Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

ATR

UT Bot + LinReg Candles (Dual Sensitivity)

Script Description:

This indicator combines the popular UT Bot Alerts system with Linear Regression Candles (open source) for enhanced trend detection and trading signals in one singel script. The UT Bot features independent, then 2 x ATR sensitivity and periods controls for buy and sell signals, allowing you to fine-tune entries and exits to match your strategy. The script also overlays colored Linear Regression Candles with an optional signal line, helping you visually identify trend strength and direction. All calculations are performed on standard chart prices (no Heikin Ashi). Suitable for all asset classes and timeframes.

Eample setting for usdjpy 5 min chart for repeated buy and sell singnals based on trend:

BUY ATR period 300 multiplier 1

SELL ATR period 1 multiplier 2

Disclaimer:

This script is for informational and educational purposes only. It is not financial advice. Use at your own risk; the author assumes no responsibility for any trading results or losses.

Credits goes to to Ugurvu for linreg candles and quantnomad for UT Bot alerts that make this script possible.

Author: Patrick

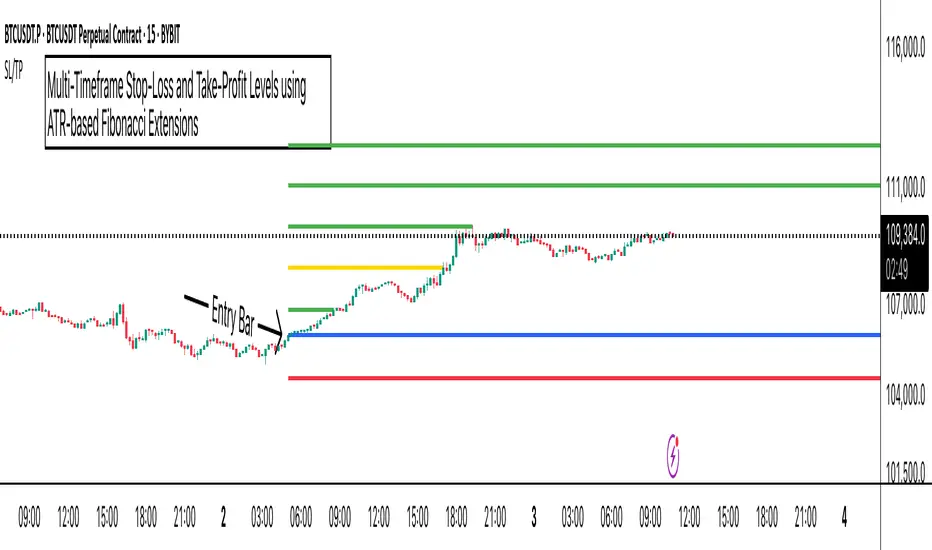

ATR Stop-Loss with Fibonacci Take-Profit [jpkxyz]ATR Stop-Loss with Fibonacci Take-Profit Indicator

This comprehensive indicator combines Average True Range (ATR) volatility analysis with Fibonacci extensions to create dynamic stop-loss and take-profit levels. It's designed to help traders set precise risk management levels and profit targets based on market volatility and mathematical ratios.

Two Operating Modes

Default Mode (Rolling Levels)

In default mode, the indicator continuously plots evolving stop-loss and take-profit levels based on real-time price action. These levels update dynamically as new bars form, creating rolling horizontal lines across the chart. I use this mode primarily to plot the rolling ATR-Level which I use to trail my Stop-Loss into profit.

Characteristics:

Levels recalculate with each new bar

All selected Fibonacci levels display simultaneously

Uses plot() functions with trackprice=true for price tracking

Custom Anchor Mode (Fixed Levels)

This is the primary mode for precision trading. You select a specific timestamp (typically your entry bar), and the indicator locks all calculations to that exact moment, creating fixed horizontal lines that represent your actual trade levels.

Characteristics:

Entry line (blue) marks your anchor point

Stop-loss calculated using ATR from the anchor bar

Fibonacci levels projected from entry-to-stop distance

Lines terminate when price breaks through them

Includes comprehensive alert system

Core Calculation Logic

ATR Stop-Loss Calculation:

Stop Loss = Entry Price ± (ATR × Multiplier)

Long positions: SL = Entry - (ATR × Multiplier)

Short positions: SL = Entry + (ATR × Multiplier)

ATR uses your chosen smoothing method (RMA, SMA, EMA, or WMA)

Default multiplier is 1.5, adjustable to your risk tolerance

Fibonacci Take-Profit Projection:

The distance from entry to stop-loss becomes the base unit (1.0) for Fibonacci extensions:

TP Level = Entry + (Entry-to-SL Distance × Fibonacci Ratio)

Available Fibonacci Levels:

Conservative: 0.618, 1.0, 1.618

Extended: 2.618, 3.618, 4.618

Complete range: 0.0 to 4.764 (23 levels total)

Multi-Timeframe Functionality

One of the indicator's most powerful features is timeframe flexibility. You can analyze on one timeframe while using stop-loss and take-profit calculations from another.

Best Practices:

Identify your entry point on execution timeframe

Enable "Custom Anchor" mode

Set anchor timestamp to your entry bar

Select appropriate analysis timeframe

Choose relevant Fibonacci levels

Enable alerts for automated notifications

Example Scenario:

Analyse trend on 4-hour chart

Execute entry on 5-minute chart for precision

Set custom anchor to your 5-minute entry bar

Configure timeframe setting to "4h" for swing-level targets

Select appropriate Fibonacci Extension levels

Result: Precise entry with larger timeframe risk management

Visual Intelligence System

Line Behaviour in Custom Anchor Mode:

Active levels: Lines extend to the right edge

Hit levels: Lines terminate at the breaking bar

Entry line: Always visible in blue

Stop-loss: Red line, terminates when hit

Take-profits: Green lines (1.618 level in gold for emphasis)

Customisation Options:

Line width (1-4 pixels)

Show/hide individual Fibonacci levels

ATR length and smoothing method

ATR multiplier for stop-loss distance

ATR Buy, Target, Stop + OverlayATR Buy, Target, Stop + Overlay

This tool is to assist traders with precise trade planning using the Average True Range (ATR) as a volatility-based reference.

This script plots buy, target, and stop-loss levels on the chart based on a user-defined buy price and ATR-based multipliers, allowing for objective and adaptive trade management.

*NOTE* In order for the indicator to initiate plotted lines and table values a non-zero number must be entered into the settings.

What It Does:

Buy Price Input: Users enter a manual buy price (e.g., an executed or planned trade entry).

