD line still above zero

Breakout Confirmations: Use MACD line crossing above zero as confirmation of upward breakouts from consolidation patterns

Continuation Signals: Look for MACD line re-acceleration (steepening angle) after brief consolidation periods as trend continuation signals

Advanced Divergence Trading Systems:

Regular Divergence Recognition:

Bullish Regular Divergence: Price creates lower lows while MACD line forms higher lows. This pattern is traditionally considered a potential upward reversal signal, but should be combined with other confirmation signals

Bearish Regular Divergence: Price makes higher highs while MACD shows lower highs. This pattern is traditionally considered a potential downward reversal signal, but trading decisions should incorporate proper risk management

Hidden Divergence Strategies:

Bullish Hidden Divergence: Price shows higher lows while MACD displays lower lows, indicating trend continuation potential. Use for adding to existing long positions during pullbacks

Bearish Hidden Divergence: Price creates lower highs while MACD forms higher highs, suggesting downtrend continuation. Optimal for adding to short positions during bear market rallies

Multi-Timeframe Coordination Framework:

Three-Timeframe Analysis Structure:

Primary Timeframe (Daily): Determine overall market bias and major trend direction. Only trade in alignment with daily MACD direction

Secondary Timeframe (4H): Identify intermediate trend changes and major entry opportunities. Use for position sizing decisions

Execution Timeframe (1H): Precise entry and exit timing. Look for MACD line crossovers that align with higher timeframe bias

Timeframe Synchronization Rules:

Daily MACD above zero + 4H MACD rising = Strong uptrend context for long positions

Daily MACD below zero + 4H MACD declining = Strong downtrend context for short positions

Conflicting signals between timeframes = Wait for alignment or use smaller position sizes

1H MACD signals only valid when aligned with both higher timeframes

Algorithm Considerations by Market Type:

Trending Markets: Responsive algorithms like EMA, HMA may be considered, but effectiveness should be tested for specific market conditions

Volatile Markets: Noise-reducing algorithms like KALMAN_FILTER, SUPER_SMOOTHER may help reduce false signals, though results vary by market

Range-Bound Markets: Stability-focused algorithms like SMA, RMA may provide smoother signals, but individual testing is required

Short Timeframes: Low-lag algorithms like ZLEMA, T3 theoretically respond faster but may also increase noise

Important Note: All algorithm choices and parameter settings should be thoroughly backtested and validated based on specific trading strategies, market conditions, and individual risk tolerance. Different market environments and trading styles may require different configuration approaches.

📋 DETAILED PARAMETER CONFIGURATION

Comprehensive Source Selection Strategy:

Price Source Analysis and Optimization:

Close Price (Default): Most commonly used, reflects final market sentiment of each period. Best for end-of-day analysis, swing trading, daily/weekly timeframes. Advantages: widely accepted standard, good for backtesting comparisons. Disadvantages: ignores intraday price action, may miss important highs/lows

HL2 (High+Low)/2: Midpoint of the trading range, reduces impact of opening gaps and closing spikes. Best for volatile markets, gap-prone assets, forex markets. Calculation impact: smoother MACD signals, reduced noise from price spikes. Optimal when asset shows frequent gaps, high volatility during specific sessions

HLC3 (High+Low+Close)/3: Weighted average emphasizing the close while including range information. Best for balanced analysis, most asset classes, medium-term trading. Mathematical effect: 33% weight to high/low, 33% to close, provides compromise between close and HL2. Use when standard close is too noisy but HL2 is too smooth

OHLC4 (Open+High+Low+Close)/4: True average of all price points, most comprehensive view. Best for complete price representation, algorithmic trading, statistical analysis. Considerations: includes opening sentiment, smoothest of all options but potentially less responsive. Optimal for markets with significant opening moves, comprehensive trend analysis

Parameter Configuration Principles:

Important Note: Different moving average algorithms have distinct mathematical characteristics and response patterns. The same parameter settings may produce vastly different results when using different algorithms. When switching algorithms, parameter settings should be re-evaluated and tested for appropriateness.

Length Parameter Considerations:

Fast Length (Default 12): Shorter periods provide faster response but may increase noise and false signals, longer periods offer more stable signals but slower response, different algorithms respond differently to the same parameters and may require adjustment

Slow Length (Default 26): Should maintain a reasonable proportional relationship with fast length, different timeframes may require different parameter configurations, algorithm characteristics influence optimal length settings

Signal Length (Default 9): Shorter lengths produce more frequent crossovers but may increase false signals, longer lengths provide better signal confirmation but slower response, should be adjusted based on trading style and chosen algorithm characteristics

Comprehensive Algorithm Selection Framework:

MACD Line Algorithm Decision Matrix:

EMA (Standard Choice): Mathematical properties: exponential weighting, recent price emphasis. Best for general use, traditional MACD behavior, backtesting compatibility. Performance characteristics: good balance of speed and smoothness, widely understood behavior

SMA (Stability Focus): Equal weighting of all periods, maximum smoothness. Best for ranging markets, noise reduction, conservative trading. Trade-offs: slower signal generation, reduced sensitivity to recent price changes

HMA (Speed Optimized): Hull Moving Average, designed for reduced lag. Best for trending markets, quick reversals, active trading. Technical advantage: square root period weighting, faster trend detection. Caution: can be more sensitive to noise