ATR-Based Target and Stop: The script calculates:

Target Price = Buy + (ATR × Target Multiplier)

Stop Price = Buy − (ATR × Stop Multiplier)

Customizable Timeframe: Optionally override the ATR timeframe (e.g., use daily ATR on a 1-hour chart).

Visual Overlay: Lines are drawn directly on the price chart for the Buy, Target, and Stop levels.

Interactive Table: A table is displayed with relevant levels and ATR info.

Customization Options:

Line Settings:

Adjust color, style (solid/dashed/dotted), and width for Buy, Target, and Stop lines.

Choose whether to extend lines rightward only or in both directions.

Table Settings:

Choose position (top/bottom, left/right).

Toggle individual rows for Buy, Target, Stop, ATR Timeframe, and ATR Value.

Customize text color and background transparency.

How to Use It for Trading:

Plan Your Trade: Enter your intended buy price when planning a trade.

Assess Risk/Reward: The script immediately visualizes the potential stop-loss and target level, helping assess R:R ratios.

Adapt to Volatility: Use ATR-based levels to scale stop and target dynamically depending on current market volatility.

Higher Timeframe ATR: Select a different timeframe for the ATR calculation to smooth noise on lower timeframe charts.

On-the-Chart Reference: Visually track trade zones directly on the price chart—ideal for live trading or strategy backtesting.

Ideal For:

Swing traders and intraday traders

Risk management and trade planning

Traders using ATR-based exits or scaling

Visualizing asymmetric risk/reward setups

How I Use This:

After entering a trade, adding an entry price will plot desired ATR target and stop level for visualization.

Adjusting ATR multiplier values assists in evaluating and planning trades.

Visualization assists in comparing ATR multiples to recent support and resistance levels.

Normalized Volume & True RangeThis indicator solves a fundamental challenge that traders face when trying to analyze volume and volatility together on their charts. Traditionally, volume and price volatility exist on completely different scales, making direct comparison nearly impossible. Volume might range from thousands to millions of shares, while volatility percentages typically stay within single digits. This indicator brings both measurements onto a unified scale from 0 to 100 percent, allowing you to see their relationship clearly for the first time.

The core innovation lies in the normalization process, which automatically calculates appropriate scaling factors for both volume and volatility based on their historical statistical properties. Rather than using arbitrary fixed scales that might work for one stock but fail for another, this system adapts to each instrument's unique characteristics. The indicator establishes baseline averages for both measurements and then uses statistical analysis to determine reasonable maximum values, ensuring that extreme outliers don't distort the overall picture.

You can choose from three different volatility calculation methods depending on your analytical preferences. The "Body" option measures the distance between opening and closing prices, focusing on the actual trading range that matters most for price action. The "High/Low" method captures the full daily range including wicks and shadows, giving you a complete picture of intraday volatility. The "Close/Close" approach compares consecutive closing prices, which can be particularly useful for identifying gaps and overnight price movements.

The indicator displays volume as colored columns that match your candlestick colors, making it intuitive to see whether high volume occurred during up moves or down moves. Volatility appears as a gray histogram, providing a clean background reference that doesn't interfere with volume interpretation. Both measurements are clipped at 100 percent, which represents their calculated maximum normal values, so any readings near this level indicate unusually high activity in either volume or volatility.

The baseline reference line shows you what "normal" volume looks like for the current instrument, helping you quickly identify when trading activity is above or below average. Optional moving averages for both volume and volatility are available if you prefer smoothed trend analysis over raw daily values. The entire system updates in real-time as new data arrives, continuously refining its statistical calculations to maintain accuracy as market conditions evolve.

This two-in-one indicator provides a straightforward way to examine how price movements relate to trading volume by presenting both measurements on the same normalized scale, making it easier to spot patterns and relationships that might otherwise remain hidden when analyzing these metrics separately.

ATR RopeATR Rope is inspired by DonovanWall's "Range Filter". It implements a similar concept of filtering out smaller market movements and adjusting only for larger moves. In addition, this indicator goes one step deeper by producing actionable zones to determine market state. (Trend vs. Consolidation)

> Background

When reading up on the Range Filter indicator, it reminded me exactly of a Rope stabilization drawing tool in a program I use frequently. Rope stabilization essentially attaches a fixed length "rope" to your cursor and an anchor point (Brush). As you move your cursor, you are pulling the brush behind it. The cursor (of course) will not pull the brush until the rope is fully extended, this behavior filters out jittery movements and is used to produce smoother drawing curves.

If compared visually side-by-side, you will notice that this indicator bears striking resemblance to its inspiration.

> Goal

Other than simply distinguishing price movements between meaningful and noise, this indicator strives to create a rigid structure to frame market movements and lack-there-of, such as when to anticipate trend, and when to suspect consolidation.

Since the indicator works based on an ATR range, the resulting ATR Channel does well to get reactions from price at its extremes. Naturally, when consolidating, price will remain within the channel, neither pushing the channel significantly up or down. Likewise, when trending, price will continue to push the channel in a single direction.

With the goal of keeping it quick and simple, this indicator does not do any smoothing of data feeds, and is simply based on the deviation of price from the central rope. Adjusting the rope when price extends past the threshold created by +/- ATR from the rope.

> Features & Behaviors

- ATR Rope

ATR Rope is displayed as a 3 color single line.

This can be considered the center line, or the directional line, whichever you'd prefer.

The main point of the Rope display is to indicate direction, however it also is factually the center of the current working range.

- ATR Rope Color

When the rope's value moves up, it changes to green (uptrend), when down, red (downtrend).

When the source crosses the rope, it turns blue (flat).

With these simple rules, we've formed a structure to view market movements.

- Consolidation Zones

Consolidation Zones generate from "Flat" areas, and extend into subsequent trend areas. Consolidation is simply areas where price has crossed the Rope and remains inside the range. Over these periods, the upper and lower values are accumulated and averaged together to form the "Consolidation Zone" values. These zones are draw live, so values are averaged as the flat areas progress and don't repaint, so all values seen historically are as they would appear live.

- ATR Channel

ATR Channel displays the upper and lower bounds of the working range.

When the source moves beyond this range, the rope is adjusted based on the distance from the source to the channel. This range can be extremely useful to view, but by default it is hidden.

> Application

This indicator is not created to provide signals, or serve as a "complete" system.

(People who didn't read this far will still comment for signals. :) )

This is created to be used alongside manual interpretation and intuition. This indicator is not meant to constrain any users into a box, and I would actually encourage an open mind and idea generation, as the application of this indicator can take various forms.

> Examples

As you would probably already know, price movement can be fast impulses, and movement can be slow bleeds. In the screenshot below, we are using movements from and to consolidation zones to classify weak trend and strong trend. As you can see, there are also areas of consolidation which get broken out of and confirmed for the larger moves.