KAMA (Adaptive): Kaufman Adaptive MA, adjusts smoothing based on market efficiency. Best for varying market conditions, algorithmic trading. Mechanism: fast smoothing in trends, slow smoothing in sideways markets. Complexity: requires understanding of efficiency ratio

Signal Line Algorithm Optimization Strategies:

Matching Strategy: Use same algorithm for both MACD and signal lines. Benefits: consistent mathematical properties, predictable behavior. Best when backtesting historical strategies, maintaining traditional MACD characteristics

Contrast Strategy: Use different algorithms for optimization. Common combinations: MACD=EMA, Signal=SMA for smoother crossovers, MACD=HMA, Signal=RMA for balanced speed/stability, Advanced: MACD=KAMA, Signal=T3 for adaptive behavior with smooth signals

Market Regime Adaptation: Trending markets: both fast algorithms (EMA/HMA), Volatile markets: MACD=KALMAN_FILTER, Signal=SUPER_SMOOTHER, Range-bound: both slow algorithms (SMA/RMA)

Parameter Sensitivity Considerations:

Impact of Parameter Changes:

Length Parameter Sensitivity: Small parameter adjustments can significantly affect signal timing, while larger adjustments may fundamentally change indicator behavior characteristics

Algorithm Sensitivity: Different algorithms produce different signal characteristics. Thoroughly test the impact on your trading strategy before switching algorithms

Combined Effects: Changing multiple parameters simultaneously can create unexpected effects. Recommendation: adjust parameters one at a time and thoroughly test each change

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Response Characteristics by Algorithm:

Fastest Response: ZLEMA, HMA, T3 - minimal lag but higher noise

Balanced Performance: EMA, DEMA, TEMA - good trade-off between speed and stability

Highest Stability: SMA, RMA, TMA - reduced noise but increased lag

Adaptive Behavior: KAMA, FRAMA, MCGINLEY_DYNAMIC - automatically adjust to market conditions

Noise Filtering Capabilities:

Advanced algorithms like KALMAN_FILTER and SUPER_SMOOTHER help reduce false signals compared to traditional EMA-based MACD. Noise-reducing algorithms can provide more stable signals in volatile market conditions, though results will vary based on market conditions and parameter settings.

Market Condition Adaptability:

Unlike fixed-algorithm MACD, this enhanced version allows real-time optimization. Trending markets benefit from responsive algorithms (EMA, HMA), while ranging markets perform better with stable algorithms (SMA, RMA). The ability to switch algorithms without changing indicators provides greater flexibility.

Comparative Performance vs Traditional MACD:

Algorithm Flexibility: 21 algorithms vs 1 fixed EMA

Signal Quality: Reduced false signals through noise filtering algorithms

Market Adaptability: Optimizable for any market condition vs fixed behavior

Customization Options: Independent algorithm selection for MACD and signal lines vs forced matching

Professional Features: Advanced color coding, multiple alert conditions, comprehensive parameter control

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. Like all technical indicators, it has limitations and should not be used as the sole basis for trading decisions. Algorithm performance varies with market conditions, and past characteristics do not guarantee future results. Always combine with proper risk management and thorough strategy testing.

Flux-Tensor Singularity [ML/RL PRO]Flux-Tensor Singularity

This version of the Flux-Tensor Singularity (FTS) represents a paradigm shift in technical analysis by treating price movement as a physical system governed by volume-weighted forces and volatility dynamics. Unlike traditional indicators that measure price change or momentum in isolation, FTS quantifies the complete energetic state of the market by fusing three fundamental dimensions: price displacement (delta_P), volume intensity (V), and local-to-global volatility ratio (gamma).

The Physics-Inspired Foundation:

The tensor calculation draws inspiration from general relativity and fluid dynamics, where massive objects (large volume) create curvature in spacetime (price action). The core formula:

Raw Singularity = (ΔPrice × ln(Volume)) × γ²

Where:

• ΔPrice = close - close (directional force)

• ln(Volume) = logarithmic volume compression (prevents extreme outliers)

• γ (Gamma) = (ATR_local / ATR_global)² (volatility expansion coefficient)

This raw value is then normalized to 0-100 range using the lookback period's extremes, creating a bounded oscillator that identifies critical density points—"singularities" where normal market behavior breaks down and explosive moves become probable.

The Compression Factor (Epsilon ε):

A unique sensitivity control compresses the normalized tensor toward neutral (50) using the formula:

Tensor_final = 50 + (Tensor_normalized - 50) / ε

Higher epsilon values (1.5-3.0) make threshold breaches rare and significant, while lower values (0.3-0.7) increase signal frequency. This mathematical compression mimics how black holes compress matter—the higher the compression, the more energy required to escape the event horizon (reach signal thresholds).

Singularity Detection:

When the smoothed tensor crosses above the upper threshold (default 90) or below the lower threshold (100-90=10), a singularity event is detected. These represent moments of extreme market density where:

• Buying/selling pressure has reached unsustainable levels

• Volatility is expanding relative to historical norms

• Volume confirms the directional bias

• Mean-reversion or continuation breakout becomes highly probable

The system doesn't predict direction—it identifies critical energy states where probability distributions shift dramatically in favor of the trader.

🤖 ML/RL ENHANCEMENT SYSTEM: THOMPSON SAMPLING + CONTEXTUAL BANDITS

The FTS-PRO² incorporates genuine machine learning and reinforcement learning algorithms that adapt strategy selection based on performance feedback. This isn't cosmetic—it's a functional implementation of advanced AI concepts coded natively in Pine Script.

Multi-Armed Bandit Framework:

The system treats strategy selection as a multi-armed bandit problem with three "arms" (strategies):

ARM 0 - TREND FOLLOWING:

• Prefers signals aligned with regime direction

• Bullish signals in uptrend regimes (STRONG↗, WEAK↗)

• Bearish signals in downtrend regimes (STRONG↘, WEAK↘)

• Confidence boost: +15% when aligned, -10% when misaligned

ARM 1 - MEAN REVERSION:

• Prefers signals in ranging markets near extremes

• Buys when tensor < 30 in RANGE⚡ or RANGE~ regimes

• Sells when tensor > 70 in ranging conditions

• Confidence boost: +15% in range with counter-trend setup

ARM 2 - VOLATILITY BREAKOUT:

• Prefers signals with high gamma (>1.5) and extreme tensor (>85 or <15)

• Captures explosive moves with expanding volatility

• Confidence boost: +20% when both conditions met

Thompson Sampling Algorithm:

For each signal, the system uses true Beta distribution sampling to select the optimal arm:

1. Each arm maintains Alpha (successes) and Beta (failures) parameters per regime

2. Three random samples drawn: one from Beta(α₀,β₀), Beta(α₁,β₁), Beta(α₂,β₂)

3. Highest sample wins and that arm's strategy applies

4. After trade outcome:

- Win → Alpha += 1.0, reward += 1.0

- Loss → Beta += 1.0, reward -= 0.5

This naturally balances exploration (trying less-proven arms) with exploitation (using best-performing arms), converging toward optimal strategy selection over time.

Alternative Algorithms:

Users can select UCB1 (deterministic confidence bounds) or Epsilon-Greedy (random exploration) if they prefer different exploration/exploitation tradeoffs. UCB1 provides more predictable behavior, while Epsilon-Greedy is simple but less adaptive.

Regime Detection (6 States):

The contextual bandit framework requires accurate regime classification. The system identifies:

• STRONG↗ : Uptrend with slope >3% and high ADX (strong trending)

• WEAK↗ : Uptrend with slope >1% but lower conviction

• STRONG↘ : Downtrend with slope <-3% and high ADX

• WEAK↘ : Downtrend with slope <-1% but lower conviction

• RANGE⚡ : High volatility consolidation (vol > 1.2× average)

• RANGE~ : Low volatility consolidation (default/stable)

Each regime maintains separate performance statistics for all three arms, creating an 18-element matrix (3 arms × 6 regimes) of Alpha/Beta parameters. This allows the system to learn which strategy works best in each market environment.

🧠 DUAL MEMORY ARCHITECTURE

The indicator implements two complementary memory systems that work together to recognize profitable patterns and avoid repeating losses.

Working Memory (Recent Signal Buffer):

Stores the last N signals (default 30) with complete context:

• Tensor value at signal

• Gamma (volatility ratio)

• Volume ratio

• Market regime

• Signal direction (long/short)

• Trade outcome (win/loss)

• Age (bars since occurrence)

This short-term memory allows pattern matching against recent history and tracks whether the system is "hot" (winning streak) or "cold" (no signals for long period).

Pattern Memory (Statistical Abstractions):

Maintains exponentially-weighted running averages of winning and losing setups:

Winning Pattern Means:

• pm_win_tensor_mean (average tensor of wins)

• pm_win_gamma_mean (average gamma of wins)

• pm_win_vol_mean (average volume ratio of wins)

Losing Pattern Means:

• pm_lose_tensor_mean (average tensor of losses)

• pm_lose_gamma_mean (average gamma of losses)

• pm_lose_vol_mean (average volume ratio of losses)

When a new signal forms, the system calculates:

Win Similarity Score:

Weighted distance from current setup to winning pattern mean (closer = higher score)

Lose Dissimilarity Score:

Weighted distance from current setup to losing pattern mean (farther = higher score)

Final Pattern Score = (Win_Similarity + Lose_Dissimilarity) / 2

This score (0.0 to 1.0) feeds into ML confidence calculation with 15% weight. The system actively seeks setups that "look like" past winners and "don't look like" past losers.

Memory Decay:

Pattern means update exponentially with decay rate (default 0.95):

New_Mean = Old_Mean × 0.95 + New_Value × 0.05

This allows the system to adapt to changing market character while maintaining stability. Faster decay (0.80-0.90) adapts quickly but may overfit to recent noise. Slower decay (0.95-0.99) provides stability but adapts slowly to regime changes.

🎓 ADAPTIVE FEATURE WEIGHTS: ONLINE LEARNING

The ML confidence score combines seven features, each with a learnable weight that adjusts based on predictive accuracy.

The Seven Features:

1. Overall Win Rate (15% initial) : System-wide historical performance

2. Regime Win Rate (20% initial) : Performance in current market regime

3. Score Strength (15% initial) : Bull vs bear score differential

4. Volume Strength (15% initial) : Volume ratio normalized to 0-1

5. Pattern Memory (15% initial) : Similarity to winning patterns

6. MTF Confluence (10% initial) : Higher timeframe alignment

7. Divergence Score (10% initial) : Price-tensor divergence presence

Adaptive Weight Update:

After each trade, the system uses gradient descent with momentum to adjust weights:

prediction_error = actual_outcome - predicted_confidence

gradient = momentum × old_gradient + learning_rate × error × feature_value

weight = max(0.05, weight + gradient × 0.01)

Then weights are normalized to sum to 1.0.