Author's Note: In each of these examples, I have outlined the start and end of each session. These examples come from 1 Min Future charts, and have specifically been framed with day trading in mind.

"Breakout Retest" or "Support/Resistance Flips" or "Structure Retests" are all generally the same thing, with different traders referring to them by different names, all of which can be seen throughout these examples.

In the next example, we have a day which started with an early reversal leading into long, slow, trend. Notice how each area throughout the trend essentially moves slightly higher, then consolidates while holding support of the previous zone. This day had a few sharp movements, however there was a large amount of neutrality throughout this day with continuous higher lows.

In contrast to the previous example, next up, we have a very choppy day. Throughout which we see a significant amount of retests before fast directional movements. We also see a few examples of places where previous zones remained relevant into the future. While the zones only display into the resulting trend area, they do not become immediately meaningless once they stop drawing.

> Abstract

In the screenshot below, I have stacked 2 of these indicators, using the high as the source for one and the low as the source for the other. I've hidden lines of the high and low channels to create a 4 lined channel based on the wicks of price.

This is not necessary to use the indicator, but should help provide an idea of creative ways the simple indicator could be used to produce more complicated analysis.

If you've made it this far, I would hope it's clear to you how this indicator could provide value to your trading.

Thank you to DonovonWall for the inspiration.

Enjoy!

BK AK-Scope🔭 Introducing BK AK-Scope — Target Locked. Signal Acquired. 🔭

After building five precision weapons for traders, I’m proud to unveil the sixth.

BK AK-Scope — the eye of the arsenal.

This is not just an indicator. It’s an intelligence system for volatility, signal clarity, and rate-of-change dynamics — forged for elite vision in any market terrain.

🧠 Why “Scope”? And Why “AK”?

Every shooter knows: you can’t hit what you can’t see.

The Scope brings range, clarity, and target distinction. It filters motion from noise. Purpose from panic.

“AK” continues to honor the man who trained my sight — my mentor, A.K.

His discipline taught me to wait for alignment. To move with reason, not emotion.

His vision lives in every code line here.

🔬 What Is BK AK-Scope?

A Triple-Tier TSI Correlation Engine, fused with adaptive opacity logic, a volatility scoring system, and real-time signal clarity. It’s momentum dissected — by speed, depth, and rate of change.

Built to serve traders who:

Need visual hierarchy between fast, mid, and slow TSI responses.

Want adaptive fills that pulse with volatility — not static zones.

Require a volatility scoring overlay that reads the battlefield in real time.

⚙️ Core Systems: How BK AK-Scope Works

✅ Fast/Mid/Slow TSI →

Three layers of correlation: like scopes with zoom levels.

You track micro moves, mid swings, and macro flow simultaneously.

✅ Rate-of-Change Adaptive Opacity →

Momentum fills fade or flash based on speed — giving you movement density at a glance.

Bull vs. Bear zones adapt to strength. You feel the market’s pulse.

✅ Volatility Score Intelligence →

Custom algorithm measuring:

Range expansion

Rate-of-change differentials

ATR dynamics

Standard deviation pressure

All combined into a score from 0–100 with live icons:

🔥 = Extreme Heat (70+)

🧊 = Cold Zone (<30)

⚠️ = ROC Warning

• = Neutral drift

✅ Auto-Detect Volatility Modes →

Scalp = <15min

Swing = intraday/hourly

Macro = daily/weekly

Or override manually with total control.

🎯 How To Use BK AK-Scope

🔹 Trend Continuation → When all three TSI layers align in direction + volatility score climbs, ride with the trend.

🔹 Early Reversals → Opposing TSI + rapid opacity change + volatility shift = sniper reversal zone.

🔹 Consolidation Filter → Neutral fills + score < 30 = stay out, wait for signal surge.

🔹 Signal Confluence → Pair with:

• Gann fans or angles

• Fib time/price clusters

• Elliott Wave structure

• Harmonics or divergence

To isolate entry perfection.

🛡️ Why This Indicator Changes the Game

It's not just momentum. It’s TSI with depth hierarchy.

It’s not just color. It’s real-time strength visualization.

It’s not just volatility. It’s rate-weighted market intelligence.

This is market optics for the advanced trader — built for vision, clarity, and discipline.

🙏 Final Thoughts

🔹 In honor of A.K., my mentor. The man who taught me to see what others miss.

🔹 Inspired by the power of vision — because execution without clarity is chaos.

🔹 Powered by faith — because Gd alone gives sight beyond the visible.

“He gives sight to the blind and wisdom to the humble.” — Psalms 146

Every tool I build is a prayer in code — that it helps someone trade with clarity, integrity, and precision.

⚡ Zoom In. Focus Deep. Trade Clean.

BK AK-Scope — Lock on the target. See what others don’t.

🔫 Clarity is power. 🔫

Gd bless. 🙏

Not-So-Average True Range (nsATR)Not-So-Average True Range (nsATR)

*By Sherlock_MacGyver*

---

Long Story Short

The nsATR is a complete overhaul of traditional ATR analysis. It was designed to solve the fundamental issues with standard ATR, such as lag, lack of contextual awareness, and equal treatment of all volatility events.

Key innovations include:

* A smarter ATR that reacts dynamically when price movement exceeds normal expectations.

* Envelope zones that distinguish between moderate and extreme volatility conditions.

* A long-term ATR baseline that adds historical context to current readings.

* A compression detection system that flags when the market is coiled and ready to break out.

This indicator is designed for traders who want to see volatility the way it actually behaves — contextually, asymmetrically, and with predictive power.

---

What Is This Thing?

Standard ATR (Average True Range) has limitations:

* It smooths too slowly (using Wilder's RMA), which delays detection of meaningful moves.

* It lacks context — no way to know if current volatility is high or low relative to history.

* It treats all volatility equally, regardless of scale or significance.

nsATR** was built from scratch to overcome these weaknesses by applying:

* Amplification of large True Range spikes.

* Visual envelope zones for detecting volatility regimes.

* A long-term context line to anchor current readings.

* Multi-factor compression analysis to anticipate breakouts.

---

Core Features

1. Breach Detection with Amplification

When True Range exceeds a user-defined threshold (e.g., ATR × 1.2), it is amplified using a power function to reflect nonlinear volatility. This amplified value is then smoothed and cascades into future ATR values, affecting the indicator beyond a single bar.

2. Direction Tagging

Volatility spikes are tagged as upward or downward based on basic price momentum (close vs previous close). This provides visual context for how volatility is behaving in real-time.