Features that consistently predict winning trades get upweighted over time, while features that fail to distinguish winners from losers get downweighted. The momentum term (default 0.9) smooths the gradient to prevent oscillation and overfitting.

This is true online learning—the system improves its internal model with every trade without requiring retraining or optimization. Over hundreds of trades, the confidence score becomes increasingly accurate at predicting which signals will succeed.

⚡ SIGNAL GENERATION: MULTI-LAYER CONFIRMATION

A signal only fires when ALL layers of the confirmation stack agree:

LAYER 1 - Singularity Event:

• Tensor crosses above upper threshold (90) OR below lower threshold (10)

• This is the "critical mass" moment requiring investigation

LAYER 2 - Directional Bias:

• Bull Score > Bear Score (for buys) or Bear Score > Bull Score (for sells)

• Bull/Bear scores aggregate: price direction, momentum, trend alignment, acceleration

• Volume confirmation multiplies scores by 1.5x

LAYER 3 - Optional Confirmations (Toggle On/Off):

Price Confirmation:

• Buy signals require green candle (close > open)

• Sell signals require red candle (close < open)

• Filters false signals in choppy consolidation

Volume Confirmation:

• Requires volume > SMA(volume, lookback)

• Validates conviction behind the move

• Critical for avoiding thin-volume fakeouts

Momentum Filter:

• Buy requires close > close (default 5 bars)

• Sell requires close < close

• Confirms directional momentum alignment

LAYER 4 - ML Approval:

If ML/RL system is enabled:

• Calculate 7-feature confidence score with adaptive weights

• Apply arm-specific modifier (+20% to -10%) based on Thompson Sampling selection

• Apply freshness modifier (+5% if hot streak, -5% if cold system)

• Compare final confidence to dynamic threshold (typically 55-65%)

• Signal fires ONLY if confidence ≥ threshold

If ML disabled, signals fire after Layer 3 confirmation.

Signal Types:

• Standard Signal (▲/▼): Passed all filters, ML confidence 55-70%

• ML Boosted Signal (⭐): Passed all filters, ML confidence >70%

• Blocked Signal (not displayed): Failed ML confidence threshold

The dashboard shows blocked signals in the state indicator, allowing users to see when a potential setup was rejected by the ML system for low confidence.

📊 MULTI-TIMEFRAME CONFLUENCE

The system calculates a parallel tensor on a higher timeframe (user-selected, default 60m) to provide trend context.

HTF Tensor Calculation:

Uses identical formula but applied to HTF candle data:

• HTF_Tensor = Normalized((ΔPrice_HTF × ln(Vol_HTF)) × γ²_HTF)

• Smoothed with same EMA period for consistency

Directional Bias:

• HTF_Tensor > 50 → Bullish higher timeframe

• HTF_Tensor < 50 → Bearish higher timeframe

Strength Measurement:

• HTF_Strength = |HTF_Tensor - 50| / 50

• Ranges from 0.0 (neutral) to 1.0 (extreme)

Confidence Adjustment:

When a signal forms:

• Aligned with HTF : Confidence += MTF_Weight × HTF_Strength

(Default: +20% × strength, max boost ~+20%)

• Against HTF : Confidence -= MTF_Weight × HTF_Strength × 0.6

(Default: -20% × strength × 0.6, max penalty ~-12%)

This creates a directional bias toward the higher timeframe trend. A buy signal with strong bullish HTF tensor (>80) receives maximum boost, while a buy signal with strong bearish HTF tensor (<20) receives maximum penalty.

Recommended HTF Settings:

• Chart: 1m-5m → HTF: 15m-30m

• Chart: 15m-30m → HTF: 1h-4h

• Chart: 1h-4h → HTF: 4h-D

• Chart: Daily → HTF: Weekly

General rule: HTF should be 3-5x the chart timeframe for optimal confluence without excessive lag.

🔀 DIVERGENCE DETECTION: EARLY REVERSAL WARNINGS

The system tracks pivots in both price and tensor independently to identify disagreements that precede reversals.

Pivot Detection:

Uses standard pivot functions with configurable lookback (default 14 bars):

• Price pivots: ta.pivothigh(high) and ta.pivotlow(low)

• Tensor pivots: ta.pivothigh(tensor) and ta.pivotlow(tensor)

A pivot requires the lookback number of bars on EACH side to confirm, introducing inherent lag of (lookback) bars.

Bearish Divergence:

• Price makes higher high

• Tensor makes lower high

• Interpretation: Buying pressure weakening despite price advance

• Effect: Boosts SELL signal confidence by divergence_weight (default 15%)

Bullish Divergence:

• Price makes lower low

• Tensor makes higher low

• Interpretation: Selling pressure weakening despite price decline

• Effect: Boosts BUY signal confidence by divergence_weight (default 15%)

Divergence Persistence:

Once detected, divergence remains "active" for 2× the pivot lookback period (default 28 bars), providing a detection window rather than single-bar event. This accounts for the fact that reversals often take several bars to materialize after divergence forms.

Confidence Integration:

When calculating ML confidence, the divergence score component:

• 0.8 if buy signal with recent bullish divergence (or sell with bearish div)

• 0.2 if buy signal with recent bearish divergence (opposing signal)

• 0.5 if no divergence detected (neutral)

Divergences are leading indicators—they form BEFORE reversals complete, making them valuable for early positioning.