3. Envelope Zones

Two adaptive envelopes highlight the current volatility regime:

* Stage 1: Moderate volatility (default: ATR × 1.5)

* Stage 2: Extreme volatility (default: ATR × 2.0)

Breaching these zones signals meaningful expansion in volatility.

4. Long-Term Context Baseline

A 200-period simple moving average of the classic ATR establishes whether current readings are above or below long-term volatility expectations.

5. Multi-Signal Compression Detection

Flags potential breakout conditions when:

* ATR is below its long-term baseline

* Price Bollinger Bands are compressed

* RSI Bollinger Bands are also compressed

All three signals must align to plot a "Volatility Confluence Dot" — an early warning of potential expansion.

---

Chart Outputs

In the Indicator Pane:

* Breach Amplified ATR (Orange line)

* Classic ATR baseline (White line)

* Long-Term context baseline (Cyan line)

* Stage 1 and Stage 2 Envelopes (Purple and Yellow lines)

On the Price Chart:

* Triangles for breach direction (green/red)

* Diamonds for compression zones

* Optional background coloring for visual clarity

---

Alerts

Built-in alert conditions:

1. ATR breach detected

2. Stage 1 envelope breached

3. Stage 2 envelope breached

4. Compression zone detected

---

Customization

All components are modular. Traders can adjust:

* Display toggles for each visual layer

* Colors and line widths

* Breach threshold and amplification power

* Envelope sensitivity

* Compression sensitivity and lookback windows

Some options are disabled by default to reduce clutter but can be turned on for more aggressive signal detection.

---

Real-Time Behavior (Non-Repainting Clarification)

The indicator updates in real time on the current bar as new data comes in. This is expected behavior for live trading tools. Once a bar closes, values do not change. In other words, the indicator *does not repaint history* — but the current bar can update dynamically until it closes.

---

Use Cases

* Day traders: Use compression zones to anticipate volatility surges.

* Swing traders: Use envelope breaches for regime awareness.

* System developers: Replace standard ATR in your logic for better responsiveness.

* Risk managers: Use directional volatility signals to better model exposure.

---

About the Developer

Sherlock_MacGyver develops original trading systems that question default assumptions and solve real trader problems.

True Range eXpansion🕯️ TRX — True Range eXpansion

Clean Candle Bodies · Volatility Bands · Adaptive Range Envelope System

Not your grandfather’s candles. Not your brokerage’s bands.

----------------------------------------------------

TRX begins with a simple concept: visualize the true range of every candle, without the noise of flickering wicks.

From there, it grows into a fully adaptive price visualization framework.

What started as a candle-only visualizer evolved into a modular, user-controlled price engine.

From wickless candle clarity to dynamic volatility envelopes, TRX adapts to you.

There are plenty of band and channel indicators out there — Bollinger, Keltner, Donchian, Envelope, the whole crew.

But none of them are built on the true candle range, adaptive ATR shaping, and full user control like TRX.

This isn’t just another indicator — it’s a new framework.

Most bands and channels are based on close price and statistical deviation — useful, but limited.

TRX uses the full true range of each candle as its foundation, then applies customizable smoothing and directional ATR scaling to form a dynamic, volatility-reactive envelope.

The result? Bands that breathe with the market — not lag behind it.

----------------------------------------------------

🔧 Core Features:

🕯️ True Range Candles — Each candle is plotted from low to high, body-only, colored by open/close.

📈 Adjustable High/Low Moving Averages — Select your smoothing style: SMA, EMA, WMA, RMA, or HMA.

🌬️ ATR-Based Expansion — Bands dynamically breathe based on market volatility.

🔀 Per-Band Multipliers — Fine-tune expansion individually for the upper and lower bands.

⚖️ Basis Line — Optional centerline between bands for structure tracking and equilibrium zones.

🎛️ Full Visual Control — Width, transparency, color, on/off toggles for each element.

----------------------------------------------------

🧠 Default Use Case:

With the included default settings, TRX behaves like an evolved Bollinger Band system — based on True Range candle structure, not just close price and standard deviation.

----------------------------------------------------

🔄 How to Zero Out the Bands (for Minimalist Use):

Want just candles? A clean MA? Single band? You got it.

➤ Use TRX like a clean moving average:

• Set ATR Multiplier to 0

• Set both Band ATR Adjustments to 0

• Leave the Basis Line ON or OFF — your call

➤ Show only candles (no bands at all):

• Turn off "Show High/Low MAs"

• Turn off Basis Line

➤ Single-line ceiling or floor tracking:

• Set one band’s Transparency to 100

• Use the remaining band as a price envelope or support/resistance guide

----------------------------------------------------

🧬 Notes:

TRX can be made:

• Spiky or silky (via smoothing & ATR)

• Wide or tight (via multipliers)

• Subtle or aggressive (via color/transparency)

• Clean as a compass or dirty as a chaos meter

Built by accident. Tuned with intention.

Released to the world as one of the most adaptable and expressive visual overlays ever made.

Created by Sherlock_MacGyver

Range Progress TrackerRANGE PROGRESS TRACKER(RPT)

PURPOSE

This indicator helps traders visually and statistically understand how much of the typical price range (measured by ATR) has already been covered in the current period (Daily, Weekly, or Monthly). It includes key features to assist in trend exhaustion analysis, reversal spotting, and smart alerting.

CORE LOGIC

The indicator calculates the current range of the selected time frame (e.g., Daily), which is:

Current Range = High - Low

This is then compared to the ATR (Average True Range) of the same time frame, which represents the average price movement range over a defined period (default is 14).

The comparison is expressed as a percentage, calculated with this formula:

Range % = (Current Range / ATR) × 100

This percentage shows how much of the “average expected move” has already occurred.

WHY IT MATTERS

When the current range approaches or exceeds 100% of ATR, it means the price has already moved as much as it typically does in a full session.

This indicates a lower probability of continuing the trend with a new high or low, especially when the price is already near the session's high or low.

This setup can signal:

A possible consolidation phase

A reversal in trend

The market entering a corrective phase

SMART ALERTS

The indicator can alert you when:

A new high is made after the range percentage exceeds your set threshold.

A new low is made after the range percentage exceeds your set threshold.

You can adjust the Range % Alert Threshold in the settings to tailor it to your trading style.

Realtime ATR-Based Stop Loss Numerical OverlayRealtime ATR-Based Stop Loss Numerical Overlay

A simple, effective tool for dynamic risk management based on ATR (Average True Range) without adding cluttered and distracting lines all over your chart.

📌 Description

This script plots a real-time stop loss level using the Average True Range (ATR) on your chart, helping you set consistent, volatility-based stops. It supports both:

✅ Current chart timeframe

✅ Custom fixed timeframe inputs (1m, 5m, 15m, 1h, etc.)