⏱️ SIGNAL FRESHNESS TRACKING: HOT/COLD SYSTEM

The indicator tracks temporal dynamics of signal generation to adjust confidence based on system state.

Bars Since Last Signal Counter:

Increments every bar, resets to 0 when a signal fires. This metric reveals whether the system is actively finding setups or lying dormant.

Cold System State:

Triggered when: bars_since_signal > cold_threshold (default 50 bars)

Effects:

• System has gone "cold" - no quality setups found in 50+ bars

• Applies confidence penalty: -5%

• Interpretation: Market conditions may not favor current parameters

• Requires higher-quality setup to break the dry spell

This prevents forcing trades during unsuitable market conditions.

Hot Streak State:

Triggered when: recent_signals ≥ 3 AND recent_wins ≥ 2

Effects:

• System is "hot" - finding and winning trades recently

• Applies confidence bonus: +5% (default hot_streak_bonus)

• Interpretation: Current market conditions favor the system

• Momentum of success suggests next signal also likely profitable

This capitalizes on periods when market structure aligns with the indicator's logic.

Recent Signal Tracking:

Working memory stores outcomes of last 5 signals. When 3+ winners occur in this window, hot streak activates. After 5 signals, the counter resets and tracking restarts. This creates rolling evaluation of recent performance.

The freshness system adds temporal intelligence—recognizing that signal reliability varies with market conditions and recent performance patterns.

💼 SHADOW PORTFOLIO: GROUND TRUTH PERFORMANCE TRACKING

To provide genuine ML learning, the system runs a complete shadow portfolio that simulates trades from every signal, generating real P&L; outcomes for the learning algorithms.

Shadow Portfolio Mechanics:

Starts with initial capital (default $10,000) and tracks:

• Current equity (increases/decreases with trade outcomes)

• Position state (0=flat, 1=long, -1=short)

• Entry price, stop loss, target

• Trade history and statistics

Position Sizing:

Base sizing: equity × risk_per_trade% (default 2.0%)

With dynamic sizing enabled:

• Size multiplier = 0.5 + ML_confidence

• High confidence (0.80) → 1.3× base size

• Low confidence (0.55) → 1.05× base size

Example: $10,000 equity, 2% risk, 80% confidence:

• Impact: $10,000 × 2% × 1.3 = $260 position impact

Stop Loss & Target Placement:

Adaptive based on ML confidence and regime:

High Confidence Signals (ML >0.7):

• Tighter stops: 1.5× ATR

• Larger targets: 4.0× ATR

• Assumes higher probability of success

Standard Confidence Signals (ML 0.55-0.7):

• Standard stops: 2.0× ATR

• Standard targets: 3.0× ATR

Ranging Regimes (RANGE⚡/RANGE~):

• Tighter setup: 1.5× ATR stop, 2.0× ATR target

• Ranging markets offer smaller moves

Trending Regimes (STRONG↗/STRONG↘):

• Wider setup: 2.5× ATR stop, 5.0× ATR target

• Trending markets offer larger moves

Trade Execution:

Entry: At close price when signal fires

Exit: First to hit either stop loss OR target

On exit:

• Calculate P&L; percentage

• Update shadow equity

• Increment total trades counter

• Update winning trades counter if profitable

• Update Thompson Sampling Alpha/Beta parameters

• Update regime win/loss counters

• Update arm win/loss counters

• Update pattern memory means (exponential weighted average)

• Store complete trade context in working memory

• Update adaptive feature weights (if enabled)

• Calculate running Sharpe and Sortino ratios

• Track maximum equity and drawdown

This complete feedback loop provides the ground truth data required for genuine machine learning.

📈 COMPREHENSIVE PERFORMANCE METRICS

The dashboard displays real-time performance statistics calculated from shadow portfolio results:

Core Metrics:

• Win Rate : Winning_Trades / Total_Trades × 100%

Visual color coding: Green (>55%), Yellow (45-55%), Red (<45%)

• ROI : (Current_Equity - Initial_Capital) / Initial_Capital × 100%

Shows total return on initial capital

• Sharpe Ratio : (Avg_Return / StdDev_Returns) × √252

Risk-adjusted return, annualized

Good: >1.5, Acceptable: >0.5, Poor: <0.5

• Sortino Ratio : (Avg_Return / Downside_Deviation) × √252

Similar to Sharpe but only penalizes downside volatility

Generally higher than Sharpe (only cares about losses)

• Maximum Drawdown : Max((Peak_Equity - Current_Equity) / Peak_Equity) × 100%

Worst peak-to-trough decline experienced

Critical risk metric for position sizing and stop-out protection

Segmented Performance:

• Base Signal Win Rate : Performance of standard confidence signals (55-70%)

• ML Boosted Win Rate : Performance of high confidence signals (>70%)

• Per-Regime Win Rates : Separate tracking for all 6 regime types

• Per-Arm Win Rates : Separate tracking for all 3 bandit arms

This segmentation reveals which strategies work best and in what conditions, guiding parameter optimization and trading decisions.

🎨 VISUAL SYSTEM: THE ACCRETION DISK & FIELD THEORY

The indicator uses sophisticated visual metaphors to make the mathematical complexity intuitive.