The stop level is calculated as:

Stop = ATR × Multiplier

and updates in real-time. An overlay table displays on the bottom-right of your chart with the calculated stop value in a clean, simple way.

⚙️ Settings

ATR Timeframe Source:

Choose between using the current chart's timeframe or a fixed one (e.g. 5, 15, 60, D, etc).

ATR Length:

Period used to calculate the ATR (default is 14).

Stop Loss Multiplier:

Multiplies the ATR value to define your stop (e.g., 1.5 × ATR).

Wait for Timeframe Closes:

If enabled, the ATR value waits for the selected timeframe’s candle to close before updating. If unselected, it will update in real time.

🛠️ How to Use

Add this script to your chart from your indicators list.

Configure your desired timeframe, ATR length, and multiplier in the settings panel.

Use the value shown in the table overlay as your suggested stop loss distance from entry.

Adjust your position sizing accordingly to fit your risk tolerance.

This tool is especially useful for traders looking for adaptive risk management that evolves with market volatility — whether scalping intraday or swing trading.

💡 Pro Tip

The ATR stop can also be used to dynamically trail your stop behind price movement.

Filtered DTR Table📊 Filtered Daily True Range (DTR) Indicator

This indicator calculates and displays a filtered version of the Daily True Range (DTR) over the last 14 trading days, using high and low prices of each day.

It filters out extreme values by excluding any daily range that is:

Less than 0.5× the average range

Greater than 2× the average range

The indicator shows a table in the bottom-right corner of the main chart, containing:

Filtered ATR – The average of valid (filtered) daily ranges over the past 14 days, based on the high-low difference.

Current Day's Range – The high-low range of the current trading day.

% of ATR – How much of the filtered ATR has been covered by today's range, expressed as a whole number percentage.

Filt ADR🟠 Script Name: Filtered Average Daily Range (Filt ADR)

This script calculates a filtered version of the Average Daily Range (ADR) based on the last 14 daily candles. It's designed to reduce the influence of unusually high or low daily ranges (outliers) by applying a filter before calculating the average.

🔧 How It Works — Step by Step

1. Calculate Daily Ranges (High - Low)

It retrieves the daily price ranges (difference between daily high and low) for the last 14 days using request.security() with the "D" (daily) timeframe.

pinescript

Копировать

Редактировать

high - low // today's daily range

high - low // yesterday's daily range

...

These values are stored into individual variables dr0 to dr13.

2. Build an Array of Daily Ranges

An array named ranges is used to store the 14 daily ranges, but only if they are not na (missing data). This avoids errors during processing.

3. Calculate the Initial (Unfiltered) Average Range

The script sums all values in the ranges array and calculates their average:

pinescript

Копировать

Редактировать

avg_all = total sum of ranges / number of valid entries

4. Filter Out Outliers

Now it filters the values in ranges:

Only keeps the ranges that are between 0.5×avg_all and 2×avg_all.

This is to remove abnormally small or large daily ranges that could distort the average.

The filtered values are added to a second array called filtered.

5. Calculate the Filtered ADR

Finally, it calculates the average of the filtered daily ranges:

pinescript

Копировать

Редактировать

avg_filt = sum of filtered ranges / number of filtered values

This is the Filtered ADR.

6. Plot the Result

The result (avg_filt) is plotted as an orange line on the chart. It updates on each bar (depending on the current timeframe you're viewing) but the underlying data is based on the last 14 daily candles.

pinescript

Копировать

Редактировать

plot(avg_filt, title="Filtered ADR", color=color.orange, linewidth=2)

✅ Use Case

This script is useful for traders who use the Average Daily Range (ADR) to:

Estimate expected price movement during a day

Set volatility-based stop-loss or take-profit levels

Identify days with unusually high or low volatility

By filtering out extreme values, it provides a more stable and reliable estimate of daily volatility.

Chandelier Exit + EMA Filtered SignalsThis script is a powerful upgrade to the original Chandelier Exit by Alex Orekhov (everget), combining trend-following logic with higher-quality trade filtering.

✅ Key Features:

Chandelier Exit logic with ATR-based stop levels

Buy/Sell signals only when trend is confirmed:

Buy: Price must be above EMA 13, 50, and 200

Sell: Price must be below EMA 13, 50, and 200

Candle highlighting: Green for Buy, Red for Sell

Signal labels for visual clarity

Toggle to show/hide EMAs

Built-in alerts for:

Buy signal

Sell signal

Trend direction change

🛠️ Inputs:

ATR Period and Multiplier

Toggle: Use Close Price for High/Low Calculation

Toggle: Show/Hide Labels and State Highlight

Toggle: Show/Hide EMA 13, 50, 200

Toggle: Await confirmed bar for alerts

🔔 Alerts Included:

Chandelier Exit Buy

Chandelier Exit Sell

Direction Change (long to short or vice versa)

💡 How to Use:

Use on trending assets (e.g., Gold, Indices, Crypto).

Combine with support/resistance or session filters for optimal results.

Enable alerts to be notified on trade setups.

📢 Credits:

Based on the original Chandelier Exit script by everget.

Enhancements by AP Capital for filtered signals and better visual feedback.

ADR, ATR & VOL OverlayThis is a combined version of 2 of my other indicators:

ADR / ATR Overlay

VOL / AVG Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Custom Session Volume

Average For Selected Session

Volume Percentage Comparison

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Custom Session Volume : User chosen time frame to monitor volume

Average For Selected Session : Average for the custom session volume

Volume Percentage Comparison : Current session compared to the average (calculated at session close)

Options:

ADR/ATR:

Time Frame

Length

Smoothing

Volume:

Set Custom Time Frame For Calculations

Set Custom Time Frame For Average Comparison

Set Custom Time Zone

Table:

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Add/Remove extra row for placement

ADR / ATR Example:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential (coverage) move of 30% in Pre/Post market as suggested by averages.

Custom Volume Session Example:

Set indicator to 30 period average. Set custom time frame to 9:30am to 10:30am Eastern/New York.

When the time frame for the calculation is closed, the indicator will provide a comparison of the current days volume compared to the average of 30 previous days for that same time frame and display it as a percentage in the table.

In this example you could compare how the first hour of the trading day compares to the previous 30 day's average, aiding in evaluating the potential volume for the remainder of the day.

Notes:

Times must be entered in 24 hour format. (1pm = 13:00 etc.)

Volume indicator is for Intra-day time frames, not > Day.

How I use these values:

I use these calculations to determine if a ticker symbol has the necessary range to achieve target gains, to determine if the price oscillation is within "normal" ranges to determine if the trading day will be choppy, and to determine placement of stops and targets within average ranges in combination with support, resistance and retracement levels.

Impulse Zones | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Impulse Zones indicator, a powerful tool designed to identify significant price movements accompanied by strong volume, highlighting potential areas of support and resistance. These Impulse Zones can offer valuable insights into market momentum and potential reversal or continuation points. For more information about the process, please check the "HOW DOES IT WORK ?" section.

Impulse Zones Features :

Dynamic Zone Creation : Automatically identifies and plots potential supply and demand zones based on significant price impulses and volume spikes.

Customizable Settings : Allows you to adjust the sensitivity of zone detection based on your trading style and market conditions.

Retests and Breakouts : Clearly marks instances where price retests or breaks through established Impulse Zones, providing potential entry or exit signals.

Alerts : You can set alerts for Bullish & Bearish Impulse Zone detection and their retests.

🚩 UNIQUENESS

Our Impulse Zones indicator stands out by combining both price action (impulsive moves) and volume confirmation to define significant zones. Unlike simple support and resistance indicators, it emphasizes the strength behind price movements, potentially filtering out less significant levels. The inclusion of retest and breakout visuals directly on the chart provides immediate context for potential trading opportunities. The user can also set up alerts for freshly detected Impulse Zones & the retests of them.

📌 HOW DOES IT WORK ?

The indicator identifies bars where the price range (high - low) is significantly larger than the average true range (ATR), indicating a strong price movement. The Size Sensitivity input allows you to control how large this impulse needs to be relative to the ATR.

Simultaneously, it checks if the volume on the impulse bar is significantly higher than the average volume. The Volume Sensitivity input governs this threshold.

When both the price impulse and volume confirmation criteria are met, an Impulse Zone is created in the corresponding direction. The high and low of the impulse bar define the initial boundaries of the zone. Zones are extended forward in time to remain relevant. The indicator manages the number of active zones to maintain chart clarity and can remove zones that haven't been touched for a specified period. The indicator monitors price action within and around established zones.

A retest is identified when the price touches a zone and then moves away. A break occurs when the price closes beyond the invalidation point of a zone. Keep in mind that if "Show Historic Zones" setting is disabled, you will not see break labels as their zones will be removed from the chart.

The detection of Impulse Zones are immediate signs of significant buying or selling pressure entering the market. These zones represent areas where a strong imbalance between buyers and sellers has led to a rapid price movement accompanied by high volume. Bullish Impulse Zones act as a possible future support zone, and Bearish Impulse Zones act as a possible future resistance zone. Retests of the zones suggest a strong potential movement in the corresponding direction.

⚙️ SETTINGS

1. General Configuration

Show Historic Zones: If enabled, invalidated or expired Impulse Zones will remain visible on the chart.

2. Impulse Zones

Invalidation Method: Determines which part of the candle (Wick or Close) is used to invalidate a zone break.

Size Sensitivity: Controls the required size of the impulse bar relative to the ATR for a zone to be detected. Higher values may identify fewer, larger zones. Lower values may detect more, smaller zones.

Volume Sensitivity: Controls the required volume of the impulse bar relative to the average volume for a zone to be detected. Higher values require more significant volume.

Labels: Toggles the display of "IZ" labels on the identified zones.

Retests: Enables the visual highlighting of retests on the zones.

Breaks: Enables the visual highlighting of zone breaks.

ATR Volatility giua64ATR Volatility giua64 – Smart Signal + VIX Filter

📘 Script Explanation (in English)

Title: ATR Volatility giua64 – Smart Signal + VIX Filter

This script analyzes market volatility using the Average True Range (ATR) and compares it to its moving average to determine whether volatility is HIGH, MEDIUM, or LOW.

It includes:

✅ Custom or preset configurations for different asset classes (Forex, Indices, Gold, etc.).

✅ An optional external volatility index input (like the VIX) to refine directional bias.

✅ A directional signal (LONG, SHORT, FLAT) based on ATR strength, direction, and external volatility conditions.

✅ A clean visual table showing key values such as ATR, ATR average, ATR %, VIX level, current range, extended range, and final signal.

This tool is ideal for traders looking to:

Monitor the intensity of price movements

Filter trading strategies based on volatility conditions

Identify momentum acceleration or exhaustion

⚙️ Settings Guide

Here’s a breakdown of the user inputs:

🔹 ATR Settings

Setting Description

ATR Length Number of periods for ATR calculation (default: 14)

ATR Smoothing Type of moving average used (RMA, SMA, EMA, WMA)

ATR Average Length Period for the ATR moving average baseline

🔹 Asset Class Preset

Choose between:

Manual – Define your own point multiplier and thresholds

Forex (Pips) – Auto-set for FX markets (high precision)

Indices (0.1 Points) – For index instruments like DAX or S&P

Gold (USD) – Preset suitable for XAU/USD

If Manual is selected, configure:

Setting Description

Points Multiplier Multiplies raw price ranges into useful units (e.g., 10 for Gold)

Low Volatility Threshold Threshold to define "LOW" volatility

High Volatility Threshold Threshold to define "HIGH" volatility

🔹 Extended Range and VIX

Setting Description

Timeframe for Extended High/Low Used to compare larger price ranges (e.g., Daily or Weekly)

External Volatility Index (VIX) Symbol for a volatility index like "VIX" or "EUVI"

Low VIX Threshold Below this level, VIX is considered "low" (default: 20)

High VIX Threshold Above this level, VIX is considered "high" (default: 30)

🔹 Table Display

Setting Description

Table Position Where the visual table appears on the chart (e.g., bottom_center, top_left)

Show ATR Line on Chart Whether to display the ATR line directly on the chart

✅ Signal Logic Summary

The script determines the final signal based on:

ATR being above or below its average

ATR rising or falling

ATR percentage being significant (>2%)

VIX being high or low

Conditions Signal

ATR rising + high volatility + low VIX LONG

ATR falling + high volatility + high VIX SHORT

ATR flat or low volatility or low %ATR FLAT

Daily Price RangeThe indicator is designed to analyze an instrument’s volatility based on daily extremes (High-Low) and to compare the current day’s range with the typical (median) range over a selected period. This helps traders assess how much of the "usual" daily movement has already occurred and how much may still be possible during the trading day.

ADR & ATR OverlayADR & ATR Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Options:

Time Frame

Length

Smoothing

Enable or Disable each value

Text Color

Background Color

How to use this indicator:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential move of 30% in Pre/Post market as suggested by averages.

Notes:

These indicators are available as oscillators to place under your chart through trading view but this indicator will place them on the chart in numerical only format.