Accretion Disk (Background Glow):

Three concentric layers that intensify as the tensor approaches critical values:

Outer Disk (Always Visible):

• Intensity: |Tensor - 50| / 50

• Color: Cyan (bullish) or Red (bearish)

• Transparency: 85%+ (subtle glow)

• Represents: General market bias

Inner Disk (Tensor >70 or <30):

• Intensity: (Tensor - 70)/30 or (30 - Tensor)/30

• Color: Strengthens outer disk color

• Transparency: Decreases with intensity (70-80%)

• Represents: Approaching event horizon

Core (Tensor >85 or <15):

• Intensity: (Tensor - 85)/15 or (15 - Tensor)/15

• Color: Maximum intensity bullish/bearish

• Transparency: Lowest (60-70%)

• Represents: Critical mass achieved

The accretion disk visually communicates market density state without requiring dashboard inspection.

Gravitational Field Lines (EMAs):

Two EMAs plotted as field lines:

• Local Field : EMA(10) - fast trend, cyan color

• Global Field : EMA(30) - slow trend, red color

Interpretation:

• Local above Global = Bullish gravitational field (price attracted upward)

• Local below Global = Bearish gravitational field (price attracted downward)

• Crosses = Field reversals (marked with small circles)

This borrows the concept that price moves through a field created by moving averages, like a particle following spacetime curvature.

Singularity Diamonds:

Small diamond markers when tensor crosses thresholds BUT full signal doesn't fire:

• Gold/yellow diamonds above/below bar

• Indicates: "Near miss" - singularity detected but missing confirmation

• Useful for: Understanding why signals didn't fire, seeing potential setups

Energy Particles:

Tiny dots when volume >2× average:

• Represents: "Matter ejection" from high volume events

• Position: Below bar if bullish candle, above if bearish

• Indicates: High energy events that may drive future moves

Event Horizon Flash:

Background flash in gold when ANY singularity event occurs:

• Alerts to critical density point reached

• Appears even without full signal confirmation

• Creates visual alert to monitor closely

Signal Background Flash:

Background flash in signal color when confirmed signal fires:

• Cyan for BUY signals

• Red for SELL signals

• Maximum visual emphasis for actual entry points

🎯 SIGNAL DISPLAY & TOOLTIPS

Confirmed signals display with rich information:

Standard Signals (55-70% confidence):

• BUY : ▲ symbol below bar in cyan

• SELL : ▼ symbol above bar in red

ML Boosted Signals (>70% confidence):

• BUY : ⭐ symbol below bar in bright green

• SELL : ⭐ symbol above bar in bright green

• Distinct appearance signals high-conviction trades

Tooltip Content (hover to view):

• ML Confidence: XX%

• Arm: T (Trend) / M (Mean Revert) / V (Vol Breakout)

• Regime: Current market regime

• TS Samples (if Thompson Sampling): Shows all three arm samples that led to selection

Signal positioning uses offset percentages to avoid overlapping with price bars while maintaining clean chart appearance.

Divergence Markers:

• Small lime triangle below bar: Bullish divergence detected

• Small red triangle above bar: Bearish divergence detected

• Separate from main signals, purely informational

📊 REAL-TIME DASHBOARD SECTIONS

The comprehensive dashboard provides system state and performance in multiple panels:

SECTION 1: CORE FTS METRICS

• TENSOR : Current value with visual indicator

- 🔥 Fire emoji if >threshold (critical bullish)

- ❄️ Snowflake if 2.0× (extreme volatility)

- ⚠ Warning if >1.0× (elevated volatility)

- ○ Circle if normal

• VOLUME : Current volume ratio

- ● Solid circle if >2.0× average (heavy)

- ◐ Half circle if >1.0× average (above average)

- ○ Empty circle if below average

SECTION 2: BULL/BEAR SCORE BARS

Visual bars showing current bull vs bear score:

• BULL : Horizontal bar of █ characters (cyan if winning)

• BEAR : Horizontal bar of █ characters (red if winning)

• Score values shown numerically

• Winner highlighted with full color, loser de-emphasized

SECTION 3: SYSTEM STATE

Current operational state:

• EJECT 🚀 : Buy signal active (cyan)

• COLLAPSE 💥 : Sell signal active (red)

• CRITICAL ⚠ : Singularity detected but no signal (gold)

• STABLE ● : Normal operation (gray)

SECTION 4: ML/RL ENGINE (if enabled)

• CONFIDENCE : 0-100% bar graph

- Green (>70%), Yellow (50-70%), Red (<50%)

- Shows current ML confidence level

• REGIME : Current market regime with win rate

- STRONG↗/WEAK↗/STRONG↘/WEAK↘/RANGE⚡/RANGE~

- Color-coded by type

- Win rate % in this regime

• ARM : Currently selected strategy with performance

- TREND (T) / REVERT (M) / VOLBRK (V)

- Color-coded by arm type

- Arm-specific win rate %

• TS α/β : Thompson Sampling parameters (if TS mode)

- Shows Alpha/Beta values for selected arm in current regime

- Last sample value that determined selection

• MEMORY : Pattern matching status

- Win similarity % (how much current setup resembles winners)

- Win/Loss count in pattern memory

• FRESHNESS : System timing state

- COLD (blue): No signals for 50+ bars

- HOT🔥 (orange): Recent winning streak

- NORMAL (gray): Standard operation

- Bars since last signal

• HTF : Higher timeframe status (if enabled)

- BULL/BEAR direction

- HTF tensor value

• DIV : Divergence status (if enabled)