Please feel free to modify this script if you like but please acknowledge me, I am only a hobby coder so this takes some time & effort.

MACD-V with Volatility Normalisation [DCD]MACD-V with Volatility Normalisation

This indicator is a modified version of the traditional MACD, designed to account for market volatility by normalizing the MACD line using the Average True Range (ATR). It provides a more adaptive approach to identifying momentum shifts and potential trend reversals. This indicator was developed by Alex Spiroglou in this paper:

Spiroglou, Alex, MACD-V: Volatility Normalised Momentum (May 3, 2022).

Features:

Volatility Normalization: The MACD line is adjusted using ATR to standardize its values across different market conditions.

Customizable Parameters: Users can adjust the MACD fast length, slow length, signal line smoothing, and ATR length to suit their trading style.

Histogram Visualization: The histogram highlights the difference between the MACD and signal lines, with customizable colors for positive and negative momentum.

Crossover Signals: Green and red dots indicate bullish and bearish crossovers between the MACD and signal lines.

Background Highlighting: The chart background changes to green when the MACD is above 0 and red when it is below 0, providing a clear visual cue for bullish and bearish conditions.

Horizontal Levels: Dotted horizontal lines are plotted at key levels for better visualization of MACD values.

How to Use:

Look for crossovers between the MACD and signal lines to identify potential buy or sell signals.

Use the histogram to gauge the strength of momentum.

Pay attention to the background color for quick identification of bullish (green) or bearish (red) conditions.

This indicator is ideal for traders who want a more dynamic MACD that adapts to market volatility. Customize the settings to align with your trading strategy and timeframe.

Daily ATR Bonanza: Expected Moves - Tr33man Daily ATR Bonanza: Expected Moves

Overview 🤷♂️

The Daily ATR Bonanza script is a powerful trading tool designed to help traders visualize and understand potential price movements using the Average True Range (ATR). It provides daily and weekly ATR levels, historical statistics, and conditional probability analysis to give traders actionable insights. The script also plots the daily Keltner channel. This script is ideal for traders who want to gauge volatility, identify key levels, and make data-driven decisions.

b]Key Features:

📈 1. Daily and Weekly ATR Levels

🔵ATR Levels: The script calculates and displays ATR-based levels for the day and week. These levels are derived from the previous day's or week's close price and are adjusted using customizable multipliers (0.5x, 1x, and 1.5x by default).

🔵You can choose the number of ATR levels (1, 2, or 3) and adjust the multipliers to suit your trading strategy.

🌐 2. ATR Bands (Keltner Channels)

🔵The script includes an option to display ATR Bands, which are volatility-based envelopes around a moving average. These bands help identify overbought and oversold conditions.

🔵You can adjust the ATR multiplier and the length of the moving average used for the bands.

🧮 3. Historical Statistics and Conditional Probability

🔵 Historical Analysis: The script analyzes historical price movements to calculate the likelihood of closing at certain ATR levels.

🔵 Conditional Probability: This feature shows the probability of the price reaching specific ATR levels given the current market conditions. The conditional matches historical data by an open in the same opening ATR bucket, as well as the current price bucket having been visited in the historical case. Conditional probabilities are just statistics, and do not predict anything.

Data Table: 📚

🔵 Historical Close Probability: The percentage of days the price closed within each ATR level.

🔵 Conditional Close Probability: The likelihood of the price closing within each ATR level today.

❓ What is Conditional Probability? ❓

Conditional probability is a statistical measure that calculates the likelihood of an event occurring given that another event has already occurred. In this script, it is used to determine the probability of the price reaching specific ATR levels based on the current opening range as well as current ATR distance from the previous close.

For example:

If the market opens near the lower end of the first ATR level, the script calculates the likelihood of the price reaching the upper end of the first, second, or third ATR level.

This analysis is based on historical data, making it a powerful tool for understanding potential price movements.

🌟 Understanding the Levels

🔵Daily Levels: These are based on the previous day's close price and ATR. They are updated at the start of each new day.

🔵Weekly Levels: These are based on the previous week's close price and ATR. They are updated at the start of each new week.

🔵ATR Bands: These are dynamic levels that adjust with market volatility.

🔬 Analyze the Statistics (Daily only for now, no weekly yet)

🔵Use the interactive table to understand historical probabilities and conditional probabilities.

🔵Focus on the current opening range and the likelihood of reaching specific levels.

🧠 Make Trading Decisions

🔵Use the ATR levels and bands to identify key support and resistance levels.

🔵Use the conditional probability table to gauge the likelihood of reaching specific targets.

🔵Adjust your strategy based on the historical performance of the market.

Example Use Cases

1. Day Trading

Use the daily ATR levels to set intraday targets and stop-loss levels.

Monitor the conditional probability table to adjust your expectations based on the opening range.

2. Swing Trading

Use the weekly ATR levels to identify longer-term support and resistance levels.

3. Scalping

Use the ATR bands to identify overbought and oversold conditions.

Use the conditional probability table to quickly assess the likelihood of price movements.

Smart Market Matrix Smart Market Matrix

This indicator is designed for intraday, scalping, providing automated detection of price pivots, liquidity traps, and breakout confirmations, along with a context dashboard featuring volatility, trend, and volume.

## Summary Description

### Menu Settings & Their Roles

- **Swing Pivot Strength**: Controls the sensitivity for detecting High/Low pivots.

- **Show Pivot Points**: Toggles the display of HH/LL markers on the chart.

- **VWMA Length for Trap Volume** & **Volume Spike Multiplier**: Identify concentrated volume spikes for liquidity traps.

- **Wick Ratio Threshold** & **Max Body Size Ratio**: Detect candles with disproportionate wicks and small bodies (doji-ish) for traps.

- **ATR Length for Trap**: Measures volatility specific to trap detection.

- **VWMA Length for Breakout Volume**, **ATR Multiplier for Breakout**, **ATR Length for Breakout**, **Min Body/Range Ratio**: Set adaptive breakout thresholds based on volatility and volume.

- **OBV Smooth Length**: Smooths OBV momentum for breakout confirmation.

- **Enable VWAP Filter for Confirmations**: Optionally validate breakouts against the VWAP.

- **Enable Higher-TF Trend Filter** & **Trend Filter Timeframe**: Align breakout signals with the 1h/4h/Daily trend.

- **ADX Length**, **EMA Fast/Slow Length for Context**: Parameters for the context dashboard (Volatility, Trend, Volume).

- **Show Intraday VWAP Line**, **VWAP Line Color/Width**: Display the intraday VWAP line with custom style.

### Signal Interpretation Map

| Signal | Description | Recommended Action |

|--------------------------------|-----------------------------------------------------------|-------------------------------------------|

| 📌 **HH / LL (pivot)** | Market structure (support/resistance) | Note key levels |

| **Bull Trap(green diamond)** | Sweep down + volume spike + wick + rejection | Go long with trend filter

| **Bear Trap(red diamond)** | Sweep up + volume spike + wick + rejection | Go short with trend filter

| 🔵⬆️ **Breakout Confirmed Up** | Close > ATR‑scaled high + volume + OBV↑ | Go long with trend filter |

| 🔵⬇️ **Breakout Confirmed Down** | Close < ATR‑scaled low + volume + OBV↓ | Go short with trend filter |

| 📊 **VWAP Line** | Intraday reference to guide price | Use as dynamic support/resistance |

| ⚡ **Volatility** | ATR ratio High/Med/Low | Adjust position size |

| 📈 **Trend Context** | ADX+EMA Strong/Moderate/Weak | Confirm trend direction |

| 🔍 **Volume Context** | Breakout / Rising / Falling / Calm | Check volume momentum |

*This summary gives you a quick overview of the key settings and how to interpret signals for efficient intraday scalping.*

### Suggested Settings

- **Intraday Scalping (5m–15m)**

- `Swing Pivot Strength = 5`

- `VWMA Length for Trap Volume = 10`, `Volume Spike Multiplier = 1.6`

- `ATR Length for Trap = 7`

- `VWMA Length for Breakout Volume = 12`, `ATR Length for Breakout = 9`, `ATR Multiplier for Breakout = 0.5`

- `Min Body/Range Ratio for Breakout = 0.5`, `OBV Smooth Length = 7`

- `Enable Higher-TF Trend Filter = true` (TF = 60)

- `Show Intraday VWAP Line = true` (Color = orange, Width = 2)

- **Swing Trading (4h–Daily)**

- `Swing Pivot Strength = 10`

- `VWMA Length for Trap Volume = 20`, `Volume Spike Multiplier = 2.0`

- `ATR Length for Trap = 14`

- `VWMA Length for Breakout Volume = 30`, `ATR Length for Breakout = 14`, `ATR Multiplier for Breakout = 0.8`

- `Min Body/Range Ratio for Breakout = 0.7`, `OBV Smooth Length = 14`

- `Enable Higher-TF Trend Filter = true` (TF = D)

- `Show Intraday VWAP Line = false`

*Adjust these values based on the symbol and market volatility for optimal performance.*

[Stop!Loss] ADR Signal ADR Signal - a technical indicator located in a separate window, which displays by default the 80%-level , as well as the 100%-level of the average daily range (ADR) for the last 10 days and compares it with the current intraday range. The indicator helps not only with the use of a mathematical-statistical method to identify a potential reversal at the moment during intraday trading, but can also serves as an effective assistant in risk management.

👉 Basic mechanics of the indicator

Firstly, this indicator tracks the performance of the standard ATR indicator on the daily chart, in other words, ADR (Average Daily Range).

Important ❗️The ATR (Average True Range) indicator was created by J. Welles Wilder Jr. He first introduced ATR in his book "New Concepts in Technical Trading Systems", published in 1978. Wilder developed this indicator to measure market volatility to help traders estimate the range of price movements. This indicator is built into TradingView, more details can be found by link: www.tradingview.com

Like ATR , ADR calculates the average true range for a specified period. In this case, the distance in points from the maximum of each day to its minimum is calculated, after which the arithmetic mean is calculated - this is ADR .

👉 Visualization

ADR Signal is located in a separate window on the chart and has 3 levels:

1) "ADR level" (green line) - the same parameter, the calculations of which are briefly described above. There is 100%-level of ATR on the daily chart (ADR).

2) "Current level" (red line) - this is the current price passage within the day, calculated in points. At the start of a new day, this parameter is reset. Therefore, in the indicator window, this line has sharp drops at the start of a new trading day: "A new trading day - the instrument's power reserve is renewed again".

3) "Signal level" (blue line) - this is an individually customized value that demonstrates a certain part of the ADR parameter.

👉 Inputs

1) - is responsible for the ATR indicator period, the value of which will always be calculated on the daily chart. The default value is "10", that is, ATR is calculated for the last 10 days (not including the current one).

2) - signal level (in %). The default value is "0.8", that is, 80%-level of the ADR parameter (set earlier) is calculated.

👉 Style

1) - by default, this level is colored "blue".

2) - by default, this level is colored "red".

3) - by default, this level is colored "green".

👉 How to use this indicator

Important❗️ The two methods of the use of the ADR Signal indicator described below will be most effective when trading intraday (which is highlighted quite well below), so it is more logical to use the indicator information on time periods H1 and below.

1) Identifying potential reversals during intraday trading:

The ADR Signal indicator can be used as a potential individual reversal strategy.

Important ❗️It should be noted that using it in it without additional confirming analysis tools will be a rather aggressive trading approach. Therefore, it is best to support the entry point in particular with other methods.

In this case, the crossing of the red line (the number of points passed within the current day, that is, from the minimum of the current day to its maximum) and the blue line (color of the Signal level based on the default settings), indicates that the trading instrument has passed 80% (based on the default settings for the "Signal level") of its average distance from the maximum to the minimum over the past 10 days (based on the default settings for the "ADR Length"). Such a situation in the context of the mathematical-statistical approach indicates a probable reversal, since the "power reserve" of this instrument is mostly exhausted, so one can expect with a higher probability, at least, a price stop and possibly a reversal. In case of crossing of the red line and the green one (ADR level), it says again that based on the mathematical-statistical approach, this trading instrument has completely exhausted its intraday "power reserve". In this situation, a stop or reversal of the price will be even more likely.

Of course, using the "Signal level" parameter, one can filter out even more reliable situations for potential price reversals within a day, namely, by specifying, for example, 1.5 in the field of this parameter. Under such conditions, in the case of crossing the red and blue lines (based on the default style settings), to say that the trading instrument has passed 150% of its average distance over the last 10 days (based on the default style settings "ADR length"). In this case, the probability of a stop or reversal of the price increases even more.

2) Use in risk management:

In terms of risk management, this indicator is more applicable to open trades. For example, if one had an open Buy-position (especially if it is an intraday trade) and the price has raised significantly during the day, then the crossing of the red line with the blue line , and especially the red line with the green line , may indicate that the price will most likely stop growing, since the "power reserve" is almost or completely exhausted for this instrument within the current day. In this case, one can, at a minimum, move the trade to breakeven or even partially fix the profit.

We will continue to discuss the methods of using this indicator and strategies based on it here. And we are always waiting for your reactions and feedback on this topic 💬.

Thank you for your support 🚀