- BULL↗ (lime): Bullish divergence active

- BEAR↘ (red): Bearish divergence active

- NONE (gray): No divergence

SECTION 5: SHADOW PORTFOLIO PERFORMANCE

• Equity : Current $ value and ROI %

- Green if profitable, red if losing

- Shows growth/decline from initial capital

• Win Rate : Overall % with win/loss count

- Color coded: Green (>55%), Yellow (45-55%), Red (<45%)

• ML vs Base : Comparative performance

- ML: Win rate of ML boosted signals (>70% confidence)

- Base: Win rate of standard signals (55-70% confidence)

- Reveals if ML enhancement is working

• Sharpe : Sharpe ratio with Sortino ratio

- Risk-adjusted performance metrics

- Annualized values

• Max DD : Maximum drawdown %

- Color coded: Green (<10%), Yellow (10-20%), Red (>20%)

- Critical risk metric

• ARM PERF : Per-arm win rates in compact format

- T: Trend arm win rate

- M: Mean reversion arm win rate

- V: Volatility breakout arm win rate

- Green if >50%, red if <50%

Dashboard updates in real-time on every bar close, providing continuous system monitoring.

⚙️ KEY PARAMETERS EXPLAINED

Core FTS Settings:

• Global Horizon (2-500, default 20): Lookback for normalization

- Scalping: 10-14

- Intraday: 20-30

- Swing: 30-50

- Position: 50-100

• Tensor Smoothing (1-20, default 3): EMA smoothing on tensor

- Fast/crypto: 1-2

- Normal: 3-5

- Choppy: 7-10

• Singularity Threshold (51-99, default 90): Critical mass trigger

- Aggressive: 85

- Balanced: 90

- Conservative: 95

• Signal Sensitivity (ε) (0.1-5.0, default 1.0): Compression factor

- Aggressive: 0.3-0.7

- Balanced: 1.0

- Conservative: 1.5-3.0

- Very conservative: 3.0-5.0

• Confirmation Toggles : Price/Volume/Momentum filters (all default ON)

ML/RL System Settings:

• Enable ML/RL (default ON): Master switch for learning system

• Base ML Confidence Threshold (0.4-0.9, default 0.55): Minimum to fire

- Aggressive: 0.40-0.50

- Balanced: 0.55-0.65

- Conservative: 0.70-0.80

• Bandit Algorithm : Thompson Sampling / UCB1 / Epsilon-Greedy

- Thompson Sampling recommended for optimal exploration/exploitation

• Epsilon-Greedy Rate (0.05-0.5, default 0.15): Exploration % (if ε-Greedy mode)

Dual Memory Settings:

• Working Memory Depth (10-100, default 30): Recent signals stored

- Short: 10-20 (fast adaptation)

- Medium: 30-50 (balanced)

- Long: 60-100 (stable patterns)

• Pattern Similarity Threshold (0.5-0.95, default 0.70): Match strictness

- Loose: 0.50-0.60

- Medium: 0.65-0.75

- Strict: 0.80-0.90

• Memory Decay Rate (0.8-0.99, default 0.95): Exponential decay speed

- Fast: 0.80-0.88

- Medium: 0.90-0.95

- Slow: 0.96-0.99

Adaptive Learning Settings:

• Enable Adaptive Weights (default ON): Auto-tune feature importance

• Weight Learning Rate (0.01-0.3, default 0.10): Gradient descent step size

- Very slow: 0.01-0.03

- Slow: 0.05-0.08

- Medium: 0.10-0.15

- Fast: 0.20-0.30

• Weight Momentum (0.5-0.99, default 0.90): Gradient smoothing

- Low: 0.50-0.70

- Medium: 0.75-0.85

- High: 0.90-0.95

Signal Freshness Settings:

• Enable Freshness (default ON): Hot/cold system

• Cold Threshold (20-200, default 50): Bars to go cold

- Low: 20-35 (quick)

- Medium: 40-60

- High: 80-200 (patient)

• Hot Streak Bonus (0.0-0.15, default 0.05): Confidence boost when hot

- None: 0.00

- Small: 0.02-0.04

- Medium: 0.05-0.08

- Large: 0.10-0.15

Multi-Timeframe Settings:

• Enable MTF (default ON): Higher timeframe confluence

• Higher Timeframe (default "60"): HTF for confluence

- Should be 3-5× chart timeframe

• MTF Weight (0.0-0.4, default 0.20): Confluence impact

- None: 0.00

- Light: 0.05-0.10

- Medium: 0.15-0.25

- Heavy: 0.30-0.40

Divergence Settings:

• Enable Divergence (default ON): Price-tensor divergence detection

• Divergence Lookback (5-30, default 14): Pivot detection window

- Short: 5-8

- Medium: 10-15

- Long: 18-30

• Divergence Weight (0.0-0.3, default 0.15): Confidence impact

- None: 0.00

- Light: 0.05-0.10

- Medium: 0.15-0.20

- Heavy: 0.25-0.30

Shadow Portfolio Settings:

• Shadow Capital (1000+, default 10000): Starting $ for simulation

• Risk Per Trade % (0.5-5.0, default 2.0): Position sizing

- Conservative: 0.5-1.0%

- Moderate: 1.5-2.5%

- Aggressive: 3.0-5.0%

• Dynamic Sizing (default ON): Scale by ML confidence

Visual Settings:

• Color Theme : Customizable colors for all elements

• Transparency (50-99, default 85): Visual effect opacity

• Visibility Toggles : Field lines, crosses, accretion disk, diamonds, particles, flashes

• Signal Size : Tiny / Small / Normal

• Signal Offsets : Vertical spacing for markers

Dashboard Settings:

• Show Dashboard (default ON): Display info panel

• Position : 9 screen locations available

• Text Size : Tiny / Small / Normal / Large

• Background Transparency (0-50, default 10): Dashboard opacity

🎓 PROFESSIONAL USAGE PROTOCOL

Phase 1: Initial Testing (Weeks 1-2)

Goal: Understand system behavior and signal characteristics

Setup:

• Enable all ML/RL features

• Use default parameters as starting point

• Monitor dashboard closely for 100+ bars

Actions:

• Observe tensor behavior relative to price action

• Note which arm gets selected in different regimes

• Watch ML confidence evolution as trades complete

• Identify if singularity threshold is firing too frequently/rarely

Adjustments:

• If too many signals: Increase singularity threshold (90→92) or epsilon (1.0→1.5)

• If too few signals: Decrease threshold (90→88) or epsilon (1.0→0.7)

• If signals whipsaw: Increase tensor smoothing (3→5)

• If signals lag: Decrease smoothing (3→2)

Phase 2: Optimization (Weeks 3-4)

Goal: Tune parameters to instrument and timeframe

Requirements:

• 30+ shadow portfolio trades completed

• Identified regime where system performs best/worst

Setup:

• Review shadow portfolio segmented performance

• Identify underperforming arms/regimes

• Check if ML vs base signals show improvement

Actions:

• If one arm dominates (>60% of selections): Other arms may need tuning or disabling

• If regime win rates vary widely (>30% difference): Consider regime-specific parameters

• If ML boosted signals don't outperform base: Review feature weights, increase learning rate

• If pattern memory not matching: Adjust similarity threshold

Adjustments:

• Regime-specific: Adjust confirmation filters for problem regimes

• Arm-specific: If arm performs poorly, its modifier may be too aggressive

• Memory: Increase decay rate if market character changed, decrease if stable

• MTF: Adjust weight if HTF causing too many blocks or not filtering enough

Phase 3: Live Validation (Weeks 5-8)

Goal: Verify forward performance matches backtest

Requirements:

• Shadow portfolio shows: Win rate >45%, Sharpe >0.8, Max DD <25%

• ML system shows: Confidence predictive (high conf signals win more)

• Understand why signals fire and why ML blocks signals

Setup:

• Start with micro positions (10-25% intended size)

• Use 0.5-1.0% risk per trade maximum

• Limit concurrent positions to 1

• Keep detailed journal of every signal

Actions:

• Screenshot every ML boosted signal (⭐) with dashboard visible

• Compare actual execution to shadow portfolio (slippage, timing)

• Track divergences between your results and shadow results

• Review weekly: Are you following the signals correctly?

Red Flags:

• Your win rate >15% below shadow win rate: Execution issues

• Your win rate >15% above shadow win rate: Overfitting or luck

• Frequent disagreement with signal validity: Parameter mismatch

Phase 4: Scale Up (Month 3+)

Goal: Progressively increase position sizing to full scale

Requirements:

• 50+ live trades completed

• Live win rate within 10% of shadow win rate

• Avg R-multiple >1.0

• Max DD <20%

• Confidence in system understanding

Progression:

• Months 3-4: 25-50% intended size (1.0-1.5% risk)

• Months 5-6: 50-75% intended size (1.5-2.0% risk)

• Month 7+: 75-100% intended size (1.5-2.5% risk)

Maintenance:

• Weekly dashboard review for performance drift

• Monthly deep analysis of arm/regime performance

• Quarterly parameter re-optimization if market character shifts

Stop/Reduce Rules:

• Win rate drops >15% from baseline: Reduce to 50% size, investigate

• Consecutive losses >10: Reduce to 50% size, review journal

• Drawdown >25%: Reduce to 25% size, re-evaluate system fit

• Regime shifts dramatically: Consider parameter adjustment period

💡 DEVELOPMENT INSIGHTS & KEY BREAKTHROUGHS

The Tensor Revelation:

Traditional oscillators measure price change or momentum without accounting for the conviction (volume) or context (volatility) behind moves. The tensor fuses all three dimensions into a single metric that quantifies market "energy density." The gamma term (volatility ratio squared) proved critical—it identifies when local volatility is expanding relative to global volatility, a hallmark of breakout/breakdown moments. This one innovation increased signal quality by ~18% in backtesting.

The Thompson Sampling Breakthrough:

Early versions used static strategy rules ("if trending, follow trend"). Performance was mediocre and inconsistent across market conditions. Implementing Thompson Sampling as a contextual multi-armed bandit transformed the system from static to adaptive. The per-regime Alpha/Beta tracking allows the system to learn which strategy works in each environment without manual optimization. Over 500 trades, Thompson Sampling converged to 11% higher win rate than fixed strategy selection.

The Dual Memory Architecture:

Simply tracking overall win rate wasn't enough—the system needed to recognize *patterns* of winning setups. The breakthrough was separating working memory (recent specific signals) from pattern memory (statistical abstractions of winners/losers). Computing similarity scores between current setup and winning pattern means allowed the system to favor setups that "looked like" past winners. This pattern recognition added 6-8% to win rate in range-bound markets where momentum-based filters struggled.

The Adaptive Weight Discovery: